Financial Analysis of Concetta Ltd.: Job Costing Assignment

VerifiedAdded on 2022/11/24

|8

|1770

|55

Homework Assignment

AI Summary

This assignment solution analyzes the job costing methods used by Concetta Ltd. It begins by explaining the appropriateness of job costing for specialized goods and provides examples of companies where it is applicable. The solution then addresses the calculation of ending Work in Process (WIP) in...

For, Concetta Ltd. 2019

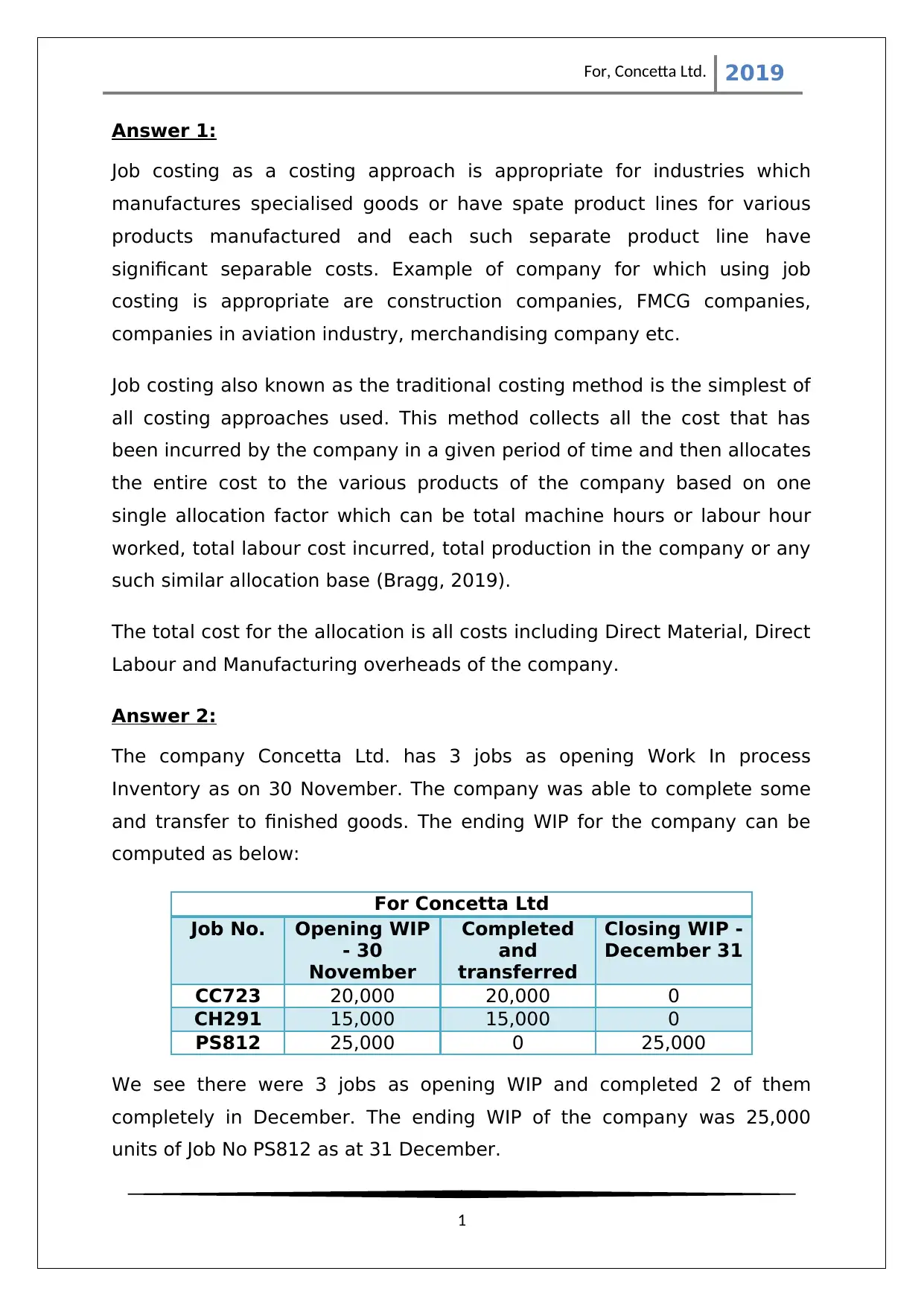

Answer 1:

Job costing as a costing approach is appropriate for industries which

manufactures specialised goods or have spate product lines for various

products manufactured and each such separate product line have

significant separable costs. Example of company for which using job

costing is appropriate are construction companies, FMCG companies,

companies in aviation industry, merchandising company etc.

Job costing also known as the traditional costing method is the simplest of

all costing approaches used. This method collects all the cost that has

been incurred by the company in a given period of time and then allocates

the entire cost to the various products of the company based on one

single allocation factor which can be total machine hours or labour hour

worked, total labour cost incurred, total production in the company or any

such similar allocation base (Bragg, 2019).

The total cost for the allocation is all costs including Direct Material, Direct

Labour and Manufacturing overheads of the company.

Answer 2:

The company Concetta Ltd. has 3 jobs as opening Work In process

Inventory as on 30 November. The company was able to complete some

and transfer to finished goods. The ending WIP for the company can be

computed as below:

For Concetta Ltd

Job No. Opening WIP

- 30

November

Completed

and

transferred

Closing WIP -

December 31

CC723 20,000 20,000 0

CH291 15,000 15,000 0

PS812 25,000 0 25,000

We see there were 3 jobs as opening WIP and completed 2 of them

completely in December. The ending WIP of the company was 25,000

units of Job No PS812 as at 31 December.

1

Answer 1:

Job costing as a costing approach is appropriate for industries which

manufactures specialised goods or have spate product lines for various

products manufactured and each such separate product line have

significant separable costs. Example of company for which using job

costing is appropriate are construction companies, FMCG companies,

companies in aviation industry, merchandising company etc.

Job costing also known as the traditional costing method is the simplest of

all costing approaches used. This method collects all the cost that has

been incurred by the company in a given period of time and then allocates

the entire cost to the various products of the company based on one

single allocation factor which can be total machine hours or labour hour

worked, total labour cost incurred, total production in the company or any

such similar allocation base (Bragg, 2019).

The total cost for the allocation is all costs including Direct Material, Direct

Labour and Manufacturing overheads of the company.

Answer 2:

The company Concetta Ltd. has 3 jobs as opening Work In process

Inventory as on 30 November. The company was able to complete some

and transfer to finished goods. The ending WIP for the company can be

computed as below:

For Concetta Ltd

Job No. Opening WIP

- 30

November

Completed

and

transferred

Closing WIP -

December 31

CC723 20,000 20,000 0

CH291 15,000 15,000 0

PS812 25,000 0 25,000

We see there were 3 jobs as opening WIP and completed 2 of them

completely in December. The ending WIP of the company was 25,000

units of Job No PS812 as at 31 December.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For, Concetta Ltd. 2019

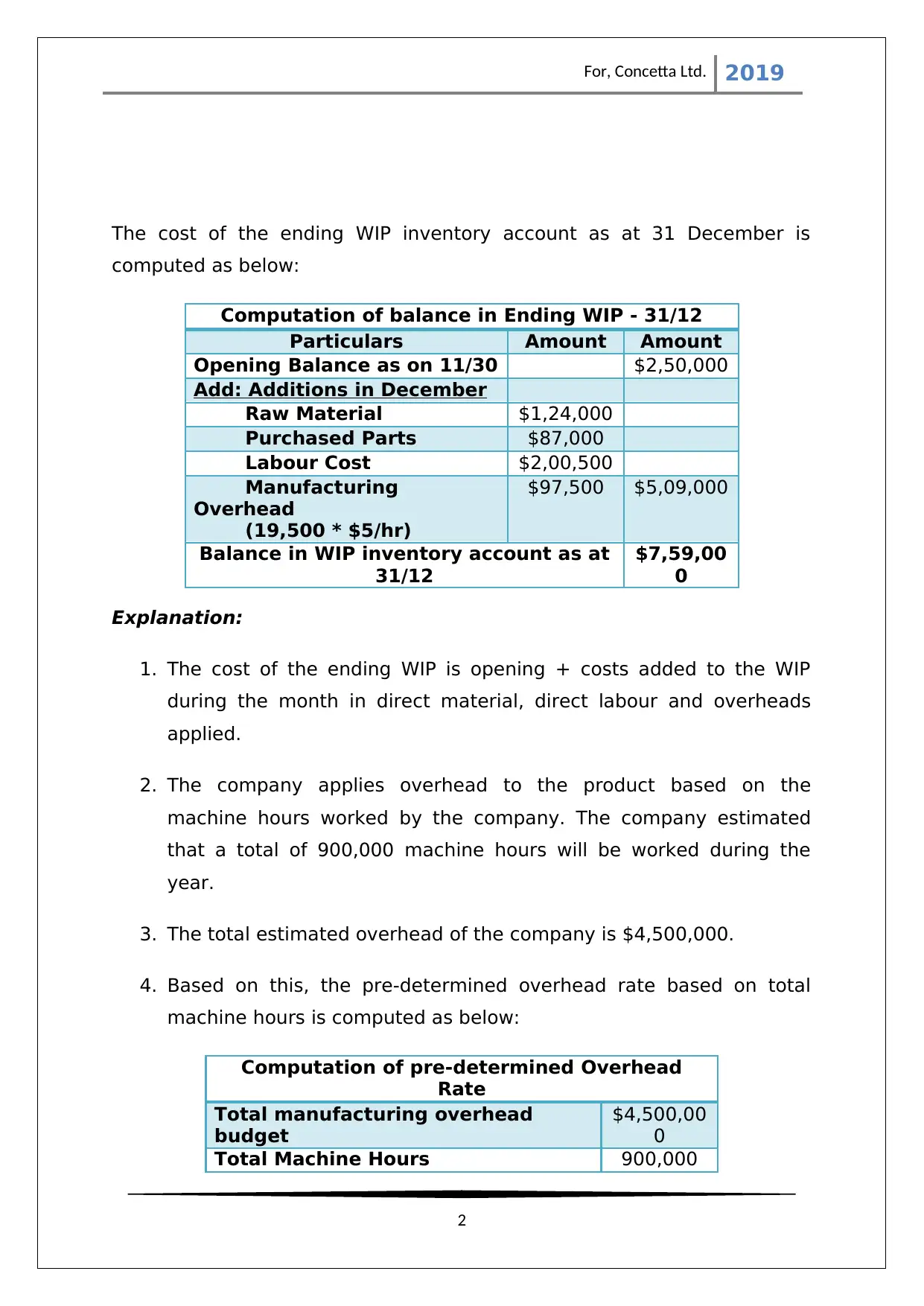

The cost of the ending WIP inventory account as at 31 December is

computed as below:

Computation of balance in Ending WIP - 31/12

Particulars Amount Amount

Opening Balance as on 11/30 $2,50,000

Add: Additions in December

Raw Material $1,24,000

Purchased Parts $87,000

Labour Cost $2,00,500

Manufacturing

Overhead

(19,500 * $5/hr)

$97,500 $5,09,000

Balance in WIP inventory account as at

31/12

$7,59,00

0

Explanation:

1. The cost of the ending WIP is opening + costs added to the WIP

during the month in direct material, direct labour and overheads

applied.

2. The company applies overhead to the product based on the

machine hours worked by the company. The company estimated

that a total of 900,000 machine hours will be worked during the

year.

3. The total estimated overhead of the company is $4,500,000.

4. Based on this, the pre-determined overhead rate based on total

machine hours is computed as below:

Computation of pre-determined Overhead

Rate

Total manufacturing overhead

budget

$4,500,00

0

Total Machine Hours 900,000

2

The cost of the ending WIP inventory account as at 31 December is

computed as below:

Computation of balance in Ending WIP - 31/12

Particulars Amount Amount

Opening Balance as on 11/30 $2,50,000

Add: Additions in December

Raw Material $1,24,000

Purchased Parts $87,000

Labour Cost $2,00,500

Manufacturing

Overhead

(19,500 * $5/hr)

$97,500 $5,09,000

Balance in WIP inventory account as at

31/12

$7,59,00

0

Explanation:

1. The cost of the ending WIP is opening + costs added to the WIP

during the month in direct material, direct labour and overheads

applied.

2. The company applies overhead to the product based on the

machine hours worked by the company. The company estimated

that a total of 900,000 machine hours will be worked during the

year.

3. The total estimated overhead of the company is $4,500,000.

4. Based on this, the pre-determined overhead rate based on total

machine hours is computed as below:

Computation of pre-determined Overhead

Rate

Total manufacturing overhead

budget

$4,500,00

0

Total Machine Hours 900,000

2

For, Concetta Ltd. 2019

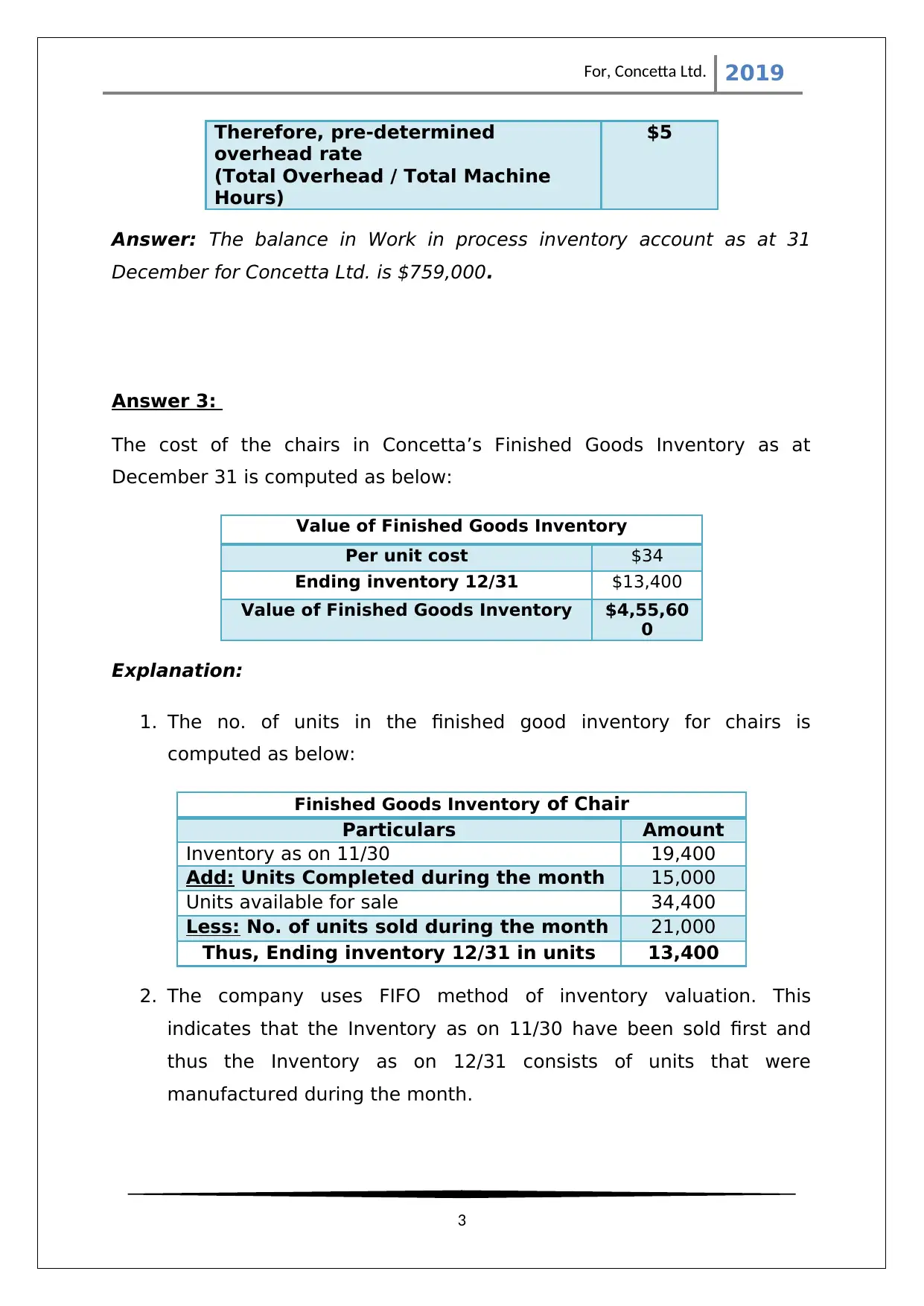

Therefore, pre-determined

overhead rate

(Total Overhead / Total Machine

Hours)

$5

Answer: The balance in Work in process inventory account as at 31

December for Concetta Ltd. is $759,000.

Answer 3:

The cost of the chairs in Concetta’s Finished Goods Inventory as at

December 31 is computed as below:

Value of Finished Goods Inventory

Per unit cost $34

Ending inventory 12/31 $13,400

Value of Finished Goods Inventory $4,55,60

0

Explanation:

1. The no. of units in the finished good inventory for chairs is

computed as below:

Finished Goods Inventory of Chair

Particulars Amount

Inventory as on 11/30 19,400

Add: Units Completed during the month 15,000

Units available for sale 34,400

Less: No. of units sold during the month 21,000

Thus, Ending inventory 12/31 in units 13,400

2. The company uses FIFO method of inventory valuation. This

indicates that the Inventory as on 11/30 have been sold first and

thus the Inventory as on 12/31 consists of units that were

manufactured during the month.

3

Therefore, pre-determined

overhead rate

(Total Overhead / Total Machine

Hours)

$5

Answer: The balance in Work in process inventory account as at 31

December for Concetta Ltd. is $759,000.

Answer 3:

The cost of the chairs in Concetta’s Finished Goods Inventory as at

December 31 is computed as below:

Value of Finished Goods Inventory

Per unit cost $34

Ending inventory 12/31 $13,400

Value of Finished Goods Inventory $4,55,60

0

Explanation:

1. The no. of units in the finished good inventory for chairs is

computed as below:

Finished Goods Inventory of Chair

Particulars Amount

Inventory as on 11/30 19,400

Add: Units Completed during the month 15,000

Units available for sale 34,400

Less: No. of units sold during the month 21,000

Thus, Ending inventory 12/31 in units 13,400

2. The company uses FIFO method of inventory valuation. This

indicates that the Inventory as on 11/30 have been sold first and

thus the Inventory as on 12/31 consists of units that were

manufactured during the month.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For, Concetta Ltd. 2019

3. The cost of the 15,000 units that were manufactured during the

month is computed as below:

Units of Chairs Completed in December

Particulars Amount Amount

WIP Inventory as on 11/30 $4,31,000

Add: Additions in December

Raw Material, $3,000

Purchased Parts $10,800

Labour Cost $43,200

Manufacturing

Overhead

(4,400 * $5/hr)

$22,000 $79,000

Total Cost of the Chairs in the

month

$5,10,00

0

4. Based on total cost $510,000 for 15,000 units manufactured during

the month. The per unit rate is computed as below:

Per unit cost of Chairs Produced

Total Chairs Manufactured during the

month

15,000

Total Cost of the Chairs in the month $5,10,00

0

Per unit cost $34

5. The ending inventory is then simply this per unit cost * units in

ending inventory.

Answer: The cost of the chairs in Concetta’s Finished Goods Inventory as

at December 31 is $455,600.

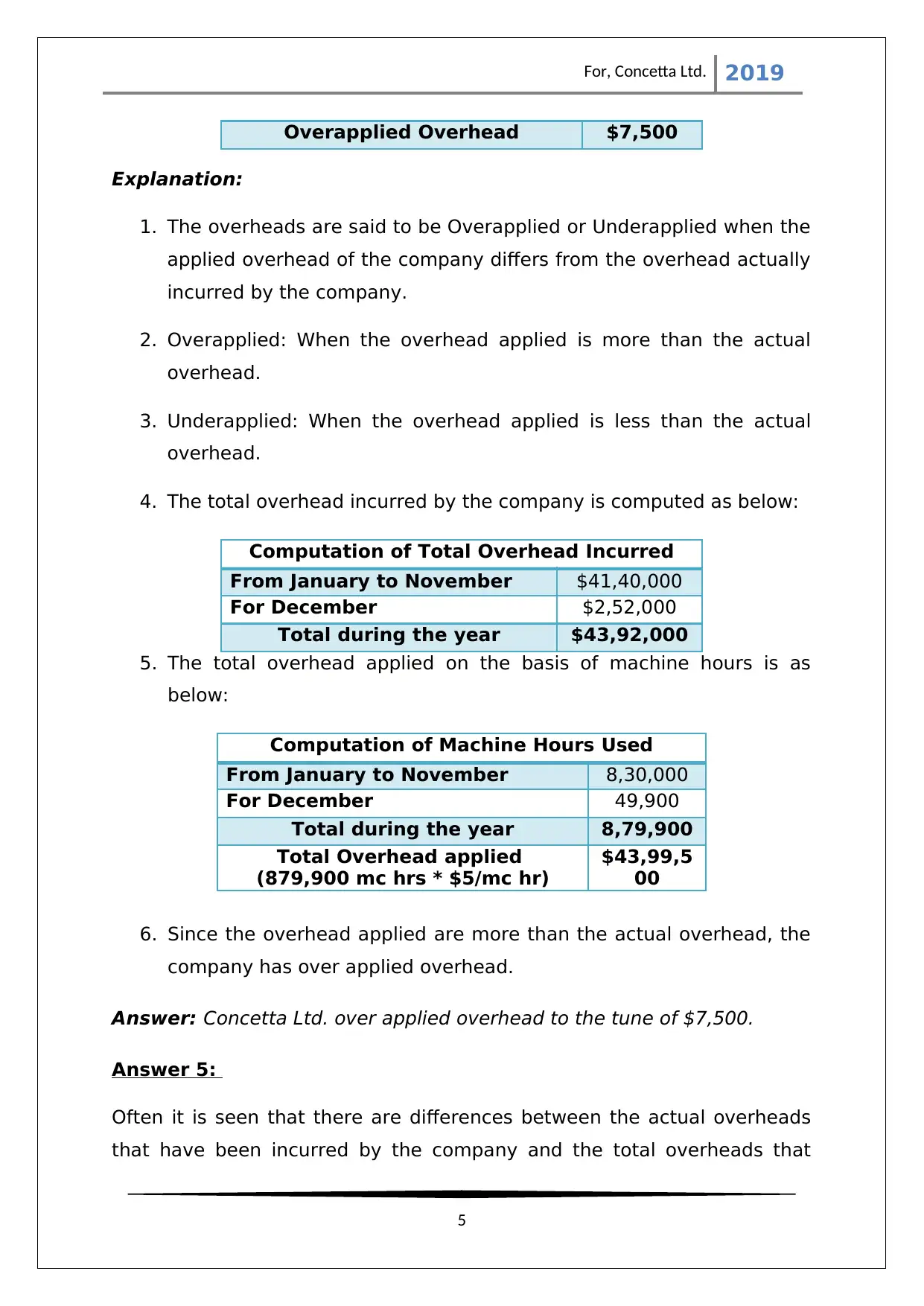

Answer 4:

The overapplied or underapplied overhead for the company is computed

as below:

Overapplied Overhead

Overhead applied during the

year

$43,99,50

0

Actual Overhead incurred $43,92,00

0

4

3. The cost of the 15,000 units that were manufactured during the

month is computed as below:

Units of Chairs Completed in December

Particulars Amount Amount

WIP Inventory as on 11/30 $4,31,000

Add: Additions in December

Raw Material, $3,000

Purchased Parts $10,800

Labour Cost $43,200

Manufacturing

Overhead

(4,400 * $5/hr)

$22,000 $79,000

Total Cost of the Chairs in the

month

$5,10,00

0

4. Based on total cost $510,000 for 15,000 units manufactured during

the month. The per unit rate is computed as below:

Per unit cost of Chairs Produced

Total Chairs Manufactured during the

month

15,000

Total Cost of the Chairs in the month $5,10,00

0

Per unit cost $34

5. The ending inventory is then simply this per unit cost * units in

ending inventory.

Answer: The cost of the chairs in Concetta’s Finished Goods Inventory as

at December 31 is $455,600.

Answer 4:

The overapplied or underapplied overhead for the company is computed

as below:

Overapplied Overhead

Overhead applied during the

year

$43,99,50

0

Actual Overhead incurred $43,92,00

0

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For, Concetta Ltd. 2019

Overapplied Overhead $7,500

Explanation:

1. The overheads are said to be Overapplied or Underapplied when the

applied overhead of the company differs from the overhead actually

incurred by the company.

2. Overapplied: When the overhead applied is more than the actual

overhead.

3. Underapplied: When the overhead applied is less than the actual

overhead.

4. The total overhead incurred by the company is computed as below:

Computation of Total Overhead Incurred

From January to November $41,40,000

For December $2,52,000

Total during the year $43,92,000

5. The total overhead applied on the basis of machine hours is as

below:

Computation of Machine Hours Used

From January to November 8,30,000

For December 49,900

Total during the year 8,79,900

Total Overhead applied

(879,900 mc hrs * $5/mc hr)

$43,99,5

00

6. Since the overhead applied are more than the actual overhead, the

company has over applied overhead.

Answer: Concetta Ltd. over applied overhead to the tune of $7,500.

Answer 5:

Often it is seen that there are differences between the actual overheads

that have been incurred by the company and the total overheads that

5

Overapplied Overhead $7,500

Explanation:

1. The overheads are said to be Overapplied or Underapplied when the

applied overhead of the company differs from the overhead actually

incurred by the company.

2. Overapplied: When the overhead applied is more than the actual

overhead.

3. Underapplied: When the overhead applied is less than the actual

overhead.

4. The total overhead incurred by the company is computed as below:

Computation of Total Overhead Incurred

From January to November $41,40,000

For December $2,52,000

Total during the year $43,92,000

5. The total overhead applied on the basis of machine hours is as

below:

Computation of Machine Hours Used

From January to November 8,30,000

For December 49,900

Total during the year 8,79,900

Total Overhead applied

(879,900 mc hrs * $5/mc hr)

$43,99,5

00

6. Since the overhead applied are more than the actual overhead, the

company has over applied overhead.

Answer: Concetta Ltd. over applied overhead to the tune of $7,500.

Answer 5:

Often it is seen that there are differences between the actual overheads

that have been incurred by the company and the total overheads that

5

For, Concetta Ltd. 2019

have been applied by the company using principles of job costing method.

These differences refer to either over application of overheads (When the

actual overhead is less than the overhead applied by the company) or

under application of overheads (When the actual overhead is more than

the overhead applied by the company).

At the end of the financial year this difference must be balanced and for

doing so the company can use either of the two accounting treatments as

mentioned below:

Treatment – 1: Assign to Cost of Goods Sold and balance

When the difference between the actual and applied overhead is not

material in volume or nature, the same is simply adjusted (added for

under application and subtracted for over application) to the cost of goods

sold computed during the year.

This is feasible only when the differences are not substantial in amount

and will not affect the cost of goods sold exponentially, because if the

adjustment leads to unproportionate lower or higher cost of goods sold,

the profit for the year will be affected adversely giving misguiding results.

The allocation of the difference directly to the cost of goods sold balances

the difference during the given period of time.

Treatment – 2: Assign the difference to units worked on during the year

When the difference between the actual and applied overhead is material

in volume or nature, adjusting it with the cost of goods sold will affect the

profitability of the company adversely. Keeping the view the requirement

that the accounts of the company should reflect true and fair view of the

state of affairs of the company, the same is not recommended.

In such a situation, the adjustment is made to all the products that were

affected during the year, be it the WIP, Finished goods inventory or sales

made. This is because the overheads were applied to these units only, and

6

have been applied by the company using principles of job costing method.

These differences refer to either over application of overheads (When the

actual overhead is less than the overhead applied by the company) or

under application of overheads (When the actual overhead is more than

the overhead applied by the company).

At the end of the financial year this difference must be balanced and for

doing so the company can use either of the two accounting treatments as

mentioned below:

Treatment – 1: Assign to Cost of Goods Sold and balance

When the difference between the actual and applied overhead is not

material in volume or nature, the same is simply adjusted (added for

under application and subtracted for over application) to the cost of goods

sold computed during the year.

This is feasible only when the differences are not substantial in amount

and will not affect the cost of goods sold exponentially, because if the

adjustment leads to unproportionate lower or higher cost of goods sold,

the profit for the year will be affected adversely giving misguiding results.

The allocation of the difference directly to the cost of goods sold balances

the difference during the given period of time.

Treatment – 2: Assign the difference to units worked on during the year

When the difference between the actual and applied overhead is material

in volume or nature, adjusting it with the cost of goods sold will affect the

profitability of the company adversely. Keeping the view the requirement

that the accounts of the company should reflect true and fair view of the

state of affairs of the company, the same is not recommended.

In such a situation, the adjustment is made to all the products that were

affected during the year, be it the WIP, Finished goods inventory or sales

made. This is because the overheads were applied to these units only, and

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For, Concetta Ltd. 2019

the difference is also adjusted with each of them reflecting their true cost

and ultimately the true profitability of the company.

Answer 6:

The activity based costing is a modern approach to costing wherein the

product costs of the organization is computed on the basis of the costs of

each activity that is being consumed by the product till it reaches a the

delivery point for the consumers. ABC starts with identification of the

underlying activities or resources of the organisation and then allocates

the resource costs to the products and/or services based on the usage of

these resources. This is a more robust approach of allocating overhead

costs to the products of an organization.

Both Conventional and ABC costing method allocates the cost of the

company to the product sold. The major point of difference between the

two is the allocation base that they use to allocate the costs to the

company to the products.

While, ABC costing starts with accumulation of overhead costs for each of

the resource activities of an organization, and then assignment of these

costs to various activity drivers based on their usage of the resource

activity, the conventional costing method uses a single plantwide rate for

overhead allocation.

7

the difference is also adjusted with each of them reflecting their true cost

and ultimately the true profitability of the company.

Answer 6:

The activity based costing is a modern approach to costing wherein the

product costs of the organization is computed on the basis of the costs of

each activity that is being consumed by the product till it reaches a the

delivery point for the consumers. ABC starts with identification of the

underlying activities or resources of the organisation and then allocates

the resource costs to the products and/or services based on the usage of

these resources. This is a more robust approach of allocating overhead

costs to the products of an organization.

Both Conventional and ABC costing method allocates the cost of the

company to the product sold. The major point of difference between the

two is the allocation base that they use to allocate the costs to the

company to the products.

While, ABC costing starts with accumulation of overhead costs for each of

the resource activities of an organization, and then assignment of these

costs to various activity drivers based on their usage of the resource

activity, the conventional costing method uses a single plantwide rate for

overhead allocation.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For, Concetta Ltd. 2019

References

AccountingCoach.com. (2019). Activity Based Costing | Explanation |

AccountingCoach. Retrieved from

https://www.accountingcoach.com/activity-based-costing/explanation

on 14 Apr. 2019

Bragg, S. (2019). Job costing. [online] AccountingTools. Retrieved from

https://www.accountingtools.com/articles/2017/5/14/job-costing on 14

Apr. 2019

Copeland, R. (2000). Managerial accounting. Houston, TX: Dame.

Garrison, R., Noreen, E. and Brewer, P. (n.d.). Managerial accounting.

Horngren, C.T., Datar, S.M., Rajan, M.V., M., Maguire, W. & Tan, R. (2018).

Cost Accounting: A Managerial Emphasis (3rd ed.). Frenchs Forest,

NSW: Pearson Australia

Jiambalvo, J. (n.d.). Managerial accounting.

Lucey, T. (2009). Costing. Australia: South-Western Cengage Learning.

Turney, P. (2012). Activity based costing. London: Kogan Page.

8

References

AccountingCoach.com. (2019). Activity Based Costing | Explanation |

AccountingCoach. Retrieved from

https://www.accountingcoach.com/activity-based-costing/explanation

on 14 Apr. 2019

Bragg, S. (2019). Job costing. [online] AccountingTools. Retrieved from

https://www.accountingtools.com/articles/2017/5/14/job-costing on 14

Apr. 2019

Copeland, R. (2000). Managerial accounting. Houston, TX: Dame.

Garrison, R., Noreen, E. and Brewer, P. (n.d.). Managerial accounting.

Horngren, C.T., Datar, S.M., Rajan, M.V., M., Maguire, W. & Tan, R. (2018).

Cost Accounting: A Managerial Emphasis (3rd ed.). Frenchs Forest,

NSW: Pearson Australia

Jiambalvo, J. (n.d.). Managerial accounting.

Lucey, T. (2009). Costing. Australia: South-Western Cengage Learning.

Turney, P. (2012). Activity based costing. London: Kogan Page.

8

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.