Financial Reporting Analysis: Performance and Investment Evaluation

VerifiedAdded on 2020/11/12

|15

|4365

|378

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, focusing on the context of financial reporting including regulatory frameworks and governance, and the purpose of financial reporting for meeting organizational objectives, development, and growth. It includes an interpretation of profit and loss, cash flow, and balance sheets, along with an analysis of financial ratios for organizational performance and investments. The report also discusses the benefits of International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), and evaluates models of financial reporting. Furthermore, it examines the differences and importance of financial reporting across different countries, providing a detailed overview of financial reporting practices and their implications for stakeholders like investors, government, and directors, using Dixons Carphone as a case study. The report also covers limitations of accounting and financial reporting.

FINANCIAL

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1: Analysis of context of financial reporting including regulatory frameworks and

governance of financial reporting...............................................................................................1

P2: Analysis of purpose of the financial reporting for meeting organisational objectives,

development and growth.............................................................................................................2

LO2..................................................................................................................................................3

P3: Interpretation of profit and loss, cash flow and balance sheet..............................................3

P4: Financial ratios for organisational performance and investments........................................4

LO3..................................................................................................................................................6

P5: Benefits of International Accounting Standards (IAS) and International Financial

Reporting and Standards (IFRS) ................................................................................................6

P6: Evaluation of models of financial reporting and auditing....................................................7

LO4..................................................................................................................................................8

P7: Differences and importance of financial reporting across different countries:.....................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1: Analysis of context of financial reporting including regulatory frameworks and

governance of financial reporting...............................................................................................1

P2: Analysis of purpose of the financial reporting for meeting organisational objectives,

development and growth.............................................................................................................2

LO2..................................................................................................................................................3

P3: Interpretation of profit and loss, cash flow and balance sheet..............................................3

P4: Financial ratios for organisational performance and investments........................................4

LO3..................................................................................................................................................6

P5: Benefits of International Accounting Standards (IAS) and International Financial

Reporting and Standards (IFRS) ................................................................................................6

P6: Evaluation of models of financial reporting and auditing....................................................7

LO4..................................................................................................................................................8

P7: Differences and importance of financial reporting across different countries:.....................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial reporting means disclosure of the financial results and other relating

information of management and the external stakeholders like investors, customers etc. relating

to the company's performance over a specific period of time. Financial reports include statement

of financial position, income statement, statement of change in equity and cash flow statement.

The primary motive of financial reporting is to provide information which are relating to the

financial position and changes in the financial position in the business of organisation like

“Dixons Carphone” that is useful in making effective economic decisions. This report is divided

into four tasks. First task contain analysis of context of financial reporting framework and its

purpose for meeting organisational objectives. Second task contains interpretation of financial

statements, third task defines the financial reporting standards and its theoretical models and

standards. Last task contains evaluation of international differences in financial reporting.

LO1

P1: Analysis of context of financial reporting including regulatory frameworks and governance

of financial reporting

Financial reporting is the process in which financial statements of the organisation are

disclosed for management, investors and the government. Regulatory framework provides rules

and regulations for the purpose of accounting(Alyousif and Kalenkoski, 2017). The International

Accounting Standards Broad (IASB) provides a regularity frameworks for accounting in form of

international accounting standards(Feng, 2018). Regulatory framework combines the legal

obligations and regulations which are set by the UK higher authority for accounting which are

used by companies like Dixons Carphone. Regulations of IABS which are helpful for

stakeholder which are imposed in specific format of IFRS are as follows:

International Financial Reporting Standard(IFRS): These are introduced through

IASB. This body is responsible for formulating the principles and regulatory norms. Some of the

principles are:

IFRS 1: It is used in initial implementation of IFRS, on which companies IFRS will be

adopted. It would have related to the Dixons Carphone for preparation and presentation of

financial statements.

1

Financial reporting means disclosure of the financial results and other relating

information of management and the external stakeholders like investors, customers etc. relating

to the company's performance over a specific period of time. Financial reports include statement

of financial position, income statement, statement of change in equity and cash flow statement.

The primary motive of financial reporting is to provide information which are relating to the

financial position and changes in the financial position in the business of organisation like

“Dixons Carphone” that is useful in making effective economic decisions. This report is divided

into four tasks. First task contain analysis of context of financial reporting framework and its

purpose for meeting organisational objectives. Second task contains interpretation of financial

statements, third task defines the financial reporting standards and its theoretical models and

standards. Last task contains evaluation of international differences in financial reporting.

LO1

P1: Analysis of context of financial reporting including regulatory frameworks and governance

of financial reporting

Financial reporting is the process in which financial statements of the organisation are

disclosed for management, investors and the government. Regulatory framework provides rules

and regulations for the purpose of accounting(Alyousif and Kalenkoski, 2017). The International

Accounting Standards Broad (IASB) provides a regularity frameworks for accounting in form of

international accounting standards(Feng, 2018). Regulatory framework combines the legal

obligations and regulations which are set by the UK higher authority for accounting which are

used by companies like Dixons Carphone. Regulations of IABS which are helpful for

stakeholder which are imposed in specific format of IFRS are as follows:

International Financial Reporting Standard(IFRS): These are introduced through

IASB. This body is responsible for formulating the principles and regulatory norms. Some of the

principles are:

IFRS 1: It is used in initial implementation of IFRS, on which companies IFRS will be

adopted. It would have related to the Dixons Carphone for preparation and presentation of

financial statements.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

IFRS 3: It is used in merger and acquisition. It would assist organisation to sell or

transfer assets and liabilities in case of amalgamation and merger.

Regulatory frameworks and governance of financial reporting:

It is a responsible for guiding organisation and helps in attaining overall aims and

objectives of Dixons Carphone during future time. The main purpose of these framework is to

examine business performance, which helps the stakeholders to take decisions regarding

company (Hung and Chuang, 2012). The objectives of regulatory frameworks and governance

related to international regulations are:

Quality of financial statements: This means specific features of the financial statements

and information that assist to make reliable decision.

Relevance: Actual and correct data are recorded by the organisation helps the

organisation to achieve its goal.

Faithful representation: The financial information used in preparation and presentation

of financial statements helps in making financial decisions for stakeholders.

Effect of financial reporting on government, investors and directors:

Government: Financial reporting includes financial statements that discloses financial

results and related information to management and stakeholders. Government being an external

stakeholder gain true and fair information regarding financial position of Dixons Carphone.

Calculation of tax imposed by government is calculated on this information and this serves as

main source of revenue for government.

Investors: Financial information of an organisation provides real situation and condition

of the Dixons Carphone. This gives a fair chance to investors to analyse different investment

options and select most productive. For this analysis financial statements are used that gives

correct information required in decision making.

Directors: Directors are the one who operates business functions in Dixons Carphone

organisation. Before performing multi-pal business activities planes and policies are designed

that gives basis to set objects for business that will be achieved in long run. Directors by

analysing the financial statements decides that company is performing as per plans or not and

corrective action are taken.

2

transfer assets and liabilities in case of amalgamation and merger.

Regulatory frameworks and governance of financial reporting:

It is a responsible for guiding organisation and helps in attaining overall aims and

objectives of Dixons Carphone during future time. The main purpose of these framework is to

examine business performance, which helps the stakeholders to take decisions regarding

company (Hung and Chuang, 2012). The objectives of regulatory frameworks and governance

related to international regulations are:

Quality of financial statements: This means specific features of the financial statements

and information that assist to make reliable decision.

Relevance: Actual and correct data are recorded by the organisation helps the

organisation to achieve its goal.

Faithful representation: The financial information used in preparation and presentation

of financial statements helps in making financial decisions for stakeholders.

Effect of financial reporting on government, investors and directors:

Government: Financial reporting includes financial statements that discloses financial

results and related information to management and stakeholders. Government being an external

stakeholder gain true and fair information regarding financial position of Dixons Carphone.

Calculation of tax imposed by government is calculated on this information and this serves as

main source of revenue for government.

Investors: Financial information of an organisation provides real situation and condition

of the Dixons Carphone. This gives a fair chance to investors to analyse different investment

options and select most productive. For this analysis financial statements are used that gives

correct information required in decision making.

Directors: Directors are the one who operates business functions in Dixons Carphone

organisation. Before performing multi-pal business activities planes and policies are designed

that gives basis to set objects for business that will be achieved in long run. Directors by

analysing the financial statements decides that company is performing as per plans or not and

corrective action are taken.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Customer: In recent time, customer before making any major contract focuses to review

the financial statements of supplier that helps them to determine overall financial ability in long

run so that goods and services can be mandated in the contract.

Employee: Nowadays company may select to give detail financial reports to employees

which help in increasing their involvement in different operation making them more profitable to

attain the desired result of company.

P2: Analysis of purpose of the financial reporting for meeting organisational objectives,

development and growth

In every organisation like Dixons Carphone, it is important to use reliable reporting

system which lead to make profits in future. This is an effective process of producing statements

for disclosure of financial data of the organisation like Dixons Carphone to owners, investors

and government(Jayasinghe, 2014). Financial reports include preparation and presentation of

statement of financial position, income statement, statement of change in equity and cash flow

statement. It is used in providing idea of integrity and worth of the company to the stakeholders.

Crucial and reliable business decisions are also made through this reporting.

As per IASB, “ Dixons Carphone” have to formulate its financial records to present the

financial outcomes of the company to their shareholders. It need transparency of the data which

help the business entity in operating business effectively. It is very crucial for Dixons Carphone

to follow all the rules and regulations and principles related to preparation and presentation of

financial statements. Dixons Carphone is preparing their financial reports for operating the

business at international level.

Purpose:

The primary objective of the financial reporting is to give financial information of the

Dixons Carphone regarding its performance, financial position and change in financial position

of the organisation that helps the organisation to achieve its long term goals. The purpose of

financial reporting is to assist the management of Dixons Carphone to frame the financial

strategies and decide the way it can increase its market share and revenue(Khanzhyn, 2012).

Some of the main objective or purpose of financial reporting which support in overall growth

and development of organisation in specific time frame such as:

Provide meaningful information to valuable investors: All investor wants to have a

detail knowledge about how cash is being reinvested in the business and capital must be

3

the financial statements of supplier that helps them to determine overall financial ability in long

run so that goods and services can be mandated in the contract.

Employee: Nowadays company may select to give detail financial reports to employees

which help in increasing their involvement in different operation making them more profitable to

attain the desired result of company.

P2: Analysis of purpose of the financial reporting for meeting organisational objectives,

development and growth

In every organisation like Dixons Carphone, it is important to use reliable reporting

system which lead to make profits in future. This is an effective process of producing statements

for disclosure of financial data of the organisation like Dixons Carphone to owners, investors

and government(Jayasinghe, 2014). Financial reports include preparation and presentation of

statement of financial position, income statement, statement of change in equity and cash flow

statement. It is used in providing idea of integrity and worth of the company to the stakeholders.

Crucial and reliable business decisions are also made through this reporting.

As per IASB, “ Dixons Carphone” have to formulate its financial records to present the

financial outcomes of the company to their shareholders. It need transparency of the data which

help the business entity in operating business effectively. It is very crucial for Dixons Carphone

to follow all the rules and regulations and principles related to preparation and presentation of

financial statements. Dixons Carphone is preparing their financial reports for operating the

business at international level.

Purpose:

The primary objective of the financial reporting is to give financial information of the

Dixons Carphone regarding its performance, financial position and change in financial position

of the organisation that helps the organisation to achieve its long term goals. The purpose of

financial reporting is to assist the management of Dixons Carphone to frame the financial

strategies and decide the way it can increase its market share and revenue(Khanzhyn, 2012).

Some of the main objective or purpose of financial reporting which support in overall growth

and development of organisation in specific time frame such as:

Provide meaningful information to valuable investors: All investor wants to have a

detail knowledge about how cash is being reinvested in the business and capital must be

3

effectively utilised in business operation. So these reports aid investor to check that

company have place their money is good place this satisfy them most and they keep

investing on regular basis. Appropriate investment from investors enable an organisation

to perform different operation in meaningful manner so that profit can be increase and

goals can be attained.

Track Cash Flow: It is essential for company to maintain a record of every transaction

related with cash, such as they must have a knowledge about source of money and proper

place to investment. This help in better recognizing the actual performance of business so

that company can recover the outstanding debts and keep focus on continuous growing.

Limitations of Accounting & Financial Reporting

The main disadvantage of financial reports is that it does not discuss any non-financial

problem of company due to which efficiency of operation reduces.

Sometime, financial reports are not verified which means that concept, policies, pattern

of accounting have not been evaluated due to which there are can be many problem for

investors.

Not always comparable across companies as companies uses various pattern of

accounting due to which comparison is not easy to make any decision.

LO2

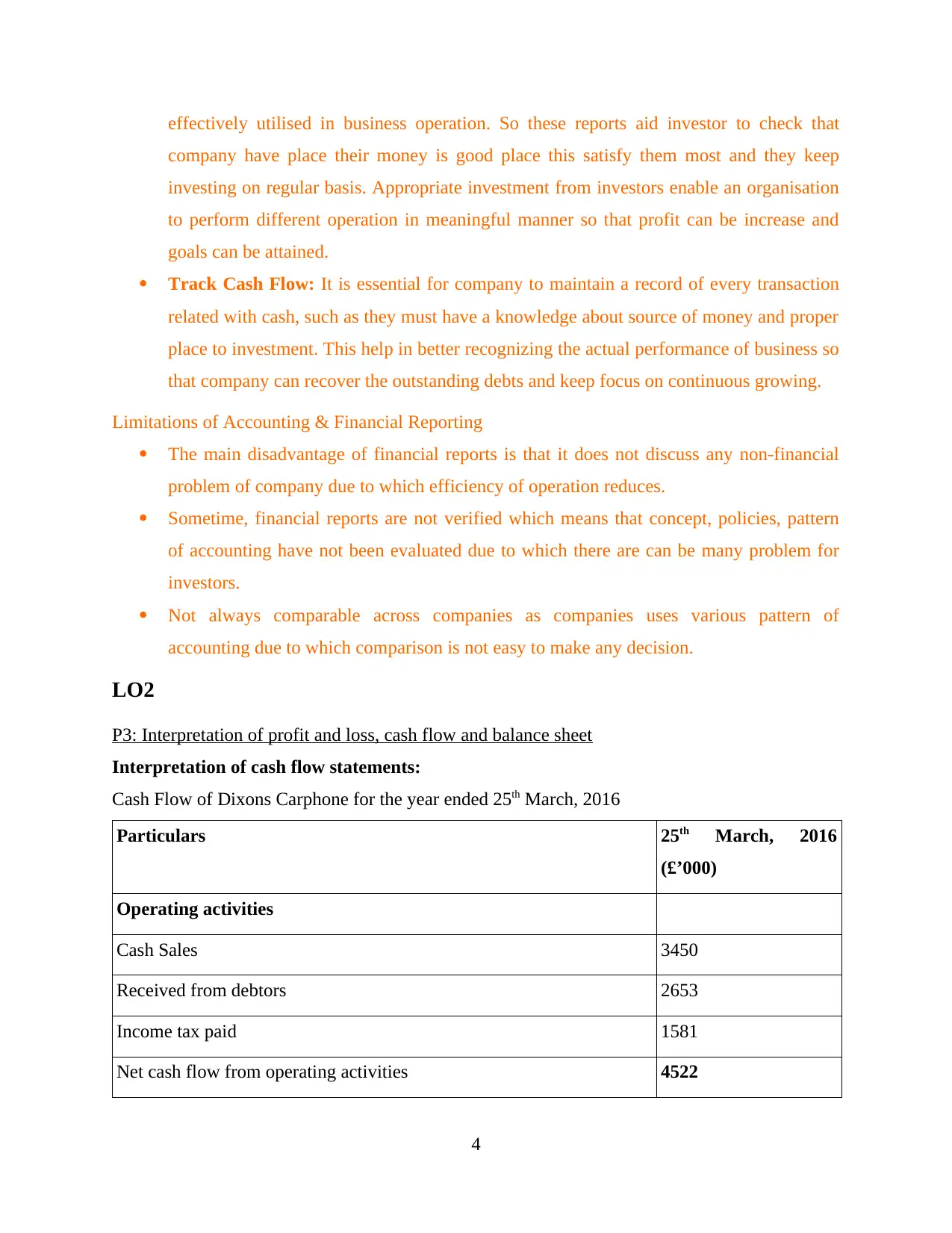

P3: Interpretation of profit and loss, cash flow and balance sheet

Interpretation of cash flow statements:

Cash Flow of Dixons Carphone for the year ended 25th March, 2016

Particulars 25th March, 2016

(£’000)

Operating activities

Cash Sales 3450

Received from debtors 2653

Income tax paid 1581

Net cash flow from operating activities 4522

4

company have place their money is good place this satisfy them most and they keep

investing on regular basis. Appropriate investment from investors enable an organisation

to perform different operation in meaningful manner so that profit can be increase and

goals can be attained.

Track Cash Flow: It is essential for company to maintain a record of every transaction

related with cash, such as they must have a knowledge about source of money and proper

place to investment. This help in better recognizing the actual performance of business so

that company can recover the outstanding debts and keep focus on continuous growing.

Limitations of Accounting & Financial Reporting

The main disadvantage of financial reports is that it does not discuss any non-financial

problem of company due to which efficiency of operation reduces.

Sometime, financial reports are not verified which means that concept, policies, pattern

of accounting have not been evaluated due to which there are can be many problem for

investors.

Not always comparable across companies as companies uses various pattern of

accounting due to which comparison is not easy to make any decision.

LO2

P3: Interpretation of profit and loss, cash flow and balance sheet

Interpretation of cash flow statements:

Cash Flow of Dixons Carphone for the year ended 25th March, 2016

Particulars 25th March, 2016

(£’000)

Operating activities

Cash Sales 3450

Received from debtors 2653

Income tax paid 1581

Net cash flow from operating activities 4522

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

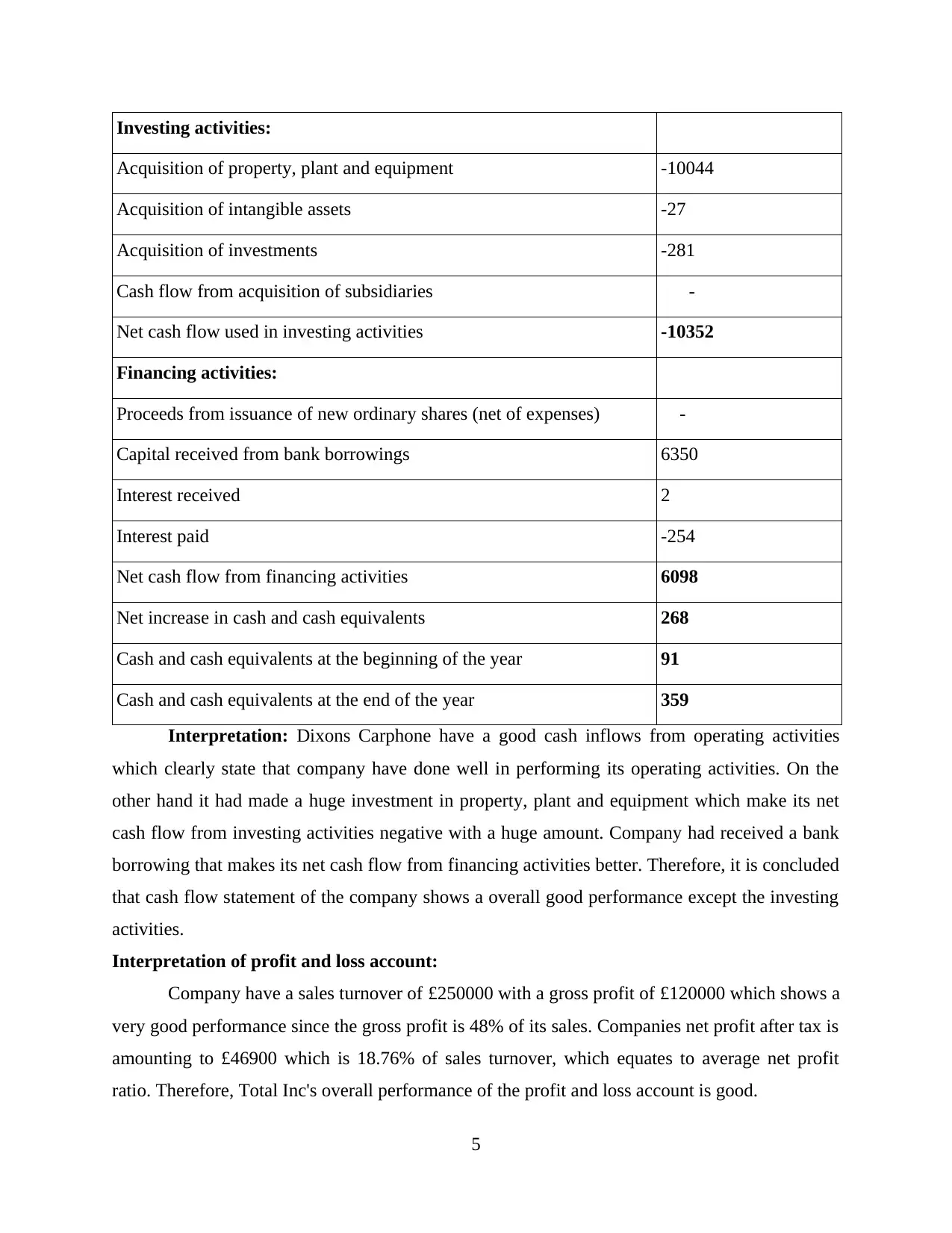

Investing activities:

Acquisition of property, plant and equipment -10044

Acquisition of intangible assets -27

Acquisition of investments -281

Cash flow from acquisition of subsidiaries -

Net cash flow used in investing activities -10352

Financing activities:

Proceeds from issuance of new ordinary shares (net of expenses) -

Capital received from bank borrowings 6350

Interest received 2

Interest paid -254

Net cash flow from financing activities 6098

Net increase in cash and cash equivalents 268

Cash and cash equivalents at the beginning of the year 91

Cash and cash equivalents at the end of the year 359

Interpretation: Dixons Carphone have a good cash inflows from operating activities

which clearly state that company have done well in performing its operating activities. On the

other hand it had made a huge investment in property, plant and equipment which make its net

cash flow from investing activities negative with a huge amount. Company had received a bank

borrowing that makes its net cash flow from financing activities better. Therefore, it is concluded

that cash flow statement of the company shows a overall good performance except the investing

activities.

Interpretation of profit and loss account:

Company have a sales turnover of £250000 with a gross profit of £120000 which shows a

very good performance since the gross profit is 48% of its sales. Companies net profit after tax is

amounting to £46900 which is 18.76% of sales turnover, which equates to average net profit

ratio. Therefore, Total Inc's overall performance of the profit and loss account is good.

5

Acquisition of property, plant and equipment -10044

Acquisition of intangible assets -27

Acquisition of investments -281

Cash flow from acquisition of subsidiaries -

Net cash flow used in investing activities -10352

Financing activities:

Proceeds from issuance of new ordinary shares (net of expenses) -

Capital received from bank borrowings 6350

Interest received 2

Interest paid -254

Net cash flow from financing activities 6098

Net increase in cash and cash equivalents 268

Cash and cash equivalents at the beginning of the year 91

Cash and cash equivalents at the end of the year 359

Interpretation: Dixons Carphone have a good cash inflows from operating activities

which clearly state that company have done well in performing its operating activities. On the

other hand it had made a huge investment in property, plant and equipment which make its net

cash flow from investing activities negative with a huge amount. Company had received a bank

borrowing that makes its net cash flow from financing activities better. Therefore, it is concluded

that cash flow statement of the company shows a overall good performance except the investing

activities.

Interpretation of profit and loss account:

Company have a sales turnover of £250000 with a gross profit of £120000 which shows a

very good performance since the gross profit is 48% of its sales. Companies net profit after tax is

amounting to £46900 which is 18.76% of sales turnover, which equates to average net profit

ratio. Therefore, Total Inc's overall performance of the profit and loss account is good.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

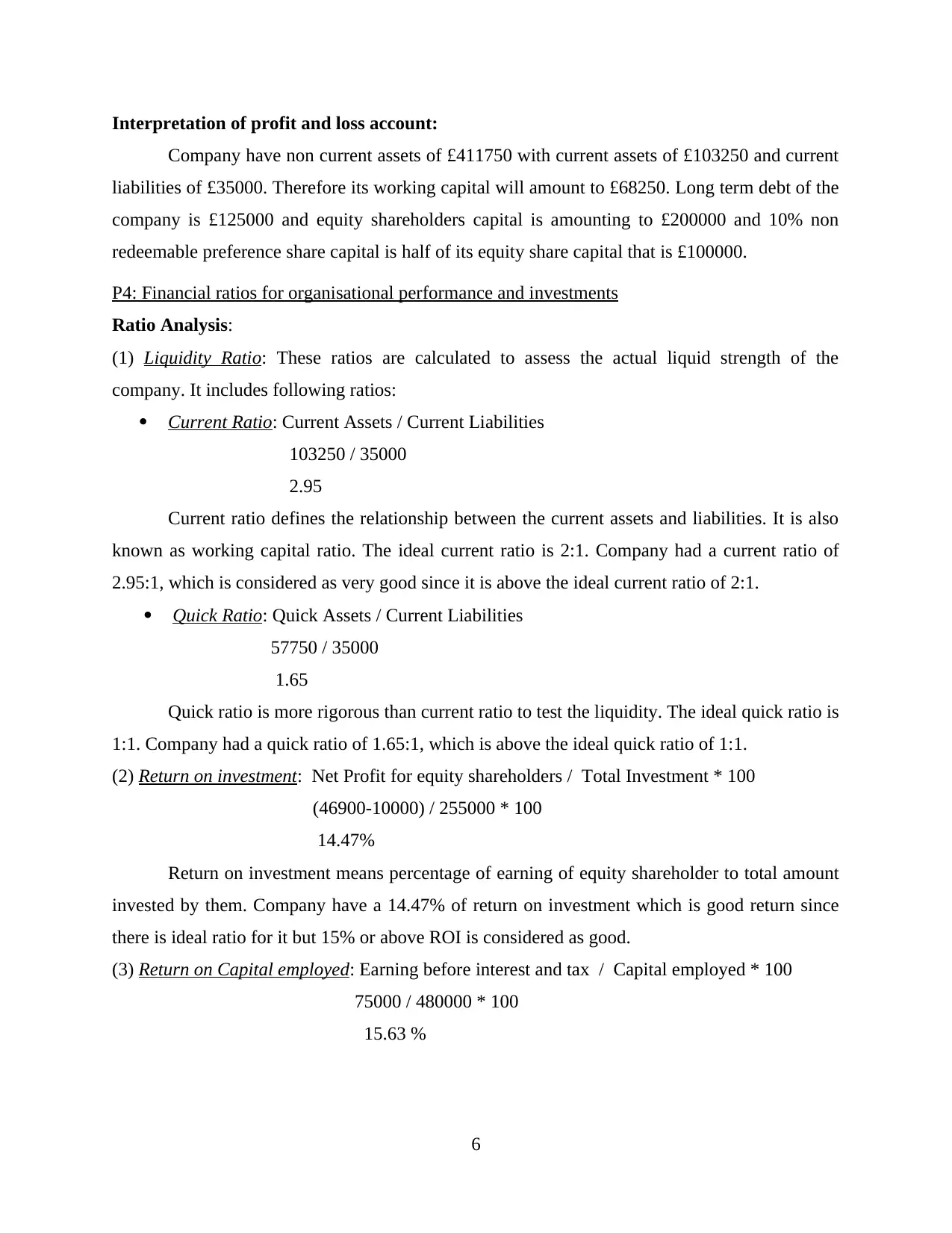

Interpretation of profit and loss account:

Company have non current assets of £411750 with current assets of £103250 and current

liabilities of £35000. Therefore its working capital will amount to £68250. Long term debt of the

company is £125000 and equity shareholders capital is amounting to £200000 and 10% non

redeemable preference share capital is half of its equity share capital that is £100000.

P4: Financial ratios for organisational performance and investments

Ratio Analysis:

(1) Liquidity Ratio: These ratios are calculated to assess the actual liquid strength of the

company. It includes following ratios:

Current Ratio: Current Assets / Current Liabilities

103250 / 35000

2.95

Current ratio defines the relationship between the current assets and liabilities. It is also

known as working capital ratio. The ideal current ratio is 2:1. Company had a current ratio of

2.95:1, which is considered as very good since it is above the ideal current ratio of 2:1.

Quick Ratio: Quick Assets / Current Liabilities

57750 / 35000

1.65

Quick ratio is more rigorous than current ratio to test the liquidity. The ideal quick ratio is

1:1. Company had a quick ratio of 1.65:1, which is above the ideal quick ratio of 1:1.

(2) Return on investment: Net Profit for equity shareholders / Total Investment * 100

(46900-10000) / 255000 * 100

14.47%

Return on investment means percentage of earning of equity shareholder to total amount

invested by them. Company have a 14.47% of return on investment which is good return since

there is ideal ratio for it but 15% or above ROI is considered as good.

(3) Return on Capital employed: Earning before interest and tax / Capital employed * 100

75000 / 480000 * 100

15.63 %

6

Company have non current assets of £411750 with current assets of £103250 and current

liabilities of £35000. Therefore its working capital will amount to £68250. Long term debt of the

company is £125000 and equity shareholders capital is amounting to £200000 and 10% non

redeemable preference share capital is half of its equity share capital that is £100000.

P4: Financial ratios for organisational performance and investments

Ratio Analysis:

(1) Liquidity Ratio: These ratios are calculated to assess the actual liquid strength of the

company. It includes following ratios:

Current Ratio: Current Assets / Current Liabilities

103250 / 35000

2.95

Current ratio defines the relationship between the current assets and liabilities. It is also

known as working capital ratio. The ideal current ratio is 2:1. Company had a current ratio of

2.95:1, which is considered as very good since it is above the ideal current ratio of 2:1.

Quick Ratio: Quick Assets / Current Liabilities

57750 / 35000

1.65

Quick ratio is more rigorous than current ratio to test the liquidity. The ideal quick ratio is

1:1. Company had a quick ratio of 1.65:1, which is above the ideal quick ratio of 1:1.

(2) Return on investment: Net Profit for equity shareholders / Total Investment * 100

(46900-10000) / 255000 * 100

14.47%

Return on investment means percentage of earning of equity shareholder to total amount

invested by them. Company have a 14.47% of return on investment which is good return since

there is ideal ratio for it but 15% or above ROI is considered as good.

(3) Return on Capital employed: Earning before interest and tax / Capital employed * 100

75000 / 480000 * 100

15.63 %

6

Return on capital employed means percentage of operating profit earned by the company.

Company earns return on capital employed of 15.63% which is considered as average return as

per the market to attract investors.

(4) Capital Gearing Ratio: Fixed income bearing securities / Equity shareholders fund

18000 / 255000 * 100

7.06%

It measures the company's borrowed fund's proportion to its equity. Ideal capital gearing

ratio is approx 50%. Presently company had a very low capital gearing ratio of 7.06%, which is

very poor and therefore company have to improve this ratio by reducing its fixed income bearing

securities or increasing its equity fund.

(5) Debtor Collection Period: Accounts receivables / Credit sales * 365

52500 / 187500 * 365

102.2 or 103 days

It means average collection period from the debtors. Ideally 30 days or less is considered

as better. Presently company had a debtor collection period of 103 days, which is much higher

than the standard. Therefore company have to improve its debtor collection period by reducing it.

Theories and models for existing and potential financial problems:

While running business, organisation like Dixons Carphone faces many financial

problems like liquidity, profitability etc. and for responding these problems, organisation have to

use appropriate theories and models like: Decision Making: Management make many financial decisions like investment,

operational strategies etc. Therefore for making this decisions management uses ratios

and interpretation of financial statements so that financial problems are resolved

(Kimbro and Xu, 2016). Marginal Costing: Marginal costing is a technique in which variable manufacturing

cost are considered and decision is taken that whether to accept the particular project or

not. Absorption Costing: In this all manufacturing costs are considered for reporting

purpose, in this decision for the proposal is taken by considering all the cost except

fixed overhead cost of goods sold.

7

Company earns return on capital employed of 15.63% which is considered as average return as

per the market to attract investors.

(4) Capital Gearing Ratio: Fixed income bearing securities / Equity shareholders fund

18000 / 255000 * 100

7.06%

It measures the company's borrowed fund's proportion to its equity. Ideal capital gearing

ratio is approx 50%. Presently company had a very low capital gearing ratio of 7.06%, which is

very poor and therefore company have to improve this ratio by reducing its fixed income bearing

securities or increasing its equity fund.

(5) Debtor Collection Period: Accounts receivables / Credit sales * 365

52500 / 187500 * 365

102.2 or 103 days

It means average collection period from the debtors. Ideally 30 days or less is considered

as better. Presently company had a debtor collection period of 103 days, which is much higher

than the standard. Therefore company have to improve its debtor collection period by reducing it.

Theories and models for existing and potential financial problems:

While running business, organisation like Dixons Carphone faces many financial

problems like liquidity, profitability etc. and for responding these problems, organisation have to

use appropriate theories and models like: Decision Making: Management make many financial decisions like investment,

operational strategies etc. Therefore for making this decisions management uses ratios

and interpretation of financial statements so that financial problems are resolved

(Kimbro and Xu, 2016). Marginal Costing: Marginal costing is a technique in which variable manufacturing

cost are considered and decision is taken that whether to accept the particular project or

not. Absorption Costing: In this all manufacturing costs are considered for reporting

purpose, in this decision for the proposal is taken by considering all the cost except

fixed overhead cost of goods sold.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variances: In this variances are calculated with the help of actual and budgeted cost

and this difference between actual and budgeted is known as variance. If this variance

is negative then management will try to improve its actual performance as compare to

budgeted performance of cost.

LO3

P5: Benefits of International Accounting Standards (IAS) and International Financial Reporting

and Standards (IFRS)

IFRS (International Financial Reporting Standards): It is a set of accounting

standards which are developed by International Accounting Standards Board(IASB). It contains

the framework which is used globally for preparation and presentation of financial statements of

the companies like Dixons Carphone. Using IFRS for financial reporting gives benefits of

contributing the economy by providing the opportunities to the investors. It direct the

organisations in recording the appropriate information in the financial statement, which is used

by shareholders for analysing their money is used effectively or not(.Lemieux , 2012). It aslo

helps in setting benchmark for companies for attaining competitive advantage in the industry.

Together with this it set the global language for preparation and presentation of financial

statements so that investor from anywhere in the world can understand it. For example- Using

international financial reporting by Dixons Carphone will make all the financial information

relevand all over the world.

IAS (International Accounting Standards): These are the oldest accounting standards

which are now replaced by IFRS in 2001. The Standards in IAS are introduced by International

Accounting Standards Committee (IASC) in which organisations follows accounting standards in

their accounting of financial information. It focuses to record financial information appropriately

in the books of accounts(Lu and Fang , 2013). Several benefits of implementing IAS in business

organisation is that it facilitate the ethical compliance in preparation and presentation of financial

statements and also give suggestions from accounting professionals throughout the world. IAS

helps in improving the international investment since it make it easier and cheaper for the

company in raising the capital for the business from the investors globally. Together with this it

encourages the international trade where companies can seek strategic partners, suppliers or

customers in other countries also. For example- Using international accounting standards all the

8

and this difference between actual and budgeted is known as variance. If this variance

is negative then management will try to improve its actual performance as compare to

budgeted performance of cost.

LO3

P5: Benefits of International Accounting Standards (IAS) and International Financial Reporting

and Standards (IFRS)

IFRS (International Financial Reporting Standards): It is a set of accounting

standards which are developed by International Accounting Standards Board(IASB). It contains

the framework which is used globally for preparation and presentation of financial statements of

the companies like Dixons Carphone. Using IFRS for financial reporting gives benefits of

contributing the economy by providing the opportunities to the investors. It direct the

organisations in recording the appropriate information in the financial statement, which is used

by shareholders for analysing their money is used effectively or not(.Lemieux , 2012). It aslo

helps in setting benchmark for companies for attaining competitive advantage in the industry.

Together with this it set the global language for preparation and presentation of financial

statements so that investor from anywhere in the world can understand it. For example- Using

international financial reporting by Dixons Carphone will make all the financial information

relevand all over the world.

IAS (International Accounting Standards): These are the oldest accounting standards

which are now replaced by IFRS in 2001. The Standards in IAS are introduced by International

Accounting Standards Committee (IASC) in which organisations follows accounting standards in

their accounting of financial information. It focuses to record financial information appropriately

in the books of accounts(Lu and Fang , 2013). Several benefits of implementing IAS in business

organisation is that it facilitate the ethical compliance in preparation and presentation of financial

statements and also give suggestions from accounting professionals throughout the world. IAS

helps in improving the international investment since it make it easier and cheaper for the

company in raising the capital for the business from the investors globally. Together with this it

encourages the international trade where companies can seek strategic partners, suppliers or

customers in other countries also. For example- Using international accounting standards all the

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting of the organisation will be prepared as per rules and regulations athat are accepted

internationally.

P6: Evaluation of models of financial reporting and auditing

Models of financial reporting:

The financial reporting model is the set of structure and content of financial reports

issued by the government (local and state). This model includes the basic financial statements

and its supporting notes and information. In this review of existing standards to ensure that

whether they are meeting the objectives of the company in the present financial reporting

environment(Mir, 2013). The GASB's research gathers the input to help the Board to decide the

financial reporting model projects in the current environment. In this model include the

following issues in the project of GASB:

Management's Discussion and Analysis

Government Wide Financial Statements

Major Funds

Governmental Fund Financial Statements

Proprietary Fund and Business- Type Activity Financial Statements

Budgetary Comparision

Auditing Model:

It is a model performed for a tasks while conducting due diligence on a model of finance.

The scope of model audit are:

A model's logic review

A contractual and financial documentation model review

Local GAAP and tax model review

A sensitivity review

The purpose of model audit:

The main purpose of this model is to provide assurance for the reliable results. If any

error or omission is detected in this model due to negligence of the auditor's part, then the

organisation depending upon this report may opt model auditor to recover the loss(Russo,

Mitschow and Schinski, 2015).

9

internationally.

P6: Evaluation of models of financial reporting and auditing

Models of financial reporting:

The financial reporting model is the set of structure and content of financial reports

issued by the government (local and state). This model includes the basic financial statements

and its supporting notes and information. In this review of existing standards to ensure that

whether they are meeting the objectives of the company in the present financial reporting

environment(Mir, 2013). The GASB's research gathers the input to help the Board to decide the

financial reporting model projects in the current environment. In this model include the

following issues in the project of GASB:

Management's Discussion and Analysis

Government Wide Financial Statements

Major Funds

Governmental Fund Financial Statements

Proprietary Fund and Business- Type Activity Financial Statements

Budgetary Comparision

Auditing Model:

It is a model performed for a tasks while conducting due diligence on a model of finance.

The scope of model audit are:

A model's logic review

A contractual and financial documentation model review

Local GAAP and tax model review

A sensitivity review

The purpose of model audit:

The main purpose of this model is to provide assurance for the reliable results. If any

error or omission is detected in this model due to negligence of the auditor's part, then the

organisation depending upon this report may opt model auditor to recover the loss(Russo,

Mitschow and Schinski, 2015).

9

Every organisation that prepares financial statements tell a story about the value of

business. Financial statements are the starting point in any appraisal of a business. As financial

statement includes income statement that reflects about activities that are beneficial for Dixons

Carphone. Together with this it matches expenditure and income and shows difference amount as

profits. Balance sheet describes about assets and liabilities in the business. Together with this it

helps in calculating value of the organisation. Ratio analysis in financial statements creates value

of the business by reflecting efficiency of the organisation. Financial statements that are prepared

in business are quite effective to reflect the financial position of Dixons Carphone. Need of

improvement in the financial satement keeps on going with change in budsiness environment on

an on going process.

Consolidation Model: This kind of accounting model basically involve large number of

business unit that are added to individual model. In each kind of business there is one tab that

also contain consolidation tab that mainly sum all the other business unit which support to create

consolidation worksheet. This worksheet help in making more descriptive decision so that

improvement can be made in attainment of goals.

Budget Model: In present time, budget model is used by the professional and finance

manager to make effective financial planning and analysis so that any future business situation

can be resolved in appropriate manner. Budget models are typically designed to be based on

monthly or quarterly figures and focus heavily on the income statement.

LO4

P7: Differences and importance of financial reporting across different countries:

There are many accounting standards in the world, because each country is using its own

version of generally accepted accounting principles (GAAP). These is necessary to maintain

same standard for all companies incorporated in the a country. There are differences in each

country's GAAP with others country due specific conditions and situations which lies within the

boundary of each country. For understanding its differences and importance, financial reporting

standards of two country should be taken which is as follows:

International Financial Reporting Standards (IFRS)

US GAAP

Differences between IFRS and US GAAP:

10

business. Financial statements are the starting point in any appraisal of a business. As financial

statement includes income statement that reflects about activities that are beneficial for Dixons

Carphone. Together with this it matches expenditure and income and shows difference amount as

profits. Balance sheet describes about assets and liabilities in the business. Together with this it

helps in calculating value of the organisation. Ratio analysis in financial statements creates value

of the business by reflecting efficiency of the organisation. Financial statements that are prepared

in business are quite effective to reflect the financial position of Dixons Carphone. Need of

improvement in the financial satement keeps on going with change in budsiness environment on

an on going process.

Consolidation Model: This kind of accounting model basically involve large number of

business unit that are added to individual model. In each kind of business there is one tab that

also contain consolidation tab that mainly sum all the other business unit which support to create

consolidation worksheet. This worksheet help in making more descriptive decision so that

improvement can be made in attainment of goals.

Budget Model: In present time, budget model is used by the professional and finance

manager to make effective financial planning and analysis so that any future business situation

can be resolved in appropriate manner. Budget models are typically designed to be based on

monthly or quarterly figures and focus heavily on the income statement.

LO4

P7: Differences and importance of financial reporting across different countries:

There are many accounting standards in the world, because each country is using its own

version of generally accepted accounting principles (GAAP). These is necessary to maintain

same standard for all companies incorporated in the a country. There are differences in each

country's GAAP with others country due specific conditions and situations which lies within the

boundary of each country. For understanding its differences and importance, financial reporting

standards of two country should be taken which is as follows:

International Financial Reporting Standards (IFRS)

US GAAP

Differences between IFRS and US GAAP:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.