Superannuation Fund Accounting

VerifiedAdded on 2020/05/11

|12

|2055

|46

AI Summary

This assignment tasks students with analyzing the financial statements of a superannuation fund. The analysis involves examining various components like service cost, contributions received, benefits paid, return on plan assets, actuarial losses, and journal entries to reconcile balance sheet items. It requires an understanding of accounting principles applied to superannuation funds.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL REPORTING 1

Financial Reporting

Name:

Institution:

Date:

Financial Reporting

Name:

Institution:

Date:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL REPORTING 2

Question 1

The highest and best use principle

This is a principle used by the valuation experts in finding the possible and probably the best

use in which a property particularly land can yield the maximum reward if put into best use.

It is based on the principle of maximum gain from a real estate. This is presumably so if the

current use of land does not yield maximum output therefore not relevant to the best use and

highest principle. It is usually established by conducting a site analysis for the property where

the following factors are then considered by the valuer; first is the physical possibility and

whether the land is legally allowable. Then the valuer will ascertain whether the use will be

financially feasible and profitability levels that would accrue also known as the maximum

utility level (Harrington, Nunes & Roland, 2010).

In this report, Anne Lockwood is discouraging valuation at fair value as it has too much

judgment required to make a decision. There is a lot of time used and consumed in

determining the fair value where the global economic volatility always causes the fair value

to vary. The financial auditor suggest that it is wise to use the market value in valuation of a

property due to a lot of inconsistencies in the way different businesses use the fair value to

give account in Plant, Property and Equipment valuation.

AASB 13 gives clear directions to accountants on how to prepare financials using the market

value and not fair value due to changes in valuations. The highest and best use principle is

always considered in determining the value of a property but also possess a lot of problems

for nonprofit making organizations (Hitchner, Hyden & Mard, 2013).

The example given is that the age care home will be knocked down and the owner of the

building will build flats on the same piece of land. In this case, considering that the age care

Question 1

The highest and best use principle

This is a principle used by the valuation experts in finding the possible and probably the best

use in which a property particularly land can yield the maximum reward if put into best use.

It is based on the principle of maximum gain from a real estate. This is presumably so if the

current use of land does not yield maximum output therefore not relevant to the best use and

highest principle. It is usually established by conducting a site analysis for the property where

the following factors are then considered by the valuer; first is the physical possibility and

whether the land is legally allowable. Then the valuer will ascertain whether the use will be

financially feasible and profitability levels that would accrue also known as the maximum

utility level (Harrington, Nunes & Roland, 2010).

In this report, Anne Lockwood is discouraging valuation at fair value as it has too much

judgment required to make a decision. There is a lot of time used and consumed in

determining the fair value where the global economic volatility always causes the fair value

to vary. The financial auditor suggest that it is wise to use the market value in valuation of a

property due to a lot of inconsistencies in the way different businesses use the fair value to

give account in Plant, Property and Equipment valuation.

AASB 13 gives clear directions to accountants on how to prepare financials using the market

value and not fair value due to changes in valuations. The highest and best use principle is

always considered in determining the value of a property but also possess a lot of problems

for nonprofit making organizations (Hitchner, Hyden & Mard, 2013).

The example given is that the age care home will be knocked down and the owner of the

building will build flats on the same piece of land. In this case, considering that the age care

FINANCIAL REPORTING 3

home was not for profit organization, it wasn’t expected to realize profits. However, building

of the block of flats will ensure that the land is put into maximum use and not used for

altruistic purposes. Furthermore, the real challenge is determining the value of the asset as

there is no intention shown by the owners to get the value of the land. The value given of

$10 million is not the market value and factors such as inflation of the assets makes the

valuation even more complex and requires the judgment call for use of fair value in asset

determination (Hyman, n.d.).

Question 2

Determine how Last Ltd should account for the results of the impairment tests at both 31

December 2016 and 31 December 2017.

Relevant Issues:

IAS 36 brings into limelight the concept of cash generating units (CGU). Cash generating

units are also called cash impairment units (Reeve, 2012)

Impairment Test for year ended 31/12/16

a. Calculations:

Impairment loss= Carrying amount CA- Recoverable amount RA

At Time= 1500 – 1044

= $ 456

Impairment loss at Leisure= CA – RA

home was not for profit organization, it wasn’t expected to realize profits. However, building

of the block of flats will ensure that the land is put into maximum use and not used for

altruistic purposes. Furthermore, the real challenge is determining the value of the asset as

there is no intention shown by the owners to get the value of the land. The value given of

$10 million is not the market value and factors such as inflation of the assets makes the

valuation even more complex and requires the judgment call for use of fair value in asset

determination (Hyman, n.d.).

Question 2

Determine how Last Ltd should account for the results of the impairment tests at both 31

December 2016 and 31 December 2017.

Relevant Issues:

IAS 36 brings into limelight the concept of cash generating units (CGU). Cash generating

units are also called cash impairment units (Reeve, 2012)

Impairment Test for year ended 31/12/16

a. Calculations:

Impairment loss= Carrying amount CA- Recoverable amount RA

At Time= 1500 – 1044

= $ 456

Impairment loss at Leisure= CA – RA

FINANCIAL REPORTING 4

= 1200-990

= $ 210

Since it is impairment at Cost model impairment loss is recognized as following in the ledger

journals entries

DR; PL impairment loss CR; Asset allowance account

b. General Journal Entries 31/12/16:

Date Account DR CR

31/12/2016 Profit and loss account - Time 456

31/12/2016 Asset allowance account 456

31/12/2016 P&L - Leisure 210

31/12/2016 Asset allowance account 210

2. Impairment Test 31/12/17

a. Calculations

This is a revaluation model/ Revaluation surplus

Impairment loss= Carrying amount CA- Recoverable amount RA

At Time= 1322 – 1502

= $ (180)

Impairment loss at leisure= CA – RA

= 1200-990

= $ 210

Since it is impairment at Cost model impairment loss is recognized as following in the ledger

journals entries

DR; PL impairment loss CR; Asset allowance account

b. General Journal Entries 31/12/16:

Date Account DR CR

31/12/2016 Profit and loss account - Time 456

31/12/2016 Asset allowance account 456

31/12/2016 P&L - Leisure 210

31/12/2016 Asset allowance account 210

2. Impairment Test 31/12/17

a. Calculations

This is a revaluation model/ Revaluation surplus

Impairment loss= Carrying amount CA- Recoverable amount RA

At Time= 1322 – 1502

= $ (180)

Impairment loss at leisure= CA – RA

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL REPORTING 5

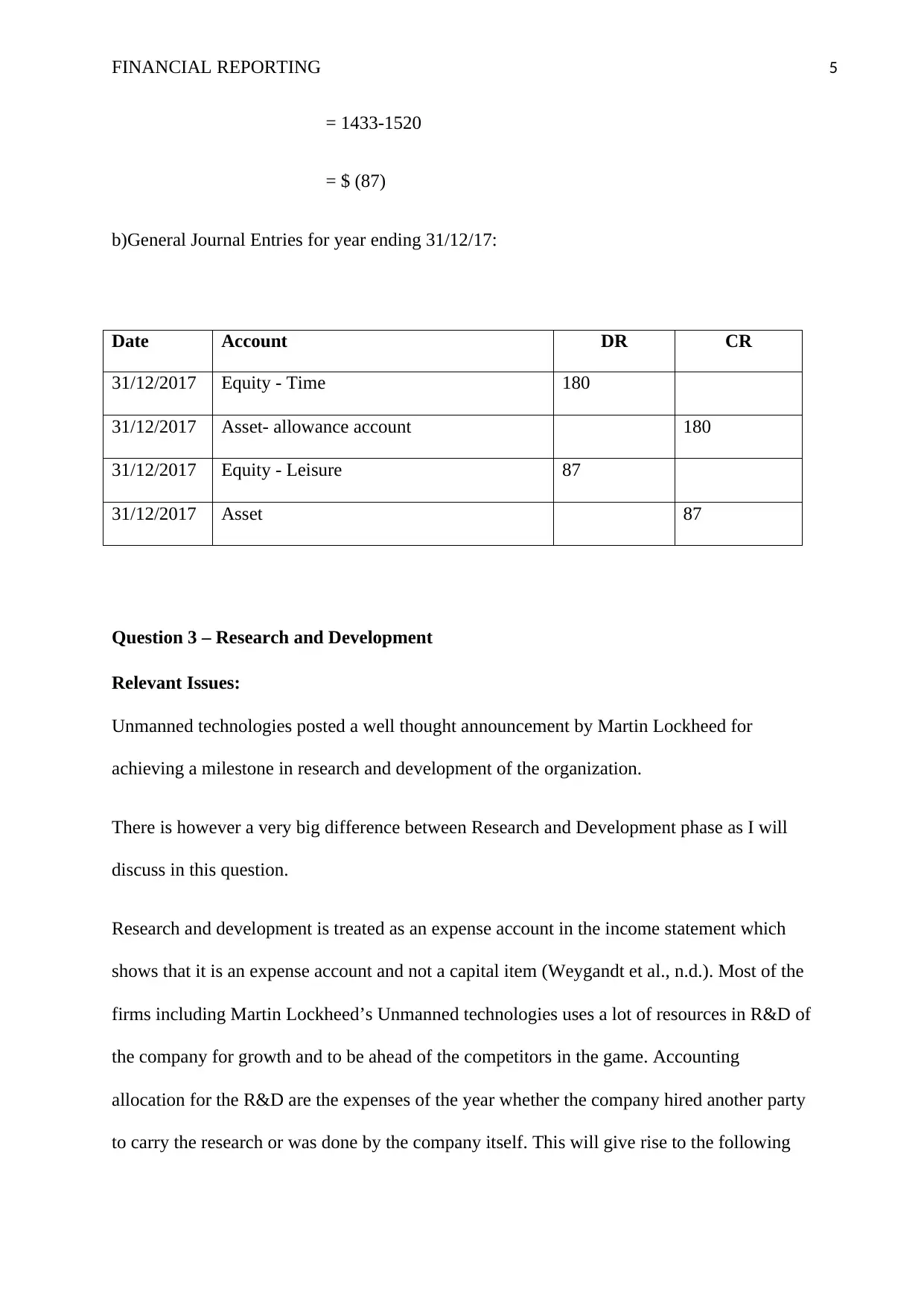

= 1433-1520

= $ (87)

b)General Journal Entries for year ending 31/12/17:

Date Account DR CR

31/12/2017 Equity - Time 180

31/12/2017 Asset- allowance account 180

31/12/2017 Equity - Leisure 87

31/12/2017 Asset 87

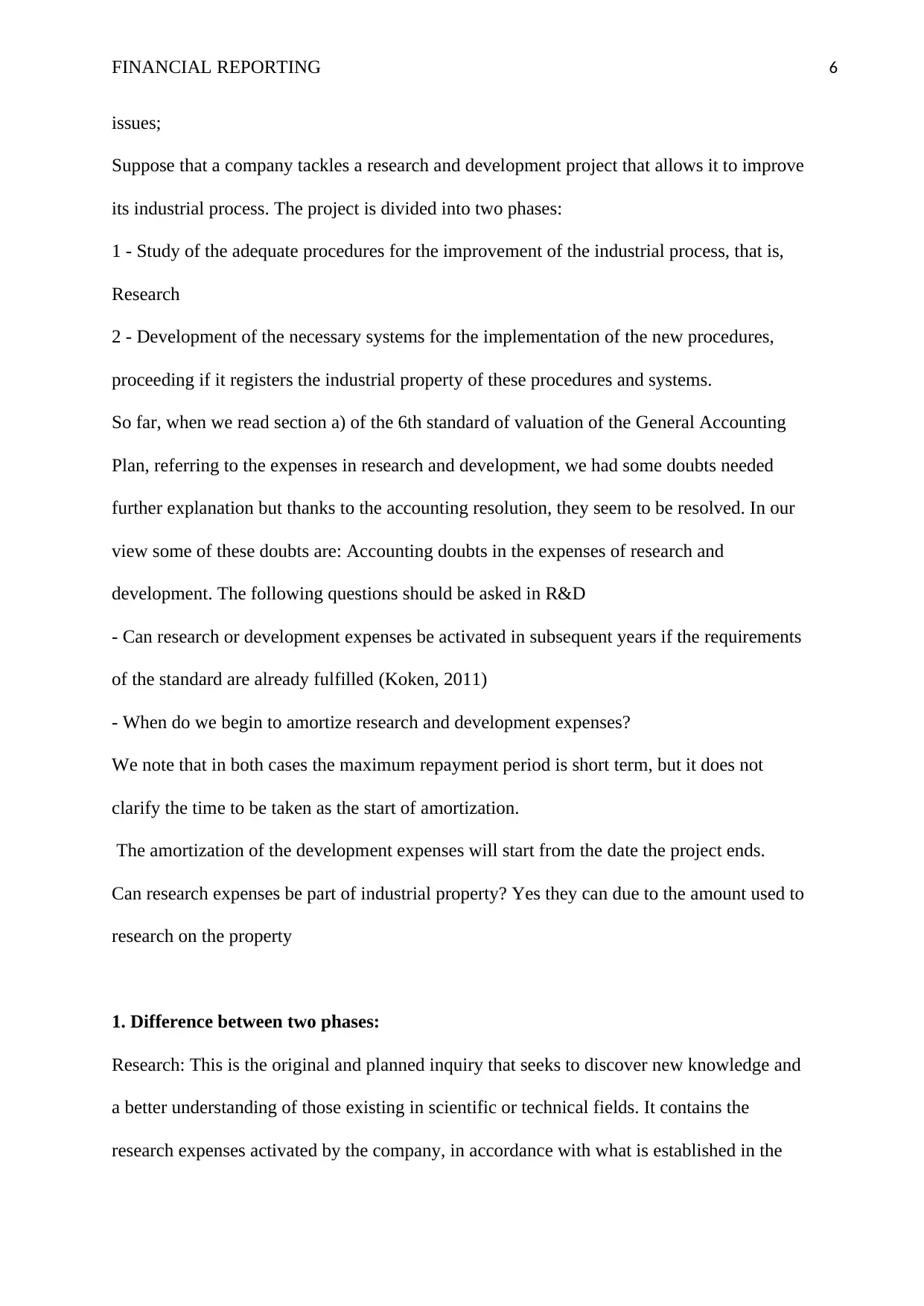

Question 3 – Research and Development

Relevant Issues:

Unmanned technologies posted a well thought announcement by Martin Lockheed for

achieving a milestone in research and development of the organization.

There is however a very big difference between Research and Development phase as I will

discuss in this question.

Research and development is treated as an expense account in the income statement which

shows that it is an expense account and not a capital item (Weygandt et al., n.d.). Most of the

firms including Martin Lockheed’s Unmanned technologies uses a lot of resources in R&D of

the company for growth and to be ahead of the competitors in the game. Accounting

allocation for the R&D are the expenses of the year whether the company hired another party

to carry the research or was done by the company itself. This will give rise to the following

= 1433-1520

= $ (87)

b)General Journal Entries for year ending 31/12/17:

Date Account DR CR

31/12/2017 Equity - Time 180

31/12/2017 Asset- allowance account 180

31/12/2017 Equity - Leisure 87

31/12/2017 Asset 87

Question 3 – Research and Development

Relevant Issues:

Unmanned technologies posted a well thought announcement by Martin Lockheed for

achieving a milestone in research and development of the organization.

There is however a very big difference between Research and Development phase as I will

discuss in this question.

Research and development is treated as an expense account in the income statement which

shows that it is an expense account and not a capital item (Weygandt et al., n.d.). Most of the

firms including Martin Lockheed’s Unmanned technologies uses a lot of resources in R&D of

the company for growth and to be ahead of the competitors in the game. Accounting

allocation for the R&D are the expenses of the year whether the company hired another party

to carry the research or was done by the company itself. This will give rise to the following

FINANCIAL REPORTING 6

issues;

Suppose that a company tackles a research and development project that allows it to improve

its industrial process. The project is divided into two phases:

1 - Study of the adequate procedures for the improvement of the industrial process, that is,

Research

2 - Development of the necessary systems for the implementation of the new procedures,

proceeding if it registers the industrial property of these procedures and systems.

So far, when we read section a) of the 6th standard of valuation of the General Accounting

Plan, referring to the expenses in research and development, we had some doubts needed

further explanation but thanks to the accounting resolution, they seem to be resolved. In our

view some of these doubts are: Accounting doubts in the expenses of research and

development. The following questions should be asked in R&D

- Can research or development expenses be activated in subsequent years if the requirements

of the standard are already fulfilled (Koken, 2011)

- When do we begin to amortize research and development expenses?

We note that in both cases the maximum repayment period is short term, but it does not

clarify the time to be taken as the start of amortization.

The amortization of the development expenses will start from the date the project ends.

Can research expenses be part of industrial property? Yes they can due to the amount used to

research on the property

1. Difference between two phases:

Research: This is the original and planned inquiry that seeks to discover new knowledge and

a better understanding of those existing in scientific or technical fields. It contains the

research expenses activated by the company, in accordance with what is established in the

issues;

Suppose that a company tackles a research and development project that allows it to improve

its industrial process. The project is divided into two phases:

1 - Study of the adequate procedures for the improvement of the industrial process, that is,

Research

2 - Development of the necessary systems for the implementation of the new procedures,

proceeding if it registers the industrial property of these procedures and systems.

So far, when we read section a) of the 6th standard of valuation of the General Accounting

Plan, referring to the expenses in research and development, we had some doubts needed

further explanation but thanks to the accounting resolution, they seem to be resolved. In our

view some of these doubts are: Accounting doubts in the expenses of research and

development. The following questions should be asked in R&D

- Can research or development expenses be activated in subsequent years if the requirements

of the standard are already fulfilled (Koken, 2011)

- When do we begin to amortize research and development expenses?

We note that in both cases the maximum repayment period is short term, but it does not

clarify the time to be taken as the start of amortization.

The amortization of the development expenses will start from the date the project ends.

Can research expenses be part of industrial property? Yes they can due to the amount used to

research on the property

1. Difference between two phases:

Research: This is the original and planned inquiry that seeks to discover new knowledge and

a better understanding of those existing in scientific or technical fields. It contains the

research expenses activated by the company, in accordance with what is established in the

FINANCIAL REPORTING 7

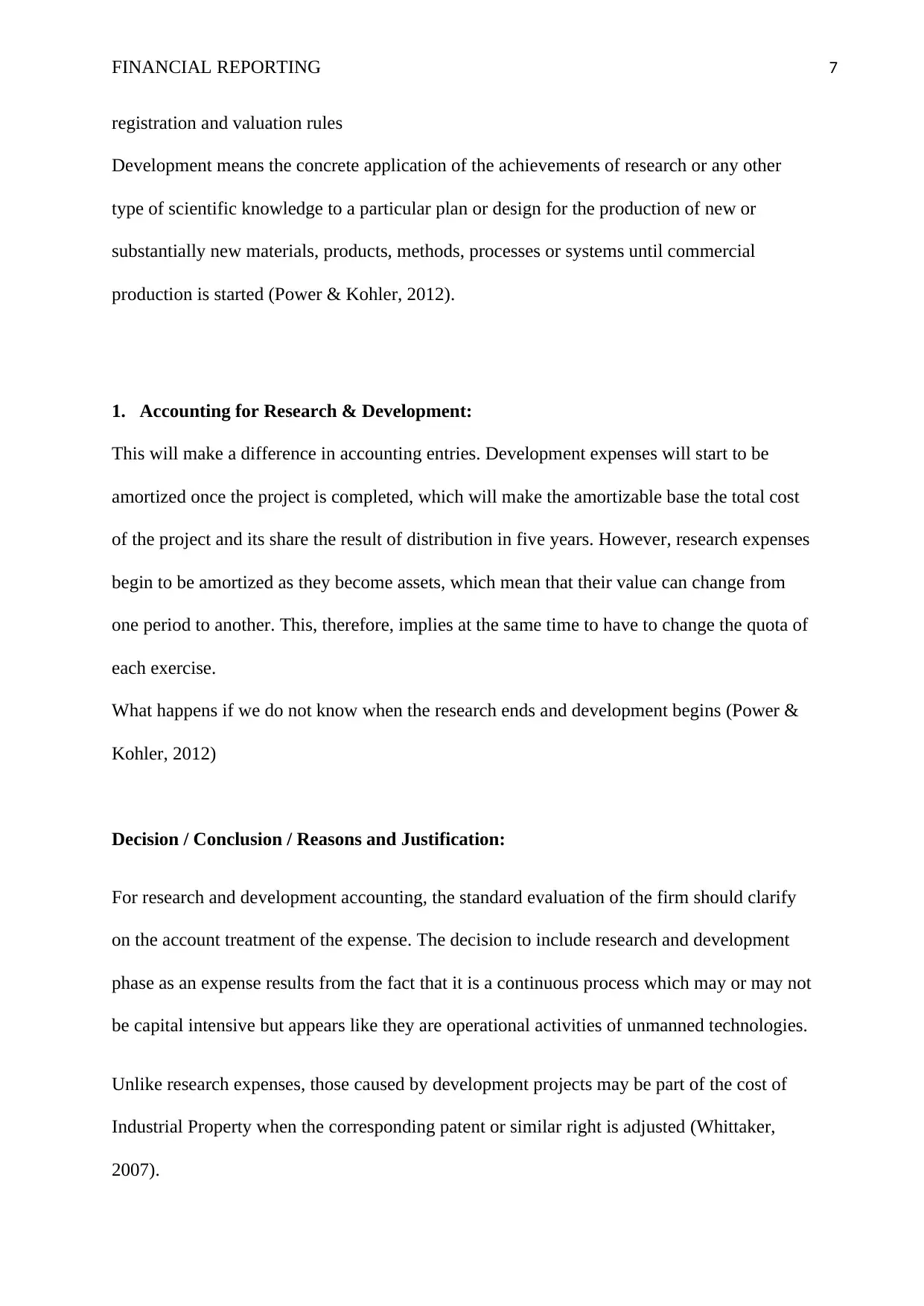

registration and valuation rules

Development means the concrete application of the achievements of research or any other

type of scientific knowledge to a particular plan or design for the production of new or

substantially new materials, products, methods, processes or systems until commercial

production is started (Power & Kohler, 2012).

1. Accounting for Research & Development:

This will make a difference in accounting entries. Development expenses will start to be

amortized once the project is completed, which will make the amortizable base the total cost

of the project and its share the result of distribution in five years. However, research expenses

begin to be amortized as they become assets, which mean that their value can change from

one period to another. This, therefore, implies at the same time to have to change the quota of

each exercise.

What happens if we do not know when the research ends and development begins (Power &

Kohler, 2012)

Decision / Conclusion / Reasons and Justification:

For research and development accounting, the standard evaluation of the firm should clarify

on the account treatment of the expense. The decision to include research and development

phase as an expense results from the fact that it is a continuous process which may or may not

be capital intensive but appears like they are operational activities of unmanned technologies.

Unlike research expenses, those caused by development projects may be part of the cost of

Industrial Property when the corresponding patent or similar right is adjusted (Whittaker,

2007).

registration and valuation rules

Development means the concrete application of the achievements of research or any other

type of scientific knowledge to a particular plan or design for the production of new or

substantially new materials, products, methods, processes or systems until commercial

production is started (Power & Kohler, 2012).

1. Accounting for Research & Development:

This will make a difference in accounting entries. Development expenses will start to be

amortized once the project is completed, which will make the amortizable base the total cost

of the project and its share the result of distribution in five years. However, research expenses

begin to be amortized as they become assets, which mean that their value can change from

one period to another. This, therefore, implies at the same time to have to change the quota of

each exercise.

What happens if we do not know when the research ends and development begins (Power &

Kohler, 2012)

Decision / Conclusion / Reasons and Justification:

For research and development accounting, the standard evaluation of the firm should clarify

on the account treatment of the expense. The decision to include research and development

phase as an expense results from the fact that it is a continuous process which may or may not

be capital intensive but appears like they are operational activities of unmanned technologies.

Unlike research expenses, those caused by development projects may be part of the cost of

Industrial Property when the corresponding patent or similar right is adjusted (Whittaker,

2007).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL REPORTING 8

Under the Plan's standard, we know the requirements that must be given in order to activate

certain expenses and consider them as intangible assets therefore the expenses can be

activated in subsequent years. However, expenses that fall under the research and

development can de activated or deactivated in later stages depending on the policy of the

firm (Whittaker, 2007).

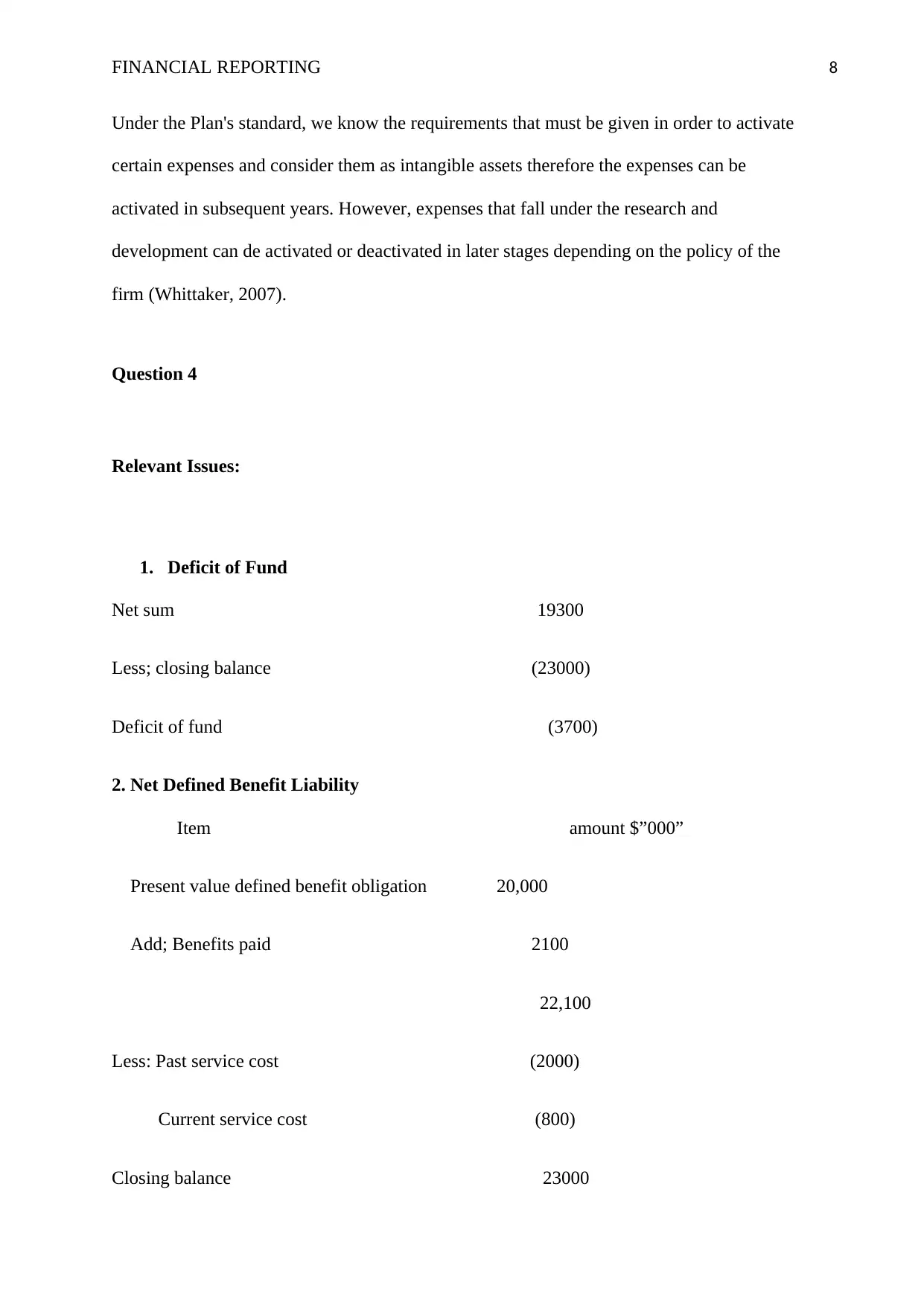

Question 4

Relevant Issues:

1. Deficit of Fund

Net sum 19300

Less; closing balance (23000)

Deficit of fund (3700)

2. Net Defined Benefit Liability

Item amount $”000”

Present value defined benefit obligation 20,000

Add; Benefits paid 2100

22,100

Less: Past service cost (2000)

Current service cost (800)

Closing balance 23000

Under the Plan's standard, we know the requirements that must be given in order to activate

certain expenses and consider them as intangible assets therefore the expenses can be

activated in subsequent years. However, expenses that fall under the research and

development can de activated or deactivated in later stages depending on the policy of the

firm (Whittaker, 2007).

Question 4

Relevant Issues:

1. Deficit of Fund

Net sum 19300

Less; closing balance (23000)

Deficit of fund (3700)

2. Net Defined Benefit Liability

Item amount $”000”

Present value defined benefit obligation 20,000

Add; Benefits paid 2100

22,100

Less: Past service cost (2000)

Current service cost (800)

Closing balance 23000

FINANCIAL REPORTING 9

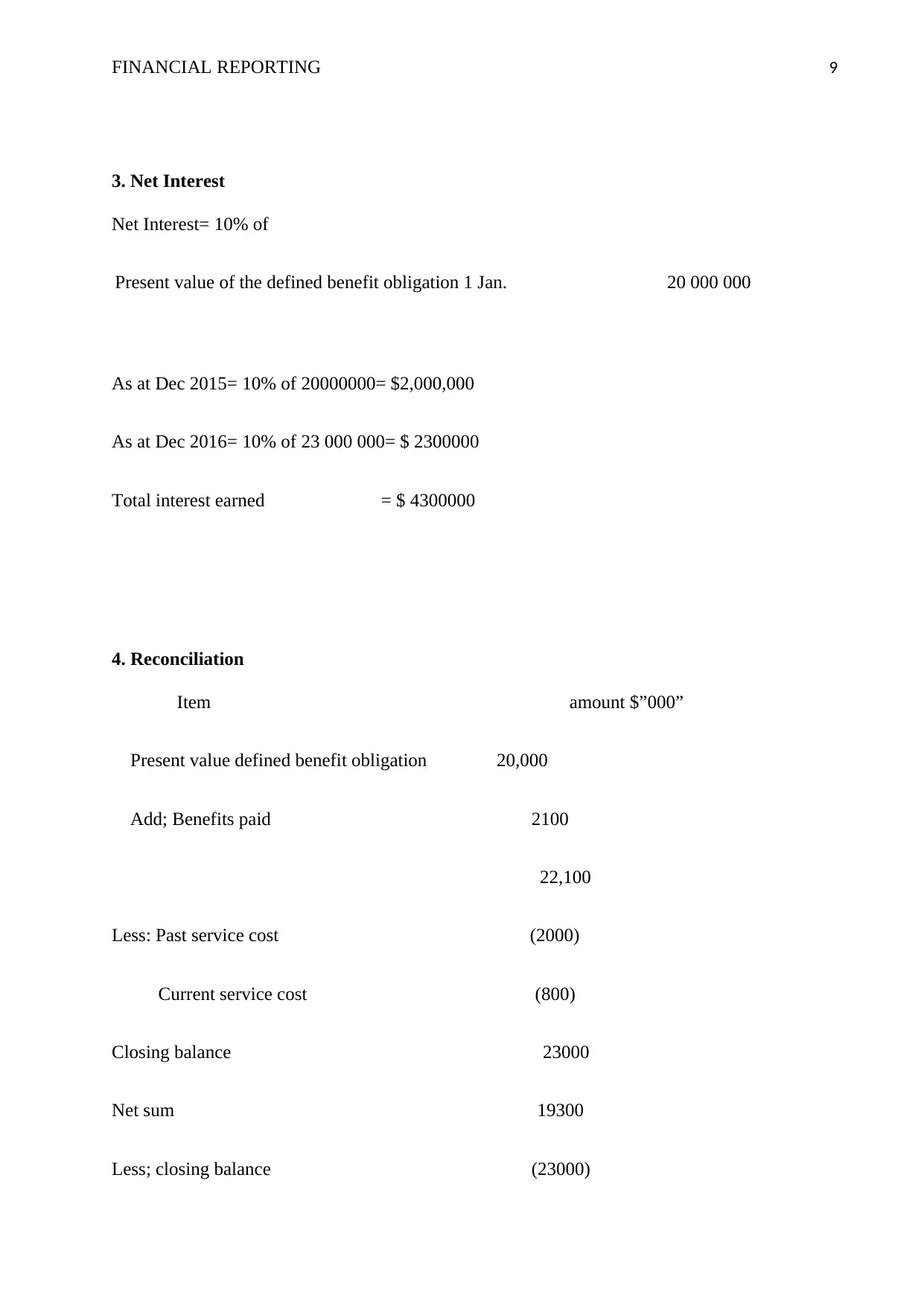

3. Net Interest

Net Interest= 10% of

Present value of the defined benefit obligation 1 Jan. 20 000 000

As at Dec 2015= 10% of 20000000= $2,000,000

As at Dec 2016= 10% of 23 000 000= $ 2300000

Total interest earned = $ 4300000

4. Reconciliation

Item amount $”000”

Present value defined benefit obligation 20,000

Add; Benefits paid 2100

22,100

Less: Past service cost (2000)

Current service cost (800)

Closing balance 23000

Net sum 19300

Less; closing balance (23000)

3. Net Interest

Net Interest= 10% of

Present value of the defined benefit obligation 1 Jan. 20 000 000

As at Dec 2015= 10% of 20000000= $2,000,000

As at Dec 2016= 10% of 23 000 000= $ 2300000

Total interest earned = $ 4300000

4. Reconciliation

Item amount $”000”

Present value defined benefit obligation 20,000

Add; Benefits paid 2100

22,100

Less: Past service cost (2000)

Current service cost (800)

Closing balance 23000

Net sum 19300

Less; closing balance (23000)

FINANCIAL REPORTING 10

Deficit of fund (3700)

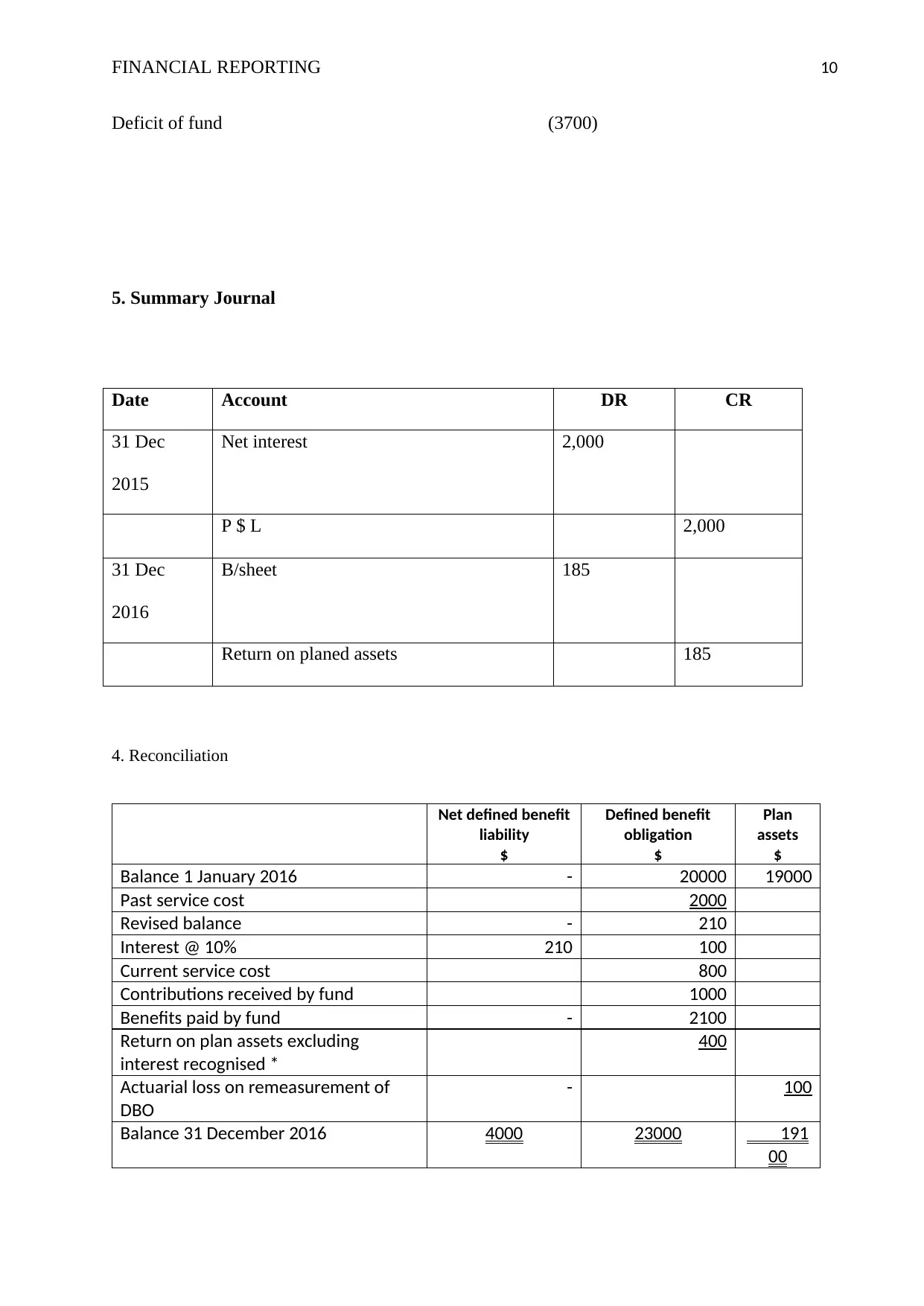

5. Summary Journal

Date Account DR CR

31 Dec

2015

Net interest 2,000

P $ L 2,000

31 Dec

2016

B/sheet 185

Return on planed assets 185

4. Reconciliation

Net defined benefit

liability

$

Defined benefit

obligation

$

Plan

assets

$

Balance 1 January 2016 - 20000 19000

Past service cost 2000

Revised balance - 210

Interest @ 10% 210 100

Current service cost 800

Contributions received by fund 1000

Benefits paid by fund - 2100

Return on plan assets excluding

interest recognised *

400

Actuarial loss on remeasurement of

DBO

- 100

Balance 31 December 2016 4000 23000 191

00

Deficit of fund (3700)

5. Summary Journal

Date Account DR CR

31 Dec

2015

Net interest 2,000

P $ L 2,000

31 Dec

2016

B/sheet 185

Return on planed assets 185

4. Reconciliation

Net defined benefit

liability

$

Defined benefit

obligation

$

Plan

assets

$

Balance 1 January 2016 - 20000 19000

Past service cost 2000

Revised balance - 210

Interest @ 10% 210 100

Current service cost 800

Contributions received by fund 1000

Benefits paid by fund - 2100

Return on plan assets excluding

interest recognised *

400

Actuarial loss on remeasurement of

DBO

- 100

Balance 31 December 2016 4000 23000 191

00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL REPORTING 11

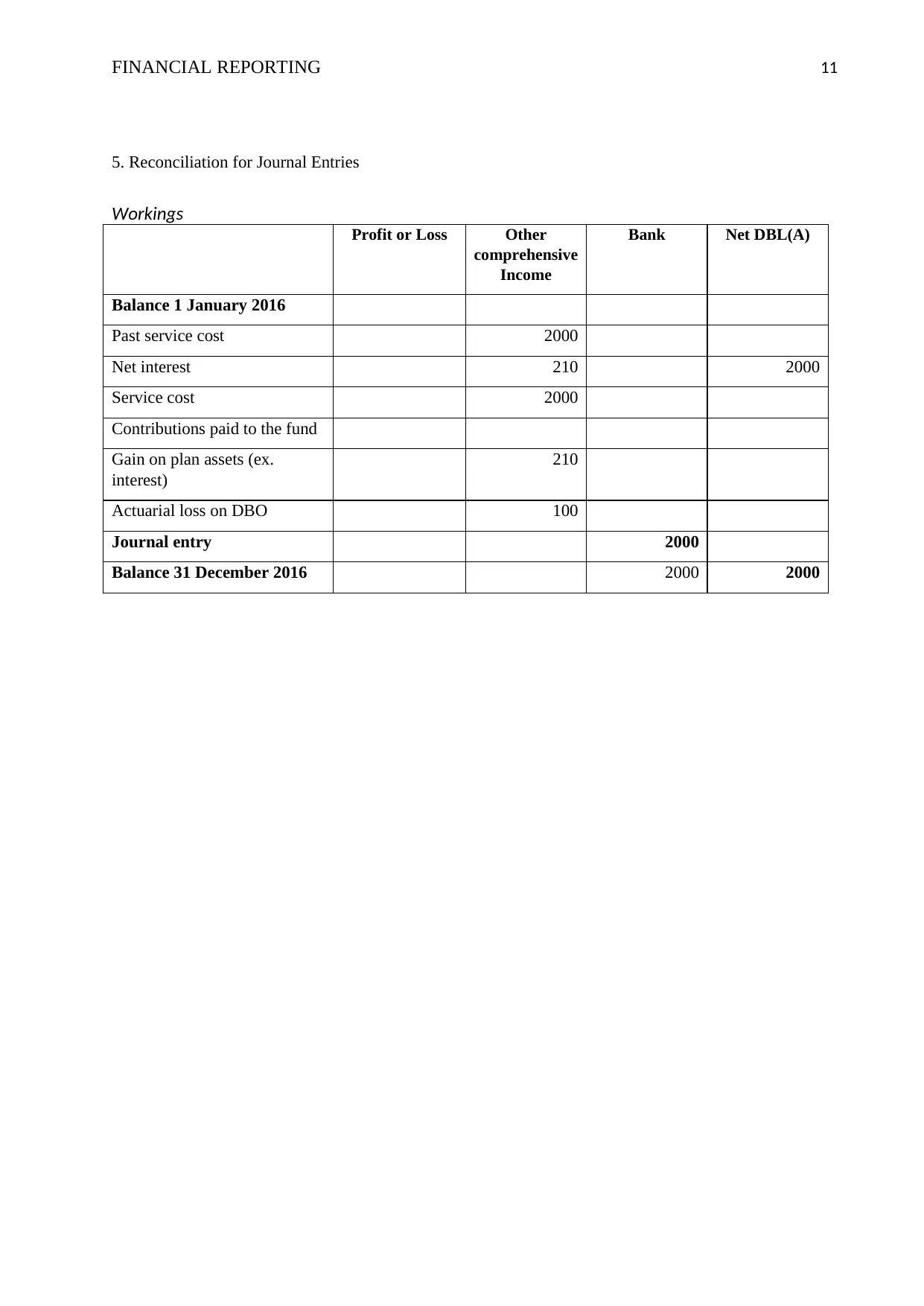

5. Reconciliation for Journal Entries

Workings

Profit or Loss Other

comprehensive

Income

Bank Net DBL(A)

Balance 1 January 2016

Past service cost 2000

Net interest 210 2000

Service cost 2000

Contributions paid to the fund

Gain on plan assets (ex.

interest)

210

Actuarial loss on DBO 100

Journal entry 2000

Balance 31 December 2016 2000 2000

5. Reconciliation for Journal Entries

Workings

Profit or Loss Other

comprehensive

Income

Bank Net DBL(A)

Balance 1 January 2016

Past service cost 2000

Net interest 210 2000

Service cost 2000

Contributions paid to the fund

Gain on plan assets (ex.

interest)

210

Actuarial loss on DBO 100

Journal entry 2000

Balance 31 December 2016 2000 2000

FINANCIAL REPORTING 12

References

Harrington, J., Nunes, C., & Roland, G. (2010). 2010 goodwill impairment study.

[Morristown, N.J.]: Financial Executives Research Foundation.

Hitchner, J., Hyden, S., & Mard, M. (2013). Valuation for financial reporting. Hoboken, N.J.:

Wiley.

Hyman, M. Guides sixth impairment training workbook.

Koken, E. (2011). The Superannuation Handbook 2008-09. Wrightbooks.

Power, T., & Kohler, A. (2012). Superannuation For Dummies. Hoboken: John Wiley &

Sons.

Racine, S. (2010). Accounting principles. Charleston, SC: BiblioLife.

Reeve, F. (2012). Accounting principles. [Place of publication not identified]: Nabu Press.

Weygandt, J., Kieso, D., Kimmel, P., Trenholm, B., Warren, V., & Novak, L. Accounting

principles.

References

Harrington, J., Nunes, C., & Roland, G. (2010). 2010 goodwill impairment study.

[Morristown, N.J.]: Financial Executives Research Foundation.

Hitchner, J., Hyden, S., & Mard, M. (2013). Valuation for financial reporting. Hoboken, N.J.:

Wiley.

Hyman, M. Guides sixth impairment training workbook.

Koken, E. (2011). The Superannuation Handbook 2008-09. Wrightbooks.

Power, T., & Kohler, A. (2012). Superannuation For Dummies. Hoboken: John Wiley &

Sons.

Racine, S. (2010). Accounting principles. Charleston, SC: BiblioLife.

Reeve, F. (2012). Accounting principles. [Place of publication not identified]: Nabu Press.

Weygandt, J., Kieso, D., Kimmel, P., Trenholm, B., Warren, V., & Novak, L. Accounting

principles.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.