Auditing Inventory Transactions and Risk

VerifiedAdded on 2020/02/24

|9

|1974

|201

AI Summary

This assignment delves into the crucial aspect of auditing inventory transactions within organizations. It emphasizes the auditor's responsibility to investigate financial data related to assets and liabilities, particularly inventory balances, to ensure accurate recording and minimize fraud risks. The assignment also highlights the importance of evaluating operational processes and planning audit steps to mitigate potential issues and provide a faithful opinion on financial declarations.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDITING THEORY AND PRACTICE

Auditing theory and practice

Name of the University

Name of the student

Authors note

Auditing theory and practice

Name of the University

Name of the student

Authors note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

AUDITING THEORY AND PRACTICE

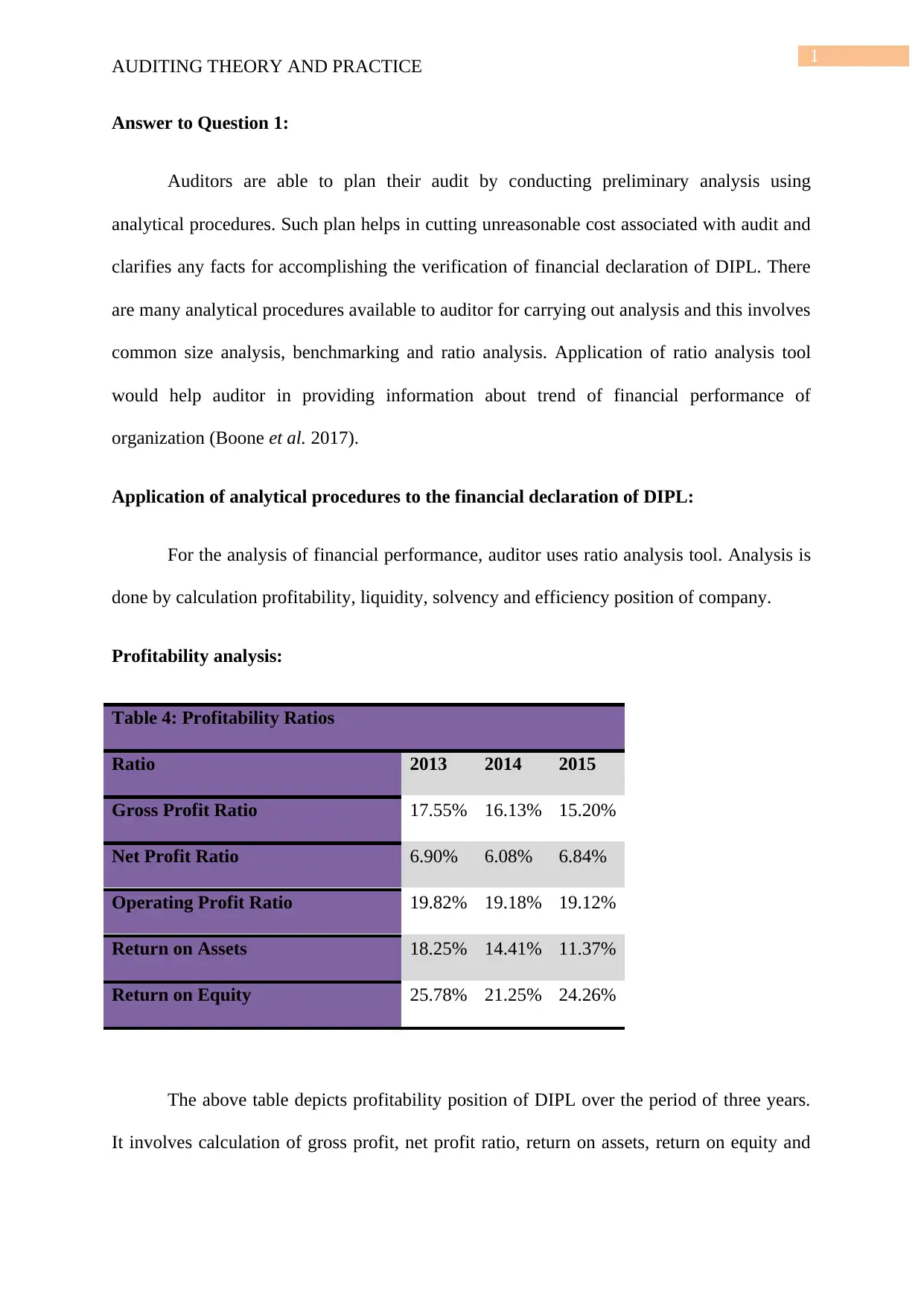

Answer to Question 1:

Auditors are able to plan their audit by conducting preliminary analysis using

analytical procedures. Such plan helps in cutting unreasonable cost associated with audit and

clarifies any facts for accomplishing the verification of financial declaration of DIPL. There

are many analytical procedures available to auditor for carrying out analysis and this involves

common size analysis, benchmarking and ratio analysis. Application of ratio analysis tool

would help auditor in providing information about trend of financial performance of

organization (Boone et al. 2017).

Application of analytical procedures to the financial declaration of DIPL:

For the analysis of financial performance, auditor uses ratio analysis tool. Analysis is

done by calculation profitability, liquidity, solvency and efficiency position of company.

Profitability analysis:

Table 4: Profitability Ratios

Ratio 2013 2014 2015

Gross Profit Ratio 17.55% 16.13% 15.20%

Net Profit Ratio 6.90% 6.08% 6.84%

Operating Profit Ratio 19.82% 19.18% 19.12%

Return on Assets 18.25% 14.41% 11.37%

Return on Equity 25.78% 21.25% 24.26%

The above table depicts profitability position of DIPL over the period of three years.

It involves calculation of gross profit, net profit ratio, return on assets, return on equity and

AUDITING THEORY AND PRACTICE

Answer to Question 1:

Auditors are able to plan their audit by conducting preliminary analysis using

analytical procedures. Such plan helps in cutting unreasonable cost associated with audit and

clarifies any facts for accomplishing the verification of financial declaration of DIPL. There

are many analytical procedures available to auditor for carrying out analysis and this involves

common size analysis, benchmarking and ratio analysis. Application of ratio analysis tool

would help auditor in providing information about trend of financial performance of

organization (Boone et al. 2017).

Application of analytical procedures to the financial declaration of DIPL:

For the analysis of financial performance, auditor uses ratio analysis tool. Analysis is

done by calculation profitability, liquidity, solvency and efficiency position of company.

Profitability analysis:

Table 4: Profitability Ratios

Ratio 2013 2014 2015

Gross Profit Ratio 17.55% 16.13% 15.20%

Net Profit Ratio 6.90% 6.08% 6.84%

Operating Profit Ratio 19.82% 19.18% 19.12%

Return on Assets 18.25% 14.41% 11.37%

Return on Equity 25.78% 21.25% 24.26%

The above table depicts profitability position of DIPL over the period of three years.

It involves calculation of gross profit, net profit ratio, return on assets, return on equity and

2

AUDITING THEORY AND PRACTICE

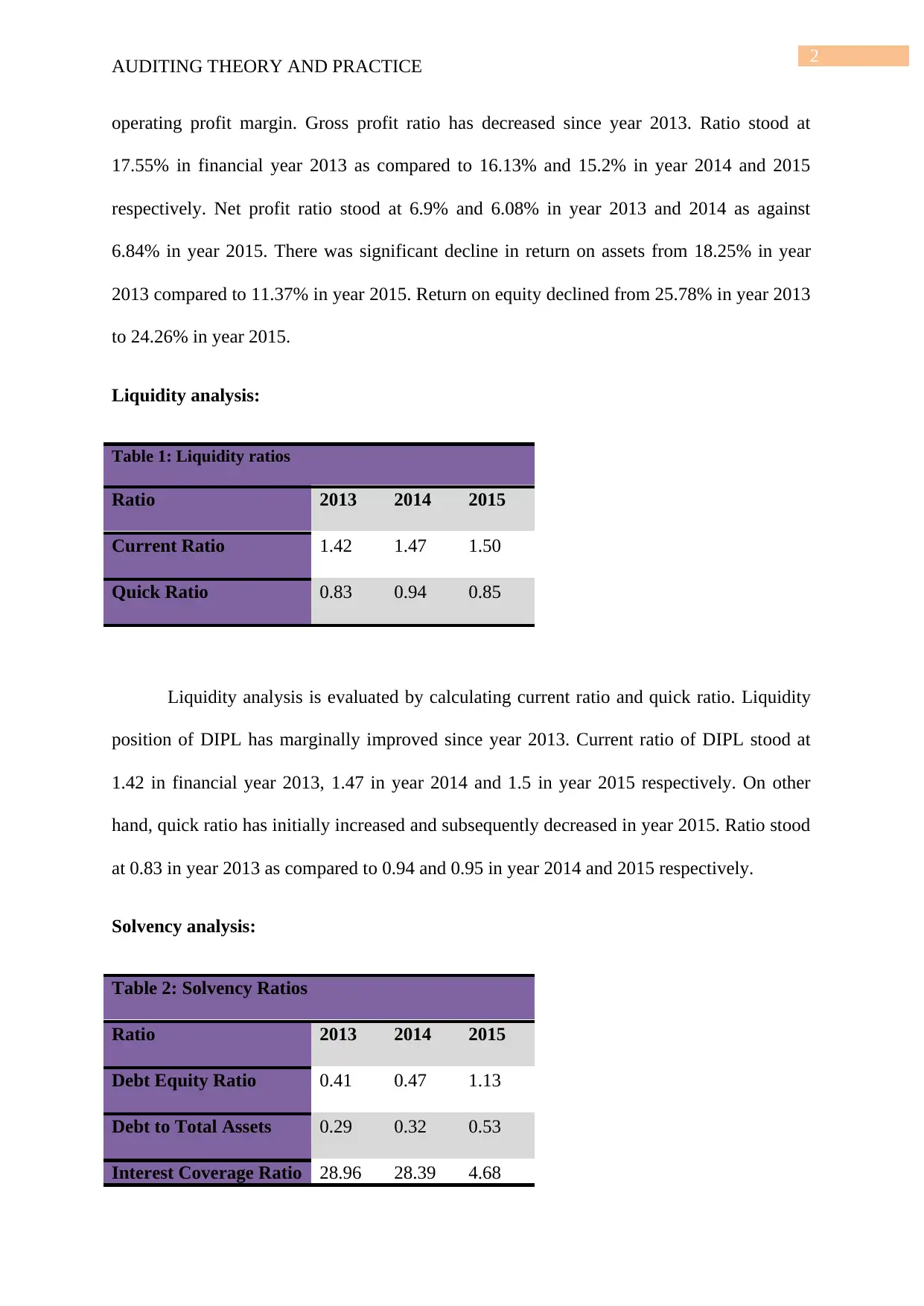

operating profit margin. Gross profit ratio has decreased since year 2013. Ratio stood at

17.55% in financial year 2013 as compared to 16.13% and 15.2% in year 2014 and 2015

respectively. Net profit ratio stood at 6.9% and 6.08% in year 2013 and 2014 as against

6.84% in year 2015. There was significant decline in return on assets from 18.25% in year

2013 compared to 11.37% in year 2015. Return on equity declined from 25.78% in year 2013

to 24.26% in year 2015.

Liquidity analysis:

Table 1: Liquidity ratios

Ratio 2013 2014 2015

Current Ratio 1.42 1.47 1.50

Quick Ratio 0.83 0.94 0.85

Liquidity analysis is evaluated by calculating current ratio and quick ratio. Liquidity

position of DIPL has marginally improved since year 2013. Current ratio of DIPL stood at

1.42 in financial year 2013, 1.47 in year 2014 and 1.5 in year 2015 respectively. On other

hand, quick ratio has initially increased and subsequently decreased in year 2015. Ratio stood

at 0.83 in year 2013 as compared to 0.94 and 0.95 in year 2014 and 2015 respectively.

Solvency analysis:

Table 2: Solvency Ratios

Ratio 2013 2014 2015

Debt Equity Ratio 0.41 0.47 1.13

Debt to Total Assets 0.29 0.32 0.53

Interest Coverage Ratio 28.96 28.39 4.68

AUDITING THEORY AND PRACTICE

operating profit margin. Gross profit ratio has decreased since year 2013. Ratio stood at

17.55% in financial year 2013 as compared to 16.13% and 15.2% in year 2014 and 2015

respectively. Net profit ratio stood at 6.9% and 6.08% in year 2013 and 2014 as against

6.84% in year 2015. There was significant decline in return on assets from 18.25% in year

2013 compared to 11.37% in year 2015. Return on equity declined from 25.78% in year 2013

to 24.26% in year 2015.

Liquidity analysis:

Table 1: Liquidity ratios

Ratio 2013 2014 2015

Current Ratio 1.42 1.47 1.50

Quick Ratio 0.83 0.94 0.85

Liquidity analysis is evaluated by calculating current ratio and quick ratio. Liquidity

position of DIPL has marginally improved since year 2013. Current ratio of DIPL stood at

1.42 in financial year 2013, 1.47 in year 2014 and 1.5 in year 2015 respectively. On other

hand, quick ratio has initially increased and subsequently decreased in year 2015. Ratio stood

at 0.83 in year 2013 as compared to 0.94 and 0.95 in year 2014 and 2015 respectively.

Solvency analysis:

Table 2: Solvency Ratios

Ratio 2013 2014 2015

Debt Equity Ratio 0.41 0.47 1.13

Debt to Total Assets 0.29 0.32 0.53

Interest Coverage Ratio 28.96 28.39 4.68

3

AUDITING THEORY AND PRACTICE

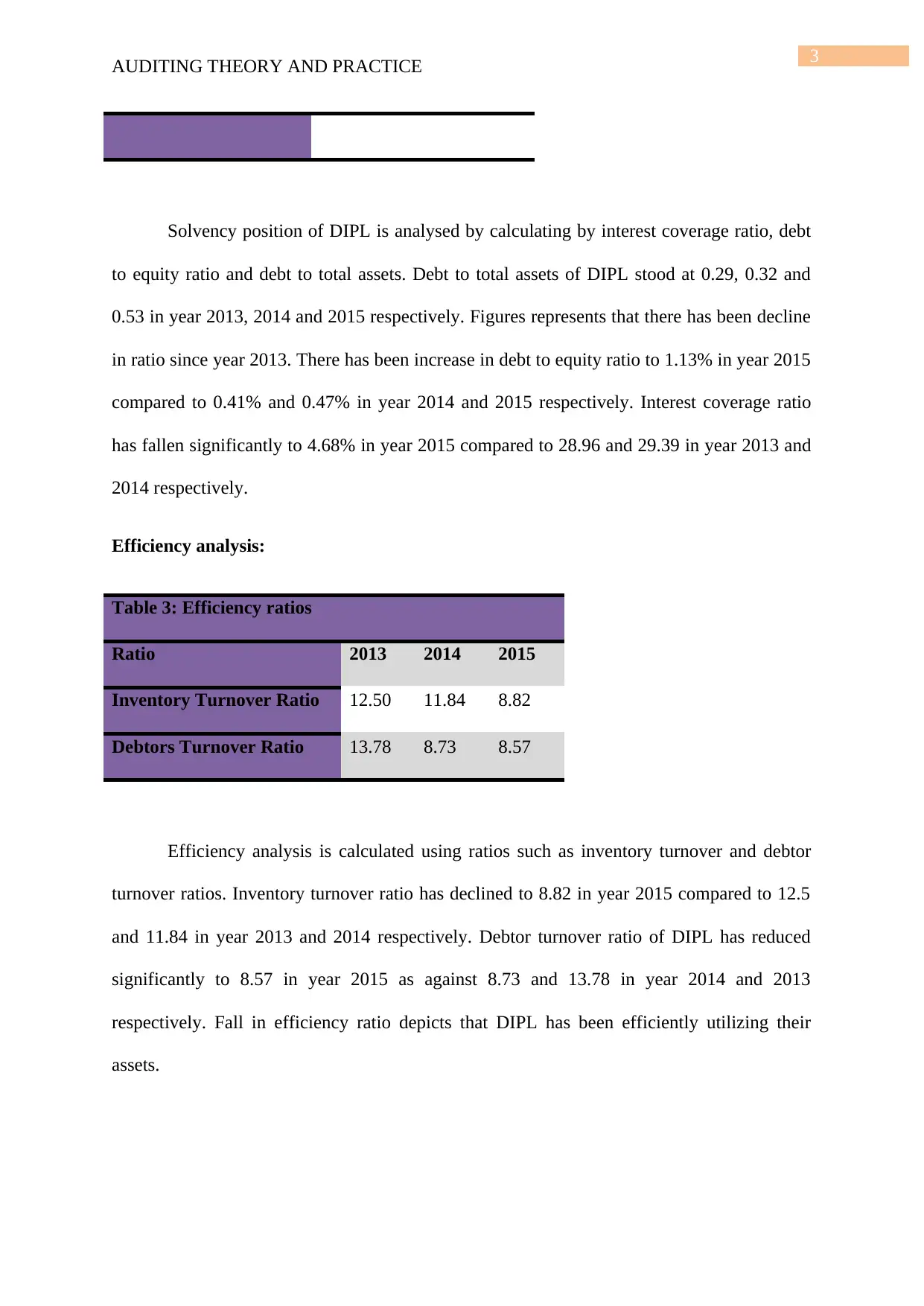

Solvency position of DIPL is analysed by calculating by interest coverage ratio, debt

to equity ratio and debt to total assets. Debt to total assets of DIPL stood at 0.29, 0.32 and

0.53 in year 2013, 2014 and 2015 respectively. Figures represents that there has been decline

in ratio since year 2013. There has been increase in debt to equity ratio to 1.13% in year 2015

compared to 0.41% and 0.47% in year 2014 and 2015 respectively. Interest coverage ratio

has fallen significantly to 4.68% in year 2015 compared to 28.96 and 29.39 in year 2013 and

2014 respectively.

Efficiency analysis:

Table 3: Efficiency ratios

Ratio 2013 2014 2015

Inventory Turnover Ratio 12.50 11.84 8.82

Debtors Turnover Ratio 13.78 8.73 8.57

Efficiency analysis is calculated using ratios such as inventory turnover and debtor

turnover ratios. Inventory turnover ratio has declined to 8.82 in year 2015 compared to 12.5

and 11.84 in year 2013 and 2014 respectively. Debtor turnover ratio of DIPL has reduced

significantly to 8.57 in year 2015 as against 8.73 and 13.78 in year 2014 and 2013

respectively. Fall in efficiency ratio depicts that DIPL has been efficiently utilizing their

assets.

AUDITING THEORY AND PRACTICE

Solvency position of DIPL is analysed by calculating by interest coverage ratio, debt

to equity ratio and debt to total assets. Debt to total assets of DIPL stood at 0.29, 0.32 and

0.53 in year 2013, 2014 and 2015 respectively. Figures represents that there has been decline

in ratio since year 2013. There has been increase in debt to equity ratio to 1.13% in year 2015

compared to 0.41% and 0.47% in year 2014 and 2015 respectively. Interest coverage ratio

has fallen significantly to 4.68% in year 2015 compared to 28.96 and 29.39 in year 2013 and

2014 respectively.

Efficiency analysis:

Table 3: Efficiency ratios

Ratio 2013 2014 2015

Inventory Turnover Ratio 12.50 11.84 8.82

Debtors Turnover Ratio 13.78 8.73 8.57

Efficiency analysis is calculated using ratios such as inventory turnover and debtor

turnover ratios. Inventory turnover ratio has declined to 8.82 in year 2015 compared to 12.5

and 11.84 in year 2013 and 2014 respectively. Debtor turnover ratio of DIPL has reduced

significantly to 8.57 in year 2015 as against 8.73 and 13.78 in year 2014 and 2013

respectively. Fall in efficiency ratio depicts that DIPL has been efficiently utilizing their

assets.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

AUDITING THEORY AND PRACTICE

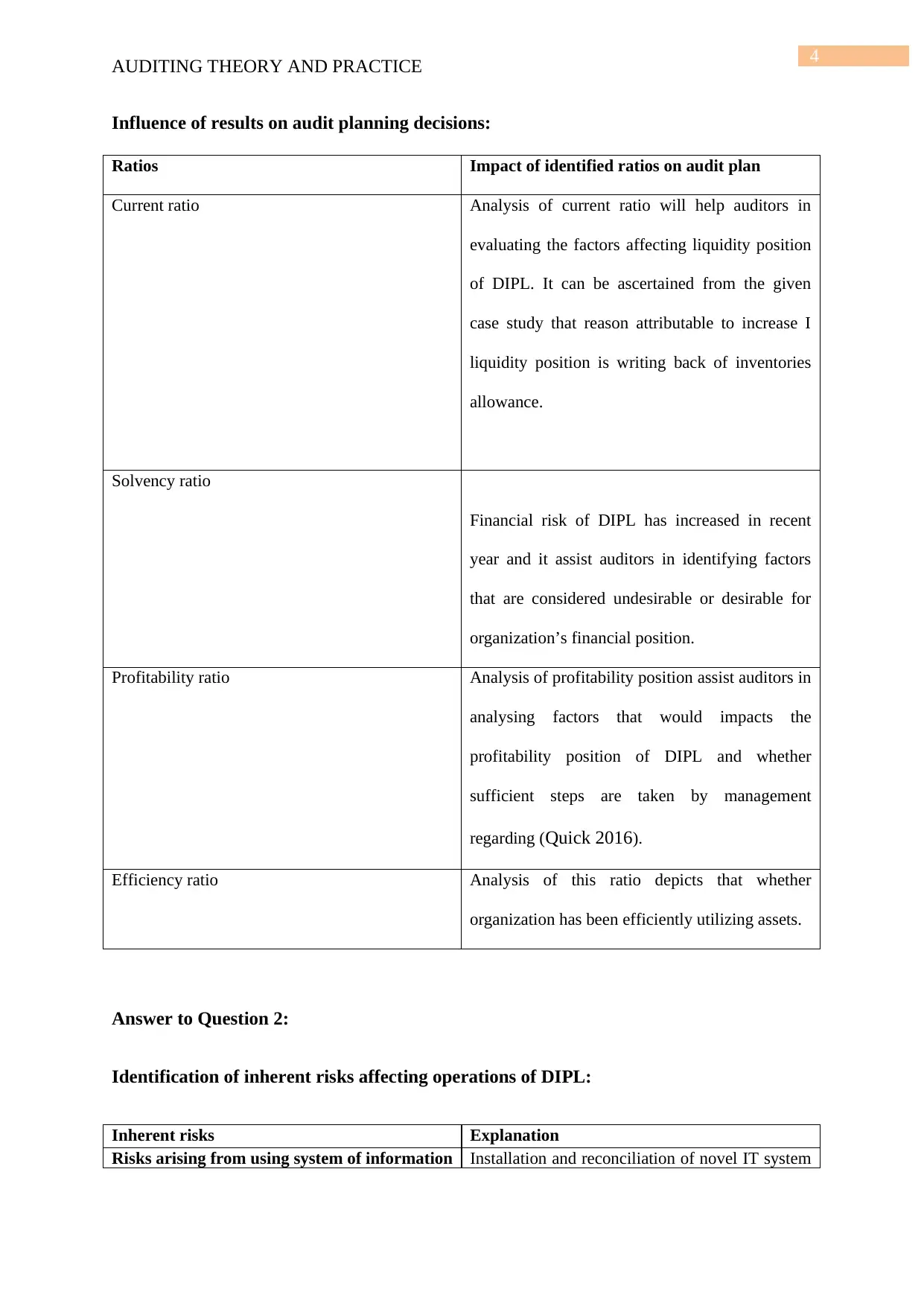

Influence of results on audit planning decisions:

Ratios Impact of identified ratios on audit plan

Current ratio Analysis of current ratio will help auditors in

evaluating the factors affecting liquidity position

of DIPL. It can be ascertained from the given

case study that reason attributable to increase I

liquidity position is writing back of inventories

allowance.

Solvency ratio

Financial risk of DIPL has increased in recent

year and it assist auditors in identifying factors

that are considered undesirable or desirable for

organization’s financial position.

Profitability ratio Analysis of profitability position assist auditors in

analysing factors that would impacts the

profitability position of DIPL and whether

sufficient steps are taken by management

regarding (Quick 2016).

Efficiency ratio Analysis of this ratio depicts that whether

organization has been efficiently utilizing assets.

Answer to Question 2:

Identification of inherent risks affecting operations of DIPL:

Inherent risks Explanation

Risks arising from using system of information Installation and reconciliation of novel IT system

AUDITING THEORY AND PRACTICE

Influence of results on audit planning decisions:

Ratios Impact of identified ratios on audit plan

Current ratio Analysis of current ratio will help auditors in

evaluating the factors affecting liquidity position

of DIPL. It can be ascertained from the given

case study that reason attributable to increase I

liquidity position is writing back of inventories

allowance.

Solvency ratio

Financial risk of DIPL has increased in recent

year and it assist auditors in identifying factors

that are considered undesirable or desirable for

organization’s financial position.

Profitability ratio Analysis of profitability position assist auditors in

analysing factors that would impacts the

profitability position of DIPL and whether

sufficient steps are taken by management

regarding (Quick 2016).

Efficiency ratio Analysis of this ratio depicts that whether

organization has been efficiently utilizing assets.

Answer to Question 2:

Identification of inherent risks affecting operations of DIPL:

Inherent risks Explanation

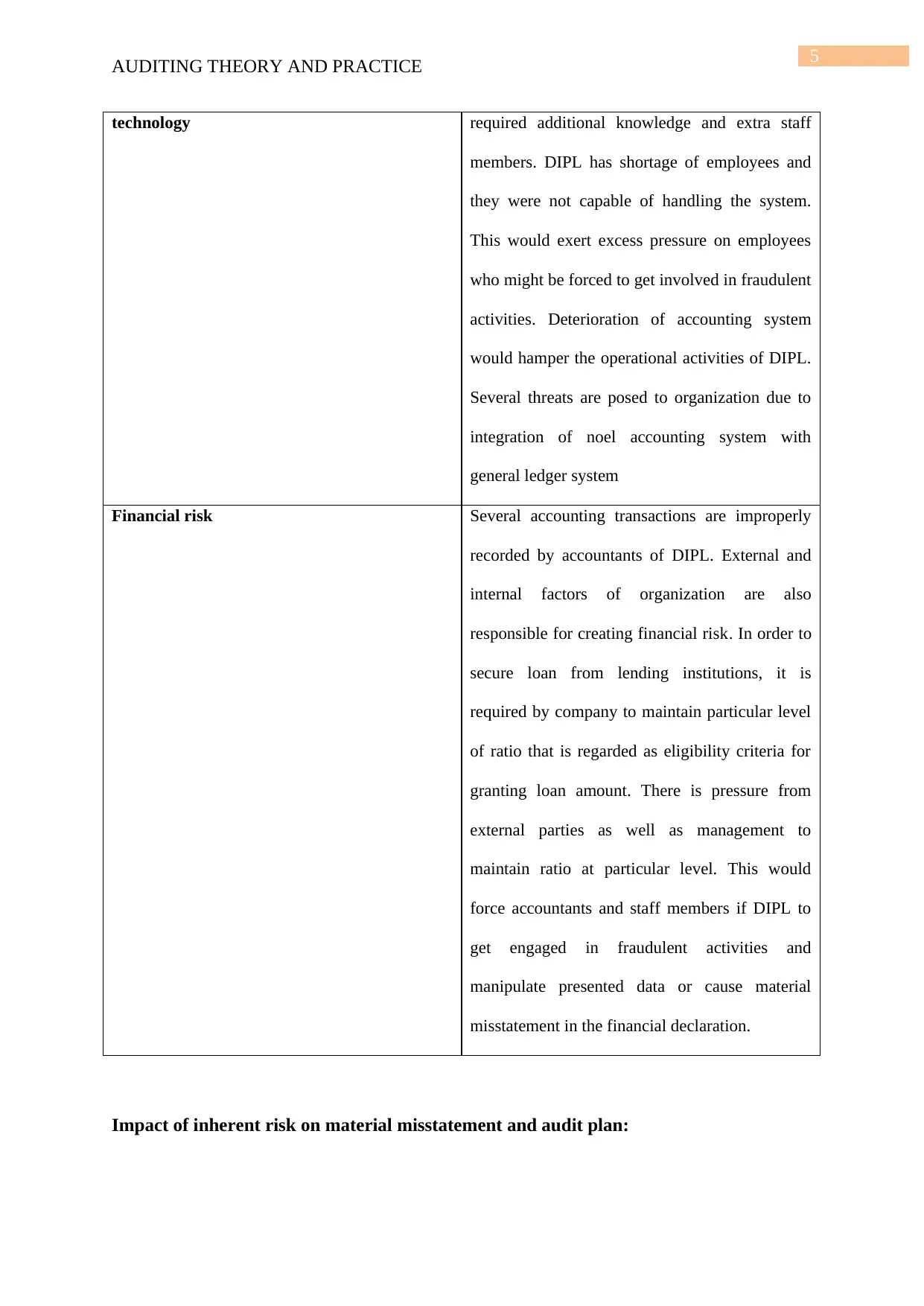

Risks arising from using system of information Installation and reconciliation of novel IT system

5

AUDITING THEORY AND PRACTICE

technology required additional knowledge and extra staff

members. DIPL has shortage of employees and

they were not capable of handling the system.

This would exert excess pressure on employees

who might be forced to get involved in fraudulent

activities. Deterioration of accounting system

would hamper the operational activities of DIPL.

Several threats are posed to organization due to

integration of noel accounting system with

general ledger system

Financial risk Several accounting transactions are improperly

recorded by accountants of DIPL. External and

internal factors of organization are also

responsible for creating financial risk. In order to

secure loan from lending institutions, it is

required by company to maintain particular level

of ratio that is regarded as eligibility criteria for

granting loan amount. There is pressure from

external parties as well as management to

maintain ratio at particular level. This would

force accountants and staff members if DIPL to

get engaged in fraudulent activities and

manipulate presented data or cause material

misstatement in the financial declaration.

Impact of inherent risk on material misstatement and audit plan:

AUDITING THEORY AND PRACTICE

technology required additional knowledge and extra staff

members. DIPL has shortage of employees and

they were not capable of handling the system.

This would exert excess pressure on employees

who might be forced to get involved in fraudulent

activities. Deterioration of accounting system

would hamper the operational activities of DIPL.

Several threats are posed to organization due to

integration of noel accounting system with

general ledger system

Financial risk Several accounting transactions are improperly

recorded by accountants of DIPL. External and

internal factors of organization are also

responsible for creating financial risk. In order to

secure loan from lending institutions, it is

required by company to maintain particular level

of ratio that is regarded as eligibility criteria for

granting loan amount. There is pressure from

external parties as well as management to

maintain ratio at particular level. This would

force accountants and staff members if DIPL to

get engaged in fraudulent activities and

manipulate presented data or cause material

misstatement in the financial declaration.

Impact of inherent risk on material misstatement and audit plan:

6

AUDITING THEORY AND PRACTICE

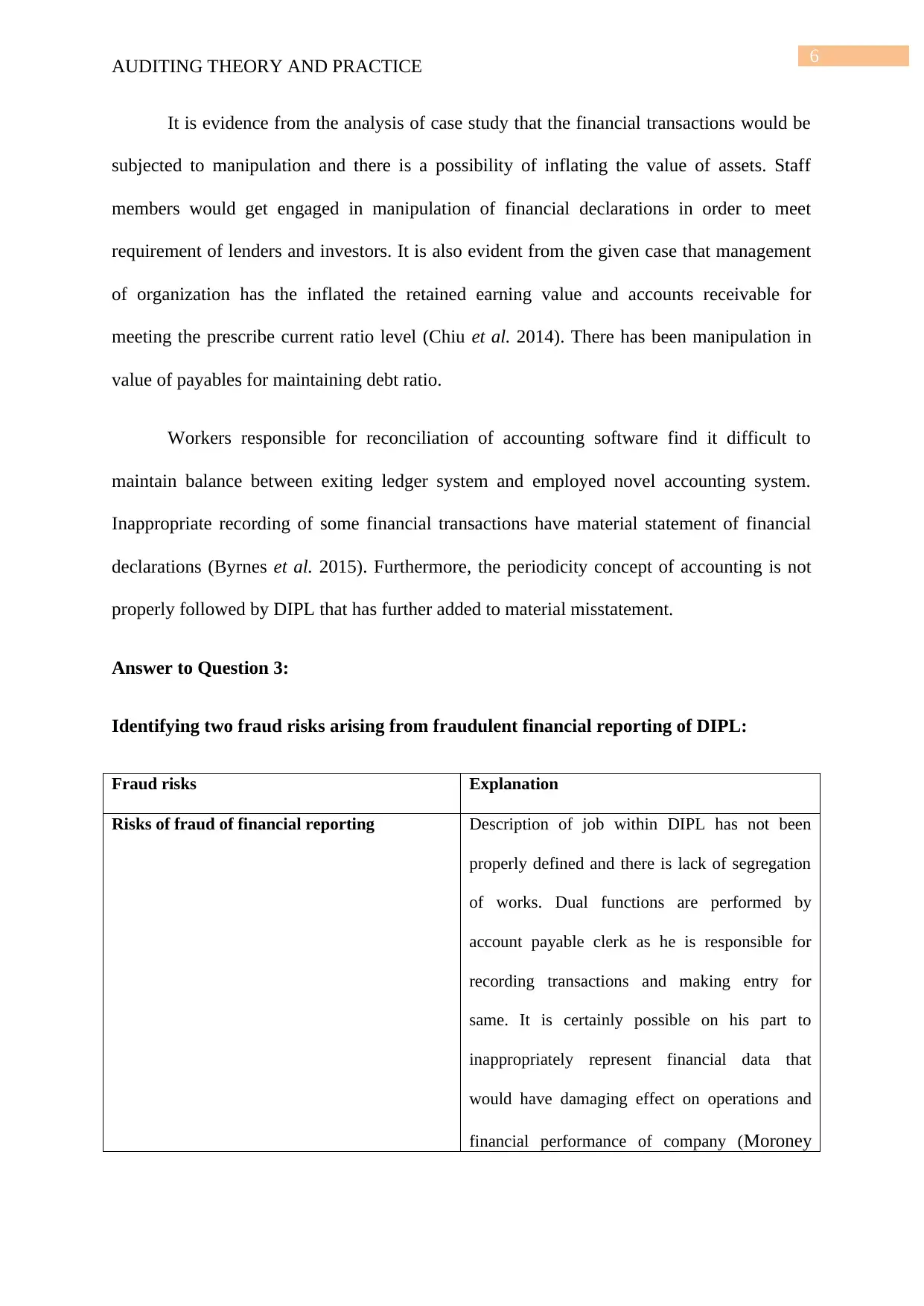

It is evidence from the analysis of case study that the financial transactions would be

subjected to manipulation and there is a possibility of inflating the value of assets. Staff

members would get engaged in manipulation of financial declarations in order to meet

requirement of lenders and investors. It is also evident from the given case that management

of organization has the inflated the retained earning value and accounts receivable for

meeting the prescribe current ratio level (Chiu et al. 2014). There has been manipulation in

value of payables for maintaining debt ratio.

Workers responsible for reconciliation of accounting software find it difficult to

maintain balance between exiting ledger system and employed novel accounting system.

Inappropriate recording of some financial transactions have material statement of financial

declarations (Byrnes et al. 2015). Furthermore, the periodicity concept of accounting is not

properly followed by DIPL that has further added to material misstatement.

Answer to Question 3:

Identifying two fraud risks arising from fraudulent financial reporting of DIPL:

Fraud risks Explanation

Risks of fraud of financial reporting Description of job within DIPL has not been

properly defined and there is lack of segregation

of works. Dual functions are performed by

account payable clerk as he is responsible for

recording transactions and making entry for

same. It is certainly possible on his part to

inappropriately represent financial data that

would have damaging effect on operations and

financial performance of company (Moroney

AUDITING THEORY AND PRACTICE

It is evidence from the analysis of case study that the financial transactions would be

subjected to manipulation and there is a possibility of inflating the value of assets. Staff

members would get engaged in manipulation of financial declarations in order to meet

requirement of lenders and investors. It is also evident from the given case that management

of organization has the inflated the retained earning value and accounts receivable for

meeting the prescribe current ratio level (Chiu et al. 2014). There has been manipulation in

value of payables for maintaining debt ratio.

Workers responsible for reconciliation of accounting software find it difficult to

maintain balance between exiting ledger system and employed novel accounting system.

Inappropriate recording of some financial transactions have material statement of financial

declarations (Byrnes et al. 2015). Furthermore, the periodicity concept of accounting is not

properly followed by DIPL that has further added to material misstatement.

Answer to Question 3:

Identifying two fraud risks arising from fraudulent financial reporting of DIPL:

Fraud risks Explanation

Risks of fraud of financial reporting Description of job within DIPL has not been

properly defined and there is lack of segregation

of works. Dual functions are performed by

account payable clerk as he is responsible for

recording transactions and making entry for

same. It is certainly possible on his part to

inappropriately represent financial data that

would have damaging effect on operations and

financial performance of company (Moroney

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING THEORY AND PRACTICE

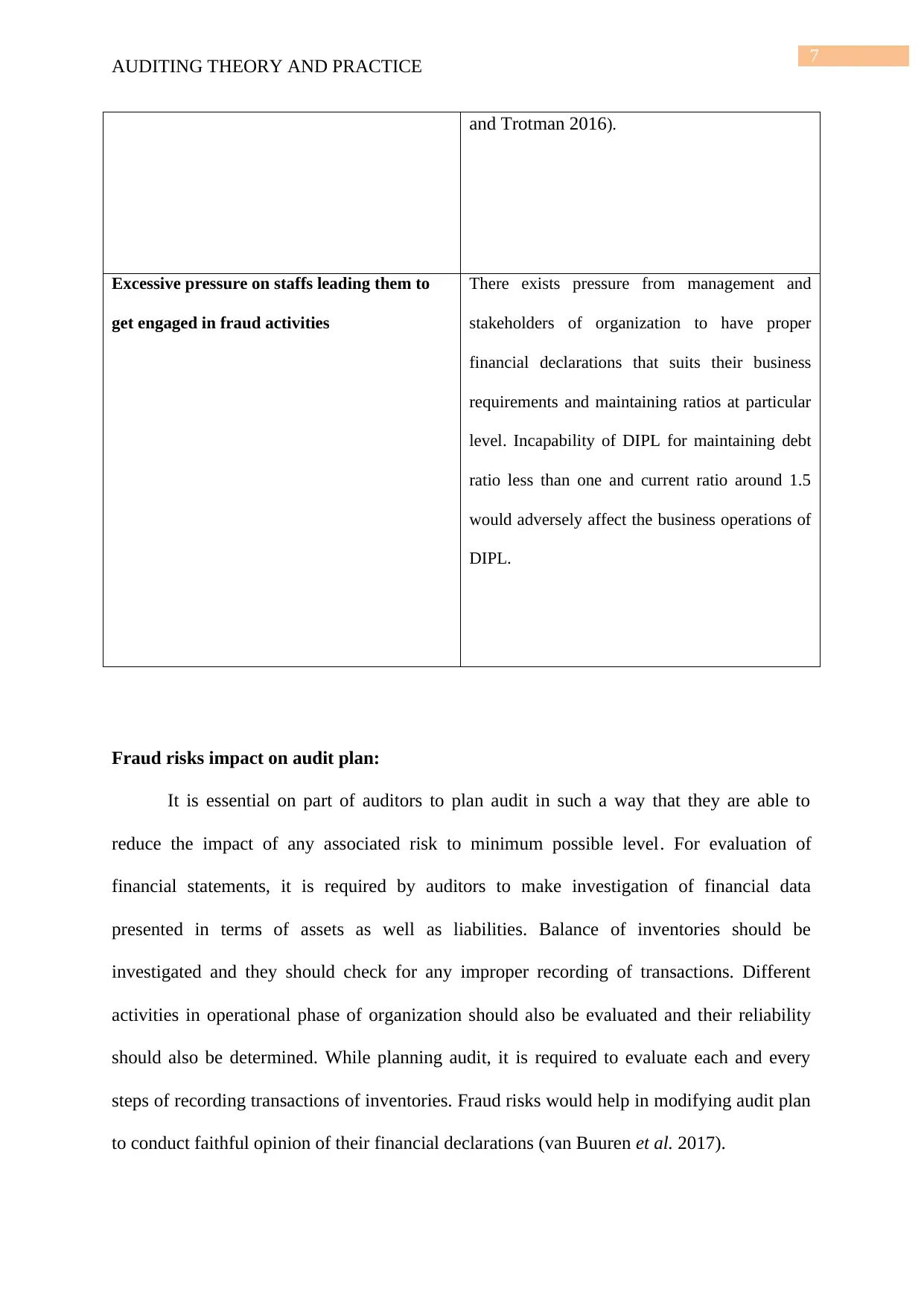

and Trotman 2016).

Excessive pressure on staffs leading them to

get engaged in fraud activities

There exists pressure from management and

stakeholders of organization to have proper

financial declarations that suits their business

requirements and maintaining ratios at particular

level. Incapability of DIPL for maintaining debt

ratio less than one and current ratio around 1.5

would adversely affect the business operations of

DIPL.

Fraud risks impact on audit plan:

It is essential on part of auditors to plan audit in such a way that they are able to

reduce the impact of any associated risk to minimum possible level. For evaluation of

financial statements, it is required by auditors to make investigation of financial data

presented in terms of assets as well as liabilities. Balance of inventories should be

investigated and they should check for any improper recording of transactions. Different

activities in operational phase of organization should also be evaluated and their reliability

should also be determined. While planning audit, it is required to evaluate each and every

steps of recording transactions of inventories. Fraud risks would help in modifying audit plan

to conduct faithful opinion of their financial declarations (van Buuren et al. 2017).

AUDITING THEORY AND PRACTICE

and Trotman 2016).

Excessive pressure on staffs leading them to

get engaged in fraud activities

There exists pressure from management and

stakeholders of organization to have proper

financial declarations that suits their business

requirements and maintaining ratios at particular

level. Incapability of DIPL for maintaining debt

ratio less than one and current ratio around 1.5

would adversely affect the business operations of

DIPL.

Fraud risks impact on audit plan:

It is essential on part of auditors to plan audit in such a way that they are able to

reduce the impact of any associated risk to minimum possible level. For evaluation of

financial statements, it is required by auditors to make investigation of financial data

presented in terms of assets as well as liabilities. Balance of inventories should be

investigated and they should check for any improper recording of transactions. Different

activities in operational phase of organization should also be evaluated and their reliability

should also be determined. While planning audit, it is required to evaluate each and every

steps of recording transactions of inventories. Fraud risks would help in modifying audit plan

to conduct faithful opinion of their financial declarations (van Buuren et al. 2017).

8

AUDITING THEORY AND PRACTICE

References:

Boone, J.P., Khurana, I.K., Raman, K.K., Chen, L.H., Chung, H.H.S., Peters, G.F., Wynn,

J.P.J., Chen, Y., Knechel, W.R., Marisetty, V.B. and Truong, C., 2017. Auditing: A Journal

of Practice & Theory A Publication of the Auditing Section of the American Accounting

Association.

Broberg, P., Umans, T. and Gerlofstig, C., 2013. Balance between auditing and marketing:

An explorative study. Journal of International Accounting, Auditing and Taxation, 22(1),

pp.57-70.

Byrnes, P.E., Al-Awadhi, C.A., Gullvist, B., Brown-Liburd, H., Teeter, C.R., Warren Jr, J.D.

and Vasarhelyi, M., 2015. Evolution of auditing: from the traditional approach to the future

audit. Audit Analytics, 71.

Chiu, V., Liu, Q. and Vasarhelyi, M.A., 2014. The development and intellectual structure of

continuous auditing research. Journal of accounting literature, 33(1), pp.37-57.

Hardy, C.A. and Laslett, G., 2014. Continuous Auditing and Monitoring in Practice: Lessons

from Metcash's Business Assurance Group. Journal of Information Systems, 29(2), pp.183-

194.

Krahel, J.P. and Titera, W.R., 2015. Consequences of big data and formalization on

accounting and auditing standards. Accounting Horizons, 29(2), pp.409-422.

AUDITING THEORY AND PRACTICE

References:

Boone, J.P., Khurana, I.K., Raman, K.K., Chen, L.H., Chung, H.H.S., Peters, G.F., Wynn,

J.P.J., Chen, Y., Knechel, W.R., Marisetty, V.B. and Truong, C., 2017. Auditing: A Journal

of Practice & Theory A Publication of the Auditing Section of the American Accounting

Association.

Broberg, P., Umans, T. and Gerlofstig, C., 2013. Balance between auditing and marketing:

An explorative study. Journal of International Accounting, Auditing and Taxation, 22(1),

pp.57-70.

Byrnes, P.E., Al-Awadhi, C.A., Gullvist, B., Brown-Liburd, H., Teeter, C.R., Warren Jr, J.D.

and Vasarhelyi, M., 2015. Evolution of auditing: from the traditional approach to the future

audit. Audit Analytics, 71.

Chiu, V., Liu, Q. and Vasarhelyi, M.A., 2014. The development and intellectual structure of

continuous auditing research. Journal of accounting literature, 33(1), pp.37-57.

Hardy, C.A. and Laslett, G., 2014. Continuous Auditing and Monitoring in Practice: Lessons

from Metcash's Business Assurance Group. Journal of Information Systems, 29(2), pp.183-

194.

Krahel, J.P. and Titera, W.R., 2015. Consequences of big data and formalization on

accounting and auditing standards. Accounting Horizons, 29(2), pp.409-422.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.