Assessment Cover Sheet

VerifiedAdded on 2023/02/01

|14

|2820

|86

AI Summary

This form is to be completed by the assessor and used as a final record of student competency. All student submissions including any associated checklists are to be attached to this cover sheet before placing on the student's file.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Assessment

Summary

Sheet

This form is to be

completed by the

assessor and used a

final record of student

competency.

All student

submissions including

any associated

checklists (outlined

below) are to be

attached to this cover

sheet before placing on

the students file.

Student results

are not to be entered

onto the Student

Database unless all

relevant paperwork

is completed and

attached to this form.

Unit Code: FNSACC507

Unit Title: Provide Management Accounting

Information

Please attach the following documentation to this form Result

Assessment Week 1 Questioning and case study

S /

NYS /

DNS

Assessment Week 2 Case Analysis and written response

S /

NYS /

DNS

Final Assessment Result for this unit C /

NYC

Feedback is given to the student on each Assessment task Yes /

No

Feedback is given to the student on final outcome of the unit Yes /

No

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Summary

Sheet

This form is to be

completed by the

assessor and used a

final record of student

competency.

All student

submissions including

any associated

checklists (outlined

below) are to be

attached to this cover

sheet before placing on

the students file.

Student results

are not to be entered

onto the Student

Database unless all

relevant paperwork

is completed and

attached to this form.

Unit Code: FNSACC507

Unit Title: Provide Management Accounting

Information

Please attach the following documentation to this form Result

Assessment Week 1 Questioning and case study

S /

NYS /

DNS

Assessment Week 2 Case Analysis and written response

S /

NYS /

DNS

Final Assessment Result for this unit C /

NYC

Feedback is given to the student on each Assessment task Yes /

No

Feedback is given to the student on final outcome of the unit Yes /

No

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Student Declaration I have been assessed in a

fair and flexible manner. I understand that the Elite

Education Vocation Institute’s Student Assessment,

Reassessment and Repeating Units of

Competency Guidelines apply to these assessment

tasks.

Assessor

Declaration:

I declare that

I have

conducted a

fair, valid,

reliable and

flexible

assessment

with this

student, and

I have

provided

appropriate

feedback.

Name: Name:

Signature: Signature:

Date: Date:

Assessment Cover

Sheet

Assessment Week

One Details

Assessment Type Questioning and case study

Date:

Qualification : FNS50215 Diploma of Accounting

Unit Title: Provide Management Accounting

Information

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

fair and flexible manner. I understand that the Elite

Education Vocation Institute’s Student Assessment,

Reassessment and Repeating Units of

Competency Guidelines apply to these assessment

tasks.

Assessor

Declaration:

I declare that

I have

conducted a

fair, valid,

reliable and

flexible

assessment

with this

student, and

I have

provided

appropriate

feedback.

Name: Name:

Signature: Signature:

Date: Date:

Assessment Cover

Sheet

Assessment Week

One Details

Assessment Type Questioning and case study

Date:

Qualification : FNS50215 Diploma of Accounting

Unit Title: Provide Management Accounting

Information

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Student Declaration: I declare that this work has been

completed by me honestly and with integrity. I

understand that the Elite Education Vocation Institute’s

Student Assessment, Reassessment and Repeating

Units of Competency Guidelines apply to these

assessment tasks.

Assessor

Declaration: I

declare that I

have conducted a

fair, valid, reliable

and flexible

assessment with

this student, and I

have provided

appropriate

feedback.

Name: Name:

Signature: Signature:

Date: Date:

Student was

absent from the

feedback session.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

completed by me honestly and with integrity. I

understand that the Elite Education Vocation Institute’s

Student Assessment, Reassessment and Repeating

Units of Competency Guidelines apply to these

assessment tasks.

Assessor

Declaration: I

declare that I

have conducted a

fair, valid, reliable

and flexible

assessment with

this student, and I

have provided

appropriate

feedback.

Name: Name:

Signature: Signature:

Date: Date:

Student was

absent from the

feedback session.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

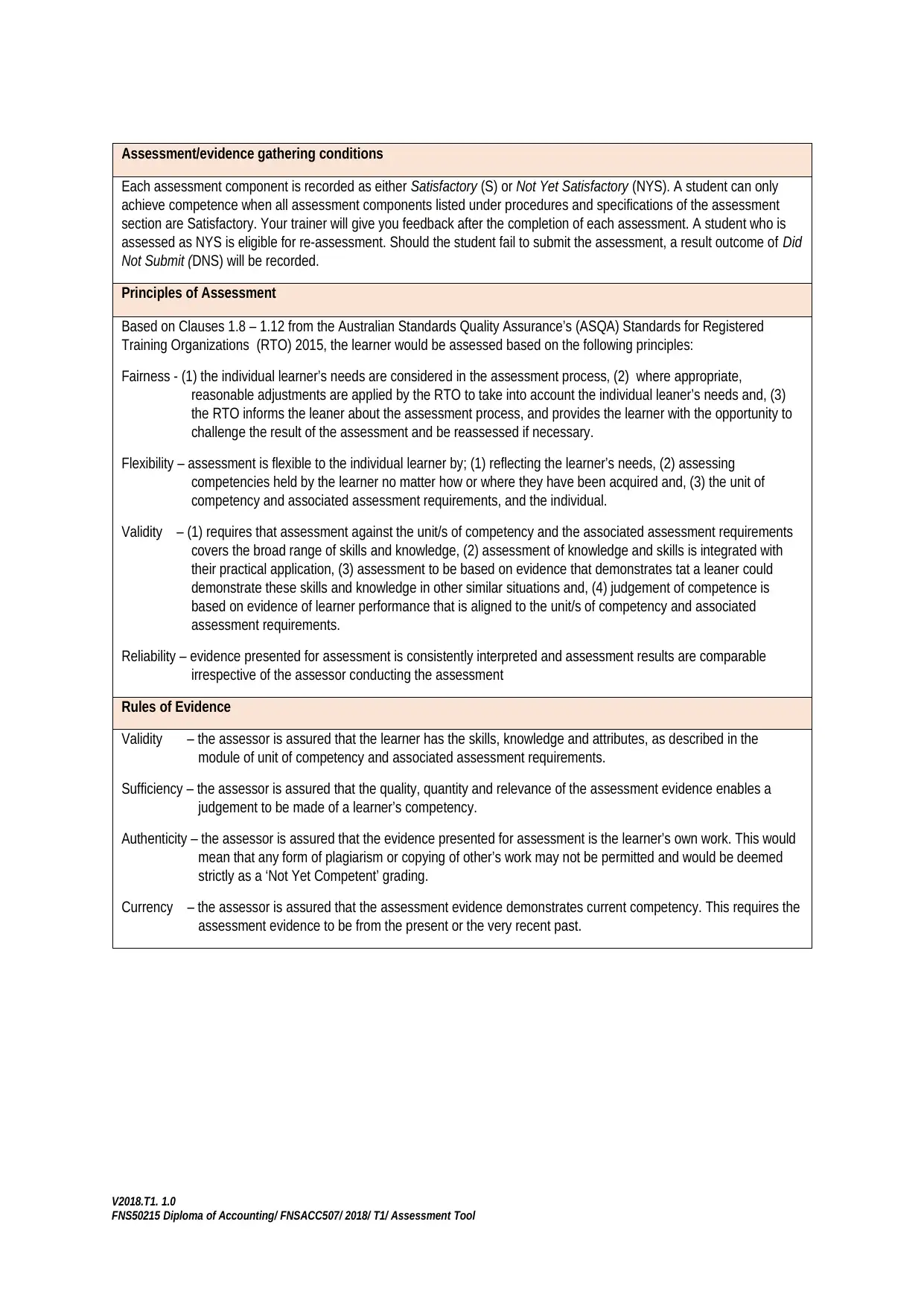

Assessment/evidence gathering conditions

Each assessment component is recorded as either Satisfactory (S) or Not Yet Satisfactory (NYS). A student can only

achieve competence when all assessment components listed under procedures and specifications of the assessment

section are Satisfactory. Your trainer will give you feedback after the completion of each assessment. A student who is

assessed as NYS is eligible for re-assessment. Should the student fail to submit the assessment, a result outcome of Did

Not Submit (DNS) will be recorded.

Principles of Assessment

Based on Clauses 1.8 – 1.12 from the Australian Standards Quality Assurance’s (ASQA) Standards for Registered

Training Organizations (RTO) 2015, the learner would be assessed based on the following principles:

Fairness - (1) the individual learner’s needs are considered in the assessment process, (2) where appropriate,

reasonable adjustments are applied by the RTO to take into account the individual leaner’s needs and, (3)

the RTO informs the leaner about the assessment process, and provides the learner with the opportunity to

challenge the result of the assessment and be reassessed if necessary.

Flexibility – assessment is flexible to the individual learner by; (1) reflecting the learner’s needs, (2) assessing

competencies held by the learner no matter how or where they have been acquired and, (3) the unit of

competency and associated assessment requirements, and the individual.

Validity – (1) requires that assessment against the unit/s of competency and the associated assessment requirements

covers the broad range of skills and knowledge, (2) assessment of knowledge and skills is integrated with

their practical application, (3) assessment to be based on evidence that demonstrates tat a leaner could

demonstrate these skills and knowledge in other similar situations and, (4) judgement of competence is

based on evidence of learner performance that is aligned to the unit/s of competency and associated

assessment requirements.

Reliability – evidence presented for assessment is consistently interpreted and assessment results are comparable

irrespective of the assessor conducting the assessment

Rules of Evidence

Validity – the assessor is assured that the learner has the skills, knowledge and attributes, as described in the

module of unit of competency and associated assessment requirements.

Sufficiency – the assessor is assured that the quality, quantity and relevance of the assessment evidence enables a

judgement to be made of a learner’s competency.

Authenticity – the assessor is assured that the evidence presented for assessment is the learner’s own work. This would

mean that any form of plagiarism or copying of other’s work may not be permitted and would be deemed

strictly as a ‘Not Yet Competent’ grading.

Currency – the assessor is assured that the assessment evidence demonstrates current competency. This requires the

assessment evidence to be from the present or the very recent past.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Each assessment component is recorded as either Satisfactory (S) or Not Yet Satisfactory (NYS). A student can only

achieve competence when all assessment components listed under procedures and specifications of the assessment

section are Satisfactory. Your trainer will give you feedback after the completion of each assessment. A student who is

assessed as NYS is eligible for re-assessment. Should the student fail to submit the assessment, a result outcome of Did

Not Submit (DNS) will be recorded.

Principles of Assessment

Based on Clauses 1.8 – 1.12 from the Australian Standards Quality Assurance’s (ASQA) Standards for Registered

Training Organizations (RTO) 2015, the learner would be assessed based on the following principles:

Fairness - (1) the individual learner’s needs are considered in the assessment process, (2) where appropriate,

reasonable adjustments are applied by the RTO to take into account the individual leaner’s needs and, (3)

the RTO informs the leaner about the assessment process, and provides the learner with the opportunity to

challenge the result of the assessment and be reassessed if necessary.

Flexibility – assessment is flexible to the individual learner by; (1) reflecting the learner’s needs, (2) assessing

competencies held by the learner no matter how or where they have been acquired and, (3) the unit of

competency and associated assessment requirements, and the individual.

Validity – (1) requires that assessment against the unit/s of competency and the associated assessment requirements

covers the broad range of skills and knowledge, (2) assessment of knowledge and skills is integrated with

their practical application, (3) assessment to be based on evidence that demonstrates tat a leaner could

demonstrate these skills and knowledge in other similar situations and, (4) judgement of competence is

based on evidence of learner performance that is aligned to the unit/s of competency and associated

assessment requirements.

Reliability – evidence presented for assessment is consistently interpreted and assessment results are comparable

irrespective of the assessor conducting the assessment

Rules of Evidence

Validity – the assessor is assured that the learner has the skills, knowledge and attributes, as described in the

module of unit of competency and associated assessment requirements.

Sufficiency – the assessor is assured that the quality, quantity and relevance of the assessment evidence enables a

judgement to be made of a learner’s competency.

Authenticity – the assessor is assured that the evidence presented for assessment is the learner’s own work. This would

mean that any form of plagiarism or copying of other’s work may not be permitted and would be deemed

strictly as a ‘Not Yet Competent’ grading.

Currency – the assessor is assured that the assessment evidence demonstrates current competency. This requires the

assessment evidence to be from the present or the very recent past.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Resources required for this Assessment

All documents must be created using Microsoft Office suites i.e., MS Word, Excel, PowerPoint

Upon completion, submit the assessment via the student learning management system to your trainer along

with the completed assessment coversheet.

Refer the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment is to be completed according to the instructions given by your assessor.

Students are allowed to take this assessment home.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will be

provided with feedback on your work within 2 weeks of the assessment due date.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment and re-enrolment policy for more information.

Procedures and Specifications of the Assessment

To complete the unit requirements safely and effectively, the individual must:

Define international marketing

Identify international trade patterns

Explain international trade policies and agreements

Identify legislative requirements

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

All documents must be created using Microsoft Office suites i.e., MS Word, Excel, PowerPoint

Upon completion, submit the assessment via the student learning management system to your trainer along

with the completed assessment coversheet.

Refer the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer

Instructions for Students

Please read the following instructions carefully

This assessment is to be completed according to the instructions given by your assessor.

Students are allowed to take this assessment home.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will be

provided with feedback on your work within 2 weeks of the assessment due date.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment and re-enrolment policy for more information.

Procedures and Specifications of the Assessment

To complete the unit requirements safely and effectively, the individual must:

Define international marketing

Identify international trade patterns

Explain international trade policies and agreements

Identify legislative requirements

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

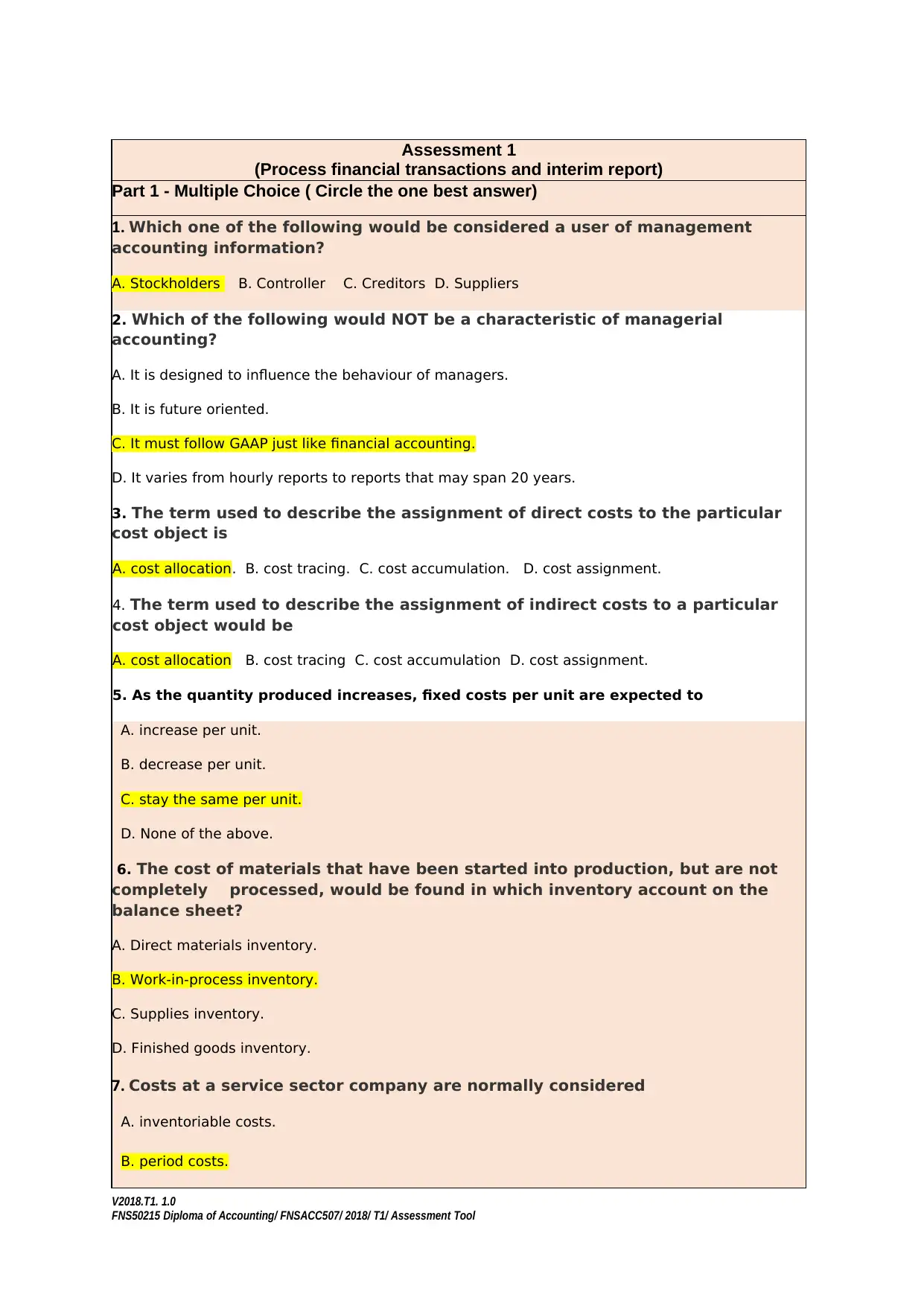

Assessment 1

(Process financial transactions and interim report)

Part 1 - Multiple Choice ( Circle the one best answer)

1. Which one of the following would be considered a user of management

accounting information?

A. Stockholders B. Controller C. Creditors D. Suppliers

2. Which of the following would NOT be a characteristic of managerial

accounting?

A. It is designed to influence the behaviour of managers.

B. It is future oriented.

C. It must follow GAAP just like financial accounting.

D. It varies from hourly reports to reports that may span 20 years.

3. The term used to describe the assignment of direct costs to the particular

cost object is

A. cost allocation. B. cost tracing. C. cost accumulation. D. cost assignment.

4. The term used to describe the assignment of indirect costs to a particular

cost object would be

A. cost allocation B. cost tracing C. cost accumulation D. cost assignment.

5. As the quantity produced increases, fixed costs per unit are expected to

A. increase per unit.

B. decrease per unit.

C. stay the same per unit.

D. None of the above.

6. The cost of materials that have been started into production, but are not

completely processed, would be found in which inventory account on the

balance sheet?

A. Direct materials inventory.

B. Work-in-process inventory.

C. Supplies inventory.

D. Finished goods inventory.

7. Costs at a service sector company are normally considered

A. inventoriable costs.

B. period costs.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

(Process financial transactions and interim report)

Part 1 - Multiple Choice ( Circle the one best answer)

1. Which one of the following would be considered a user of management

accounting information?

A. Stockholders B. Controller C. Creditors D. Suppliers

2. Which of the following would NOT be a characteristic of managerial

accounting?

A. It is designed to influence the behaviour of managers.

B. It is future oriented.

C. It must follow GAAP just like financial accounting.

D. It varies from hourly reports to reports that may span 20 years.

3. The term used to describe the assignment of direct costs to the particular

cost object is

A. cost allocation. B. cost tracing. C. cost accumulation. D. cost assignment.

4. The term used to describe the assignment of indirect costs to a particular

cost object would be

A. cost allocation B. cost tracing C. cost accumulation D. cost assignment.

5. As the quantity produced increases, fixed costs per unit are expected to

A. increase per unit.

B. decrease per unit.

C. stay the same per unit.

D. None of the above.

6. The cost of materials that have been started into production, but are not

completely processed, would be found in which inventory account on the

balance sheet?

A. Direct materials inventory.

B. Work-in-process inventory.

C. Supplies inventory.

D. Finished goods inventory.

7. Costs at a service sector company are normally considered

A. inventoriable costs.

B. period costs.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

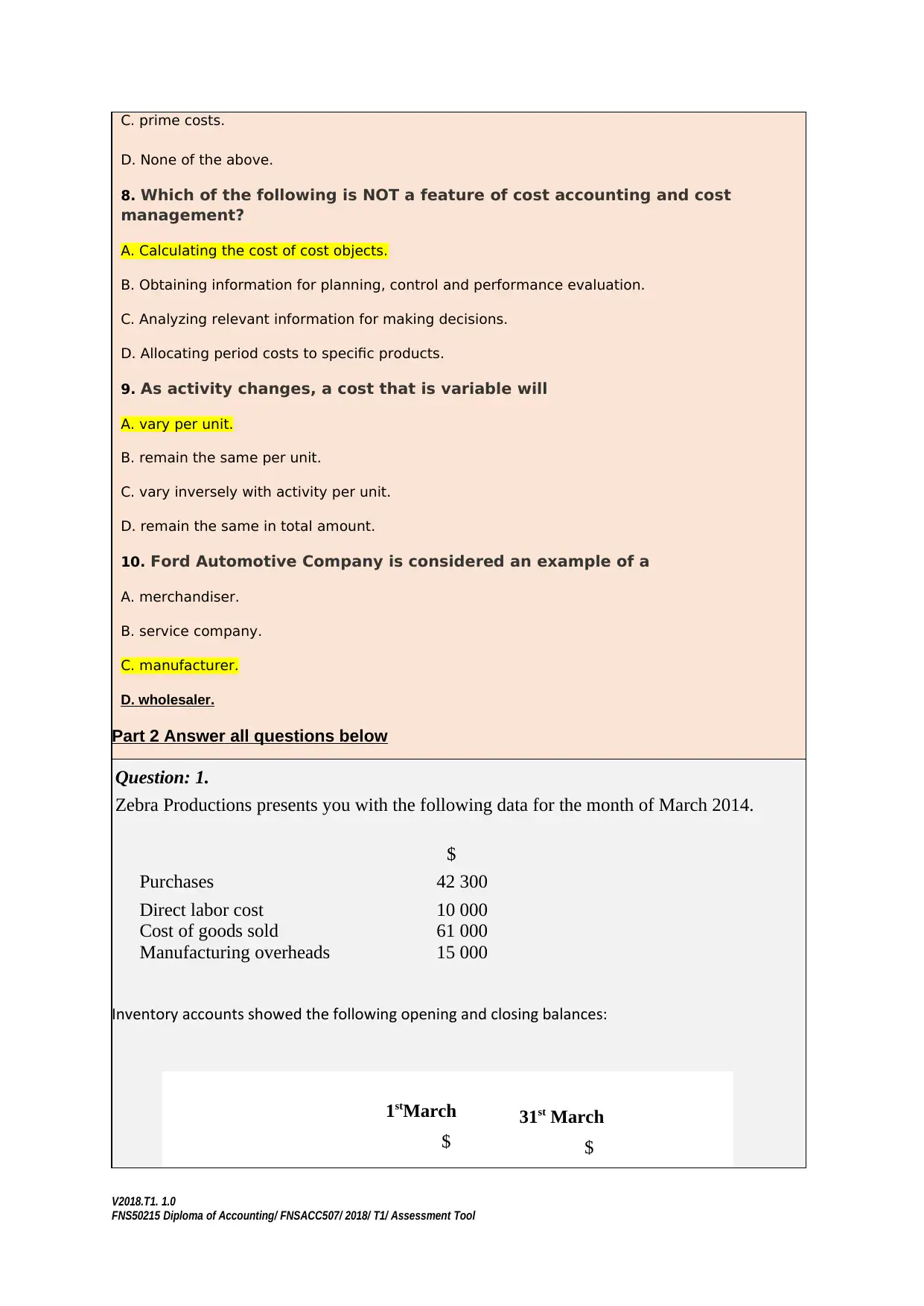

C. prime costs.

D. None of the above.

8. Which of the following is NOT a feature of cost accounting and cost

management?

A. Calculating the cost of cost objects.

B. Obtaining information for planning, control and performance evaluation.

C. Analyzing relevant information for making decisions.

D. Allocating period costs to specific products.

9. As activity changes, a cost that is variable will

A. vary per unit.

B. remain the same per unit.

C. vary inversely with activity per unit.

D. remain the same in total amount.

10. Ford Automotive Company is considered an example of a

A. merchandiser.

B. service company.

C. manufacturer.

D. wholesaler.

Part 2 Answer all questions below

Question: 1.

Zebra Productions presents you with the following data for the month of March 2014.

$

Purchases 42 300

Direct labor cost 10 000

Cost of goods sold 61 000

Manufacturing overheads 15 000

Inventory accounts showed the following opening and closing balances:

1stMarch

$

31st March

$

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

D. None of the above.

8. Which of the following is NOT a feature of cost accounting and cost

management?

A. Calculating the cost of cost objects.

B. Obtaining information for planning, control and performance evaluation.

C. Analyzing relevant information for making decisions.

D. Allocating period costs to specific products.

9. As activity changes, a cost that is variable will

A. vary per unit.

B. remain the same per unit.

C. vary inversely with activity per unit.

D. remain the same in total amount.

10. Ford Automotive Company is considered an example of a

A. merchandiser.

B. service company.

C. manufacturer.

D. wholesaler.

Part 2 Answer all questions below

Question: 1.

Zebra Productions presents you with the following data for the month of March 2014.

$

Purchases 42 300

Direct labor cost 10 000

Cost of goods sold 61 000

Manufacturing overheads 15 000

Inventory accounts showed the following opening and closing balances:

1stMarch

$

31st March

$

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

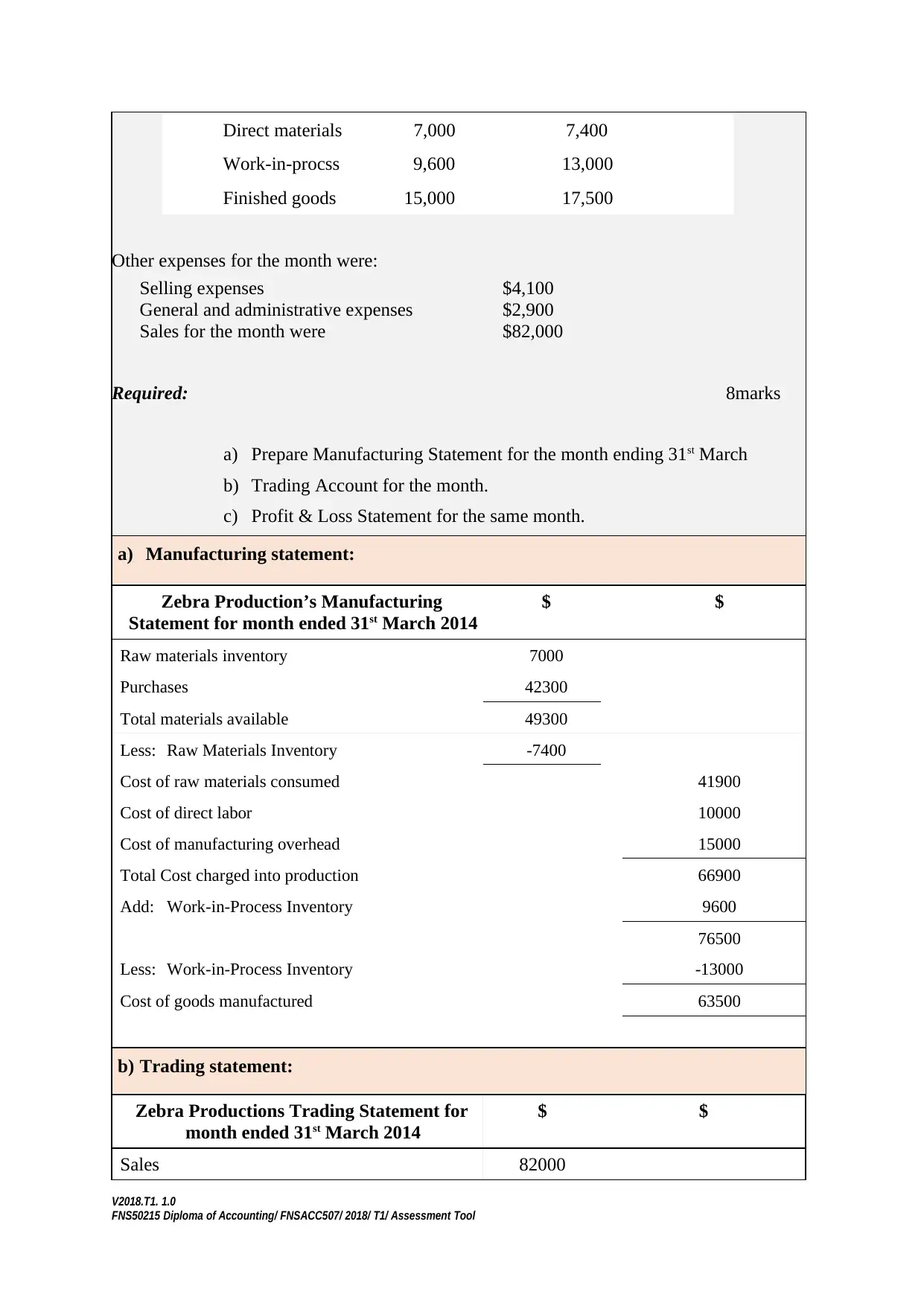

Direct materials 7,000 7,400

Work-in-procss 9,600 13,000

Finished goods 15,000 17,500

Other expenses for the month were:

Selling expenses $4,100

General and administrative expenses $2,900

Sales for the month were $82,000

Required: 8marks

a) Prepare Manufacturing Statement for the month ending 31st March

b) Trading Account for the month.

c) Profit & Loss Statement for the same month.

a) Manufacturing statement:

Zebra Production’s Manufacturing

Statement for month ended 31st March 2014

$ $

Raw materials inventory 7000

Purchases 42300

Total materials available 49300

Less: Raw Materials Inventory -7400

Cost of raw materials consumed 41900

Cost of direct labor 10000

Cost of manufacturing overhead 15000

Total Cost charged into production 66900

Add: Work-in-Process Inventory 9600

76500

Less: Work-in-Process Inventory -13000

Cost of goods manufactured 63500

b) Trading statement:

Zebra Productions Trading Statement for

month ended 31st March 2014

$ $

Sales 82000

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Work-in-procss 9,600 13,000

Finished goods 15,000 17,500

Other expenses for the month were:

Selling expenses $4,100

General and administrative expenses $2,900

Sales for the month were $82,000

Required: 8marks

a) Prepare Manufacturing Statement for the month ending 31st March

b) Trading Account for the month.

c) Profit & Loss Statement for the same month.

a) Manufacturing statement:

Zebra Production’s Manufacturing

Statement for month ended 31st March 2014

$ $

Raw materials inventory 7000

Purchases 42300

Total materials available 49300

Less: Raw Materials Inventory -7400

Cost of raw materials consumed 41900

Cost of direct labor 10000

Cost of manufacturing overhead 15000

Total Cost charged into production 66900

Add: Work-in-Process Inventory 9600

76500

Less: Work-in-Process Inventory -13000

Cost of goods manufactured 63500

b) Trading statement:

Zebra Productions Trading Statement for

month ended 31st March 2014

$ $

Sales 82000

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

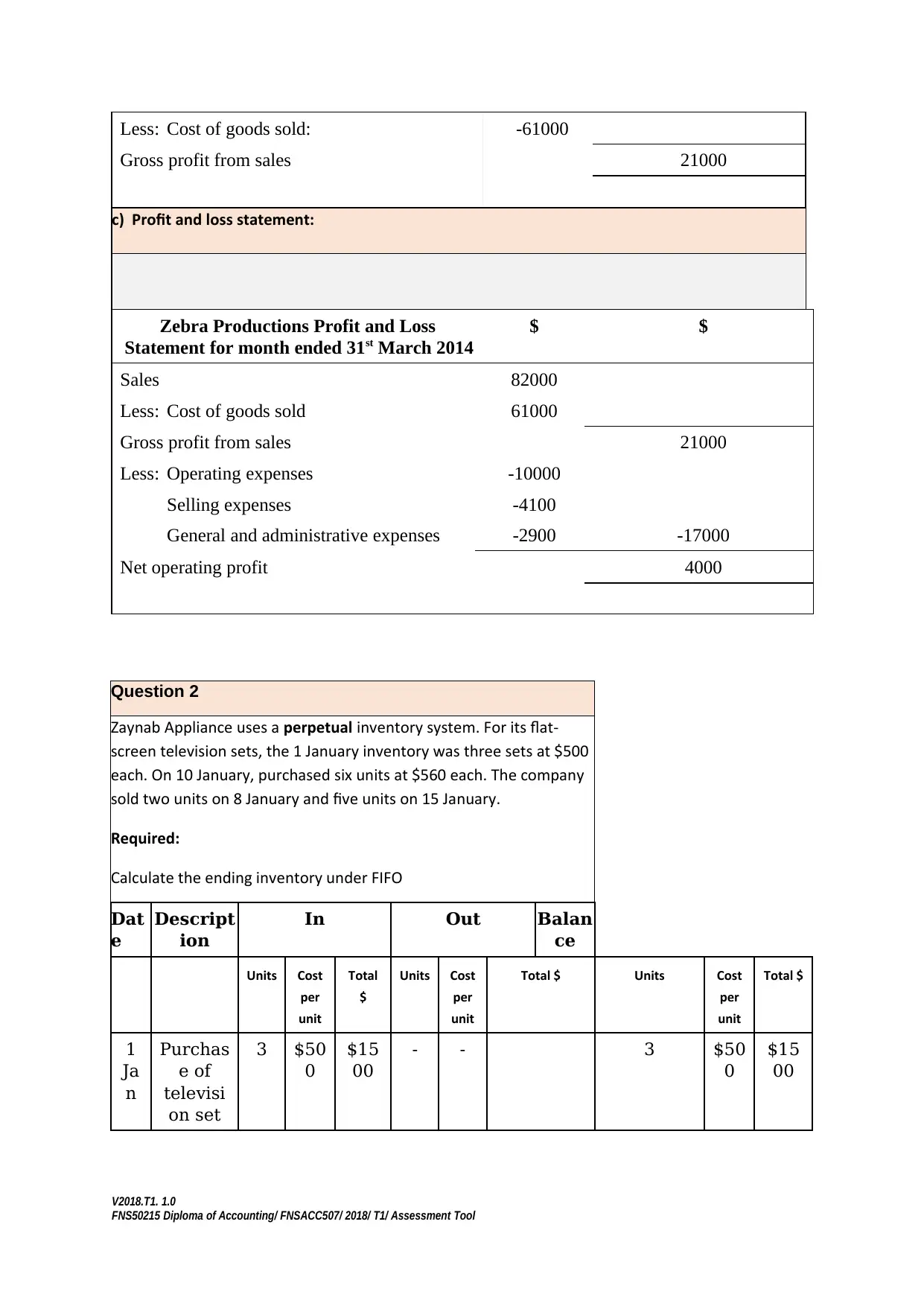

Less: Cost of goods sold: -61000

Gross profit from sales 21000

c) Profit and loss statement:

Zebra Productions Profit and Loss

Statement for month ended 31st March 2014

$ $

Sales 82000

Less: Cost of goods sold 61000

Gross profit from sales 21000

Less: Operating expenses -10000

Selling expenses -4100

General and administrative expenses -2900 -17000

Net operating profit 4000

Question 2

Zaynab Appliance uses a perpetual inventory system. For its flat-

screen television sets, the 1 January inventory was three sets at $500

each. On 10 January, purchased six units at $560 each. The company

sold two units on 8 January and five units on 15 January.

Required:

Calculate the ending inventory under FIFO

Dat

e

Descript

ion

In Out Balan

ce

Units Cost

per

unit

Total

$

Units Cost

per

unit

Total $ Units Cost

per

unit

Total $

1

Ja

n

Purchas

e of

televisi

on set

3 $50

0

$15

00

- - 3 $50

0

$15

00

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Gross profit from sales 21000

c) Profit and loss statement:

Zebra Productions Profit and Loss

Statement for month ended 31st March 2014

$ $

Sales 82000

Less: Cost of goods sold 61000

Gross profit from sales 21000

Less: Operating expenses -10000

Selling expenses -4100

General and administrative expenses -2900 -17000

Net operating profit 4000

Question 2

Zaynab Appliance uses a perpetual inventory system. For its flat-

screen television sets, the 1 January inventory was three sets at $500

each. On 10 January, purchased six units at $560 each. The company

sold two units on 8 January and five units on 15 January.

Required:

Calculate the ending inventory under FIFO

Dat

e

Descript

ion

In Out Balan

ce

Units Cost

per

unit

Total

$

Units Cost

per

unit

Total $ Units Cost

per

unit

Total $

1

Ja

n

Purchas

e of

televisi

on set

3 $50

0

$15

00

- - 3 $50

0

$15

00

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

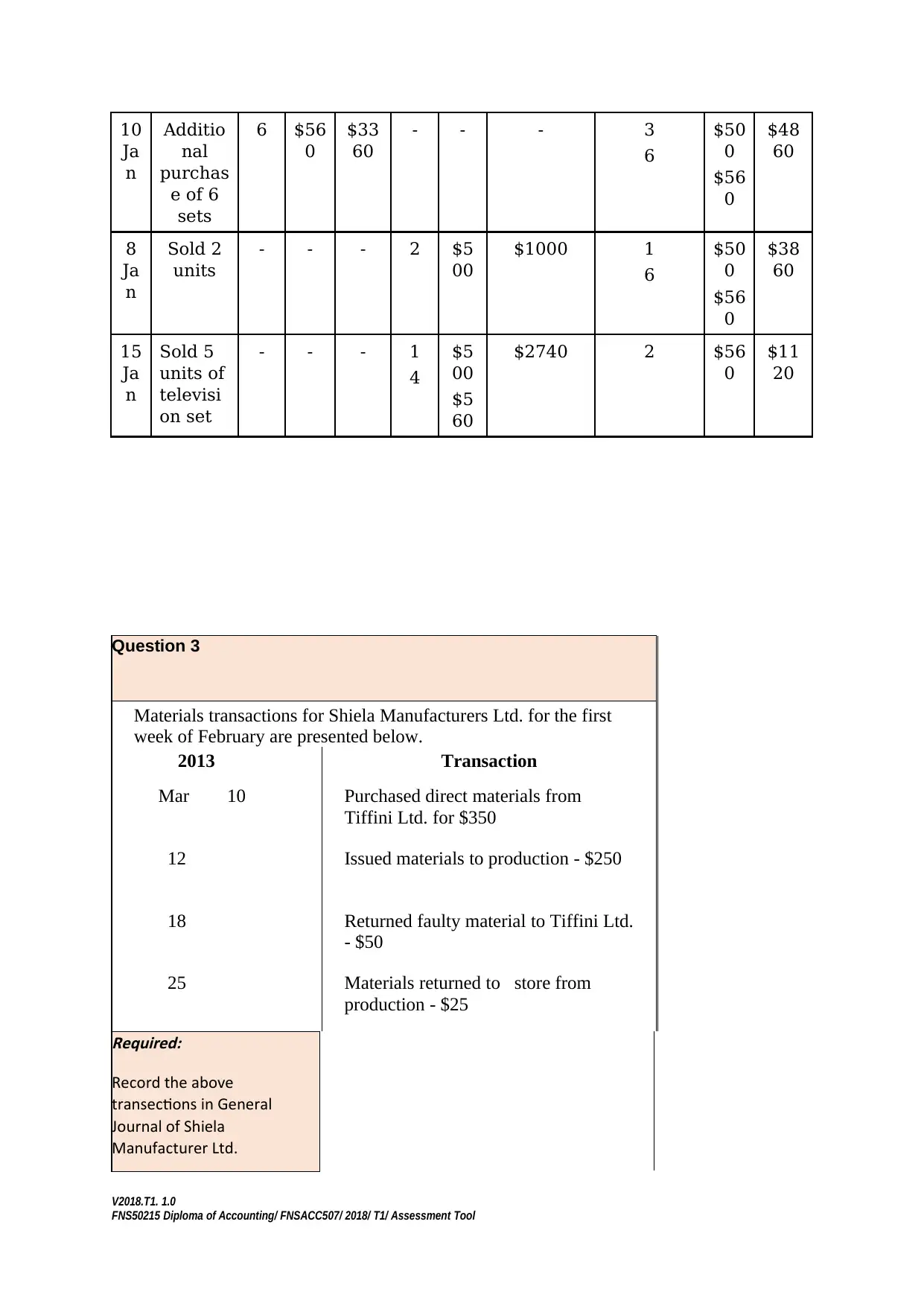

10

Ja

n

Additio

nal

purchas

e of 6

sets

6 $56

0

$33

60

- - - 3

6

$50

0

$56

0

$48

60

8

Ja

n

Sold 2

units

- - - 2 $5

00

$1000 1

6

$50

0

$56

0

$38

60

15

Ja

n

Sold 5

units of

televisi

on set

- - - 1

4

$5

00

$5

60

$2740 2 $56

0

$11

20

Question 3

Materials transactions for Shiela Manufacturers Ltd. for the first

week of February are presented below.

2013 Transaction

Mar 10 Purchased direct materials from

Tiffini Ltd. for $350

12 Issued materials to production - $250

18 Returned faulty material to Tiffini Ltd.

- $50

25 Materials returned to store from

production - $25Required:

Record the above

transections in General

Journal of Shiela

Manufacturer Ltd.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Ja

n

Additio

nal

purchas

e of 6

sets

6 $56

0

$33

60

- - - 3

6

$50

0

$56

0

$48

60

8

Ja

n

Sold 2

units

- - - 2 $5

00

$1000 1

6

$50

0

$56

0

$38

60

15

Ja

n

Sold 5

units of

televisi

on set

- - - 1

4

$5

00

$5

60

$2740 2 $56

0

$11

20

Question 3

Materials transactions for Shiela Manufacturers Ltd. for the first

week of February are presented below.

2013 Transaction

Mar 10 Purchased direct materials from

Tiffini Ltd. for $350

12 Issued materials to production - $250

18 Returned faulty material to Tiffini Ltd.

- $50

25 Materials returned to store from

production - $25Required:

Record the above

transections in General

Journal of Shiela

Manufacturer Ltd.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

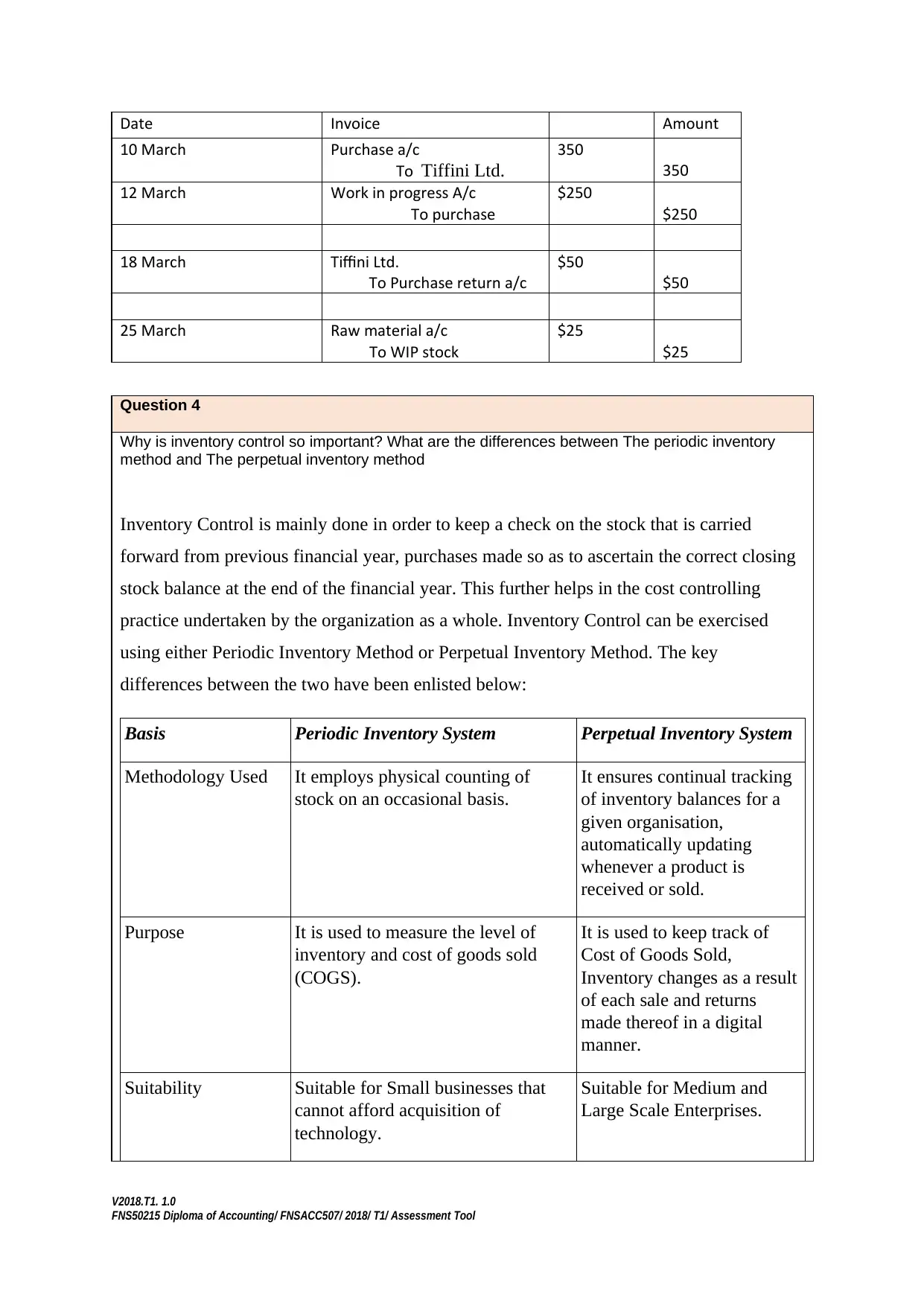

Date Invoice Amount

10 March Purchase a/c

To Tiffini Ltd.

350

350

12 March Work in progress A/c

To purchase

$250

$250

18 March Tiffini Ltd.

To Purchase return a/c

$50

$50

25 March Raw material a/c

To WIP stock

$25

$25

Question 4

Why is inventory control so important? What are the differences between The periodic inventory

method and The perpetual inventory method

Inventory Control is mainly done in order to keep a check on the stock that is carried

forward from previous financial year, purchases made so as to ascertain the correct closing

stock balance at the end of the financial year. This further helps in the cost controlling

practice undertaken by the organization as a whole. Inventory Control can be exercised

using either Periodic Inventory Method or Perpetual Inventory Method. The key

differences between the two have been enlisted below:

Basis Periodic Inventory System Perpetual Inventory System

Methodology Used It employs physical counting of

stock on an occasional basis.

It ensures continual tracking

of inventory balances for a

given organisation,

automatically updating

whenever a product is

received or sold.

Purpose It is used to measure the level of

inventory and cost of goods sold

(COGS).

It is used to keep track of

Cost of Goods Sold,

Inventory changes as a result

of each sale and returns

made thereof in a digital

manner.

Suitability Suitable for Small businesses that

cannot afford acquisition of

technology.

Suitable for Medium and

Large Scale Enterprises.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

10 March Purchase a/c

To Tiffini Ltd.

350

350

12 March Work in progress A/c

To purchase

$250

$250

18 March Tiffini Ltd.

To Purchase return a/c

$50

$50

25 March Raw material a/c

To WIP stock

$25

$25

Question 4

Why is inventory control so important? What are the differences between The periodic inventory

method and The perpetual inventory method

Inventory Control is mainly done in order to keep a check on the stock that is carried

forward from previous financial year, purchases made so as to ascertain the correct closing

stock balance at the end of the financial year. This further helps in the cost controlling

practice undertaken by the organization as a whole. Inventory Control can be exercised

using either Periodic Inventory Method or Perpetual Inventory Method. The key

differences between the two have been enlisted below:

Basis Periodic Inventory System Perpetual Inventory System

Methodology Used It employs physical counting of

stock on an occasional basis.

It ensures continual tracking

of inventory balances for a

given organisation,

automatically updating

whenever a product is

received or sold.

Purpose It is used to measure the level of

inventory and cost of goods sold

(COGS).

It is used to keep track of

Cost of Goods Sold,

Inventory changes as a result

of each sale and returns

made thereof in a digital

manner.

Suitability Suitable for Small businesses that

cannot afford acquisition of

technology.

Suitable for Medium and

Large Scale Enterprises.

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Assessment

Feedback One

Evaluation

Unit name:

FNSACC507 Provide

management accounting

information

Assessment Submission

Checklist to be completed

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Feedback One

Evaluation

Unit name:

FNSACC507 Provide

management accounting

information

Assessment Submission

Checklist to be completed

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

by the Trainer/Assessor

Did the student complete

and provide evidence for the

following:

Yes No

1. Provide a discussion

on the short questions?

2. Provide an analysis

for costs classification?

3. Provide an

understanding of

inventory calculation?

4. Submit within agreed

timeframe?

Has the learner proven they

can: Yes No

1.1. Identify and establish

systems to generate

operating and cost data

1.2 Systematically code,

classify and check data

for accuracy and

reliability in accordance

with organisational policy

and procedures

2.1 Analyse costs and

identify cost behaviour

characteristics

2.2 Assign costs to specified

products, services and

organisational units, and

reconcile data to ensure

calculations are accurate

and comply with

organisational

procedures

2.3 Ensure interpretation of

revenues and costs is

supported by valid

analysis and is

consistent with

organisation’s business

performance objectives

FEEDBACK TO STUDENT:

Assessment outcome Satisfactory Not Yet Satisfactory Re-assessment required

Student Signature The result of my performance in this

unit has been discussed and explained

to me.

_______________________

_____

Date:

________

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Did the student complete

and provide evidence for the

following:

Yes No

1. Provide a discussion

on the short questions?

2. Provide an analysis

for costs classification?

3. Provide an

understanding of

inventory calculation?

4. Submit within agreed

timeframe?

Has the learner proven they

can: Yes No

1.1. Identify and establish

systems to generate

operating and cost data

1.2 Systematically code,

classify and check data

for accuracy and

reliability in accordance

with organisational policy

and procedures

2.1 Analyse costs and

identify cost behaviour

characteristics

2.2 Assign costs to specified

products, services and

organisational units, and

reconcile data to ensure

calculations are accurate

and comply with

organisational

procedures

2.3 Ensure interpretation of

revenues and costs is

supported by valid

analysis and is

consistent with

organisation’s business

performance objectives

FEEDBACK TO STUDENT:

Assessment outcome Satisfactory Not Yet Satisfactory Re-assessment required

Student Signature The result of my performance in this

unit has been discussed and explained

to me.

_______________________

_____

Date:

________

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

______

Student signature

Trainer/ Assessor’s

Signature

Trainer/ Assessor’s

declaratio

n:

I hereby certify that the above student

has been

assessed by

myself and all

assessments

are carried

out as

required by

the Principles

of

Assessments

(Clause 1.8 of

the Standards

for RTO

2015).

_______________________

_____

Date:

________

______

Assessor signature

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

Student signature

Trainer/ Assessor’s

Signature

Trainer/ Assessor’s

declaratio

n:

I hereby certify that the above student

has been

assessed by

myself and all

assessments

are carried

out as

required by

the Principles

of

Assessments

(Clause 1.8 of

the Standards

for RTO

2015).

_______________________

_____

Date:

________

______

Assessor signature

V2018.T1. 1.0

FNS50215 Diploma of Accounting/ FNSACC507/ 2018/ T1/ Assessment Tool

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.