MGT723 Research Project: Green Gas Emission and Firm Disclosure

VerifiedAdded on 2023/06/12

|10

|1644

|302

Report

AI Summary

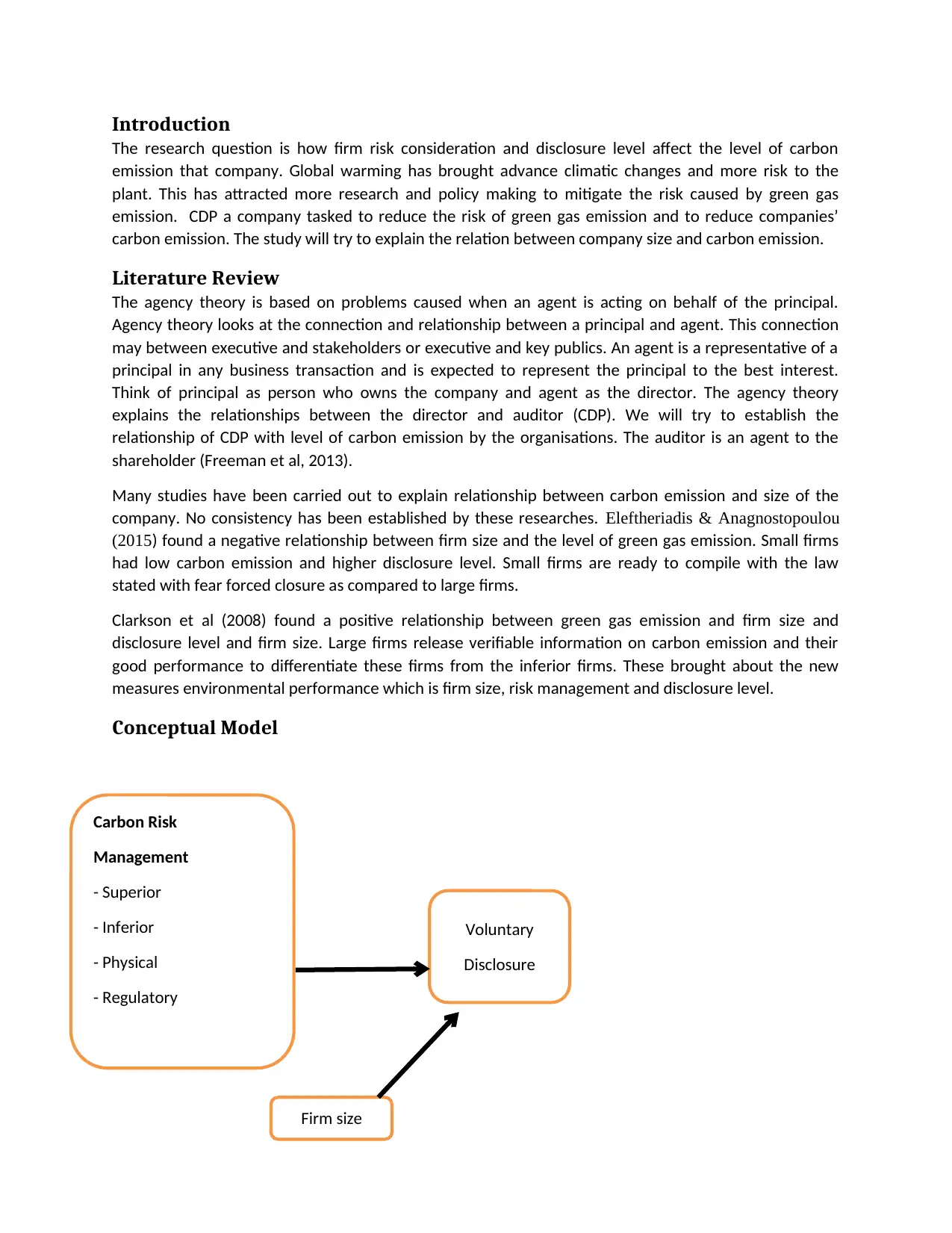

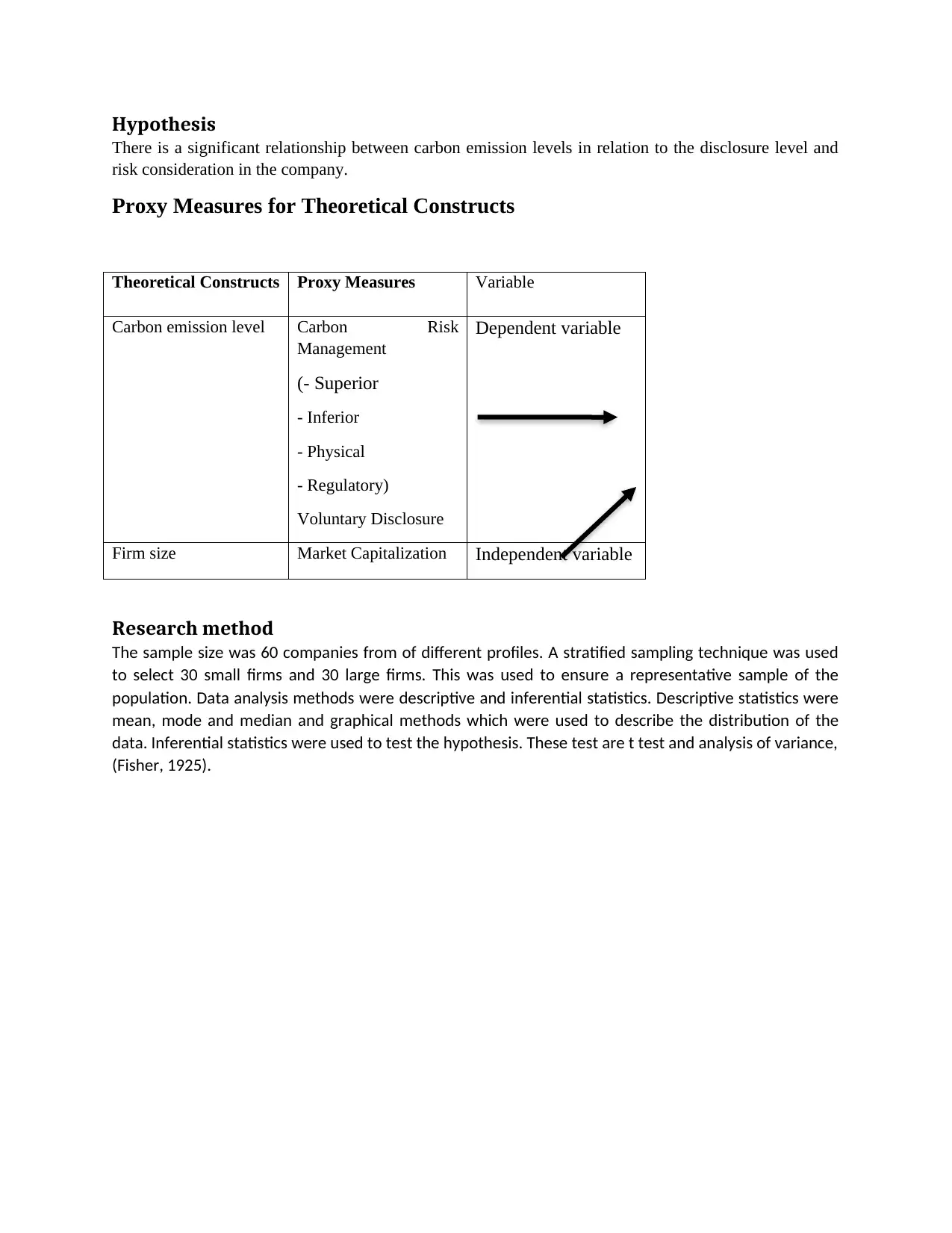

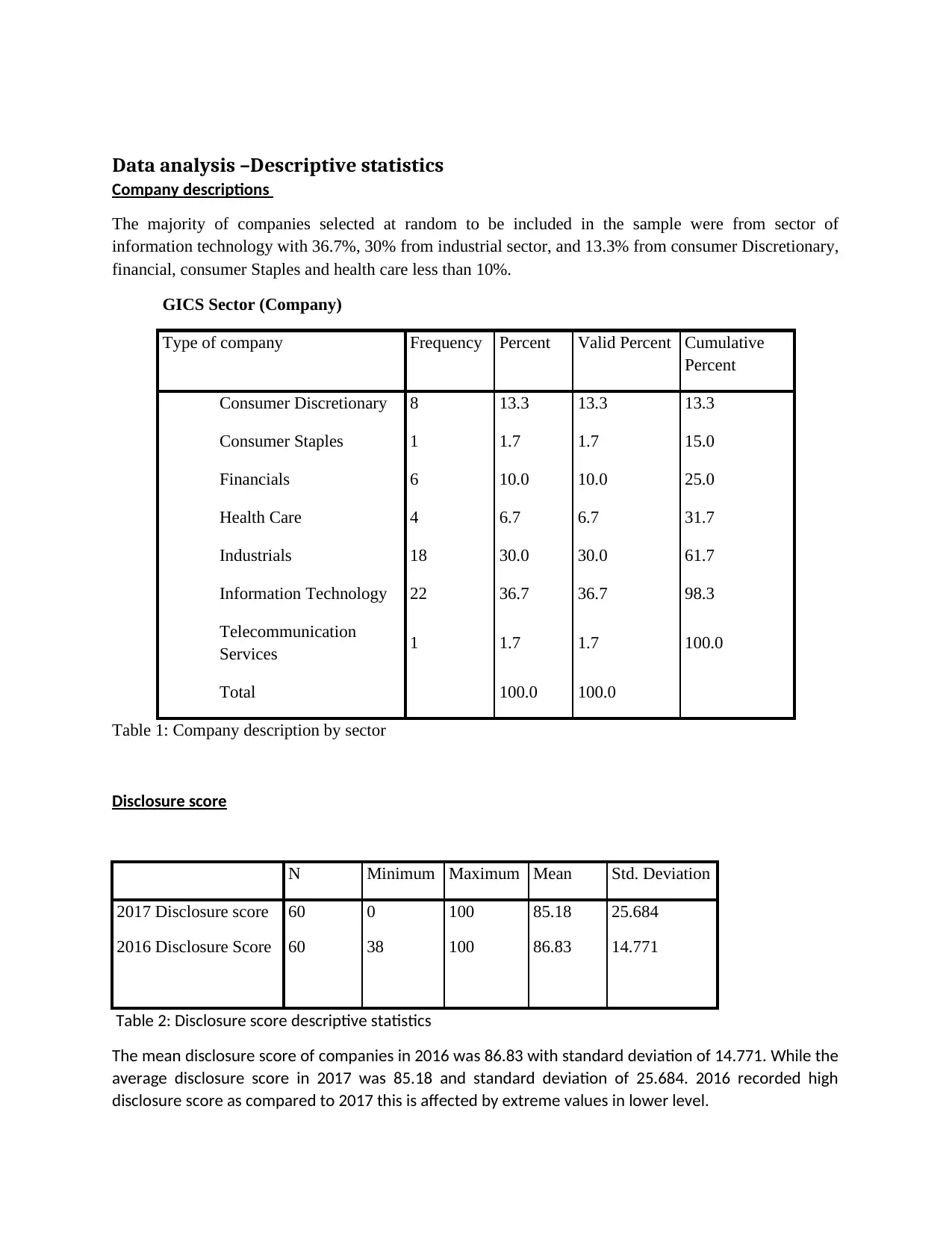

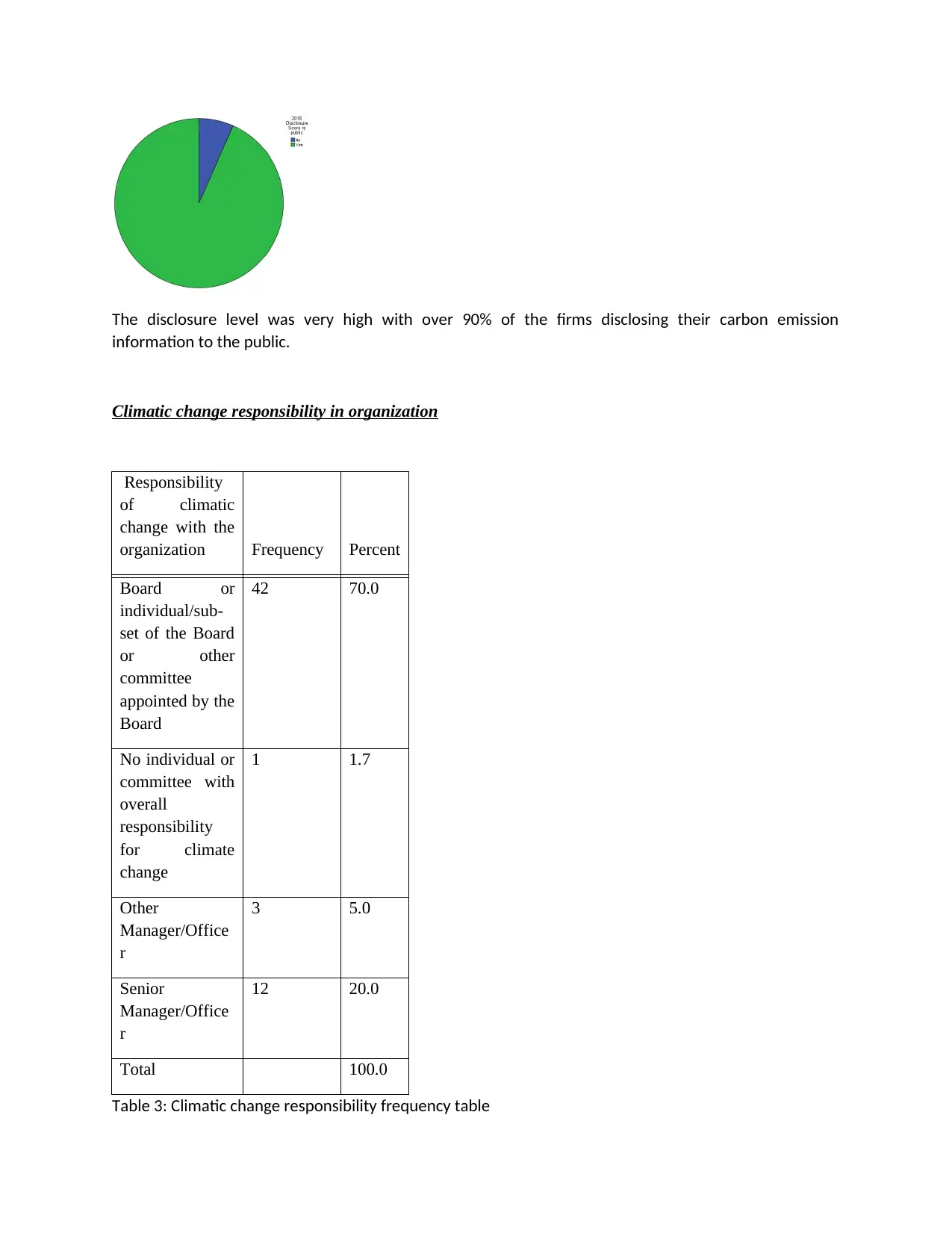

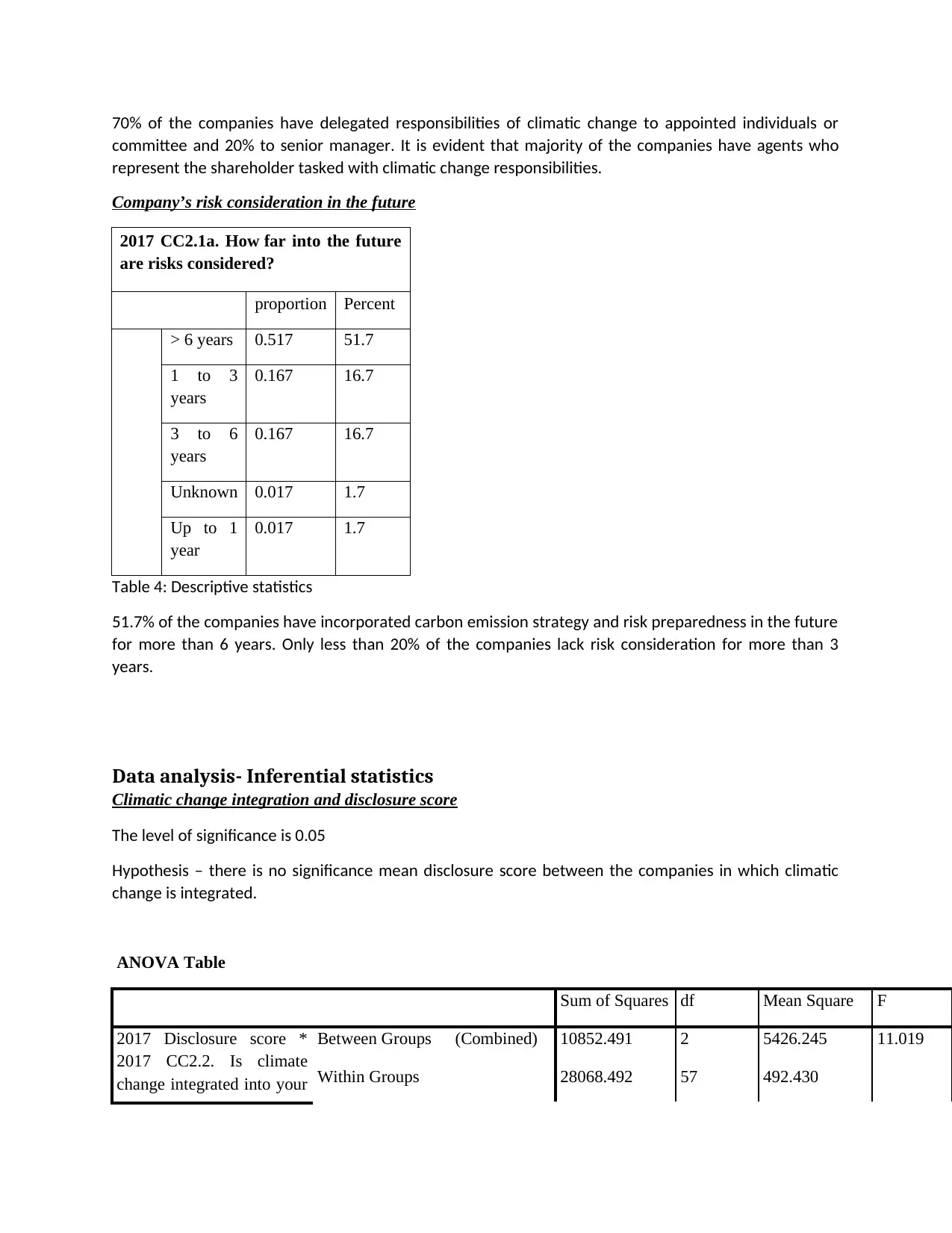

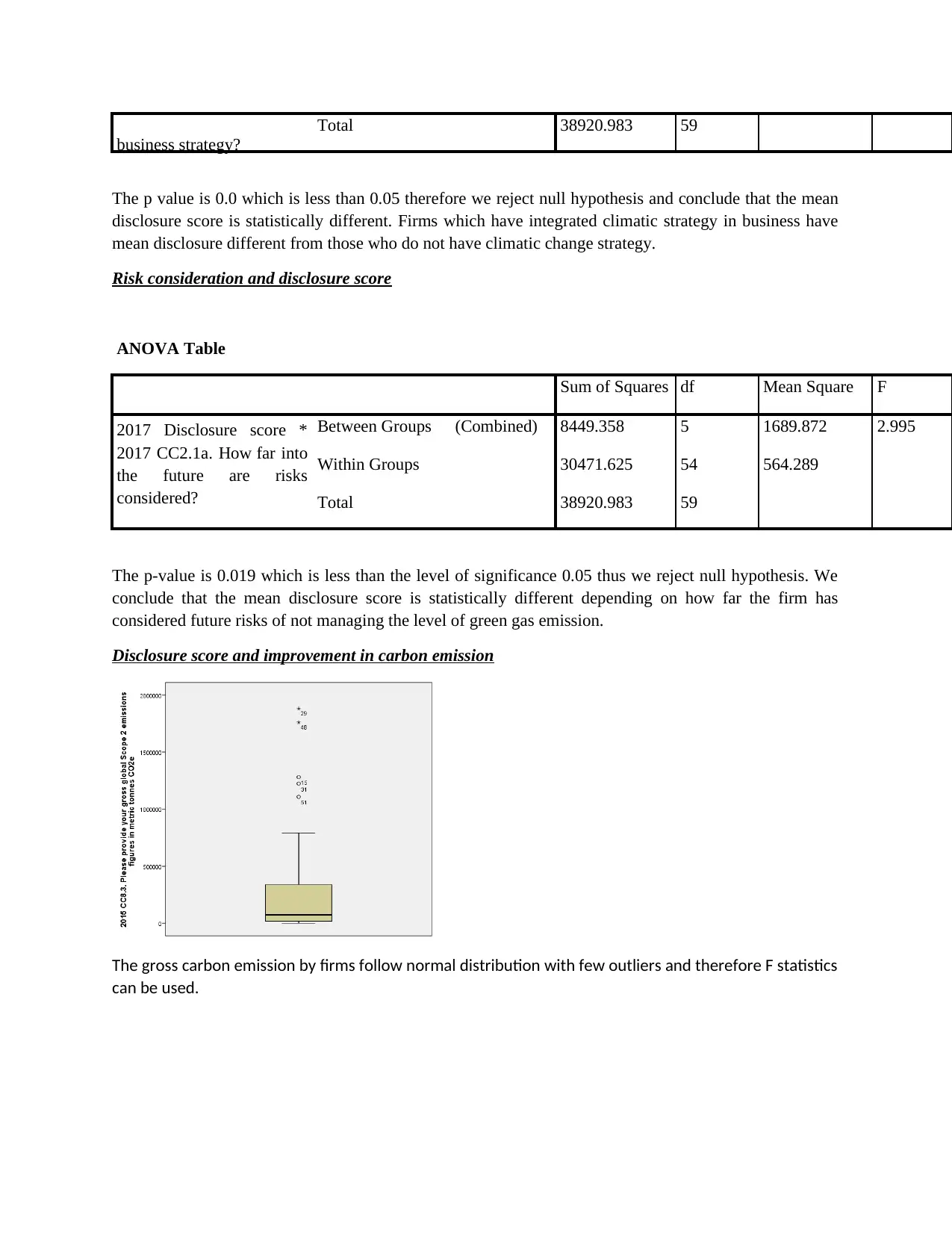

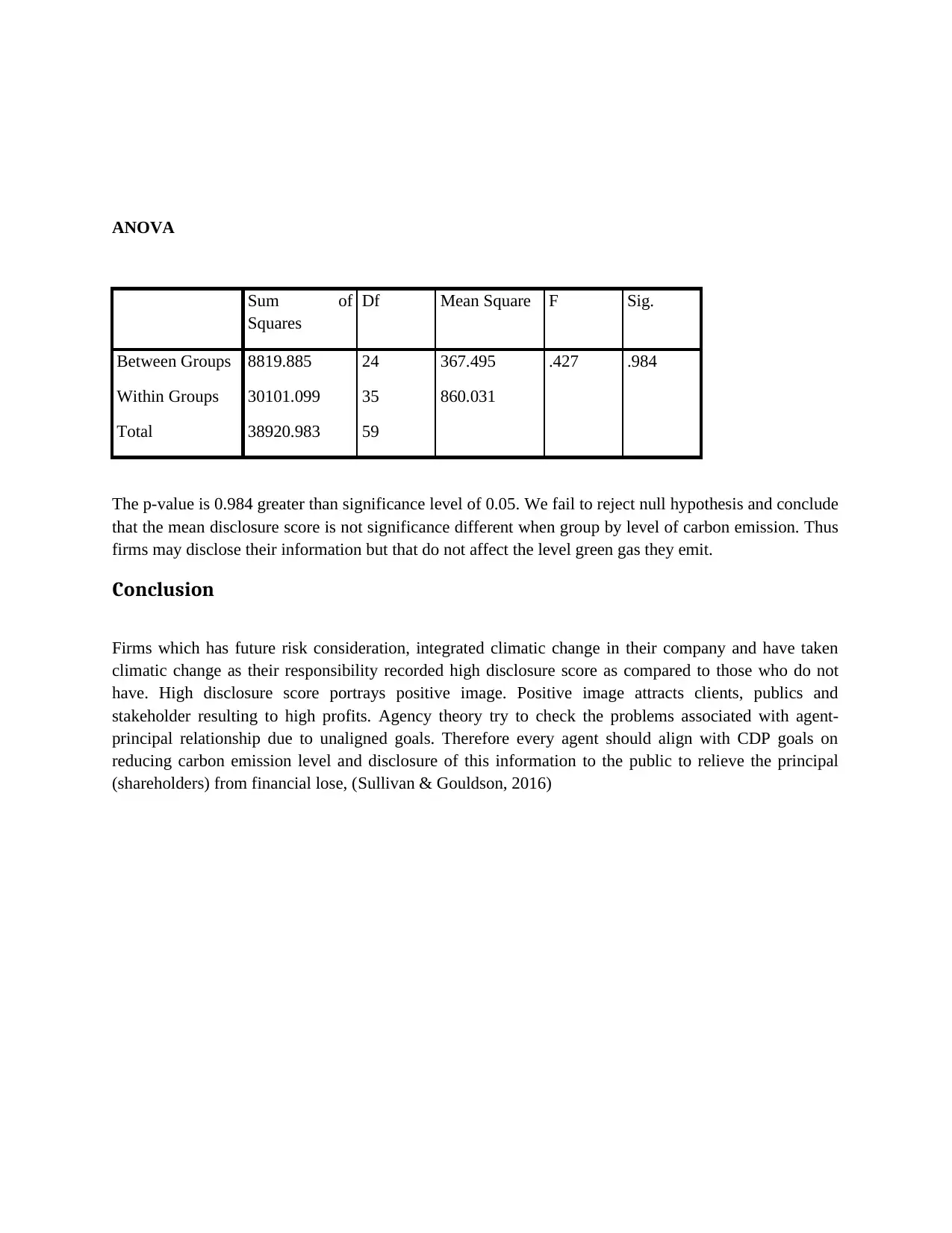

This research project investigates the relationship between green gas emissions and firm disclosure levels, applying agency theory to understand the dynamics between firms and stakeholders. The study examines the influence of carbon risk management, voluntary disclosure, and firm size on carbon emission levels. Data from 60 companies were analyzed using descriptive and inferential statistics. Key findings indicate that firms with future risk considerations and integrated climate change strategies exhibit higher disclosure scores. While disclosure scores do not directly correlate with reduced carbon emissions, they enhance a firm's positive image, attracting clients and stakeholders. The research emphasizes the importance of aligning agent-principal relationships with CDP goals to reduce carbon emissions and promote transparency, mitigating potential financial losses for shareholders. Desklib provides access to similar research projects and solved assignments for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.