Financial Ratio Analysis for Myer Holdings Ltd

VerifiedAdded on 2023/05/28

|14

|3146

|164

AI Summary

This article provides a financial ratio analysis for Myer Holdings Ltd, including liquidity ratios, capital structure ratios, profitability ratios, and activity ratios. The analysis suggests that while the liquidity position has improved marginally, the profitability position has decreased due to falling revenue and rising costs. The article also provides recommendations for improving the company's financial position.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCING ENTERPRISES

Financing Enterprises

Name of the Student:

Name of the University:

Author’s Note:

Financing Enterprises

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

In Response to Question 1...............................................................................................................5

In Response to Question 2...............................................................................................................6

In Response to Question 3...............................................................................................................7

In Response to Question 4...............................................................................................................8

In Response to Question 5...............................................................................................................9

Reference.......................................................................................................................................10

Appendix........................................................................................................................................12

.......................................................................................................................................................12

In Response to Question 1...............................................................................................................5

In Response to Question 2...............................................................................................................6

In Response to Question 3...............................................................................................................7

In Response to Question 4...............................................................................................................8

In Response to Question 5...............................................................................................................9

Reference.......................................................................................................................................10

Appendix........................................................................................................................................12

.......................................................................................................................................................12

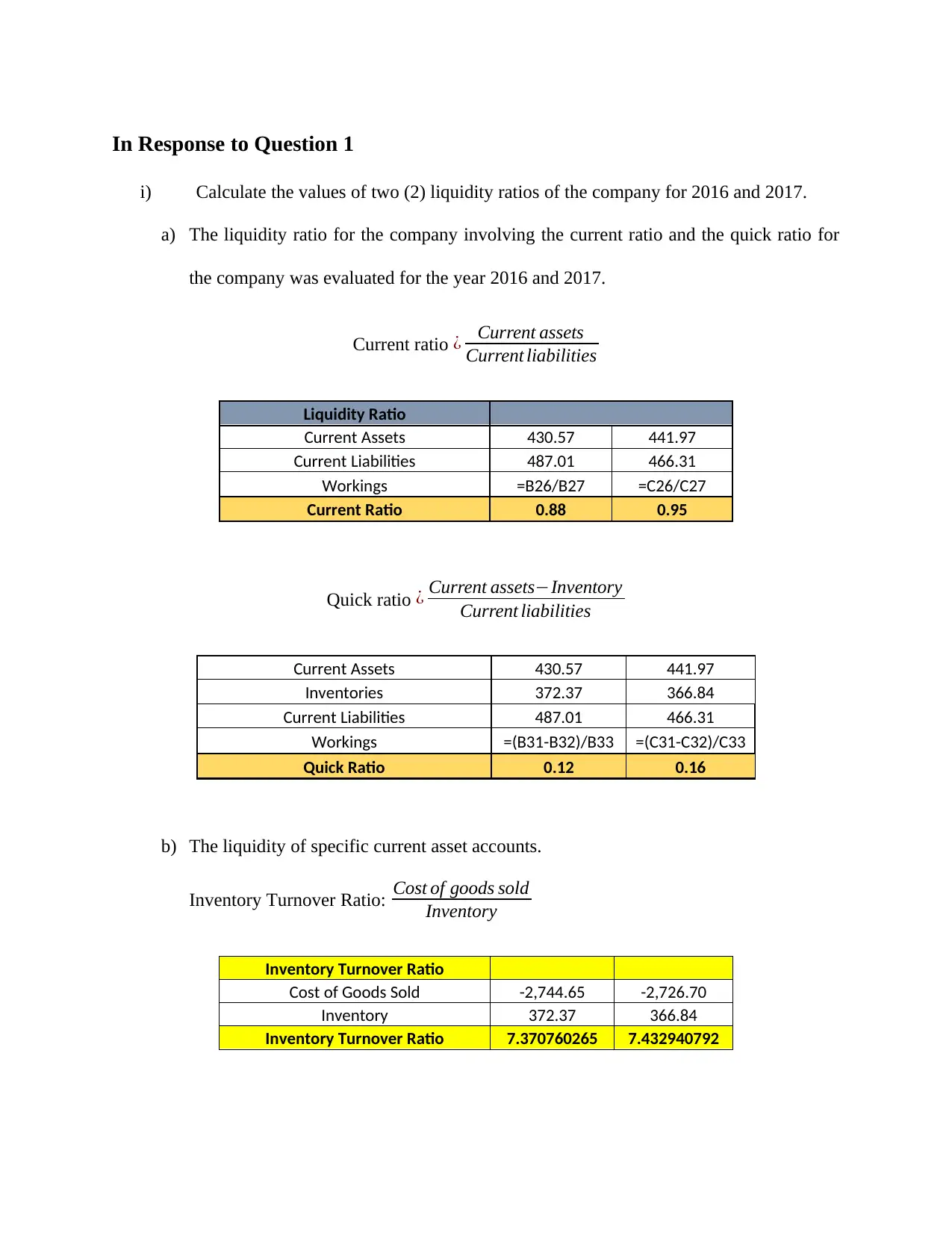

In Response to Question 1

i) Calculate the values of two (2) liquidity ratios of the company for 2016 and 2017.

a) The liquidity ratio for the company involving the current ratio and the quick ratio for

the company was evaluated for the year 2016 and 2017.

Current ratio ¿ Current assets

Current liabilities

Liquidity Ratio

Current Assets 430.57 441.97

Current Liabilities 487.01 466.31

Workings =B26/B27 =C26/C27

Current Ratio 0.88 0.95

Quick ratio ¿ Current assets−Inventory

Current liabilities

Current Assets 430.57 441.97

Inventories 372.37 366.84

Current Liabilities 487.01 466.31

Workings =(B31-B32)/B33 =(C31-C32)/C33

Quick Ratio 0.12 0.16

b) The liquidity of specific current asset accounts.

Inventory Turnover Ratio: Cost of goods sold

Inventory

Inventory Turnover Ratio

Cost of Goods Sold -2,744.65 -2,726.70

Inventory 372.37 366.84

Inventory Turnover Ratio 7.370760265 7.432940792

i) Calculate the values of two (2) liquidity ratios of the company for 2016 and 2017.

a) The liquidity ratio for the company involving the current ratio and the quick ratio for

the company was evaluated for the year 2016 and 2017.

Current ratio ¿ Current assets

Current liabilities

Liquidity Ratio

Current Assets 430.57 441.97

Current Liabilities 487.01 466.31

Workings =B26/B27 =C26/C27

Current Ratio 0.88 0.95

Quick ratio ¿ Current assets−Inventory

Current liabilities

Current Assets 430.57 441.97

Inventories 372.37 366.84

Current Liabilities 487.01 466.31

Workings =(B31-B32)/B33 =(C31-C32)/C33

Quick Ratio 0.12 0.16

b) The liquidity of specific current asset accounts.

Inventory Turnover Ratio: Cost of goods sold

Inventory

Inventory Turnover Ratio

Cost of Goods Sold -2,744.65 -2,726.70

Inventory 372.37 366.84

Inventory Turnover Ratio 7.370760265 7.432940792

ii) The liquidity position of the company shows the ability of the company in meeting up

the current obligations of the company and the current liabilities of the company

(Setiawan and Amboningtyas 2018). The current ratio for the company has increased

indicating that the liquidity position for the company has improved. The current ratio

for the company has increased from 0.88times in the year 2016-17 to around 0.95 in

the year 2017-18. The quick ratio for the company shows the company net liquidity

position of the company in meeting up the current liabilities of the company. The

quick ratio for the company has also increased from 0.10 in the year 2016-17 to

around 0.12 in the year 2017-18. The company needs to focus on the quick ratio of

the company, as the same is not sufficient in order to meet the current liabilities of the

company (Alper 2018). It is very important for the company to maintain a healthy and

sufficient liquidity in the operations of the business so that the operations of the

company is not hampered and the company is able to meet the current liabilities of

the company. The liquidity position of the company on an overall basis has improved

for the company but the same is not consistent and the liquidity of the company

should be around 1.

iii) The company has maintained a good current ratio in the trend period analyzed for the

company however, the quick ratio for the company needs to be improved for the

company. The net liquidity position of the company needs to be improved so that the

operations of the company runs in a smooth manner and the company is able to meet

the short-term obligations of the company.

In Response to Question 2

i) The two common capital structure ratio’s for the company analyzed were:

the current obligations of the company and the current liabilities of the company

(Setiawan and Amboningtyas 2018). The current ratio for the company has increased

indicating that the liquidity position for the company has improved. The current ratio

for the company has increased from 0.88times in the year 2016-17 to around 0.95 in

the year 2017-18. The quick ratio for the company shows the company net liquidity

position of the company in meeting up the current liabilities of the company. The

quick ratio for the company has also increased from 0.10 in the year 2016-17 to

around 0.12 in the year 2017-18. The company needs to focus on the quick ratio of

the company, as the same is not sufficient in order to meet the current liabilities of the

company (Alper 2018). It is very important for the company to maintain a healthy and

sufficient liquidity in the operations of the business so that the operations of the

company is not hampered and the company is able to meet the current liabilities of

the company. The liquidity position of the company on an overall basis has improved

for the company but the same is not consistent and the liquidity of the company

should be around 1.

iii) The company has maintained a good current ratio in the trend period analyzed for the

company however, the quick ratio for the company needs to be improved for the

company. The net liquidity position of the company needs to be improved so that the

operations of the company runs in a smooth manner and the company is able to meet

the short-term obligations of the company.

In Response to Question 2

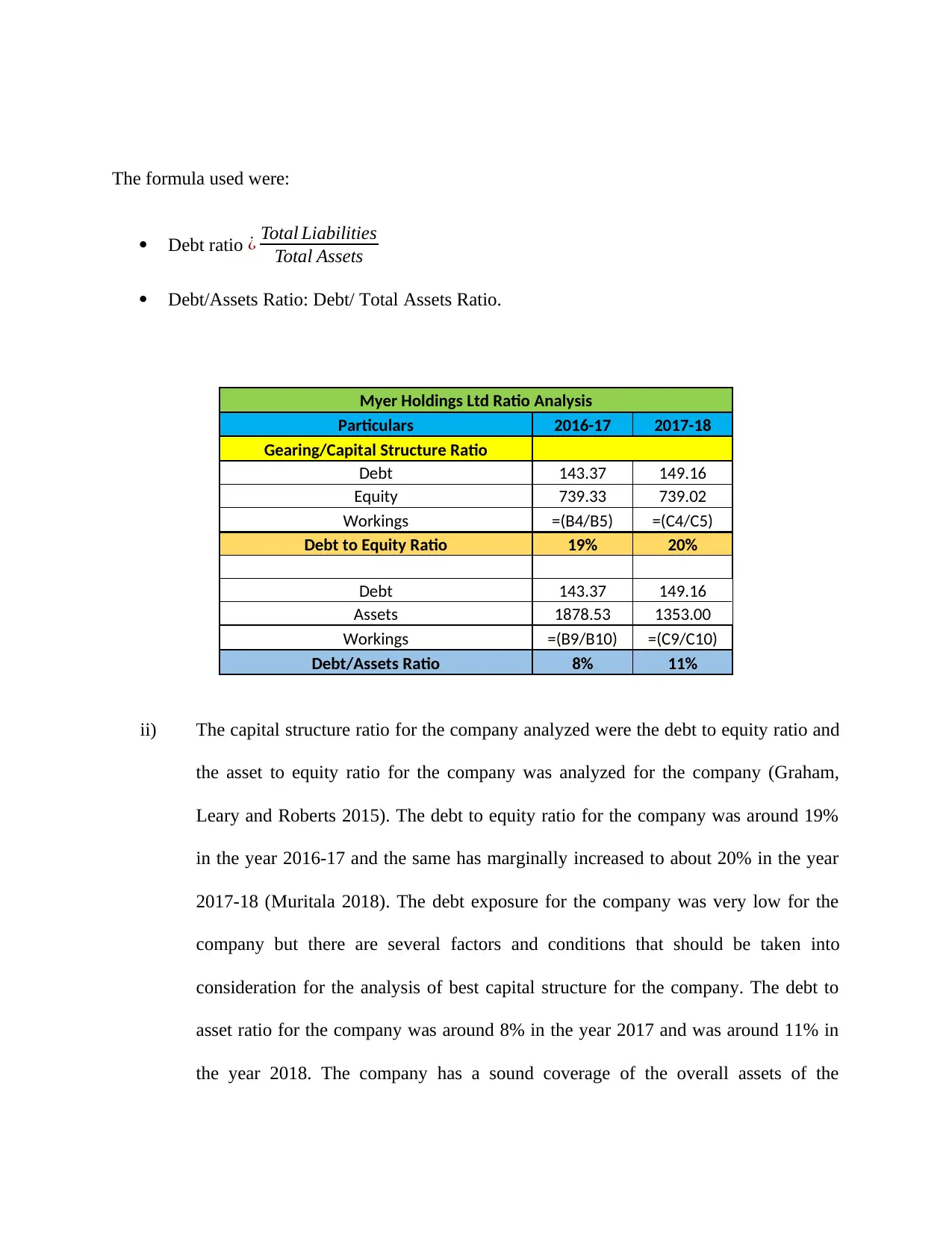

i) The two common capital structure ratio’s for the company analyzed were:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

The formula used were:

Debt ratio ¿ Total Liabilities

Total Assets

Debt/Assets Ratio: Debt/ Total Assets Ratio.

Myer Holdings Ltd Ratio Analysis

Particulars 2016-17 2017-18

Gearing/Capital Structure Ratio

Debt 143.37 149.16

Equity 739.33 739.02

Workings =(B4/B5) =(C4/C5)

Debt to Equity Ratio 19% 20%

Debt 143.37 149.16

Assets 1878.53 1353.00

Workings =(B9/B10) =(C9/C10)

Debt/Assets Ratio 8% 11%

ii) The capital structure ratio for the company analyzed were the debt to equity ratio and

the asset to equity ratio for the company was analyzed for the company (Graham,

Leary and Roberts 2015). The debt to equity ratio for the company was around 19%

in the year 2016-17 and the same has marginally increased to about 20% in the year

2017-18 (Muritala 2018). The debt exposure for the company was very low for the

company but there are several factors and conditions that should be taken into

consideration for the analysis of best capital structure for the company. The debt to

asset ratio for the company was around 8% in the year 2017 and was around 11% in

the year 2018. The company has a sound coverage of the overall assets of the

Debt ratio ¿ Total Liabilities

Total Assets

Debt/Assets Ratio: Debt/ Total Assets Ratio.

Myer Holdings Ltd Ratio Analysis

Particulars 2016-17 2017-18

Gearing/Capital Structure Ratio

Debt 143.37 149.16

Equity 739.33 739.02

Workings =(B4/B5) =(C4/C5)

Debt to Equity Ratio 19% 20%

Debt 143.37 149.16

Assets 1878.53 1353.00

Workings =(B9/B10) =(C9/C10)

Debt/Assets Ratio 8% 11%

ii) The capital structure ratio for the company analyzed were the debt to equity ratio and

the asset to equity ratio for the company was analyzed for the company (Graham,

Leary and Roberts 2015). The debt to equity ratio for the company was around 19%

in the year 2016-17 and the same has marginally increased to about 20% in the year

2017-18 (Muritala 2018). The debt exposure for the company was very low for the

company but there are several factors and conditions that should be taken into

consideration for the analysis of best capital structure for the company. The debt to

asset ratio for the company was around 8% in the year 2017 and was around 11% in

the year 2018. The company has a sound coverage of the overall assets of the

company in comparison to the equity level of the company. The assets of the

company in comparison to the equity of the company has been stable and at sufficient

level. The overall financial risk of the company as assessed was very low with low

level of debt in the financials of the company (Klasa et al. 2018). The company

should analyze various aspect of effect of debt on the company and the benefit the

company is getting by taking exposure in the form of tax savings for the company.

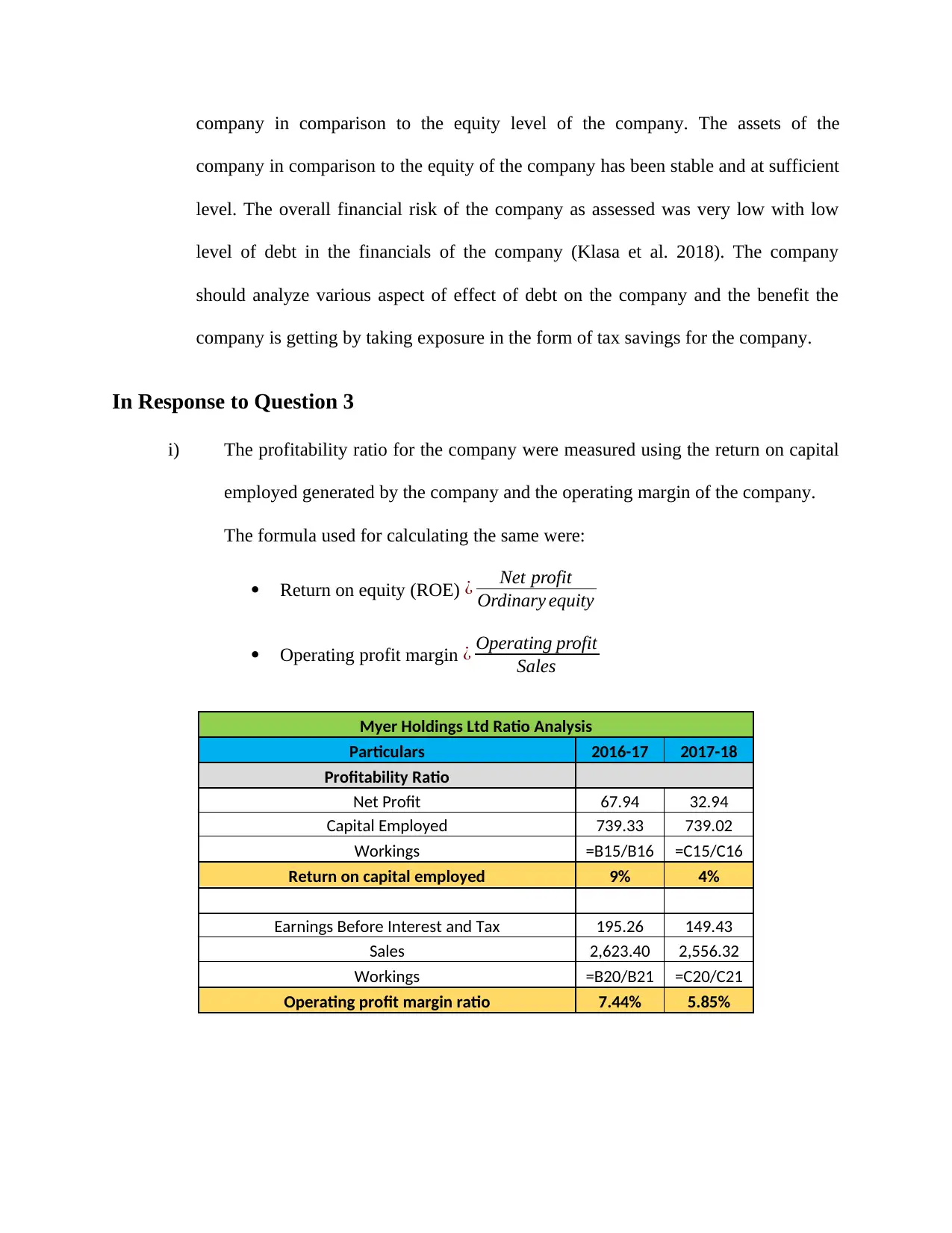

In Response to Question 3

i) The profitability ratio for the company were measured using the return on capital

employed generated by the company and the operating margin of the company.

The formula used for calculating the same were:

Return on equity (ROE) ¿ Net profit

Ordinary equity

Operating profit margin ¿ Operating profit

Sales

Myer Holdings Ltd Ratio Analysis

Particulars 2016-17 2017-18

Profitability Ratio

Net Profit 67.94 32.94

Capital Employed 739.33 739.02

Workings =B15/B16 =C15/C16

Return on capital employed 9% 4%

Earnings Before Interest and Tax 195.26 149.43

Sales 2,623.40 2,556.32

Workings =B20/B21 =C20/C21

Operating profit margin ratio 7.44% 5.85%

company in comparison to the equity of the company has been stable and at sufficient

level. The overall financial risk of the company as assessed was very low with low

level of debt in the financials of the company (Klasa et al. 2018). The company

should analyze various aspect of effect of debt on the company and the benefit the

company is getting by taking exposure in the form of tax savings for the company.

In Response to Question 3

i) The profitability ratio for the company were measured using the return on capital

employed generated by the company and the operating margin of the company.

The formula used for calculating the same were:

Return on equity (ROE) ¿ Net profit

Ordinary equity

Operating profit margin ¿ Operating profit

Sales

Myer Holdings Ltd Ratio Analysis

Particulars 2016-17 2017-18

Profitability Ratio

Net Profit 67.94 32.94

Capital Employed 739.33 739.02

Workings =B15/B16 =C15/C16

Return on capital employed 9% 4%

Earnings Before Interest and Tax 195.26 149.43

Sales 2,623.40 2,556.32

Workings =B20/B21 =C20/C21

Operating profit margin ratio 7.44% 5.85%

ii) The return on capital employed for the company shows the return generated by

the company on the capital employed by the shareholders of the company. The

ROCE for the company has fallen by more than 50% in the trend period analyzed

for the company indicating that the company might not be creating value for the

shareholders of the company. The net profitability for the company has fallen in

the trend period analyzed for the company and the same has been due to the rising

expenses for the company in the form of operating expenses and depreciation

expenses for the company (Parsian and Shams Koloukhi 2014). The return on

capital employed for the company was around 9% in the year 2016-17 and was

around 4% in the year 2017-18. The falling return was because of the rising costs

for the company and the falling revenue of the company. The operating margin

for the company was evaluated by using the Earning before tax, depreciation and

tax and the net sales of the company (Ogiela and Ogiela 2014). The operating

margin of the company was around 7.44% in the year 2016-17 and was around

5.85% in the year 2017-18. The operating margin decreased due to falling revenue

of the company and the rising costs and expenses for the company.

iii) The key recommendation that would be recommended is that the company should

reduce the operating expenses of the company and increasing the revenue of the

company. The reduction in the expenses of the company will help the company

grow its profitability and maintain an overall growth of the company in the long-

term.

the company on the capital employed by the shareholders of the company. The

ROCE for the company has fallen by more than 50% in the trend period analyzed

for the company indicating that the company might not be creating value for the

shareholders of the company. The net profitability for the company has fallen in

the trend period analyzed for the company and the same has been due to the rising

expenses for the company in the form of operating expenses and depreciation

expenses for the company (Parsian and Shams Koloukhi 2014). The return on

capital employed for the company was around 9% in the year 2016-17 and was

around 4% in the year 2017-18. The falling return was because of the rising costs

for the company and the falling revenue of the company. The operating margin

for the company was evaluated by using the Earning before tax, depreciation and

tax and the net sales of the company (Ogiela and Ogiela 2014). The operating

margin of the company was around 7.44% in the year 2016-17 and was around

5.85% in the year 2017-18. The operating margin decreased due to falling revenue

of the company and the rising costs and expenses for the company.

iii) The key recommendation that would be recommended is that the company should

reduce the operating expenses of the company and increasing the revenue of the

company. The reduction in the expenses of the company will help the company

grow its profitability and maintain an overall growth of the company in the long-

term.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

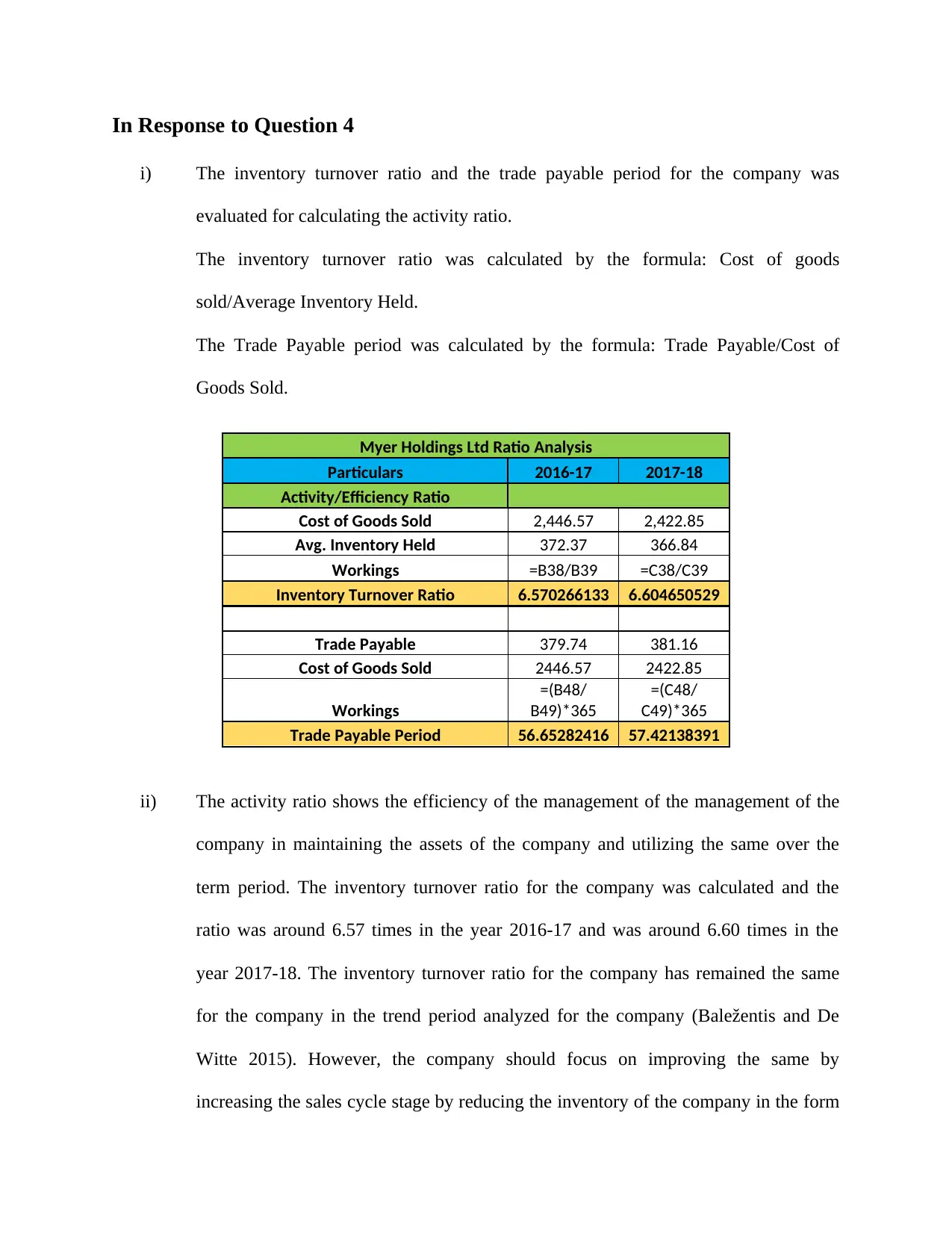

In Response to Question 4

i) The inventory turnover ratio and the trade payable period for the company was

evaluated for calculating the activity ratio.

The inventory turnover ratio was calculated by the formula: Cost of goods

sold/Average Inventory Held.

The Trade Payable period was calculated by the formula: Trade Payable/Cost of

Goods Sold.

Myer Holdings Ltd Ratio Analysis

Particulars 2016-17 2017-18

Activity/Efficiency Ratio

Cost of Goods Sold 2,446.57 2,422.85

Avg. Inventory Held 372.37 366.84

Workings =B38/B39 =C38/C39

Inventory Turnover Ratio 6.570266133 6.604650529

Trade Payable 379.74 381.16

Cost of Goods Sold 2446.57 2422.85

Workings

=(B48/

B49)*365

=(C48/

C49)*365

Trade Payable Period 56.65282416 57.42138391

ii) The activity ratio shows the efficiency of the management of the management of the

company in maintaining the assets of the company and utilizing the same over the

term period. The inventory turnover ratio for the company was calculated and the

ratio was around 6.57 times in the year 2016-17 and was around 6.60 times in the

year 2017-18. The inventory turnover ratio for the company has remained the same

for the company in the trend period analyzed for the company (Baležentis and De

Witte 2015). However, the company should focus on improving the same by

increasing the sales cycle stage by reducing the inventory of the company in the form

i) The inventory turnover ratio and the trade payable period for the company was

evaluated for calculating the activity ratio.

The inventory turnover ratio was calculated by the formula: Cost of goods

sold/Average Inventory Held.

The Trade Payable period was calculated by the formula: Trade Payable/Cost of

Goods Sold.

Myer Holdings Ltd Ratio Analysis

Particulars 2016-17 2017-18

Activity/Efficiency Ratio

Cost of Goods Sold 2,446.57 2,422.85

Avg. Inventory Held 372.37 366.84

Workings =B38/B39 =C38/C39

Inventory Turnover Ratio 6.570266133 6.604650529

Trade Payable 379.74 381.16

Cost of Goods Sold 2446.57 2422.85

Workings

=(B48/

B49)*365

=(C48/

C49)*365

Trade Payable Period 56.65282416 57.42138391

ii) The activity ratio shows the efficiency of the management of the management of the

company in maintaining the assets of the company and utilizing the same over the

term period. The inventory turnover ratio for the company was calculated and the

ratio was around 6.57 times in the year 2016-17 and was around 6.60 times in the

year 2017-18. The inventory turnover ratio for the company has remained the same

for the company in the trend period analyzed for the company (Baležentis and De

Witte 2015). However, the company should focus on improving the same by

increasing the sales cycle stage by reducing the inventory of the company in the form

of sales of the company. The trade payable period for the company was calculated

using the trade payable of the company and the cost of goods sold for the company.

The trade payable period for the company was around 56.65 days and was around

57.42 days in the year 2017-18. It is recommended that the asset management ratio

for the company should be well utilized and should be well utilized by the company

thereby ensuring that there is an optimum utilization of resources for the company.

The asset management ratio for the company could be improved thereby reflecting

the efficiency position for the company (Olson and Zoubi 2017).

In Response to Question 5

The financial analysis of the company was evaluated by applying the ratio analysis of the

company reflecting that the liquidity position for the company has increased marginally but still

the current assets of the company is not sufficient for the company in meeting up the current

obligations of the company (Dewachter et al. 2015). The profitability position of the company

indicates that the same has decreased for the company, which has been due to the falling revenue

base of the company and the rising costs of the company. The financial risk for the company is

also dependenmt on the level of debt for the company and the same inflInvestor can invest in the

company after assessing the financial condition and the viability of the project in the long-term

perspective (Cucchiella, D’Adamo and Gastaldi 2015).

using the trade payable of the company and the cost of goods sold for the company.

The trade payable period for the company was around 56.65 days and was around

57.42 days in the year 2017-18. It is recommended that the asset management ratio

for the company should be well utilized and should be well utilized by the company

thereby ensuring that there is an optimum utilization of resources for the company.

The asset management ratio for the company could be improved thereby reflecting

the efficiency position for the company (Olson and Zoubi 2017).

In Response to Question 5

The financial analysis of the company was evaluated by applying the ratio analysis of the

company reflecting that the liquidity position for the company has increased marginally but still

the current assets of the company is not sufficient for the company in meeting up the current

obligations of the company (Dewachter et al. 2015). The profitability position of the company

indicates that the same has decreased for the company, which has been due to the falling revenue

base of the company and the rising costs of the company. The financial risk for the company is

also dependenmt on the level of debt for the company and the same inflInvestor can invest in the

company after assessing the financial condition and the viability of the project in the long-term

perspective (Cucchiella, D’Adamo and Gastaldi 2015).

Reference

Alper, K., Binici, M., Demiralp, S., Kara, H. and ÖZLÜ, P., 2018. Reserve requirements,

liquidity risk, and bank lending behavior. Journal of Money, Credit and Banking, vol.50 no.(4),

pp.817-827

Baležentis, T. and De Witte, K., 2015. One-and multi-directional conditional efficiency

measurement–Efficiency in Lithuanian family farms. European Journal of Operational

Research, vol.245 no.(2), pp.612-622.

Cucchiella, F., D’Adamo, I. and Gastaldi, M., 2015. Financial analysis for investment and policy

decisions in the renewable energy sector. Clean Technologies and Environmental Policy, vol.17

no.(4), pp.887-904.

Dewachter, H., Iania, L., Lyrio, M. and de Sola Perea, M., 2015. A macro-financial analysis of

the euro area sovereign bond market. Journal of Banking & Finance, vol.50, pp.308-325.

Graham, J.R., Leary, M.T. and Roberts, M.R., 2015. A century of capital structure: The

leveraging of corporate America. Journal of Financial Economics, vol.118 no.(3), pp.658-683.

Klasa, S., Ortiz-Molina, H., Serfling, M. and Srinivasan, S., 2018. Protection of trade secrets and

capital structure decisions. Journal of Financial Economics, vol.128 no.(2), pp.266-286.

Olson, D. and Zoubi, T., 2017. Convergence in bank performance for commercial and Islamic

banks during and after the Global Financial Crisis. The Quarterly Review of Economics and

Finance, vol.65, pp.71-87.

Parsian, H. and Shams Koloukhi, A., 2014. A study on the effect of free cash flow and

profitability current ratio on dividend payout ratio: Evidence from Tehran Stock Exchange.

Management Science Letters, vol. 4, pp.63-70.

Setiawan, H. and Amboningtyas, D., 2018. FINANCIAL RATIO ANALYSIS FOR

PREDICTING FINANCIAL DISTRESS CONDITIONS (Study on Telecommunication

Companies Listed In Indonesia Stock Exchange Period 2010-2016). Journal of Management,

vol.4 no.(4).

Alper, K., Binici, M., Demiralp, S., Kara, H. and ÖZLÜ, P., 2018. Reserve requirements,

liquidity risk, and bank lending behavior. Journal of Money, Credit and Banking, vol.50 no.(4),

pp.817-827

Baležentis, T. and De Witte, K., 2015. One-and multi-directional conditional efficiency

measurement–Efficiency in Lithuanian family farms. European Journal of Operational

Research, vol.245 no.(2), pp.612-622.

Cucchiella, F., D’Adamo, I. and Gastaldi, M., 2015. Financial analysis for investment and policy

decisions in the renewable energy sector. Clean Technologies and Environmental Policy, vol.17

no.(4), pp.887-904.

Dewachter, H., Iania, L., Lyrio, M. and de Sola Perea, M., 2015. A macro-financial analysis of

the euro area sovereign bond market. Journal of Banking & Finance, vol.50, pp.308-325.

Graham, J.R., Leary, M.T. and Roberts, M.R., 2015. A century of capital structure: The

leveraging of corporate America. Journal of Financial Economics, vol.118 no.(3), pp.658-683.

Klasa, S., Ortiz-Molina, H., Serfling, M. and Srinivasan, S., 2018. Protection of trade secrets and

capital structure decisions. Journal of Financial Economics, vol.128 no.(2), pp.266-286.

Olson, D. and Zoubi, T., 2017. Convergence in bank performance for commercial and Islamic

banks during and after the Global Financial Crisis. The Quarterly Review of Economics and

Finance, vol.65, pp.71-87.

Parsian, H. and Shams Koloukhi, A., 2014. A study on the effect of free cash flow and

profitability current ratio on dividend payout ratio: Evidence from Tehran Stock Exchange.

Management Science Letters, vol. 4, pp.63-70.

Setiawan, H. and Amboningtyas, D., 2018. FINANCIAL RATIO ANALYSIS FOR

PREDICTING FINANCIAL DISTRESS CONDITIONS (Study on Telecommunication

Companies Listed In Indonesia Stock Exchange Period 2010-2016). Journal of Management,

vol.4 no.(4).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

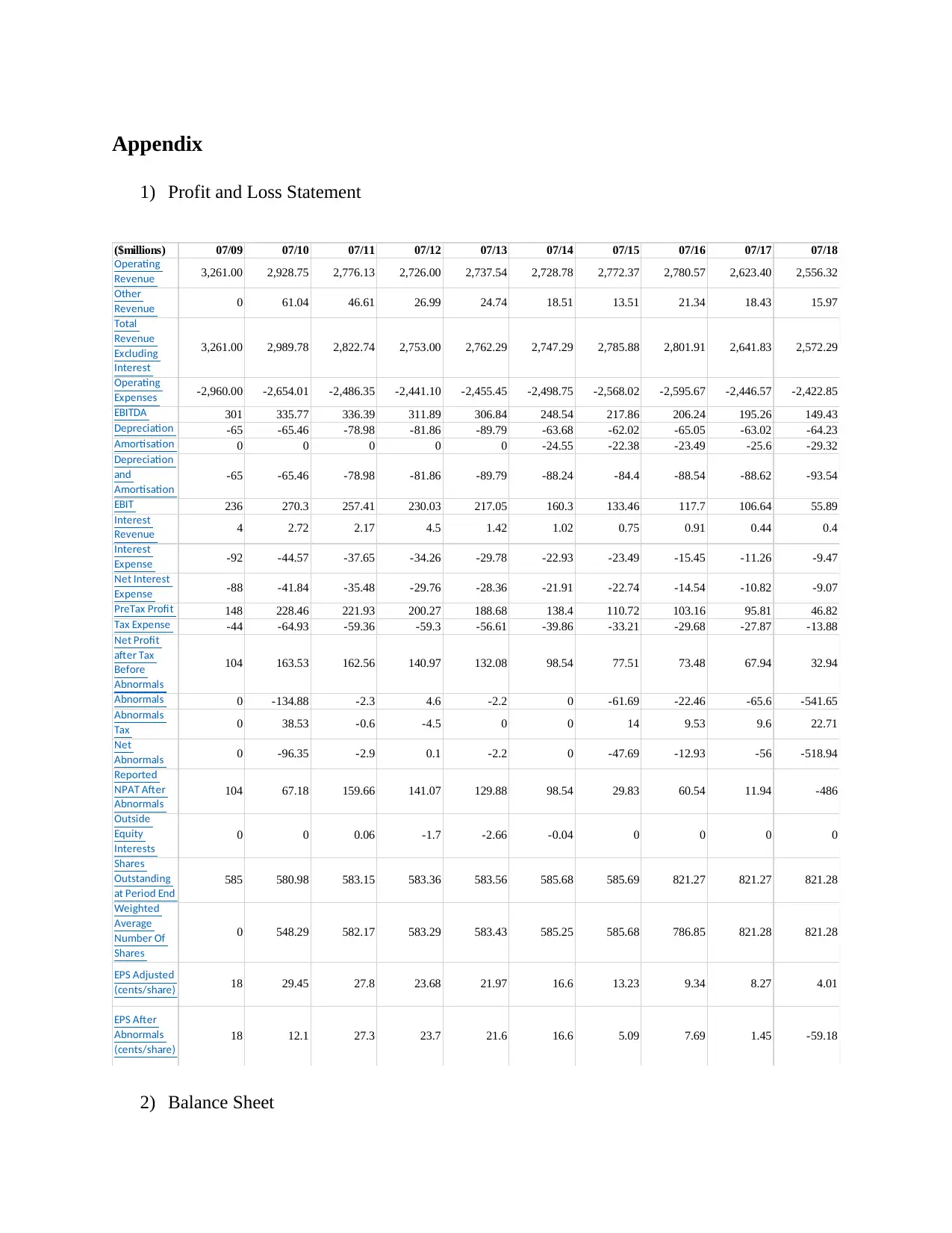

Appendix

1) Profit and Loss Statement

($millions) 07/09 07/10 07/11 07/12 07/13 07/14 07/15 07/16 07/17 07/18

Operating

Revenue 3,261.00 2,928.75 2,776.13 2,726.00 2,737.54 2,728.78 2,772.37 2,780.57 2,623.40 2,556.32

Other

Revenue 0 61.04 46.61 26.99 24.74 18.51 13.51 21.34 18.43 15.97

Total

Revenue

Excluding

Interest

3,261.00 2,989.78 2,822.74 2,753.00 2,762.29 2,747.29 2,785.88 2,801.91 2,641.83 2,572.29

Operating

Expenses -2,960.00 -2,654.01 -2,486.35 -2,441.10 -2,455.45 -2,498.75 -2,568.02 -2,595.67 -2,446.57 -2,422.85

EBITDA 301 335.77 336.39 311.89 306.84 248.54 217.86 206.24 195.26 149.43

Depreciation -65 -65.46 -78.98 -81.86 -89.79 -63.68 -62.02 -65.05 -63.02 -64.23

Amortisation 0 0 0 0 0 -24.55 -22.38 -23.49 -25.6 -29.32

Depreciation

and

Amortisation

-65 -65.46 -78.98 -81.86 -89.79 -88.24 -84.4 -88.54 -88.62 -93.54

EBIT 236 270.3 257.41 230.03 217.05 160.3 133.46 117.7 106.64 55.89

Interest

Revenue 4 2.72 2.17 4.5 1.42 1.02 0.75 0.91 0.44 0.4

Interest

Expense -92 -44.57 -37.65 -34.26 -29.78 -22.93 -23.49 -15.45 -11.26 -9.47

Net Interest

Expense -88 -41.84 -35.48 -29.76 -28.36 -21.91 -22.74 -14.54 -10.82 -9.07

PreTax Profit 148 228.46 221.93 200.27 188.68 138.4 110.72 103.16 95.81 46.82

Tax Expense -44 -64.93 -59.36 -59.3 -56.61 -39.86 -33.21 -29.68 -27.87 -13.88

Net Profit

after Tax

Before

Abnormals

104 163.53 162.56 140.97 132.08 98.54 77.51 73.48 67.94 32.94

Abnormals 0 -134.88 -2.3 4.6 -2.2 0 -61.69 -22.46 -65.6 -541.65

Abnormals

Tax 0 38.53 -0.6 -4.5 0 0 14 9.53 9.6 22.71

Net

Abnormals 0 -96.35 -2.9 0.1 -2.2 0 -47.69 -12.93 -56 -518.94

Reported

NPAT After

Abnormals

104 67.18 159.66 141.07 129.88 98.54 29.83 60.54 11.94 -486

Outside

Equity

Interests

0 0 0.06 -1.7 -2.66 -0.04 0 0 0 0

Shares

Outstanding

at Period End

585 580.98 583.15 583.36 583.56 585.68 585.69 821.27 821.27 821.28

Weighted

Average

Number Of

Shares

0 548.29 582.17 583.29 583.43 585.25 585.68 786.85 821.28 821.28

EPS Adjusted

(cents/share) 18 29.45 27.8 23.68 21.97 16.6 13.23 9.34 8.27 4.01

EPS After

Abnormals

(cents/share)

18 12.1 27.3 23.7 21.6 16.6 5.09 7.69 1.45 -59.18

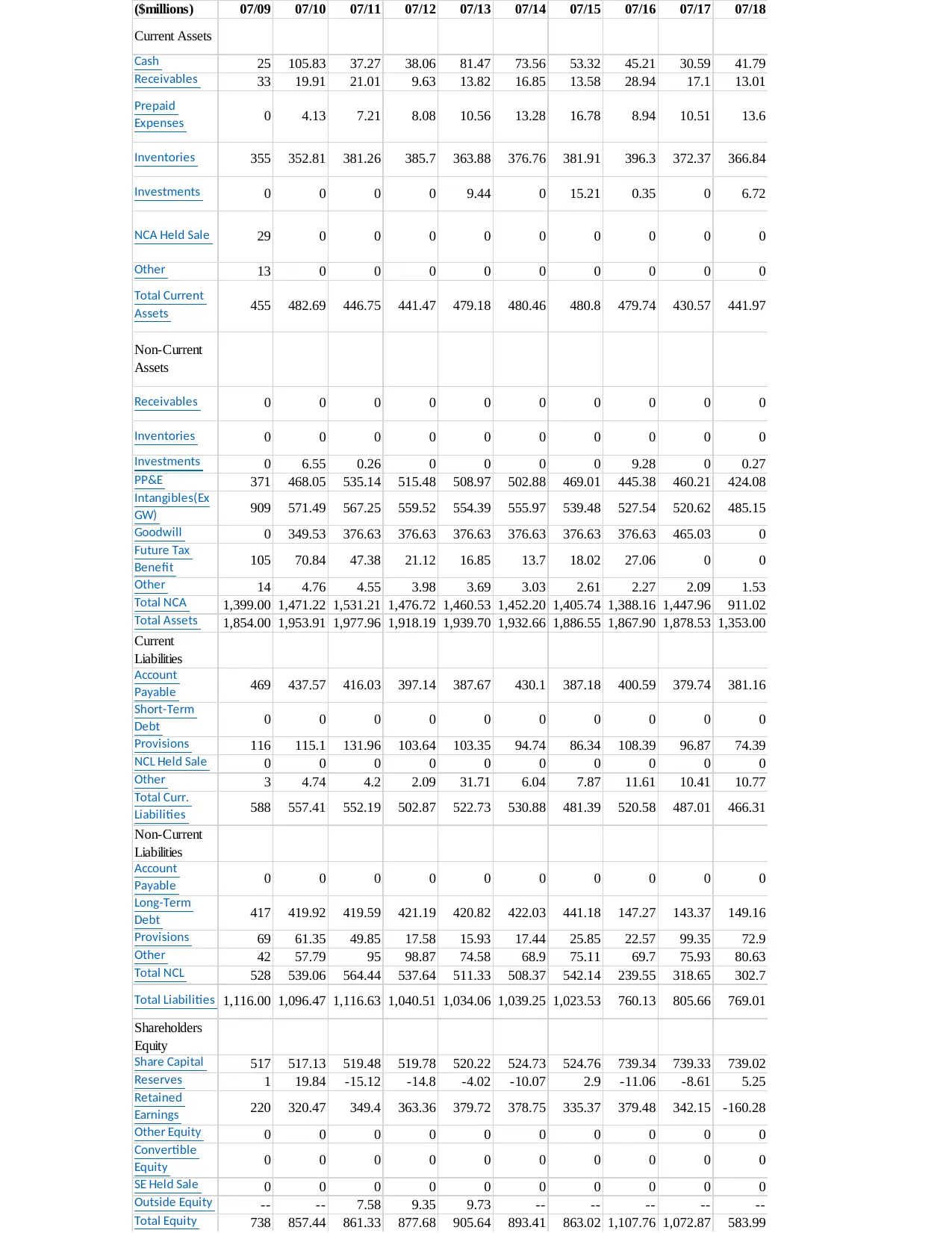

2) Balance Sheet

1) Profit and Loss Statement

($millions) 07/09 07/10 07/11 07/12 07/13 07/14 07/15 07/16 07/17 07/18

Operating

Revenue 3,261.00 2,928.75 2,776.13 2,726.00 2,737.54 2,728.78 2,772.37 2,780.57 2,623.40 2,556.32

Other

Revenue 0 61.04 46.61 26.99 24.74 18.51 13.51 21.34 18.43 15.97

Total

Revenue

Excluding

Interest

3,261.00 2,989.78 2,822.74 2,753.00 2,762.29 2,747.29 2,785.88 2,801.91 2,641.83 2,572.29

Operating

Expenses -2,960.00 -2,654.01 -2,486.35 -2,441.10 -2,455.45 -2,498.75 -2,568.02 -2,595.67 -2,446.57 -2,422.85

EBITDA 301 335.77 336.39 311.89 306.84 248.54 217.86 206.24 195.26 149.43

Depreciation -65 -65.46 -78.98 -81.86 -89.79 -63.68 -62.02 -65.05 -63.02 -64.23

Amortisation 0 0 0 0 0 -24.55 -22.38 -23.49 -25.6 -29.32

Depreciation

and

Amortisation

-65 -65.46 -78.98 -81.86 -89.79 -88.24 -84.4 -88.54 -88.62 -93.54

EBIT 236 270.3 257.41 230.03 217.05 160.3 133.46 117.7 106.64 55.89

Interest

Revenue 4 2.72 2.17 4.5 1.42 1.02 0.75 0.91 0.44 0.4

Interest

Expense -92 -44.57 -37.65 -34.26 -29.78 -22.93 -23.49 -15.45 -11.26 -9.47

Net Interest

Expense -88 -41.84 -35.48 -29.76 -28.36 -21.91 -22.74 -14.54 -10.82 -9.07

PreTax Profit 148 228.46 221.93 200.27 188.68 138.4 110.72 103.16 95.81 46.82

Tax Expense -44 -64.93 -59.36 -59.3 -56.61 -39.86 -33.21 -29.68 -27.87 -13.88

Net Profit

after Tax

Before

Abnormals

104 163.53 162.56 140.97 132.08 98.54 77.51 73.48 67.94 32.94

Abnormals 0 -134.88 -2.3 4.6 -2.2 0 -61.69 -22.46 -65.6 -541.65

Abnormals

Tax 0 38.53 -0.6 -4.5 0 0 14 9.53 9.6 22.71

Net

Abnormals 0 -96.35 -2.9 0.1 -2.2 0 -47.69 -12.93 -56 -518.94

Reported

NPAT After

Abnormals

104 67.18 159.66 141.07 129.88 98.54 29.83 60.54 11.94 -486

Outside

Equity

Interests

0 0 0.06 -1.7 -2.66 -0.04 0 0 0 0

Shares

Outstanding

at Period End

585 580.98 583.15 583.36 583.56 585.68 585.69 821.27 821.27 821.28

Weighted

Average

Number Of

Shares

0 548.29 582.17 583.29 583.43 585.25 585.68 786.85 821.28 821.28

EPS Adjusted

(cents/share) 18 29.45 27.8 23.68 21.97 16.6 13.23 9.34 8.27 4.01

EPS After

Abnormals

(cents/share)

18 12.1 27.3 23.7 21.6 16.6 5.09 7.69 1.45 -59.18

2) Balance Sheet

($millions) 07/09 07/10 07/11 07/12 07/13 07/14 07/15 07/16 07/17 07/18

Current Assets

Cash 25 105.83 37.27 38.06 81.47 73.56 53.32 45.21 30.59 41.79

Receivables 33 19.91 21.01 9.63 13.82 16.85 13.58 28.94 17.1 13.01

Prepaid

Expenses 0 4.13 7.21 8.08 10.56 13.28 16.78 8.94 10.51 13.6

Inventories 355 352.81 381.26 385.7 363.88 376.76 381.91 396.3 372.37 366.84

Investments 0 0 0 0 9.44 0 15.21 0.35 0 6.72

NCA Held Sale 29 0 0 0 0 0 0 0 0 0

Other 13 0 0 0 0 0 0 0 0 0

Total Current

Assets 455 482.69 446.75 441.47 479.18 480.46 480.8 479.74 430.57 441.97

Non-Current

Assets

Receivables 0 0 0 0 0 0 0 0 0 0

Inventories 0 0 0 0 0 0 0 0 0 0

Investments 0 6.55 0.26 0 0 0 0 9.28 0 0.27

PP&E 371 468.05 535.14 515.48 508.97 502.88 469.01 445.38 460.21 424.08

Intangibles(Ex

GW) 909 571.49 567.25 559.52 554.39 555.97 539.48 527.54 520.62 485.15

Goodwill 0 349.53 376.63 376.63 376.63 376.63 376.63 376.63 465.03 0

Future Tax

Benefit 105 70.84 47.38 21.12 16.85 13.7 18.02 27.06 0 0

Other 14 4.76 4.55 3.98 3.69 3.03 2.61 2.27 2.09 1.53

Total NCA 1,399.00 1,471.22 1,531.21 1,476.72 1,460.53 1,452.20 1,405.74 1,388.16 1,447.96 911.02

Total Assets 1,854.00 1,953.91 1,977.96 1,918.19 1,939.70 1,932.66 1,886.55 1,867.90 1,878.53 1,353.00

Current

Liabilities

Account

Payable 469 437.57 416.03 397.14 387.67 430.1 387.18 400.59 379.74 381.16

Short-Term

Debt 0 0 0 0 0 0 0 0 0 0

Provisions 116 115.1 131.96 103.64 103.35 94.74 86.34 108.39 96.87 74.39

NCL Held Sale 0 0 0 0 0 0 0 0 0 0

Other 3 4.74 4.2 2.09 31.71 6.04 7.87 11.61 10.41 10.77

Total Curr.

Liabilities 588 557.41 552.19 502.87 522.73 530.88 481.39 520.58 487.01 466.31

Non-Current

Liabilities

Account

Payable 0 0 0 0 0 0 0 0 0 0

Long-Term

Debt 417 419.92 419.59 421.19 420.82 422.03 441.18 147.27 143.37 149.16

Provisions 69 61.35 49.85 17.58 15.93 17.44 25.85 22.57 99.35 72.9

Other 42 57.79 95 98.87 74.58 68.9 75.11 69.7 75.93 80.63

Total NCL 528 539.06 564.44 537.64 511.33 508.37 542.14 239.55 318.65 302.7

Total Liabilities 1,116.00 1,096.47 1,116.63 1,040.51 1,034.06 1,039.25 1,023.53 760.13 805.66 769.01

Shareholders

Equity

Share Capital 517 517.13 519.48 519.78 520.22 524.73 524.76 739.34 739.33 739.02

Reserves 1 19.84 -15.12 -14.8 -4.02 -10.07 2.9 -11.06 -8.61 5.25

Retained

Earnings 220 320.47 349.4 363.36 379.72 378.75 335.37 379.48 342.15 -160.28

Other Equity 0 0 0 0 0 0 0 0 0 0

Convertible

Equity 0 0 0 0 0 0 0 0 0 0

SE Held Sale 0 0 0 0 0 0 0 0 0 0

Outside Equity -- -- 7.58 9.35 9.73 -- -- -- -- --

Total Equity 738 857.44 861.33 877.68 905.64 893.41 863.02 1,107.76 1,072.87 583.99

Current Assets

Cash 25 105.83 37.27 38.06 81.47 73.56 53.32 45.21 30.59 41.79

Receivables 33 19.91 21.01 9.63 13.82 16.85 13.58 28.94 17.1 13.01

Prepaid

Expenses 0 4.13 7.21 8.08 10.56 13.28 16.78 8.94 10.51 13.6

Inventories 355 352.81 381.26 385.7 363.88 376.76 381.91 396.3 372.37 366.84

Investments 0 0 0 0 9.44 0 15.21 0.35 0 6.72

NCA Held Sale 29 0 0 0 0 0 0 0 0 0

Other 13 0 0 0 0 0 0 0 0 0

Total Current

Assets 455 482.69 446.75 441.47 479.18 480.46 480.8 479.74 430.57 441.97

Non-Current

Assets

Receivables 0 0 0 0 0 0 0 0 0 0

Inventories 0 0 0 0 0 0 0 0 0 0

Investments 0 6.55 0.26 0 0 0 0 9.28 0 0.27

PP&E 371 468.05 535.14 515.48 508.97 502.88 469.01 445.38 460.21 424.08

Intangibles(Ex

GW) 909 571.49 567.25 559.52 554.39 555.97 539.48 527.54 520.62 485.15

Goodwill 0 349.53 376.63 376.63 376.63 376.63 376.63 376.63 465.03 0

Future Tax

Benefit 105 70.84 47.38 21.12 16.85 13.7 18.02 27.06 0 0

Other 14 4.76 4.55 3.98 3.69 3.03 2.61 2.27 2.09 1.53

Total NCA 1,399.00 1,471.22 1,531.21 1,476.72 1,460.53 1,452.20 1,405.74 1,388.16 1,447.96 911.02

Total Assets 1,854.00 1,953.91 1,977.96 1,918.19 1,939.70 1,932.66 1,886.55 1,867.90 1,878.53 1,353.00

Current

Liabilities

Account

Payable 469 437.57 416.03 397.14 387.67 430.1 387.18 400.59 379.74 381.16

Short-Term

Debt 0 0 0 0 0 0 0 0 0 0

Provisions 116 115.1 131.96 103.64 103.35 94.74 86.34 108.39 96.87 74.39

NCL Held Sale 0 0 0 0 0 0 0 0 0 0

Other 3 4.74 4.2 2.09 31.71 6.04 7.87 11.61 10.41 10.77

Total Curr.

Liabilities 588 557.41 552.19 502.87 522.73 530.88 481.39 520.58 487.01 466.31

Non-Current

Liabilities

Account

Payable 0 0 0 0 0 0 0 0 0 0

Long-Term

Debt 417 419.92 419.59 421.19 420.82 422.03 441.18 147.27 143.37 149.16

Provisions 69 61.35 49.85 17.58 15.93 17.44 25.85 22.57 99.35 72.9

Other 42 57.79 95 98.87 74.58 68.9 75.11 69.7 75.93 80.63

Total NCL 528 539.06 564.44 537.64 511.33 508.37 542.14 239.55 318.65 302.7

Total Liabilities 1,116.00 1,096.47 1,116.63 1,040.51 1,034.06 1,039.25 1,023.53 760.13 805.66 769.01

Shareholders

Equity

Share Capital 517 517.13 519.48 519.78 520.22 524.73 524.76 739.34 739.33 739.02

Reserves 1 19.84 -15.12 -14.8 -4.02 -10.07 2.9 -11.06 -8.61 5.25

Retained

Earnings 220 320.47 349.4 363.36 379.72 378.75 335.37 379.48 342.15 -160.28

Other Equity 0 0 0 0 0 0 0 0 0 0

Convertible

Equity 0 0 0 0 0 0 0 0 0 0

SE Held Sale 0 0 0 0 0 0 0 0 0 0

Outside Equity -- -- 7.58 9.35 9.73 -- -- -- -- --

Total Equity 738 857.44 861.33 877.68 905.64 893.41 863.02 1,107.76 1,072.87 583.99

3) Ratio Analysis

Particulars 2016-17 2017-18

Gearing/Capital Structure Ratio

Debt 143.37 149.16

Equity 739.33 739.02

Workings =(B4/B5) =(C4/C5)

Debt to Equity Ratio 19% 20%

Assets 1878.53 1353.00

Equity 739.33 739.02

Workings =(B9/B10) =(C9/C10)

Asset/Equity Ratio 254% 183%

Profitability Ratio

Net Profit 67.94 32.94

Capital Employed 739.33 739.02

Workings =B15/B16 =C15/C16

Return on capital employed 9% 4%

Earnings Before Interest and Tax 195.26 149.43

Sales 2,623.40 2,556.32

Workings =B20/B21 =C20/C21

Operating profit margin ratio 7.44% 5.85%

Liquidity Ratio

Current Assets 430.57 441.97

Current Liabilities 487.01 466.31

Workings =B26/B27 =C26/C27

Current Ratio 0.88 0.95

Cash 30.59 41.79

Accounts Receivable 17.1 13.01

Current Liabilities 487.01 466.31

Workings =(B31+B32)/B33 =(C31+C32)/C33

Quick Ratio 0.10 0.12

Activity/Efficiency Ratio

Cost of Goods Sold 2,446.57 2,422.85

Avg. Inventory Held 372.37 366.84

Workings =B38/B39 =C38/C39

Inventory Turnover Ratio 6.570266133 6.604650529

Trade Payable 379.74 381.16

Cost of Goods Sold 2446.57 2422.85

Workings =(B48/B49)*365 =(C48/C49)*365

Trade Payable Period 56.65282416 57.42138391

Myer Holdings Ltd Ratio Analysis

Particulars 2016-17 2017-18

Gearing/Capital Structure Ratio

Debt 143.37 149.16

Equity 739.33 739.02

Workings =(B4/B5) =(C4/C5)

Debt to Equity Ratio 19% 20%

Assets 1878.53 1353.00

Equity 739.33 739.02

Workings =(B9/B10) =(C9/C10)

Asset/Equity Ratio 254% 183%

Profitability Ratio

Net Profit 67.94 32.94

Capital Employed 739.33 739.02

Workings =B15/B16 =C15/C16

Return on capital employed 9% 4%

Earnings Before Interest and Tax 195.26 149.43

Sales 2,623.40 2,556.32

Workings =B20/B21 =C20/C21

Operating profit margin ratio 7.44% 5.85%

Liquidity Ratio

Current Assets 430.57 441.97

Current Liabilities 487.01 466.31

Workings =B26/B27 =C26/C27

Current Ratio 0.88 0.95

Cash 30.59 41.79

Accounts Receivable 17.1 13.01

Current Liabilities 487.01 466.31

Workings =(B31+B32)/B33 =(C31+C32)/C33

Quick Ratio 0.10 0.12

Activity/Efficiency Ratio

Cost of Goods Sold 2,446.57 2,422.85

Avg. Inventory Held 372.37 366.84

Workings =B38/B39 =C38/C39

Inventory Turnover Ratio 6.570266133 6.604650529

Trade Payable 379.74 381.16

Cost of Goods Sold 2446.57 2422.85

Workings =(B48/B49)*365 =(C48/C49)*365

Trade Payable Period 56.65282416 57.42138391

Myer Holdings Ltd Ratio Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.