Idea Selection and Business Pitch

VerifiedAdded on 2023/01/20

|11

|2135

|86

AI Summary

This document discusses the process of idea selection and business pitch. It explores the criteria for selecting the most rational and delightful idea and provides insights on improving the chosen idea before pitching it to investors. The document also includes a revised canvas business model and financial feasibility analysis.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: IDEA SELECTION AND BUSINESS PITCH 1

IDEA SELECTION AND BUSINESS PITCH

Name

Institutional Affiliation

IDEA SELECTION AND BUSINESS PITCH

Name

Institutional Affiliation

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

IDEA SELECTION AND BUSINESS PITCH 2

Idea Evaluation

The four categories model which focuses on which idea is the most rational,

delightful, and darling and one with the longest short is used in the process of selecting which

idea to implement. On the basis of the above mentioned, idea one which is concerned with

the establishment of an online service retailer named Overstock in the USA is chosen. The

business will fundamentally be engaged in the selling of home decors and furniture. This

business is the most rational compared to the other two idea because it is the most innovative,

unique, offers an immediate and bigger problem and most importantly its profitability

potential is not in doubt(Afuah, 2014).

Idea Selection

Compared to idea 2 which is concerned with the creation of Afterpay.com, it is clear

that idea two is not rational enough because it does not specifically pin point which product

it will be providing to the potential clients. Its rationality is therefore in doubt. Equally for

idea three which is concerned with the Minimus idea that seeks to compromise and provide

diverse and exclusively packed merchandises, there is no clear product or service mentioned

that the business aims to provide a solution for. There is therefore no uniqueness to it and

neither does it appear to be promising from a profit point of view (Abdou, etal.2016). On the

aspect of which idea is most delightful, idea one whose intention is to provide an online

service retailer with a specific bias in the selling of home decors and furniture provides the

most excitement to customers and investors. It is precise and clear which something is not

associated with idea two and three which do not specifically state the service or problem to be

solved (Håkansson & Waluszewski, 2017). In terms of how darling it is and overall

feasibility, business clearly seeks to entrench its self in the minds of its customers (Kim and

Min, 2015). Focus is put on creating mechanisms on how best to reach the customer by

exploring the benefits the customer is likely to experience and how best to communicate with

each other(Malarkey, 2014). Idea two and three’s customer benefit model are not elaborate

enough to generate enough endearment with the customers compared to idea one. On the

basis of the above analysis, Idea one whose focus is on the provision of online service retail

services with a specific focus on selling of home decors and furniture is chosen for pitching

(Carayannis, etal.2014).

Improvements

Idea Evaluation

The four categories model which focuses on which idea is the most rational,

delightful, and darling and one with the longest short is used in the process of selecting which

idea to implement. On the basis of the above mentioned, idea one which is concerned with

the establishment of an online service retailer named Overstock in the USA is chosen. The

business will fundamentally be engaged in the selling of home decors and furniture. This

business is the most rational compared to the other two idea because it is the most innovative,

unique, offers an immediate and bigger problem and most importantly its profitability

potential is not in doubt(Afuah, 2014).

Idea Selection

Compared to idea 2 which is concerned with the creation of Afterpay.com, it is clear

that idea two is not rational enough because it does not specifically pin point which product

it will be providing to the potential clients. Its rationality is therefore in doubt. Equally for

idea three which is concerned with the Minimus idea that seeks to compromise and provide

diverse and exclusively packed merchandises, there is no clear product or service mentioned

that the business aims to provide a solution for. There is therefore no uniqueness to it and

neither does it appear to be promising from a profit point of view (Abdou, etal.2016). On the

aspect of which idea is most delightful, idea one whose intention is to provide an online

service retailer with a specific bias in the selling of home decors and furniture provides the

most excitement to customers and investors. It is precise and clear which something is not

associated with idea two and three which do not specifically state the service or problem to be

solved (Håkansson & Waluszewski, 2017). In terms of how darling it is and overall

feasibility, business clearly seeks to entrench its self in the minds of its customers (Kim and

Min, 2015). Focus is put on creating mechanisms on how best to reach the customer by

exploring the benefits the customer is likely to experience and how best to communicate with

each other(Malarkey, 2014). Idea two and three’s customer benefit model are not elaborate

enough to generate enough endearment with the customers compared to idea one. On the

basis of the above analysis, Idea one whose focus is on the provision of online service retail

services with a specific focus on selling of home decors and furniture is chosen for pitching

(Carayannis, etal.2014).

Improvements

IDEA SELECTION AND BUSINESS PITCH 3

There are a few improvements which are proposed for the idea before pitching it to

the investors. There is a management and personnel gap within the business idea. It shall be

important for the company to put in a well-defined management team including the bios of

the company managers and executives(Pantano, 2014).This should include an explanation of

how their expertise will be essential in meeting the organisation’s business goals (Visnjic,

etal.2016). The investors are always interested in risk evaluation and usually prefer to invest

in a company whose management team has the necessary experience and expertise to execute

the business goals and objectives (Hvass, 2015). The other issues left undressed which needs

fixing for this idea before it’s presented before an investor is the competitive analysis. The

idea must present a clear and well defined comparison of the business’s direct as well as

indirect competitors. It is important to for the business to demonstrate that it knows the

strengths and weaknesses of the competitors and that it will work it out (Autio, etal.2014).

The other aspect which needs to be addressed concerns the financial aspect of the

business. It is necessary for the business to provide financial numbers to help back up

everything described within the marketing as well as organisational sections (Winston, 2016).

These are important elements for the investor to look at to try and assess the viability of the

project to be undertaken. The project will have to include a conservative projection of the

profit and loss statements, the cash flows as well as balance sheet for at least the first two

years of business operation (Chesbrough, 2010).

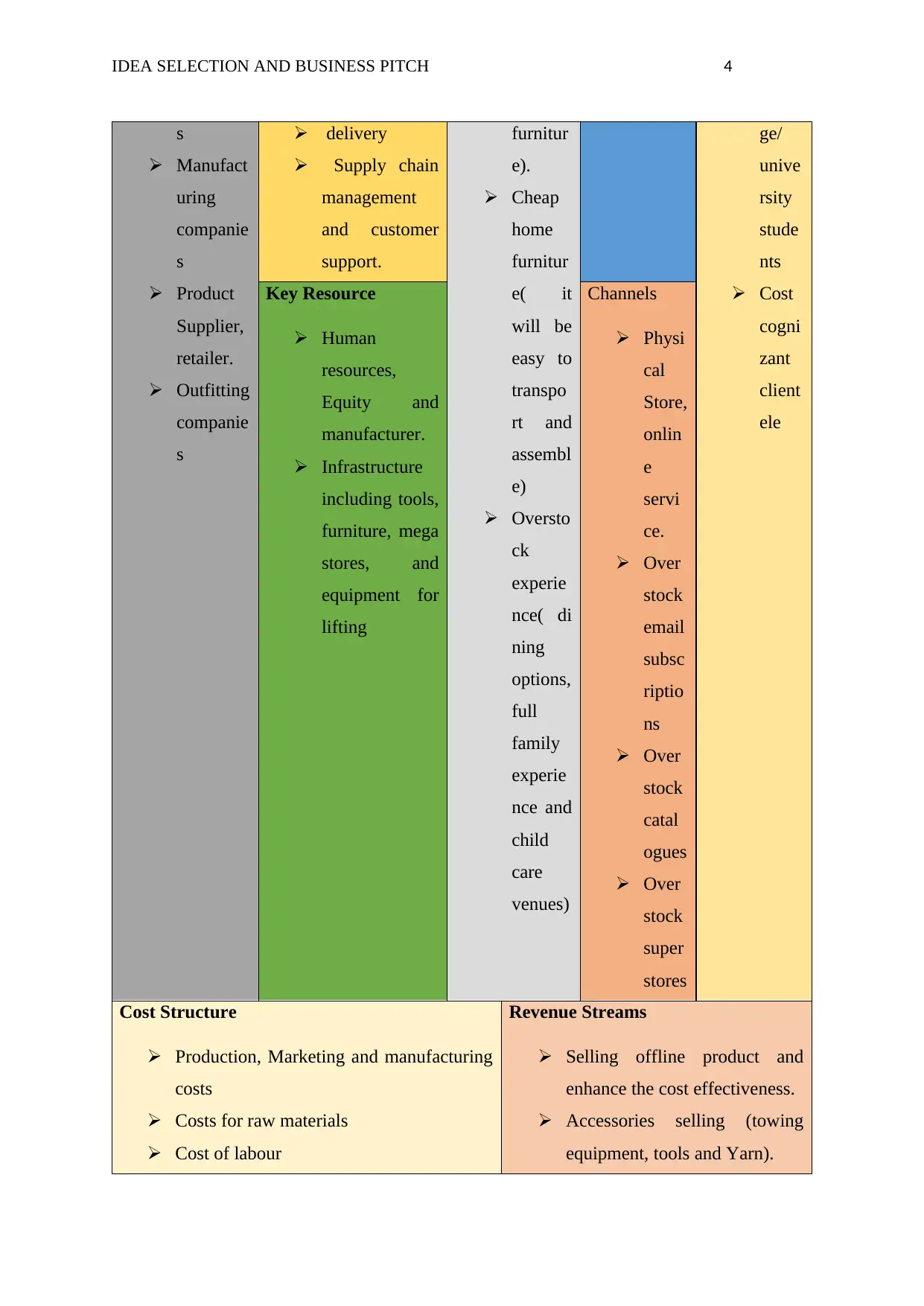

Revised Canvas Business Model

Key partner

Wood

makers

Delivery

firms

Trucking

and

transport

ation

companie

Key Activities

Modular

furniture

design

Modular

Furniture

manufacturing

Service

Marketing,

Product

Value

Proposition

House

Holds

(Bed,

Amirah

, Sofa

as well

as other

home

Customer

relationship

Email,

Social

Media,

mobile

contact,

newsletters.

Customer

segment

Local

Area

Custo

mers.

Small

busin

esses

Colle

There are a few improvements which are proposed for the idea before pitching it to

the investors. There is a management and personnel gap within the business idea. It shall be

important for the company to put in a well-defined management team including the bios of

the company managers and executives(Pantano, 2014).This should include an explanation of

how their expertise will be essential in meeting the organisation’s business goals (Visnjic,

etal.2016). The investors are always interested in risk evaluation and usually prefer to invest

in a company whose management team has the necessary experience and expertise to execute

the business goals and objectives (Hvass, 2015). The other issues left undressed which needs

fixing for this idea before it’s presented before an investor is the competitive analysis. The

idea must present a clear and well defined comparison of the business’s direct as well as

indirect competitors. It is important to for the business to demonstrate that it knows the

strengths and weaknesses of the competitors and that it will work it out (Autio, etal.2014).

The other aspect which needs to be addressed concerns the financial aspect of the

business. It is necessary for the business to provide financial numbers to help back up

everything described within the marketing as well as organisational sections (Winston, 2016).

These are important elements for the investor to look at to try and assess the viability of the

project to be undertaken. The project will have to include a conservative projection of the

profit and loss statements, the cash flows as well as balance sheet for at least the first two

years of business operation (Chesbrough, 2010).

Revised Canvas Business Model

Key partner

Wood

makers

Delivery

firms

Trucking

and

transport

ation

companie

Key Activities

Modular

furniture

design

Modular

Furniture

manufacturing

Service

Marketing,

Product

Value

Proposition

House

Holds

(Bed,

Amirah

, Sofa

as well

as other

home

Customer

relationship

Email,

Social

Media,

mobile

contact,

newsletters.

Customer

segment

Local

Area

Custo

mers.

Small

busin

esses

Colle

IDEA SELECTION AND BUSINESS PITCH 4

s

Manufact

uring

companie

s

Product

Supplier,

retailer.

Outfitting

companie

s

delivery

Supply chain

management

and customer

support.

furnitur

e).

Cheap

home

furnitur

e( it

will be

easy to

transpo

rt and

assembl

e)

Oversto

ck

experie

nce( di

ning

options,

full

family

experie

nce and

child

care

venues)

ge/

unive

rsity

stude

nts

Cost

cogni

zant

client

ele

Key Resource

Human

resources,

Equity and

manufacturer.

Infrastructure

including tools,

furniture, mega

stores, and

equipment for

lifting

Channels

Physi

cal

Store,

onlin

e

servi

ce.

Over

stock

email

subsc

riptio

ns

Over

stock

catal

ogues

Over

stock

super

stores

Cost Structure

Production, Marketing and manufacturing

costs

Costs for raw materials

Cost of labour

Revenue Streams

Selling offline product and

enhance the cost effectiveness.

Accessories selling (towing

equipment, tools and Yarn).

s

Manufact

uring

companie

s

Product

Supplier,

retailer.

Outfitting

companie

s

delivery

Supply chain

management

and customer

support.

furnitur

e).

Cheap

home

furnitur

e( it

will be

easy to

transpo

rt and

assembl

e)

Oversto

ck

experie

nce( di

ning

options,

full

family

experie

nce and

child

care

venues)

ge/

unive

rsity

stude

nts

Cost

cogni

zant

client

ele

Key Resource

Human

resources,

Equity and

manufacturer.

Infrastructure

including tools,

furniture, mega

stores, and

equipment for

lifting

Channels

Physi

cal

Store,

onlin

e

servi

ce.

Over

stock

subsc

riptio

ns

Over

stock

catal

ogues

Over

stock

super

stores

Cost Structure

Production, Marketing and manufacturing

costs

Costs for raw materials

Cost of labour

Revenue Streams

Selling offline product and

enhance the cost effectiveness.

Accessories selling (towing

equipment, tools and Yarn).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

IDEA SELECTION AND BUSINESS PITCH 5

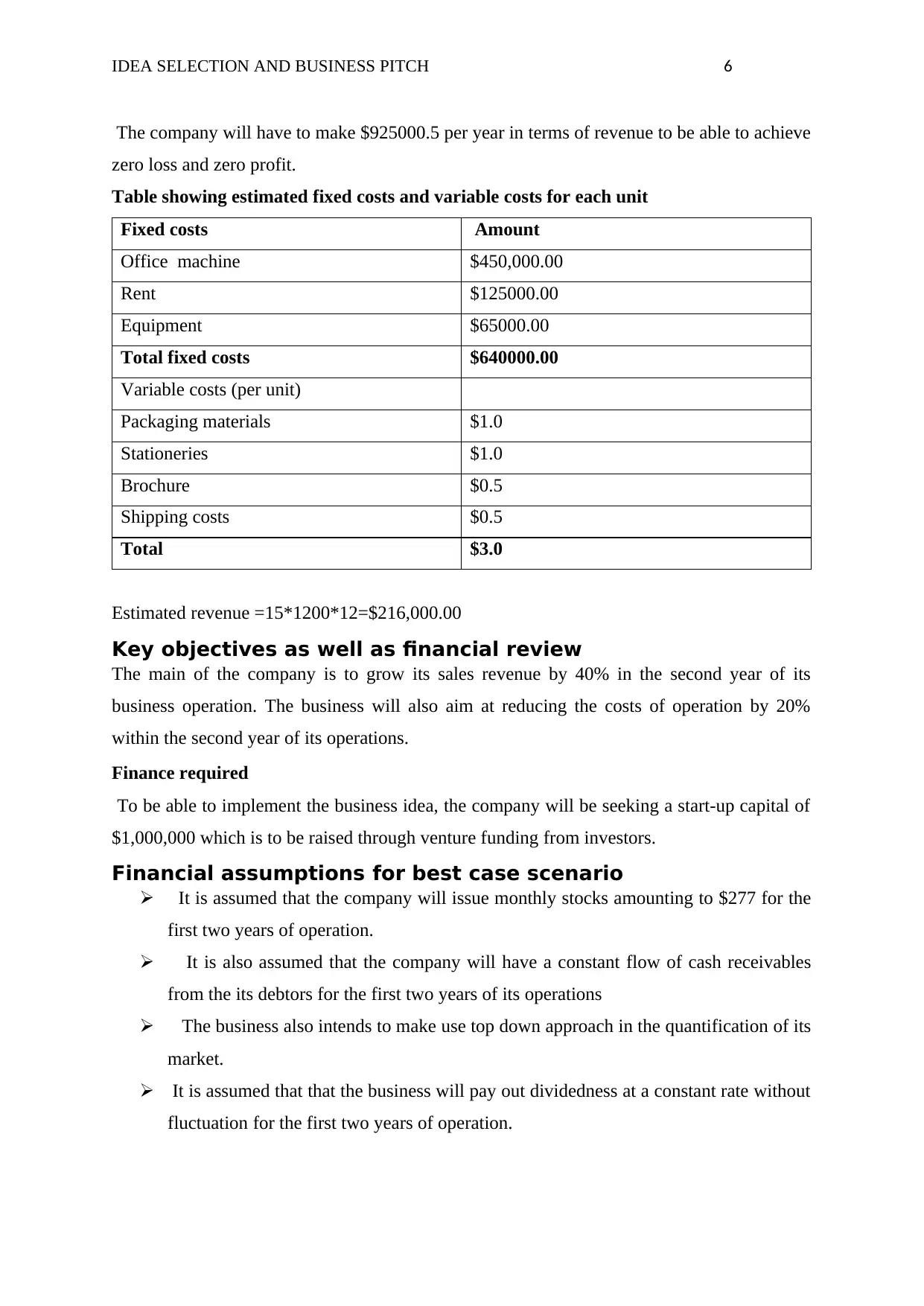

Costs of transportations Fees for services( assembly and

delivery)

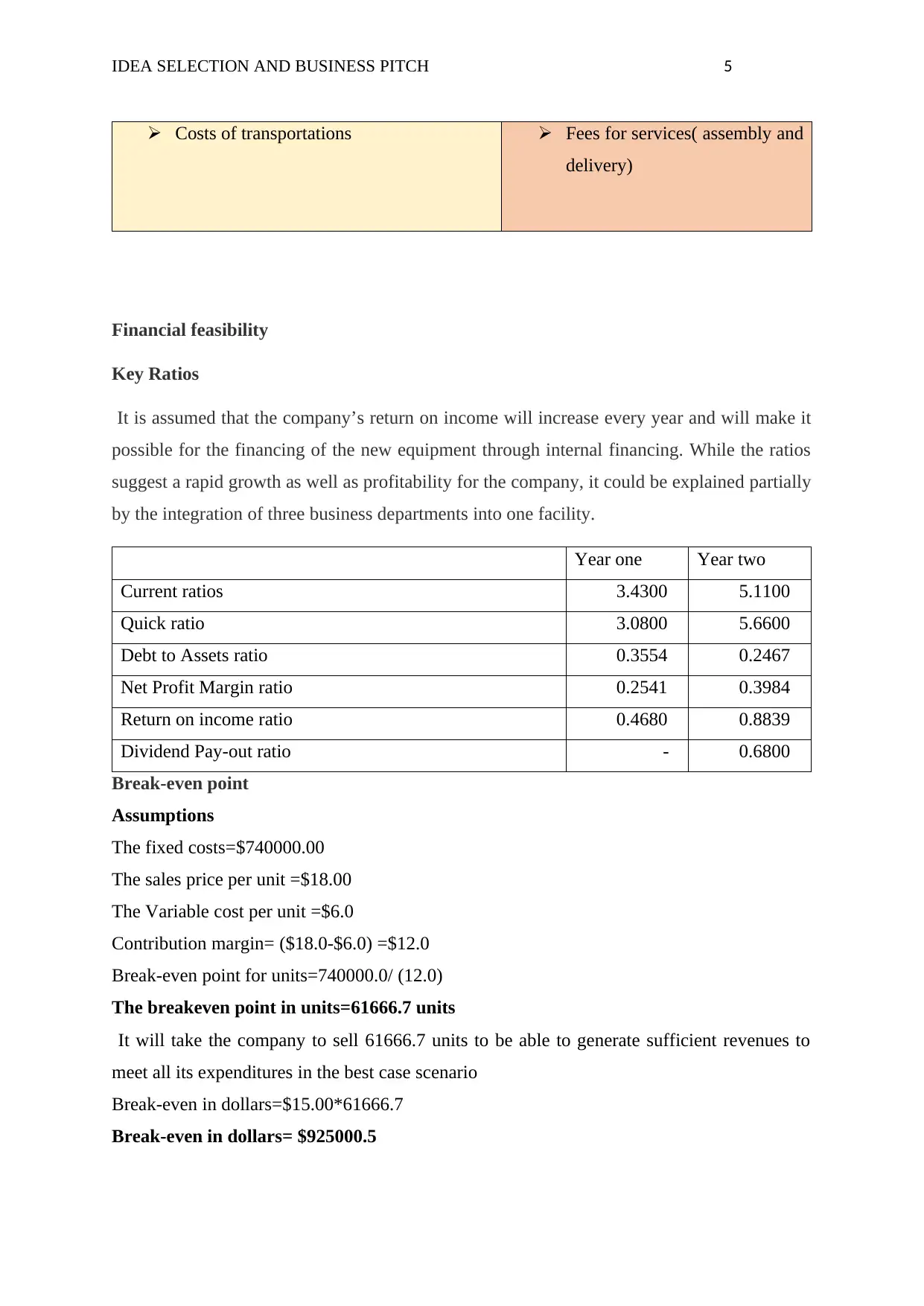

Financial feasibility

Key Ratios

It is assumed that the company’s return on income will increase every year and will make it

possible for the financing of the new equipment through internal financing. While the ratios

suggest a rapid growth as well as profitability for the company, it could be explained partially

by the integration of three business departments into one facility.

Year one Year two

Current ratios 3.4300 5.1100

Quick ratio 3.0800 5.6600

Debt to Assets ratio 0.3554 0.2467

Net Profit Margin ratio 0.2541 0.3984

Return on income ratio 0.4680 0.8839

Dividend Pay-out ratio - 0.6800

Break-even point

Assumptions

The fixed costs=$740000.00

The sales price per unit =$18.00

The Variable cost per unit =$6.0

Contribution margin= ($18.0-$6.0) =$12.0

Break-even point for units=740000.0/ (12.0)

The breakeven point in units=61666.7 units

It will take the company to sell 61666.7 units to be able to generate sufficient revenues to

meet all its expenditures in the best case scenario

Break-even in dollars=$15.00*61666.7

Break-even in dollars= $925000.5

Costs of transportations Fees for services( assembly and

delivery)

Financial feasibility

Key Ratios

It is assumed that the company’s return on income will increase every year and will make it

possible for the financing of the new equipment through internal financing. While the ratios

suggest a rapid growth as well as profitability for the company, it could be explained partially

by the integration of three business departments into one facility.

Year one Year two

Current ratios 3.4300 5.1100

Quick ratio 3.0800 5.6600

Debt to Assets ratio 0.3554 0.2467

Net Profit Margin ratio 0.2541 0.3984

Return on income ratio 0.4680 0.8839

Dividend Pay-out ratio - 0.6800

Break-even point

Assumptions

The fixed costs=$740000.00

The sales price per unit =$18.00

The Variable cost per unit =$6.0

Contribution margin= ($18.0-$6.0) =$12.0

Break-even point for units=740000.0/ (12.0)

The breakeven point in units=61666.7 units

It will take the company to sell 61666.7 units to be able to generate sufficient revenues to

meet all its expenditures in the best case scenario

Break-even in dollars=$15.00*61666.7

Break-even in dollars= $925000.5

IDEA SELECTION AND BUSINESS PITCH 6

The company will have to make $925000.5 per year in terms of revenue to be able to achieve

zero loss and zero profit.

Table showing estimated fixed costs and variable costs for each unit

Fixed costs Amount

Office machine $450,000.00

Rent $125000.00

Equipment $65000.00

Total fixed costs $640000.00

Variable costs (per unit)

Packaging materials $1.0

Stationeries $1.0

Brochure $0.5

Shipping costs $0.5

Total $3.0

Estimated revenue =15*1200*12=$216,000.00

Key objectives as well as financial review

The main of the company is to grow its sales revenue by 40% in the second year of its

business operation. The business will also aim at reducing the costs of operation by 20%

within the second year of its operations.

Finance required

To be able to implement the business idea, the company will be seeking a start-up capital of

$1,000,000 which is to be raised through venture funding from investors.

Financial assumptions for best case scenario

It is assumed that the company will issue monthly stocks amounting to $277 for the

first two years of operation.

It is also assumed that the company will have a constant flow of cash receivables

from the its debtors for the first two years of its operations

The business also intends to make use top down approach in the quantification of its

market.

It is assumed that that the business will pay out dividedness at a constant rate without

fluctuation for the first two years of operation.

The company will have to make $925000.5 per year in terms of revenue to be able to achieve

zero loss and zero profit.

Table showing estimated fixed costs and variable costs for each unit

Fixed costs Amount

Office machine $450,000.00

Rent $125000.00

Equipment $65000.00

Total fixed costs $640000.00

Variable costs (per unit)

Packaging materials $1.0

Stationeries $1.0

Brochure $0.5

Shipping costs $0.5

Total $3.0

Estimated revenue =15*1200*12=$216,000.00

Key objectives as well as financial review

The main of the company is to grow its sales revenue by 40% in the second year of its

business operation. The business will also aim at reducing the costs of operation by 20%

within the second year of its operations.

Finance required

To be able to implement the business idea, the company will be seeking a start-up capital of

$1,000,000 which is to be raised through venture funding from investors.

Financial assumptions for best case scenario

It is assumed that the company will issue monthly stocks amounting to $277 for the

first two years of operation.

It is also assumed that the company will have a constant flow of cash receivables

from the its debtors for the first two years of its operations

The business also intends to make use top down approach in the quantification of its

market.

It is assumed that that the business will pay out dividedness at a constant rate without

fluctuation for the first two years of operation.

IDEA SELECTION AND BUSINESS PITCH 7

It is further presumed that the business will have a positive net cash valance within

the first two years of its operations.

Average case scenario assumptions

It is assumed that the company will issue monthly stocks amounting to $177 for the

first two years of operation and more specifically within the first six months of

operation

It is also assumed that the company will have a constant flow of cash receivables

from the its debtors for the first two years of its operations at a rate sufficient enough

to keep the company running

It is assumed that that the business will pay out dividedness at a constant rate without

fluctuation for the first two years of operation.

The business is also presumed to have a positive net cash valance within the first two

years of its operations at a constant rate

Worst case scenario assumptions

It is assumed that the company will issue monthly stocks amounting to $377 for the

first two years of operation and more specifically within the first six months of

operation

The company is not expected to receive cash enough to sustain its operations within

the first two years of operations.

The business is also presumed to have a negative net cash valance within the first two

years of its operations at a constant rate

It is further presumed that the business will have a positive net cash valance within

the first two years of its operations.

Average case scenario assumptions

It is assumed that the company will issue monthly stocks amounting to $177 for the

first two years of operation and more specifically within the first six months of

operation

It is also assumed that the company will have a constant flow of cash receivables

from the its debtors for the first two years of its operations at a rate sufficient enough

to keep the company running

It is assumed that that the business will pay out dividedness at a constant rate without

fluctuation for the first two years of operation.

The business is also presumed to have a positive net cash valance within the first two

years of its operations at a constant rate

Worst case scenario assumptions

It is assumed that the company will issue monthly stocks amounting to $377 for the

first two years of operation and more specifically within the first six months of

operation

The company is not expected to receive cash enough to sustain its operations within

the first two years of operations.

The business is also presumed to have a negative net cash valance within the first two

years of its operations at a constant rate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IDEA SELECTION AND BUSINESS PITCH 8

References

Afuah, A. (2014). Business model innovation: concepts, analysis, and cases. Routledge.

Autio, E., Kenney, M., Mustar, P., Siegel, D., & Wright, M. (2014). Entrepreneurial

innovation: The importance of context. Research Policy, 43(7), 1097-1108.

Carayannis, E. G., Grigoroudis, E., Sindakis, S., & Walter, C. (2014). Business model

innovation as antecedent of sustainable enterprise excellence and resilience. Journal

of the Knowledge Economy, 5(3), 440-463.

Chesbrough, H. (2010). Business model innovation: opportunities and barriers. Long range

planning, 42(2-3), 354-363.

Håkansson, H., & Waluszewski, A. (2017). Knowledge and innovation in business and

industry: The importance of using others. Routledge.

Hvass, K. K. (2015). Business model innovation through second hand retailing: a fashion

industry case. Journal of Corporate Citizenship, (57), 11-32.

Kim, S. K., & Min, S. (2015). Business model innovation performance: when does adding a

new business model benefit an incumbent?. Strategic Entrepreneurship Journal, 9(1),

34-57.

Malarkey, A. (2014). Australia: Business model innovation - Part 2: Understanding

innovation.Retrieved May 1, 2019, from

http://www.mondaq.com/australia/x/313020/technology/Business+model+innovation

+Part+2+Understanding+inno

Pantano, E. (2014). Innovation drivers in retail industry. International Journal of Information

Management, 34(3), 344-350.

Souto, J. E. (2015). Business model innovation and business concept innovation as the

context of incremental innovation and radical innovation. Tourism Management, 51,

142-155.

Visnjic, I., Wiengarten, F., & Neely, A. (2016). Only the brave: Product innovation, service

business model innovation, and their impact on performance. Journal of Product

Innovation Management, 33(1), 36-52.

References

Afuah, A. (2014). Business model innovation: concepts, analysis, and cases. Routledge.

Autio, E., Kenney, M., Mustar, P., Siegel, D., & Wright, M. (2014). Entrepreneurial

innovation: The importance of context. Research Policy, 43(7), 1097-1108.

Carayannis, E. G., Grigoroudis, E., Sindakis, S., & Walter, C. (2014). Business model

innovation as antecedent of sustainable enterprise excellence and resilience. Journal

of the Knowledge Economy, 5(3), 440-463.

Chesbrough, H. (2010). Business model innovation: opportunities and barriers. Long range

planning, 42(2-3), 354-363.

Håkansson, H., & Waluszewski, A. (2017). Knowledge and innovation in business and

industry: The importance of using others. Routledge.

Hvass, K. K. (2015). Business model innovation through second hand retailing: a fashion

industry case. Journal of Corporate Citizenship, (57), 11-32.

Kim, S. K., & Min, S. (2015). Business model innovation performance: when does adding a

new business model benefit an incumbent?. Strategic Entrepreneurship Journal, 9(1),

34-57.

Malarkey, A. (2014). Australia: Business model innovation - Part 2: Understanding

innovation.Retrieved May 1, 2019, from

http://www.mondaq.com/australia/x/313020/technology/Business+model+innovation

+Part+2+Understanding+inno

Pantano, E. (2014). Innovation drivers in retail industry. International Journal of Information

Management, 34(3), 344-350.

Souto, J. E. (2015). Business model innovation and business concept innovation as the

context of incremental innovation and radical innovation. Tourism Management, 51,

142-155.

Visnjic, I., Wiengarten, F., & Neely, A. (2016). Only the brave: Product innovation, service

business model innovation, and their impact on performance. Journal of Product

Innovation Management, 33(1), 36-52.

IDEA SELECTION AND BUSINESS PITCH 9

Abdou, S. M, Yong, K., Othman, M. (2016). Project Complexity Influence on Project

management performance. The Malaysian perspective. MATEC Web of Conferences.

66: 00065. doi:10.1051/matecconf/20166600065. ISSN 2261-236X.

Winston W. (2016). Managing the Development of Large Software SystemsArchived 2016-

03-15 at the Wayback Machine in: Technical Papers of Western Electronic Show and

Convention (WesCon), Los Angeles, USA.

Abdou, S. M, Yong, K., Othman, M. (2016). Project Complexity Influence on Project

management performance. The Malaysian perspective. MATEC Web of Conferences.

66: 00065. doi:10.1051/matecconf/20166600065. ISSN 2261-236X.

Winston W. (2016). Managing the Development of Large Software SystemsArchived 2016-

03-15 at the Wayback Machine in: Technical Papers of Western Electronic Show and

Convention (WesCon), Los Angeles, USA.

IDEA SELECTION AND BUSINESS PITCH 10

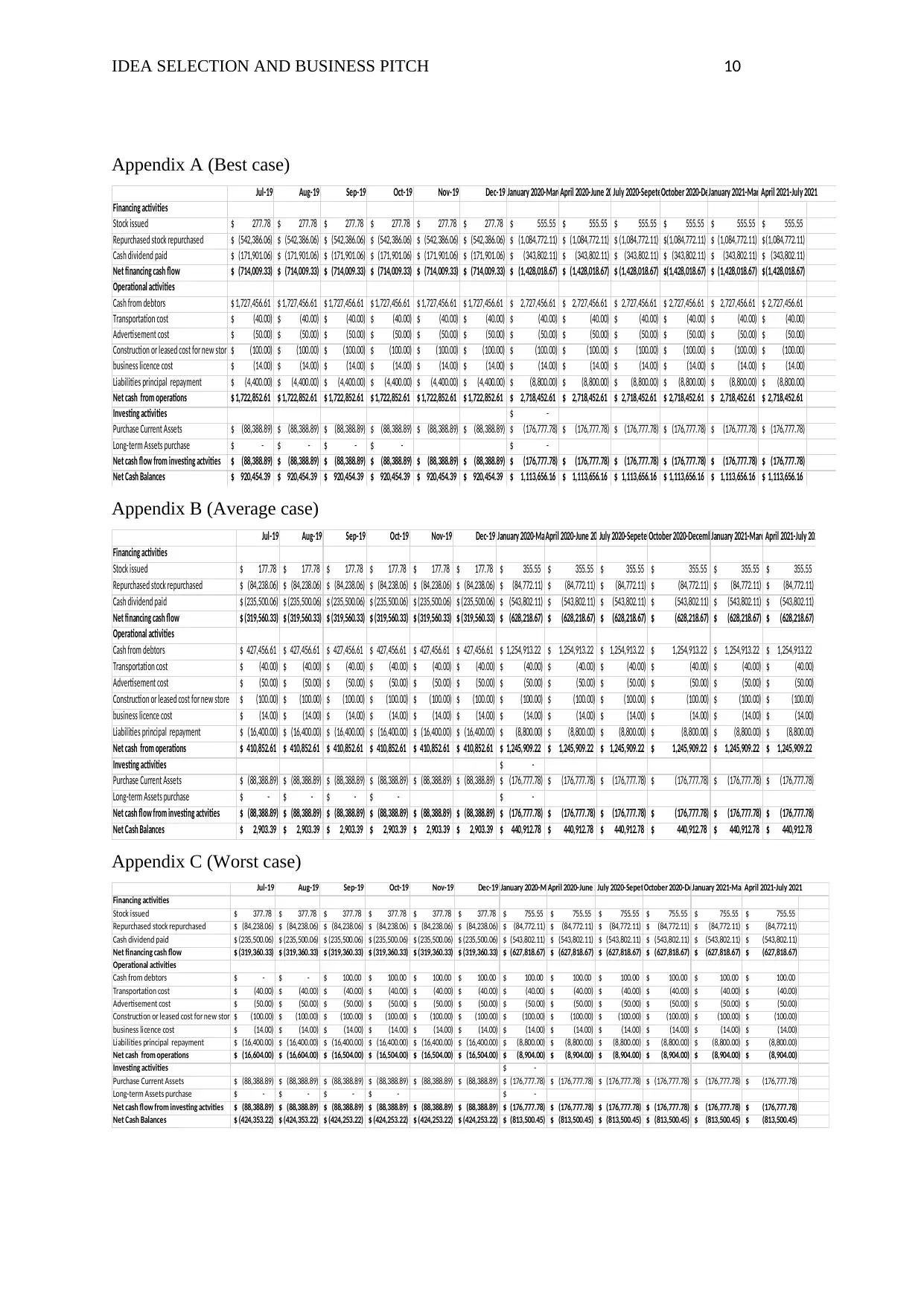

Appendix A (Best case)

Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 January 2020-March 2020April 2020-June 2020July 2020-Sepetember 2020October 2020-December 2020January 2021-March 2021April 2021-July 2021

Financing activities

Stock issued 277.78$ 277.78$ 277.78$ 277.78$ 277.78$ 277.78$ 555.55$ 555.55$ 555.55$ 555.55$ 555.55$ 555.55$

Repurchased stock repurchased (542,386.06)$ (542,386.06)$ (542,386.06)$ (542,386.06)$ (542,386.06)$ (542,386.06)$ (1,084,772.11)$ (1,084,772.11)$ (1,084,772.11)$ (1,084,772.11)$ (1,084,772.11)$ (1,084,772.11)$

Cash dividend paid (171,901.06)$ (171,901.06)$ (171,901.06)$ (171,901.06)$ (171,901.06)$ (171,901.06)$ (343,802.11)$ (343,802.11)$ (343,802.11)$ (343,802.11)$ (343,802.11)$ (343,802.11)$

Net financing cash flow (714,009.33)$ (714,009.33)$ (714,009.33)$ (714,009.33)$ (714,009.33)$ (714,009.33)$ (1,428,018.67)$ (1,428,018.67)$ (1,428,018.67)$ (1,428,018.67)$ (1,428,018.67)$ (1,428,018.67)$

Operational activities

Cash from debtors 1,727,456.61$ 1,727,456.61$ 1,727,456.61$ 1,727,456.61$ 1,727,456.61$ 1,727,456.61$ 2,727,456.61$ 2,727,456.61$ 2,727,456.61$ 2,727,456.61$ 2,727,456.61$ 2,727,456.61$

Transportation cost (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$

Advertisement cost (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$

Construction or leased cost for new store (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$

business licence cost (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$

Liabilities principal repayment (4,400.00)$ (4,400.00)$ (4,400.00)$ (4,400.00)$ (4,400.00)$ (4,400.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$

Net cash from operations 1,722,852.61$ 1,722,852.61$ 1,722,852.61$ 1,722,852.61$ 1,722,852.61$ 1,722,852.61$ 2,718,452.61$ 2,718,452.61$ 2,718,452.61$ 2,718,452.61$ 2,718,452.61$ 2,718,452.61$

Investing activities -$

Purchase Current Assets (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$

Long-term Assets purchase -$ -$ -$ -$ -$

Net cash flow from investing actvities (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$

Net Cash Balances 920,454.39$ 920,454.39$ 920,454.39$ 920,454.39$ 920,454.39$ 920,454.39$ 1,113,656.16$ 1,113,656.16$ 1,113,656.16$ 1,113,656.16$ 1,113,656.16$ 1,113,656.16$

Appendix B (Average case)

Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 January 2020-March 2020April 2020-June 2020July 2020-Sepetember 2020October 2020-December 2020January 2021-March 2021April 2021-July 2021

Financing activities

Stock issued 177.78$ 177.78$ 177.78$ 177.78$ 177.78$ 177.78$ 355.55$ 355.55$ 355.55$ 355.55$ 355.55$ 355.55$

Repurchased stock repurchased (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,772.11)$ (84,772.11)$ (84,772.11)$ (84,772.11)$ (84,772.11)$ (84,772.11)$

Cash dividend paid (235,500.06)$ (235,500.06)$ (235,500.06)$ (235,500.06)$ (235,500.06)$ (235,500.06)$ (543,802.11)$ (543,802.11)$ (543,802.11)$ (543,802.11)$ (543,802.11)$ (543,802.11)$

Net financing cash flow (319,560.33)$ (319,560.33)$ (319,560.33)$ (319,560.33)$ (319,560.33)$ (319,560.33)$ (628,218.67)$ (628,218.67)$ (628,218.67)$ (628,218.67)$ (628,218.67)$ (628,218.67)$

Operational activities

Cash from debtors 427,456.61$ 427,456.61$ 427,456.61$ 427,456.61$ 427,456.61$ 427,456.61$ 1,254,913.22$ 1,254,913.22$ 1,254,913.22$ 1,254,913.22$ 1,254,913.22$ 1,254,913.22$

Transportation cost (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$

Advertisement cost (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$

Construction or leased cost for new store (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$

business licence cost (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$

Liabilities principal repayment (16,400.00)$ (16,400.00)$ (16,400.00)$ (16,400.00)$ (16,400.00)$ (16,400.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$

Net cash from operations 410,852.61$ 410,852.61$ 410,852.61$ 410,852.61$ 410,852.61$ 410,852.61$ 1,245,909.22$ 1,245,909.22$ 1,245,909.22$ 1,245,909.22$ 1,245,909.22$ 1,245,909.22$

Investing activities -$

Purchase Current Assets (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$

Long-term Assets purchase -$ -$ -$ -$ -$

Net cash flow from investing actvities (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$

Net Cash Balances 2,903.39$ 2,903.39$ 2,903.39$ 2,903.39$ 2,903.39$ 2,903.39$ 440,912.78$ 440,912.78$ 440,912.78$ 440,912.78$ 440,912.78$ 440,912.78$

Appendix C (Worst case)

Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 January 2020-March 2020April 2020-June 2020July 2020-Sepetember 2020October 2020-December 2020January 2021-March 2021April 2021-July 2021

Financing activities

Stock issued 377.78$ 377.78$ 377.78$ 377.78$ 377.78$ 377.78$ 755.55$ 755.55$ 755.55$ 755.55$ 755.55$ 755.55$

Repurchased stock repurchased (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,772.11)$ (84,772.11)$ (84,772.11)$ (84,772.11)$ (84,772.11)$ (84,772.11)$

Cash dividend paid (235,500.06)$ (235,500.06)$ (235,500.06)$ (235,500.06)$ (235,500.06)$ (235,500.06)$ (543,802.11)$ (543,802.11)$ (543,802.11)$ (543,802.11)$ (543,802.11)$ (543,802.11)$

Net financing cash flow (319,360.33)$ (319,360.33)$ (319,360.33)$ (319,360.33)$ (319,360.33)$ (319,360.33)$ (627,818.67)$ (627,818.67)$ (627,818.67)$ (627,818.67)$ (627,818.67)$ (627,818.67)$

Operational activities

Cash from debtors -$ -$ 100.00$ 100.00$ 100.00$ 100.00$ 100.00$ 100.00$ 100.00$ 100.00$ 100.00$ 100.00$

Transportation cost (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$

Advertisement cost (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$

Construction or leased cost for new store (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$

business licence cost (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$

Liabilities principal repayment (16,400.00)$ (16,400.00)$ (16,400.00)$ (16,400.00)$ (16,400.00)$ (16,400.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$

Net cash from operations (16,604.00)$ (16,604.00)$ (16,504.00)$ (16,504.00)$ (16,504.00)$ (16,504.00)$ (8,904.00)$ (8,904.00)$ (8,904.00)$ (8,904.00)$ (8,904.00)$ (8,904.00)$

Investing activities -$

Purchase Current Assets (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$

Long-term Assets purchase -$ -$ -$ -$ -$

Net cash flow from investing actvities (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$

Net Cash Balances (424,353.22)$ (424,353.22)$ (424,253.22)$ (424,253.22)$ (424,253.22)$ (424,253.22)$ (813,500.45)$ (813,500.45)$ (813,500.45)$ (813,500.45)$ (813,500.45)$ (813,500.45)$

Appendix A (Best case)

Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 January 2020-March 2020April 2020-June 2020July 2020-Sepetember 2020October 2020-December 2020January 2021-March 2021April 2021-July 2021

Financing activities

Stock issued 277.78$ 277.78$ 277.78$ 277.78$ 277.78$ 277.78$ 555.55$ 555.55$ 555.55$ 555.55$ 555.55$ 555.55$

Repurchased stock repurchased (542,386.06)$ (542,386.06)$ (542,386.06)$ (542,386.06)$ (542,386.06)$ (542,386.06)$ (1,084,772.11)$ (1,084,772.11)$ (1,084,772.11)$ (1,084,772.11)$ (1,084,772.11)$ (1,084,772.11)$

Cash dividend paid (171,901.06)$ (171,901.06)$ (171,901.06)$ (171,901.06)$ (171,901.06)$ (171,901.06)$ (343,802.11)$ (343,802.11)$ (343,802.11)$ (343,802.11)$ (343,802.11)$ (343,802.11)$

Net financing cash flow (714,009.33)$ (714,009.33)$ (714,009.33)$ (714,009.33)$ (714,009.33)$ (714,009.33)$ (1,428,018.67)$ (1,428,018.67)$ (1,428,018.67)$ (1,428,018.67)$ (1,428,018.67)$ (1,428,018.67)$

Operational activities

Cash from debtors 1,727,456.61$ 1,727,456.61$ 1,727,456.61$ 1,727,456.61$ 1,727,456.61$ 1,727,456.61$ 2,727,456.61$ 2,727,456.61$ 2,727,456.61$ 2,727,456.61$ 2,727,456.61$ 2,727,456.61$

Transportation cost (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$

Advertisement cost (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$

Construction or leased cost for new store (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$

business licence cost (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$

Liabilities principal repayment (4,400.00)$ (4,400.00)$ (4,400.00)$ (4,400.00)$ (4,400.00)$ (4,400.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$

Net cash from operations 1,722,852.61$ 1,722,852.61$ 1,722,852.61$ 1,722,852.61$ 1,722,852.61$ 1,722,852.61$ 2,718,452.61$ 2,718,452.61$ 2,718,452.61$ 2,718,452.61$ 2,718,452.61$ 2,718,452.61$

Investing activities -$

Purchase Current Assets (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$

Long-term Assets purchase -$ -$ -$ -$ -$

Net cash flow from investing actvities (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$

Net Cash Balances 920,454.39$ 920,454.39$ 920,454.39$ 920,454.39$ 920,454.39$ 920,454.39$ 1,113,656.16$ 1,113,656.16$ 1,113,656.16$ 1,113,656.16$ 1,113,656.16$ 1,113,656.16$

Appendix B (Average case)

Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 January 2020-March 2020April 2020-June 2020July 2020-Sepetember 2020October 2020-December 2020January 2021-March 2021April 2021-July 2021

Financing activities

Stock issued 177.78$ 177.78$ 177.78$ 177.78$ 177.78$ 177.78$ 355.55$ 355.55$ 355.55$ 355.55$ 355.55$ 355.55$

Repurchased stock repurchased (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,772.11)$ (84,772.11)$ (84,772.11)$ (84,772.11)$ (84,772.11)$ (84,772.11)$

Cash dividend paid (235,500.06)$ (235,500.06)$ (235,500.06)$ (235,500.06)$ (235,500.06)$ (235,500.06)$ (543,802.11)$ (543,802.11)$ (543,802.11)$ (543,802.11)$ (543,802.11)$ (543,802.11)$

Net financing cash flow (319,560.33)$ (319,560.33)$ (319,560.33)$ (319,560.33)$ (319,560.33)$ (319,560.33)$ (628,218.67)$ (628,218.67)$ (628,218.67)$ (628,218.67)$ (628,218.67)$ (628,218.67)$

Operational activities

Cash from debtors 427,456.61$ 427,456.61$ 427,456.61$ 427,456.61$ 427,456.61$ 427,456.61$ 1,254,913.22$ 1,254,913.22$ 1,254,913.22$ 1,254,913.22$ 1,254,913.22$ 1,254,913.22$

Transportation cost (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$

Advertisement cost (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$

Construction or leased cost for new store (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$

business licence cost (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$

Liabilities principal repayment (16,400.00)$ (16,400.00)$ (16,400.00)$ (16,400.00)$ (16,400.00)$ (16,400.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$

Net cash from operations 410,852.61$ 410,852.61$ 410,852.61$ 410,852.61$ 410,852.61$ 410,852.61$ 1,245,909.22$ 1,245,909.22$ 1,245,909.22$ 1,245,909.22$ 1,245,909.22$ 1,245,909.22$

Investing activities -$

Purchase Current Assets (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$

Long-term Assets purchase -$ -$ -$ -$ -$

Net cash flow from investing actvities (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$

Net Cash Balances 2,903.39$ 2,903.39$ 2,903.39$ 2,903.39$ 2,903.39$ 2,903.39$ 440,912.78$ 440,912.78$ 440,912.78$ 440,912.78$ 440,912.78$ 440,912.78$

Appendix C (Worst case)

Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 January 2020-March 2020April 2020-June 2020July 2020-Sepetember 2020October 2020-December 2020January 2021-March 2021April 2021-July 2021

Financing activities

Stock issued 377.78$ 377.78$ 377.78$ 377.78$ 377.78$ 377.78$ 755.55$ 755.55$ 755.55$ 755.55$ 755.55$ 755.55$

Repurchased stock repurchased (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,238.06)$ (84,772.11)$ (84,772.11)$ (84,772.11)$ (84,772.11)$ (84,772.11)$ (84,772.11)$

Cash dividend paid (235,500.06)$ (235,500.06)$ (235,500.06)$ (235,500.06)$ (235,500.06)$ (235,500.06)$ (543,802.11)$ (543,802.11)$ (543,802.11)$ (543,802.11)$ (543,802.11)$ (543,802.11)$

Net financing cash flow (319,360.33)$ (319,360.33)$ (319,360.33)$ (319,360.33)$ (319,360.33)$ (319,360.33)$ (627,818.67)$ (627,818.67)$ (627,818.67)$ (627,818.67)$ (627,818.67)$ (627,818.67)$

Operational activities

Cash from debtors -$ -$ 100.00$ 100.00$ 100.00$ 100.00$ 100.00$ 100.00$ 100.00$ 100.00$ 100.00$ 100.00$

Transportation cost (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$ (40.00)$

Advertisement cost (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$ (50.00)$

Construction or leased cost for new store (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$ (100.00)$

business licence cost (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$ (14.00)$

Liabilities principal repayment (16,400.00)$ (16,400.00)$ (16,400.00)$ (16,400.00)$ (16,400.00)$ (16,400.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$ (8,800.00)$

Net cash from operations (16,604.00)$ (16,604.00)$ (16,504.00)$ (16,504.00)$ (16,504.00)$ (16,504.00)$ (8,904.00)$ (8,904.00)$ (8,904.00)$ (8,904.00)$ (8,904.00)$ (8,904.00)$

Investing activities -$

Purchase Current Assets (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$

Long-term Assets purchase -$ -$ -$ -$ -$

Net cash flow from investing actvities (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (88,388.89)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$ (176,777.78)$

Net Cash Balances (424,353.22)$ (424,353.22)$ (424,253.22)$ (424,253.22)$ (424,253.22)$ (424,253.22)$ (813,500.45)$ (813,500.45)$ (813,500.45)$ (813,500.45)$ (813,500.45)$ (813,500.45)$

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

IDEA SELECTION AND BUSINESS PITCH 11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.