Case Study: Tax Consequences of Timber Disposal

VerifiedAdded on 2019/10/30

|10

|2806

|122

Report

AI Summary

A case study highlights the issue of tax evasion by Duke, who guaranteed to pay his fellows for their services provided. The agreement was written and submitted to his fellows, declaring that Duke will make payments with extra payment if there would be any for the payment made in exchange for their service provided. However, Duke attempted to claim these types of payments as a tax deduction for tax evasion. The regulatory provisions and applicability of provisions are discussed, including the treatment of employment agreements, yearly payments, and tax compliance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

HI6028 Taxation Theory, Practice

& Law

T2 2017 Individual Assignment

& Law

T2 2017 Individual Assignment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Question 1..................................................................................................................................3

Issue........................................................................................................................................3

Regulatory provisions............................................................................................................3

Applicability of provisions.....................................................................................................3

Conclusion..............................................................................................................................3

Question 2..................................................................................................................................3

Issue........................................................................................................................................3

Regulatory provisions............................................................................................................3

Applicability of provisions.....................................................................................................3

Conclusion..............................................................................................................................3

Question 3..................................................................................................................................3

Issue........................................................................................................................................3

Regulatory provisions............................................................................................................3

Applicability of provisions.....................................................................................................3

Conclusion..............................................................................................................................3

Question 4..................................................................................................................................3

Issue........................................................................................................................................3

Regulatory provisions............................................................................................................3

Applicability of provisions.....................................................................................................3

Conclusion..............................................................................................................................3

Question 5..................................................................................................................................3

Issue........................................................................................................................................3

Regulatory provisions............................................................................................................3

Applicability of provisions.....................................................................................................3

Conclusion..............................................................................................................................3

References..................................................................................................................................4

Question 1..................................................................................................................................3

Issue........................................................................................................................................3

Regulatory provisions............................................................................................................3

Applicability of provisions.....................................................................................................3

Conclusion..............................................................................................................................3

Question 2..................................................................................................................................3

Issue........................................................................................................................................3

Regulatory provisions............................................................................................................3

Applicability of provisions.....................................................................................................3

Conclusion..............................................................................................................................3

Question 3..................................................................................................................................3

Issue........................................................................................................................................3

Regulatory provisions............................................................................................................3

Applicability of provisions.....................................................................................................3

Conclusion..............................................................................................................................3

Question 4..................................................................................................................................3

Issue........................................................................................................................................3

Regulatory provisions............................................................................................................3

Applicability of provisions.....................................................................................................3

Conclusion..............................................................................................................................3

Question 5..................................................................................................................................3

Issue........................................................................................................................................3

Regulatory provisions............................................................................................................3

Applicability of provisions.....................................................................................................3

Conclusion..............................................................................................................................3

References..................................................................................................................................4

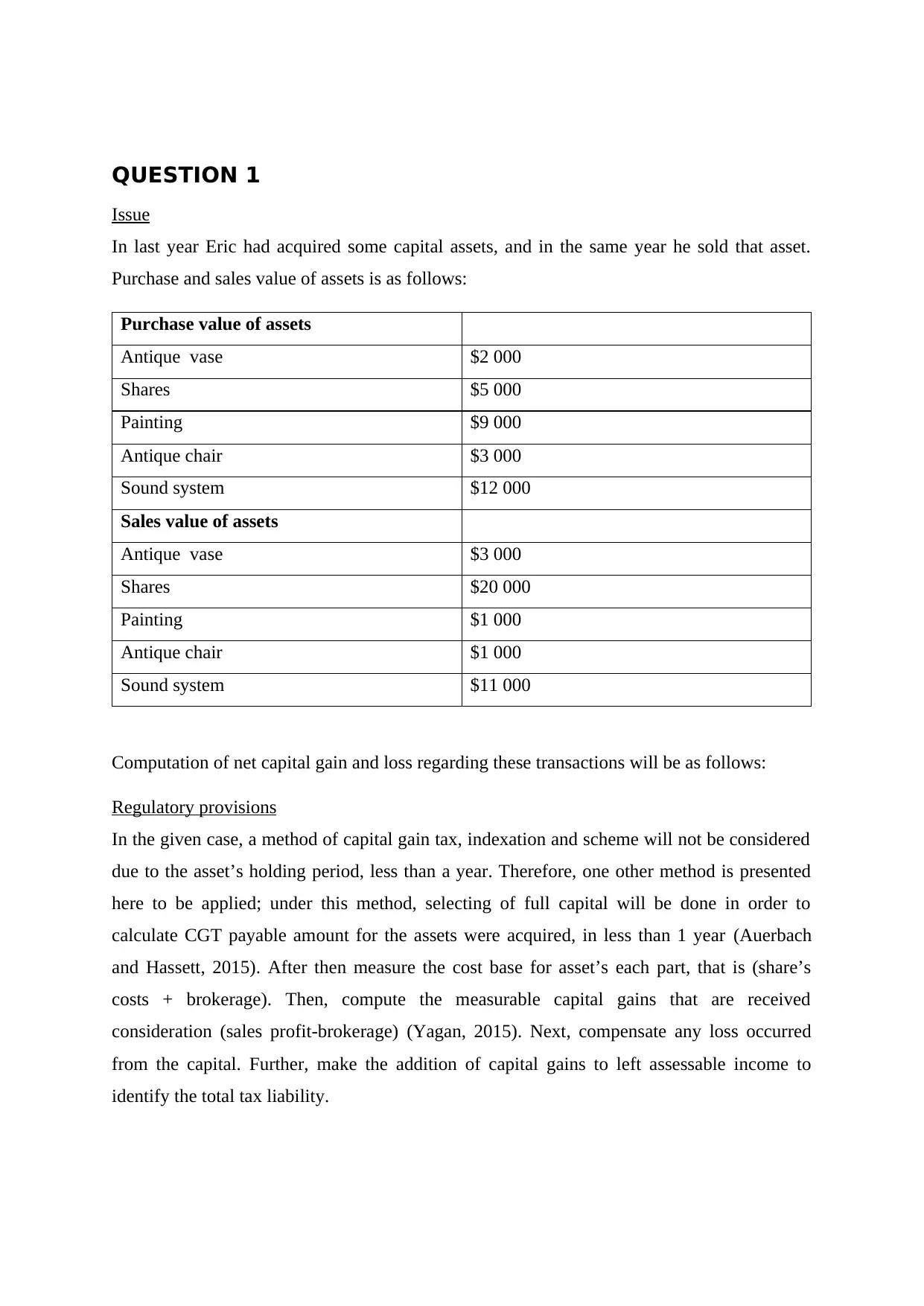

QUESTION 1

Issue

In last year Eric had acquired some capital assets, and in the same year he sold that asset.

Purchase and sales value of assets is as follows:

Purchase value of assets

Antique vase $2 000

Shares $5 000

Painting $9 000

Antique chair $3 000

Sound system $12 000

Sales value of assets

Antique vase $3 000

Shares $20 000

Painting $1 000

Antique chair $1 000

Sound system $11 000

Computation of net capital gain and loss regarding these transactions will be as follows:

Regulatory provisions

In the given case, a method of capital gain tax, indexation and scheme will not be considered

due to the asset’s holding period, less than a year. Therefore, one other method is presented

here to be applied; under this method, selecting of full capital will be done in order to

calculate CGT payable amount for the assets were acquired, in less than 1 year (Auerbach

and Hassett, 2015). After then measure the cost base for asset’s each part, that is (share’s

costs + brokerage). Then, compute the measurable capital gains that are received

consideration (sales profit-brokerage) (Yagan, 2015). Next, compensate any loss occurred

from the capital. Further, make the addition of capital gains to left assessable income to

identify the total tax liability.

Issue

In last year Eric had acquired some capital assets, and in the same year he sold that asset.

Purchase and sales value of assets is as follows:

Purchase value of assets

Antique vase $2 000

Shares $5 000

Painting $9 000

Antique chair $3 000

Sound system $12 000

Sales value of assets

Antique vase $3 000

Shares $20 000

Painting $1 000

Antique chair $1 000

Sound system $11 000

Computation of net capital gain and loss regarding these transactions will be as follows:

Regulatory provisions

In the given case, a method of capital gain tax, indexation and scheme will not be considered

due to the asset’s holding period, less than a year. Therefore, one other method is presented

here to be applied; under this method, selecting of full capital will be done in order to

calculate CGT payable amount for the assets were acquired, in less than 1 year (Auerbach

and Hassett, 2015). After then measure the cost base for asset’s each part, that is (share’s

costs + brokerage). Then, compute the measurable capital gains that are received

consideration (sales profit-brokerage) (Yagan, 2015). Next, compensate any loss occurred

from the capital. Further, make the addition of capital gains to left assessable income to

identify the total tax liability.

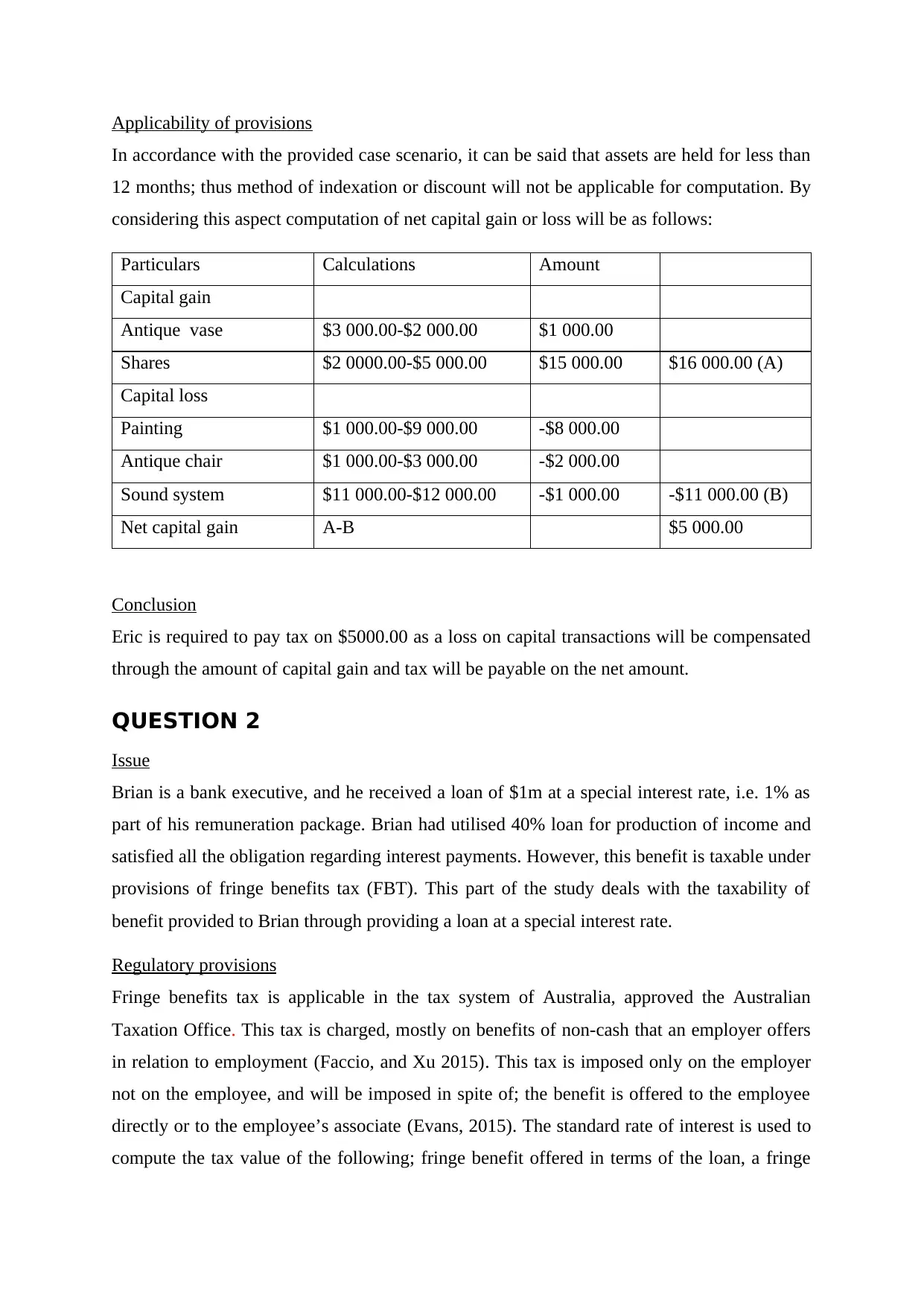

Applicability of provisions

In accordance with the provided case scenario, it can be said that assets are held for less than

12 months; thus method of indexation or discount will not be applicable for computation. By

considering this aspect computation of net capital gain or loss will be as follows:

Particulars Calculations Amount

Capital gain

Antique vase $3 000.00-$2 000.00 $1 000.00

Shares $2 0000.00-$5 000.00 $15 000.00 $16 000.00 (A)

Capital loss

Painting $1 000.00-$9 000.00 -$8 000.00

Antique chair $1 000.00-$3 000.00 -$2 000.00

Sound system $11 000.00-$12 000.00 -$1 000.00 -$11 000.00 (B)

Net capital gain A-B $5 000.00

Conclusion

Eric is required to pay tax on $5000.00 as a loss on capital transactions will be compensated

through the amount of capital gain and tax will be payable on the net amount.

QUESTION 2

Issue

Brian is a bank executive, and he received a loan of $1m at a special interest rate, i.e. 1% as

part of his remuneration package. Brian had utilised 40% loan for production of income and

satisfied all the obligation regarding interest payments. However, this benefit is taxable under

provisions of fringe benefits tax (FBT). This part of the study deals with the taxability of

benefit provided to Brian through providing a loan at a special interest rate.

Regulatory provisions

Fringe benefits tax is applicable in the tax system of Australia, approved the Australian

Taxation Office. This tax is charged, mostly on benefits of non-cash that an employer offers

in relation to employment (Faccio, and Xu 2015). This tax is imposed only on the employer

not on the employee, and will be imposed in spite of; the benefit is offered to the employee

directly or to the employee’s associate (Evans, 2015). The standard rate of interest is used to

compute the tax value of the following; fringe benefit offered in terms of the loan, a fringe

In accordance with the provided case scenario, it can be said that assets are held for less than

12 months; thus method of indexation or discount will not be applicable for computation. By

considering this aspect computation of net capital gain or loss will be as follows:

Particulars Calculations Amount

Capital gain

Antique vase $3 000.00-$2 000.00 $1 000.00

Shares $2 0000.00-$5 000.00 $15 000.00 $16 000.00 (A)

Capital loss

Painting $1 000.00-$9 000.00 -$8 000.00

Antique chair $1 000.00-$3 000.00 -$2 000.00

Sound system $11 000.00-$12 000.00 -$1 000.00 -$11 000.00 (B)

Net capital gain A-B $5 000.00

Conclusion

Eric is required to pay tax on $5000.00 as a loss on capital transactions will be compensated

through the amount of capital gain and tax will be payable on the net amount.

QUESTION 2

Issue

Brian is a bank executive, and he received a loan of $1m at a special interest rate, i.e. 1% as

part of his remuneration package. Brian had utilised 40% loan for production of income and

satisfied all the obligation regarding interest payments. However, this benefit is taxable under

provisions of fringe benefits tax (FBT). This part of the study deals with the taxability of

benefit provided to Brian through providing a loan at a special interest rate.

Regulatory provisions

Fringe benefits tax is applicable in the tax system of Australia, approved the Australian

Taxation Office. This tax is charged, mostly on benefits of non-cash that an employer offers

in relation to employment (Faccio, and Xu 2015). This tax is imposed only on the employer

not on the employee, and will be imposed in spite of; the benefit is offered to the employee

directly or to the employee’s associate (Evans, 2015). The standard rate of interest is used to

compute the tax value of the following; fringe benefit offered in terms of the loan, a fringe

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

benefit of a car, in which employee decides to value benefit by the method of operating cost.

For 2017 rate of statutory interest with reference to TD 2016/5 for FBT year1 April 2016 to

31 March 2017 is 5.65% (Woellner and et.al, 2016).

Applicability of provisions

By considering the above-described regulation of FBT, it can be said that Brian is liable to

pay tax at different amount of interest. Computation of the taxable value of the fringe benefit

for Brian for the 2016/17 FBT year is as follows:

Particulars Amount

Interest to be paid by

applying special interest rate

$1 000 000*1% $10 000.00

Interest to be paid by

applying statutory rate

$1 000 000*5.65% $56 500.00

Taxable value $56 500.00-$56 500.00 $46 500.00

This fact will not alter the calculations that only 40% is used for producing income, so loan

value will be considered as a whole.

Conclusion

In both, the cases taxable value will be same as the overall value of the benefit is considered,

and there are no specific provisions regarding monthly or annual payment for a fringe benefit.

QUESTION 3

Issue

In this case, situation rental property is purchased by Jack and Jill (his wife) as joint tenants.

For this, they formed agreement according to which profit will be distributed in the ratio of

1:9 to Jack and Jill respectively and if there is loss than Jack will be entitled to 100% of the

loss. Thus, the issue is regarding tax implication of revenue and capital loss.

Regulatory provisions

TR 93/32 taxation of rental property - division of net income or loss between co-owners

From the common perception, it is reliable to distinguish the rental property owner into

Beaumont J in McDonald's case at ATR p.96 joint owners in investments rather than instead

of partners in operational activities of the business (Barrett and Veal, 2016).

For 2017 rate of statutory interest with reference to TD 2016/5 for FBT year1 April 2016 to

31 March 2017 is 5.65% (Woellner and et.al, 2016).

Applicability of provisions

By considering the above-described regulation of FBT, it can be said that Brian is liable to

pay tax at different amount of interest. Computation of the taxable value of the fringe benefit

for Brian for the 2016/17 FBT year is as follows:

Particulars Amount

Interest to be paid by

applying special interest rate

$1 000 000*1% $10 000.00

Interest to be paid by

applying statutory rate

$1 000 000*5.65% $56 500.00

Taxable value $56 500.00-$56 500.00 $46 500.00

This fact will not alter the calculations that only 40% is used for producing income, so loan

value will be considered as a whole.

Conclusion

In both, the cases taxable value will be same as the overall value of the benefit is considered,

and there are no specific provisions regarding monthly or annual payment for a fringe benefit.

QUESTION 3

Issue

In this case, situation rental property is purchased by Jack and Jill (his wife) as joint tenants.

For this, they formed agreement according to which profit will be distributed in the ratio of

1:9 to Jack and Jill respectively and if there is loss than Jack will be entitled to 100% of the

loss. Thus, the issue is regarding tax implication of revenue and capital loss.

Regulatory provisions

TR 93/32 taxation of rental property - division of net income or loss between co-owners

From the common perception, it is reliable to distinguish the rental property owner into

Beaumont J in McDonald's case at ATR p.96 joint owners in investments rather than instead

of partners in operational activities of the business (Barrett and Veal, 2016).

Thus, rental property co owners usually are not partners in terms of general law, and with the

consequence that they are not regarded to the applicable general law of partnership inclusive

of profit and loss distribution of property or assets (TR 93/32 taxation of rental property -

division of net income or loss between co-owners, 1993).

Personally, there is no survival of any partnership according to the general law, if the partners

are respondent and their spouse. Their relation can be referred as co-ownership, even if they

can be considered under the Act of subsection 6(1). Certain circumstances are of no

consequence for our point. It sounds interesting; their academic partnership will take it out

with results and will be considered as a partnership for certain reasons. It will not allow the

respondent to make a deduction of the total loss in partnership (Pearce and Pinto, 2015).

Although, respondent can only make a deduction in own interest the loss of partnership.

Respondent’s own interest is that interest, on which a partner is entirely entitled. In contrast

to his mutual interest in the total, FCT v Whiting (1943)1.

Thus, It is vital to identify that both respondent and Mrs McDonald were only notional

partners for the Act’s purpose or were true partners as per the general law.

Applicability of provisions and Conclusion

By considering the above case provisions, jack is not entitled to the entire loss and he will

compensate loss only portion of profit, i.e. 10%, and same will be applicable in a situation

where this property is sold irrespective of the fact that there is capital gain or loss.

QUESTION 4

Issue

In the case of IRC v. Duke of Westminster, he carried out a deed with his helpers who

were its gardener or servants. In that agreement, Duke made a guaranteed to pay out some

amount of money to his fellows for their provided services (QC, 2016). Further, the

agreement was done in written and was submitted to his fellows, declaring that Duke will

make payments with extra payment, if there would be any, for the payment made in exchange

for their service provided. Duke attempted to claim these types of payments for a tax

deduction for the agreement of tax evasion.

1 68 CLR 199 at 204; 2 AITR 421 at 425-6

consequence that they are not regarded to the applicable general law of partnership inclusive

of profit and loss distribution of property or assets (TR 93/32 taxation of rental property -

division of net income or loss between co-owners, 1993).

Personally, there is no survival of any partnership according to the general law, if the partners

are respondent and their spouse. Their relation can be referred as co-ownership, even if they

can be considered under the Act of subsection 6(1). Certain circumstances are of no

consequence for our point. It sounds interesting; their academic partnership will take it out

with results and will be considered as a partnership for certain reasons. It will not allow the

respondent to make a deduction of the total loss in partnership (Pearce and Pinto, 2015).

Although, respondent can only make a deduction in own interest the loss of partnership.

Respondent’s own interest is that interest, on which a partner is entirely entitled. In contrast

to his mutual interest in the total, FCT v Whiting (1943)1.

Thus, It is vital to identify that both respondent and Mrs McDonald were only notional

partners for the Act’s purpose or were true partners as per the general law.

Applicability of provisions and Conclusion

By considering the above case provisions, jack is not entitled to the entire loss and he will

compensate loss only portion of profit, i.e. 10%, and same will be applicable in a situation

where this property is sold irrespective of the fact that there is capital gain or loss.

QUESTION 4

Issue

In the case of IRC v. Duke of Westminster, he carried out a deed with his helpers who

were its gardener or servants. In that agreement, Duke made a guaranteed to pay out some

amount of money to his fellows for their provided services (QC, 2016). Further, the

agreement was done in written and was submitted to his fellows, declaring that Duke will

make payments with extra payment, if there would be any, for the payment made in exchange

for their service provided. Duke attempted to claim these types of payments for a tax

deduction for the agreement of tax evasion.

1 68 CLR 199 at 204; 2 AITR 421 at 425-6

Regulatory provisions and Applicability of provisions

In the above-described case, the main problem lies with the deed that shall it be treated or

observed as the employment agreement. Initially, Duke was not paying his fellows on a

weekly basis nor on a monthly basis as the contract would mean to (Westminster doctrine,

2016). Thus it can be said that there was the least concern over the contract, which the most

significant term the formulation n of legally obligatory contract.

Under the deed of covenant, it payment can only be tax deductible if there is a yearly

payment made to the helpers (Bankman and et.al, 2017). Duke would only entitle to make a

claim for tax relief for the yearly payment or the payment made in exchange for services

rendered in that particular period.

Conclusion

Relevancy of this case in the present scenario

In this cited case, there was a suggestion that tax evasion will only be entitled if it practises

that established statute law, in this case, the general rule of the deed of covalent format can

decrease the tax liability of if it is accepted and the claim can only be made on a yearly basis.

In March 2011, a document was issued by the revenue as ‘Tackling Tax Avoidance’, which

showed how they would effort to solve the problems of tax evasion in upcoming future

(Sharma, 2015).

The document declared that they aim to make development in the rules of Tax Avoidance

Disclosure, as per these some schemes of tax must be informed the taxation authorities, soon

after the implementation (Bloom, 2015). The major aim is to help users for making out

differences among terms related to ‘artificial avoidance schemes’ and ‘ordinary sensible tax

planning’.

QUESTION 5

Issue

According to this case situation; Bill is engaged in the sale of timber produced on his land as

individual transaction or sale of rights. Thus this part of study deals with tax consequence in

both the scenarios.

Regulatory provisions

Taxation Ruling 95/6: Disposal of standing timber, not in the ordinary course of business

In the above-described case, the main problem lies with the deed that shall it be treated or

observed as the employment agreement. Initially, Duke was not paying his fellows on a

weekly basis nor on a monthly basis as the contract would mean to (Westminster doctrine,

2016). Thus it can be said that there was the least concern over the contract, which the most

significant term the formulation n of legally obligatory contract.

Under the deed of covenant, it payment can only be tax deductible if there is a yearly

payment made to the helpers (Bankman and et.al, 2017). Duke would only entitle to make a

claim for tax relief for the yearly payment or the payment made in exchange for services

rendered in that particular period.

Conclusion

Relevancy of this case in the present scenario

In this cited case, there was a suggestion that tax evasion will only be entitled if it practises

that established statute law, in this case, the general rule of the deed of covalent format can

decrease the tax liability of if it is accepted and the claim can only be made on a yearly basis.

In March 2011, a document was issued by the revenue as ‘Tackling Tax Avoidance’, which

showed how they would effort to solve the problems of tax evasion in upcoming future

(Sharma, 2015).

The document declared that they aim to make development in the rules of Tax Avoidance

Disclosure, as per these some schemes of tax must be informed the taxation authorities, soon

after the implementation (Bloom, 2015). The major aim is to help users for making out

differences among terms related to ‘artificial avoidance schemes’ and ‘ordinary sensible tax

planning’.

QUESTION 5

Issue

According to this case situation; Bill is engaged in the sale of timber produced on his land as

individual transaction or sale of rights. Thus this part of study deals with tax consequence in

both the scenarios.

Regulatory provisions

Taxation Ruling 95/6: Disposal of standing timber, not in the ordinary course of business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trees for disposal has been owned by a taxpayer, that has planted but not essentially by the

taxpayer and intended for the sale might affect the actual value of trees contained in the

assessable income of taxpayer as per the subsection 36(1), when the disposal would take

place (Frecknall-Hughes and Kirchler, 2015).

The tax will be payable irrespective of aspect that business is carried out of the forest

operations, as long as the business is carried out by the taxpayer and the disposal is not done

in the regular course of business (Burkhauser, Hahn and Wilkins, 2015). The major

requirement is that the trees represent the business assets as a whole.

If or if not the specific contract leads to trees disposal, as per distinct, from the sale of Land's

interest, will mostly depend on the analyzing of the contract (Taxation Ruling: TR 95/6PW -

Notice of Partial Withdrawal, 2010). The Subsection 36(1) will not be applicable, in case the

trees are land leased and there is no entire ownership of the lessee on the leased land for this

aspect case of Rose v. FC2 can be considered (Bond and Wright, 2017).

Disposal of rights to standing timber

A taxpayer has been carrying a business of forest operations can put standing timber into a

sale by providing the right to some individual to cut out the timber, if or if not there is right to

cut the timber is practised (Taxation Ruling: TR 95/6PW - Notice of Partial Withdrawal,

2010). The income has been generated from the sale can be assessable, as per the subsection

25(1) (McNeil, 2015).

Applicability of provisions and Conclusion

In accordance with the regulatory provisions covered under Taxation Ruling 95/6, sales of

timber is taxable in both the cases however provisions will differ. If Brian is engaged in

Disposal of standing timber not in the ordinary course of business than taxability will be as

per subsection 36(1) and if direct rights of procurement of timber are sold than taxability will

be as per provisions of subsection 25(1).

2 T (1951) 84 CLR 118; 9 ATD 334.

taxpayer and intended for the sale might affect the actual value of trees contained in the

assessable income of taxpayer as per the subsection 36(1), when the disposal would take

place (Frecknall-Hughes and Kirchler, 2015).

The tax will be payable irrespective of aspect that business is carried out of the forest

operations, as long as the business is carried out by the taxpayer and the disposal is not done

in the regular course of business (Burkhauser, Hahn and Wilkins, 2015). The major

requirement is that the trees represent the business assets as a whole.

If or if not the specific contract leads to trees disposal, as per distinct, from the sale of Land's

interest, will mostly depend on the analyzing of the contract (Taxation Ruling: TR 95/6PW -

Notice of Partial Withdrawal, 2010). The Subsection 36(1) will not be applicable, in case the

trees are land leased and there is no entire ownership of the lessee on the leased land for this

aspect case of Rose v. FC2 can be considered (Bond and Wright, 2017).

Disposal of rights to standing timber

A taxpayer has been carrying a business of forest operations can put standing timber into a

sale by providing the right to some individual to cut out the timber, if or if not there is right to

cut the timber is practised (Taxation Ruling: TR 95/6PW - Notice of Partial Withdrawal,

2010). The income has been generated from the sale can be assessable, as per the subsection

25(1) (McNeil, 2015).

Applicability of provisions and Conclusion

In accordance with the regulatory provisions covered under Taxation Ruling 95/6, sales of

timber is taxable in both the cases however provisions will differ. If Brian is engaged in

Disposal of standing timber not in the ordinary course of business than taxability will be as

per subsection 36(1) and if direct rights of procurement of timber are sold than taxability will

be as per provisions of subsection 25(1).

2 T (1951) 84 CLR 118; 9 ATD 334.

REFERENCES

Books and journals

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. The

Economic Review, 105(5), pp.38-42.

Yagan, D., 2015. Capital tax reform and the real economy: The effects of the 2003 dividend

tax cut. The American Economic Review, 105(12), pp.3531-3563.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Barrett, J.M. and Veal, J.A., 2016. Tax Rationality, Politics, and Media Spin: A Case Study

of the Failed ‘Car Park Tax’Proposal.

Pearce, P. and Pinto, D., 2015. An evaluation of the case for a congestion tax in

Australia. The Tax Specialist, 18(4), pp.146-153.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2017. Federal Income Taxation.

Wolters Kluwer Law & Business.

Bloom, D., 2015. Tax avoidance-a view from the dark side. Melb. UL Rev., 39, p.950.

QC, J.M., 2016. Ethics and tax compliance: the morality of tax avoidance. The good old

days. Trusts & Trustees, 22(1), p.166.

Frecknall-Hughes, J. and Kirchler, E., 2015. Towards a general theory of tax practice. Social

& Legal Studies, 24(2), pp.289-312.

Evans, S., 2015. It's' Clean Hands' Again: The Dirtiness of Not Paying Tax Considered in the

Supreme Court.

Sharma, S.K., 2015. 020_Law of Sales Tax.

McNeil, K., 2015. Indigenous Territorial Rights in the Common Law.

Bond, D. and Wright, A., 2017. A Snapshot of the Australian Taxpayer.

Books and journals

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. The

Economic Review, 105(5), pp.38-42.

Yagan, D., 2015. Capital tax reform and the real economy: The effects of the 2003 dividend

tax cut. The American Economic Review, 105(12), pp.3531-3563.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Barrett, J.M. and Veal, J.A., 2016. Tax Rationality, Politics, and Media Spin: A Case Study

of the Failed ‘Car Park Tax’Proposal.

Pearce, P. and Pinto, D., 2015. An evaluation of the case for a congestion tax in

Australia. The Tax Specialist, 18(4), pp.146-153.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2017. Federal Income Taxation.

Wolters Kluwer Law & Business.

Bloom, D., 2015. Tax avoidance-a view from the dark side. Melb. UL Rev., 39, p.950.

QC, J.M., 2016. Ethics and tax compliance: the morality of tax avoidance. The good old

days. Trusts & Trustees, 22(1), p.166.

Frecknall-Hughes, J. and Kirchler, E., 2015. Towards a general theory of tax practice. Social

& Legal Studies, 24(2), pp.289-312.

Evans, S., 2015. It's' Clean Hands' Again: The Dirtiness of Not Paying Tax Considered in the

Supreme Court.

Sharma, S.K., 2015. 020_Law of Sales Tax.

McNeil, K., 2015. Indigenous Territorial Rights in the Common Law.

Bond, D. and Wright, A., 2017. A Snapshot of the Australian Taxpayer.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Online

TR 93/32 taxation of rental property - division of net income or loss between co-owners.

1993. [Online]. Available through <https://www.ato.gov.au/law/view/document?

docid=TXR/TR9332/NAT/ATO/00001>. [Accessed on 13th September 2017].

Westminster doctrine. 2016. [Online]. Available through

<http://oxfordindex.oup.com/view/10.1093/oi/authority.20110803121911242>. [Accessed on

13th September 2017].

Taxation Ruling: TR 95/6PW - Notice of Partial Withdrawal. 2010. [Online]. Available

through <http://law.ato.gov.au/atolaw/view.htm?docid=TXR/TR956PW/NAT/ATO/00001>.

[Accessed on 13th September 2017].

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Online

TR 93/32 taxation of rental property - division of net income or loss between co-owners.

1993. [Online]. Available through <https://www.ato.gov.au/law/view/document?

docid=TXR/TR9332/NAT/ATO/00001>. [Accessed on 13th September 2017].

Westminster doctrine. 2016. [Online]. Available through

<http://oxfordindex.oup.com/view/10.1093/oi/authority.20110803121911242>. [Accessed on

13th September 2017].

Taxation Ruling: TR 95/6PW - Notice of Partial Withdrawal. 2010. [Online]. Available

through <http://law.ato.gov.au/atolaw/view.htm?docid=TXR/TR956PW/NAT/ATO/00001>.

[Accessed on 13th September 2017].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.