Prepare Financial Statements & Budgets Assignment - FNS40217

VerifiedAdded on 2023/05/31

|11

|2778

|416

Practical Assignment

AI Summary

This document presents a comprehensive solution to an Accounting and Budgeting assignment for a Certificate IV in Accounting and Bookkeeping (FNS40217) course. The assignment encompasses multiple parts, including a written response section requiring explanations of coding, classifying, and checking data. A significant portion involves practical tasks using MS Excel, such as preparing income statements and balance sheets from a trial balance, and creating various charts and graphs to analyze a company's financial position, including variance analysis. Furthermore, the assignment includes a group presentation component where students discuss financial statement preparation, key differences between profit and non-profit entities, and financial legislation. Finally, a role-play scenario is presented, requiring students to simulate a discussion about budgeting for a new business venture, addressing issues like cost calculations, break-even analysis, and budget control. The solution demonstrates a strong understanding of accounting principles and practical application of financial analysis tools.

T-1.8.1

Details of Assessment

Term and Year Term 4, 2018 Time allowed 6 Weeks

Assessment No 2 Assessment Weighting 40%

Assessment Type Assignment

Due Date Week No. 8 Room 710

Details of Subject

Qualification FNS40217 Certificate IV in Accounting & Bookkeeping

Subject Name Accounting and Budgeting

Details of Unit(s) of competency

Unit Code (s) and

Names

FNSACC414 Prepare financial statements for non-reporting entities

FNSACC412 Prepare operational budgets

Details of Student

Student

Name

College Student ID

Student Declaration: I declare that the work

submitted is my own, and has not been

copied or plagiarised from any person or

source.

Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name Tashfiq Chowdhury

Assessment Outcome

Results Competent Notyet competent Marks / 40

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

Student Declaration: I declare that I have been

assessed in this unit, and I have been advised of my

result. I also am aware of my appeal rights and

reassessment procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have provided

appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/_____

Assessment/evidence gathering conditions

Accounting & Budgeting, Assessment No. 2 Page 1

v1.1, Last updated on 18/09/2018

Details of Assessment

Term and Year Term 4, 2018 Time allowed 6 Weeks

Assessment No 2 Assessment Weighting 40%

Assessment Type Assignment

Due Date Week No. 8 Room 710

Details of Subject

Qualification FNS40217 Certificate IV in Accounting & Bookkeeping

Subject Name Accounting and Budgeting

Details of Unit(s) of competency

Unit Code (s) and

Names

FNSACC414 Prepare financial statements for non-reporting entities

FNSACC412 Prepare operational budgets

Details of Student

Student

Name

College Student ID

Student Declaration: I declare that the work

submitted is my own, and has not been

copied or plagiarised from any person or

source.

Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name Tashfiq Chowdhury

Assessment Outcome

Results Competent Notyet competent Marks / 40

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

Student Declaration: I declare that I have been

assessed in this unit, and I have been advised of my

result. I also am aware of my appeal rights and

reassessment procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have provided

appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/_____

Assessment/evidence gathering conditions

Accounting & Budgeting, Assessment No. 2 Page 1

v1.1, Last updated on 18/09/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

Each assessment component is recorded as either Competent (C) or Not Yet Competent (NYC). A student can only

achieve competence when all assessment components listed under “Purpose of the assessment” section are recorded

as competent. Your trainer will give you feedback after the completion of each assessment. A student who is assessed

as NYC (Not Yet Competent) is eligible for re-assessment.

Resources required for this Assessment

Computer with relevant software applications and access to internet

Weekly eLearning notes relevant to the tasks/questions

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will be

provided with feedback on your work within two weeks of the assessment due date. All other feedback will be

provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspects of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment for more information (Student Handbook).

Accounting & Budgeting, Assessment No. 2 Page 2

v1.1, Last updated on 18/09/2018

Each assessment component is recorded as either Competent (C) or Not Yet Competent (NYC). A student can only

achieve competence when all assessment components listed under “Purpose of the assessment” section are recorded

as competent. Your trainer will give you feedback after the completion of each assessment. A student who is assessed

as NYC (Not Yet Competent) is eligible for re-assessment.

Resources required for this Assessment

Computer with relevant software applications and access to internet

Weekly eLearning notes relevant to the tasks/questions

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will be

provided with feedback on your work within two weeks of the assessment due date. All other feedback will be

provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspects of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment for more information (Student Handbook).

Accounting & Budgeting, Assessment No. 2 Page 2

v1.1, Last updated on 18/09/2018

T-1.8.1

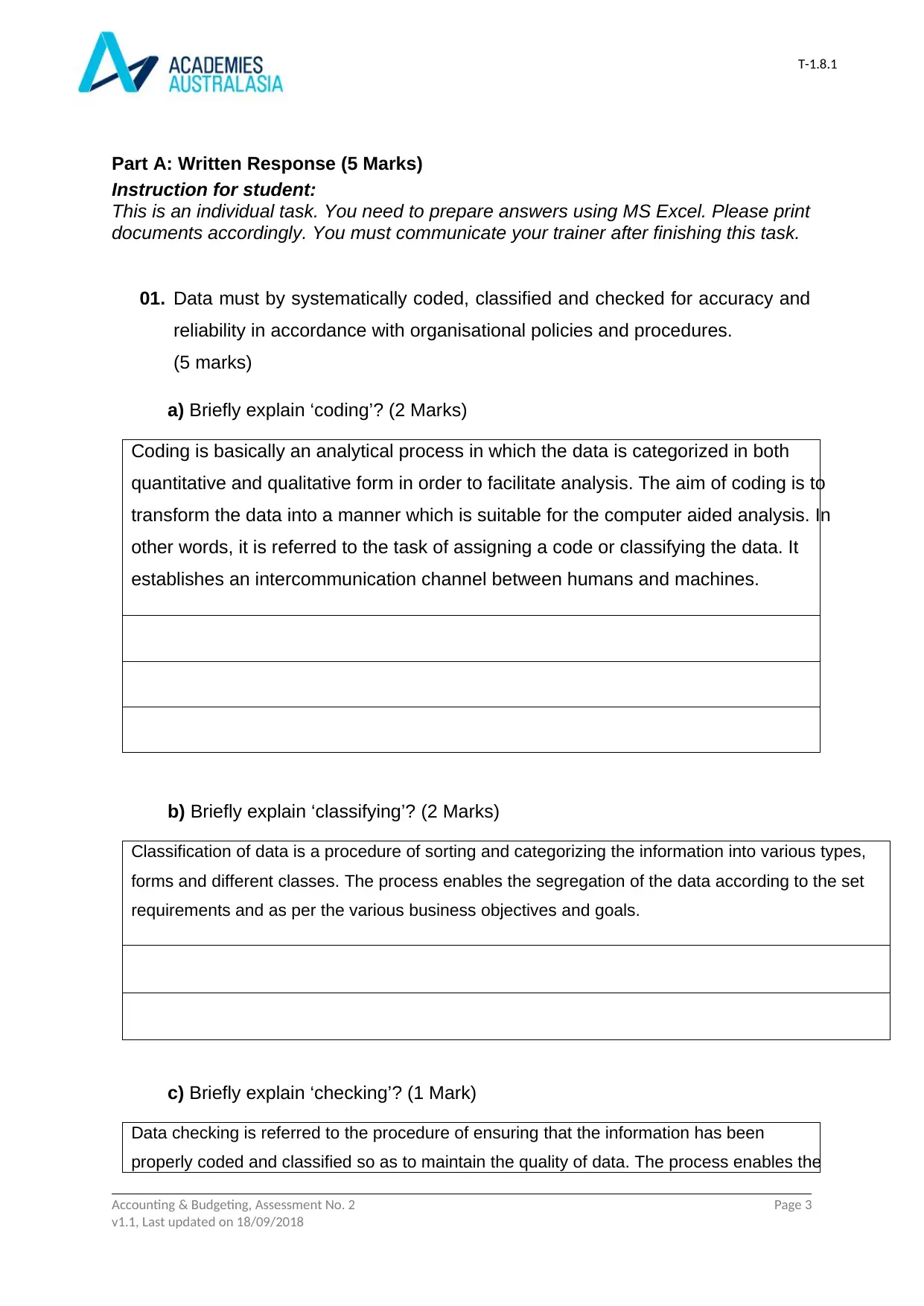

Part A: Written Response (5 Marks)

Instruction for student:

This is an individual task. You need to prepare answers using MS Excel. Please print

documents accordingly. You must communicate your trainer after finishing this task.

01. Data must by systematically coded, classified and checked for accuracy and

reliability in accordance with organisational policies and procedures.

(5 marks)

a) Briefly explain ‘coding’? (2 Marks)

Coding is basically an analytical process in which the data is categorized in both

quantitative and qualitative form in order to facilitate analysis. The aim of coding is to

transform the data into a manner which is suitable for the computer aided analysis. In

other words, it is referred to the task of assigning a code or classifying the data. It

establishes an intercommunication channel between humans and machines.

b) Briefly explain ‘classifying’? (2 Marks)

Classification of data is a procedure of sorting and categorizing the information into various types,

forms and different classes. The process enables the segregation of the data according to the set

requirements and as per the various business objectives and goals.

c) Briefly explain ‘checking’? (1 Mark)

Data checking is referred to the procedure of ensuring that the information has been

properly coded and classified so as to maintain the quality of data. The process enables the

Accounting & Budgeting, Assessment No. 2 Page 3

v1.1, Last updated on 18/09/2018

Part A: Written Response (5 Marks)

Instruction for student:

This is an individual task. You need to prepare answers using MS Excel. Please print

documents accordingly. You must communicate your trainer after finishing this task.

01. Data must by systematically coded, classified and checked for accuracy and

reliability in accordance with organisational policies and procedures.

(5 marks)

a) Briefly explain ‘coding’? (2 Marks)

Coding is basically an analytical process in which the data is categorized in both

quantitative and qualitative form in order to facilitate analysis. The aim of coding is to

transform the data into a manner which is suitable for the computer aided analysis. In

other words, it is referred to the task of assigning a code or classifying the data. It

establishes an intercommunication channel between humans and machines.

b) Briefly explain ‘classifying’? (2 Marks)

Classification of data is a procedure of sorting and categorizing the information into various types,

forms and different classes. The process enables the segregation of the data according to the set

requirements and as per the various business objectives and goals.

c) Briefly explain ‘checking’? (1 Mark)

Data checking is referred to the procedure of ensuring that the information has been

properly coded and classified so as to maintain the quality of data. The process enables the

Accounting & Budgeting, Assessment No. 2 Page 3

v1.1, Last updated on 18/09/2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

T-1.8.1

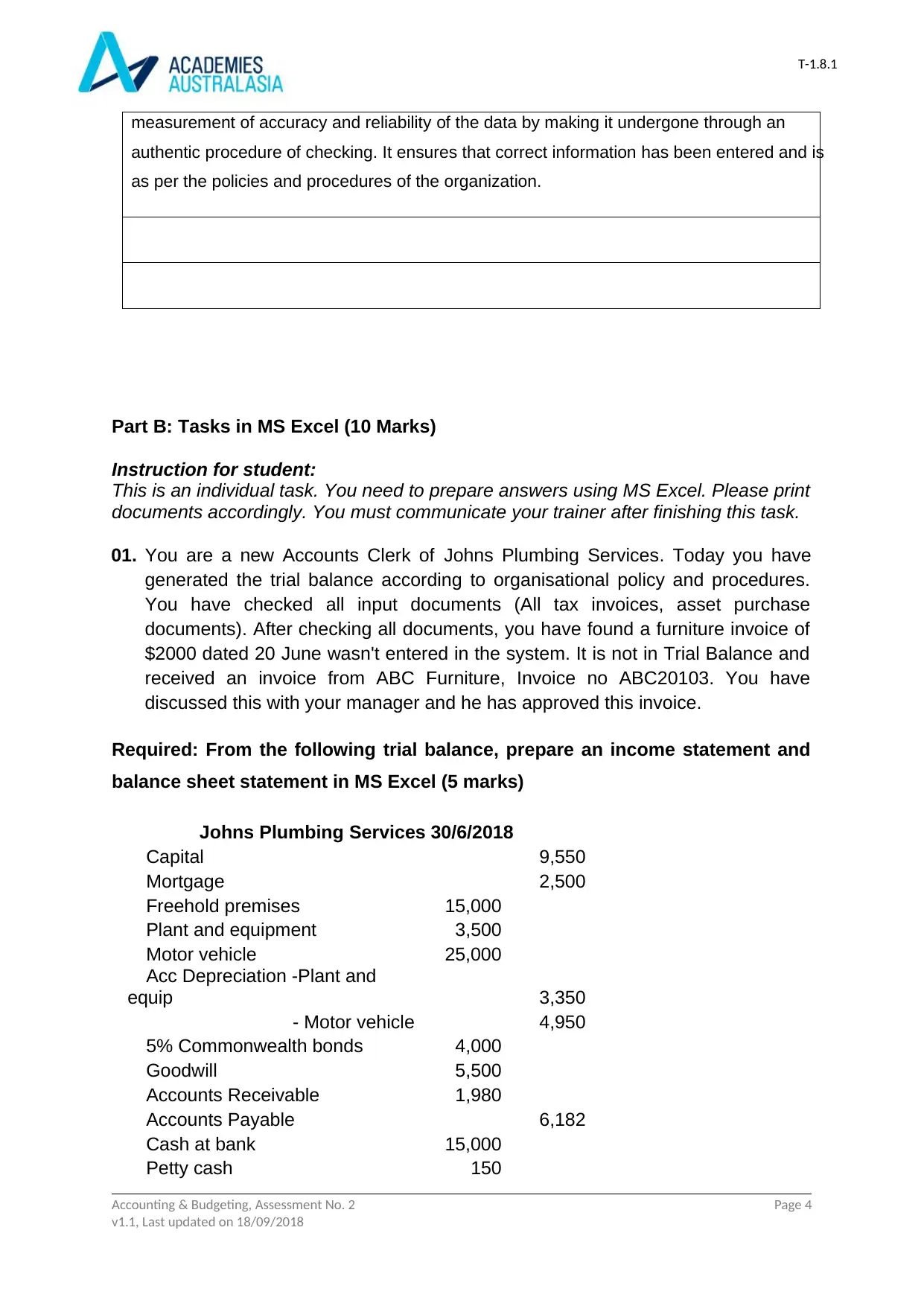

measurement of accuracy and reliability of the data by making it undergone through an

authentic procedure of checking. It ensures that correct information has been entered and is

as per the policies and procedures of the organization.

Part B: Tasks in MS Excel (10 Marks)

Instruction for student:

This is an individual task. You need to prepare answers using MS Excel. Please print

documents accordingly. You must communicate your trainer after finishing this task.

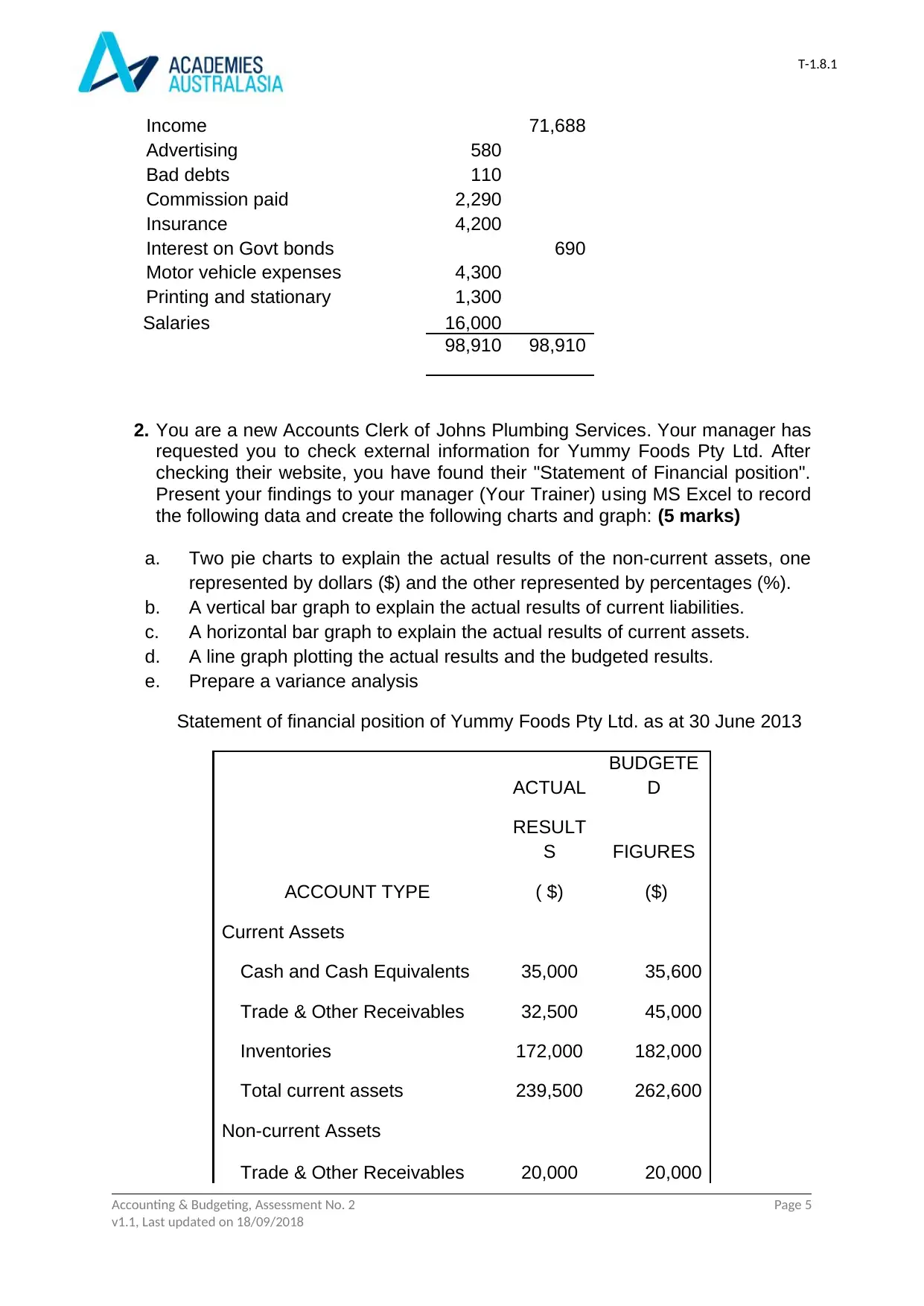

01. You are a new Accounts Clerk of Johns Plumbing Services. Today you have

generated the trial balance according to organisational policy and procedures.

You have checked all input documents (All tax invoices, asset purchase

documents). After checking all documents, you have found a furniture invoice of

$2000 dated 20 June wasn't entered in the system. It is not in Trial Balance and

received an invoice from ABC Furniture, Invoice no ABC20103. You have

discussed this with your manager and he has approved this invoice.

Required: From the following trial balance, prepare an income statement and

balance sheet statement in MS Excel (5 marks)

Johns Plumbing Services 30/6/2018

Capital 9,550

Mortgage 2,500

Freehold premises 15,000

Plant and equipment 3,500

Motor vehicle 25,000

Acc Depreciation -Plant and

equip 3,350

- Motor vehicle 4,950

5% Commonwealth bonds 4,000

Goodwill 5,500

Accounts Receivable 1,980

Accounts Payable 6,182

Cash at bank 15,000

Petty cash 150

Accounting & Budgeting, Assessment No. 2 Page 4

v1.1, Last updated on 18/09/2018

measurement of accuracy and reliability of the data by making it undergone through an

authentic procedure of checking. It ensures that correct information has been entered and is

as per the policies and procedures of the organization.

Part B: Tasks in MS Excel (10 Marks)

Instruction for student:

This is an individual task. You need to prepare answers using MS Excel. Please print

documents accordingly. You must communicate your trainer after finishing this task.

01. You are a new Accounts Clerk of Johns Plumbing Services. Today you have

generated the trial balance according to organisational policy and procedures.

You have checked all input documents (All tax invoices, asset purchase

documents). After checking all documents, you have found a furniture invoice of

$2000 dated 20 June wasn't entered in the system. It is not in Trial Balance and

received an invoice from ABC Furniture, Invoice no ABC20103. You have

discussed this with your manager and he has approved this invoice.

Required: From the following trial balance, prepare an income statement and

balance sheet statement in MS Excel (5 marks)

Johns Plumbing Services 30/6/2018

Capital 9,550

Mortgage 2,500

Freehold premises 15,000

Plant and equipment 3,500

Motor vehicle 25,000

Acc Depreciation -Plant and

equip 3,350

- Motor vehicle 4,950

5% Commonwealth bonds 4,000

Goodwill 5,500

Accounts Receivable 1,980

Accounts Payable 6,182

Cash at bank 15,000

Petty cash 150

Accounting & Budgeting, Assessment No. 2 Page 4

v1.1, Last updated on 18/09/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

Income 71,688

Advertising 580

Bad debts 110

Commission paid 2,290

Insurance 4,200

Interest on Govt bonds 690

Motor vehicle expenses 4,300

Printing and stationary 1,300

Salaries 16,000

98,910 98,910

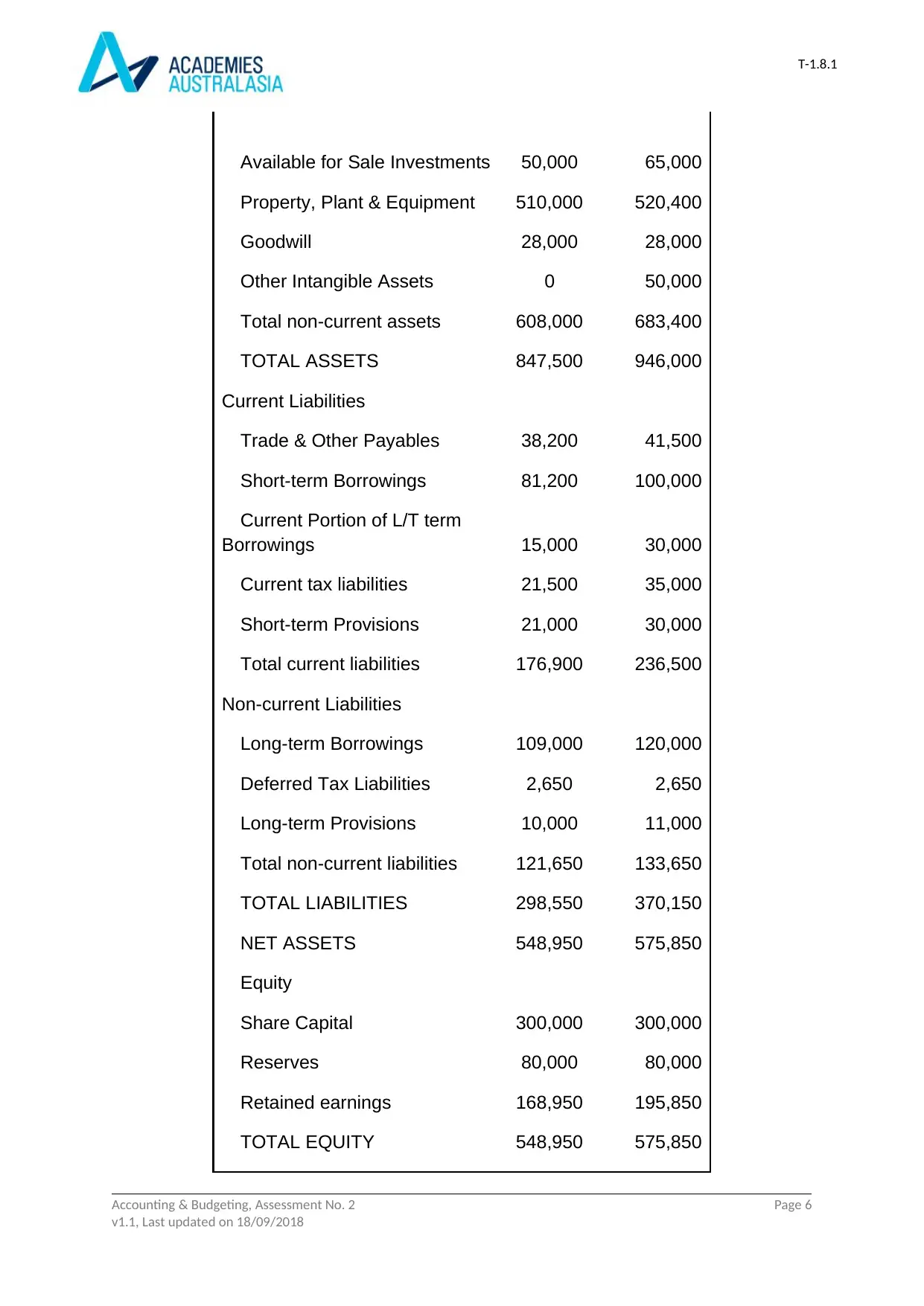

2. You are a new Accounts Clerk of Johns Plumbing Services. Your manager has

requested you to check external information for Yummy Foods Pty Ltd. After

checking their website, you have found their "Statement of Financial position".

Present your findings to your manager (Your Trainer) using MS Excel to record

the following data and create the following charts and graph: (5 marks)

a. Two pie charts to explain the actual results of the non-current assets, one

represented by dollars ($) and the other represented by percentages (%).

b. A vertical bar graph to explain the actual results of current liabilities.

c. A horizontal bar graph to explain the actual results of current assets.

d. A line graph plotting the actual results and the budgeted results.

e. Prepare a variance analysis

Statement of financial position of Yummy Foods Pty Ltd. as at 30 June 2013

ACTUAL

BUDGETE

D

ACCOUNT TYPE

RESULT

S

( $)

FIGURES

($)

Current Assets

Cash and Cash Equivalents 35,000 35,600

Trade & Other Receivables 32,500 45,000

Inventories 172,000 182,000

Total current assets 239,500 262,600

Non-current Assets

Trade & Other Receivables 20,000 20,000

Accounting & Budgeting, Assessment No. 2 Page 5

v1.1, Last updated on 18/09/2018

Income 71,688

Advertising 580

Bad debts 110

Commission paid 2,290

Insurance 4,200

Interest on Govt bonds 690

Motor vehicle expenses 4,300

Printing and stationary 1,300

Salaries 16,000

98,910 98,910

2. You are a new Accounts Clerk of Johns Plumbing Services. Your manager has

requested you to check external information for Yummy Foods Pty Ltd. After

checking their website, you have found their "Statement of Financial position".

Present your findings to your manager (Your Trainer) using MS Excel to record

the following data and create the following charts and graph: (5 marks)

a. Two pie charts to explain the actual results of the non-current assets, one

represented by dollars ($) and the other represented by percentages (%).

b. A vertical bar graph to explain the actual results of current liabilities.

c. A horizontal bar graph to explain the actual results of current assets.

d. A line graph plotting the actual results and the budgeted results.

e. Prepare a variance analysis

Statement of financial position of Yummy Foods Pty Ltd. as at 30 June 2013

ACTUAL

BUDGETE

D

ACCOUNT TYPE

RESULT

S

( $)

FIGURES

($)

Current Assets

Cash and Cash Equivalents 35,000 35,600

Trade & Other Receivables 32,500 45,000

Inventories 172,000 182,000

Total current assets 239,500 262,600

Non-current Assets

Trade & Other Receivables 20,000 20,000

Accounting & Budgeting, Assessment No. 2 Page 5

v1.1, Last updated on 18/09/2018

T-1.8.1

Available for Sale Investments 50,000 65,000

Property, Plant & Equipment 510,000 520,400

Goodwill 28,000 28,000

Other Intangible Assets 0 50,000

Total non-current assets 608,000 683,400

TOTAL ASSETS 847,500 946,000

Current Liabilities

Trade & Other Payables 38,200 41,500

Short-term Borrowings 81,200 100,000

Current Portion of L/T term

Borrowings 15,000 30,000

Current tax liabilities 21,500 35,000

Short-term Provisions 21,000 30,000

Total current liabilities 176,900 236,500

Non-current Liabilities

Long-term Borrowings 109,000 120,000

Deferred Tax Liabilities 2,650 2,650

Long-term Provisions 10,000 11,000

Total non-current liabilities 121,650 133,650

TOTAL LIABILITIES 298,550 370,150

NET ASSETS 548,950 575,850

Equity

Share Capital 300,000 300,000

Reserves 80,000 80,000

Retained earnings 168,950 195,850

TOTAL EQUITY 548,950 575,850

Accounting & Budgeting, Assessment No. 2 Page 6

v1.1, Last updated on 18/09/2018

Available for Sale Investments 50,000 65,000

Property, Plant & Equipment 510,000 520,400

Goodwill 28,000 28,000

Other Intangible Assets 0 50,000

Total non-current assets 608,000 683,400

TOTAL ASSETS 847,500 946,000

Current Liabilities

Trade & Other Payables 38,200 41,500

Short-term Borrowings 81,200 100,000

Current Portion of L/T term

Borrowings 15,000 30,000

Current tax liabilities 21,500 35,000

Short-term Provisions 21,000 30,000

Total current liabilities 176,900 236,500

Non-current Liabilities

Long-term Borrowings 109,000 120,000

Deferred Tax Liabilities 2,650 2,650

Long-term Provisions 10,000 11,000

Total non-current liabilities 121,650 133,650

TOTAL LIABILITIES 298,550 370,150

NET ASSETS 548,950 575,850

Equity

Share Capital 300,000 300,000

Reserves 80,000 80,000

Retained earnings 168,950 195,850

TOTAL EQUITY 548,950 575,850

Accounting & Budgeting, Assessment No. 2 Page 6

v1.1, Last updated on 18/09/2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

T-1.8.1

Part C: Presentation (10 marks)

Instruction for student:

This is a group base task. Your trainer will form each group. Each member of the

group must complete the assigned responsibilities to achieve maximum output.

You have 10 minutes to present this financial information. Every presenter will

have 3 minutes to present.

Using the data in the task in Part B, 2

Discuss the following:

Two pie charts to explain the actual results of the non-current assets, one

represented by dollars ($) and the other represented by percentages (%).

A vertical bar graph to explain the actual results of current liabilities.

A horizontal bar graph to explain the actual results of current assets.

A line graph plotting the actual results and the budgeted results.

Prepare a variance analysis

The key differences between the standards in terms of preparation and

presentation of financial statements between profit entities and not for profit

entities

Describe the key features of financial legislation covering for non reporting

entities:

a) taxable transactions

b) reporting requirements

Presentation guidelines:

Prepare a presentation using MS PowerPoint

Discuss all issues

No slide limits

You may add any relevant topics

Maximum 3 in each group

Accounting & Budgeting, Assessment No. 2 Page 7

v1.1, Last updated on 18/09/2018

Part C: Presentation (10 marks)

Instruction for student:

This is a group base task. Your trainer will form each group. Each member of the

group must complete the assigned responsibilities to achieve maximum output.

You have 10 minutes to present this financial information. Every presenter will

have 3 minutes to present.

Using the data in the task in Part B, 2

Discuss the following:

Two pie charts to explain the actual results of the non-current assets, one

represented by dollars ($) and the other represented by percentages (%).

A vertical bar graph to explain the actual results of current liabilities.

A horizontal bar graph to explain the actual results of current assets.

A line graph plotting the actual results and the budgeted results.

Prepare a variance analysis

The key differences between the standards in terms of preparation and

presentation of financial statements between profit entities and not for profit

entities

Describe the key features of financial legislation covering for non reporting

entities:

a) taxable transactions

b) reporting requirements

Presentation guidelines:

Prepare a presentation using MS PowerPoint

Discuss all issues

No slide limits

You may add any relevant topics

Maximum 3 in each group

Accounting & Budgeting, Assessment No. 2 Page 7

v1.1, Last updated on 18/09/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

Part D: Role Play (15 marks)

Instruction for student:

This is a group base task. Your trainer will form each group. Each member of the

group must complete the assigned responsibilities to achieve maximum output.

You are required to prepare and present a 15 minutes role play using the below

scenario.

Scenario

You are a new Accounts Clerk of Robin’s landscaping services. Matt Robin is the

manager of this lawn mowing business Robin’s Landscaping Services operating at

277 Kent Street, Sydney 2000. Matt has no budgeting knowledge. He wants to

start a new shop in Minto.

Sandra is willing to invest in this project and who will assist in budgeting for the

new investment at Minto. Sandra has prepared all financial reports and she was

seeking another partner in the business and she has presented a report to Matt

without consulting with you. She didn’t plan and think about the risks involved at

the new project. She had wrong revenue and costs calculations. She had

calculated the total cost to be $400000 per year where she didn’t consider rental

advance of $ 40000 and council charge of $600 per month. She also calculated

the weeding services at $50 per hour. Her break-even calculation was wrong. You

have done your calculation on all budget’s financial statements. Sandra has

completed Certificate IV in Accounting and forgot few concepts of budgeting.

Usual charge at Sydney customers (inclusive of GST) to make 30% net profit:

Ride on mowing service @ $77 per hour

Weeding service @ $66 per hour

Whipper-snipper service @ $22 per hour

Rubbish removal service @ $110 per load of rubbish

You, Sandra and Matt have started a discussion session for 15 minutes in

Budgeting, Budgeting Basic, Budgeting Process, Budgeting Control, Revenue

Budget, Operating Budget, Cash Budget, Forecasting Technique, budgetary

milestones and performance indicators and Break-even calculation.

Solution

Accounting & Budgeting, Assessment No. 2 Page 8

v1.1, Last updated on 18/09/2018

Part D: Role Play (15 marks)

Instruction for student:

This is a group base task. Your trainer will form each group. Each member of the

group must complete the assigned responsibilities to achieve maximum output.

You are required to prepare and present a 15 minutes role play using the below

scenario.

Scenario

You are a new Accounts Clerk of Robin’s landscaping services. Matt Robin is the

manager of this lawn mowing business Robin’s Landscaping Services operating at

277 Kent Street, Sydney 2000. Matt has no budgeting knowledge. He wants to

start a new shop in Minto.

Sandra is willing to invest in this project and who will assist in budgeting for the

new investment at Minto. Sandra has prepared all financial reports and she was

seeking another partner in the business and she has presented a report to Matt

without consulting with you. She didn’t plan and think about the risks involved at

the new project. She had wrong revenue and costs calculations. She had

calculated the total cost to be $400000 per year where she didn’t consider rental

advance of $ 40000 and council charge of $600 per month. She also calculated

the weeding services at $50 per hour. Her break-even calculation was wrong. You

have done your calculation on all budget’s financial statements. Sandra has

completed Certificate IV in Accounting and forgot few concepts of budgeting.

Usual charge at Sydney customers (inclusive of GST) to make 30% net profit:

Ride on mowing service @ $77 per hour

Weeding service @ $66 per hour

Whipper-snipper service @ $22 per hour

Rubbish removal service @ $110 per load of rubbish

You, Sandra and Matt have started a discussion session for 15 minutes in

Budgeting, Budgeting Basic, Budgeting Process, Budgeting Control, Revenue

Budget, Operating Budget, Cash Budget, Forecasting Technique, budgetary

milestones and performance indicators and Break-even calculation.

Solution

Accounting & Budgeting, Assessment No. 2 Page 8

v1.1, Last updated on 18/09/2018

T-1.8.1

Role play

Matt Robin: Good morning people. We are gathered here to discuss about our new

investment project in Minto. It is known that our company is looking forward for

establishing a new shop in Minto and Sandra is ready to invest in our project along

with some budgeting advice.

Sandra: Hello Matt. I have prepared all the financial reports and budgets related to

the new investment project. Moreover, the estimation of total cost has also been

made.

Me: Hello sir. After looking at the reports and budgets prepared by Sandra, I would

like to inform you that she has missed many things and some of her calculations are

wrong.

Matt: Can you please tell the issues in the budgets prepared as I cannot find

anything wrong.

Me: Sure sir. First of all, the cost calculated by Sandra is wrong as she has forgot to

include the rental advance and council charge worth $40,000 and $600 respectively.

This made her calculation wrong. Furthermore, she calculated weeding service

charge at $50 per hour whereas our usual charge is $66 per hour.

Sandra: Thank you for identifying my mistakes. Is there anything else which has

gone wrong in the reports as I have forgotten some budgeting concepts?

Me: Yes. The break even calculation done by you are also wrong because of the

incorrect estimates. We need to understand this that preparation of budgets is a very

important task to be performed. It involves setting of the targets, estimation of

expenses and incomes and preparation of different budgets.

Matt: what type of budgets we need to prepare and what are the performance

indicators that are to be kept in mind.

You: Various budgets such as cash budget, sales budget, operating budget and

other are required to be prepared so that proper and accurate estimations can be

done for our new investment.

You: Budgets are used as the tools to measure the actual results and identify the

variances. Therefore, it is very much important to set our standards correct.

Sandra: What about break even calculation?

You: Breakeven is the point where the business is in no profit and no loss situation. It

is important to know exactly the point after which our company will start making

profit. It will help us in maintaining the inventory levels also.

Accounting & Budgeting, Assessment No. 2 Page 9

v1.1, Last updated on 18/09/2018

Role play

Matt Robin: Good morning people. We are gathered here to discuss about our new

investment project in Minto. It is known that our company is looking forward for

establishing a new shop in Minto and Sandra is ready to invest in our project along

with some budgeting advice.

Sandra: Hello Matt. I have prepared all the financial reports and budgets related to

the new investment project. Moreover, the estimation of total cost has also been

made.

Me: Hello sir. After looking at the reports and budgets prepared by Sandra, I would

like to inform you that she has missed many things and some of her calculations are

wrong.

Matt: Can you please tell the issues in the budgets prepared as I cannot find

anything wrong.

Me: Sure sir. First of all, the cost calculated by Sandra is wrong as she has forgot to

include the rental advance and council charge worth $40,000 and $600 respectively.

This made her calculation wrong. Furthermore, she calculated weeding service

charge at $50 per hour whereas our usual charge is $66 per hour.

Sandra: Thank you for identifying my mistakes. Is there anything else which has

gone wrong in the reports as I have forgotten some budgeting concepts?

Me: Yes. The break even calculation done by you are also wrong because of the

incorrect estimates. We need to understand this that preparation of budgets is a very

important task to be performed. It involves setting of the targets, estimation of

expenses and incomes and preparation of different budgets.

Matt: what type of budgets we need to prepare and what are the performance

indicators that are to be kept in mind.

You: Various budgets such as cash budget, sales budget, operating budget and

other are required to be prepared so that proper and accurate estimations can be

done for our new investment.

You: Budgets are used as the tools to measure the actual results and identify the

variances. Therefore, it is very much important to set our standards correct.

Sandra: What about break even calculation?

You: Breakeven is the point where the business is in no profit and no loss situation. It

is important to know exactly the point after which our company will start making

profit. It will help us in maintaining the inventory levels also.

Accounting & Budgeting, Assessment No. 2 Page 9

v1.1, Last updated on 18/09/2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

T-1.8.1

Matt: From this discussion, it seems like there are many

things needed to be change in the reports prepared by Sandra. I want you and

Sandra to prepare all the financial reports again with the correct estimations and

calculations.

Sandra and You: Ok sir.

Matt: Thank you. We will take the review of reports in next meeting.

PRESENTATIONAND ROLE PLAY CHECK LIST (for trainer use only)

S/N Communication Requirements Satisfactory Not

Satisfactory

1 Discussed Financial Position

2 Presented Budgeted Variance

3 Presented key features of financial legislation

covering for non-reporting entities

4 Presentation slides met requirements

5 Discussed Budgeting Basics

6 Discussed Break even points

MARKINGRUBRIC FOR ALL TASKS (for trainer use only)

The assessor needs to use judgment in providing marks for the tasks based on learner performance.

(Accounting and Budgeting Assessment 02)

TASK NO. MARK

ALLOCATED

MARK

RECEIVED

Part A: Written Response 5 / 5

Part B: Tasks in Excel 1 5 / 5

Part B: Tasks in Excel 2 5 / 5

Part C: Presentation 10 / 10

Part D: Role Play 15 / 15

Accounting & Budgeting, Assessment No. 2 Page 10

v1.1, Last updated on 18/09/2018

Matt: From this discussion, it seems like there are many

things needed to be change in the reports prepared by Sandra. I want you and

Sandra to prepare all the financial reports again with the correct estimations and

calculations.

Sandra and You: Ok sir.

Matt: Thank you. We will take the review of reports in next meeting.

PRESENTATIONAND ROLE PLAY CHECK LIST (for trainer use only)

S/N Communication Requirements Satisfactory Not

Satisfactory

1 Discussed Financial Position

2 Presented Budgeted Variance

3 Presented key features of financial legislation

covering for non-reporting entities

4 Presentation slides met requirements

5 Discussed Budgeting Basics

6 Discussed Break even points

MARKINGRUBRIC FOR ALL TASKS (for trainer use only)

The assessor needs to use judgment in providing marks for the tasks based on learner performance.

(Accounting and Budgeting Assessment 02)

TASK NO. MARK

ALLOCATED

MARK

RECEIVED

Part A: Written Response 5 / 5

Part B: Tasks in Excel 1 5 / 5

Part B: Tasks in Excel 2 5 / 5

Part C: Presentation 10 / 10

Part D: Role Play 15 / 15

Accounting & Budgeting, Assessment No. 2 Page 10

v1.1, Last updated on 18/09/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

TOTAL 40 / 40

End of Assessment

Accounting & Budgeting, Assessment No. 2 Page 11

v1.1, Last updated on 18/09/2018

TOTAL 40 / 40

End of Assessment

Accounting & Budgeting, Assessment No. 2 Page 11

v1.1, Last updated on 18/09/2018

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.