Accounts 506: Comprehensive Financial Statement Analysis Report

VerifiedAdded on 2024/05/29

|11

|1618

|265

Report

AI Summary

This report presents a comprehensive financial analysis for Accounts 506, including adjustment entries, closing entries, and an adjusted trial balance. It features an income statement, statement of retained earnings, balance sheet, and common-size comparative balance sheet. Ratio analysis, including net profit ratio, return on assets, and return on equity, is performed to assess the company's financial health. The report also discusses strategies to improve the financial position, such as depreciation methods and inventory valuation, and addresses organizational structure and economic factors affecting the business. Desklib offers a wide range of solved assignments and past papers to aid students in their studies.

Accounts 506

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

2. Adjustment entries:..................................................................................................................2

3. Closing entries:........................................................................................................................3

4. Adjusted trial balance:.............................................................................................................4

5...................................................................................................................................................5

a. Income statement..................................................................................................................5

b. Statement of retained Earnings:............................................................................................5

C & d. Balance-sheet and comparative balance-sheet.................................................................6

e. Common-size Comparative balance sheet...............................................................................7

6. Ratio analysis:..........................................................................................................................8

7...................................................................................................................................................9

a. Improve the financial position..............................................................................................9

b. Ratio analysis:.......................................................................................................................9

c. Comparative balance sheet and common-size comparative balance sheet.........................10

d. Other issues:........................................................................................................................10

2. Adjustment entries:..................................................................................................................2

3. Closing entries:........................................................................................................................3

4. Adjusted trial balance:.............................................................................................................4

5...................................................................................................................................................5

a. Income statement..................................................................................................................5

b. Statement of retained Earnings:............................................................................................5

C & d. Balance-sheet and comparative balance-sheet.................................................................6

e. Common-size Comparative balance sheet...............................................................................7

6. Ratio analysis:..........................................................................................................................8

7...................................................................................................................................................9

a. Improve the financial position..............................................................................................9

b. Ratio analysis:.......................................................................................................................9

c. Comparative balance sheet and common-size comparative balance sheet.........................10

d. Other issues:........................................................................................................................10

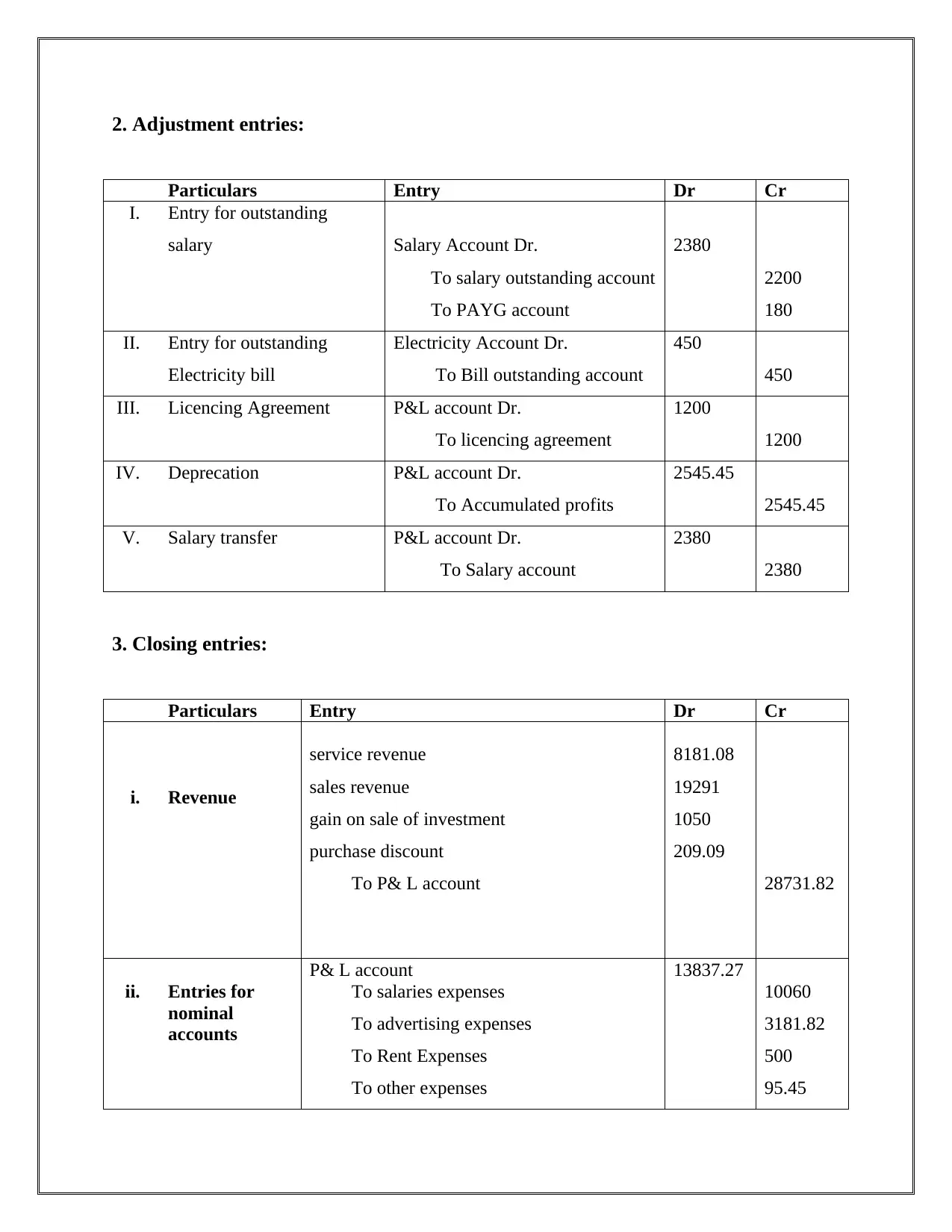

2. Adjustment entries:

Particulars Entry Dr Cr

I. Entry for outstanding

salary Salary Account Dr.

To salary outstanding account

To PAYG account

2380

2200

180

II. Entry for outstanding

Electricity bill

Electricity Account Dr.

To Bill outstanding account

450

450

III. Licencing Agreement P&L account Dr.

To licencing agreement

1200

1200

IV. Deprecation P&L account Dr.

To Accumulated profits

2545.45

2545.45

V. Salary transfer P&L account Dr.

To Salary account

2380

2380

3. Closing entries:

Particulars Entry Dr Cr

i. Revenue

service revenue

sales revenue

gain on sale of investment

purchase discount

To P& L account

8181.08

19291

1050

209.09

28731.82

ii. Entries for

nominal

accounts

P& L account

To salaries expenses

To advertising expenses

To Rent Expenses

To other expenses

13837.27

10060

3181.82

500

95.45

Particulars Entry Dr Cr

I. Entry for outstanding

salary Salary Account Dr.

To salary outstanding account

To PAYG account

2380

2200

180

II. Entry for outstanding

Electricity bill

Electricity Account Dr.

To Bill outstanding account

450

450

III. Licencing Agreement P&L account Dr.

To licencing agreement

1200

1200

IV. Deprecation P&L account Dr.

To Accumulated profits

2545.45

2545.45

V. Salary transfer P&L account Dr.

To Salary account

2380

2380

3. Closing entries:

Particulars Entry Dr Cr

i. Revenue

service revenue

sales revenue

gain on sale of investment

purchase discount

To P& L account

8181.08

19291

1050

209.09

28731.82

ii. Entries for

nominal

accounts

P& L account

To salaries expenses

To advertising expenses

To Rent Expenses

To other expenses

13837.27

10060

3181.82

500

95.45

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

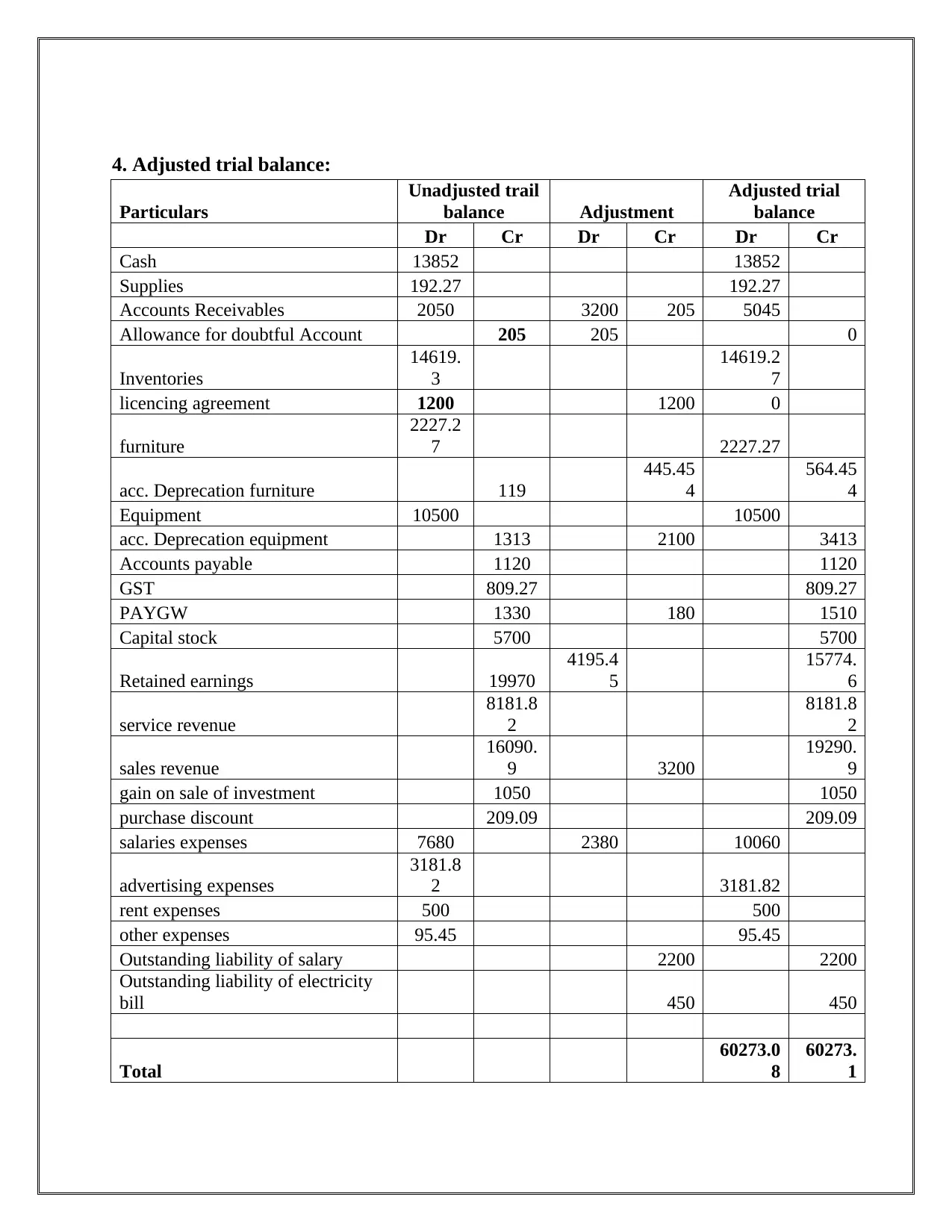

4. Adjusted trial balance:

Particulars

Unadjusted trail

balance Adjustment

Adjusted trial

balance

Dr Cr Dr Cr Dr Cr

Cash 13852 13852

Supplies 192.27 192.27

Accounts Receivables 2050 3200 205 5045

Allowance for doubtful Account 205 205 0

Inventories

14619.

3

14619.2

7

licencing agreement 1200 1200 0

furniture

2227.2

7 2227.27

acc. Deprecation furniture 119

445.45

4

564.45

4

Equipment 10500 10500

acc. Deprecation equipment 1313 2100 3413

Accounts payable 1120 1120

GST 809.27 809.27

PAYGW 1330 180 1510

Capital stock 5700 5700

Retained earnings 19970

4195.4

5

15774.

6

service revenue

8181.8

2

8181.8

2

sales revenue

16090.

9 3200

19290.

9

gain on sale of investment 1050 1050

purchase discount 209.09 209.09

salaries expenses 7680 2380 10060

advertising expenses

3181.8

2 3181.82

rent expenses 500 500

other expenses 95.45 95.45

Outstanding liability of salary 2200 2200

Outstanding liability of electricity

bill 450 450

Total

60273.0

8

60273.

1

Particulars

Unadjusted trail

balance Adjustment

Adjusted trial

balance

Dr Cr Dr Cr Dr Cr

Cash 13852 13852

Supplies 192.27 192.27

Accounts Receivables 2050 3200 205 5045

Allowance for doubtful Account 205 205 0

Inventories

14619.

3

14619.2

7

licencing agreement 1200 1200 0

furniture

2227.2

7 2227.27

acc. Deprecation furniture 119

445.45

4

564.45

4

Equipment 10500 10500

acc. Deprecation equipment 1313 2100 3413

Accounts payable 1120 1120

GST 809.27 809.27

PAYGW 1330 180 1510

Capital stock 5700 5700

Retained earnings 19970

4195.4

5

15774.

6

service revenue

8181.8

2

8181.8

2

sales revenue

16090.

9 3200

19290.

9

gain on sale of investment 1050 1050

purchase discount 209.09 209.09

salaries expenses 7680 2380 10060

advertising expenses

3181.8

2 3181.82

rent expenses 500 500

other expenses 95.45 95.45

Outstanding liability of salary 2200 2200

Outstanding liability of electricity

bill 450 450

Total

60273.0

8

60273.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

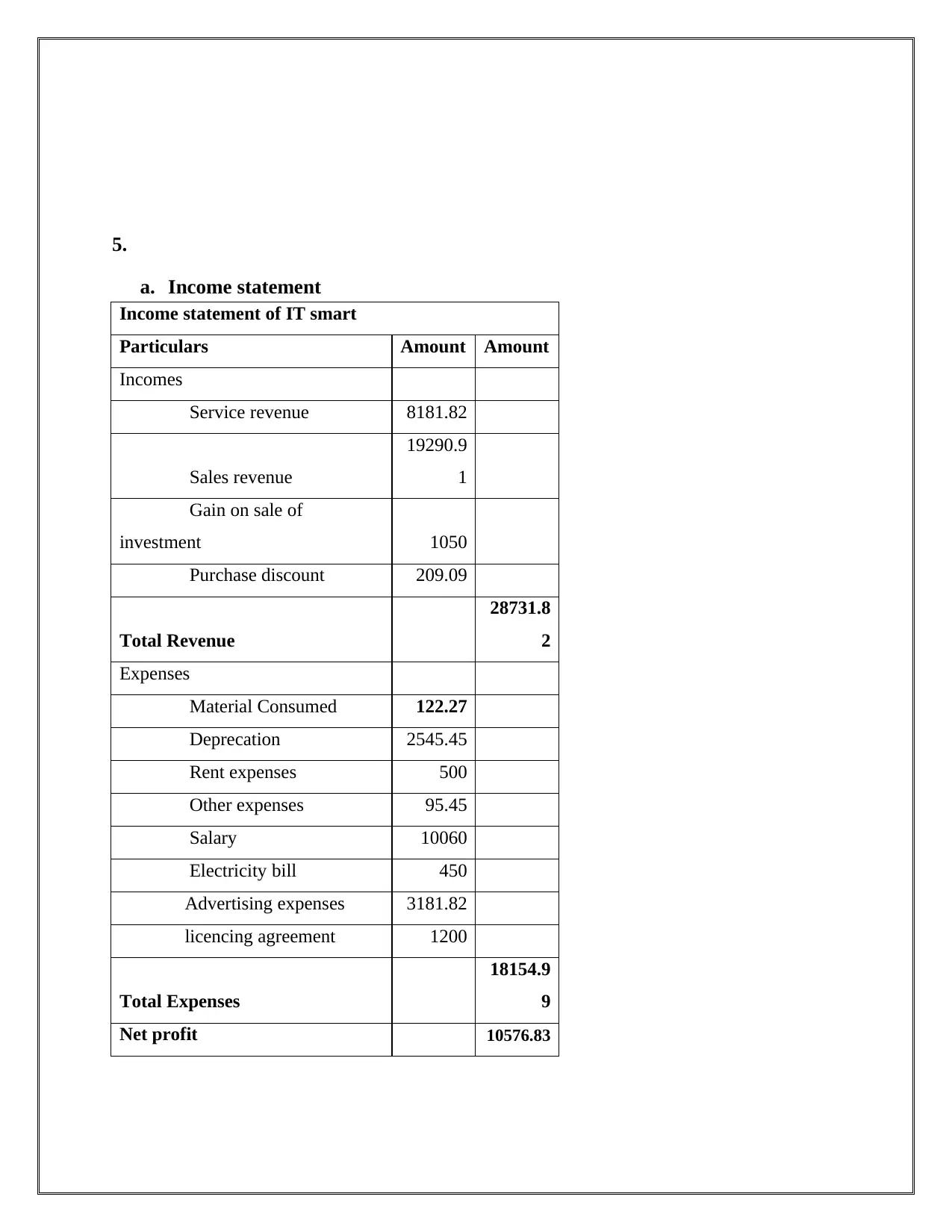

5.

a. Income statement

Income statement of IT smart

Particulars Amount Amount

Incomes

Service revenue 8181.82

Sales revenue

19290.9

1

Gain on sale of

investment 1050

Purchase discount 209.09

Total Revenue

28731.8

2

Expenses

Material Consumed 122.27

Deprecation 2545.45

Rent expenses 500

Other expenses 95.45

Salary 10060

Electricity bill 450

Advertising expenses 3181.82

licencing agreement 1200

Total Expenses

18154.9

9

Net profit 10576.83

a. Income statement

Income statement of IT smart

Particulars Amount Amount

Incomes

Service revenue 8181.82

Sales revenue

19290.9

1

Gain on sale of

investment 1050

Purchase discount 209.09

Total Revenue

28731.8

2

Expenses

Material Consumed 122.27

Deprecation 2545.45

Rent expenses 500

Other expenses 95.45

Salary 10060

Electricity bill 450

Advertising expenses 3181.82

licencing agreement 1200

Total Expenses

18154.9

9

Net profit 10576.83

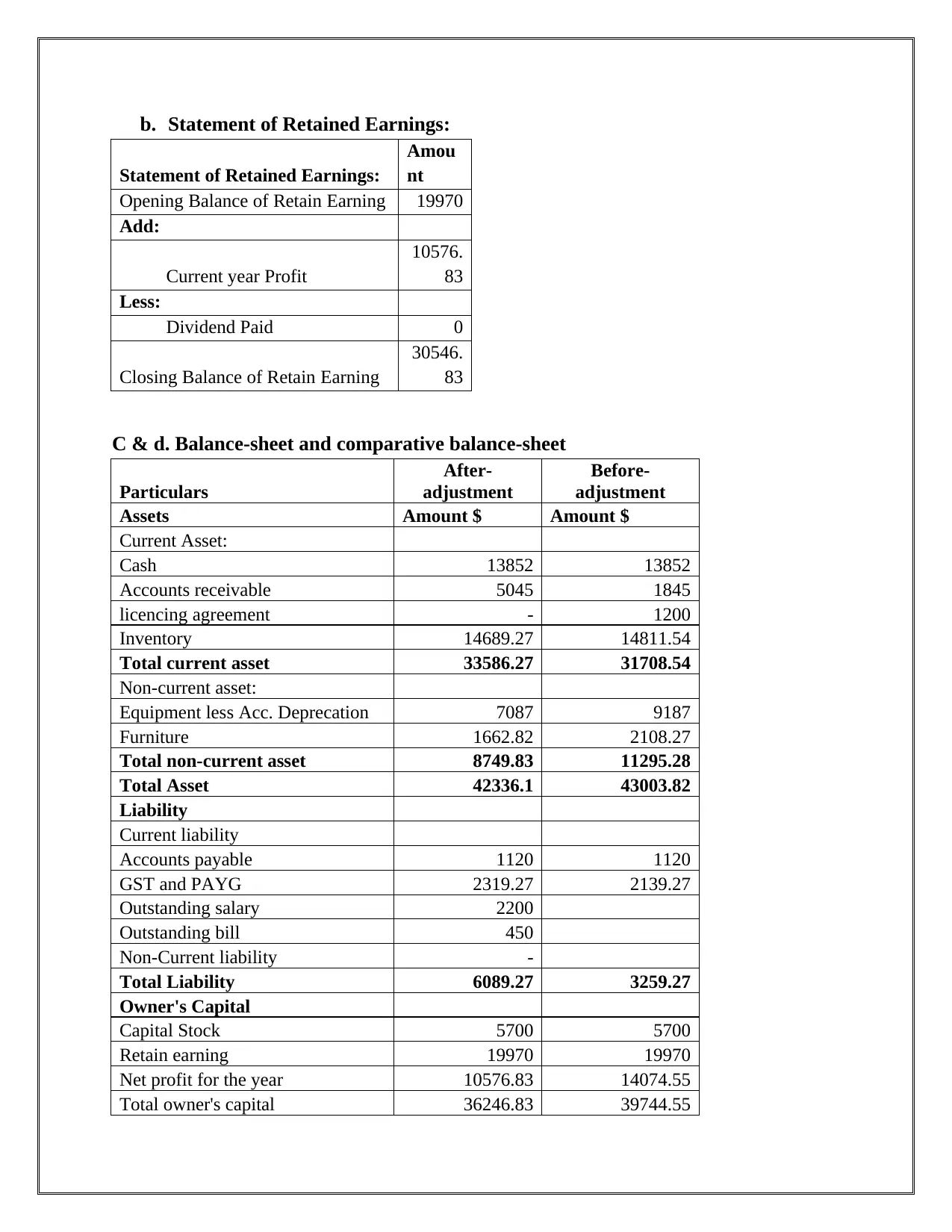

b. Statement of Retained Earnings:

Statement of Retained Earnings:

Amou

nt

Opening Balance of Retain Earning 19970

Add:

Current year Profit

10576.

83

Less:

Dividend Paid 0

Closing Balance of Retain Earning

30546.

83

C & d. Balance-sheet and comparative balance-sheet

Particulars

After-

adjustment

Before-

adjustment

Assets Amount $ Amount $

Current Asset:

Cash 13852 13852

Accounts receivable 5045 1845

licencing agreement - 1200

Inventory 14689.27 14811.54

Total current asset 33586.27 31708.54

Non-current asset:

Equipment less Acc. Deprecation 7087 9187

Furniture 1662.82 2108.27

Total non-current asset 8749.83 11295.28

Total Asset 42336.1 43003.82

Liability

Current liability

Accounts payable 1120 1120

GST and PAYG 2319.27 2139.27

Outstanding salary 2200

Outstanding bill 450

Non-Current liability -

Total Liability 6089.27 3259.27

Owner's Capital

Capital Stock 5700 5700

Retain earning 19970 19970

Net profit for the year 10576.83 14074.55

Total owner's capital 36246.83 39744.55

Statement of Retained Earnings:

Amou

nt

Opening Balance of Retain Earning 19970

Add:

Current year Profit

10576.

83

Less:

Dividend Paid 0

Closing Balance of Retain Earning

30546.

83

C & d. Balance-sheet and comparative balance-sheet

Particulars

After-

adjustment

Before-

adjustment

Assets Amount $ Amount $

Current Asset:

Cash 13852 13852

Accounts receivable 5045 1845

licencing agreement - 1200

Inventory 14689.27 14811.54

Total current asset 33586.27 31708.54

Non-current asset:

Equipment less Acc. Deprecation 7087 9187

Furniture 1662.82 2108.27

Total non-current asset 8749.83 11295.28

Total Asset 42336.1 43003.82

Liability

Current liability

Accounts payable 1120 1120

GST and PAYG 2319.27 2139.27

Outstanding salary 2200

Outstanding bill 450

Non-Current liability -

Total Liability 6089.27 3259.27

Owner's Capital

Capital Stock 5700 5700

Retain earning 19970 19970

Net profit for the year 10576.83 14074.55

Total owner's capital 36246.83 39744.55

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total liabilities and owner's

capital 42336.1 43003.82

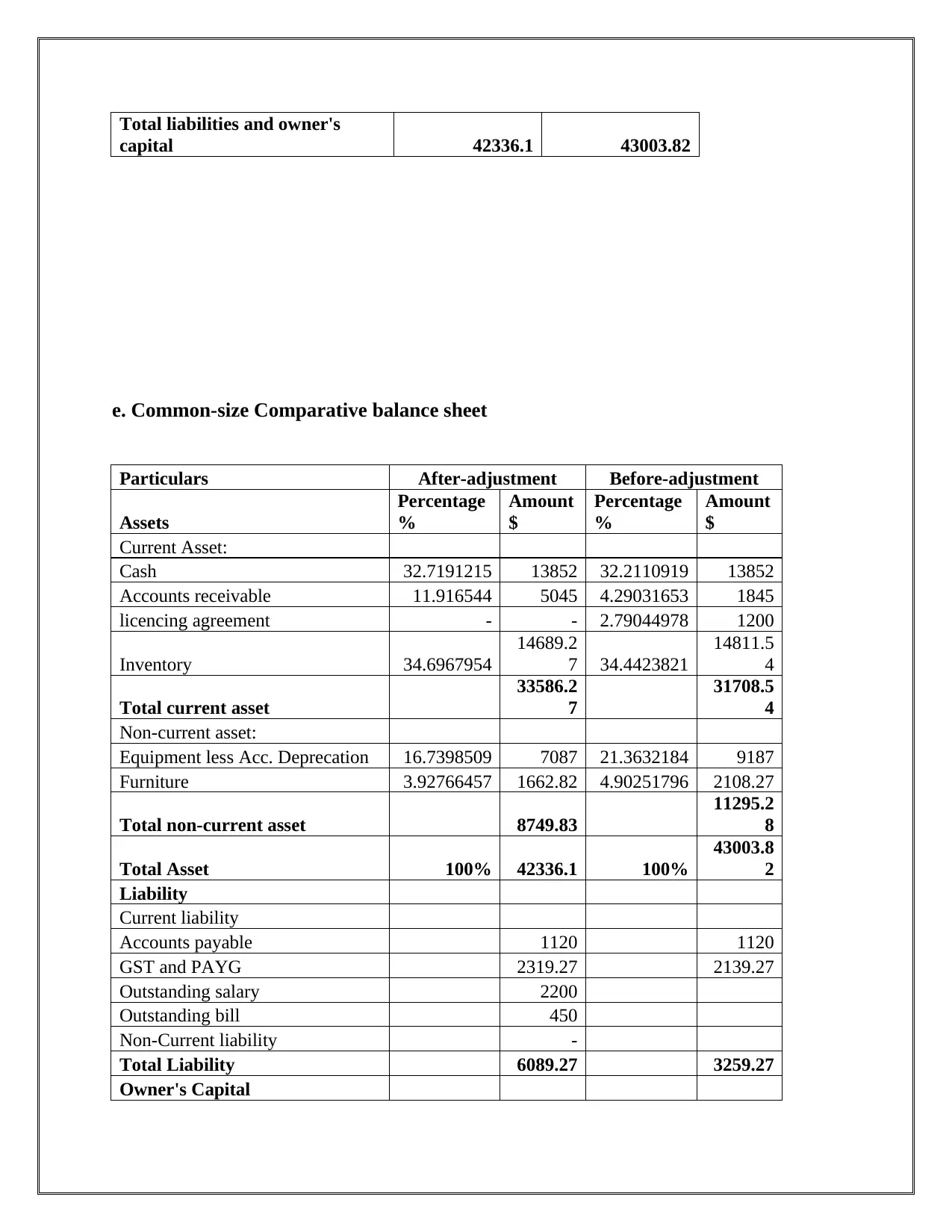

e. Common-size Comparative balance sheet

Particulars After-adjustment Before-adjustment

Assets

Percentage

%

Amount

$

Percentage

%

Amount

$

Current Asset:

Cash 32.7191215 13852 32.2110919 13852

Accounts receivable 11.916544 5045 4.29031653 1845

licencing agreement - - 2.79044978 1200

Inventory 34.6967954

14689.2

7 34.4423821

14811.5

4

Total current asset

33586.2

7

31708.5

4

Non-current asset:

Equipment less Acc. Deprecation 16.7398509 7087 21.3632184 9187

Furniture 3.92766457 1662.82 4.90251796 2108.27

Total non-current asset 8749.83

11295.2

8

Total Asset 100% 42336.1 100%

43003.8

2

Liability

Current liability

Accounts payable 1120 1120

GST and PAYG 2319.27 2139.27

Outstanding salary 2200

Outstanding bill 450

Non-Current liability -

Total Liability 6089.27 3259.27

Owner's Capital

capital 42336.1 43003.82

e. Common-size Comparative balance sheet

Particulars After-adjustment Before-adjustment

Assets

Percentage

%

Amount

$

Percentage

%

Amount

$

Current Asset:

Cash 32.7191215 13852 32.2110919 13852

Accounts receivable 11.916544 5045 4.29031653 1845

licencing agreement - - 2.79044978 1200

Inventory 34.6967954

14689.2

7 34.4423821

14811.5

4

Total current asset

33586.2

7

31708.5

4

Non-current asset:

Equipment less Acc. Deprecation 16.7398509 7087 21.3632184 9187

Furniture 3.92766457 1662.82 4.90251796 2108.27

Total non-current asset 8749.83

11295.2

8

Total Asset 100% 42336.1 100%

43003.8

2

Liability

Current liability

Accounts payable 1120 1120

GST and PAYG 2319.27 2139.27

Outstanding salary 2200

Outstanding bill 450

Non-Current liability -

Total Liability 6089.27 3259.27

Owner's Capital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital Stock 5700 5700

Retain earning 19970 19970

Net profit for the year

10576.8

3

14074.5

5

Total owner's capital

36246.8

3

39744.5

5

Total liabilities and owner's

capital 42336.1

43003.8

2

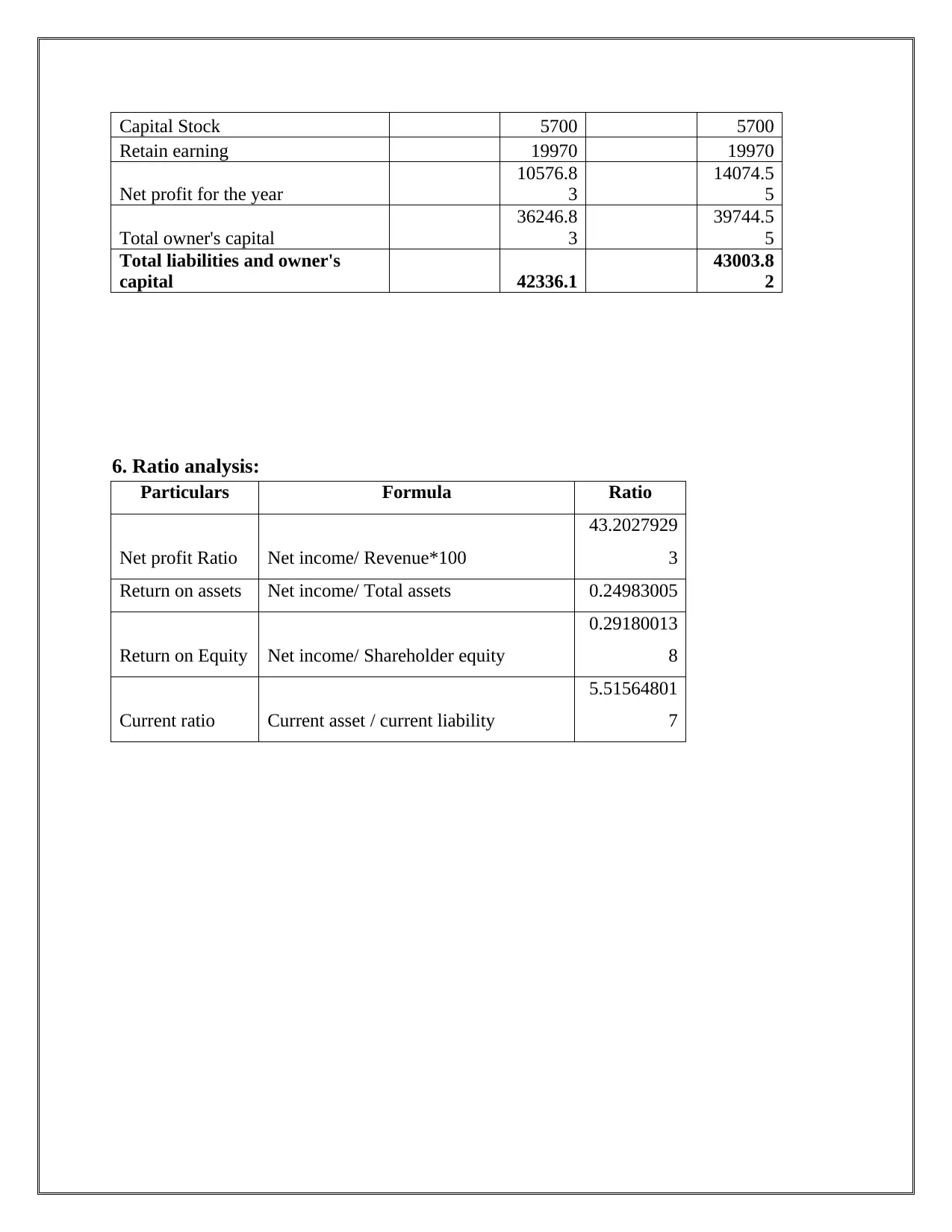

6. Ratio analysis:

Particulars Formula Ratio

Net profit Ratio Net income/ Revenue*100

43.2027929

3

Return on assets Net income/ Total assets 0.24983005

Return on Equity Net income/ Shareholder equity

0.29180013

8

Current ratio Current asset / current liability

5.51564801

7

Retain earning 19970 19970

Net profit for the year

10576.8

3

14074.5

5

Total owner's capital

36246.8

3

39744.5

5

Total liabilities and owner's

capital 42336.1

43003.8

2

6. Ratio analysis:

Particulars Formula Ratio

Net profit Ratio Net income/ Revenue*100

43.2027929

3

Return on assets Net income/ Total assets 0.24983005

Return on Equity Net income/ Shareholder equity

0.29180013

8

Current ratio Current asset / current liability

5.51564801

7

7.

a. Improve the financial position

Deprecation: various alternative approaches are available for the recording of

depreciation. In the present case, IT smart is using Stateline method for the calculation of

depreciation. The organisation can use WDV method to compute the depreciation and

which more comparable method of valuation. The organisation can write off its

accumulated depreciation to ensure the better representation of financial statement.

Inventory: for the valuation of inventory various method are available like FIFO, LIFO

and weighted average. For the better representation and practical valuation, the company

should use FIFO or weighted average method.

Uncollectable: uncollectable or bad debts are those amounts which are not receivable for

a business organisation. The organisation should make appropriate allowance reserve for

bad-debts.

b. Ratio analysis:

Net profit ratio: net profit ratio is a profitability measurement ratio which denotes the

net margin of an organisation. A higher ratio denotes the higher profitability and a low

profitability ratio shows that currently, the organisation does not make enough profits. In

a. Improve the financial position

Deprecation: various alternative approaches are available for the recording of

depreciation. In the present case, IT smart is using Stateline method for the calculation of

depreciation. The organisation can use WDV method to compute the depreciation and

which more comparable method of valuation. The organisation can write off its

accumulated depreciation to ensure the better representation of financial statement.

Inventory: for the valuation of inventory various method are available like FIFO, LIFO

and weighted average. For the better representation and practical valuation, the company

should use FIFO or weighted average method.

Uncollectable: uncollectable or bad debts are those amounts which are not receivable for

a business organisation. The organisation should make appropriate allowance reserve for

bad-debts.

b. Ratio analysis:

Net profit ratio: net profit ratio is a profitability measurement ratio which denotes the

net margin of an organisation. A higher ratio denotes the higher profitability and a low

profitability ratio shows that currently, the organisation does not make enough profits. In

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the current situation, IT smart is reporting 43.20% profit margin ratio which is a great

level and it proves that company is doing good.

Return on asset: ROA denotes the profitability of an entity on the basis of total assets

and earning. This ratio reports that how efficiently a company earning profits by using its

assets. A higher percentage of ROA shows that company is doing well and a low ROA

means high-value assets are introduced but returns are very low. In the case of IT smart,

the company is reporting 24.95% ROA which is a good situation.

Return on equity: ROE is used to determinate that how much return an organisation

currently earing by introducing one dollar as capital. It is also a profitability ratio and

also used to find the efficiency of business operations. In the current situation, IT smart

is reporting 29.18% ROE which is good sigh and proves the efficiency of company

operations.

c. Comparative balance sheet and common-size comparative balance sheet

Comparative balance sheet:

The comparative statement can be defined as the document which is used to compare the

previous financial results of an organisation with current year financial results or financial results

of an organisation with a different organisation.

The comparative balance sheet is a financial statement which denotes the financial situation of an

organisation along with previous year financial data to enable the user to understand the financial

situation of that organisation.

The specified format of the comparative balance sheet is notified for the companies and it is very

useful because it shows the comparison between two years so that a user can easily understand

the financial trend of organisation and can take appropriate decisions.

Common-Size comparative balance sheet:

The common-size balance sheet also shows the financial situation of an organisation but it

includes an additional column which denotes the percentage of each asset side item against ‘total

asset’ and percentage of each liability side item against ‘total liability and owner’s capital’.

level and it proves that company is doing good.

Return on asset: ROA denotes the profitability of an entity on the basis of total assets

and earning. This ratio reports that how efficiently a company earning profits by using its

assets. A higher percentage of ROA shows that company is doing well and a low ROA

means high-value assets are introduced but returns are very low. In the case of IT smart,

the company is reporting 24.95% ROA which is a good situation.

Return on equity: ROE is used to determinate that how much return an organisation

currently earing by introducing one dollar as capital. It is also a profitability ratio and

also used to find the efficiency of business operations. In the current situation, IT smart

is reporting 29.18% ROE which is good sigh and proves the efficiency of company

operations.

c. Comparative balance sheet and common-size comparative balance sheet

Comparative balance sheet:

The comparative statement can be defined as the document which is used to compare the

previous financial results of an organisation with current year financial results or financial results

of an organisation with a different organisation.

The comparative balance sheet is a financial statement which denotes the financial situation of an

organisation along with previous year financial data to enable the user to understand the financial

situation of that organisation.

The specified format of the comparative balance sheet is notified for the companies and it is very

useful because it shows the comparison between two years so that a user can easily understand

the financial trend of organisation and can take appropriate decisions.

Common-Size comparative balance sheet:

The common-size balance sheet also shows the financial situation of an organisation but it

includes an additional column which denotes the percentage of each asset side item against ‘total

asset’ and percentage of each liability side item against ‘total liability and owner’s capital’.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It works like a tool in the comparison of financial data and gives more significant information so

that user can make more suitable and logical decisions. This format is also very useful in

benchmarking study. An entity can make a comparison of own financial situation with industry

trends without extra efforts and clerical work. Common size comparative balance sheets are not

necessary under Accounting rules or GAAP but sometimes it works like helping hand for the

managers of an organisation.

d. Other issues:

Organisational structure: organisational structure can be defined as the allocation of

management powers and ways of information transfer within an organisation. An

appropriate distribution of powers is must to ensure the sustainable success of the

organisation. If an entity does not have appropriate organisational structure, it will

enhance the chances of fraud, misuse of powers and losses which may affect the

sustainability of entity.

Economic factors: economic factors are macro-environmental factors and directly have

an impact on the profitability of businesses. It may be adverse or favourable. Economic

factors like foreign exchange rate also have a serious impact on the performance of an

organisation. These factors are uncontrollable for a business organisation.

Staff ability: the ability of staff also affects the performance of an organisation. If an

entity has skilled and satisfied employees along with happy working environment, it will

enhance the productivity of staff and make a profit for the organisation.

that user can make more suitable and logical decisions. This format is also very useful in

benchmarking study. An entity can make a comparison of own financial situation with industry

trends without extra efforts and clerical work. Common size comparative balance sheets are not

necessary under Accounting rules or GAAP but sometimes it works like helping hand for the

managers of an organisation.

d. Other issues:

Organisational structure: organisational structure can be defined as the allocation of

management powers and ways of information transfer within an organisation. An

appropriate distribution of powers is must to ensure the sustainable success of the

organisation. If an entity does not have appropriate organisational structure, it will

enhance the chances of fraud, misuse of powers and losses which may affect the

sustainability of entity.

Economic factors: economic factors are macro-environmental factors and directly have

an impact on the profitability of businesses. It may be adverse or favourable. Economic

factors like foreign exchange rate also have a serious impact on the performance of an

organisation. These factors are uncontrollable for a business organisation.

Staff ability: the ability of staff also affects the performance of an organisation. If an

entity has skilled and satisfied employees along with happy working environment, it will

enhance the productivity of staff and make a profit for the organisation.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.