Corporate Accounting Report: Rio Tinto Financial Statement Analysis

VerifiedAdded on 2021/06/16

|15

|3165

|98

Report

AI Summary

This report provides a detailed analysis of Rio Tinto's financial statements, focusing on the years 2015, 2016, and 2017. It examines the company's cash flow statement, including operating, investing, and financing activities, highlighting significant changes and trends. The analysis covers the direct method of cash flow preparation, revenue generation, and the impact of various transactions on cash and cash equivalents. Furthermore, the report explores the other comprehensive income statement, detailing its components and the reasons for their inclusion. It also addresses accounting for income tax, specifically deferred tax assets and liabilities, providing explanations for their recording and implications. The report concludes with an overview of the company's financial performance and position over the analyzed period, offering insights into its accounting practices.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author Note

Corporate Accounting

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Cash Flow Statement.......................................................................................................................3

Other Comprehensive Income Statement........................................................................................7

Accounting for Income tax:.............................................................................................................9

Conclusion:....................................................................................................................................10

References:....................................................................................................................................11

Appendix........................................................................................................................................13

CORPORATE ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Cash Flow Statement.......................................................................................................................3

Other Comprehensive Income Statement........................................................................................7

Accounting for Income tax:.............................................................................................................9

Conclusion:....................................................................................................................................10

References:....................................................................................................................................11

Appendix........................................................................................................................................13

2

CORPORATE ACCOUNTING

Introduction

The present report is centred on the analysis of the financial statements of a specific

chosen company. The purpose of conducting the analysis of the financial statement will be to

determine whether the reports that are being prepared and presented by the company for the

consideration of the stakeholders, are showing the true and fair view of the entity or not. The

various elements or constituents of the financial statements are to be analysed which includes the

company’s cash flow statement, the income statement and the balance sheet.

Rio Tinto is the company that has been chosen for the given purpose. The main activities

of the entity include mining and metals. By making use of its whole range of subsidiaries, the

company conducts its own mining operations. 2015, 2016 and 2017 are the three years over the

period of which the financial statements of the company will be analysed with respect to the

performance recorded by it and its financial position (Gordon et al. 2017). The position of the

company and the performance of the company over the years will be analysed over the period of

these three years.

.

CORPORATE ACCOUNTING

Introduction

The present report is centred on the analysis of the financial statements of a specific

chosen company. The purpose of conducting the analysis of the financial statement will be to

determine whether the reports that are being prepared and presented by the company for the

consideration of the stakeholders, are showing the true and fair view of the entity or not. The

various elements or constituents of the financial statements are to be analysed which includes the

company’s cash flow statement, the income statement and the balance sheet.

Rio Tinto is the company that has been chosen for the given purpose. The main activities

of the entity include mining and metals. By making use of its whole range of subsidiaries, the

company conducts its own mining operations. 2015, 2016 and 2017 are the three years over the

period of which the financial statements of the company will be analysed with respect to the

performance recorded by it and its financial position (Gordon et al. 2017). The position of the

company and the performance of the company over the years will be analysed over the period of

these three years.

.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

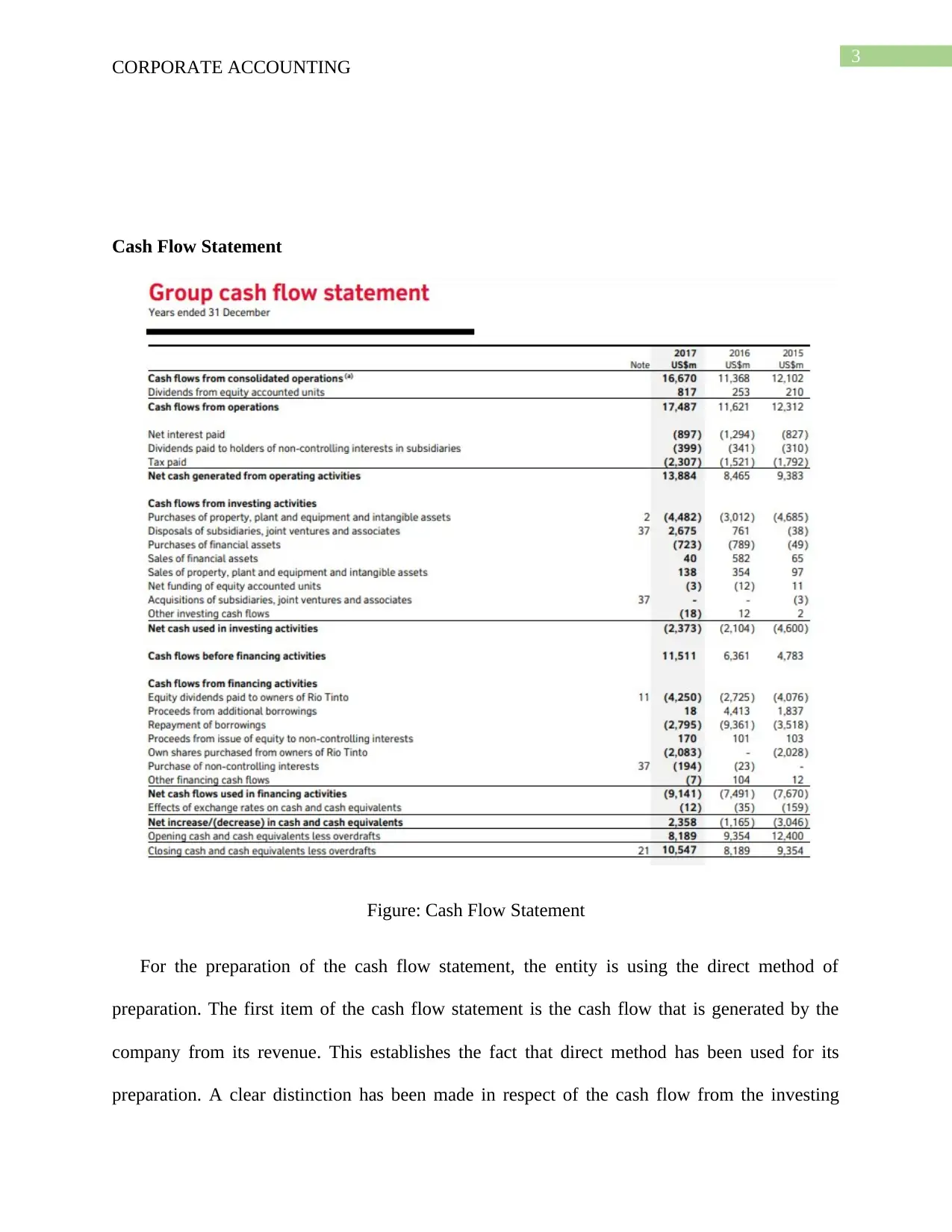

Cash Flow Statement

Figure: Cash Flow Statement

For the preparation of the cash flow statement, the entity is using the direct method of

preparation. The first item of the cash flow statement is the cash flow that is generated by the

company from its revenue. This establishes the fact that direct method has been used for its

preparation. A clear distinction has been made in respect of the cash flow from the investing

CORPORATE ACCOUNTING

Cash Flow Statement

Figure: Cash Flow Statement

For the preparation of the cash flow statement, the entity is using the direct method of

preparation. The first item of the cash flow statement is the cash flow that is generated by the

company from its revenue. This establishes the fact that direct method has been used for its

preparation. A clear distinction has been made in respect of the cash flow from the investing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

activities, operating activities and the financing activities. The operating activities of the

company refers to the amount of cash flow that is being generated by the company form the core

business operations that are being conducted by it (Miao et al. 2016). The cash flow from

investing activities refer to the cash flow that is being generated in the favour of the company by

the sale and purchase of the fixed assets of the company and the various other investments that

are being made by the company. the cash flow generated or the outflow incurred by the company

under the head financing activities refer to the various payments that are being made by the

entity in respect of the interest payment and other obligatory payments that are incurred by the

entity in respect fo the various sources of finance that are arranged by the company. Like interest

payments in respect of the borrowings, dividend from the shares of the company and fixed rate

of payments that are being made to the preference shares (Reid and Myddelton 2017). The

various individual components of the cash flow statements of the entity are as follows:

a) Receipt from consolidate operations- this item represents that cash flow that has been

generated from the principle revenue generating activities of the entity.

b) Dividends from equity oriented units- this item represents the amount that has been

received by the company in the form of dividend from the various other companies in

which the company has made investment.

c) Net interest paid- this item represents the net interest that is received by the company.

The net interest is computed by deducting the interest expense incurred by the company

from the interest revenue that is being generated by the company (Grant 2016).

d) Interest paid to holders of non-controlling interest in the subsidiaries- this item represents

the amount that is paid to the shareholders of the subsidiary companies of the group who

hold a non-controlling interest in the company.

CORPORATE ACCOUNTING

activities, operating activities and the financing activities. The operating activities of the

company refers to the amount of cash flow that is being generated by the company form the core

business operations that are being conducted by it (Miao et al. 2016). The cash flow from

investing activities refer to the cash flow that is being generated in the favour of the company by

the sale and purchase of the fixed assets of the company and the various other investments that

are being made by the company. the cash flow generated or the outflow incurred by the company

under the head financing activities refer to the various payments that are being made by the

entity in respect of the interest payment and other obligatory payments that are incurred by the

entity in respect fo the various sources of finance that are arranged by the company. Like interest

payments in respect of the borrowings, dividend from the shares of the company and fixed rate

of payments that are being made to the preference shares (Reid and Myddelton 2017). The

various individual components of the cash flow statements of the entity are as follows:

a) Receipt from consolidate operations- this item represents that cash flow that has been

generated from the principle revenue generating activities of the entity.

b) Dividends from equity oriented units- this item represents the amount that has been

received by the company in the form of dividend from the various other companies in

which the company has made investment.

c) Net interest paid- this item represents the net interest that is received by the company.

The net interest is computed by deducting the interest expense incurred by the company

from the interest revenue that is being generated by the company (Grant 2016).

d) Interest paid to holders of non-controlling interest in the subsidiaries- this item represents

the amount that is paid to the shareholders of the subsidiary companies of the group who

hold a non-controlling interest in the company.

5

CORPORATE ACCOUNTING

e) Taxes paid – this item comprises of the total amount that is being paid by the company

towards taxes.

f) Purchase of property, plant and equipment and intangible assets by the company- this

represents that amount that is incurred by the company for acquiring the essential

property, plant and equipment that are going to be used by the company or the production

of its products and the generation of the revenue (Penman and Yehuda 2015).

g) Disposals of subsidiaries, joint ventures and associates- this item represents the amount

that is being realised by the company in respect of the sale of the subsidiaries, joint

ventures and the associates that are held by the company.

h) Purchase and sale of financial assets- this item represents the net amount that is realised

by the company in respect of the sale of the fixed financial assets of the company and the

reduction to be made from it in respect of the purchase of the fixed financial assets by the

company (Robinson et al. 2015).

i) Sale of property, plant, equipment and intangibles- this item represents the amount that

the company has generated from the sale of the property, plant, equipment and the

intangibles of the company.

j) Equity dividends paid to owner of the Rio Tinto- this item represents that the

shareholders of the company have received from it as dividend.

k) Proceeds from additional borrowings- this item represents the amount that the company

has collected from the various third parties and the financial institutions in the form of

debt.

CORPORATE ACCOUNTING

e) Taxes paid – this item comprises of the total amount that is being paid by the company

towards taxes.

f) Purchase of property, plant and equipment and intangible assets by the company- this

represents that amount that is incurred by the company for acquiring the essential

property, plant and equipment that are going to be used by the company or the production

of its products and the generation of the revenue (Penman and Yehuda 2015).

g) Disposals of subsidiaries, joint ventures and associates- this item represents the amount

that is being realised by the company in respect of the sale of the subsidiaries, joint

ventures and the associates that are held by the company.

h) Purchase and sale of financial assets- this item represents the net amount that is realised

by the company in respect of the sale of the fixed financial assets of the company and the

reduction to be made from it in respect of the purchase of the fixed financial assets by the

company (Robinson et al. 2015).

i) Sale of property, plant, equipment and intangibles- this item represents the amount that

the company has generated from the sale of the property, plant, equipment and the

intangibles of the company.

j) Equity dividends paid to owner of the Rio Tinto- this item represents that the

shareholders of the company have received from it as dividend.

k) Proceeds from additional borrowings- this item represents the amount that the company

has collected from the various third parties and the financial institutions in the form of

debt.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

l) Proceeds from the issue of equity to non-controlling interests- this item represents the

amount that has been contributed to the company by the shareholders who hold a non-

controlling interest in the company by way of subscribing the shares of the company.

m) Own shares purchased from the owners of the Rio Tinto- this item represents the amount

that the company has paid to shareholders of the company in respect of buying back the

equity shares that were previously being allocated to them (Harris 2016).

Over the period of three years, the revenue that has been generated from the operating activities

of the company has increased significantly. This has occurred because FO the fact that the

revenue of the company has increased significantly during these three years. The amount that

was received by the company from the primary revenue generating activities of the company for

the ear 2015 and 2017 amounted to US$ 12102 and US$ 16670 respectively (Lin et al. 2015).

This demonstrates the significant rise that has occurred in the revenue of the entity. Lot of

fluctuations have occurred in the investing activities of the company. The amount of the outflows

of the cash from the investing activities of the company amounted to (US 4600) and (US 2104)

respectively for the year 2015 and 2016 respectively. The purchase made by the company in

respect of the property, plant and equipment of the company has reduced significantly over the

years. This has resulted in the cash outflow from the investing activities of the company being

reduced over this period (Banker et al. 2016). The reduction of the flow from the investing

activates was further pushed by the increase in the sale of the financial assets of the company.

The decrease in the cash flow of the company can be because FO the fact that the company has

incurred no amount in respect of purchasing the issued shares of the company back from the

shareholders of the company. The company had also taken up huge borrowings from outsiders in

the year 2016 and this has increased the cash inflow of the company. In the year, 2016 and 2017

CORPORATE ACCOUNTING

l) Proceeds from the issue of equity to non-controlling interests- this item represents the

amount that has been contributed to the company by the shareholders who hold a non-

controlling interest in the company by way of subscribing the shares of the company.

m) Own shares purchased from the owners of the Rio Tinto- this item represents the amount

that the company has paid to shareholders of the company in respect of buying back the

equity shares that were previously being allocated to them (Harris 2016).

Over the period of three years, the revenue that has been generated from the operating activities

of the company has increased significantly. This has occurred because FO the fact that the

revenue of the company has increased significantly during these three years. The amount that

was received by the company from the primary revenue generating activities of the company for

the ear 2015 and 2017 amounted to US$ 12102 and US$ 16670 respectively (Lin et al. 2015).

This demonstrates the significant rise that has occurred in the revenue of the entity. Lot of

fluctuations have occurred in the investing activities of the company. The amount of the outflows

of the cash from the investing activities of the company amounted to (US 4600) and (US 2104)

respectively for the year 2015 and 2016 respectively. The purchase made by the company in

respect of the property, plant and equipment of the company has reduced significantly over the

years. This has resulted in the cash outflow from the investing activities of the company being

reduced over this period (Banker et al. 2016). The reduction of the flow from the investing

activates was further pushed by the increase in the sale of the financial assets of the company.

The decrease in the cash flow of the company can be because FO the fact that the company has

incurred no amount in respect of purchasing the issued shares of the company back from the

shareholders of the company. The company had also taken up huge borrowings from outsiders in

the year 2016 and this has increased the cash inflow of the company. In the year, 2016 and 2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

the cash outflow of the entity amounted to (7491) and (9141) respectively. The company had

paid a huge amount of dividend to its shareholders in the year 2017 and this has resulted in the

increase in the cash outflow of the company. The effect of the changes in the activities of the

company that involve cash can be felt in the changing balance of the cash and cash equivalent of

the company. For the closing date of the year, 2015, 2016 and 2017 the amount of cash and cash

equivalent of the company amounted to (30146), (1165) and 2358 respectively. The core

business of the entity has contributed significantly to the increase in the cash and cash

equivalents of the company. one of the other most significant reasons for the increase in the

balance of the cash and cash equivalent of the company can be attributed to the fact that the

amount recovered by the company from the sale of its subsidiaries, joint ventures and various

associated increased significantly over the years. One of the other major reasons for the increase

in the cash and cash equivalent balance of the company can be attributed to the fact that the

amount that is recovered by way of subscription of shares by the shareholders that do not hold

controlling interest in the entity have increased significantly over the period of time (Jeppson et

al. 2016).

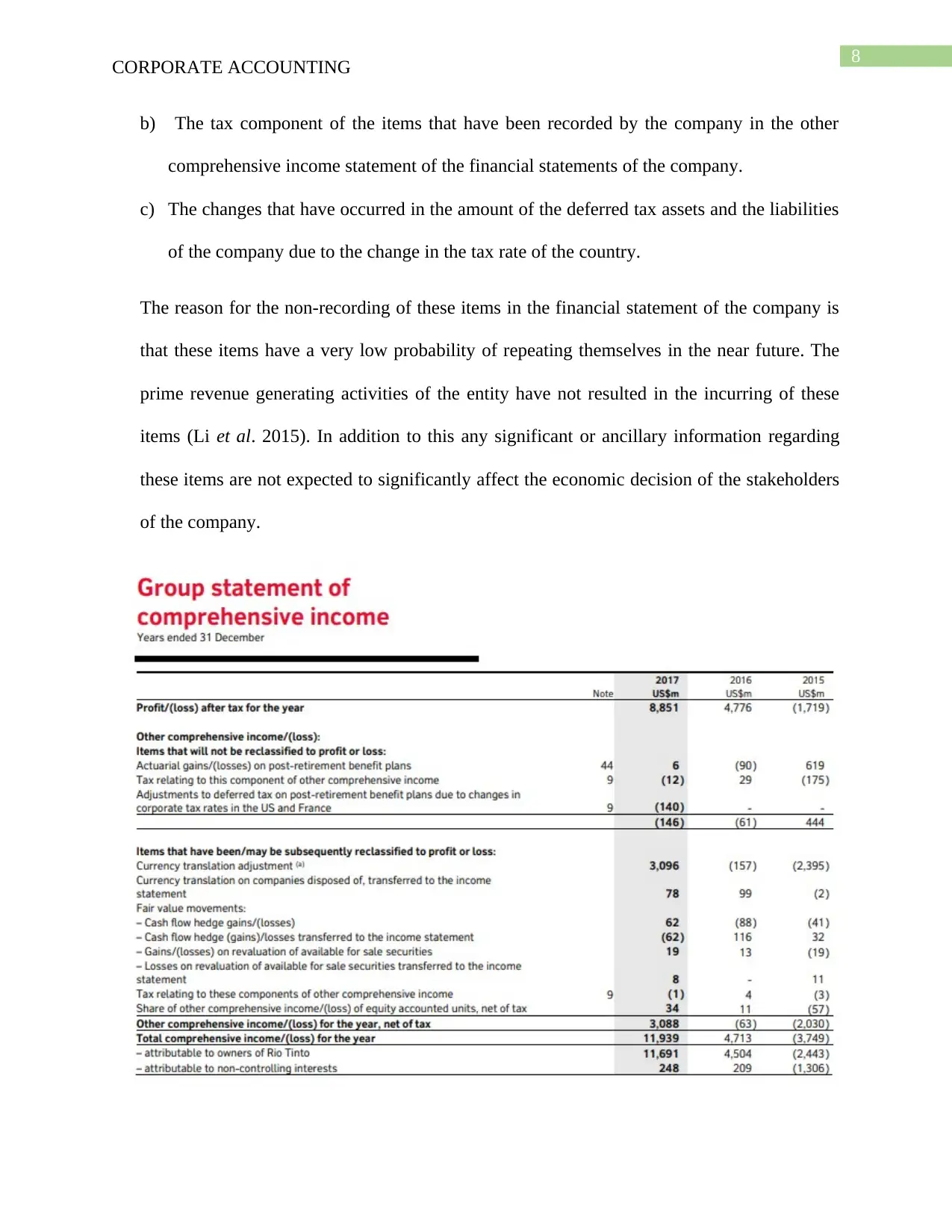

Other Comprehensive Income Statement

The components of the comprehensive income statement that has been included in the

financial report of the company are as follows:

a) Actuarial losses/ income in respect of post retirement benefit plans- this itme in the other

comprehensive incoem statemetn represents the amount that has been realised by the

company in respect of the gains that have accrued towards it by way of the actuarial

estimate made by the company of the amount of post retirement beenfit plans of the

company (Gitman et al. 2015).

CORPORATE ACCOUNTING

the cash outflow of the entity amounted to (7491) and (9141) respectively. The company had

paid a huge amount of dividend to its shareholders in the year 2017 and this has resulted in the

increase in the cash outflow of the company. The effect of the changes in the activities of the

company that involve cash can be felt in the changing balance of the cash and cash equivalent of

the company. For the closing date of the year, 2015, 2016 and 2017 the amount of cash and cash

equivalent of the company amounted to (30146), (1165) and 2358 respectively. The core

business of the entity has contributed significantly to the increase in the cash and cash

equivalents of the company. one of the other most significant reasons for the increase in the

balance of the cash and cash equivalent of the company can be attributed to the fact that the

amount recovered by the company from the sale of its subsidiaries, joint ventures and various

associated increased significantly over the years. One of the other major reasons for the increase

in the cash and cash equivalent balance of the company can be attributed to the fact that the

amount that is recovered by way of subscription of shares by the shareholders that do not hold

controlling interest in the entity have increased significantly over the period of time (Jeppson et

al. 2016).

Other Comprehensive Income Statement

The components of the comprehensive income statement that has been included in the

financial report of the company are as follows:

a) Actuarial losses/ income in respect of post retirement benefit plans- this itme in the other

comprehensive incoem statemetn represents the amount that has been realised by the

company in respect of the gains that have accrued towards it by way of the actuarial

estimate made by the company of the amount of post retirement beenfit plans of the

company (Gitman et al. 2015).

8

CORPORATE ACCOUNTING

b) The tax component of the items that have been recorded by the company in the other

comprehensive income statement of the financial statements of the company.

c) The changes that have occurred in the amount of the deferred tax assets and the liabilities

of the company due to the change in the tax rate of the country.

The reason for the non-recording of these items in the financial statement of the company is

that these items have a very low probability of repeating themselves in the near future. The

prime revenue generating activities of the entity have not resulted in the incurring of these

items (Li et al. 2015). In addition to this any significant or ancillary information regarding

these items are not expected to significantly affect the economic decision of the stakeholders

of the company.

CORPORATE ACCOUNTING

b) The tax component of the items that have been recorded by the company in the other

comprehensive income statement of the financial statements of the company.

c) The changes that have occurred in the amount of the deferred tax assets and the liabilities

of the company due to the change in the tax rate of the country.

The reason for the non-recording of these items in the financial statement of the company is

that these items have a very low probability of repeating themselves in the near future. The

prime revenue generating activities of the entity have not resulted in the incurring of these

items (Li et al. 2015). In addition to this any significant or ancillary information regarding

these items are not expected to significantly affect the economic decision of the stakeholders

of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

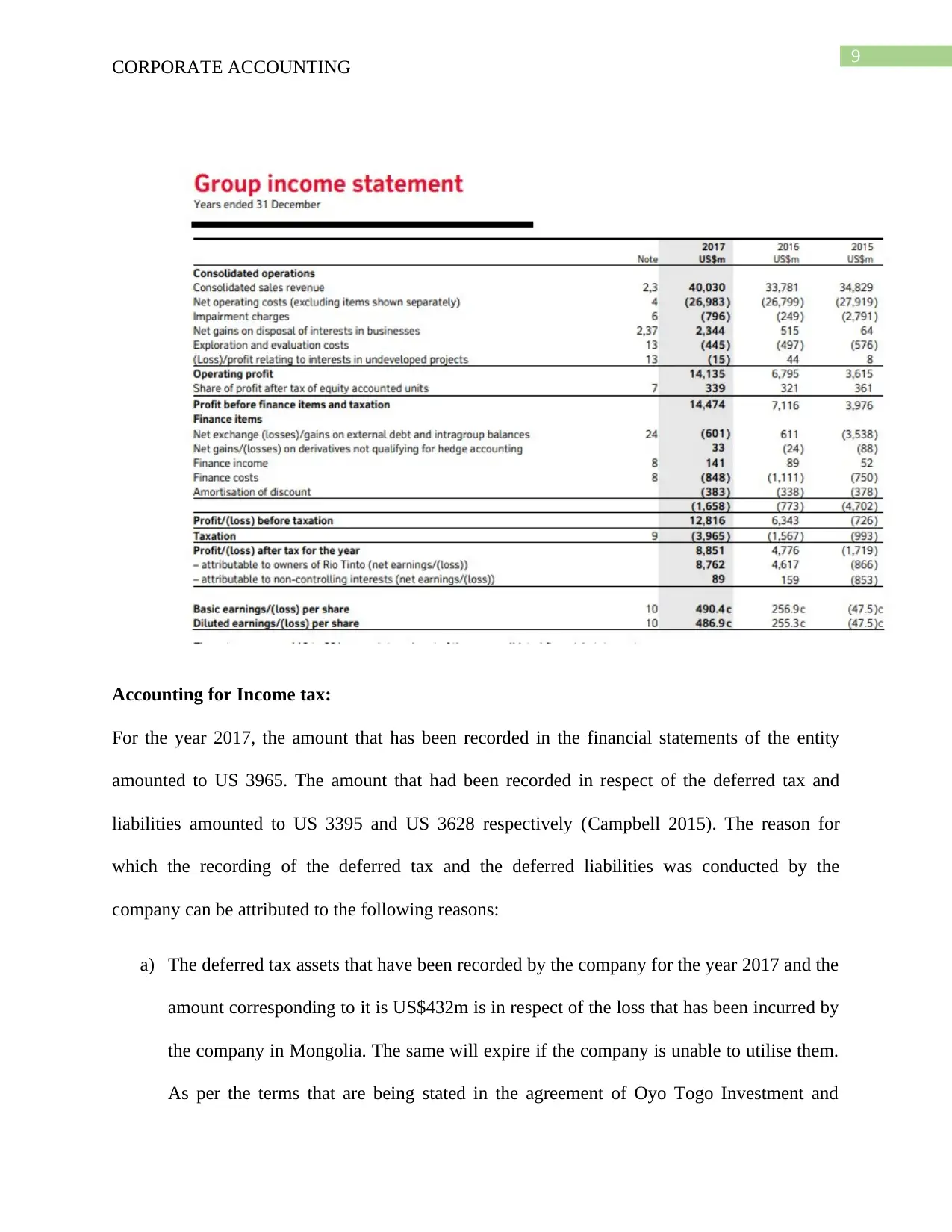

Accounting for Income tax:

For the year 2017, the amount that has been recorded in the financial statements of the entity

amounted to US 3965. The amount that had been recorded in respect of the deferred tax and

liabilities amounted to US 3395 and US 3628 respectively (Campbell 2015). The reason for

which the recording of the deferred tax and the deferred liabilities was conducted by the

company can be attributed to the following reasons:

a) The deferred tax assets that have been recorded by the company for the year 2017 and the

amount corresponding to it is US$432m is in respect of the loss that has been incurred by

the company in Mongolia. The same will expire if the company is unable to utilise them.

As per the terms that are being stated in the agreement of Oyo Togo Investment and

CORPORATE ACCOUNTING

Accounting for Income tax:

For the year 2017, the amount that has been recorded in the financial statements of the entity

amounted to US 3965. The amount that had been recorded in respect of the deferred tax and

liabilities amounted to US 3395 and US 3628 respectively (Campbell 2015). The reason for

which the recording of the deferred tax and the deferred liabilities was conducted by the

company can be attributed to the following reasons:

a) The deferred tax assets that have been recorded by the company for the year 2017 and the

amount corresponding to it is US$432m is in respect of the loss that has been incurred by

the company in Mongolia. The same will expire if the company is unable to utilise them.

As per the terms that are being stated in the agreement of Oyo Togo Investment and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

Mongolian Laws, has guided the company towards the calculation of the tax losses

(Louis et al. 2014). The same has been recorded as an asset by the company because it is

going to be realised by the company only after the year 2023 if no unforeseen changes

occur in the business environment of the company. Near about US$777 m amount in the

financial statements of the company have been recorded in respect of the realised and the

unrealised capital losses that are being encountered by the company. Only if any future

capital gain in respect of the company happens this amount will be recovered (Lei et al.

2018).

Conclusion:

A detailed analysis was being conducted in respect of the financial statements of the

company that are constituted by the cash flow statement of the company, other comprehensive

income statement and other elements of the profit and loss statement of the company that were

related to the tax treatment of the company. After the analysis, the results suggest that the

financial statements of the company have been prepared as per the applicable rules and

regulations. In addition to that, the analysis revealed that the revenue of the company has

increased significantly over the period of three years and the same is being reflected in increased

cash balance of the company. It is seen that the cash and cash equivalent balance of the company

has increased significantly over the period of three years. The reason for this increase can be

attributed to many significant reasons. These reasons include the significant rise in the income

that is being generated by the company from its core business activities has increased

significantly over the period of three years, the amount that is realised by the company from the

sale of its various associates, joint ventures and the assets have increased substantially over the

period of time.

CORPORATE ACCOUNTING

Mongolian Laws, has guided the company towards the calculation of the tax losses

(Louis et al. 2014). The same has been recorded as an asset by the company because it is

going to be realised by the company only after the year 2023 if no unforeseen changes

occur in the business environment of the company. Near about US$777 m amount in the

financial statements of the company have been recorded in respect of the realised and the

unrealised capital losses that are being encountered by the company. Only if any future

capital gain in respect of the company happens this amount will be recovered (Lei et al.

2018).

Conclusion:

A detailed analysis was being conducted in respect of the financial statements of the

company that are constituted by the cash flow statement of the company, other comprehensive

income statement and other elements of the profit and loss statement of the company that were

related to the tax treatment of the company. After the analysis, the results suggest that the

financial statements of the company have been prepared as per the applicable rules and

regulations. In addition to that, the analysis revealed that the revenue of the company has

increased significantly over the period of three years and the same is being reflected in increased

cash balance of the company. It is seen that the cash and cash equivalent balance of the company

has increased significantly over the period of three years. The reason for this increase can be

attributed to many significant reasons. These reasons include the significant rise in the income

that is being generated by the company from its core business activities has increased

significantly over the period of three years, the amount that is realised by the company from the

sale of its various associates, joint ventures and the assets have increased substantially over the

period of time.

11

CORPORATE ACCOUNTING

References:

Banker, R.D., Basu, S. and Byzalov, D., 2016. Implications of Impairment Decisions and Assets'

Cash-Flow Horizons for Conservatism Research. The Accounting Review, 92(2), pp.41-67.

Campbell, J.L., 2015. The fair value of cash flow hedges, future profitability, and stock

returns. Contemporary Accounting Research, 32(1), pp.243-279.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Gordon, E.A., Henry, E., Jorgensen, B.N. and Linthicum, C.L., 2017. Flexibility in cash-flow

classification under IFRS: determinants and consequences. Review of Accounting Studies, 22(2),

pp.839-872.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. John Wiley & Sons.

Harris, P., 2016. A case study of the cash flow statement: US GAAP conversion to

IFRS. Journal of Business Case Studies (Online), 12(1), p.1.

Jeppson, N.H., Ruddy, J.A. and Salerno, D.F., 2016. The Statement of Cash Flows and the Direct

Method of Presentation. Management Accounting Quarterly, 17(3), p.1.

Lee, T.A. ed., 2014. Cash Flow Reporting (RLE Accounting): A Recent History of an Accounting

Practice. Routledge.

Lei, J., Qiu, J. and Wan, C., 2018. Asset tangibility, cash holdings, and financial

development. Journal of Corporate Finance, 50, pp.223-242.

CORPORATE ACCOUNTING

References:

Banker, R.D., Basu, S. and Byzalov, D., 2016. Implications of Impairment Decisions and Assets'

Cash-Flow Horizons for Conservatism Research. The Accounting Review, 92(2), pp.41-67.

Campbell, J.L., 2015. The fair value of cash flow hedges, future profitability, and stock

returns. Contemporary Accounting Research, 32(1), pp.243-279.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Gordon, E.A., Henry, E., Jorgensen, B.N. and Linthicum, C.L., 2017. Flexibility in cash-flow

classification under IFRS: determinants and consequences. Review of Accounting Studies, 22(2),

pp.839-872.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. John Wiley & Sons.

Harris, P., 2016. A case study of the cash flow statement: US GAAP conversion to

IFRS. Journal of Business Case Studies (Online), 12(1), p.1.

Jeppson, N.H., Ruddy, J.A. and Salerno, D.F., 2016. The Statement of Cash Flows and the Direct

Method of Presentation. Management Accounting Quarterly, 17(3), p.1.

Lee, T.A. ed., 2014. Cash Flow Reporting (RLE Accounting): A Recent History of an Accounting

Practice. Routledge.

Lei, J., Qiu, J. and Wan, C., 2018. Asset tangibility, cash holdings, and financial

development. Journal of Corporate Finance, 50, pp.223-242.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.