Financial Reporting: Contingencies, Provisions, Leased Items, Non-current Assets

VerifiedAdded on 2023/06/12

|12

|1959

|345

AI Summary

This report analyzes the financial reporting of Fairfax Limited, covering contingencies, provisions, leased items, and non-current assets. It evaluates adherence to accounting standards and provides recommendations for valuation methods.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL REPORTING

Financial reporting

Name of the Student:

Name of the University:

Author Note

Financial reporting

Name of the Student:

Name of the University:

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCIAL REPORTING

Table of Contents

Introduction:....................................................................................................................................2

1. discussion on Contingencies and Provisions reported by organization:......................................2

2. Recognition Criteria and Measurement issues associated with provision or contingent liability

.........................................................................................................................................................3

3. Disclosure of specific Contingency recorded by company:........................................................3

4. Details of disclosure of leased items recorded by company:.......................................................3

5. Presentation and classification of leased items and explanation of Treatment of leases:............4

6. Hypothetical situation depicting reclassification of leased items:...............................................5

7. Disclosure of Non-current asset – impairment method..............................................................6

8. Valuation Method for Non Current Assets with reference to quantitative characteristics:.........6

Conclusion:......................................................................................................................................6

References list:.................................................................................................................................6

Table of Contents

Introduction:....................................................................................................................................2

1. discussion on Contingencies and Provisions reported by organization:......................................2

2. Recognition Criteria and Measurement issues associated with provision or contingent liability

.........................................................................................................................................................3

3. Disclosure of specific Contingency recorded by company:........................................................3

4. Details of disclosure of leased items recorded by company:.......................................................3

5. Presentation and classification of leased items and explanation of Treatment of leases:............4

6. Hypothetical situation depicting reclassification of leased items:...............................................5

7. Disclosure of Non-current asset – impairment method..............................................................6

8. Valuation Method for Non Current Assets with reference to quantitative characteristics:.........6

Conclusion:......................................................................................................................................6

References list:.................................................................................................................................6

2FINANCIAL REPORTING

Introduction:

The report is prepared for addressing the accounting statements elements of Fairfax

limited by reviewing its annual report. It intends to evaluate whether the financial statement are

prepared in adherence to the accounting standards recommended by Australian accounting

standard board. Analysis of accounts is done by extracting the data from annual reports of the

financial year 2017.

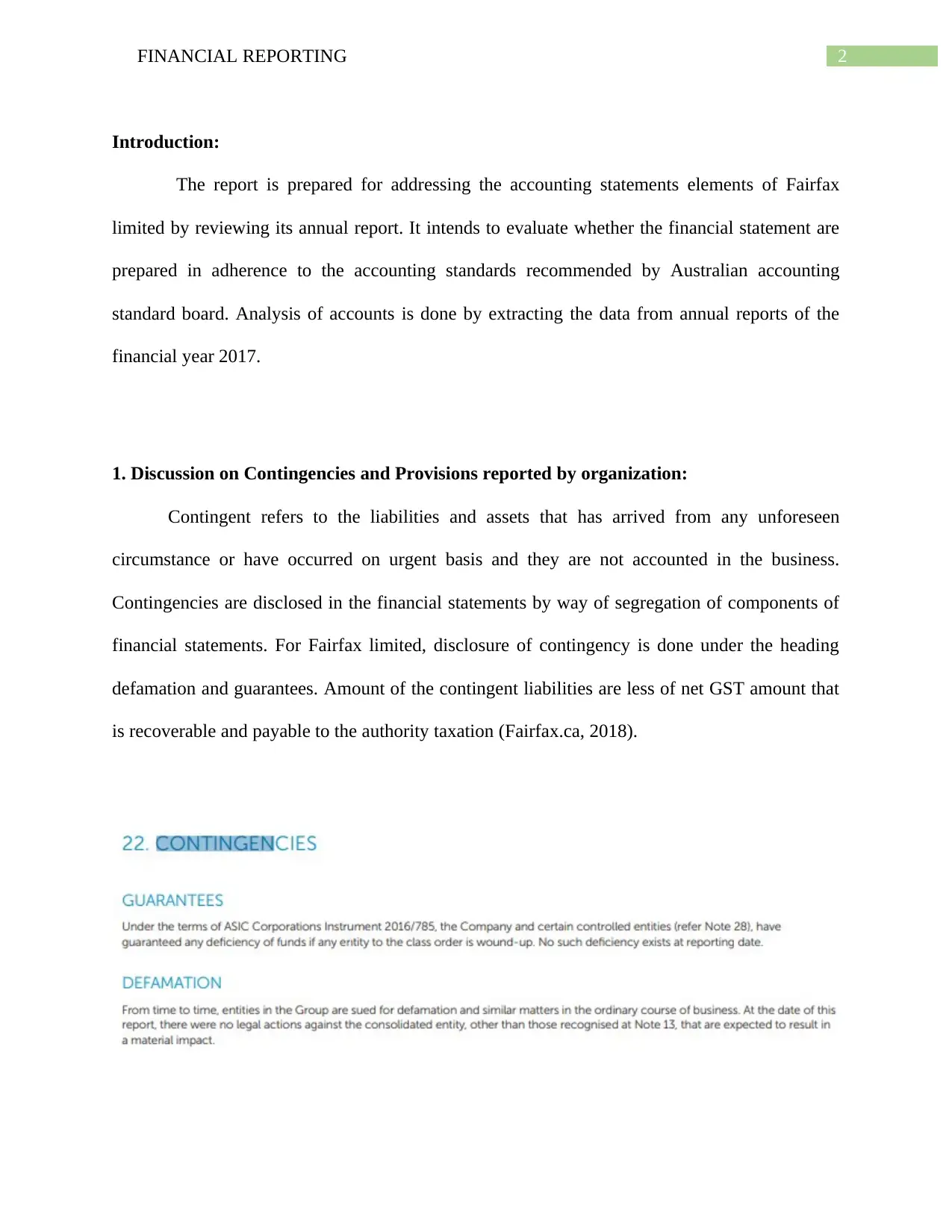

1. Discussion on Contingencies and Provisions reported by organization:

Contingent refers to the liabilities and assets that has arrived from any unforeseen

circumstance or have occurred on urgent basis and they are not accounted in the business.

Contingencies are disclosed in the financial statements by way of segregation of components of

financial statements. For Fairfax limited, disclosure of contingency is done under the heading

defamation and guarantees. Amount of the contingent liabilities are less of net GST amount that

is recoverable and payable to the authority taxation (Fairfax.ca, 2018).

Introduction:

The report is prepared for addressing the accounting statements elements of Fairfax

limited by reviewing its annual report. It intends to evaluate whether the financial statement are

prepared in adherence to the accounting standards recommended by Australian accounting

standard board. Analysis of accounts is done by extracting the data from annual reports of the

financial year 2017.

1. Discussion on Contingencies and Provisions reported by organization:

Contingent refers to the liabilities and assets that has arrived from any unforeseen

circumstance or have occurred on urgent basis and they are not accounted in the business.

Contingencies are disclosed in the financial statements by way of segregation of components of

financial statements. For Fairfax limited, disclosure of contingency is done under the heading

defamation and guarantees. Amount of the contingent liabilities are less of net GST amount that

is recoverable and payable to the authority taxation (Fairfax.ca, 2018).

3FINANCIAL REPORTING

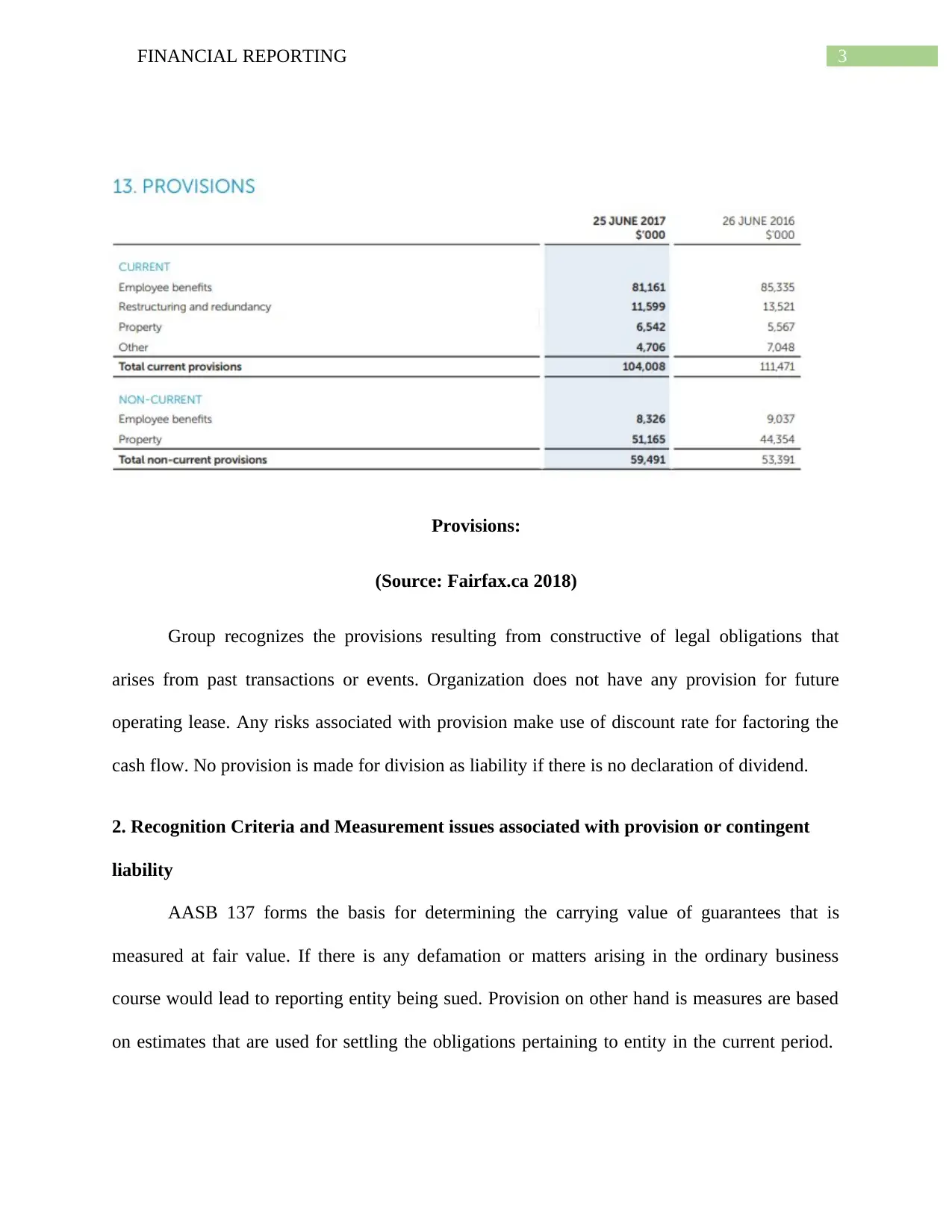

Provisions:

(Source: Fairfax.ca 2018)

Group recognizes the provisions resulting from constructive of legal obligations that

arises from past transactions or events. Organization does not have any provision for future

operating lease. Any risks associated with provision make use of discount rate for factoring the

cash flow. No provision is made for division as liability if there is no declaration of dividend.

2. Recognition Criteria and Measurement issues associated with provision or contingent

liability

AASB 137 forms the basis for determining the carrying value of guarantees that is

measured at fair value. If there is any defamation or matters arising in the ordinary business

course would lead to reporting entity being sued. Provision on other hand is measures are based

on estimates that are used for settling the obligations pertaining to entity in the current period.

Provisions:

(Source: Fairfax.ca 2018)

Group recognizes the provisions resulting from constructive of legal obligations that

arises from past transactions or events. Organization does not have any provision for future

operating lease. Any risks associated with provision make use of discount rate for factoring the

cash flow. No provision is made for division as liability if there is no declaration of dividend.

2. Recognition Criteria and Measurement issues associated with provision or contingent

liability

AASB 137 forms the basis for determining the carrying value of guarantees that is

measured at fair value. If there is any defamation or matters arising in the ordinary business

course would lead to reporting entity being sued. Provision on other hand is measures are based

on estimates that are used for settling the obligations pertaining to entity in the current period.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCIAL REPORTING

The discounting factor reflects the associated risk and any current assessment of the

market situation (Koo et al., 2017).

3. Disclosure of specific Contingency recorded by company:

Under the contingencies, there are two items that is disclosed as depicted from the

annual report of Fairfax limited that is guarantees and defamation. No such deficiency exists at

the time of reporting period. In event of defamation, reporting entity can be sued and in the

current reporting period, there was no legal action against the entity expects some of the items

having material impact (Martin et al., 2017).

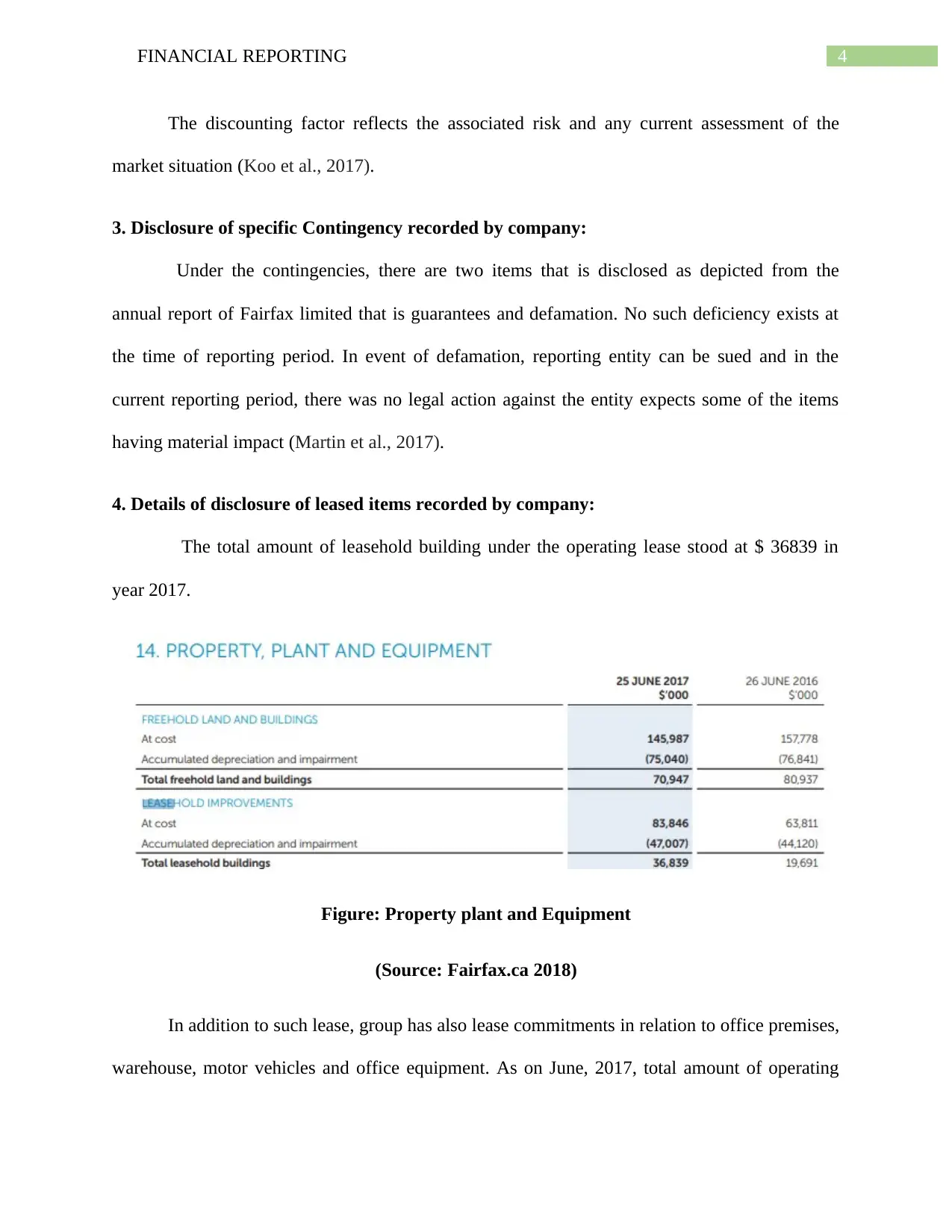

4. Details of disclosure of leased items recorded by company:

The total amount of leasehold building under the operating lease stood at $ 36839 in

year 2017.

Figure: Property plant and Equipment

(Source: Fairfax.ca 2018)

In addition to such lease, group has also lease commitments in relation to office premises,

warehouse, motor vehicles and office equipment. As on June, 2017, total amount of operating

The discounting factor reflects the associated risk and any current assessment of the

market situation (Koo et al., 2017).

3. Disclosure of specific Contingency recorded by company:

Under the contingencies, there are two items that is disclosed as depicted from the

annual report of Fairfax limited that is guarantees and defamation. No such deficiency exists at

the time of reporting period. In event of defamation, reporting entity can be sued and in the

current reporting period, there was no legal action against the entity expects some of the items

having material impact (Martin et al., 2017).

4. Details of disclosure of leased items recorded by company:

The total amount of leasehold building under the operating lease stood at $ 36839 in

year 2017.

Figure: Property plant and Equipment

(Source: Fairfax.ca 2018)

In addition to such lease, group has also lease commitments in relation to office premises,

warehouse, motor vehicles and office equipment. As on June, 2017, total amount of operating

5FINANCIAL REPORTING

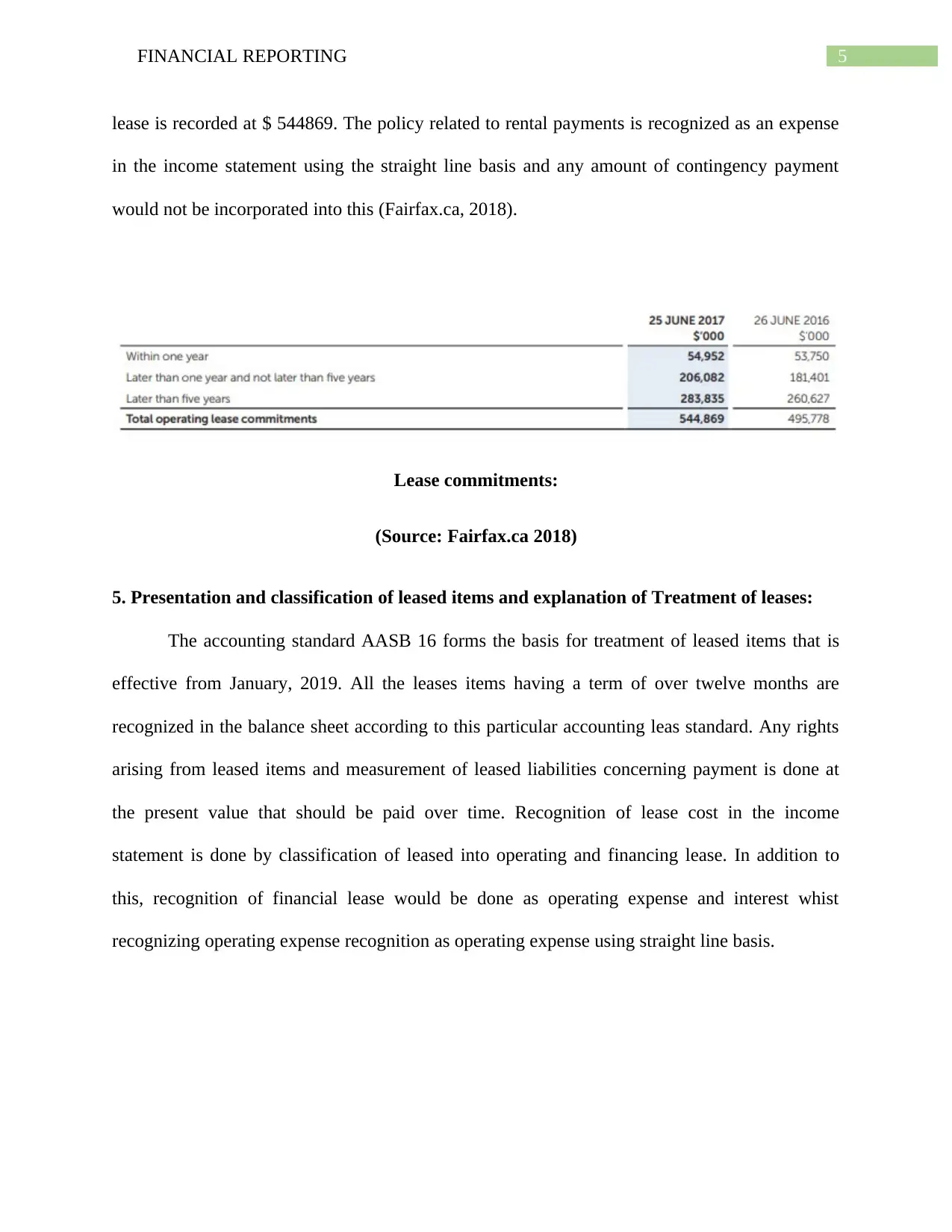

lease is recorded at $ 544869. The policy related to rental payments is recognized as an expense

in the income statement using the straight line basis and any amount of contingency payment

would not be incorporated into this (Fairfax.ca, 2018).

Lease commitments:

(Source: Fairfax.ca 2018)

5. Presentation and classification of leased items and explanation of Treatment of leases:

The accounting standard AASB 16 forms the basis for treatment of leased items that is

effective from January, 2019. All the leases items having a term of over twelve months are

recognized in the balance sheet according to this particular accounting leas standard. Any rights

arising from leased items and measurement of leased liabilities concerning payment is done at

the present value that should be paid over time. Recognition of lease cost in the income

statement is done by classification of leased into operating and financing lease. In addition to

this, recognition of financial lease would be done as operating expense and interest whist

recognizing operating expense recognition as operating expense using straight line basis.

lease is recorded at $ 544869. The policy related to rental payments is recognized as an expense

in the income statement using the straight line basis and any amount of contingency payment

would not be incorporated into this (Fairfax.ca, 2018).

Lease commitments:

(Source: Fairfax.ca 2018)

5. Presentation and classification of leased items and explanation of Treatment of leases:

The accounting standard AASB 16 forms the basis for treatment of leased items that is

effective from January, 2019. All the leases items having a term of over twelve months are

recognized in the balance sheet according to this particular accounting leas standard. Any rights

arising from leased items and measurement of leased liabilities concerning payment is done at

the present value that should be paid over time. Recognition of lease cost in the income

statement is done by classification of leased into operating and financing lease. In addition to

this, recognition of financial lease would be done as operating expense and interest whist

recognizing operating expense recognition as operating expense using straight line basis.

6FINANCIAL REPORTING

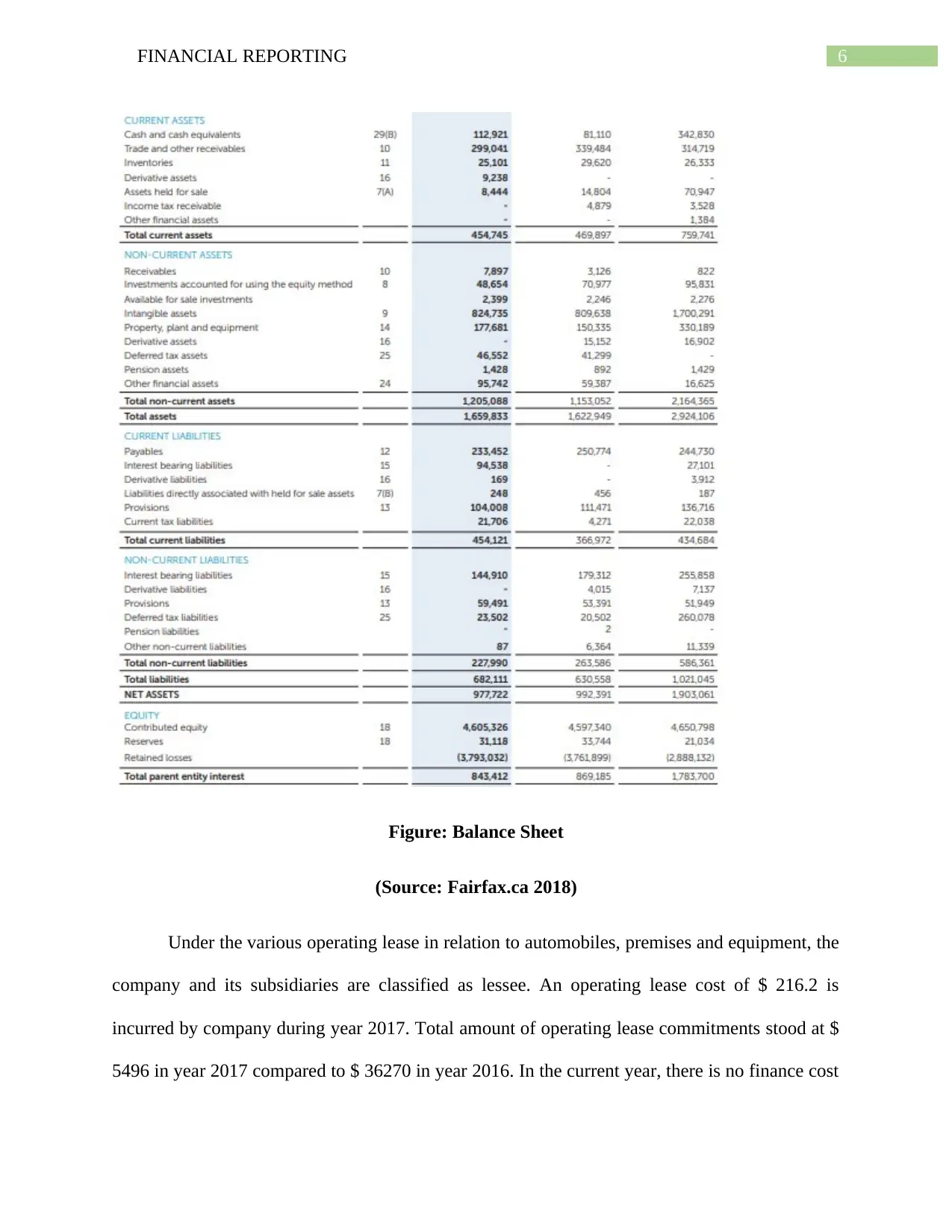

Figure: Balance Sheet

(Source: Fairfax.ca 2018)

Under the various operating lease in relation to automobiles, premises and equipment, the

company and its subsidiaries are classified as lessee. An operating lease cost of $ 216.2 is

incurred by company during year 2017. Total amount of operating lease commitments stood at $

5496 in year 2017 compared to $ 36270 in year 2016. In the current year, there is no finance cost

Figure: Balance Sheet

(Source: Fairfax.ca 2018)

Under the various operating lease in relation to automobiles, premises and equipment, the

company and its subsidiaries are classified as lessee. An operating lease cost of $ 216.2 is

incurred by company during year 2017. Total amount of operating lease commitments stood at $

5496 in year 2017 compared to $ 36270 in year 2016. In the current year, there is no finance cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL REPORTING

incurred by organization as against leased amount of $ 1208 in year 2016. On such lease,

recognition of cost is done in the income statement and is dependent upon the classification of

operating lease and financing lease.

6. Hypothetical situation depicting reclassification of leased items:

The reclassification of leased items is done by using a hypothetical situation that present

the issues that are listed below:

Lessees are enabled by the nature of leased assets without identification of any

modification by utilizing the leased assets.

At the end of lease term, there is a transfer of ownership of leased assets by way of

entering into lease.

An option to experience lease is made relating to the purchasing of assets at a lower of

fair value and at an expected price (Lee & Parker, 2014).

7. Disclosure of Non-current asset – impairment method

In this particular requirement, it is asked to evaluate the valuation of noncurrent assets by

selecting one specific asset. For the analysis purpose, receivables have been selected from items

of noncurrent assets as presented under the statement of financial position. Receivables are the

amounts that are due from debtors of company and are yet to be received against which the

company can claim in event of nonpayment. For year 2017, amount of receivable stood at $ 7897

as against $ 3126 in year 2016 indicating that there is significant increase in value of receivables.

incurred by organization as against leased amount of $ 1208 in year 2016. On such lease,

recognition of cost is done in the income statement and is dependent upon the classification of

operating lease and financing lease.

6. Hypothetical situation depicting reclassification of leased items:

The reclassification of leased items is done by using a hypothetical situation that present

the issues that are listed below:

Lessees are enabled by the nature of leased assets without identification of any

modification by utilizing the leased assets.

At the end of lease term, there is a transfer of ownership of leased assets by way of

entering into lease.

An option to experience lease is made relating to the purchasing of assets at a lower of

fair value and at an expected price (Lee & Parker, 2014).

7. Disclosure of Non-current asset – impairment method

In this particular requirement, it is asked to evaluate the valuation of noncurrent assets by

selecting one specific asset. For the analysis purpose, receivables have been selected from items

of noncurrent assets as presented under the statement of financial position. Receivables are the

amounts that are due from debtors of company and are yet to be received against which the

company can claim in event of nonpayment. For year 2017, amount of receivable stood at $ 7897

as against $ 3126 in year 2016 indicating that there is significant increase in value of receivables.

8FINANCIAL REPORTING

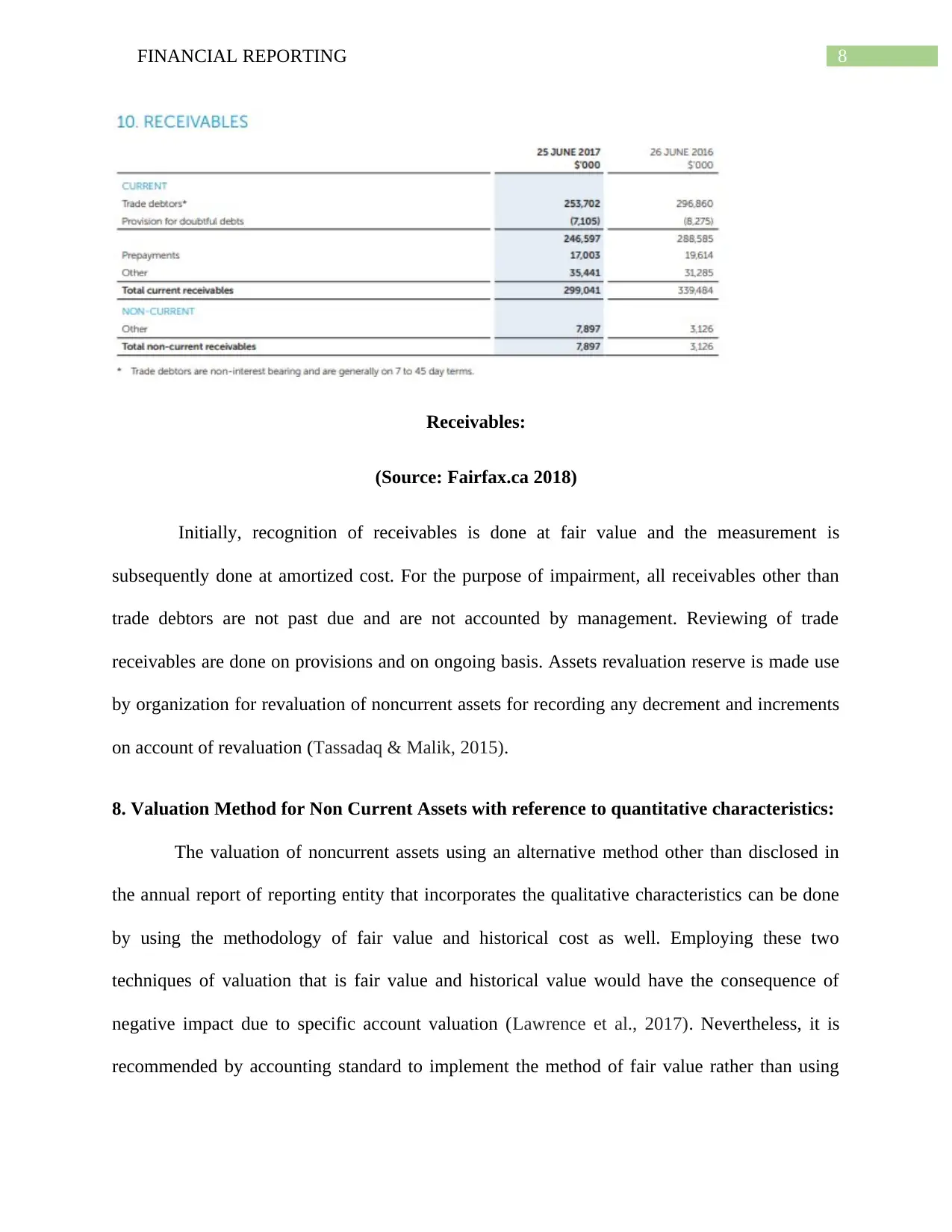

Receivables:

(Source: Fairfax.ca 2018)

Initially, recognition of receivables is done at fair value and the measurement is

subsequently done at amortized cost. For the purpose of impairment, all receivables other than

trade debtors are not past due and are not accounted by management. Reviewing of trade

receivables are done on provisions and on ongoing basis. Assets revaluation reserve is made use

by organization for revaluation of noncurrent assets for recording any decrement and increments

on account of revaluation (Tassadaq & Malik, 2015).

8. Valuation Method for Non Current Assets with reference to quantitative characteristics:

The valuation of noncurrent assets using an alternative method other than disclosed in

the annual report of reporting entity that incorporates the qualitative characteristics can be done

by using the methodology of fair value and historical cost as well. Employing these two

techniques of valuation that is fair value and historical value would have the consequence of

negative impact due to specific account valuation (Lawrence et al., 2017). Nevertheless, it is

recommended by accounting standard to implement the method of fair value rather than using

Receivables:

(Source: Fairfax.ca 2018)

Initially, recognition of receivables is done at fair value and the measurement is

subsequently done at amortized cost. For the purpose of impairment, all receivables other than

trade debtors are not past due and are not accounted by management. Reviewing of trade

receivables are done on provisions and on ongoing basis. Assets revaluation reserve is made use

by organization for revaluation of noncurrent assets for recording any decrement and increments

on account of revaluation (Tassadaq & Malik, 2015).

8. Valuation Method for Non Current Assets with reference to quantitative characteristics:

The valuation of noncurrent assets using an alternative method other than disclosed in

the annual report of reporting entity that incorporates the qualitative characteristics can be done

by using the methodology of fair value and historical cost as well. Employing these two

techniques of valuation that is fair value and historical value would have the consequence of

negative impact due to specific account valuation (Lawrence et al., 2017). Nevertheless, it is

recommended by accounting standard to implement the method of fair value rather than using

9FINANCIAL REPORTING

the technique of historical cost for valuing the noncurrent assets. Therefore, it is recommended to

organization to employ the methodology of fair value for valuing the noncurrent assets.

Conclusion:

The above report present detailed analysis of several accounts of Fairfax limited by

referring to the financial statements as disclosed in the annual report of current year. This also

incorporates evaluation of accounts such as noncurrent assets, provision, contingencies and

methodology of valuation. Conclusions regarding the accounts in the financial statements have

been drawn from the analysis conducted. It can be concluded that the financial report of Fairfax

limited has been prepared in compliance with the accounting standard and it adheres to several

principles as required and recommended by the accounting standard. Evaluation of financial

statements indicates the fact that the measurement issues and recognition criteria for assets and

liabilities are done in accordance with applicable accounting rules and regulations. However,

there is no appropriate disclosure made regarding the contingencies and measurement basis of

noncurrent assets such as receivables.

the technique of historical cost for valuing the noncurrent assets. Therefore, it is recommended to

organization to employ the methodology of fair value for valuing the noncurrent assets.

Conclusion:

The above report present detailed analysis of several accounts of Fairfax limited by

referring to the financial statements as disclosed in the annual report of current year. This also

incorporates evaluation of accounts such as noncurrent assets, provision, contingencies and

methodology of valuation. Conclusions regarding the accounts in the financial statements have

been drawn from the analysis conducted. It can be concluded that the financial report of Fairfax

limited has been prepared in compliance with the accounting standard and it adheres to several

principles as required and recommended by the accounting standard. Evaluation of financial

statements indicates the fact that the measurement issues and recognition criteria for assets and

liabilities are done in accordance with applicable accounting rules and regulations. However,

there is no appropriate disclosure made regarding the contingencies and measurement basis of

noncurrent assets such as receivables.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10FINANCIAL REPORTING

References list:

Fairfax.ca. (2018). Fairfax - Financials - Annual Reports . [online] Available at:

https://www.fairfax.ca/financials/annual-reports/default.aspx [Accessed 21 May 2018].

Filip, A., Labelle, R., & Rousseau, S. (2015). Legal regime and financial reporting

quality. Contemporary Accounting Research, 32(1), 280-307.

Fontes, A., Rodrigues, L. L., & Craig, R. (2017, June). A response to commentaries on a

theoretical model of stakeholder perceptions of a new financial reporting system.

In Accounting Forum (Vol. 41, No. 2, pp. 132-137). Elsevier.

Jiang, J., Nanda, V., & Xiao, S. C. (2016). Market Disruption and Managerial Responses:

Evidence from Financial Reporting and Management Forecasts.

Koo, D. S., Ramalingegowda, S., & Yu, Y. (2017). The effect of financial reporting quality on

corporate dividend policy. Review of Accounting Studies, 22(2), 753-790.

Lawrence, A., Minutti-Meza, M., & Vyas, D. (2017). Is Operational Control Risk Informative of

Financial Reporting Deficiencies?. Auditing: A Journal of Practice and Theory.

Lee, T. A., & Parker, R. H. (Eds.). (2014). Evolution of Corporate Financial Reporting (RLE

Accounting). Routledge.

Martin, G. W., Thomas, W. B., & Diaz, J. (2017). Financial Reporting Quality and Auditor

Locality Contagion.

Page, M. (2014). Business models as a basis for regulation of financial reporting. Journal of

Management & Governance, 18(3), 683-695.

Rajgopal, S. (2015). Financial Reporting Disclosures: Market and Regulatory Failures.

References list:

Fairfax.ca. (2018). Fairfax - Financials - Annual Reports . [online] Available at:

https://www.fairfax.ca/financials/annual-reports/default.aspx [Accessed 21 May 2018].

Filip, A., Labelle, R., & Rousseau, S. (2015). Legal regime and financial reporting

quality. Contemporary Accounting Research, 32(1), 280-307.

Fontes, A., Rodrigues, L. L., & Craig, R. (2017, June). A response to commentaries on a

theoretical model of stakeholder perceptions of a new financial reporting system.

In Accounting Forum (Vol. 41, No. 2, pp. 132-137). Elsevier.

Jiang, J., Nanda, V., & Xiao, S. C. (2016). Market Disruption and Managerial Responses:

Evidence from Financial Reporting and Management Forecasts.

Koo, D. S., Ramalingegowda, S., & Yu, Y. (2017). The effect of financial reporting quality on

corporate dividend policy. Review of Accounting Studies, 22(2), 753-790.

Lawrence, A., Minutti-Meza, M., & Vyas, D. (2017). Is Operational Control Risk Informative of

Financial Reporting Deficiencies?. Auditing: A Journal of Practice and Theory.

Lee, T. A., & Parker, R. H. (Eds.). (2014). Evolution of Corporate Financial Reporting (RLE

Accounting). Routledge.

Martin, G. W., Thomas, W. B., & Diaz, J. (2017). Financial Reporting Quality and Auditor

Locality Contagion.

Page, M. (2014). Business models as a basis for regulation of financial reporting. Journal of

Management & Governance, 18(3), 683-695.

Rajgopal, S. (2015). Financial Reporting Disclosures: Market and Regulatory Failures.

11FINANCIAL REPORTING

Tassadaq, F., & Malik, Q. A. (2015). Creative Accounting & Financial Reporting: Model

Development & Empirical Testing. International Journal of Economics and Financial

Issues, 5(2).

Tassadaq, F., & Malik, Q. A. (2015). Creative Accounting & Financial Reporting: Model

Development & Empirical Testing. International Journal of Economics and Financial

Issues, 5(2).

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.