HI5020 Corporate Accounting: Detailed Cash Flow & Tax Analysis-Adairs

VerifiedAdded on 2024/05/29

|15

|2922

|103

Report

AI Summary

This report provides a detailed analysis of Adairs Limited's cash flow statements for the years 2015, 2016, and 2017, focusing on operating, investing, and financing activities. It examines key items such as payments to suppliers and employees, income tax paid, and acquisitions of property, plant, and equipment. The report includes comparative analyses of cash flow generated from operating, investing, and financing activities, highlighting trends and significant changes. Furthermore, it discusses items reported in the other comprehensive income statement, reasons for their exclusion from the income statement, and an analysis of tax expenses, deferred tax assets/liabilities, and income tax payable. The report also addresses the differences between income tax expense and income tax paid, offering insights into the treatment of tax in Adairs' financial statements. This student contributed assignment is available on Desklib, a platform offering a wide range of study tools and resources.

HI5020 Corporate Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction.................................................................................................................................................3

1 Various items of cash flow statement.......................................................................................................4

2 comparative analyses of cash flow statements..........................................................................................5

3 What items have been reported in the other comprehensive income statement?.......................................6

4 Understanding of identified items.............................................................................................................6

5 Reasons for not including them in income statements..............................................................................6

6 Tax expense in latest financial statements................................................................................................7

7 Is this figure the same as the company tax rate times your firm’s accounting income? Explain why this

is, or is not, the case for your firm...............................................................................................................7

8 Comment on deferred tax assets/liabilities that are reported on the balance sheet articulating the possible

reasons why they have been recorded..........................................................................................................7

9 Is there any current tax assets or income tax payable recorded by your company? Why is the income tax

payable not the same as income tax expense?.............................................................................................8

10 Is the income tax expense shown in the income statement same as the income tax paid shown in the

cash flow statement? If not why is the difference?......................................................................................8

11 What do you find interesting, confusing, surprising or difficult to understand about the treatment of tax

in your firm’s financial statements? What new insights, if any, have you gained about how companies

account for income tax as a result of examining your firm’s tax expense in its accounts?..........................8

Conclusion.................................................................................................................................................10

Reference...................................................................................................................................................11

2

Introduction.................................................................................................................................................3

1 Various items of cash flow statement.......................................................................................................4

2 comparative analyses of cash flow statements..........................................................................................5

3 What items have been reported in the other comprehensive income statement?.......................................6

4 Understanding of identified items.............................................................................................................6

5 Reasons for not including them in income statements..............................................................................6

6 Tax expense in latest financial statements................................................................................................7

7 Is this figure the same as the company tax rate times your firm’s accounting income? Explain why this

is, or is not, the case for your firm...............................................................................................................7

8 Comment on deferred tax assets/liabilities that are reported on the balance sheet articulating the possible

reasons why they have been recorded..........................................................................................................7

9 Is there any current tax assets or income tax payable recorded by your company? Why is the income tax

payable not the same as income tax expense?.............................................................................................8

10 Is the income tax expense shown in the income statement same as the income tax paid shown in the

cash flow statement? If not why is the difference?......................................................................................8

11 What do you find interesting, confusing, surprising or difficult to understand about the treatment of tax

in your firm’s financial statements? What new insights, if any, have you gained about how companies

account for income tax as a result of examining your firm’s tax expense in its accounts?..........................8

Conclusion.................................................................................................................................................10

Reference...................................................................................................................................................11

2

Introduction

Adairs limited is a leading company and specialty retailer that produces home furnishings and it

operates in Australia. It consists of a national footprint of stores with a number of store formats.

This company aims to present consumers with providing trending fashion products, quality,

strong value and a well-managed customer service. Adairs' has a wide range of products such as

bedding, bed linen, towels, and other home furnishing. Adairs provides vertically integrated

product design and do retail operations. Almost all the products of this company is sold under its

own private brands. Some of the products of this company are sold under some third-party

brands. Currently, Adairs has established 160 stores in Australia and some of them are named

Adairs, Adairs Kids, Adairs Homemaker and Adairs Outlets. This company is also growing its

reach with the online stores. The profit margin of this company has shown exponential growth in

last few years.

3

Adairs limited is a leading company and specialty retailer that produces home furnishings and it

operates in Australia. It consists of a national footprint of stores with a number of store formats.

This company aims to present consumers with providing trending fashion products, quality,

strong value and a well-managed customer service. Adairs' has a wide range of products such as

bedding, bed linen, towels, and other home furnishing. Adairs provides vertically integrated

product design and do retail operations. Almost all the products of this company is sold under its

own private brands. Some of the products of this company are sold under some third-party

brands. Currently, Adairs has established 160 stores in Australia and some of them are named

Adairs, Adairs Kids, Adairs Homemaker and Adairs Outlets. This company is also growing its

reach with the online stores. The profit margin of this company has shown exponential growth in

last few years.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

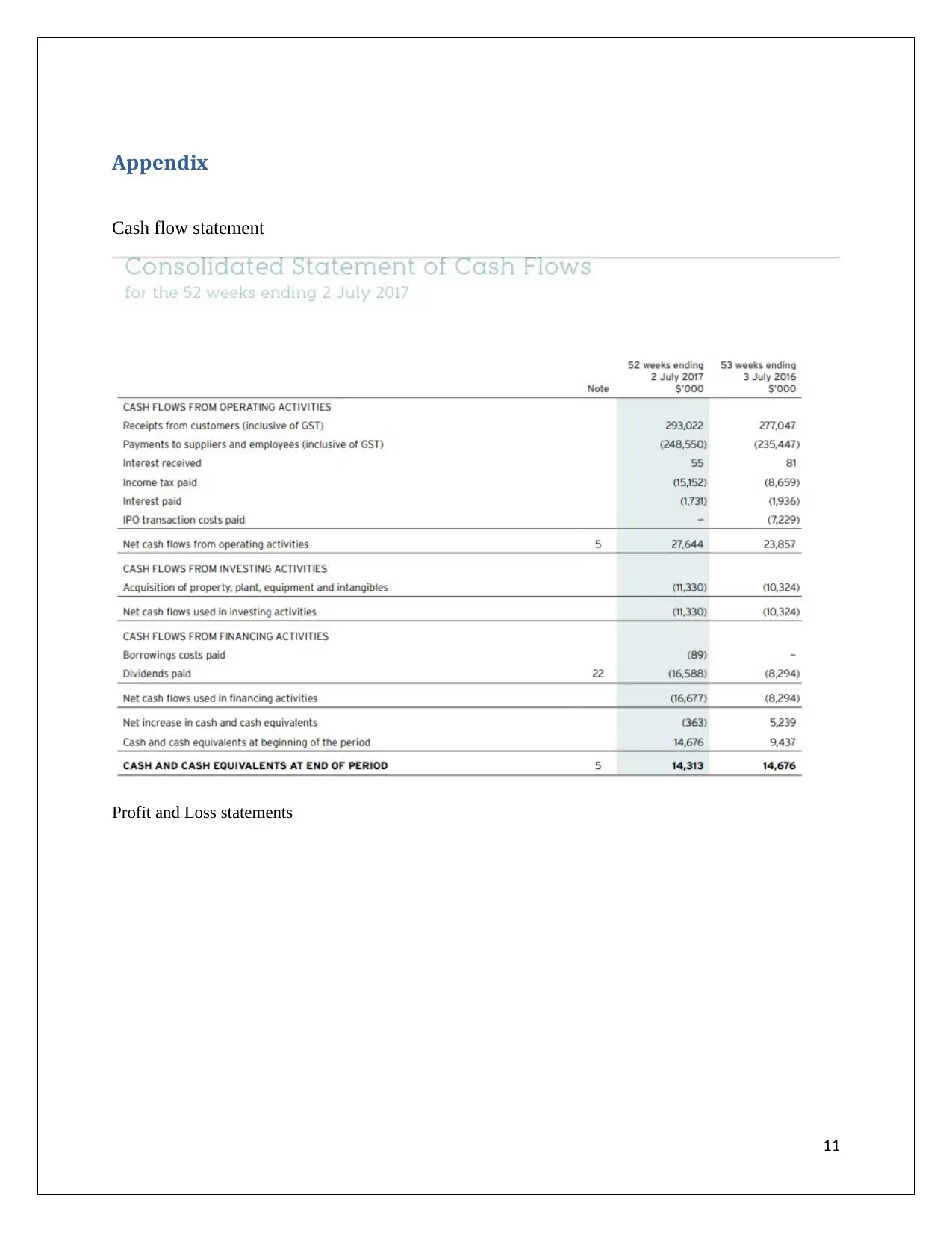

1 Various items of cash flow statement

The cash flow statement of Adairs is determined in this report regarding the assessment of the

finance and overall cash flow of the company in the year 2015, 2016 and 2017. This cash flow

statement has multiple cash flow statements such as the cash flow from operating activities, cash

flow statement from investing activities and from financing activities. The cash flow statement of

Adairs is given below:

Cash flow statement from operating activities:

According to the cash flow statement of Adairs from operating activities, the Payments to

suppliers and employees (inclusive of GST) has shown extensive growth in 2017 which is

248,550$ which is very high in comparison to 2016 and 2015. Income tax paid by this company

is also increased in 2017 which is 15,152$ that was only 8,659 $ in 2016. On the other hand, the

interest paid by Adairs is getting low in 2017 which is 1,731 and in 2016 it was 1,936 $. So the

new cash flow from operating activities is 27,644 $ in 2017 which is maximum in comparison to

2015 and 2016.

Cash flow statement from investing activities:

According to the cash flow statement from investing activities, the Acquisition of property, plant

and equipment is 11330 $ in 2017 which was 10324 $ in 2016 and 6878 $ in 2015 so it can be

said that the property acquisition has increased exponentially in 2017. Investing cash flows from

discontinued operations is not present in 2016 and 2017 but in 2016 it was 1,374 $. Along with

that, Cash loss attributable to a discontinued operation is also not present in the cash flow

statement of 2016 and 2017 but it was 7,044 $ in 2015.

Cash flow statement from financing activities

In accordance to the cash flow statement from financing activities, Net increase in cash and cash

equivalents is decreased in 2017 on a higher scale which is 363$ which was 5,239 $ in 2016 and

14,940$ in 2015. The Cash and cash equivalents at beginning of the period are also increased in

2017 which is 14,676 and in 2016 it was 9,437$.

4

The cash flow statement of Adairs is determined in this report regarding the assessment of the

finance and overall cash flow of the company in the year 2015, 2016 and 2017. This cash flow

statement has multiple cash flow statements such as the cash flow from operating activities, cash

flow statement from investing activities and from financing activities. The cash flow statement of

Adairs is given below:

Cash flow statement from operating activities:

According to the cash flow statement of Adairs from operating activities, the Payments to

suppliers and employees (inclusive of GST) has shown extensive growth in 2017 which is

248,550$ which is very high in comparison to 2016 and 2015. Income tax paid by this company

is also increased in 2017 which is 15,152$ that was only 8,659 $ in 2016. On the other hand, the

interest paid by Adairs is getting low in 2017 which is 1,731 and in 2016 it was 1,936 $. So the

new cash flow from operating activities is 27,644 $ in 2017 which is maximum in comparison to

2015 and 2016.

Cash flow statement from investing activities:

According to the cash flow statement from investing activities, the Acquisition of property, plant

and equipment is 11330 $ in 2017 which was 10324 $ in 2016 and 6878 $ in 2015 so it can be

said that the property acquisition has increased exponentially in 2017. Investing cash flows from

discontinued operations is not present in 2016 and 2017 but in 2016 it was 1,374 $. Along with

that, Cash loss attributable to a discontinued operation is also not present in the cash flow

statement of 2016 and 2017 but it was 7,044 $ in 2015.

Cash flow statement from financing activities

In accordance to the cash flow statement from financing activities, Net increase in cash and cash

equivalents is decreased in 2017 on a higher scale which is 363$ which was 5,239 $ in 2016 and

14,940$ in 2015. The Cash and cash equivalents at beginning of the period are also increased in

2017 which is 14,676 and in 2016 it was 9,437$.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

So the net cash flow of Adairs at the end of the period in 2017 is 14,313$ which a little bit less in

comparison to 2016 which was 14,676.

2 comparative analyses of cash flow statements

Analysis of cash flow generated from operating activities

The net margin of Adairs is getting increased after the adjustment of multiple expenses that are

paid by cash or by banking that are based on accounting. The net profit is analysed by using the

information in the net cash flow of Adairs that is interpreted from using the operating activities.

All these expenses are considered under noncash items where cash inflow and outflow does not

included. When a calculation is done regarding the cash flow by operating activities, some of the

items are added back to the net profit to get the net profit increased by an organization in cash.

Net cash flow of Adairs from operating activities is maximum in 2017 in comparison to 2015

and 2016.

The main objective of this analysis is to create the cash inflow and outflow of Adairs as the full

business operations of this company are conducted at the time of financial year. Some of the

details regarding noncash items are deducted from the statement of net profit in the income

statement, only preliminary depreciation and expenses are considered in this.

Analysis of cash flow generated from investing activities

Many companies analyse the available balance and after this, they make a decision in a manner

to use this balance effectively. There are many purchases which are made using fixed assets that

will give some additional returns to the organization. Adairs also makes purchases and after that

they sell these assets in which investments are incorporated in the net cash flow by investing

activities.

Analysis of cash flow from financing activities

Sometimes companies make cash payments to its various stakeholders who are associated with

the organization and this inflow and outflow of the cash come under cash flow of the financing

activities. Adairs Limited has generated cash dividend for the shareholders at the end of year

2015, 2016 and 2017. While generating the cash flow of financing activities of Adairs it was

5

comparison to 2016 which was 14,676.

2 comparative analyses of cash flow statements

Analysis of cash flow generated from operating activities

The net margin of Adairs is getting increased after the adjustment of multiple expenses that are

paid by cash or by banking that are based on accounting. The net profit is analysed by using the

information in the net cash flow of Adairs that is interpreted from using the operating activities.

All these expenses are considered under noncash items where cash inflow and outflow does not

included. When a calculation is done regarding the cash flow by operating activities, some of the

items are added back to the net profit to get the net profit increased by an organization in cash.

Net cash flow of Adairs from operating activities is maximum in 2017 in comparison to 2015

and 2016.

The main objective of this analysis is to create the cash inflow and outflow of Adairs as the full

business operations of this company are conducted at the time of financial year. Some of the

details regarding noncash items are deducted from the statement of net profit in the income

statement, only preliminary depreciation and expenses are considered in this.

Analysis of cash flow generated from investing activities

Many companies analyse the available balance and after this, they make a decision in a manner

to use this balance effectively. There are many purchases which are made using fixed assets that

will give some additional returns to the organization. Adairs also makes purchases and after that

they sell these assets in which investments are incorporated in the net cash flow by investing

activities.

Analysis of cash flow from financing activities

Sometimes companies make cash payments to its various stakeholders who are associated with

the organization and this inflow and outflow of the cash come under cash flow of the financing

activities. Adairs Limited has generated cash dividend for the shareholders at the end of year

2015, 2016 and 2017. While generating the cash flow of financing activities of Adairs it was

5

identified that this company has issued some debt as it has a positive cash flow which is initiated

for development of the company.

The entire cash flow statement of Adairs in year 2015, 2016 and 2017 is analysed according to

which the cash flow at the end of year is positive in 2017 which was lower in 2016 and 2015.

3 What items have been reported in the other comprehensive income statement?

In running state of a business or company there is a complete income statement created in order

keep record of the income and outcomes of the organization. The essential items that are

involved in the income statement have foreign currency translations along with the increment

which is unrealized in the investments of funds. Additionally, the reserves made to provide

advantages to the employees are also considered under the income statement. The final total of

the income statement will be divided with the equity holders and non-controlling interest to

equally distribute of the profit in relation to their investments and funding provided to Adairs.

4 Understanding of identified items

An appropriate understanding of the transactions is required which are incorporated in the

comprehensive income statements. After this, it can be evaluated that whether this value should

be added in the income statement or not. All these elements get changed along with a broad

category that is analyzed initially. An overall amount in the foreign currency translation also

included and divided into two different sections that can be reclassified along with the loss and

profit regarding Adairs limited. Whenever an organization gets involved with foreign

transactions of the prevarication of investment with the raw material purchase then the company

must take care of foreign exchange as there might be some future requirements of foreign

exchanges (Joyner, et. al., 2014).

5 Reasons for not including them in income statements

Differences of the foreign exchange translation regarding Adairs limited in the financial year

2017 has high exchange currency differences within the market. These differences are not

usually as the items that must be represented autonomously are not even in the income statement

6

for development of the company.

The entire cash flow statement of Adairs in year 2015, 2016 and 2017 is analysed according to

which the cash flow at the end of year is positive in 2017 which was lower in 2016 and 2015.

3 What items have been reported in the other comprehensive income statement?

In running state of a business or company there is a complete income statement created in order

keep record of the income and outcomes of the organization. The essential items that are

involved in the income statement have foreign currency translations along with the increment

which is unrealized in the investments of funds. Additionally, the reserves made to provide

advantages to the employees are also considered under the income statement. The final total of

the income statement will be divided with the equity holders and non-controlling interest to

equally distribute of the profit in relation to their investments and funding provided to Adairs.

4 Understanding of identified items

An appropriate understanding of the transactions is required which are incorporated in the

comprehensive income statements. After this, it can be evaluated that whether this value should

be added in the income statement or not. All these elements get changed along with a broad

category that is analyzed initially. An overall amount in the foreign currency translation also

included and divided into two different sections that can be reclassified along with the loss and

profit regarding Adairs limited. Whenever an organization gets involved with foreign

transactions of the prevarication of investment with the raw material purchase then the company

must take care of foreign exchange as there might be some future requirements of foreign

exchanges (Joyner, et. al., 2014).

5 Reasons for not including them in income statements

Differences of the foreign exchange translation regarding Adairs limited in the financial year

2017 has high exchange currency differences within the market. These differences are not

usually as the items that must be represented autonomously are not even in the income statement

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of this company. Also, Reserve movement shares also must not be added to the income statement

because these elements are not related to the income statement. This is one of the extraordinary

items that should be represented and reported separately (Omag, 2016).

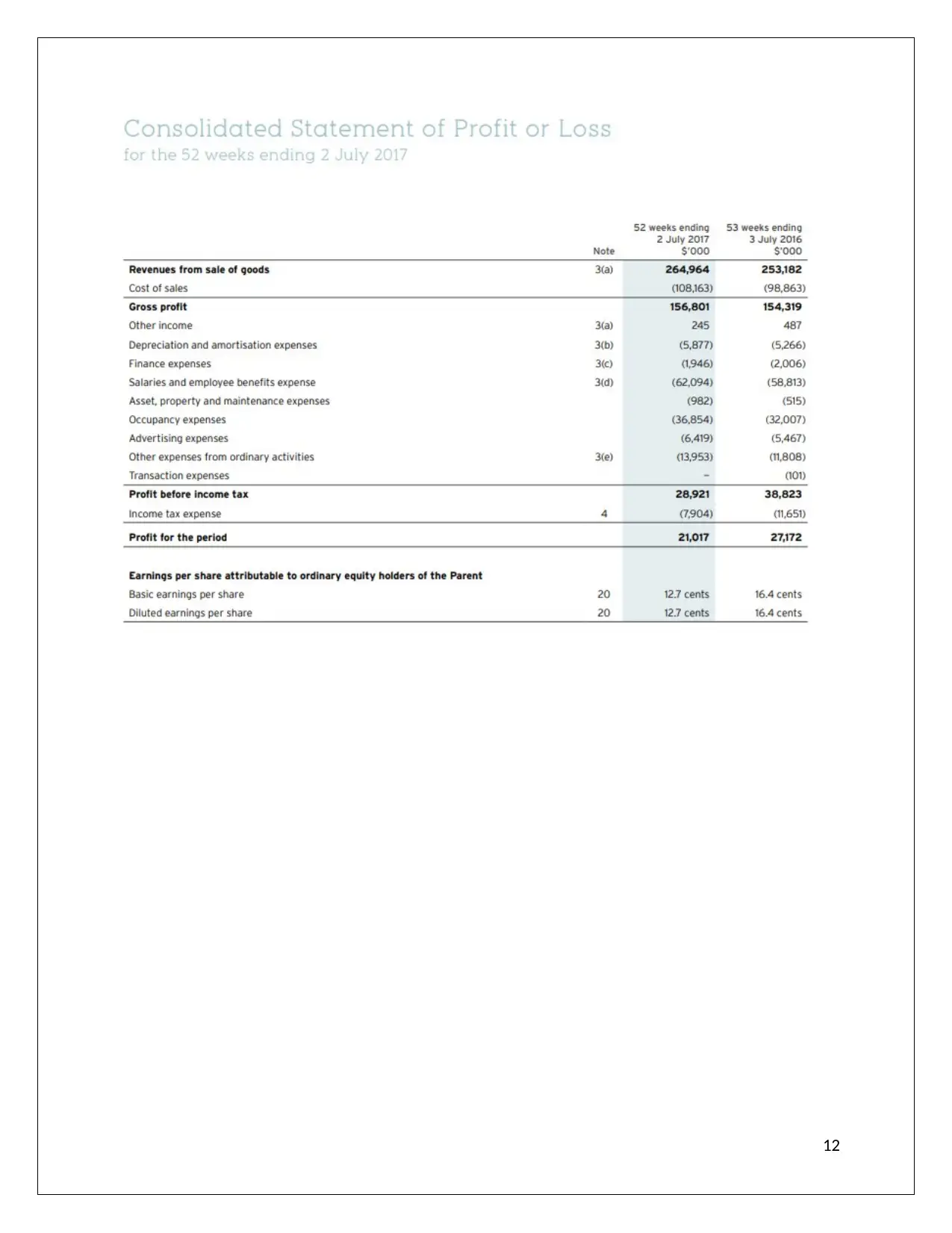

6 Tax expense in latest financial statements.

Adairs carry out the operations and tasks with aim of increasing the profits and it is required as

per the regulations that on the quantity that is earned. A business must be acknowledged with the

tax expense according to the tax rule of the company location. If the organization is in loss then a

determination of the profit is done according to the tax expenses. These essentials need to be

calculated according to the policies and rules which are predefined for the evaluation of accurate

amount and after this, this amount will be paid to the right authority. In previous years, this is

complete changes as it totally relies on the profit margin amount or loss made by Adairs limited.

In the current financial statements, all the company expenses are increased in accordance to the

profit margin (Miletić, 2014).

7 Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.

No, the evaluation of the amount is done as expense of the company which is not similar in

accordance to the accounting tax. Main reason behind this is the difference in the manner where

some of the elements are considered in accordance to the policies and laws. The taxes that will

be paid are considered in accordance to the Australian tax rate and after that some adjustments

will be made regarding the tax assessment. This is done due to some of the amounts that are

acceptable in accounts will be deducted in tax policies and laws and that could not be excluded.

In Adairs, deferred tax balances foreign exchange difference; non-deductible depreciations etc.

are determined as final tax expenses (Gobetti & Orair, 2017).

8 Comment on deferred tax assets/liabilities that are reported on the balance sheet

articulating the possible reasons why they have been recorded.

In Adairs, present and late taxes are acknowledged in the balance sheet. Deferred tax is the tax

which is calculated in order to the temporary timing difference which exists in the company. It

happens due to one of these items in law that is not allowed in a different time period. Deferred

7

because these elements are not related to the income statement. This is one of the extraordinary

items that should be represented and reported separately (Omag, 2016).

6 Tax expense in latest financial statements.

Adairs carry out the operations and tasks with aim of increasing the profits and it is required as

per the regulations that on the quantity that is earned. A business must be acknowledged with the

tax expense according to the tax rule of the company location. If the organization is in loss then a

determination of the profit is done according to the tax expenses. These essentials need to be

calculated according to the policies and rules which are predefined for the evaluation of accurate

amount and after this, this amount will be paid to the right authority. In previous years, this is

complete changes as it totally relies on the profit margin amount or loss made by Adairs limited.

In the current financial statements, all the company expenses are increased in accordance to the

profit margin (Miletić, 2014).

7 Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.

No, the evaluation of the amount is done as expense of the company which is not similar in

accordance to the accounting tax. Main reason behind this is the difference in the manner where

some of the elements are considered in accordance to the policies and laws. The taxes that will

be paid are considered in accordance to the Australian tax rate and after that some adjustments

will be made regarding the tax assessment. This is done due to some of the amounts that are

acceptable in accounts will be deducted in tax policies and laws and that could not be excluded.

In Adairs, deferred tax balances foreign exchange difference; non-deductible depreciations etc.

are determined as final tax expenses (Gobetti & Orair, 2017).

8 Comment on deferred tax assets/liabilities that are reported on the balance sheet

articulating the possible reasons why they have been recorded.

In Adairs, present and late taxes are acknowledged in the balance sheet. Deferred tax is the tax

which is calculated in order to the temporary timing difference which exists in the company. It

happens due to one of these items in law that is not allowed in a different time period. Deferred

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

tax asset is used for this amount and these amounts are considered according to the timing

differences that exist (Bhandari & Adams, 2017).

9 Is there any current tax assets or income tax payable recorded by your company? Why is

the income tax payable not the same as income tax expense?

Adairs limited keeps the full record of the entire income tax payable amount while making the

income statements. This amount has been included in the balance sheet of this company for the

assessment of tax. This is evaluated as it is the total tax amount that will be paid by Adairs in the

next year and due to this it involves current liability. The payable tax amount is not same to the

expense as in the expenses, only income of current year is included but still the current tax will

be consisted in the payable amount (Nejad, et. al., 2018).

10 Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?

The amount which is evaluated by Adairs limited in the income statement is not similar as the

amount which will be pad and included in the cash flow statements. The main cause is that these

expenses are regarding current period with considering the payments so it is not urgent to pay the

same amount while making tax payments. In the case of Adairs the current tax expenses are

higher compared to the previous year which shows that the profit is also getting increased

(Graham, et. al., 2012).

11 What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you

gained about how companies account for income tax as a result of examining your firm’s

tax expense in its accounts?

In each and every company, there are some specific rules and policies which are followed by the

shareholders and the working employees in context to the company. An arrangement of the tax-

sharing is done by members of the company for proper tax allocation with all the companies and

their subsidiaries. One other agreement is tax funding that is managed by the members of the

company. These are the interesting facts about Adairs limited regarding its financial statement

(Yap, 2012).

8

differences that exist (Bhandari & Adams, 2017).

9 Is there any current tax assets or income tax payable recorded by your company? Why is

the income tax payable not the same as income tax expense?

Adairs limited keeps the full record of the entire income tax payable amount while making the

income statements. This amount has been included in the balance sheet of this company for the

assessment of tax. This is evaluated as it is the total tax amount that will be paid by Adairs in the

next year and due to this it involves current liability. The payable tax amount is not same to the

expense as in the expenses, only income of current year is included but still the current tax will

be consisted in the payable amount (Nejad, et. al., 2018).

10 Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?

The amount which is evaluated by Adairs limited in the income statement is not similar as the

amount which will be pad and included in the cash flow statements. The main cause is that these

expenses are regarding current period with considering the payments so it is not urgent to pay the

same amount while making tax payments. In the case of Adairs the current tax expenses are

higher compared to the previous year which shows that the profit is also getting increased

(Graham, et. al., 2012).

11 What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you

gained about how companies account for income tax as a result of examining your firm’s

tax expense in its accounts?

In each and every company, there are some specific rules and policies which are followed by the

shareholders and the working employees in context to the company. An arrangement of the tax-

sharing is done by members of the company for proper tax allocation with all the companies and

their subsidiaries. One other agreement is tax funding that is managed by the members of the

company. These are the interesting facts about Adairs limited regarding its financial statement

(Yap, 2012).

8

Conclusion

Financial statement of Adairs limited is analyzed along with profit and loss assessment in this

report. Multiple items are involved in this report which can be regenerated for the profit and loss

in future. In Adairs limited, a tax consolidation assembly is created which have many Australian

subsidiaries. This work represents that Adairs has made a higher growth as profit in last few

years. .

9

Financial statement of Adairs limited is analyzed along with profit and loss assessment in this

report. Multiple items are involved in this report which can be regenerated for the profit and loss

in future. In Adairs limited, a tax consolidation assembly is created which have many Australian

subsidiaries. This work represents that Adairs has made a higher growth as profit in last few

years. .

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reference

Annual report. (2017). Adairs Limited. [Online]. Annual report. Available at:

http://investors.adairs.com.au/FormBuilder/_Resource/_module/51fbMLwe2UG-

5KJ3qHCF4w/file/Adairs-2017-Annual-Report.pdf. A[accessed on: 25th may 2018].

Bhandari, S. B., & Adams, M. T. (2017). On the Definition, Measurement, and Use of the

Free Cash Flow Concept in Financial Reporting and Analysis: A Review and

Recommendations. Journal of Accounting and Finance, 17(1), 11-19.

Gobetti, S. W., & Orair, R. O. (2017). Taxation and distribution of income in Brazil: new

evidence from personal income tax data. Revista de Economia Política, 37(2), 267-286.

Graham, J. R., Raedy, J. S., & Shackelford, D. A. (2012). Research in accounting for

income taxes. Journal of Accounting and Economics, 53(1), 412-434.

Joyner, D. T., Banatte, J. M., & Dondeti, V. R. (2014). Back to basics: Algebraic

foundations of the statement of cash flows. American Journal of Business Education

(Online), 7(1), 93.

Miletić, D. (2014). Cash flow statement: Assessment of situation and application

problems in Serbia. Industrija, 42(4), 99-114.

Nejad, M. Y., Ahmad, A., & Embong, Z. (2018). Value Relevance Of Other

Comprehensive Income. Asian Journal of Accounting and Governance, 8, 133-144.

Omag, A. (2016). Cash Flows from Financing Activities. Evidence from the Automotive

Industry. International Journal of Academic Research in Accounting, Finance and

Management Sciences, 6(1), 115-122.

Yap, C. (2012). Users' perceptions of the need for cash flow statements—Australian

evidence. European Accounting Review, 6(4), 653-672.

10

Annual report. (2017). Adairs Limited. [Online]. Annual report. Available at:

http://investors.adairs.com.au/FormBuilder/_Resource/_module/51fbMLwe2UG-

5KJ3qHCF4w/file/Adairs-2017-Annual-Report.pdf. A[accessed on: 25th may 2018].

Bhandari, S. B., & Adams, M. T. (2017). On the Definition, Measurement, and Use of the

Free Cash Flow Concept in Financial Reporting and Analysis: A Review and

Recommendations. Journal of Accounting and Finance, 17(1), 11-19.

Gobetti, S. W., & Orair, R. O. (2017). Taxation and distribution of income in Brazil: new

evidence from personal income tax data. Revista de Economia Política, 37(2), 267-286.

Graham, J. R., Raedy, J. S., & Shackelford, D. A. (2012). Research in accounting for

income taxes. Journal of Accounting and Economics, 53(1), 412-434.

Joyner, D. T., Banatte, J. M., & Dondeti, V. R. (2014). Back to basics: Algebraic

foundations of the statement of cash flows. American Journal of Business Education

(Online), 7(1), 93.

Miletić, D. (2014). Cash flow statement: Assessment of situation and application

problems in Serbia. Industrija, 42(4), 99-114.

Nejad, M. Y., Ahmad, A., & Embong, Z. (2018). Value Relevance Of Other

Comprehensive Income. Asian Journal of Accounting and Governance, 8, 133-144.

Omag, A. (2016). Cash Flows from Financing Activities. Evidence from the Automotive

Industry. International Journal of Academic Research in Accounting, Finance and

Management Sciences, 6(1), 115-122.

Yap, C. (2012). Users' perceptions of the need for cash flow statements—Australian

evidence. European Accounting Review, 6(4), 653-672.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appendix

Cash flow statement

Profit and Loss statements

11

Cash flow statement

Profit and Loss statements

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.