Exploring HSBC Bank's Business Environment in New Zealand: A Report

VerifiedAdded on 2024/06/28

|16

|3587

|454

Report

AI Summary

This report provides an analysis of the business environment for HSBC Bank in New Zealand, utilizing PESTLE analysis and Porter's Five Forces to assess the opportunities and challenges. It begins with an introduction to HSBC and its global operations, followed by a detailed examination of New Zealand's business environment, including political, economic, social, technological, environmental, and legal factors. The report further analyzes the competitive landscape using Porter's Five Forces, evaluating the threat of new entrants, the power of customers and suppliers, and the threat of substitutes. It identifies business opportunities for HSBC in New Zealand, considering factors such as the country's economic stability, technological advancements, and the existing banking structure dominated by Australian-owned banks. The analysis aims to provide insights for HSBC to develop strategies for establishing and growing its presence in the New Zealand market.

BUSINESS ENVIRONMENT AND

ORGANIZATION

ORGANIZATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

The business environment is the combination of all internal as well as external factors that affect

the performance of the business. It includes factors such as clients, customers, suppliers,

government agencies, culture, law compliance etc. which can contribute towards the growth of the

organization. This report helps in recognizing the role of the business environment within the

context of HSBC Bank. It is one of the largest banks of Europe, which provides various banking and

financial services. This report also discusses factors that need to consider while developing a new

branch of HSBC. It also shows the analysis of the business environment through PESTLE analysis and

Porter's five forces. Along with that, it discusses business opportunities for the attaining the goal of

the organization.

The business environment is the combination of all internal as well as external factors that affect

the performance of the business. It includes factors such as clients, customers, suppliers,

government agencies, culture, law compliance etc. which can contribute towards the growth of the

organization. This report helps in recognizing the role of the business environment within the

context of HSBC Bank. It is one of the largest banks of Europe, which provides various banking and

financial services. This report also discusses factors that need to consider while developing a new

branch of HSBC. It also shows the analysis of the business environment through PESTLE analysis and

Porter's five forces. Along with that, it discusses business opportunities for the attaining the goal of

the organization.

BACKGROUND

HSBC is one of the world’s leading banking and financial services organizations (Trudeau, et al.

2017). It covers 67 countries and zones across America, Asia, Africa, Europe etc. Along with that, it

has 38 million customers around the world. The revenue of HSBC was $51.445 billion in 2017 with

the asset of $2.521 billion. It is world’s seventh-largest bank by total assets and largest in Europe by

$2.374 trillion (Islam, 2018). It deals with personal banking, business banking, mortgage, wealth and

retail management, loan, credit cards and many more financial services. HSBC operations are taking

place in every financial market of the country as it is the largest bank in Hong Kong and print its

local currency as well (Huang, 2015). It ranked first by Western Europe and stands on the fourth-

largest bank by assets and measured as one of the trusted banks in India according to The Brand

trust report, 2015 The structure of the organization is divided into four business groups as global

banking, investment banking, retail and wealth management and private banking.

HSBC is one of the world’s leading banking and financial services organizations (Trudeau, et al.

2017). It covers 67 countries and zones across America, Asia, Africa, Europe etc. Along with that, it

has 38 million customers around the world. The revenue of HSBC was $51.445 billion in 2017 with

the asset of $2.521 billion. It is world’s seventh-largest bank by total assets and largest in Europe by

$2.374 trillion (Islam, 2018). It deals with personal banking, business banking, mortgage, wealth and

retail management, loan, credit cards and many more financial services. HSBC operations are taking

place in every financial market of the country as it is the largest bank in Hong Kong and print its

local currency as well (Huang, 2015). It ranked first by Western Europe and stands on the fourth-

largest bank by assets and measured as one of the trusted banks in India according to The Brand

trust report, 2015 The structure of the organization is divided into four business groups as global

banking, investment banking, retail and wealth management and private banking.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BACKGROUND INFORMATION ON BUSINESS ENVIRONMENT IN NEW ZEALAND

The business environment is the summarise format of all the factors which directly or indirectly

influence the operational activity or organization. The traits are known as customers, competitors,

suppliers and social, cultural, political, legal and technological factors, which are considered as the

factors of the business environment (Terceno, et al. 2017). The business environment helps in

analysing the strengths and weaknesses of the organization and gives direction for the growth of

the business. It is difficult to predict the changes in a business environment when the organization

set their operation in the new country. The business environment varies from place to place as the

environment of New Zealand is different from other countries.

New Zealand is a small country but it has done notable progress in the recent past and brings

various changes in the country to raise the economy positively towards the growth of the economy.

The report shows the detail examination of New Zealand through PESTLE analysis with respect to

opening a new branch by HSBC banking industry (Zalengera, et al. 2014). The PESTLE analysis helps

the bank to recognize the business environment of New Zealand. HSBC can form their strategies of

opening the new branch in New Zealand, through evaluating these factors which can influence the

performance of the industry. The PESTLE analysis consists of the following factors as follows:

Figure 1: PESTLE Analysis

[Source: Lee, 2016]

The business environment is the summarise format of all the factors which directly or indirectly

influence the operational activity or organization. The traits are known as customers, competitors,

suppliers and social, cultural, political, legal and technological factors, which are considered as the

factors of the business environment (Terceno, et al. 2017). The business environment helps in

analysing the strengths and weaknesses of the organization and gives direction for the growth of

the business. It is difficult to predict the changes in a business environment when the organization

set their operation in the new country. The business environment varies from place to place as the

environment of New Zealand is different from other countries.

New Zealand is a small country but it has done notable progress in the recent past and brings

various changes in the country to raise the economy positively towards the growth of the economy.

The report shows the detail examination of New Zealand through PESTLE analysis with respect to

opening a new branch by HSBC banking industry (Zalengera, et al. 2014). The PESTLE analysis helps

the bank to recognize the business environment of New Zealand. HSBC can form their strategies of

opening the new branch in New Zealand, through evaluating these factors which can influence the

performance of the industry. The PESTLE analysis consists of the following factors as follows:

Figure 1: PESTLE Analysis

[Source: Lee, 2016]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Political Factors:

While starting the new branch by HSBC, they need to make sure about the economic stability,

political features and law and compliance of the country. New Zealand has established a

government which has certain rules on banking sector but it gives trade freedom to industry as

well, this can help the new branch of HSBC for expanding their operations globally (Kelsey, 2015).

The labour laws are strict in New Zealand and labour-force is expensive so, for that company can

relocate the employees to New Zealand. It also has the high range of tax policies because the

lending rates of the country are high.

Economical Factor:

New Zealand is the mixed economy, which has the GDP with the growth of 2.8% in 2017 that was

equivalent to 300 per cent of the world's average. The resources for the banking sectors are also

available as it has approx. 7 million populations (Kelsey, 2015). The inflation rate is also low so the

banking sector can develop their investment banking and due to the large population, the services

as mortgage, loan, corporate banking and insurance can also rise in the country. The

unemployment rate is also low so the people can easily invest in the banking sector. The economic

factors are the positive sign of the country which can be helpful in the growth of the newly set-up

banking industry.

Social Factors:

Figure 2: Issues faced by New Zealand

[Source: Andrew, 2014]

While starting the new branch by HSBC, they need to make sure about the economic stability,

political features and law and compliance of the country. New Zealand has established a

government which has certain rules on banking sector but it gives trade freedom to industry as

well, this can help the new branch of HSBC for expanding their operations globally (Kelsey, 2015).

The labour laws are strict in New Zealand and labour-force is expensive so, for that company can

relocate the employees to New Zealand. It also has the high range of tax policies because the

lending rates of the country are high.

Economical Factor:

New Zealand is the mixed economy, which has the GDP with the growth of 2.8% in 2017 that was

equivalent to 300 per cent of the world's average. The resources for the banking sectors are also

available as it has approx. 7 million populations (Kelsey, 2015). The inflation rate is also low so the

banking sector can develop their investment banking and due to the large population, the services

as mortgage, loan, corporate banking and insurance can also rise in the country. The

unemployment rate is also low so the people can easily invest in the banking sector. The economic

factors are the positive sign of the country which can be helpful in the growth of the newly set-up

banking industry.

Social Factors:

Figure 2: Issues faced by New Zealand

[Source: Andrew, 2014]

Social factors of the country consist of changes in government policies, demographic features,

customs and trends of population etc. The political system of New Zealand is strong enough to

enhance the growth of the banking system and it also welcomes the foreign direct investment in

the country (Schyns, et al. 2016). The foreign investors get influenced by stability in government

within the country. The literacy rate is high and life expectancy of people is also about 80 years,

which can be a beneficial aspect for banking sectors in the country. The population is divided into

different cities with less unemployment ratio which influence the culture of the country. So, people

can come up at large scale to take advice from banks related to business, home, and academics etc.

Technological Factors:

New Zealand uses the most updated technology in education which is considered as the best

education system around the world and increases the literacy rate of the country. It also uses the IT

technology and internet in urban as well as rural area (Montazemi, 2015). Therefore the banking

industry can also use mobile application for regulating the banking transactions in the country as

the high technology is excess in the country it can be helpful for banking sector for implementing

the transaction among the people of the country.

Environmental Factors:

The country has the unique quality of the ecological system and the population are also aware of

the changing environment. This factor can be helpful for banking sector for providing online private

banking, loan or mortgage to individuals. New Zealand uses the latest technology to deal with the

pollution. The banking sector of the country used mobile apps and online transaction which

decreases the use of paper. Thus technological enhancement in the economy can be helpful in

establishing a new branch as it reduces the time and cost of the industry.

Legal Factors:

The government of the country changes and it reduces the crime rate from the country. The new

businesses are establishing their operation as there is larger scope for developing their business at

New Zealand but the profit margin is less because the government of the country charges high

lending amount from the businesses (Cruz, 2017). New Zealand offered business and trade freedom

to the organization which can be the positive aspect for newly set-up business and the legal

customs and trends of population etc. The political system of New Zealand is strong enough to

enhance the growth of the banking system and it also welcomes the foreign direct investment in

the country (Schyns, et al. 2016). The foreign investors get influenced by stability in government

within the country. The literacy rate is high and life expectancy of people is also about 80 years,

which can be a beneficial aspect for banking sectors in the country. The population is divided into

different cities with less unemployment ratio which influence the culture of the country. So, people

can come up at large scale to take advice from banks related to business, home, and academics etc.

Technological Factors:

New Zealand uses the most updated technology in education which is considered as the best

education system around the world and increases the literacy rate of the country. It also uses the IT

technology and internet in urban as well as rural area (Montazemi, 2015). Therefore the banking

industry can also use mobile application for regulating the banking transactions in the country as

the high technology is excess in the country it can be helpful for banking sector for implementing

the transaction among the people of the country.

Environmental Factors:

The country has the unique quality of the ecological system and the population are also aware of

the changing environment. This factor can be helpful for banking sector for providing online private

banking, loan or mortgage to individuals. New Zealand uses the latest technology to deal with the

pollution. The banking sector of the country used mobile apps and online transaction which

decreases the use of paper. Thus technological enhancement in the economy can be helpful in

establishing a new branch as it reduces the time and cost of the industry.

Legal Factors:

The government of the country changes and it reduces the crime rate from the country. The new

businesses are establishing their operation as there is larger scope for developing their business at

New Zealand but the profit margin is less because the government of the country charges high

lending amount from the businesses (Cruz, 2017). New Zealand offered business and trade freedom

to the organization which can be the positive aspect for newly set-up business and the legal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

implications for the international business community is very negligent that can be helpful for the

banking industry to follow their own laws and trade structure.

The financial system of New Zealand also influences the performance of the newly set-up banking

sector (Naheem, 2015). New Zealand banking system is highly reserve as the country owned banks

account with only 8%. The financial system is dominated by the Australian owned banks and there

is funding from offshore with a maturity period of less than a year (Murray, et al. 2014). Majority

funding is for short-term and 20 per cent of mortgages are not fixed. The retail rates also become

high due to the high cost of fund therefore newly set up banking can develop their business while

developing these factors which are faced by New Zealand and affects the economy.

banking industry to follow their own laws and trade structure.

The financial system of New Zealand also influences the performance of the newly set-up banking

sector (Naheem, 2015). New Zealand banking system is highly reserve as the country owned banks

account with only 8%. The financial system is dominated by the Australian owned banks and there

is funding from offshore with a maturity period of less than a year (Murray, et al. 2014). Majority

funding is for short-term and 20 per cent of mortgages are not fixed. The retail rates also become

high due to the high cost of fund therefore newly set up banking can develop their business while

developing these factors which are faced by New Zealand and affects the economy.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

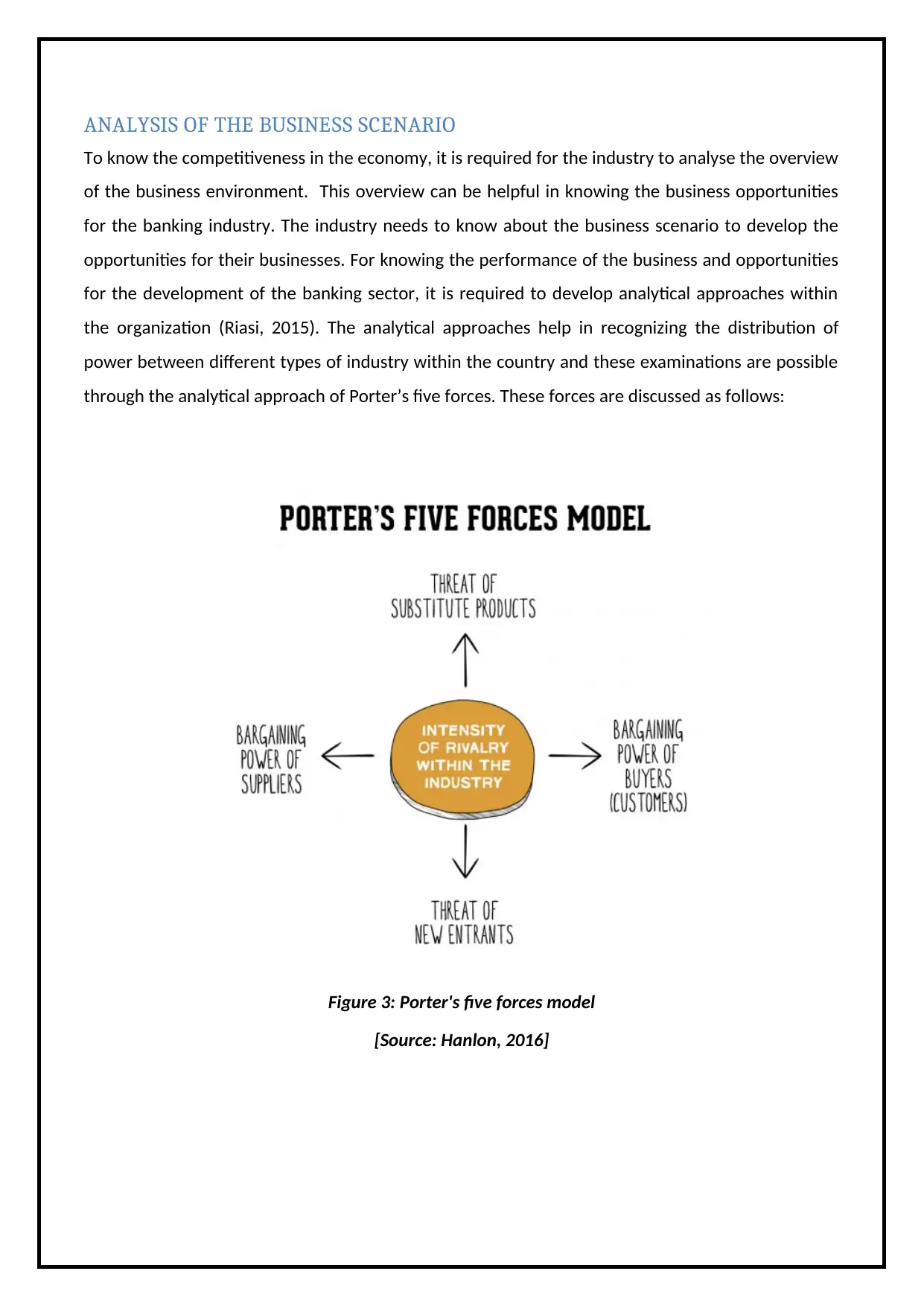

ANALYSIS OF THE BUSINESS SCENARIO

To know the competitiveness in the economy, it is required for the industry to analyse the overview

of the business environment. This overview can be helpful in knowing the business opportunities

for the banking industry. The industry needs to know about the business scenario to develop the

opportunities for their businesses. For knowing the performance of the business and opportunities

for the development of the banking sector, it is required to develop analytical approaches within

the organization (Riasi, 2015). The analytical approaches help in recognizing the distribution of

power between different types of industry within the country and these examinations are possible

through the analytical approach of Porter’s five forces. These forces are discussed as follows:

Figure 3: Porter's five forces model

[Source: Hanlon, 2016]

To know the competitiveness in the economy, it is required for the industry to analyse the overview

of the business environment. This overview can be helpful in knowing the business opportunities

for the banking industry. The industry needs to know about the business scenario to develop the

opportunities for their businesses. For knowing the performance of the business and opportunities

for the development of the banking sector, it is required to develop analytical approaches within

the organization (Riasi, 2015). The analytical approaches help in recognizing the distribution of

power between different types of industry within the country and these examinations are possible

through the analytical approach of Porter’s five forces. These forces are discussed as follows:

Figure 3: Porter's five forces model

[Source: Hanlon, 2016]

The threat of new entry:

This factors consist of entrance of new industry within the market as a new branch is opened by

HSBC in New Zealand and development of a new branch can face threat of new entry as issues by

Australian-owned banks as the majority of funding is performed by them and it can create a barrier

for banking industry but due to risk of high-interest rate and short-term funding the opportunity for

entering the new banking sectors are increases. If the newly set-up bank overcome with these

factors of New Zealand then it can cause the benefit to the industry as well as reduces threaten of

new entry within the country (Pan, et al. 2017). Therefore opportunities for newly set-up branch of

HSBC is to bring unique banking and financial services as loans, mortgage, credit, and interest rate

for the individuals, corporate and business sectors of the economy of New Zealand.

Power of customers:

It includes the power of the customers to influence the performance of the organization in the

economy. As the population is spread among different cities of New Zealand, therefore, the

numbers of customers are not huge for the banking sector and they could not influence the pricing

strategies of the industry (Alley, 2017). The literacy rate of customers is high which can influence

the performance of the industry within the economy but there are only New Zealand and

Australian-owned banking system due to which customers don’t have enough choice and they need

to follow the norms of the newly set-up banking sector. Thus, the business opportunity for the

banking sector is to influence the customers towards their services by offering them attractive and

effective financial services. Therefore the power of customers in New Zealand is not very high for

banking sectors.

Threats of substitutes:

When there are the availability of alternatives in the context of the organization then there is

threatening of substitute because customers can shift to another alternative or substitute if they

are not satisfied with the services of any industry they can switch their preferences. The power of

substitution is not very high in the banking sector of New Zealand as the customers don't have a

large number of alternatives available in the market. The country is facing obstacles in the field of

banking and financial services. Therefore, business opportunities for the new banking sector is to

come up with financial services and also overcome the barriers faced by banking sector of the

This factors consist of entrance of new industry within the market as a new branch is opened by

HSBC in New Zealand and development of a new branch can face threat of new entry as issues by

Australian-owned banks as the majority of funding is performed by them and it can create a barrier

for banking industry but due to risk of high-interest rate and short-term funding the opportunity for

entering the new banking sectors are increases. If the newly set-up bank overcome with these

factors of New Zealand then it can cause the benefit to the industry as well as reduces threaten of

new entry within the country (Pan, et al. 2017). Therefore opportunities for newly set-up branch of

HSBC is to bring unique banking and financial services as loans, mortgage, credit, and interest rate

for the individuals, corporate and business sectors of the economy of New Zealand.

Power of customers:

It includes the power of the customers to influence the performance of the organization in the

economy. As the population is spread among different cities of New Zealand, therefore, the

numbers of customers are not huge for the banking sector and they could not influence the pricing

strategies of the industry (Alley, 2017). The literacy rate of customers is high which can influence

the performance of the industry within the economy but there are only New Zealand and

Australian-owned banking system due to which customers don’t have enough choice and they need

to follow the norms of the newly set-up banking sector. Thus, the business opportunity for the

banking sector is to influence the customers towards their services by offering them attractive and

effective financial services. Therefore the power of customers in New Zealand is not very high for

banking sectors.

Threats of substitutes:

When there are the availability of alternatives in the context of the organization then there is

threatening of substitute because customers can shift to another alternative or substitute if they

are not satisfied with the services of any industry they can switch their preferences. The power of

substitution is not very high in the banking sector of New Zealand as the customers don't have a

large number of alternatives available in the market. The country is facing obstacles in the field of

banking and financial services. Therefore, business opportunities for the new banking sector is to

come up with financial services and also overcome the barriers faced by banking sector of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

country. Through which they don’t need to face threaten of substitute and can also enhance the

profitability in their industry. Thus threats for substitute are not influenced much by the banking

industry in the economy of New Zealand.

Supplier power:

The suppliers are the person who offered the services in the economy. If there is a large number of

suppliers in the market they can influence customers easily and affect the performance of the

newly set-up businesses (Avlonitis, et al 2015). The existing supplier of the banking industry in New

Zealand is Australian-owned banks which influence the majority amount of banking system and

control over the retail and interest rates of banking. There are not so many suppliers in the banking

sector but the Australian owned-banks hold the power in the country. It is quite difficult to sustain

in the banking industry of New Zealand because the suppliers in this sector are powerful but the

new banking system has the opportunity to decrease the supplier power by offering the people a

variety of financial services and alternatives, as this can overcome from the issue of supplier power

in the economy of New Zealand.

Competitive rivalry:

Competitive rivalry means the competitive environment in the economy. The more competitiveness

in the economy can cause instability for a new entrance. It shows the competitiveness in the sector

as the number of competitors in the sector influences the capability to threaten an organization. In

New Zealand, the number of competitors is not huge as there is only Australian owned banking

system but they are the well establish a system of New Zealand and it becomes difficult for newly

set-up banking industry to achieve competitive edge (Kanatani, 2017). The industry can get over

from the issue of competitiveness while developing financial services as long-term mortgage, loan,

creditworthiness, investments and many more banking services.

There is another tool other than porter’s five forces is value chain analysis. It creates a framework

of business and works as a powerful tool which can recognize the opportunity for respective

business by reducing the cost, identify the important task and differentiate from competitors.

Lowering costs can be achieved by defining financial investment involved for each activity. The

activity which is to be performed in the industry should be at a better price with appropriate

allocation of resources.

profitability in their industry. Thus threats for substitute are not influenced much by the banking

industry in the economy of New Zealand.

Supplier power:

The suppliers are the person who offered the services in the economy. If there is a large number of

suppliers in the market they can influence customers easily and affect the performance of the

newly set-up businesses (Avlonitis, et al 2015). The existing supplier of the banking industry in New

Zealand is Australian-owned banks which influence the majority amount of banking system and

control over the retail and interest rates of banking. There are not so many suppliers in the banking

sector but the Australian owned-banks hold the power in the country. It is quite difficult to sustain

in the banking industry of New Zealand because the suppliers in this sector are powerful but the

new banking system has the opportunity to decrease the supplier power by offering the people a

variety of financial services and alternatives, as this can overcome from the issue of supplier power

in the economy of New Zealand.

Competitive rivalry:

Competitive rivalry means the competitive environment in the economy. The more competitiveness

in the economy can cause instability for a new entrance. It shows the competitiveness in the sector

as the number of competitors in the sector influences the capability to threaten an organization. In

New Zealand, the number of competitors is not huge as there is only Australian owned banking

system but they are the well establish a system of New Zealand and it becomes difficult for newly

set-up banking industry to achieve competitive edge (Kanatani, 2017). The industry can get over

from the issue of competitiveness while developing financial services as long-term mortgage, loan,

creditworthiness, investments and many more banking services.

There is another tool other than porter’s five forces is value chain analysis. It creates a framework

of business and works as a powerful tool which can recognize the opportunity for respective

business by reducing the cost, identify the important task and differentiate from competitors.

Lowering costs can be achieved by defining financial investment involved for each activity. The

activity which is to be performed in the industry should be at a better price with appropriate

allocation of resources.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For achieving value chain strategy it is required for the business to recognize the important tasks

and functions to deliver effective product and services (Gereffi, 2016). It is helpful for focusing on

relevant factors. For example: While establishing new banking sector in New Zealand, the industry

needs to majorly focus on competitors because New Zealand has Australian owned banks can

influence the performance of new banking sector in the nation.

Differentiating from competitors is helpful for the industry to influence a large number of

customers towards the industry. For example, the banking industry in New Zealand could use those

financial services which are not used by the existing banking system, for attracting a large number

of customers in the economy (Backer, 2014). The newly set-up business can use new software and

technology as well for differentiating their services from the customers and it can also be helpful in

analysing the business opportunities towards the growth of the industry. Therefore, value chain

analysis can play an important role in recognizing the business opportunities for the banking

industry in New Zealand.

and functions to deliver effective product and services (Gereffi, 2016). It is helpful for focusing on

relevant factors. For example: While establishing new banking sector in New Zealand, the industry

needs to majorly focus on competitors because New Zealand has Australian owned banks can

influence the performance of new banking sector in the nation.

Differentiating from competitors is helpful for the industry to influence a large number of

customers towards the industry. For example, the banking industry in New Zealand could use those

financial services which are not used by the existing banking system, for attracting a large number

of customers in the economy (Backer, 2014). The newly set-up business can use new software and

technology as well for differentiating their services from the customers and it can also be helpful in

analysing the business opportunities towards the growth of the industry. Therefore, value chain

analysis can play an important role in recognizing the business opportunities for the banking

industry in New Zealand.

CONCLUSION

Business environment plays an important role in the growth of the country as it helps in forecasting

the business opportunities for the expansion of industry. The aim of this report is to recognize the

importance and meaning of business environment and it also shows the factors of business

environment which can influence the newly setup branch by the banking sector. These

examinations are performed within the context of HSBC bank who develops their new branch in

New Zealand. The analytical approaches as PESTLE is created for analysing the business

environment of the country and Porter's five forces are developed within the context of the

banking sector for analysing the business opportunities in New Zealand. Along with it, the report

shows value chain analysis for recognizing business opportunities for banking system. The analytical

approaches are being discussed for understanding the prospects of the banking industry in New

Zealand.

Business environment plays an important role in the growth of the country as it helps in forecasting

the business opportunities for the expansion of industry. The aim of this report is to recognize the

importance and meaning of business environment and it also shows the factors of business

environment which can influence the newly setup branch by the banking sector. These

examinations are performed within the context of HSBC bank who develops their new branch in

New Zealand. The analytical approaches as PESTLE is created for analysing the business

environment of the country and Porter's five forces are developed within the context of the

banking sector for analysing the business opportunities in New Zealand. Along with it, the report

shows value chain analysis for recognizing business opportunities for banking system. The analytical

approaches are being discussed for understanding the prospects of the banking industry in New

Zealand.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.