Financial Reporting for Businesses: Financial Ratio Analysis Report

VerifiedAdded on 2021/02/20

|15

|3784

|42

Report

AI Summary

This report provides a comprehensive financial analysis of Unite Group Plc, focusing on the years 2018 and 2017. It begins with an introduction to financial reporting and its importance for stakeholders. The main body of the report includes the calculation of various financial ratios, categorized into profitability, liquidity, efficiency, and gearing ratios. The report then delves into an analysis of the company's financial performance, interpreting the trends and implications of the calculated ratios. The analysis includes an assessment of the company's gross profit ratio, return on assets, return on equity, quick ratio, current ratio, working capital ratio, inventory turnover ratio, asset turnover ratio, days sales in inventory, debt to equity ratio, debt ratio, and equity ratio. The report concludes with an evaluation of changes related to Lease Accounting rules, specifically the transition from IAS 17 Leases to IFRS 16 Leases. The report aims to provide a clear understanding of the company's financial position and performance based on the ratio analysis.

Financial Reporting for

Businesses

Businesses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

a. Calculation of financial ratio for 2018 and 2017....................................................................3

b. Analysis of financial performance..........................................................................................8

c. Evaluating changes related to Lease Accounting rules.........................................................10

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

a. Calculation of financial ratio for 2018 and 2017....................................................................3

b. Analysis of financial performance..........................................................................................8

c. Evaluating changes related to Lease Accounting rules.........................................................10

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

The term financial reporting is related to the process of making full disclosure of all the financial

as well as non financial information of the company in its own final report as prepared for every

accounting period ending. With the help of financial reporting, the management of the company

can have overview of overall solvency as well as liquidity aspects of business and measures to be

undertaken by the management for making improvement in it. It assists many stakeholders in

getting deep insight about how the company is performing in a particular accounting period. The

present report is based on the Unite Group Plc of which financial assessment will be done with

the help of financial ratio analysis. Also, explanation will be made about its financial

performance and position for the year 2018 and 2017. At last, emphasis will be made on defining

changes in the Lease accounting rules from IAS 17 Leases to IFRS 16 Leases.

MAIN BODY

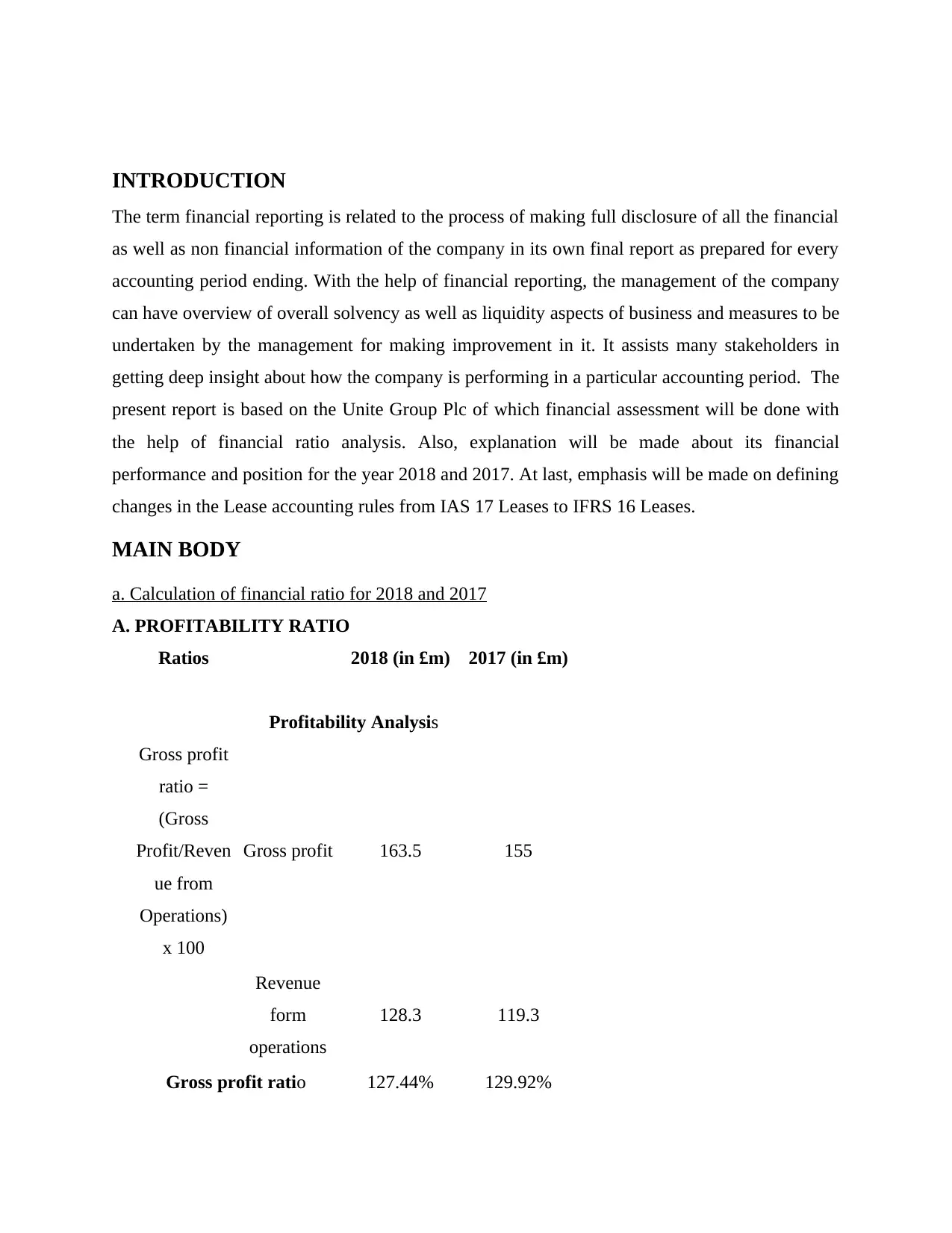

a. Calculation of financial ratio for 2018 and 2017

A. PROFITABILITY RATIO

Ratios 2018 (in £m) 2017 (in £m)

Profitability Analysis

Gross profit

ratio =

(Gross

Profit/Reven

ue from

Operations)

x 100

Gross profit 163.5 155

Revenue

form

operations

128.3 119.3

Gross profit ratio 127.44% 129.92%

The term financial reporting is related to the process of making full disclosure of all the financial

as well as non financial information of the company in its own final report as prepared for every

accounting period ending. With the help of financial reporting, the management of the company

can have overview of overall solvency as well as liquidity aspects of business and measures to be

undertaken by the management for making improvement in it. It assists many stakeholders in

getting deep insight about how the company is performing in a particular accounting period. The

present report is based on the Unite Group Plc of which financial assessment will be done with

the help of financial ratio analysis. Also, explanation will be made about its financial

performance and position for the year 2018 and 2017. At last, emphasis will be made on defining

changes in the Lease accounting rules from IAS 17 Leases to IFRS 16 Leases.

MAIN BODY

a. Calculation of financial ratio for 2018 and 2017

A. PROFITABILITY RATIO

Ratios 2018 (in £m) 2017 (in £m)

Profitability Analysis

Gross profit

ratio =

(Gross

Profit/Reven

ue from

Operations)

x 100

Gross profit 163.5 155

Revenue

form

operations

128.3 119.3

Gross profit ratio 127.44% 129.92%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Return on

Assets

(ROA) = Net

income/

Total assets

Net income 237.3 223.8

Total assets 2849.5 2431.6

Return on Assets 8.33% 9.20%

Return on

Equity = Net

income/

Shareholders

equity

Net income 237.3 223.8

Shareholders

equity 2073 1729

Return on Equity 11.45% 12.94%

B. LIQUIDITY RATIO

Ratios 2018 (in £m) 2017 (in £m)

Liquidity Analysis

Quick ratio

= (Total

current

assets –

Inventory –

Prepaid

expenses)/

Total current

assets

220.8 138.6

Assets

(ROA) = Net

income/

Total assets

Net income 237.3 223.8

Total assets 2849.5 2431.6

Return on Assets 8.33% 9.20%

Return on

Equity = Net

income/

Shareholders

equity

Net income 237.3 223.8

Shareholders

equity 2073 1729

Return on Equity 11.45% 12.94%

B. LIQUIDITY RATIO

Ratios 2018 (in £m) 2017 (in £m)

Liquidity Analysis

Quick ratio

= (Total

current

assets –

Inventory –

Prepaid

expenses)/

Total current

assets

220.8 138.6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

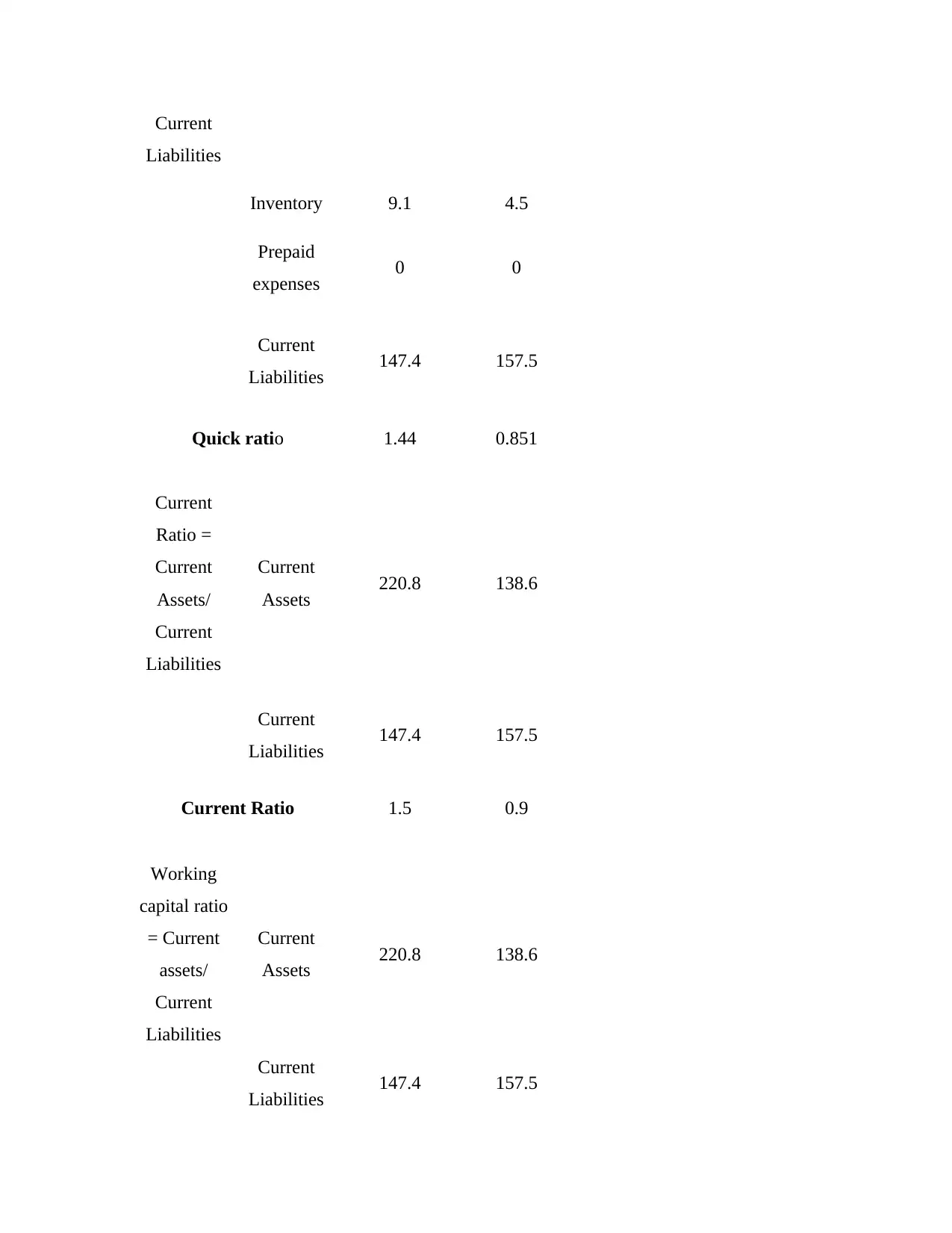

Current

Liabilities

Inventory 9.1 4.5

Prepaid

expenses 0 0

Current

Liabilities 147.4 157.5

Quick ratio 1.44 0.851

Current

Ratio =

Current

Assets/

Current

Liabilities

Current

Assets 220.8 138.6

Current

Liabilities 147.4 157.5

Current Ratio 1.5 0.9

Working

capital ratio

= Current

assets/

Current

Liabilities

Current

Assets 220.8 138.6

Current

Liabilities 147.4 157.5

Liabilities

Inventory 9.1 4.5

Prepaid

expenses 0 0

Current

Liabilities 147.4 157.5

Quick ratio 1.44 0.851

Current

Ratio =

Current

Assets/

Current

Liabilities

Current

Assets 220.8 138.6

Current

Liabilities 147.4 157.5

Current Ratio 1.5 0.9

Working

capital ratio

= Current

assets/

Current

Liabilities

Current

Assets 220.8 138.6

Current

Liabilities 147.4 157.5

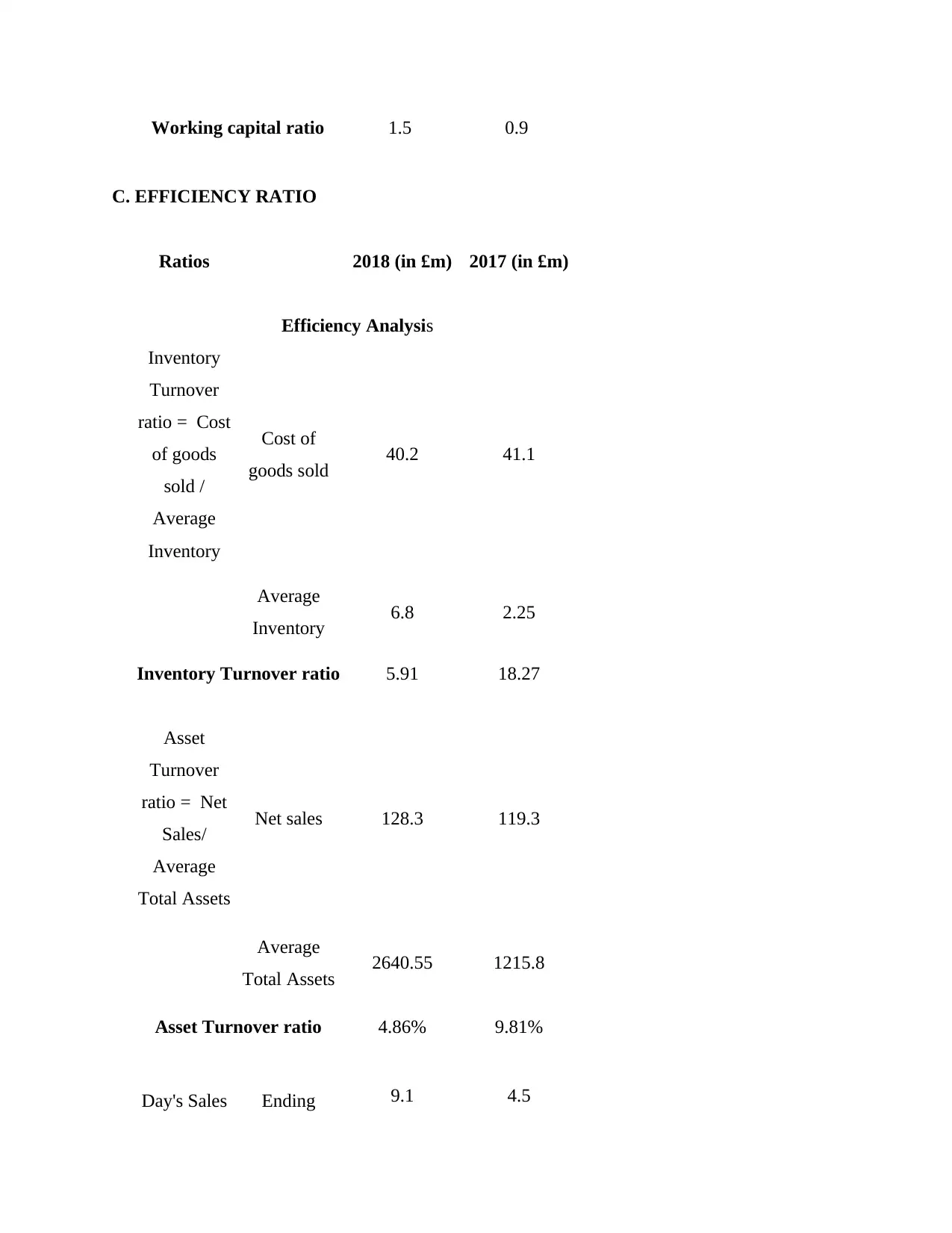

Working capital ratio 1.5 0.9

C. EFFICIENCY RATIO

Ratios 2018 (in £m) 2017 (in £m)

Efficiency Analysis

Inventory

Turnover

ratio = Cost

of goods

sold /

Average

Inventory

Cost of

goods sold 40.2 41.1

Average

Inventory 6.8 2.25

Inventory Turnover ratio 5.91 18.27

Asset

Turnover

ratio = Net

Sales/

Average

Total Assets

Net sales 128.3 119.3

Average

Total Assets 2640.55 1215.8

Asset Turnover ratio 4.86% 9.81%

Day's Sales Ending 9.1 4.5

C. EFFICIENCY RATIO

Ratios 2018 (in £m) 2017 (in £m)

Efficiency Analysis

Inventory

Turnover

ratio = Cost

of goods

sold /

Average

Inventory

Cost of

goods sold 40.2 41.1

Average

Inventory 6.8 2.25

Inventory Turnover ratio 5.91 18.27

Asset

Turnover

ratio = Net

Sales/

Average

Total Assets

Net sales 128.3 119.3

Average

Total Assets 2640.55 1215.8

Asset Turnover ratio 4.86% 9.81%

Day's Sales Ending 9.1 4.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in Inventory

= (Ending

Inventory/C

ost of Goods

Sold) * 365

Inventory

Cost of

goods sold 40.2 41.1

Day's Sales in Inventory 82.62 39.96

D. GEARING RATIO

Ratios 2018 (in £m) 2017 (in £m)

Gearing Analysis

Debt to

equity ratio

= Total

liabilities /

Shareholder

s equity

Total

Liabilities 750.7 677.4

Shareholders

equity 2073 1729

Debt to equity ratio 0.36 0.39

Debt ratio =

Total

assets /

Total debt

Total debt 609.2 525.3

= (Ending

Inventory/C

ost of Goods

Sold) * 365

Inventory

Cost of

goods sold 40.2 41.1

Day's Sales in Inventory 82.62 39.96

D. GEARING RATIO

Ratios 2018 (in £m) 2017 (in £m)

Gearing Analysis

Debt to

equity ratio

= Total

liabilities /

Shareholder

s equity

Total

Liabilities 750.7 677.4

Shareholders

equity 2073 1729

Debt to equity ratio 0.36 0.39

Debt ratio =

Total

assets /

Total debt

Total debt 609.2 525.3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

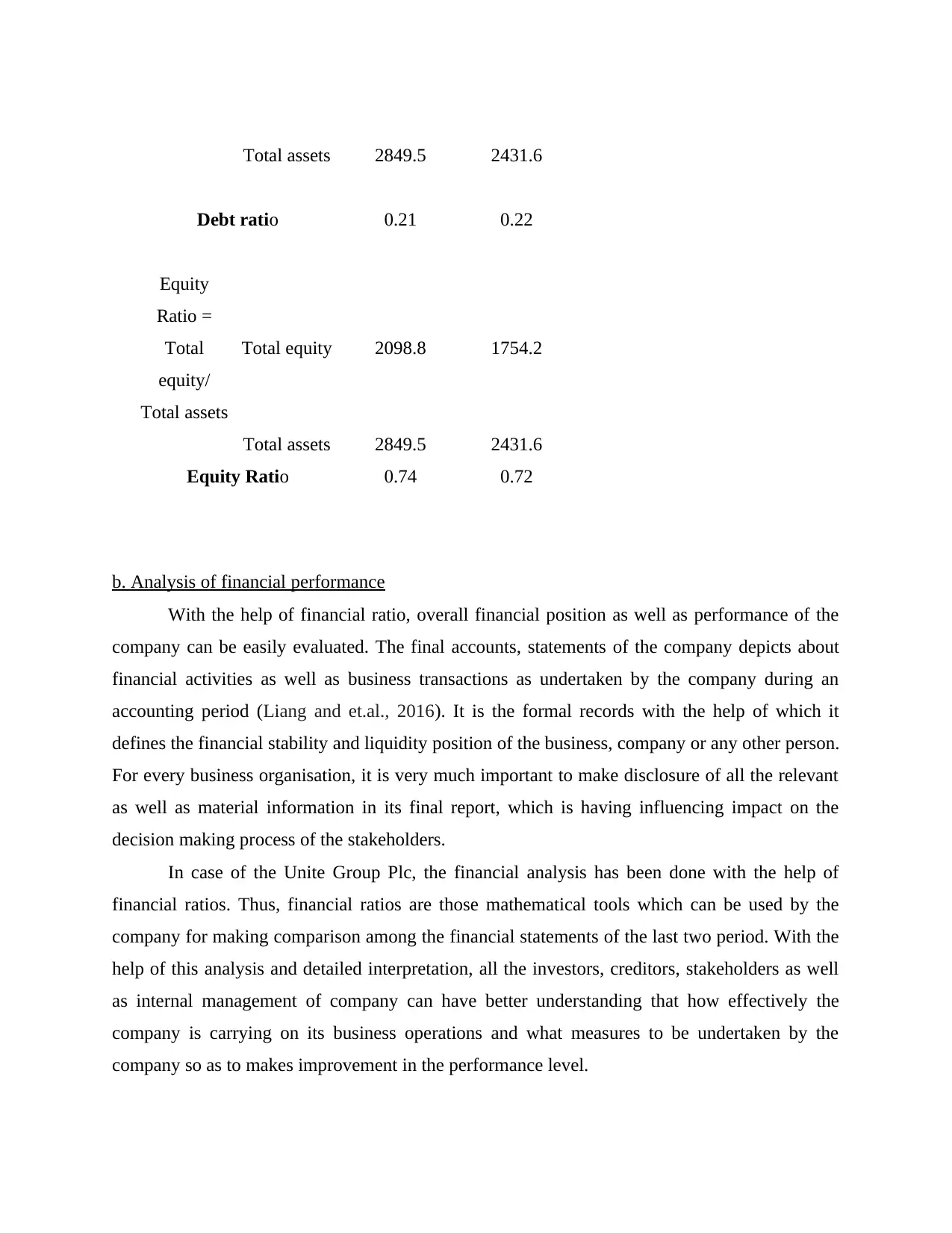

Total assets 2849.5 2431.6

Debt ratio 0.21 0.22

Equity

Ratio =

Total

equity/

Total assets

Total equity 2098.8 1754.2

Total assets 2849.5 2431.6

Equity Ratio 0.74 0.72

b. Analysis of financial performance

With the help of financial ratio, overall financial position as well as performance of the

company can be easily evaluated. The final accounts, statements of the company depicts about

financial activities as well as business transactions as undertaken by the company during an

accounting period (Liang and et.al., 2016). It is the formal records with the help of which it

defines the financial stability and liquidity position of the business, company or any other person.

For every business organisation, it is very much important to make disclosure of all the relevant

as well as material information in its final report, which is having influencing impact on the

decision making process of the stakeholders.

In case of the Unite Group Plc, the financial analysis has been done with the help of

financial ratios. Thus, financial ratios are those mathematical tools which can be used by the

company for making comparison among the financial statements of the last two period. With the

help of this analysis and detailed interpretation, all the investors, creditors, stakeholders as well

as internal management of company can have better understanding that how effectively the

company is carrying on its business operations and what measures to be undertaken by the

company so as to makes improvement in the performance level.

Debt ratio 0.21 0.22

Equity

Ratio =

Total

equity/

Total assets

Total equity 2098.8 1754.2

Total assets 2849.5 2431.6

Equity Ratio 0.74 0.72

b. Analysis of financial performance

With the help of financial ratio, overall financial position as well as performance of the

company can be easily evaluated. The final accounts, statements of the company depicts about

financial activities as well as business transactions as undertaken by the company during an

accounting period (Liang and et.al., 2016). It is the formal records with the help of which it

defines the financial stability and liquidity position of the business, company or any other person.

For every business organisation, it is very much important to make disclosure of all the relevant

as well as material information in its final report, which is having influencing impact on the

decision making process of the stakeholders.

In case of the Unite Group Plc, the financial analysis has been done with the help of

financial ratios. Thus, financial ratios are those mathematical tools which can be used by the

company for making comparison among the financial statements of the last two period. With the

help of this analysis and detailed interpretation, all the investors, creditors, stakeholders as well

as internal management of company can have better understanding that how effectively the

company is carrying on its business operations and what measures to be undertaken by the

company so as to makes improvement in the performance level.

Profitability Analysis – It is a tool which helps in measuring the amount of profit as

earned by the company because of its overall business operational efficiency. It analyses

how effectively the Unite Group is working so as to capture market share.

In case of Gross profit ratio, there has been increase in the gross profit because of improved

sales margin from 2017 to 2018 i.e. from 119.3 £m to 128.3 £m. But when it comes to gross

profit ratio, there has been decline from 129.92% to 127.44% this is because of loss which has

incurred on property disposal.

As per the return on Assets which defines that how effectively the Unite group has make use of

its available business assets in making profit (Naseem and et.al., 2019). There has been decrease

from the year 2017 to 2018 i.e. from 9.20% to 8.33%. It depicts that company is not earning

much profit from the investment made as it is having more emphasis on invested capital only and

not on earning profits from sales.

With the help of Return on equity, the Unite group has been making efforts to earn high profit

margins from improving its sales level with the help of shareholders investment. The main

reason behind decrease in the value of return on equity is that the company has shifted its capital

requirement from equity sources to debt financing. As a result there has been increase in debt

level thereby declining in return from 12.94% to 11.45%.

Liquidity Analysis – It defines whether the company is capable enough to makes

payment of its current obligations or which is going to arises in the coming year with the

help of current assets.

As per Quick ratio, current liabilities of Unite Group has decreased from 157.5 £m to 147.4 £m

which defines that company is having sufficient cash as well as quick assets o retire its current

obligations on immediate basis (Pech, Noguera and White, 2015).

In relation to Current ratio and Working capital ratio, the Unite Group is having better

liquidity aspects in the year 2018 as compared to 2017. It is because of increase in the level of

current assets from 138.6 £m to 220.8 £m which states that it is company is capable enough to

make payment of its short term obligation if arises.

Efficiency Analysis – It states that how efficiently the company is making use of its own

available business assets as well as liabilities part i.e. equity section so as to generate high

sales margin.

earned by the company because of its overall business operational efficiency. It analyses

how effectively the Unite Group is working so as to capture market share.

In case of Gross profit ratio, there has been increase in the gross profit because of improved

sales margin from 2017 to 2018 i.e. from 119.3 £m to 128.3 £m. But when it comes to gross

profit ratio, there has been decline from 129.92% to 127.44% this is because of loss which has

incurred on property disposal.

As per the return on Assets which defines that how effectively the Unite group has make use of

its available business assets in making profit (Naseem and et.al., 2019). There has been decrease

from the year 2017 to 2018 i.e. from 9.20% to 8.33%. It depicts that company is not earning

much profit from the investment made as it is having more emphasis on invested capital only and

not on earning profits from sales.

With the help of Return on equity, the Unite group has been making efforts to earn high profit

margins from improving its sales level with the help of shareholders investment. The main

reason behind decrease in the value of return on equity is that the company has shifted its capital

requirement from equity sources to debt financing. As a result there has been increase in debt

level thereby declining in return from 12.94% to 11.45%.

Liquidity Analysis – It defines whether the company is capable enough to makes

payment of its current obligations or which is going to arises in the coming year with the

help of current assets.

As per Quick ratio, current liabilities of Unite Group has decreased from 157.5 £m to 147.4 £m

which defines that company is having sufficient cash as well as quick assets o retire its current

obligations on immediate basis (Pech, Noguera and White, 2015).

In relation to Current ratio and Working capital ratio, the Unite Group is having better

liquidity aspects in the year 2018 as compared to 2017. It is because of increase in the level of

current assets from 138.6 £m to 220.8 £m which states that it is company is capable enough to

make payment of its short term obligation if arises.

Efficiency Analysis – It states that how efficiently the company is making use of its own

available business assets as well as liabilities part i.e. equity section so as to generate high

sales margin.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In case of Inventory Turnover ratio, it helps the Unite Group Plc in defining that how

efficiently it is having control over its inventory as well as merchandise level so as to gain high

sales margin along with increased market share. There has been increase in the value of its

efficiency of converting its inventory into sales as compared to 2017 ratio (Goyal and Bhatia,

2016). This states that the company with its sound and effective business policies and strategies

in respect on marketing, it has been able to increase its customer base.

As per the Asset Turnover, there has been decline from the last year i.e. from 9.81% to 4.86%

which states that the company is not making proper use of its business assets as well as of other

business resource in generating sales. It is because of the reason that the company is either

having some management issues related to the production or manufacturing function of business

or it can be because of out dated or inefficient business processes or techniques being used by the

company for sales.

Days Sales in Inventory defines the times period within which the Unite Group will be able to

completely sell its present inventory or stock. In case of the Unite Group it has been assessed

with the help of ratio, that the company is having enough inventory which will last to 83 days

and will get converted in to cash thereafter. It states that the company is not having strong

marketing techniques as well as plans or low customer demands to move out its stock present in

business premises in form of sales.

Gearing Analysis – It helps stakeholders as well as financial analyst in gaining better

understanding about the overall capital structure format which the company is having

therein. It defines how much the company is relying on debt sources for its financing

purpose along with equity sources.

In case of Debt to equity ratio, the Unite Group is having a ratio of 0.36 in the year 2018 which

is lower than 2017 and is considered as the better part on behalf of both the stakeholders as well

as investors. It helps the lenders as well as investors in protecting their interest even if the

company is having adverse business situation.

In the context of Debt ratio, it defines the total percentage of the total assets which has been

financed with the help of debt sources and the level to which it is considered as suitable as well

as stable for the business (Davis, 2019). The decline in debt ratio from 0.22 in the year 2017 to

0.21 in the year 2018 states that the company is having lower debt ratio and is having more

efficiently it is having control over its inventory as well as merchandise level so as to gain high

sales margin along with increased market share. There has been increase in the value of its

efficiency of converting its inventory into sales as compared to 2017 ratio (Goyal and Bhatia,

2016). This states that the company with its sound and effective business policies and strategies

in respect on marketing, it has been able to increase its customer base.

As per the Asset Turnover, there has been decline from the last year i.e. from 9.81% to 4.86%

which states that the company is not making proper use of its business assets as well as of other

business resource in generating sales. It is because of the reason that the company is either

having some management issues related to the production or manufacturing function of business

or it can be because of out dated or inefficient business processes or techniques being used by the

company for sales.

Days Sales in Inventory defines the times period within which the Unite Group will be able to

completely sell its present inventory or stock. In case of the Unite Group it has been assessed

with the help of ratio, that the company is having enough inventory which will last to 83 days

and will get converted in to cash thereafter. It states that the company is not having strong

marketing techniques as well as plans or low customer demands to move out its stock present in

business premises in form of sales.

Gearing Analysis – It helps stakeholders as well as financial analyst in gaining better

understanding about the overall capital structure format which the company is having

therein. It defines how much the company is relying on debt sources for its financing

purpose along with equity sources.

In case of Debt to equity ratio, the Unite Group is having a ratio of 0.36 in the year 2018 which

is lower than 2017 and is considered as the better part on behalf of both the stakeholders as well

as investors. It helps the lenders as well as investors in protecting their interest even if the

company is having adverse business situation.

In the context of Debt ratio, it defines the total percentage of the total assets which has been

financed with the help of debt sources and the level to which it is considered as suitable as well

as stable for the business (Davis, 2019). The decline in debt ratio from 0.22 in the year 2017 to

0.21 in the year 2018 states that the company is having lower debt ratio and is having more

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

stable and sound business operations having the potential of running in effective manner for long

run time frame.

As per the concept of Equity ratio, it has been evaluated that the company is having a total asset

of 2849.5 £m which has increased as compared to the last year time period. There has been

increase in the ratio which depicts that the Unite Group Plc is having its more stake in equity

sources as it is much cheaper than debt financing source. It is because of the factor that with the

debt financing option, the company is required to make payment of interest to its investors every

year which is considered as an expenses for the company and thus declines its profitability

aspects for that year.

c. Evaluating changes related to Lease Accounting rules

The term Lease Accounting is considered as one of the most important part of accounting

section as it wholly differs which its emphasis on the end user. Lease is defined as an

arrangement as per which the lessor agrees and allow the lessee to have control as well as right

of using identified property, plant as well as equipment for a definite time period in lieu of

payments of either one or more instalment (Sacarin, 2017). Every business organisation requires

assets for conducting business operations in effective as well as efficient manner which can

either be acquired or taken on lease option.

run time frame.

As per the concept of Equity ratio, it has been evaluated that the company is having a total asset

of 2849.5 £m which has increased as compared to the last year time period. There has been

increase in the ratio which depicts that the Unite Group Plc is having its more stake in equity

sources as it is much cheaper than debt financing source. It is because of the factor that with the

debt financing option, the company is required to make payment of interest to its investors every

year which is considered as an expenses for the company and thus declines its profitability

aspects for that year.

c. Evaluating changes related to Lease Accounting rules

The term Lease Accounting is considered as one of the most important part of accounting

section as it wholly differs which its emphasis on the end user. Lease is defined as an

arrangement as per which the lessor agrees and allow the lessee to have control as well as right

of using identified property, plant as well as equipment for a definite time period in lieu of

payments of either one or more instalment (Sacarin, 2017). Every business organisation requires

assets for conducting business operations in effective as well as efficient manner which can

either be acquired or taken on lease option.

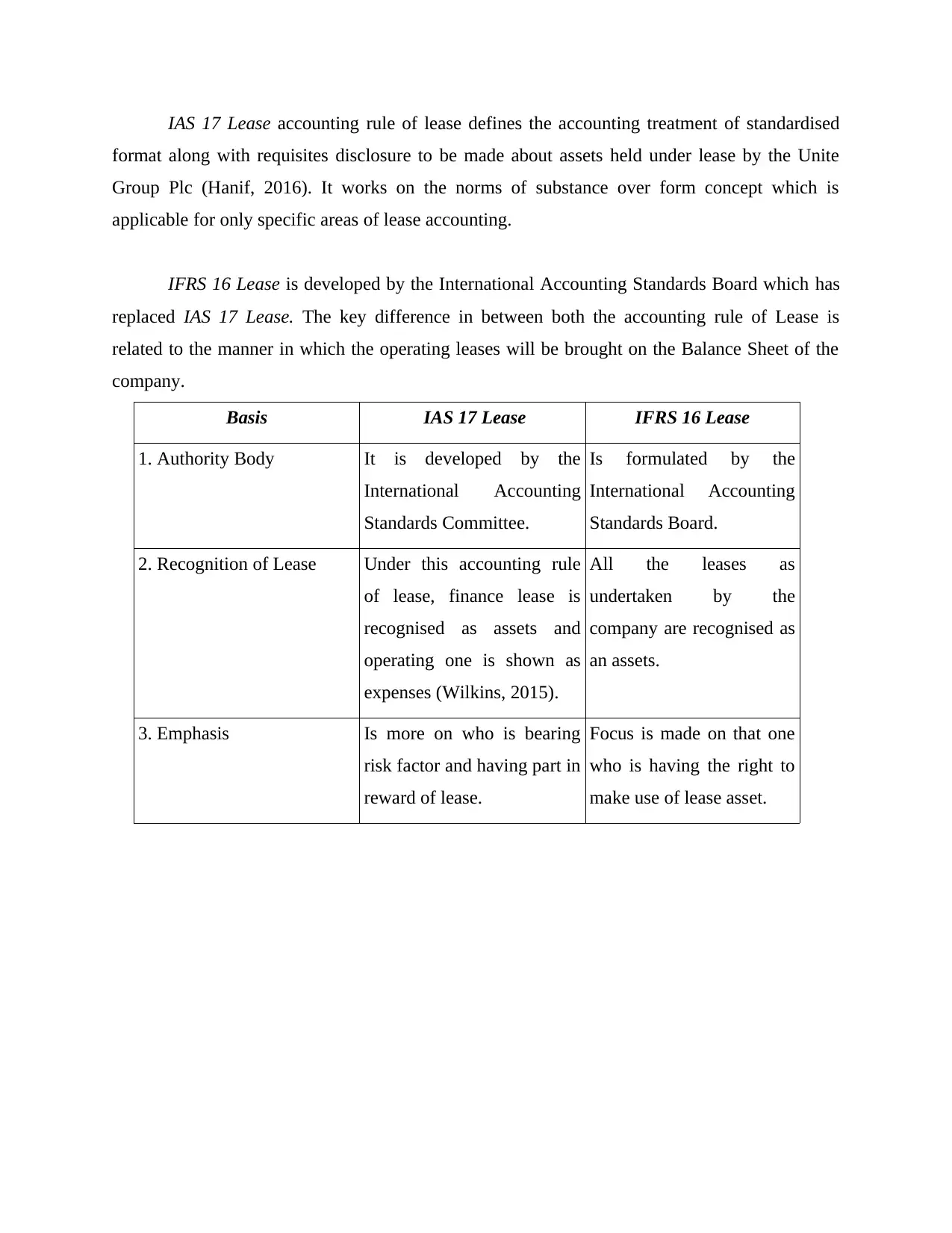

IAS 17 Lease accounting rule of lease defines the accounting treatment of standardised

format along with requisites disclosure to be made about assets held under lease by the Unite

Group Plc (Hanif, 2016). It works on the norms of substance over form concept which is

applicable for only specific areas of lease accounting.

IFRS 16 Lease is developed by the International Accounting Standards Board which has

replaced IAS 17 Lease. The key difference in between both the accounting rule of Lease is

related to the manner in which the operating leases will be brought on the Balance Sheet of the

company.

Basis IAS 17 Lease IFRS 16 Lease

1. Authority Body It is developed by the

International Accounting

Standards Committee.

Is formulated by the

International Accounting

Standards Board.

2. Recognition of Lease Under this accounting rule

of lease, finance lease is

recognised as assets and

operating one is shown as

expenses (Wilkins, 2015).

All the leases as

undertaken by the

company are recognised as

an assets.

3. Emphasis Is more on who is bearing

risk factor and having part in

reward of lease.

Focus is made on that one

who is having the right to

make use of lease asset.

format along with requisites disclosure to be made about assets held under lease by the Unite

Group Plc (Hanif, 2016). It works on the norms of substance over form concept which is

applicable for only specific areas of lease accounting.

IFRS 16 Lease is developed by the International Accounting Standards Board which has

replaced IAS 17 Lease. The key difference in between both the accounting rule of Lease is

related to the manner in which the operating leases will be brought on the Balance Sheet of the

company.

Basis IAS 17 Lease IFRS 16 Lease

1. Authority Body It is developed by the

International Accounting

Standards Committee.

Is formulated by the

International Accounting

Standards Board.

2. Recognition of Lease Under this accounting rule

of lease, finance lease is

recognised as assets and

operating one is shown as

expenses (Wilkins, 2015).

All the leases as

undertaken by the

company are recognised as

an assets.

3. Emphasis Is more on who is bearing

risk factor and having part in

reward of lease.

Focus is made on that one

who is having the right to

make use of lease asset.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.