Financial Management Report: Newton Co Acquisition Proposal

VerifiedAdded on 2019/09/30

|6

|2392

|142

Report

AI Summary

The assignment content describes a takeover offer by Mille and Co to acquire Newton and Co. The acquisition is expected to create a synergic effect of £150,000 per year, resulting in an overall percentage gain for Newton of 8.48%. The calculation also considers the delayed production of follow-on products, which would further enhance the value of the company. Shareholders of both companies are expected to be receptive to the takeover offer, with potential concerns about identity and market recognition.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

HIGHER EDUCATION ASSESSMENT

School: Professional Studies

Awarding Body: Lancaster University Module Code: BFM502

Programme Title: FdA in Business and Financial Management Occurrence: 2016/17

Module Title: Financial Management Weighting: 50%

Assessment Title: Written report Assessment No. 1 of 2

Tutor Details Name David Robinson Telephone No. 504475

Email david.robinson@blackpool.ac.uk Room SO20

Internal Verification (IV)

For Staff Use Only

Assessment Brief IV

Must be internally verified prior to

distribution to students

IV Name: Toby Weymouth

Date: 3 October 2016

Student Submission IV

To be completed if the assessment

submission forms part of the IV sample

IV Name:

Date:

Distribution Date: 10 October 2016

Submission Time: 23.55 hrs.

Submission Date: 13 November 2016

Submission Point/Location: Upload to Moodle

Feedback Week Commencing: 28 November 2016

Student Number:

Student Name:

Assessment Record

For Staff Use Only. All assessment

grades are subject to ratification by

the College board of examiners and

the awarding body.

Grade

Awarded:

Submitted: On Time

Late ___ days (days NOT working days)

Date: Penalty:

Page 1 of 6

School: Professional Studies

Awarding Body: Lancaster University Module Code: BFM502

Programme Title: FdA in Business and Financial Management Occurrence: 2016/17

Module Title: Financial Management Weighting: 50%

Assessment Title: Written report Assessment No. 1 of 2

Tutor Details Name David Robinson Telephone No. 504475

Email david.robinson@blackpool.ac.uk Room SO20

Internal Verification (IV)

For Staff Use Only

Assessment Brief IV

Must be internally verified prior to

distribution to students

IV Name: Toby Weymouth

Date: 3 October 2016

Student Submission IV

To be completed if the assessment

submission forms part of the IV sample

IV Name:

Date:

Distribution Date: 10 October 2016

Submission Time: 23.55 hrs.

Submission Date: 13 November 2016

Submission Point/Location: Upload to Moodle

Feedback Week Commencing: 28 November 2016

Student Number:

Student Name:

Assessment Record

For Staff Use Only. All assessment

grades are subject to ratification by

the College board of examiners and

the awarding body.

Grade

Awarded:

Submitted: On Time

Late ___ days (days NOT working days)

Date: Penalty:

Page 1 of 6

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Assessment Brief

Required:

Prepare a report for the Board of Directors of Newton Co that:

(a) Identifies and discusses both short –term and long-term sources of finance available to a business involved in

the design and development of tools and parts for specialist machinery;

Any company needs loan to leverage (Bouchoud, 2001) its finances. There are mainly two types of finances. Long

term finance and short term finance. Generally long term finance is used to procure long term assets which are

income generating. For eg to purchase plant and machinery, office equipment, furniture and fixtures, office building

etc. These are spread over long period. Generally the finance provider offers a moratorium period for few negotiated

months in order to give an additional space for the company to incur initial expenditures without generating any

revenue. Second type of loan is short term in nature. They are generally meant for meeting short term liquidity or

working capital requirements. These are generally against the hypothecation of stock and book debts of the

company (LaPray J, 2002). Short term finance are generally for a tenure upto 3 years and long term are more than 3

years.

Loan repayment has a thing to do with the Liquidity of the Company. A profitable company has good profit margins

from the business. However, its cash richness or liquidity can be judged from the Short term Liquidity ratios. The fast

movement of stock and receivables provide fund to repay the suppliers / creditors or outside liabilities. The banks

provide short term working capital term loans with the sole criteria of checking the cash flow statement of the

company for the defined period of loan tenure. A good turnover with low operating costs does not imply that the

company has good realizability of money from the outstanding receivables.

If the Company wishes to go for the option II, i.e. to enter into a new venture of developing a prototype, then the

Company can leverage its finances with the help of external borrowing. In my opinion Foreign investors are cheaper

than the locally available options in the market. The Company should try to get a deal from foreign investor who is in

a country with lower interest rates than the company’s residence country.

The supplier of machinery can also extend finance to the company which is another type of credit availment. The

best way to bring in money is own borrowing which are absolutely risk free. If the promotors have cash balance in

their personal name, then they should insert more capital into the balance sheet and increase their promotor

holding and control in the decision making. They can also increase share holding by adding few of their friends who

are trustworthy and work with the same wavelength as that with the existing share holders who are promotors. By

this way, the money remains with the management and so does the control.

(b) Provides a generic outline of an acquisition proposal; and

Acquisition proposal (Goyal, 2012) is a generally an official to by a purchasing company to purchase a Selling

company. The same is done with a mutually agreed purchase consideration (Harris, K., Davies et al, 1997).

Acquisitions / mergers and demergers happen for the purpose of getting a synergy effect in the industry. It boosts

revenue or reduces operating costs as compared to the aggregate of both the company. The strengths multiply and

weaknesses get divided on the transaction of an amalgamation / acquisition / merger.

In the given situation, Mille and Co, which is the proposed buyer / investor has 10 million shares in issue. The shares

are available for a trade at £4·80 each. The company’s price to earnings (P/E) ratio is 15. More over, It has sufficient

cash to pay for Newton’s (the selling company) equity and a substantial proportion of its debt, believing that this will

enable Newton to operate on a P/E level of 15 as well. In addition to this, Mille believes that it can find cost-based

Page 2 of 6

Required:

Prepare a report for the Board of Directors of Newton Co that:

(a) Identifies and discusses both short –term and long-term sources of finance available to a business involved in

the design and development of tools and parts for specialist machinery;

Any company needs loan to leverage (Bouchoud, 2001) its finances. There are mainly two types of finances. Long

term finance and short term finance. Generally long term finance is used to procure long term assets which are

income generating. For eg to purchase plant and machinery, office equipment, furniture and fixtures, office building

etc. These are spread over long period. Generally the finance provider offers a moratorium period for few negotiated

months in order to give an additional space for the company to incur initial expenditures without generating any

revenue. Second type of loan is short term in nature. They are generally meant for meeting short term liquidity or

working capital requirements. These are generally against the hypothecation of stock and book debts of the

company (LaPray J, 2002). Short term finance are generally for a tenure upto 3 years and long term are more than 3

years.

Loan repayment has a thing to do with the Liquidity of the Company. A profitable company has good profit margins

from the business. However, its cash richness or liquidity can be judged from the Short term Liquidity ratios. The fast

movement of stock and receivables provide fund to repay the suppliers / creditors or outside liabilities. The banks

provide short term working capital term loans with the sole criteria of checking the cash flow statement of the

company for the defined period of loan tenure. A good turnover with low operating costs does not imply that the

company has good realizability of money from the outstanding receivables.

If the Company wishes to go for the option II, i.e. to enter into a new venture of developing a prototype, then the

Company can leverage its finances with the help of external borrowing. In my opinion Foreign investors are cheaper

than the locally available options in the market. The Company should try to get a deal from foreign investor who is in

a country with lower interest rates than the company’s residence country.

The supplier of machinery can also extend finance to the company which is another type of credit availment. The

best way to bring in money is own borrowing which are absolutely risk free. If the promotors have cash balance in

their personal name, then they should insert more capital into the balance sheet and increase their promotor

holding and control in the decision making. They can also increase share holding by adding few of their friends who

are trustworthy and work with the same wavelength as that with the existing share holders who are promotors. By

this way, the money remains with the management and so does the control.

(b) Provides a generic outline of an acquisition proposal; and

Acquisition proposal (Goyal, 2012) is a generally an official to by a purchasing company to purchase a Selling

company. The same is done with a mutually agreed purchase consideration (Harris, K., Davies et al, 1997).

Acquisitions / mergers and demergers happen for the purpose of getting a synergy effect in the industry. It boosts

revenue or reduces operating costs as compared to the aggregate of both the company. The strengths multiply and

weaknesses get divided on the transaction of an amalgamation / acquisition / merger.

In the given situation, Mille and Co, which is the proposed buyer / investor has 10 million shares in issue. The shares

are available for a trade at £4·80 each. The company’s price to earnings (P/E) ratio is 15. More over, It has sufficient

cash to pay for Newton’s (the selling company) equity and a substantial proportion of its debt, believing that this will

enable Newton to operate on a P/E level of 15 as well. In addition to this, Mille believes that it can find cost-based

Page 2 of 6

synergies of £150,000 after tax per year for the foreseeable future. Mille’s current profit after tax is £ 3,200,000.

In the given case, if Miles and Co purchases the shares of the Newton and Co, it will be amalgamation in the nature

of absorption. Where the selling company gets absorbed in the main holding company – purchasing company. The

company newton and Co must take a wise decision if it wants to amalgamate in this manner as there are chances of

loosing its own identity in the market.

(c) Considers and evaluates the proposals facing Newton Co, particularly providing: (12 marks)

(i) Estimates of the current value of a Newton share, using the free cash flow to firm methodology;

Calculation of Discounted Cash flow of Newton and Co

Yea

r

Profit After

Tax

Depreciatio

n

Cash

PAT

Annual

Workin

g

Capital

Net

Income

Discount

Factor

@ 11%

Present

Value

0 620 1206 1826 1010 816 1.000 816

1 2283 1010 1273 0.909 1157

2 2853 1010 1843 0.826 1523

3 3566 1010 2556 0.751 1921

4 4458 1010 3448 0.683 2355

5 5573 1010 4563 0.621 2833

Net Present Value 10605

Cash Profit after tax is derived by adding 25% Growth factor. Net income is derived by deducting annual working

capital investment from the Cash Profit after tax. Discounting Factor of 11% is the expected rate of return. The

present value is a multiplication of Discounting factor x net income. According to the above calculation, the net

present value is 10605000/- with a horizon period of 5 years.

We have assumed to project life of 5 years as horizon period.

(ii) Estimates of the percentage gain in value to a Newton Co share and a Mille and Co share under each

payment offer

As per the given problem sum, Newton’s earnings before interest and tax in its first year of operation without the

amalgamation was £970,000. The same has been growing steadily in three years, to their current level. As further

explained, the cash flows grew at the same rate as well. However, the Company projects annual growth to reduce to

25% of the original rate for the foreseeable future. Newton currently has a cost of debt of 7% per year on its loans,

which is 3.8% higher than the government base rate, and corporation tax of 20% on profits after interest. Newton

and Co estimates that an overall cost of capital of 11% is reasonable compensation for the risk undertaken on an

investment of this nature. In arriving at the profit after tax figure, Newton deducted tax allowable depreciation and

other non-cash expenses totalling £1,206,000.

Mille and Co has 10 million shares in issue and these are trading for £4·80 each. Mille and Co’s price to earnings

(P/E) ratio is 15. It has sufficient cash to pay for Newton’s equity and a substantial proportion of its debt, believing

that this will enable Newton to operate on a P/E level of 15 as well. Mille’s current profit after tax is £3,200,000.

The problem is silent on the terms of payment and purchase consideration and its corresponding effect on Goodwill

or Capital Reserve. However the problem mentions that the merger might create a synergic effect of £ 150,000 after

tax every year. Percentage gain for Newton would be 8.48% (150 x 6) / 10605 = 8.48% over Net present Value of the

Page 3 of 6

In the given case, if Miles and Co purchases the shares of the Newton and Co, it will be amalgamation in the nature

of absorption. Where the selling company gets absorbed in the main holding company – purchasing company. The

company newton and Co must take a wise decision if it wants to amalgamate in this manner as there are chances of

loosing its own identity in the market.

(c) Considers and evaluates the proposals facing Newton Co, particularly providing: (12 marks)

(i) Estimates of the current value of a Newton share, using the free cash flow to firm methodology;

Calculation of Discounted Cash flow of Newton and Co

Yea

r

Profit After

Tax

Depreciatio

n

Cash

PAT

Annual

Workin

g

Capital

Net

Income

Discount

Factor

@ 11%

Present

Value

0 620 1206 1826 1010 816 1.000 816

1 2283 1010 1273 0.909 1157

2 2853 1010 1843 0.826 1523

3 3566 1010 2556 0.751 1921

4 4458 1010 3448 0.683 2355

5 5573 1010 4563 0.621 2833

Net Present Value 10605

Cash Profit after tax is derived by adding 25% Growth factor. Net income is derived by deducting annual working

capital investment from the Cash Profit after tax. Discounting Factor of 11% is the expected rate of return. The

present value is a multiplication of Discounting factor x net income. According to the above calculation, the net

present value is 10605000/- with a horizon period of 5 years.

We have assumed to project life of 5 years as horizon period.

(ii) Estimates of the percentage gain in value to a Newton Co share and a Mille and Co share under each

payment offer

As per the given problem sum, Newton’s earnings before interest and tax in its first year of operation without the

amalgamation was £970,000. The same has been growing steadily in three years, to their current level. As further

explained, the cash flows grew at the same rate as well. However, the Company projects annual growth to reduce to

25% of the original rate for the foreseeable future. Newton currently has a cost of debt of 7% per year on its loans,

which is 3.8% higher than the government base rate, and corporation tax of 20% on profits after interest. Newton

and Co estimates that an overall cost of capital of 11% is reasonable compensation for the risk undertaken on an

investment of this nature. In arriving at the profit after tax figure, Newton deducted tax allowable depreciation and

other non-cash expenses totalling £1,206,000.

Mille and Co has 10 million shares in issue and these are trading for £4·80 each. Mille and Co’s price to earnings

(P/E) ratio is 15. It has sufficient cash to pay for Newton’s equity and a substantial proportion of its debt, believing

that this will enable Newton to operate on a P/E level of 15 as well. Mille’s current profit after tax is £3,200,000.

The problem is silent on the terms of payment and purchase consideration and its corresponding effect on Goodwill

or Capital Reserve. However the problem mentions that the merger might create a synergic effect of £ 150,000 after

tax every year. Percentage gain for Newton would be 8.48% (150 x 6) / 10605 = 8.48% over Net present Value of the

Page 3 of 6

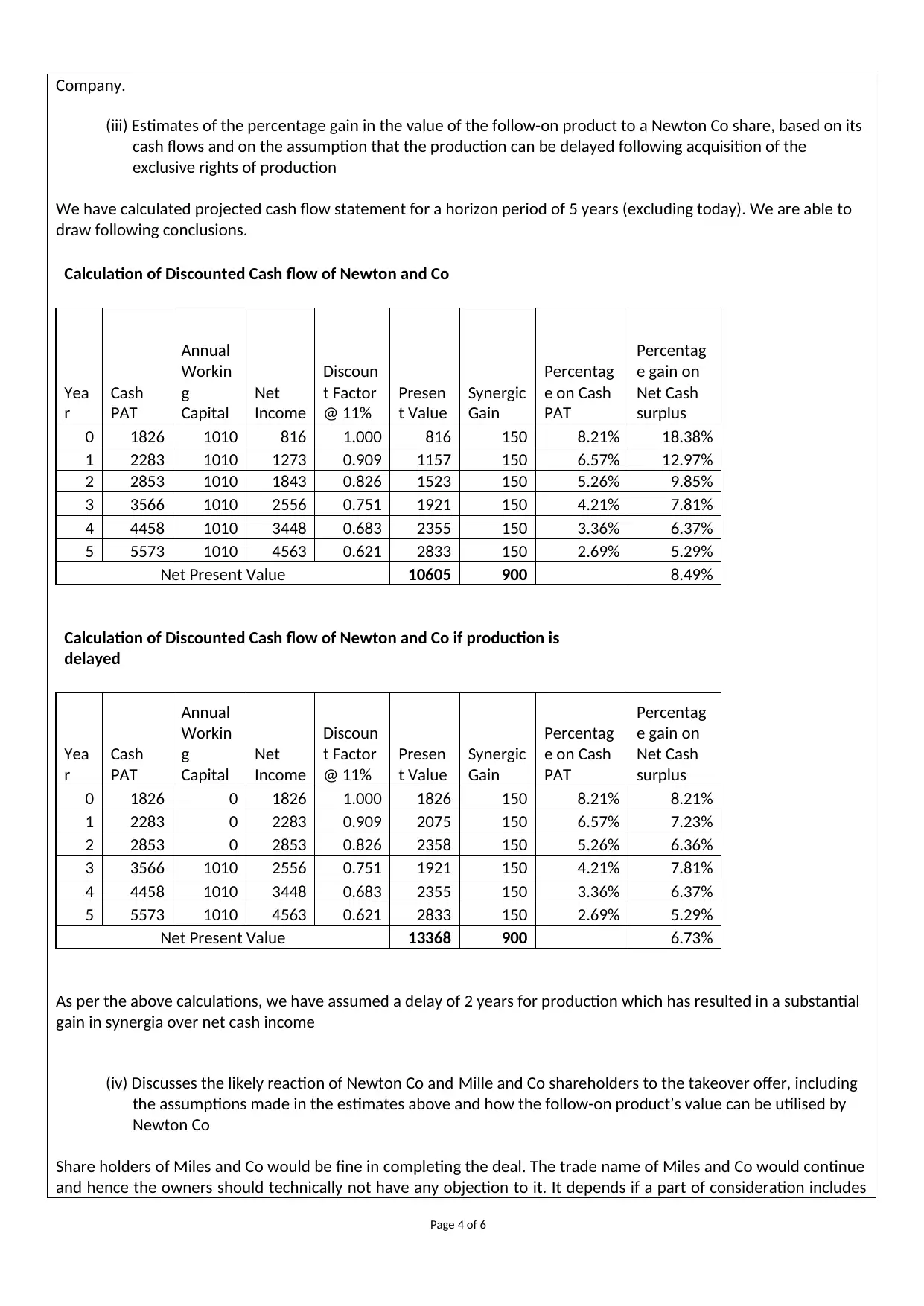

Company.

(iii) Estimates of the percentage gain in the value of the follow-on product to a Newton Co share, based on its

cash flows and on the assumption that the production can be delayed following acquisition of the

exclusive rights of production

We have calculated projected cash flow statement for a horizon period of 5 years (excluding today). We are able to

draw following conclusions.

Calculation of Discounted Cash flow of Newton and Co

Yea

r

Cash

PAT

Annual

Workin

g

Capital

Net

Income

Discoun

t Factor

@ 11%

Presen

t Value

Synergic

Gain

Percentag

e on Cash

PAT

Percentag

e gain on

Net Cash

surplus

0 1826 1010 816 1.000 816 150 8.21% 18.38%

1 2283 1010 1273 0.909 1157 150 6.57% 12.97%

2 2853 1010 1843 0.826 1523 150 5.26% 9.85%

3 3566 1010 2556 0.751 1921 150 4.21% 7.81%

4 4458 1010 3448 0.683 2355 150 3.36% 6.37%

5 5573 1010 4563 0.621 2833 150 2.69% 5.29%

Net Present Value 10605 900 8.49%

Calculation of Discounted Cash flow of Newton and Co if production is

delayed

Yea

r

Cash

PAT

Annual

Workin

g

Capital

Net

Income

Discoun

t Factor

@ 11%

Presen

t Value

Synergic

Gain

Percentag

e on Cash

PAT

Percentag

e gain on

Net Cash

surplus

0 1826 0 1826 1.000 1826 150 8.21% 8.21%

1 2283 0 2283 0.909 2075 150 6.57% 7.23%

2 2853 0 2853 0.826 2358 150 5.26% 6.36%

3 3566 1010 2556 0.751 1921 150 4.21% 7.81%

4 4458 1010 3448 0.683 2355 150 3.36% 6.37%

5 5573 1010 4563 0.621 2833 150 2.69% 5.29%

Net Present Value 13368 900 6.73%

As per the above calculations, we have assumed a delay of 2 years for production which has resulted in a substantial

gain in synergia over net cash income

(iv) Discusses the likely reaction of Newton Co and Mille and Co shareholders to the takeover offer, including

the assumptions made in the estimates above and how the follow-on product’s value can be utilised by

Newton Co

Share holders of Miles and Co would be fine in completing the deal. The trade name of Miles and Co would continue

and hence the owners should technically not have any objection to it. It depends if a part of consideration includes

Page 4 of 6

(iii) Estimates of the percentage gain in the value of the follow-on product to a Newton Co share, based on its

cash flows and on the assumption that the production can be delayed following acquisition of the

exclusive rights of production

We have calculated projected cash flow statement for a horizon period of 5 years (excluding today). We are able to

draw following conclusions.

Calculation of Discounted Cash flow of Newton and Co

Yea

r

Cash

PAT

Annual

Workin

g

Capital

Net

Income

Discoun

t Factor

@ 11%

Presen

t Value

Synergic

Gain

Percentag

e on Cash

PAT

Percentag

e gain on

Net Cash

surplus

0 1826 1010 816 1.000 816 150 8.21% 18.38%

1 2283 1010 1273 0.909 1157 150 6.57% 12.97%

2 2853 1010 1843 0.826 1523 150 5.26% 9.85%

3 3566 1010 2556 0.751 1921 150 4.21% 7.81%

4 4458 1010 3448 0.683 2355 150 3.36% 6.37%

5 5573 1010 4563 0.621 2833 150 2.69% 5.29%

Net Present Value 10605 900 8.49%

Calculation of Discounted Cash flow of Newton and Co if production is

delayed

Yea

r

Cash

PAT

Annual

Workin

g

Capital

Net

Income

Discoun

t Factor

@ 11%

Presen

t Value

Synergic

Gain

Percentag

e on Cash

PAT

Percentag

e gain on

Net Cash

surplus

0 1826 0 1826 1.000 1826 150 8.21% 8.21%

1 2283 0 2283 0.909 2075 150 6.57% 7.23%

2 2853 0 2853 0.826 2358 150 5.26% 6.36%

3 3566 1010 2556 0.751 1921 150 4.21% 7.81%

4 4458 1010 3448 0.683 2355 150 3.36% 6.37%

5 5573 1010 4563 0.621 2833 150 2.69% 5.29%

Net Present Value 13368 900 6.73%

As per the above calculations, we have assumed a delay of 2 years for production which has resulted in a substantial

gain in synergia over net cash income

(iv) Discusses the likely reaction of Newton Co and Mille and Co shareholders to the takeover offer, including

the assumptions made in the estimates above and how the follow-on product’s value can be utilised by

Newton Co

Share holders of Miles and Co would be fine in completing the deal. The trade name of Miles and Co would continue

and hence the owners should technically not have any objection to it. It depends if a part of consideration includes

Page 4 of 6

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

change of name then the shareholders need to discuss it amongst themselves whether to go for it or not.

More over with the Cost-synergic benefit, the company expects to do really well in future. With the projections of

cash flow and income statement, the Miles and Co can be comfortable in taking up the amalgamation purchase

option.

If Miles and Co purchases the shares of the Newton and Co, it will be amalgamation in the nature of absorption.

Where the selling company gets absorbed in the main holding company – purchasing company. The company

newton and Co must take a wise decision if it wants to amalgamate in this manner as there are chances of loosing its

own identity in the market. If the promotors think they do not want to develop the prototype, and considering the

fact that they are also outside debt driven and accountable to the remaining share holders, then they must forego

the idea of identity and must readily unite to sell the business to Miles and Co.

If the Company wishes to go for the option II, i.e. to enter into a new venture of developing a prototype, then the

Company can leverage its finances with the help of external borrowing. In my opinion Foreign investors are cheaper

than the locally available options in the market. The Company should try to get a deal from foreign investor who is in

a country with lower interest rates than the company’s residence country.

Student Assessment Submission

References:

Bouchaud, J. P., Matacz, A., & Potters, M. (2001). Leverage effect in financial markets: The retarded volatility

model. Physical review letters,87(22), 228701.

LaPray, J. (2002). Hypothecation Impairment as a Component of a Discount for Lack of Marketability. Business

Valuation Review, 21(3), 142-144.

Goyal, V. K., & GOYAL, R. (2012). Corporate Accounting. PHI Learning Pvt. Ltd..

Harris, K., Davies, B. J., & Baron, S. (1997). Conversations during purchase consideration: sales assistants and

customers. The International Review of Retail, Distribution and Consumer Research, 7(3), 173-190.

Page 5 of 6

More over with the Cost-synergic benefit, the company expects to do really well in future. With the projections of

cash flow and income statement, the Miles and Co can be comfortable in taking up the amalgamation purchase

option.

If Miles and Co purchases the shares of the Newton and Co, it will be amalgamation in the nature of absorption.

Where the selling company gets absorbed in the main holding company – purchasing company. The company

newton and Co must take a wise decision if it wants to amalgamate in this manner as there are chances of loosing its

own identity in the market. If the promotors think they do not want to develop the prototype, and considering the

fact that they are also outside debt driven and accountable to the remaining share holders, then they must forego

the idea of identity and must readily unite to sell the business to Miles and Co.

If the Company wishes to go for the option II, i.e. to enter into a new venture of developing a prototype, then the

Company can leverage its finances with the help of external borrowing. In my opinion Foreign investors are cheaper

than the locally available options in the market. The Company should try to get a deal from foreign investor who is in

a country with lower interest rates than the company’s residence country.

Student Assessment Submission

References:

Bouchaud, J. P., Matacz, A., & Potters, M. (2001). Leverage effect in financial markets: The retarded volatility

model. Physical review letters,87(22), 228701.

LaPray, J. (2002). Hypothecation Impairment as a Component of a Discount for Lack of Marketability. Business

Valuation Review, 21(3), 142-144.

Goyal, V. K., & GOYAL, R. (2012). Corporate Accounting. PHI Learning Pvt. Ltd..

Harris, K., Davies, B. J., & Baron, S. (1997). Conversations during purchase consideration: sales assistants and

customers. The International Review of Retail, Distribution and Consumer Research, 7(3), 173-190.

Page 5 of 6

Assessment Feedback

Outcom

e

Feedback

1

2

3

Overall Feedback

Areas for Future Development

Page 6 of 6

Outcom

e

Feedback

1

2

3

Overall Feedback

Areas for Future Development

Page 6 of 6

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.