Reduced Input Tax Credits for Big Bank Limited

VerifiedAdded on 2019/11/19

|14

|2770

|252

Report

AI Summary

Big Bank Limited has an expense worth $1,650,000, which includes GST as part of advertisement expenses for the previous year. As Big Bank is eligible for input tax credit and has exceeded the financial acquisition threshold, it will be fully entitled to claim input tax credit for the expenditures incurred on the advertisement campaign, which was done for a credible acquisition purpose.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUSTRALIAN TAXATION LAW

Australian Taxation Law

Name of the Student

Name of the University

Author’s Note

Australian Taxation Law

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1AUSTRALIAN TAXATION LAW

Table of Contents

Answer to Question 1......................................................................................................................2

Requirement 1..............................................................................................................................2

Requirement 2..............................................................................................................................3

Requirement 3..............................................................................................................................4

Requirement 4..............................................................................................................................5

Answer to Question 2......................................................................................................................6

Answer to Question 3......................................................................................................................9

Answer to Question 4....................................................................................................................10

References......................................................................................................................................11

Table of Contents

Answer to Question 1......................................................................................................................2

Requirement 1..............................................................................................................................2

Requirement 2..............................................................................................................................3

Requirement 3..............................................................................................................................4

Requirement 4..............................................................................................................................5

Answer to Question 2......................................................................................................................6

Answer to Question 3......................................................................................................................9

Answer to Question 4....................................................................................................................10

References......................................................................................................................................11

2AUSTRALIAN TAXATION LAW

Answer to Question 1

Requirement 1

Issue: The main issue is to determine that whether the cost to move machinery to a new site will

be treated as allowable deduction or not as per Section 8-1 of the IITA 1997.

Legislation: In this issue, the necessary legislations are shown below:

I. Section 8-1 of the Income Tax Assessment Act 1997

II. British Insulated & Helsby Cables

Application: The cost that is related with the moving of the machinery to a new site is capital in

nature and as per the act of 8-1 of the Income Tax Assessment Act 1997; there is not any

allowable deduction on this cost (Taylor and Richardson 2012). In this regard, it needs to be

mentioned that capital expenditure is the kind of expenditure that the business organizations

incur for acquisition and maintenance of fixed assets such as land, building, machinery,

equipment and others. As per the purpose of depreciation, to move the machinery to a new site

has incurred the cost of the particular asset. The cost related with the moving of the machinery to

a new site is taken place from the small changes and under the section of section 8-1 of the

Income Tax Assessment Act 1997; it needs to be allowed as allowable deduction. The main

reason to consider the cost of moving the machinery for allowable deduction is that the cost is a

major part of the operating expenses of the businesses and it has occurred out of the day-to-day

activity of the business (Taylor and Richardson 2013).

According to the given verdict in the case of British Insulated & Helsby Cables, the

transportation cost of the contributed to the increase in benefit of the business by proving a shift

to the depreciable assets. According to the Taxation Ruling of TD 93/126 on machinery

Answer to Question 1

Requirement 1

Issue: The main issue is to determine that whether the cost to move machinery to a new site will

be treated as allowable deduction or not as per Section 8-1 of the IITA 1997.

Legislation: In this issue, the necessary legislations are shown below:

I. Section 8-1 of the Income Tax Assessment Act 1997

II. British Insulated & Helsby Cables

Application: The cost that is related with the moving of the machinery to a new site is capital in

nature and as per the act of 8-1 of the Income Tax Assessment Act 1997; there is not any

allowable deduction on this cost (Taylor and Richardson 2012). In this regard, it needs to be

mentioned that capital expenditure is the kind of expenditure that the business organizations

incur for acquisition and maintenance of fixed assets such as land, building, machinery,

equipment and others. As per the purpose of depreciation, to move the machinery to a new site

has incurred the cost of the particular asset. The cost related with the moving of the machinery to

a new site is taken place from the small changes and under the section of section 8-1 of the

Income Tax Assessment Act 1997; it needs to be allowed as allowable deduction. The main

reason to consider the cost of moving the machinery for allowable deduction is that the cost is a

major part of the operating expenses of the businesses and it has occurred out of the day-to-day

activity of the business (Taylor and Richardson 2013).

According to the given verdict in the case of British Insulated & Helsby Cables, the

transportation cost of the contributed to the increase in benefit of the business by proving a shift

to the depreciable assets. According to the Taxation Ruling of TD 93/126 on machinery

3AUSTRALIAN TAXATION LAW

installation and the commencement of the function of the machinery, the cost related to the

moving of the machinery needs to be treated as revenue. Thus, in the provided situation, the cost

to move the machinbary to a new site is capital expenditure and needs to be treated as non-

permissible deduction (Lignier and Evans 2012).

Conclusion: Thus, based on the above discussion, it can be concluded that the cost to move the

machinery to a new site is capital in nature and the cost will not be considered for allowable

deduction as per section 8-1 of the Income Tax Assessment Act 1997.

Requirement 2

Issue: The major issue in this case is to determine whether the asset revaluation to affect the

insurance cover would be considered as permissible deduction as per section 8-1 of the Income

Tax Assessment Act 1997.

Legislation: The major legislation in this case is section 8-1 of the Income Tax Assessment Act

1997.

Application: According to the provided situation, it can be found that the expenditure is related

with the fixed assets. Thus, in the process to determine the amount of deduction, it is also crucial

to determine that whether the specific expenditure has occurred out of the assets revaluation

(Zakaria et al. 2014). It needs to be acquired for to increase the capacity of revenue production or

to protect the assets. In case the latter results in temporary character and the expenditures are

repetitive, then it needs to be treated as permissible deduction under section 8-1 of the Income

Tax Assessment Act 1997 (Sawyer 2013). As per the observation of the provided situation, the

revaluation cost of the asset to affect cover of insurance needs to be treated as allowable

deduction as per Section 8-1 as they are repetitive in nature.

installation and the commencement of the function of the machinery, the cost related to the

moving of the machinery needs to be treated as revenue. Thus, in the provided situation, the cost

to move the machinbary to a new site is capital expenditure and needs to be treated as non-

permissible deduction (Lignier and Evans 2012).

Conclusion: Thus, based on the above discussion, it can be concluded that the cost to move the

machinery to a new site is capital in nature and the cost will not be considered for allowable

deduction as per section 8-1 of the Income Tax Assessment Act 1997.

Requirement 2

Issue: The major issue in this case is to determine whether the asset revaluation to affect the

insurance cover would be considered as permissible deduction as per section 8-1 of the Income

Tax Assessment Act 1997.

Legislation: The major legislation in this case is section 8-1 of the Income Tax Assessment Act

1997.

Application: According to the provided situation, it can be found that the expenditure is related

with the fixed assets. Thus, in the process to determine the amount of deduction, it is also crucial

to determine that whether the specific expenditure has occurred out of the assets revaluation

(Zakaria et al. 2014). It needs to be acquired for to increase the capacity of revenue production or

to protect the assets. In case the latter results in temporary character and the expenditures are

repetitive, then it needs to be treated as permissible deduction under section 8-1 of the Income

Tax Assessment Act 1997 (Sawyer 2013). As per the observation of the provided situation, the

revaluation cost of the asset to affect cover of insurance needs to be treated as allowable

deduction as per Section 8-1 as they are repetitive in nature.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4AUSTRALIAN TAXATION LAW

Conclusion: As per the above discussion, it can be concluded that the insurance cover cost needs

to be considered as allowable deduction for the repetitive nature of the cost under section 8-1 of

the Income Tax Assessment Act 1997.

Requirement 3

Issue: In the provided situation, the main issue is to determine whether the legal expenses

occurred by a company in order to oppose the petition of winding up would be considered as

deduction under section 8-1 of the Income Tax Assessment Act 1997.

Legislation: The relevant legislation for this case is shown below:

I. Section 8-1 of the Income Tax Assessment Act 1997

II. FC of T v Snowden and Wilson Pty Ltd (1958) 99 CLR 431)

Application: According to section 8-1 of the Income Tax Assessment Act 1997, cost incurred by

the companies at the time of winding up process of business are considered as expenses related

with business operations and they are not allowed for permissible deduction. As per Taxation

ruling of ID 2004/367, legal costs will be allowed for deduction in case the cost is incurred to

carry out the business operations that help the individuals in the production of taxable proceeds

(Lee 2012).

As per the case of FC of T v Snowden and Wilson Pty Ltd (1958), the unusual business

expenses that do not need any earlier action of the taxpayer is not qualified under the deductible

expenditure (Douglas et al. 2014). In this case, the amount of legal expenditure against the

petition for winding up of the business will not be considered for deduction as they nature of

these expenses are capital and all these expenses have occurred out of the business operation

(Cane and Atiyah 2013).

Conclusion: As per the above discussion, it can be concluded that the insurance cover cost needs

to be considered as allowable deduction for the repetitive nature of the cost under section 8-1 of

the Income Tax Assessment Act 1997.

Requirement 3

Issue: In the provided situation, the main issue is to determine whether the legal expenses

occurred by a company in order to oppose the petition of winding up would be considered as

deduction under section 8-1 of the Income Tax Assessment Act 1997.

Legislation: The relevant legislation for this case is shown below:

I. Section 8-1 of the Income Tax Assessment Act 1997

II. FC of T v Snowden and Wilson Pty Ltd (1958) 99 CLR 431)

Application: According to section 8-1 of the Income Tax Assessment Act 1997, cost incurred by

the companies at the time of winding up process of business are considered as expenses related

with business operations and they are not allowed for permissible deduction. As per Taxation

ruling of ID 2004/367, legal costs will be allowed for deduction in case the cost is incurred to

carry out the business operations that help the individuals in the production of taxable proceeds

(Lee 2012).

As per the case of FC of T v Snowden and Wilson Pty Ltd (1958), the unusual business

expenses that do not need any earlier action of the taxpayer is not qualified under the deductible

expenditure (Douglas et al. 2014). In this case, the amount of legal expenditure against the

petition for winding up of the business will not be considered for deduction as they nature of

these expenses are capital and all these expenses have occurred out of the business operation

(Cane and Atiyah 2013).

5AUSTRALIAN TAXATION LAW

Conclusion: As per the above discussion, it can be consumed that the cost occurred in order to

oppose the petition of wwinding up of the business would be considered as non-permissible

deduction according to Section 8-1 of the Income Tax Assessment Act 1997.

Requirement 4

Issue: The main issue in this case is to determine whether the occurred legal expenditures for the

service of the solicitors related to various business operations of the client would be considered

as allowable deduction under Section 8-1 of the Income Tax Assessment Act 1997.

Legislation: The main legislation in this case is Section 8-1 of the Income Tax Assessment Act

1997.

Application: According to the regulation of Section 8-1 of the Income Tax Assessment Act

1997, the business expenses that are occurred related to the business operations in order to

produce revenues need to be considered for allowable deduction (Saad 2014). However, in this

regard, exceptions can be seen related to various legal expenditures and the nature of these

expenses is capital, domestic and private. Thus, it can be said that the legal expenditures incurred

by an individual may not be considered as allowable deduction in case there is not any

association of these expenses with the generation of taxable incomes (Devos 2012). As per the

provided situation, it can be observed that the specific legal expenditure insured by the taxpayer

for number of matters have association for the production of chargeable income; and for this

reason, they need to be treated as allowable deduction as per section 8-1 of the Income Tax

Assessment Act 1997 (Oats 2012).

Conclusion: Thus, based on the above discussion, it can be concluded that all the legal expenses

having relation with the business operations and have been occurred in order to generate taxable

Conclusion: As per the above discussion, it can be consumed that the cost occurred in order to

oppose the petition of wwinding up of the business would be considered as non-permissible

deduction according to Section 8-1 of the Income Tax Assessment Act 1997.

Requirement 4

Issue: The main issue in this case is to determine whether the occurred legal expenditures for the

service of the solicitors related to various business operations of the client would be considered

as allowable deduction under Section 8-1 of the Income Tax Assessment Act 1997.

Legislation: The main legislation in this case is Section 8-1 of the Income Tax Assessment Act

1997.

Application: According to the regulation of Section 8-1 of the Income Tax Assessment Act

1997, the business expenses that are occurred related to the business operations in order to

produce revenues need to be considered for allowable deduction (Saad 2014). However, in this

regard, exceptions can be seen related to various legal expenditures and the nature of these

expenses is capital, domestic and private. Thus, it can be said that the legal expenditures incurred

by an individual may not be considered as allowable deduction in case there is not any

association of these expenses with the generation of taxable incomes (Devos 2012). As per the

provided situation, it can be observed that the specific legal expenditure insured by the taxpayer

for number of matters have association for the production of chargeable income; and for this

reason, they need to be treated as allowable deduction as per section 8-1 of the Income Tax

Assessment Act 1997 (Oats 2012).

Conclusion: Thus, based on the above discussion, it can be concluded that all the legal expenses

having relation with the business operations and have been occurred in order to generate taxable

6AUSTRALIAN TAXATION LAW

income need to be considered as allowable deduction as per section 8-1 of the Income Tax

Assessment Act 1997.

Answer to Question 2

Issue: The main issue in this case regarding Big Bank is to determine the input tax credit related

with the advertisement expenditure that is taken place related to GSTR Act 1999.

Legislation: The major legislations in these case are shown below:

I. GST Act 1999

II. Paragraphs 11-5 and 15-5

III. Subsection 15-25

IV. Goods and Service taxation ruling of GSTR 2006/3

V. Ronpibon Tin NL v. FC of T

Application: The tax regulations of Goods and Service taxation ruling of GSTR 2006/3

provides the specific guidelines related with some specific methods to implement for the

determination of input tax credit along with the administration change for the financial suppliers

under the new system of GST Act 1999. This also includes the regulations related to actual

application under the ruling division of 11, 15 and 129 of the GST Act. All the taxable entities

are eligible for the application of this particular ruling that are registered for under the taxation

laws and are needed to be registered under the taxation law for the acquisition of financial

supplies that crosses the threshold limit for the financial acquisition. These taxable entities are

qualified for the credit of input tax and reduced input tax (Jangra and Narwal 2014).

income need to be considered as allowable deduction as per section 8-1 of the Income Tax

Assessment Act 1997.

Answer to Question 2

Issue: The main issue in this case regarding Big Bank is to determine the input tax credit related

with the advertisement expenditure that is taken place related to GSTR Act 1999.

Legislation: The major legislations in these case are shown below:

I. GST Act 1999

II. Paragraphs 11-5 and 15-5

III. Subsection 15-25

IV. Goods and Service taxation ruling of GSTR 2006/3

V. Ronpibon Tin NL v. FC of T

Application: The tax regulations of Goods and Service taxation ruling of GSTR 2006/3

provides the specific guidelines related with some specific methods to implement for the

determination of input tax credit along with the administration change for the financial suppliers

under the new system of GST Act 1999. This also includes the regulations related to actual

application under the ruling division of 11, 15 and 129 of the GST Act. All the taxable entities

are eligible for the application of this particular ruling that are registered for under the taxation

laws and are needed to be registered under the taxation law for the acquisition of financial

supplies that crosses the threshold limit for the financial acquisition. These taxable entities are

qualified for the credit of input tax and reduced input tax (Jangra and Narwal 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUSTRALIAN TAXATION LAW

As per the provided situation of Big Bank, it can be observed that Big Bank Limited has

an expense worth $ 1,650,000, as GST was the part of advertisement expenses for the previous

year. In accordance with the present situation of Big Bank Limited, it can be observed that the

taxation regulations of Goods and Service taxation ruling of GSTR 2006/3 is applicable for the

business operations of the company as the company is eligible input tax credit and lowered input

tax credit (Evans, Lignier and Tran-Nam 2013). This particular ruling states that GST needs to

be paid in order to make taxable supplies in case a business organization is registered or able for

registration. The GST legislation states that it is necessary for the taxable entities to claim input

tax credit for GST for the acquisition of import for the entity. In this case, it needs to be

mentioned that in case a taxable individual is making financial supplies and crosses the amount

of threshold acquisition, the entity will not be able to recover all the charged GST. However, the

business organization is able to recover the part of such GST.

According to the verdict of the case of Ronpibon Tin NL v. FC of T, in the analysis of

the GST legislation, there is a need for the application of the principles of ‘extent’ and ‘to the

extent’. In this regard, the methods for apportion adoption needs to be appropriate and practical

based on the circumstances of the business organizations. According to the paragraph 11-5 and

15-5, in order to make an acquisition as a credible acquisition, the entity needs to be creditable

either entirely or partly (Harrison and Keating 2014).

As per another requirement of paragraph 11-5 and 15-5 (a), the acquisition needs to be

entirely for credibility purpose for the qualification of an acquisition as credible acquisition. In

case it has been seen that the acquisition is partially credible, it is important to mention the level

of credibility purpose. The ruling of Subsection 15-25 states that in case an import is for the

purpose of partly credible, it will not be considered as fully credible. According to the section of

As per the provided situation of Big Bank, it can be observed that Big Bank Limited has

an expense worth $ 1,650,000, as GST was the part of advertisement expenses for the previous

year. In accordance with the present situation of Big Bank Limited, it can be observed that the

taxation regulations of Goods and Service taxation ruling of GSTR 2006/3 is applicable for the

business operations of the company as the company is eligible input tax credit and lowered input

tax credit (Evans, Lignier and Tran-Nam 2013). This particular ruling states that GST needs to

be paid in order to make taxable supplies in case a business organization is registered or able for

registration. The GST legislation states that it is necessary for the taxable entities to claim input

tax credit for GST for the acquisition of import for the entity. In this case, it needs to be

mentioned that in case a taxable individual is making financial supplies and crosses the amount

of threshold acquisition, the entity will not be able to recover all the charged GST. However, the

business organization is able to recover the part of such GST.

According to the verdict of the case of Ronpibon Tin NL v. FC of T, in the analysis of

the GST legislation, there is a need for the application of the principles of ‘extent’ and ‘to the

extent’. In this regard, the methods for apportion adoption needs to be appropriate and practical

based on the circumstances of the business organizations. According to the paragraph 11-5 and

15-5, in order to make an acquisition as a credible acquisition, the entity needs to be creditable

either entirely or partly (Harrison and Keating 2014).

As per another requirement of paragraph 11-5 and 15-5 (a), the acquisition needs to be

entirely for credibility purpose for the qualification of an acquisition as credible acquisition. In

case it has been seen that the acquisition is partially credible, it is important to mention the level

of credibility purpose. The ruling of Subsection 15-25 states that in case an import is for the

purpose of partly credible, it will not be considered as fully credible. According to the section of

8AUSTRALIAN TAXATION LAW

section 11-15 or 15-10, in case an entity makes the supplies in order to claim input tax credit, the

acquisition will be qualified as fully credible. In case of Big Bank Limited, it is crucial to

mention the fact that the advertisement related expenditures incurred by Big Bank Limited is for

the purpose of credible acquisition. Thus, based on the ruling of GSTR ruling of 2006/3, it can

be observed that Big Bank Limited has already crossed the limit of financial acquisition

threshold. For this reason, the amount of invoice issued to Big Bank Limited will be fully

entitled for input tax credit for the supplied made related to GST (James, Sawyer and

Wallschutzky 2015).

Conclusion: Based on the above discussion, it can be concluded that Big Bank Limited will be

fully eligible for the claiming of input tax credit related to GSTR 2006/13. In this situation, it

needs to be mentioned that Big Bank Limited will be eligible to claim input tax credit for the

specific amount that the company incurred on the expenditures for the advertisement campaign

of the company and it has been done for the purpose of credible acquisition.

section 11-15 or 15-10, in case an entity makes the supplies in order to claim input tax credit, the

acquisition will be qualified as fully credible. In case of Big Bank Limited, it is crucial to

mention the fact that the advertisement related expenditures incurred by Big Bank Limited is for

the purpose of credible acquisition. Thus, based on the ruling of GSTR ruling of 2006/3, it can

be observed that Big Bank Limited has already crossed the limit of financial acquisition

threshold. For this reason, the amount of invoice issued to Big Bank Limited will be fully

entitled for input tax credit for the supplied made related to GST (James, Sawyer and

Wallschutzky 2015).

Conclusion: Based on the above discussion, it can be concluded that Big Bank Limited will be

fully eligible for the claiming of input tax credit related to GSTR 2006/13. In this situation, it

needs to be mentioned that Big Bank Limited will be eligible to claim input tax credit for the

specific amount that the company incurred on the expenditures for the advertisement campaign

of the company and it has been done for the purpose of credible acquisition.

9AUSTRALIAN TAXATION LAW

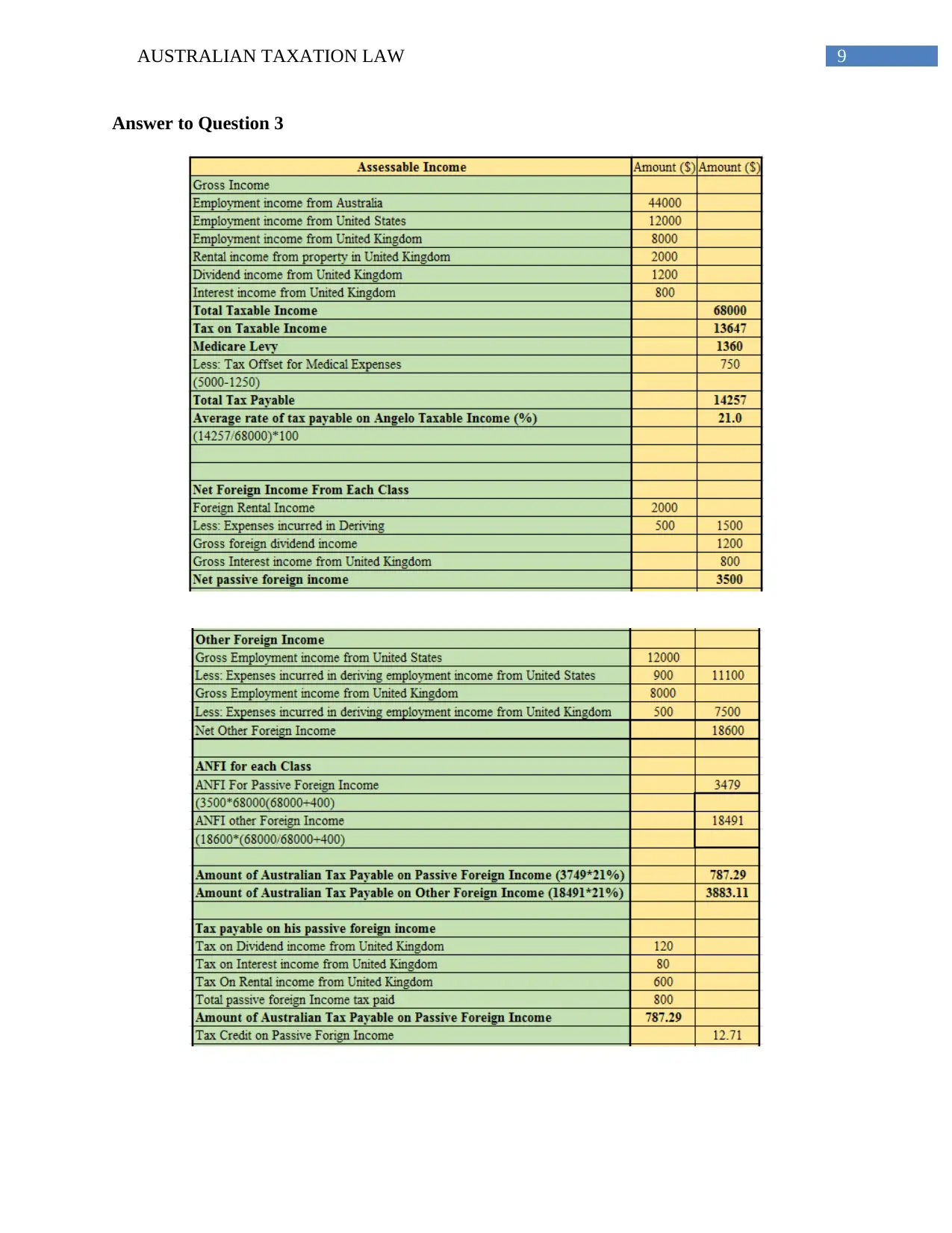

Answer to Question 3

Answer to Question 3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10AUSTRALIAN TAXATION LAW

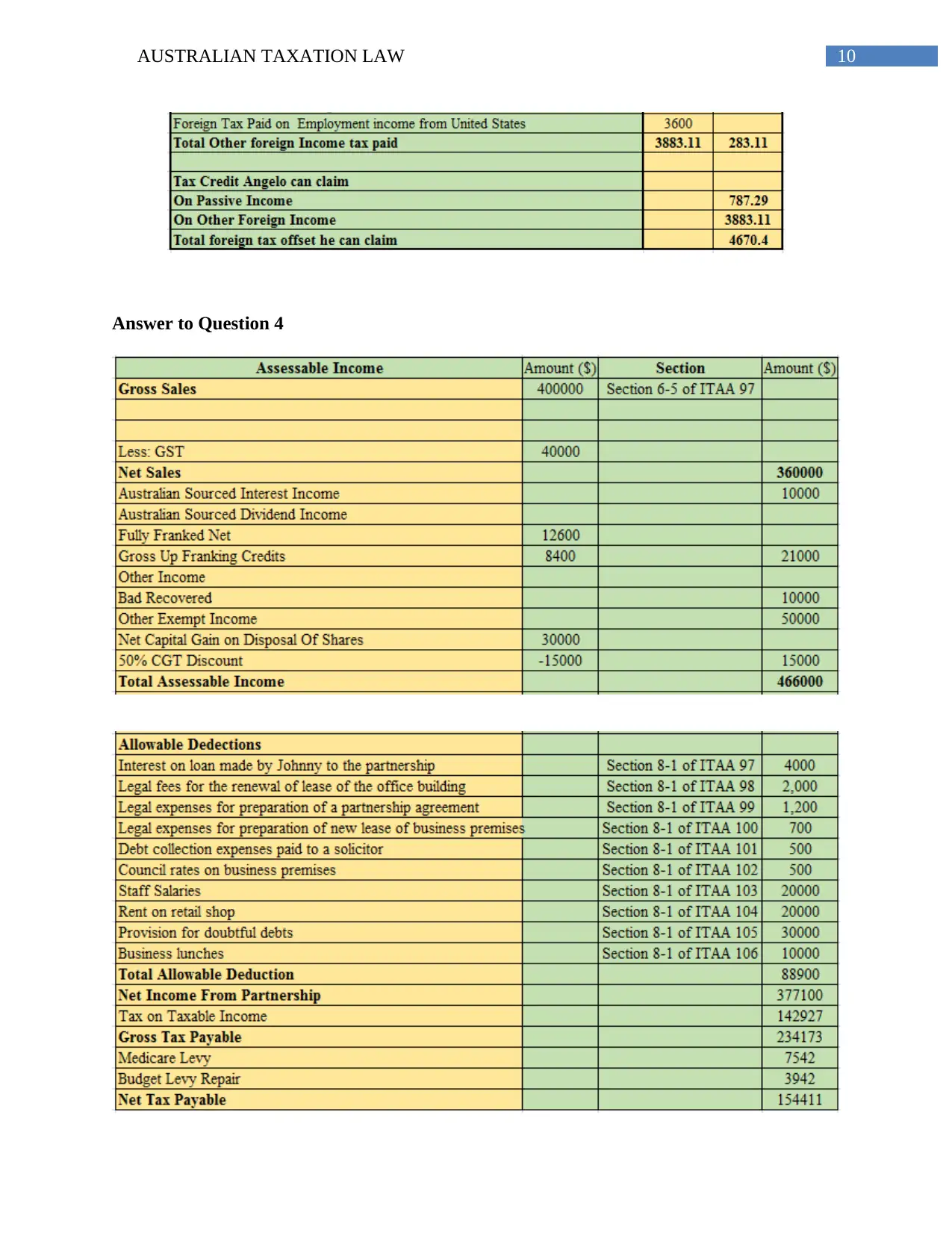

Answer to Question 4

Answer to Question 4

11AUSTRALIAN TAXATION LAW

References

Cane, P. and Atiyah, P.S., 2013. Atiyah's accidents, compensation and the law. Cambridge

University Press.

Devos, K., 2012. The impact of tax professionals upon the compliance behaviour of Australian

individual taxpayers. Revenue Law Journal, 22(1), p.31.

Douglas, H., Bartlett, F., Luker, T. and Hunter, R. eds., 2014. Australian feminist judgments:

Righting and rewriting law. Bloomsbury Publishing.

Evans, C., Lignier, P. and Tran-Nam, B., 2013. Tax compliance costs for the small and medium

enterprise business sector: Recent evidence from Australia. Tax Administration Research Centre

University of EXETER Discussion Paper, pp.003-13.

Harrison, J. and Keating, M., 2014. The deductibility of Sarbanes-Oxley costs incurred by

Australasian companies. Accounting Research Journal, 27(1), pp.52-70.

James, S., Sawyer, A. and Wallschutzky, I., 2015. Tax simplification: A review of initiatives in

Australia, New Zealand and the United Kingdom. eJournal of Tax Research, 13(1), p.280.

James, S., Sawyer, A. and Wallschutzky, I., 2015. Tax simplification: A review of initiatives in

Australia, New Zealand and the United Kingdom. eJournal of Tax Research, 13(1), p.280.

Jangra, A. and Narwal, K.P., 2014. Application of CGE Models in GST: A Literature

Review. International Journal of Economic Practices and Theories, 4(6), pp.970-978.

Lee, N., 2012. What is Financial Literacy, and Does Financial Literacy Education Achieve Its

Objectives? Evidence from Banks, Government Agencies and Financial Literacy Educators in

References

Cane, P. and Atiyah, P.S., 2013. Atiyah's accidents, compensation and the law. Cambridge

University Press.

Devos, K., 2012. The impact of tax professionals upon the compliance behaviour of Australian

individual taxpayers. Revenue Law Journal, 22(1), p.31.

Douglas, H., Bartlett, F., Luker, T. and Hunter, R. eds., 2014. Australian feminist judgments:

Righting and rewriting law. Bloomsbury Publishing.

Evans, C., Lignier, P. and Tran-Nam, B., 2013. Tax compliance costs for the small and medium

enterprise business sector: Recent evidence from Australia. Tax Administration Research Centre

University of EXETER Discussion Paper, pp.003-13.

Harrison, J. and Keating, M., 2014. The deductibility of Sarbanes-Oxley costs incurred by

Australasian companies. Accounting Research Journal, 27(1), pp.52-70.

James, S., Sawyer, A. and Wallschutzky, I., 2015. Tax simplification: A review of initiatives in

Australia, New Zealand and the United Kingdom. eJournal of Tax Research, 13(1), p.280.

James, S., Sawyer, A. and Wallschutzky, I., 2015. Tax simplification: A review of initiatives in

Australia, New Zealand and the United Kingdom. eJournal of Tax Research, 13(1), p.280.

Jangra, A. and Narwal, K.P., 2014. Application of CGE Models in GST: A Literature

Review. International Journal of Economic Practices and Theories, 4(6), pp.970-978.

Lee, N., 2012. What is Financial Literacy, and Does Financial Literacy Education Achieve Its

Objectives? Evidence from Banks, Government Agencies and Financial Literacy Educators in

12AUSTRALIAN TAXATION LAW

England. In the Proceedings of 2012 Academy of Financial Services Annual Conference at San

Antonio, USA E (Vol. 4).

Lignier, P. and Evans, C., 2012. The rise and rise of tax compliance costs for the small business

sector in Australia.

Oats, L. ed., 2012. Taxation: A fieldwork research handbook. Routledge.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Sawyer, A., 2013. Rewriting Tax Legislation-Can Polishing Silver Really Turn It into Gold. J.

Austl. Tax'n, 15, p.1.

Taylor, G. and Richardson, G., 2012. International corporate tax avoidance practices: evidence

from Australian firms. The International Journal of Accounting, 47(4), pp.469-496.

Taylor, G. and Richardson, G., 2013. The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting, Auditing and

Taxation, 22(1), pp.12-25.

Zakaria, A., Edwards, D.J., Holt, G.D. and Ramachandran, V., 2014. A Review of Property,

Plant and Equipment Asset Revaluation Decision Making in Indonesia: Development of a

Conceptual Model. Mindanao Journal of Science and Technology, 12(1), pp.1-1.

England. In the Proceedings of 2012 Academy of Financial Services Annual Conference at San

Antonio, USA E (Vol. 4).

Lignier, P. and Evans, C., 2012. The rise and rise of tax compliance costs for the small business

sector in Australia.

Oats, L. ed., 2012. Taxation: A fieldwork research handbook. Routledge.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Sawyer, A., 2013. Rewriting Tax Legislation-Can Polishing Silver Really Turn It into Gold. J.

Austl. Tax'n, 15, p.1.

Taylor, G. and Richardson, G., 2012. International corporate tax avoidance practices: evidence

from Australian firms. The International Journal of Accounting, 47(4), pp.469-496.

Taylor, G. and Richardson, G., 2013. The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting, Auditing and

Taxation, 22(1), pp.12-25.

Zakaria, A., Edwards, D.J., Holt, G.D. and Ramachandran, V., 2014. A Review of Property,

Plant and Equipment Asset Revaluation Decision Making in Indonesia: Development of a

Conceptual Model. Mindanao Journal of Science and Technology, 12(1), pp.1-1.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13AUSTRALIAN TAXATION LAW

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.