Complex Lending and Broking - Task 1a

VerifiedAdded on 2023/06/10

|27

|8554

|190

AI Summary

The article provides a list of questions that can be asked to Ray Murdoch and Steve Brown to identify their complex broking needs and understand the potential benefits and risks associated with the intended equipment purchase. The questions also help in understanding the financial aspects of the transaction and the current financial position of the business.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Written Assignment

Complex Lending and Broking

(DIPMB2_AS_v2)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number 10395520

Written Assignment result

(assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Result summary (assessor to complete)

First submission Resubmission (if required)

Task 1 Demonstrated Demonstrated

Task 2 Demonstrated Demonstrated

Task 3 Demonstrated Demonstrated

Feedback

(assessor to complete)

[insert assessor feedback]

DIPMB2_AS_v2

Complex Lending and Broking

(DIPMB2_AS_v2)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number 10395520

Written Assignment result

(assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Result summary (assessor to complete)

First submission Resubmission (if required)

Task 1 Demonstrated Demonstrated

Task 2 Demonstrated Demonstrated

Task 3 Demonstrated Demonstrated

Feedback

(assessor to complete)

[insert assessor feedback]

DIPMB2_AS_v2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Before you begin

Read everything in this document before you start your written assignment for the Complex Lending and

Broking (DIPMB2v2) subject.

About this document

This document is the written assignment and includes the following:

• Instructions for completing and submitting this written assignment

• Section 1: Case Study A – Ray Murdoch and Steve Brown – Commercial Equipment Finance

– Task 1a – Identify the clients’ complex broking needs

– Task 2a – Develop complex broking options

– Task 3a – Implement complex loan structures

• Section 2: Case Study B – Bill Smith and John Jones – Commercial Premises Finance

– Task 1b – Identify the clients’ complex broking needs

– Task 2b – Prepare complex broking options

– Task 3b – Implement complex loan structures

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete the

written assignment within your enrolment period. Your study plan is in the KapLearn Complex Lending and

Broking (DIPMB2v2) subject room.

Page 2 of 27

Read everything in this document before you start your written assignment for the Complex Lending and

Broking (DIPMB2v2) subject.

About this document

This document is the written assignment and includes the following:

• Instructions for completing and submitting this written assignment

• Section 1: Case Study A – Ray Murdoch and Steve Brown – Commercial Equipment Finance

– Task 1a – Identify the clients’ complex broking needs

– Task 2a – Develop complex broking options

– Task 3a – Implement complex loan structures

• Section 2: Case Study B – Bill Smith and John Jones – Commercial Premises Finance

– Task 1b – Identify the clients’ complex broking needs

– Task 2b – Prepare complex broking options

– Task 3b – Implement complex loan structures

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete the

written assignment within your enrolment period. Your study plan is in the KapLearn Complex Lending and

Broking (DIPMB2v2) subject room.

Page 2 of 27

Instructions for completing and submitting this written

assignment

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for this written assignment.

• Name your file as follows: Studentnumber_SubjectCode_Assignment_versionnumber_Submissionnumber

(e.g. 12345678_DIPMB2_AS_v2_Submission1).

• Include your student ID on the first page of the written assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

The written assignment

The information and data you need to complete this written assignment is presented in the case studies at

the beginning of each task.

This written assignment covers complex lending and broking and requires you to answer the questions for

one (1) of the two (2) available case studies. Each case study focuses on a different lending scenario.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing this assignment, assumptions are permitted although they must not be in conflict with

the information provided in the Case Studies.

You may also be required to source additional information from other organisations in the finance industry

to find the right products or services to meet your client’s requirements, or to calculate any service fees

that may be applicable.

Page 3 of 27

assignment

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for this written assignment.

• Name your file as follows: Studentnumber_SubjectCode_Assignment_versionnumber_Submissionnumber

(e.g. 12345678_DIPMB2_AS_v2_Submission1).

• Include your student ID on the first page of the written assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

The written assignment

The information and data you need to complete this written assignment is presented in the case studies at

the beginning of each task.

This written assignment covers complex lending and broking and requires you to answer the questions for

one (1) of the two (2) available case studies. Each case study focuses on a different lending scenario.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing this assignment, assumptions are permitted although they must not be in conflict with

the information provided in the Case Studies.

You may also be required to source additional information from other organisations in the finance industry

to find the right products or services to meet your client’s requirements, or to calculate any service fees

that may be applicable.

Page 3 of 27

Submitting the written assignment

Only Microsoft Office compatible written assignments submitted in the template file will be accepted for

marking by Kaplan Professional Education. You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed written assignment as a PDF.

The written assignment must be

completed before submitting it to Kaplan Professional Education.

Incomplete written assignments will be returned to you unmarked.

The maximum file size is 20MB for the written assignment. Once you submit your written assignment for

marking you will be unable to make any further changes to it.

You are able to submit your written assignment earlier than the deadline if you are confident you have

completed all parts and have prepared a quality submission.

Please refer to the Assignment submission/resubmission instructions (pdf) in the Assessment section of

KapLearn for details on how to submit your written assignment.

Your

written assignment must be submitted on or before your due date. Please check KapLearn for the

due date.

The written assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

If you reach the end of your initial enrolment period and have been deemed Not Yet Competent in one or

more assessment items, then an additional 4 weeks will be granted, provided you attempted all assessment

tasks during the initial enrolment period.

Your assessor will mark your written assignment and return it to you in the Complex Lending and Broking

(DIPMB2v2) subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your written assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your

completed written assignment.

Page 4 of 27

Only Microsoft Office compatible written assignments submitted in the template file will be accepted for

marking by Kaplan Professional Education. You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed written assignment as a PDF.

The written assignment must be

completed before submitting it to Kaplan Professional Education.

Incomplete written assignments will be returned to you unmarked.

The maximum file size is 20MB for the written assignment. Once you submit your written assignment for

marking you will be unable to make any further changes to it.

You are able to submit your written assignment earlier than the deadline if you are confident you have

completed all parts and have prepared a quality submission.

Please refer to the Assignment submission/resubmission instructions (pdf) in the Assessment section of

KapLearn for details on how to submit your written assignment.

Your

written assignment must be submitted on or before your due date. Please check KapLearn for the

due date.

The written assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

If you reach the end of your initial enrolment period and have been deemed Not Yet Competent in one or

more assessment items, then an additional 4 weeks will be granted, provided you attempted all assessment

tasks during the initial enrolment period.

Your assessor will mark your written assignment and return it to you in the Complex Lending and Broking

(DIPMB2v2) subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your written assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your

completed written assignment.

Page 4 of 27

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

How your written assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your written assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall competence.

You must be deemed competent in all assessment items in order to be awarded your qualification,

including demonstrating competency in:

• all of the exam questions

• the written assignment.

‘Not yet competent’ and resubmissions

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This written assignment is your opportunity to demonstrate your competency against these units:

Unit code Unit name DIPMB2 Complex

Lending and Broking

DIPMB3 Business

Management Skills

FNSFMB502 Identify and develop broking options for

clients with complex needs

Started Completed

FNSFMB503 Present broking options to clients with

complex needs

Started Completed

FNSFMB504 Implement complex loan structures Started Completed

FNSCUS501

Develop and nurture relationships with

clients, other professionals and third

party referrers

Started Completed

FNSPRM602 Improve the practice Started Completed

Note that the

Written Assignment is required to meet the requirements of the units of competency.

Page 5 of 27

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your written assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall competence.

You must be deemed competent in all assessment items in order to be awarded your qualification,

including demonstrating competency in:

• all of the exam questions

• the written assignment.

‘Not yet competent’ and resubmissions

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This written assignment is your opportunity to demonstrate your competency against these units:

Unit code Unit name DIPMB2 Complex

Lending and Broking

DIPMB3 Business

Management Skills

FNSFMB502 Identify and develop broking options for

clients with complex needs

Started Completed

FNSFMB503 Present broking options to clients with

complex needs

Started Completed

FNSFMB504 Implement complex loan structures Started Completed

FNSCUS501

Develop and nurture relationships with

clients, other professionals and third

party referrers

Started Completed

FNSPRM602 Improve the practice Started Completed

Note that the

Written Assignment is required to meet the requirements of the units of competency.

Page 5 of 27

We are here to help

If you have any questions about this written assignment you can post your query at the ‘Ask your Tutor’

forum in your subject room. You can expect an answer within 24 hours of your posting from one of our

technical advisers or student support staff.

Page 6 of 27

If you have any questions about this written assignment you can post your query at the ‘Ask your Tutor’

forum in your subject room. You can expect an answer within 24 hours of your posting from one of our

technical advisers or student support staff.

Page 6 of 27

Section 1: Case study A — Ray Murdoch and Steve Brown –

Commercial Equipment Finance

Background

You have just met with Ray Murdoch and Steve Brown, referred to you by another commercial client.

Ray Murdoch and Steve Brown jointly own a successful and growing business that manufactures metal

pallets. They trade under the name Pallets-R-Us Pty Ltd. The pallets are manufactured using material that is

lightweight and durable. There has also been a very structured approach to the research and development

for the engineering and design of the pallets. The pallets are used in all industry sectors. Part of the process

involves powder coating the finished product, which is currently outsourced to a local well-established

contractor.

It is critical that Ray and Steve’s product meets market needs. They need to maintain sustainable

production and operating costs if they are to forecast their sales and cost of sales.

They have a well-established client database that provides them with repeat ‘business-to-business’

dealings. While they have only been trading for 30 months, they have a solid business plan with written

supply contracts with three major business clients and several smaller business clients.

Ray and Steve now require finance to assist them with the purchase of a sophisticated machine, using the

technical platform system CNC. This machine can be programmed to rapidly fabricate multiple components.

The machine has an expected commercial lifespan of at least 15 years with operating software to be

updated every three years. This software and upgrades is included in the purchase price of $800,000.They

need to import the machine from the US. Initial enquiries with the US supplier have indicated that they will

require a letter of credit for the import of the machine.

Their business employs five people and, with the expected increase in business through the automation

of production, they have forecast that they will need to recruit an additional two staff members in the next

3–6 months to meet sales/production demands.

Ray has been in the metal fabrication field all his working life. He has an MBA and understands financial

management. He also has solid engineering skills and developed the majority of the design works for the

business. He is married and has no dependants. His wife is a school teacher and she will be retiring at the

end of the year.

Steve worked with Ray at ‘Protech’ as a foreman. His skills are in production and managing project/job

flow. He has high level technical skills and can complete works to specification at a high standard.

Steve and Ray have provided the last two years financial accounts for the trading business, as well as

interim accounts for the current financial year. Ray’s brother provided business with a loan $500,000 when

the business commenced and he is being repaid interest plus a principle repayment of $30,000 per annum.

Page 7 of 27

Commercial Equipment Finance

Background

You have just met with Ray Murdoch and Steve Brown, referred to you by another commercial client.

Ray Murdoch and Steve Brown jointly own a successful and growing business that manufactures metal

pallets. They trade under the name Pallets-R-Us Pty Ltd. The pallets are manufactured using material that is

lightweight and durable. There has also been a very structured approach to the research and development

for the engineering and design of the pallets. The pallets are used in all industry sectors. Part of the process

involves powder coating the finished product, which is currently outsourced to a local well-established

contractor.

It is critical that Ray and Steve’s product meets market needs. They need to maintain sustainable

production and operating costs if they are to forecast their sales and cost of sales.

They have a well-established client database that provides them with repeat ‘business-to-business’

dealings. While they have only been trading for 30 months, they have a solid business plan with written

supply contracts with three major business clients and several smaller business clients.

Ray and Steve now require finance to assist them with the purchase of a sophisticated machine, using the

technical platform system CNC. This machine can be programmed to rapidly fabricate multiple components.

The machine has an expected commercial lifespan of at least 15 years with operating software to be

updated every three years. This software and upgrades is included in the purchase price of $800,000.They

need to import the machine from the US. Initial enquiries with the US supplier have indicated that they will

require a letter of credit for the import of the machine.

Their business employs five people and, with the expected increase in business through the automation

of production, they have forecast that they will need to recruit an additional two staff members in the next

3–6 months to meet sales/production demands.

Ray has been in the metal fabrication field all his working life. He has an MBA and understands financial

management. He also has solid engineering skills and developed the majority of the design works for the

business. He is married and has no dependants. His wife is a school teacher and she will be retiring at the

end of the year.

Steve worked with Ray at ‘Protech’ as a foreman. His skills are in production and managing project/job

flow. He has high level technical skills and can complete works to specification at a high standard.

Steve and Ray have provided the last two years financial accounts for the trading business, as well as

interim accounts for the current financial year. Ray’s brother provided business with a loan $500,000 when

the business commenced and he is being repaid interest plus a principle repayment of $30,000 per annum.

Page 7 of 27

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

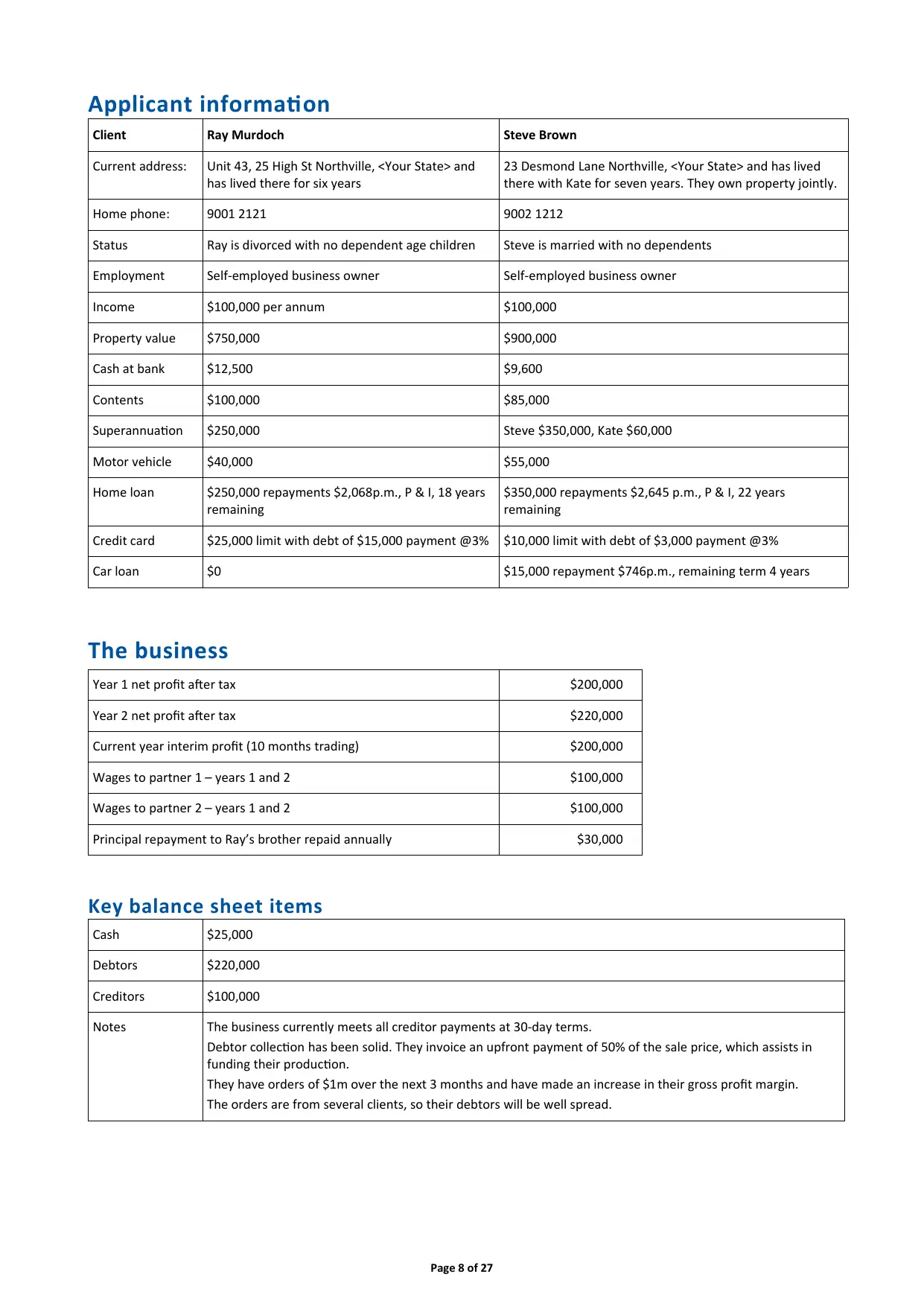

Applicant information

Client Ray Murdoch Steve Brown

Current address: Unit 43, 25 High St Northville, <Your State> and

has lived there for six years

23 Desmond Lane Northville, <Your State> and has lived

there with Kate for seven years. They own property jointly.

Home phone: 9001 2121 9002 1212

Status Ray is divorced with no dependent age children Steve is married with no dependents

Employment Self-employed business owner Self-employed business owner

Income $100,000 per annum $100,000

Property value $750,000 $900,000

Cash at bank $12,500 $9,600

Contents $100,000 $85,000

Superannuation $250,000 Steve $350,000, Kate $60,000

Motor vehicle $40,000 $55,000

Home loan $250,000 repayments $2,068p.m., P & I, 18 years

remaining

$350,000 repayments $2,645 p.m., P & I, 22 years

remaining

Credit card $25,000 limit with debt of $15,000 payment @3% $10,000 limit with debt of $3,000 payment @3%

Car loan $0 $15,000 repayment $746p.m., remaining term 4 years

The business

Year 1 net profit after tax $200,000

Year 2 net profit after tax $220,000

Current year interim profit (10 months trading) $200,000

Wages to partner 1 – years 1 and 2 $100,000

Wages to partner 2 – years 1 and 2 $100,000

Principal repayment to Ray’s brother repaid annually $30,000

Key balance sheet items

Cash $25,000

Debtors $220,000

Creditors $100,000

Notes The business currently meets all creditor payments at 30-day terms.

Debtor collection has been solid. They invoice an upfront payment of 50% of the sale price, which assists in

funding their production.

They have orders of $1m over the next 3 months and have made an increase in their gross profit margin.

The orders are from several clients, so their debtors will be well spread.

Page 8 of 27

Client Ray Murdoch Steve Brown

Current address: Unit 43, 25 High St Northville, <Your State> and

has lived there for six years

23 Desmond Lane Northville, <Your State> and has lived

there with Kate for seven years. They own property jointly.

Home phone: 9001 2121 9002 1212

Status Ray is divorced with no dependent age children Steve is married with no dependents

Employment Self-employed business owner Self-employed business owner

Income $100,000 per annum $100,000

Property value $750,000 $900,000

Cash at bank $12,500 $9,600

Contents $100,000 $85,000

Superannuation $250,000 Steve $350,000, Kate $60,000

Motor vehicle $40,000 $55,000

Home loan $250,000 repayments $2,068p.m., P & I, 18 years

remaining

$350,000 repayments $2,645 p.m., P & I, 22 years

remaining

Credit card $25,000 limit with debt of $15,000 payment @3% $10,000 limit with debt of $3,000 payment @3%

Car loan $0 $15,000 repayment $746p.m., remaining term 4 years

The business

Year 1 net profit after tax $200,000

Year 2 net profit after tax $220,000

Current year interim profit (10 months trading) $200,000

Wages to partner 1 – years 1 and 2 $100,000

Wages to partner 2 – years 1 and 2 $100,000

Principal repayment to Ray’s brother repaid annually $30,000

Key balance sheet items

Cash $25,000

Debtors $220,000

Creditors $100,000

Notes The business currently meets all creditor payments at 30-day terms.

Debtor collection has been solid. They invoice an upfront payment of 50% of the sale price, which assists in

funding their production.

They have orders of $1m over the next 3 months and have made an increase in their gross profit margin.

The orders are from several clients, so their debtors will be well spread.

Page 8 of 27

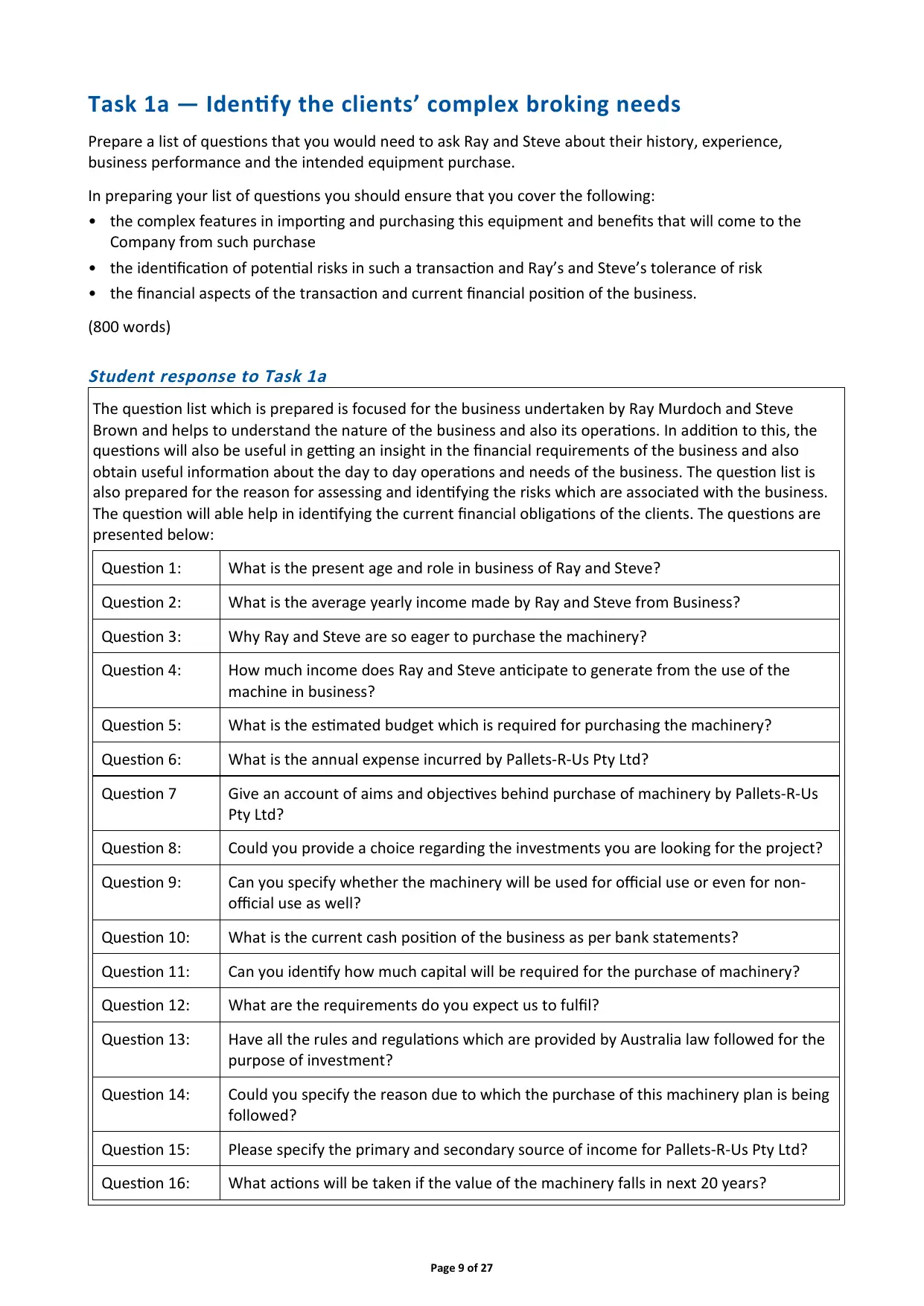

Task 1a — Identify the clients’ complex broking needs

Prepare a list of questions that you would need to ask Ray and Steve about their history, experience,

business performance and the intended equipment purchase.

In preparing your list of questions you should ensure that you cover the following:

• the complex features in importing and purchasing this equipment and benefits that will come to the

Company from such purchase

• the identification of potential risks in such a transaction and Ray’s and Steve’s tolerance of risk

• the financial aspects of the transaction and current financial position of the business.

(800 words)

Student response to Task 1a

The question list which is prepared is focused for the business undertaken by Ray Murdoch and Steve

Brown and helps to understand the nature of the business and also its operations. In addition to this, the

questions will also be useful in getting an insight in the financial requirements of the business and also

obtain useful information about the day to day operations and needs of the business. The question list is

also prepared for the reason for assessing and identifying the risks which are associated with the business.

The question will able help in identifying the current financial obligations of the clients. The questions are

presented below:

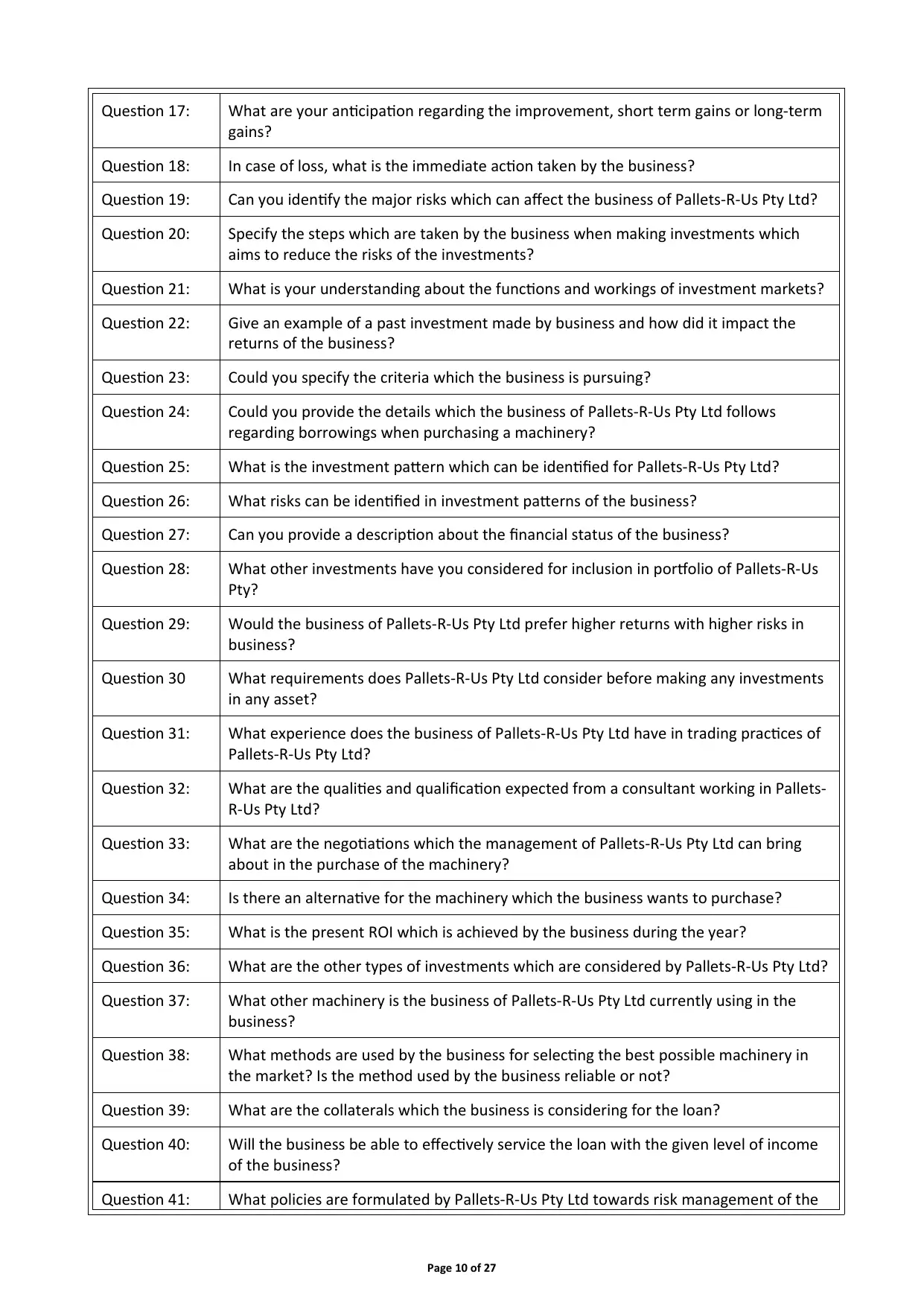

Question 1: What is the present age and role in business of Ray and Steve?

Question 2: What is the average yearly income made by Ray and Steve from Business?

Question 3: Why Ray and Steve are so eager to purchase the machinery?

Question 4: How much income does Ray and Steve anticipate to generate from the use of the

machine in business?

Question 5: What is the estimated budget which is required for purchasing the machinery?

Question 6: What is the annual expense incurred by Pallets-R-Us Pty Ltd?

Question 7 Give an account of aims and objectives behind purchase of machinery by Pallets-R-Us

Pty Ltd?

Question 8: Could you provide a choice regarding the investments you are looking for the project?

Question 9: Can you specify whether the machinery will be used for official use or even for non-

official use as well?

Question 10: What is the current cash position of the business as per bank statements?

Question 11: Can you identify how much capital will be required for the purchase of machinery?

Question 12: What are the requirements do you expect us to fulfil?

Question 13: Have all the rules and regulations which are provided by Australia law followed for the

purpose of investment?

Question 14: Could you specify the reason due to which the purchase of this machinery plan is being

followed?

Question 15: Please specify the primary and secondary source of income for Pallets-R-Us Pty Ltd?

Question 16: What actions will be taken if the value of the machinery falls in next 20 years?

Page 9 of 27

Prepare a list of questions that you would need to ask Ray and Steve about their history, experience,

business performance and the intended equipment purchase.

In preparing your list of questions you should ensure that you cover the following:

• the complex features in importing and purchasing this equipment and benefits that will come to the

Company from such purchase

• the identification of potential risks in such a transaction and Ray’s and Steve’s tolerance of risk

• the financial aspects of the transaction and current financial position of the business.

(800 words)

Student response to Task 1a

The question list which is prepared is focused for the business undertaken by Ray Murdoch and Steve

Brown and helps to understand the nature of the business and also its operations. In addition to this, the

questions will also be useful in getting an insight in the financial requirements of the business and also

obtain useful information about the day to day operations and needs of the business. The question list is

also prepared for the reason for assessing and identifying the risks which are associated with the business.

The question will able help in identifying the current financial obligations of the clients. The questions are

presented below:

Question 1: What is the present age and role in business of Ray and Steve?

Question 2: What is the average yearly income made by Ray and Steve from Business?

Question 3: Why Ray and Steve are so eager to purchase the machinery?

Question 4: How much income does Ray and Steve anticipate to generate from the use of the

machine in business?

Question 5: What is the estimated budget which is required for purchasing the machinery?

Question 6: What is the annual expense incurred by Pallets-R-Us Pty Ltd?

Question 7 Give an account of aims and objectives behind purchase of machinery by Pallets-R-Us

Pty Ltd?

Question 8: Could you provide a choice regarding the investments you are looking for the project?

Question 9: Can you specify whether the machinery will be used for official use or even for non-

official use as well?

Question 10: What is the current cash position of the business as per bank statements?

Question 11: Can you identify how much capital will be required for the purchase of machinery?

Question 12: What are the requirements do you expect us to fulfil?

Question 13: Have all the rules and regulations which are provided by Australia law followed for the

purpose of investment?

Question 14: Could you specify the reason due to which the purchase of this machinery plan is being

followed?

Question 15: Please specify the primary and secondary source of income for Pallets-R-Us Pty Ltd?

Question 16: What actions will be taken if the value of the machinery falls in next 20 years?

Page 9 of 27

Question 17: What are your anticipation regarding the improvement, short term gains or long-term

gains?

Question 18: In case of loss, what is the immediate action taken by the business?

Question 19: Can you identify the major risks which can affect the business of Pallets-R-Us Pty Ltd?

Question 20: Specify the steps which are taken by the business when making investments which

aims to reduce the risks of the investments?

Question 21: What is your understanding about the functions and workings of investment markets?

Question 22: Give an example of a past investment made by business and how did it impact the

returns of the business?

Question 23: Could you specify the criteria which the business is pursuing?

Question 24: Could you provide the details which the business of Pallets-R-Us Pty Ltd follows

regarding borrowings when purchasing a machinery?

Question 25: What is the investment pattern which can be identified for Pallets-R-Us Pty Ltd?

Question 26: What risks can be identified in investment patterns of the business?

Question 27: Can you provide a description about the financial status of the business?

Question 28: What other investments have you considered for inclusion in portfolio of Pallets-R-Us

Pty?

Question 29: Would the business of Pallets-R-Us Pty Ltd prefer higher returns with higher risks in

business?

Question 30 What requirements does Pallets-R-Us Pty Ltd consider before making any investments

in any asset?

Question 31: What experience does the business of Pallets-R-Us Pty Ltd have in trading practices of

Pallets-R-Us Pty Ltd?

Question 32: What are the qualities and qualification expected from a consultant working in Pallets-

R-Us Pty Ltd?

Question 33: What are the negotiations which the management of Pallets-R-Us Pty Ltd can bring

about in the purchase of the machinery?

Question 34: Is there an alternative for the machinery which the business wants to purchase?

Question 35: What is the present ROI which is achieved by the business during the year?

Question 36: What are the other types of investments which are considered by Pallets-R-Us Pty Ltd?

Question 37: What other machinery is the business of Pallets-R-Us Pty Ltd currently using in the

business?

Question 38: What methods are used by the business for selecting the best possible machinery in

the market? Is the method used by the business reliable or not?

Question 39: What are the collaterals which the business is considering for the loan?

Question 40: Will the business be able to effectively service the loan with the given level of income

of the business?

Question 41: What policies are formulated by Pallets-R-Us Pty Ltd towards risk management of the

Page 10 of 27

gains?

Question 18: In case of loss, what is the immediate action taken by the business?

Question 19: Can you identify the major risks which can affect the business of Pallets-R-Us Pty Ltd?

Question 20: Specify the steps which are taken by the business when making investments which

aims to reduce the risks of the investments?

Question 21: What is your understanding about the functions and workings of investment markets?

Question 22: Give an example of a past investment made by business and how did it impact the

returns of the business?

Question 23: Could you specify the criteria which the business is pursuing?

Question 24: Could you provide the details which the business of Pallets-R-Us Pty Ltd follows

regarding borrowings when purchasing a machinery?

Question 25: What is the investment pattern which can be identified for Pallets-R-Us Pty Ltd?

Question 26: What risks can be identified in investment patterns of the business?

Question 27: Can you provide a description about the financial status of the business?

Question 28: What other investments have you considered for inclusion in portfolio of Pallets-R-Us

Pty?

Question 29: Would the business of Pallets-R-Us Pty Ltd prefer higher returns with higher risks in

business?

Question 30 What requirements does Pallets-R-Us Pty Ltd consider before making any investments

in any asset?

Question 31: What experience does the business of Pallets-R-Us Pty Ltd have in trading practices of

Pallets-R-Us Pty Ltd?

Question 32: What are the qualities and qualification expected from a consultant working in Pallets-

R-Us Pty Ltd?

Question 33: What are the negotiations which the management of Pallets-R-Us Pty Ltd can bring

about in the purchase of the machinery?

Question 34: Is there an alternative for the machinery which the business wants to purchase?

Question 35: What is the present ROI which is achieved by the business during the year?

Question 36: What are the other types of investments which are considered by Pallets-R-Us Pty Ltd?

Question 37: What other machinery is the business of Pallets-R-Us Pty Ltd currently using in the

business?

Question 38: What methods are used by the business for selecting the best possible machinery in

the market? Is the method used by the business reliable or not?

Question 39: What are the collaterals which the business is considering for the loan?

Question 40: Will the business be able to effectively service the loan with the given level of income

of the business?

Question 41: What policies are formulated by Pallets-R-Us Pty Ltd towards risk management of the

Page 10 of 27

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

business?

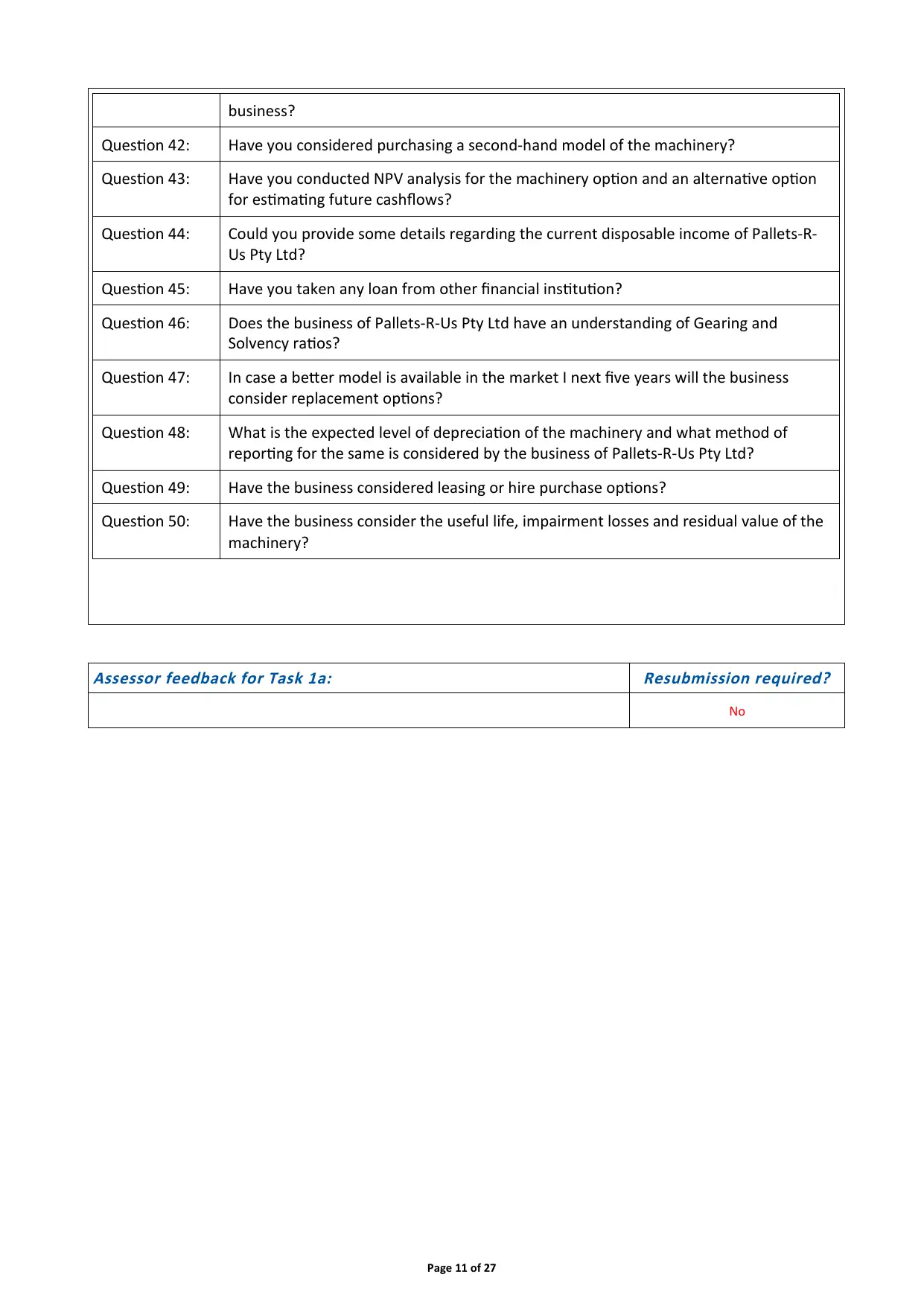

Question 42: Have you considered purchasing a second-hand model of the machinery?

Question 43: Have you conducted NPV analysis for the machinery option and an alternative option

for estimating future cashflows?

Question 44: Could you provide some details regarding the current disposable income of Pallets-R-

Us Pty Ltd?

Question 45: Have you taken any loan from other financial institution?

Question 46: Does the business of Pallets-R-Us Pty Ltd have an understanding of Gearing and

Solvency ratios?

Question 47: In case a better model is available in the market I next five years will the business

consider replacement options?

Question 48: What is the expected level of depreciation of the machinery and what method of

reporting for the same is considered by the business of Pallets-R-Us Pty Ltd?

Question 49: Have the business considered leasing or hire purchase options?

Question 50: Have the business consider the useful life, impairment losses and residual value of the

machinery?

Assessor feedback for Task 1a:

Resubmission required?

No

Page 11 of 27

Question 42: Have you considered purchasing a second-hand model of the machinery?

Question 43: Have you conducted NPV analysis for the machinery option and an alternative option

for estimating future cashflows?

Question 44: Could you provide some details regarding the current disposable income of Pallets-R-

Us Pty Ltd?

Question 45: Have you taken any loan from other financial institution?

Question 46: Does the business of Pallets-R-Us Pty Ltd have an understanding of Gearing and

Solvency ratios?

Question 47: In case a better model is available in the market I next five years will the business

consider replacement options?

Question 48: What is the expected level of depreciation of the machinery and what method of

reporting for the same is considered by the business of Pallets-R-Us Pty Ltd?

Question 49: Have the business considered leasing or hire purchase options?

Question 50: Have the business consider the useful life, impairment losses and residual value of the

machinery?

Assessor feedback for Task 1a:

Resubmission required?

No

Page 11 of 27

Task 2a —Develop complex broking options

You are required to prepare a full report addressed to Ray and Steve outlining available loan options; the

process and the risks (potential and real) of which they should be made aware.

In a suitable report format you should cover the following:

1. the parties to the loan

2. outline the type of letter of credit (LC) likely to be used, the parties to the LC and the high-level steps

involved in setting up and establishing LC to enable import of the equipment

3. the product options that are available to finance an equipment purchase once it has arrived in Australia

4. your recommendation of best product option, including amount, security/collateral, term, potential

interest rate and residual value (if any)

5. name three (3) lenders that would consider and potentially approve this transaction and advise Ray

and Steve about product type, loan term, interest rate, balloon payment (if applicable) and monthly

repayment they offer

6. the procedure to commence the import of the equipment and the loan, including documentation Ray

and Steve need to provide

7. the client responsibilities, so Steve and Ray fully understand the facility being proposed

8. outline the risks (potential and real) of which Ray and Steve should be made aware

9. whether personal guarantee will be required from the Director’s spouse

10. a summary of all fees and charges — including those for setup and those of the lender

11. advise which relevant disclosures need to be made

12. a request for client to inform you of any questions about the transaction and/or provide an

instruction to proceed.

(800 words)

Notes: Any assumptions you make should be listed, and not be in conflict with the case study information

already provided.

You are to write a report to your clients, demonstrating your professional writing skill — not simply

commenting on each of the points detailed above.

The use of tables in the report to set out some of the numeric information may be of benefit.

Student response to Task 2a

Dear Ray and Steve

You are both the owners of Pallets-R-Us Pty Ltd and the company is jointly owned by both of

you. The business intends to achieve financial aid to purchase the machinery which can bring

about improvement in the operations of the business.

The report aims to provide insights regarding the risks which the business can face while

purchasing the machinery and also considers the applicability of loan provision which can be

made available to the business. The report also shows the available resources of the business

and the various loan schemes which the business can use. The report also considers possible

sources of loan which the business can apply from and the details for the same are explained

below:

Pallets-R-Us Pty Ltd Year 1 Year 2

Net profit after tax $200,000 $220,000

Page 12 of 27

You are required to prepare a full report addressed to Ray and Steve outlining available loan options; the

process and the risks (potential and real) of which they should be made aware.

In a suitable report format you should cover the following:

1. the parties to the loan

2. outline the type of letter of credit (LC) likely to be used, the parties to the LC and the high-level steps

involved in setting up and establishing LC to enable import of the equipment

3. the product options that are available to finance an equipment purchase once it has arrived in Australia

4. your recommendation of best product option, including amount, security/collateral, term, potential

interest rate and residual value (if any)

5. name three (3) lenders that would consider and potentially approve this transaction and advise Ray

and Steve about product type, loan term, interest rate, balloon payment (if applicable) and monthly

repayment they offer

6. the procedure to commence the import of the equipment and the loan, including documentation Ray

and Steve need to provide

7. the client responsibilities, so Steve and Ray fully understand the facility being proposed

8. outline the risks (potential and real) of which Ray and Steve should be made aware

9. whether personal guarantee will be required from the Director’s spouse

10. a summary of all fees and charges — including those for setup and those of the lender

11. advise which relevant disclosures need to be made

12. a request for client to inform you of any questions about the transaction and/or provide an

instruction to proceed.

(800 words)

Notes: Any assumptions you make should be listed, and not be in conflict with the case study information

already provided.

You are to write a report to your clients, demonstrating your professional writing skill — not simply

commenting on each of the points detailed above.

The use of tables in the report to set out some of the numeric information may be of benefit.

Student response to Task 2a

Dear Ray and Steve

You are both the owners of Pallets-R-Us Pty Ltd and the company is jointly owned by both of

you. The business intends to achieve financial aid to purchase the machinery which can bring

about improvement in the operations of the business.

The report aims to provide insights regarding the risks which the business can face while

purchasing the machinery and also considers the applicability of loan provision which can be

made available to the business. The report also shows the available resources of the business

and the various loan schemes which the business can use. The report also considers possible

sources of loan which the business can apply from and the details for the same are explained

below:

Pallets-R-Us Pty Ltd Year 1 Year 2

Net profit after tax $200,000 $220,000

Page 12 of 27

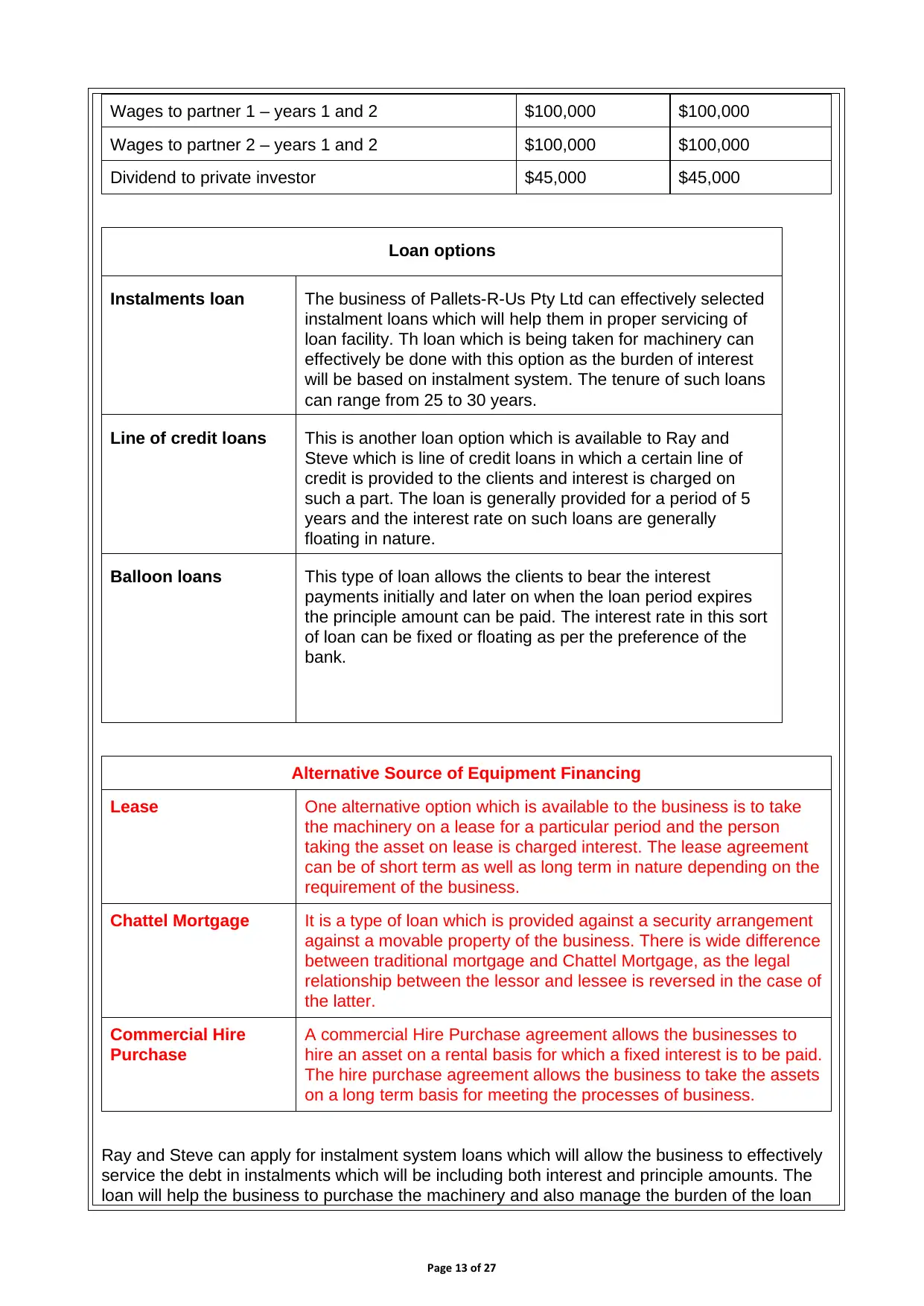

Wages to partner 1 – years 1 and 2 $100,000 $100,000

Wages to partner 2 – years 1 and 2 $100,000 $100,000

Dividend to private investor $45,000 $45,000

Loan options

Instalments loan The business of Pallets-R-Us Pty Ltd can effectively selected

instalment loans which will help them in proper servicing of

loan facility. Th loan which is being taken for machinery can

effectively be done with this option as the burden of interest

will be based on instalment system. The tenure of such loans

can range from 25 to 30 years.

Line of credit loans This is another loan option which is available to Ray and

Steve which is line of credit loans in which a certain line of

credit is provided to the clients and interest is charged on

such a part. The loan is generally provided for a period of 5

years and the interest rate on such loans are generally

floating in nature.

Balloon loans This type of loan allows the clients to bear the interest

payments initially and later on when the loan period expires

the principle amount can be paid. The interest rate in this sort

of loan can be fixed or floating as per the preference of the

bank.

Alternative Source of Equipment Financing

Lease One alternative option which is available to the business is to take

the machinery on a lease for a particular period and the person

taking the asset on lease is charged interest. The lease agreement

can be of short term as well as long term in nature depending on the

requirement of the business.

Chattel Mortgage It is a type of loan which is provided against a security arrangement

against a movable property of the business. There is wide difference

between traditional mortgage and Chattel Mortgage, as the legal

relationship between the lessor and lessee is reversed in the case of

the latter.

Commercial Hire

Purchase

A commercial Hire Purchase agreement allows the businesses to

hire an asset on a rental basis for which a fixed interest is to be paid.

The hire purchase agreement allows the business to take the assets

on a long term basis for meeting the processes of business.

Ray and Steve can apply for instalment system loans which will allow the business to effectively

service the debt in instalments which will be including both interest and principle amounts. The

loan will help the business to purchase the machinery and also manage the burden of the loan

Page 13 of 27

Wages to partner 2 – years 1 and 2 $100,000 $100,000

Dividend to private investor $45,000 $45,000

Loan options

Instalments loan The business of Pallets-R-Us Pty Ltd can effectively selected

instalment loans which will help them in proper servicing of

loan facility. Th loan which is being taken for machinery can

effectively be done with this option as the burden of interest

will be based on instalment system. The tenure of such loans

can range from 25 to 30 years.

Line of credit loans This is another loan option which is available to Ray and

Steve which is line of credit loans in which a certain line of

credit is provided to the clients and interest is charged on

such a part. The loan is generally provided for a period of 5

years and the interest rate on such loans are generally

floating in nature.

Balloon loans This type of loan allows the clients to bear the interest

payments initially and later on when the loan period expires

the principle amount can be paid. The interest rate in this sort

of loan can be fixed or floating as per the preference of the

bank.

Alternative Source of Equipment Financing

Lease One alternative option which is available to the business is to take

the machinery on a lease for a particular period and the person

taking the asset on lease is charged interest. The lease agreement

can be of short term as well as long term in nature depending on the

requirement of the business.

Chattel Mortgage It is a type of loan which is provided against a security arrangement

against a movable property of the business. There is wide difference

between traditional mortgage and Chattel Mortgage, as the legal

relationship between the lessor and lessee is reversed in the case of

the latter.

Commercial Hire

Purchase

A commercial Hire Purchase agreement allows the businesses to

hire an asset on a rental basis for which a fixed interest is to be paid.

The hire purchase agreement allows the business to take the assets

on a long term basis for meeting the processes of business.

Ray and Steve can apply for instalment system loans which will allow the business to effectively

service the debt in instalments which will be including both interest and principle amounts. The

loan will help the business to purchase the machinery and also manage the burden of the loan

Page 13 of 27

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

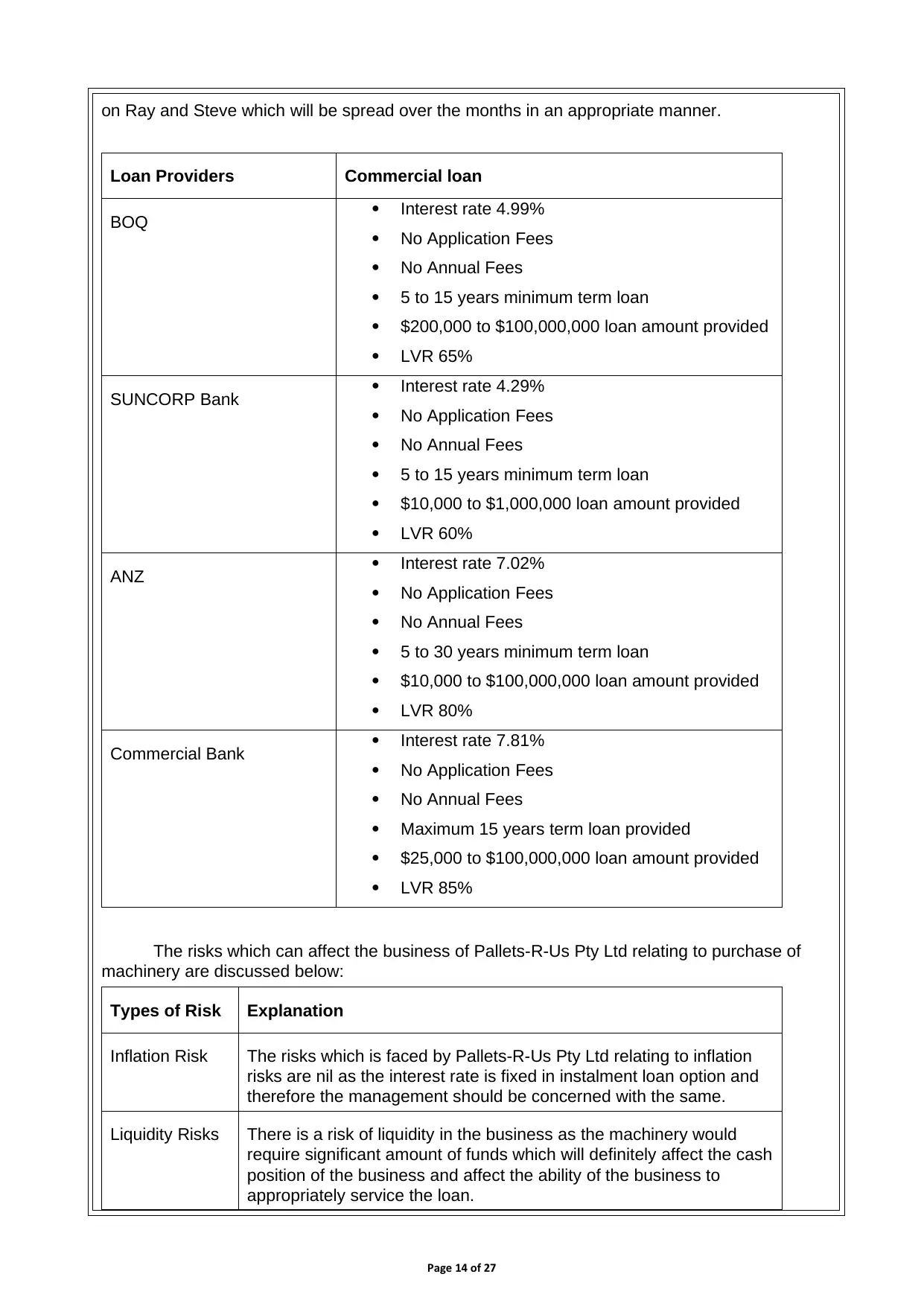

on Ray and Steve which will be spread over the months in an appropriate manner.

Loan Providers Commercial loan

BOQ Interest rate 4.99%

No Application Fees

No Annual Fees

5 to 15 years minimum term loan

$200,000 to $100,000,000 loan amount provided

LVR 65%

SUNCORP Bank Interest rate 4.29%

No Application Fees

No Annual Fees

5 to 15 years minimum term loan

$10,000 to $1,000,000 loan amount provided

LVR 60%

ANZ Interest rate 7.02%

No Application Fees

No Annual Fees

5 to 30 years minimum term loan

$10,000 to $100,000,000 loan amount provided

LVR 80%

Commercial Bank Interest rate 7.81%

No Application Fees

No Annual Fees

Maximum 15 years term loan provided

$25,000 to $100,000,000 loan amount provided

LVR 85%

The risks which can affect the business of Pallets-R-Us Pty Ltd relating to purchase of

machinery are discussed below:

Types of Risk Explanation

Inflation Risk The risks which is faced by Pallets-R-Us Pty Ltd relating to inflation

risks are nil as the interest rate is fixed in instalment loan option and

therefore the management should be concerned with the same.

Liquidity Risks There is a risk of liquidity in the business as the machinery would

require significant amount of funds which will definitely affect the cash

position of the business and affect the ability of the business to

appropriately service the loan.

Page 14 of 27

Loan Providers Commercial loan

BOQ Interest rate 4.99%

No Application Fees

No Annual Fees

5 to 15 years minimum term loan

$200,000 to $100,000,000 loan amount provided

LVR 65%

SUNCORP Bank Interest rate 4.29%

No Application Fees

No Annual Fees

5 to 15 years minimum term loan

$10,000 to $1,000,000 loan amount provided

LVR 60%

ANZ Interest rate 7.02%

No Application Fees

No Annual Fees

5 to 30 years minimum term loan

$10,000 to $100,000,000 loan amount provided

LVR 80%

Commercial Bank Interest rate 7.81%

No Application Fees

No Annual Fees

Maximum 15 years term loan provided

$25,000 to $100,000,000 loan amount provided

LVR 85%

The risks which can affect the business of Pallets-R-Us Pty Ltd relating to purchase of

machinery are discussed below:

Types of Risk Explanation

Inflation Risk The risks which is faced by Pallets-R-Us Pty Ltd relating to inflation

risks are nil as the interest rate is fixed in instalment loan option and

therefore the management should be concerned with the same.

Liquidity Risks There is a risk of liquidity in the business as the machinery would

require significant amount of funds which will definitely affect the cash

position of the business and affect the ability of the business to

appropriately service the loan.

Page 14 of 27

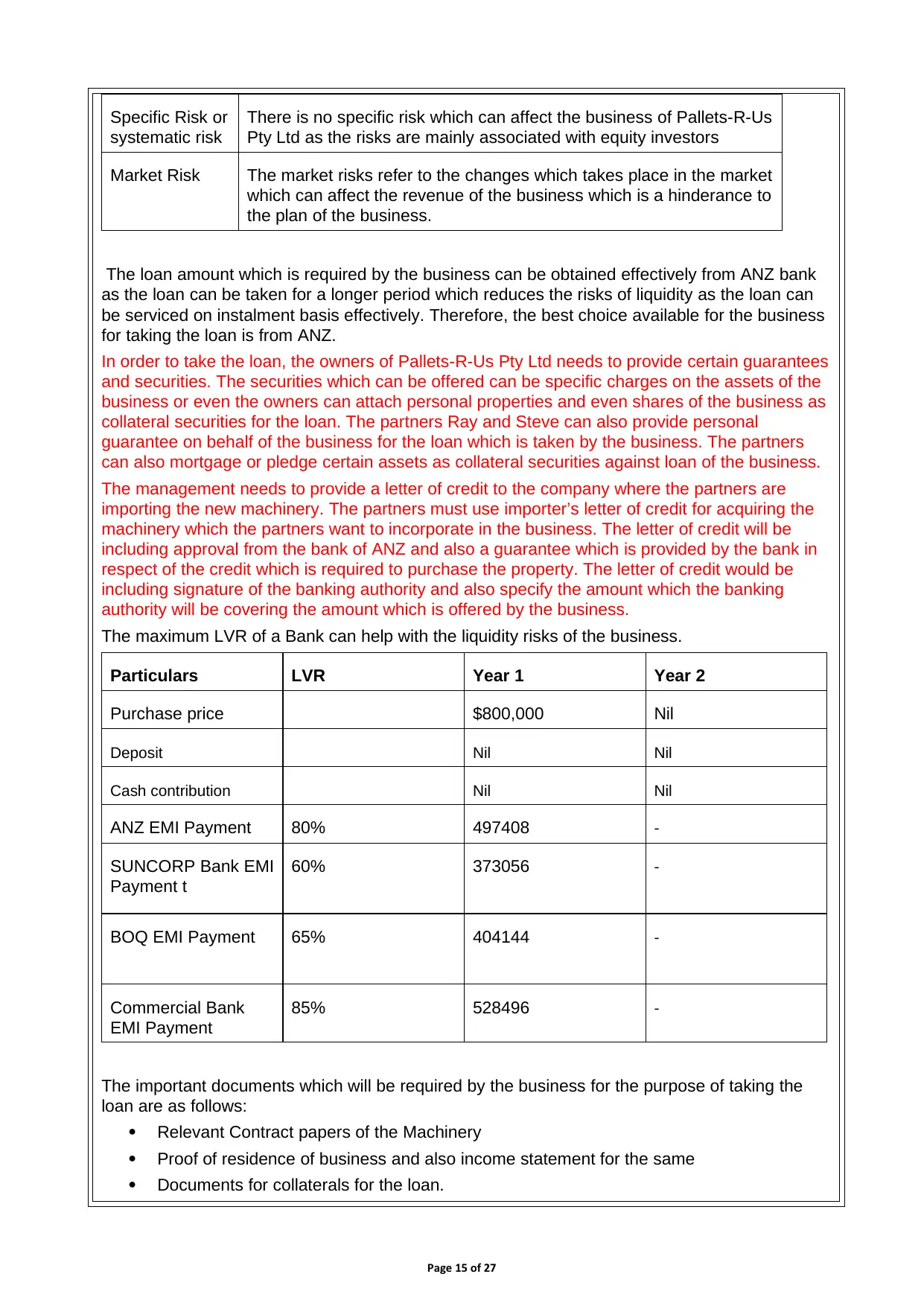

Specific Risk or

systematic risk

There is no specific risk which can affect the business of Pallets-R-Us

Pty Ltd as the risks are mainly associated with equity investors

Market Risk The market risks refer to the changes which takes place in the market

which can affect the revenue of the business which is a hinderance to

the plan of the business.

The loan amount which is required by the business can be obtained effectively from ANZ bank

as the loan can be taken for a longer period which reduces the risks of liquidity as the loan can

be serviced on instalment basis effectively. Therefore, the best choice available for the business

for taking the loan is from ANZ.

In order to take the loan, the owners of Pallets-R-Us Pty Ltd needs to provide certain guarantees

and securities. The securities which can be offered can be specific charges on the assets of the

business or even the owners can attach personal properties and even shares of the business as

collateral securities for the loan. The partners Ray and Steve can also provide personal

guarantee on behalf of the business for the loan which is taken by the business. The partners

can also mortgage or pledge certain assets as collateral securities against loan of the business.

The management needs to provide a letter of credit to the company where the partners are

importing the new machinery. The partners must use importer’s letter of credit for acquiring the

machinery which the partners want to incorporate in the business. The letter of credit will be

including approval from the bank of ANZ and also a guarantee which is provided by the bank in

respect of the credit which is required to purchase the property. The letter of credit would be

including signature of the banking authority and also specify the amount which the banking

authority will be covering the amount which is offered by the business.

The maximum LVR of a Bank can help with the liquidity risks of the business.

Particulars LVR Year 1 Year 2

Purchase price $800,000 Nil

Deposit Nil Nil

Cash contribution Nil Nil

ANZ EMI Payment 80% 497408 -

SUNCORP Bank EMI

Payment t

60% 373056 -

BOQ EMI Payment 65% 404144 -

Commercial Bank

EMI Payment

85% 528496 -

The important documents which will be required by the business for the purpose of taking the

loan are as follows:

Relevant Contract papers of the Machinery

Proof of residence of business and also income statement for the same

Documents for collaterals for the loan.

Page 15 of 27

systematic risk

There is no specific risk which can affect the business of Pallets-R-Us

Pty Ltd as the risks are mainly associated with equity investors

Market Risk The market risks refer to the changes which takes place in the market

which can affect the revenue of the business which is a hinderance to

the plan of the business.

The loan amount which is required by the business can be obtained effectively from ANZ bank

as the loan can be taken for a longer period which reduces the risks of liquidity as the loan can

be serviced on instalment basis effectively. Therefore, the best choice available for the business

for taking the loan is from ANZ.

In order to take the loan, the owners of Pallets-R-Us Pty Ltd needs to provide certain guarantees

and securities. The securities which can be offered can be specific charges on the assets of the

business or even the owners can attach personal properties and even shares of the business as

collateral securities for the loan. The partners Ray and Steve can also provide personal

guarantee on behalf of the business for the loan which is taken by the business. The partners

can also mortgage or pledge certain assets as collateral securities against loan of the business.

The management needs to provide a letter of credit to the company where the partners are

importing the new machinery. The partners must use importer’s letter of credit for acquiring the

machinery which the partners want to incorporate in the business. The letter of credit will be

including approval from the bank of ANZ and also a guarantee which is provided by the bank in

respect of the credit which is required to purchase the property. The letter of credit would be

including signature of the banking authority and also specify the amount which the banking

authority will be covering the amount which is offered by the business.

The maximum LVR of a Bank can help with the liquidity risks of the business.

Particulars LVR Year 1 Year 2

Purchase price $800,000 Nil

Deposit Nil Nil

Cash contribution Nil Nil

ANZ EMI Payment 80% 497408 -

SUNCORP Bank EMI

Payment t

60% 373056 -

BOQ EMI Payment 65% 404144 -

Commercial Bank

EMI Payment

85% 528496 -

The important documents which will be required by the business for the purpose of taking the

loan are as follows:

Relevant Contract papers of the Machinery

Proof of residence of business and also income statement for the same

Documents for collaterals for the loan.

Page 15 of 27

The business will be applying for the loan and the bank will take consideration for following:

Analyse how much the business can borrow

Calculate the cost of loan

Investigate the machinery investment option for which the loan is being taken.

Award pre-approval for the loan

The steps which can be taken are:

Determine the interest rate for the loan

Determine the time period for the loan

The expiry period of the loan also needs to be determined.

Client Responsibilities

You will be responsible for paying a portion of the principle loan amount along with

interest amount.

You are also responsible for informing the lender regarding changes in address, changes

in payment schedule.

State Revenue Requirements

Stamp duty

Import taxes and also other taxes.

The following documents needs to be provided to the lender as a proof and assurance for the

loan:

The financial statement of the business including interim statements showing current

performance for the year.

A copy of the bank statement to show the cash position of the business which needs to

how last 3 months

The income tax returns of the business and any other lease agreements and any current

loan document.

Track record of the personnel and also financial information regarding the same is also to

be provided.

The registration certificate and also the license to operate in business are also

demanded by the lenders.

In order to sanction the loan amount, the lender also needs a guarantor who can vouch for the

owners Ray and Steve and in case of any default on their parts will be held responsible for the

loan amount. The guarantor can be the spouses of the owners or any other individual.

The suggest list of lenders for the loan amount are:

ANZ bank

BOQ bank

Suncorp bank.

I shall be remunerated by the owners in form of commission payable which will be disclosed

after an appropriate option is selected. The commission will be payable after appropriate option

is selected by the business.

Assessor feedback for Task 2a:

Resubmission required?

No

Page 16 of 27

Analyse how much the business can borrow

Calculate the cost of loan

Investigate the machinery investment option for which the loan is being taken.

Award pre-approval for the loan

The steps which can be taken are:

Determine the interest rate for the loan

Determine the time period for the loan

The expiry period of the loan also needs to be determined.

Client Responsibilities

You will be responsible for paying a portion of the principle loan amount along with

interest amount.

You are also responsible for informing the lender regarding changes in address, changes

in payment schedule.

State Revenue Requirements

Stamp duty

Import taxes and also other taxes.

The following documents needs to be provided to the lender as a proof and assurance for the

loan:

The financial statement of the business including interim statements showing current

performance for the year.

A copy of the bank statement to show the cash position of the business which needs to

how last 3 months

The income tax returns of the business and any other lease agreements and any current

loan document.

Track record of the personnel and also financial information regarding the same is also to

be provided.

The registration certificate and also the license to operate in business are also

demanded by the lenders.

In order to sanction the loan amount, the lender also needs a guarantor who can vouch for the

owners Ray and Steve and in case of any default on their parts will be held responsible for the

loan amount. The guarantor can be the spouses of the owners or any other individual.

The suggest list of lenders for the loan amount are:

ANZ bank

BOQ bank

Suncorp bank.

I shall be remunerated by the owners in form of commission payable which will be disclosed

after an appropriate option is selected. The commission will be payable after appropriate option

is selected by the business.

Assessor feedback for Task 2a:

Resubmission required?

No

Page 16 of 27

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Task 3a — Implement complex loan structures

Ray and Steve have accepted your recommendations and have given you authority to proceed with their

application.

As part of implementing their loan application you are required to prepare a formal written loan

submission to the lender for pre-approval. Your loan submission must include the following:

• details of borrower, guarantors and all contact details

• borrowers background

• an overview of the proposal — what the finance is for

• the proposed structure of the facility being recommended — product type, deposit amount (if required),

loan amount, term, interest rate and residual value (if any)

• full details of the security/collateral that is to be provided

• serviceability calculations including Debt Service Cover Ratio (DSCR) calculations, including all personal

borrowing facilities of the directors

• provide a ‘funds-to-complete’ table including statutory costs and any relevant fees

• highlight the relevant risks — industry, business, transactional — and how they are mitigated

• any other information that is relevant to assist the lender provide an approval

• your comments and recommendations

• list attachments

(800 words)

Notes: Any assumptions you make should be listed, and not be in conflict with the case study information

already provided.

You are to write a formal submission to the lender; not simply commenting on each of the points detailed

above.

The use of tables in the report, to set out some of the numeric information, may be of benefit.

Student response to Task 3a

The important information which are available for the business are shown below in a table form

showing the net profit for the current year in case of the borrower:

Pallets-R-Us Pty Ltd Year 1 Year 2

Net profit after tax $200,000 $220,000

Wages to partner 1 – years 1 and 2 $100,000 $100,000

Wages to partner 2 – years 1 and 2 $100,000 $100,000

Dividend to private investor $45,000 $45,000

Borrowing Entity: Pallets-R-Us Pty Ltd

ABN & A.C.N:

Address: Unit 43, 25 High St Northville

Phone: 9001 2121

Fax: NA

Mobile: NA

Date of birth: NA

Page 17 of 27

Ray and Steve have accepted your recommendations and have given you authority to proceed with their

application.

As part of implementing their loan application you are required to prepare a formal written loan

submission to the lender for pre-approval. Your loan submission must include the following:

• details of borrower, guarantors and all contact details

• borrowers background

• an overview of the proposal — what the finance is for

• the proposed structure of the facility being recommended — product type, deposit amount (if required),

loan amount, term, interest rate and residual value (if any)

• full details of the security/collateral that is to be provided

• serviceability calculations including Debt Service Cover Ratio (DSCR) calculations, including all personal

borrowing facilities of the directors

• provide a ‘funds-to-complete’ table including statutory costs and any relevant fees

• highlight the relevant risks — industry, business, transactional — and how they are mitigated

• any other information that is relevant to assist the lender provide an approval

• your comments and recommendations

• list attachments

(800 words)

Notes: Any assumptions you make should be listed, and not be in conflict with the case study information

already provided.

You are to write a formal submission to the lender; not simply commenting on each of the points detailed

above.

The use of tables in the report, to set out some of the numeric information, may be of benefit.

Student response to Task 3a

The important information which are available for the business are shown below in a table form

showing the net profit for the current year in case of the borrower:

Pallets-R-Us Pty Ltd Year 1 Year 2

Net profit after tax $200,000 $220,000

Wages to partner 1 – years 1 and 2 $100,000 $100,000

Wages to partner 2 – years 1 and 2 $100,000 $100,000

Dividend to private investor $45,000 $45,000

Borrowing Entity: Pallets-R-Us Pty Ltd

ABN & A.C.N:

Address: Unit 43, 25 High St Northville

Phone: 9001 2121

Fax: NA

Mobile: NA

Date of birth: NA

Page 17 of 27

Loan Amount: $800,000

Purpose of the loan

The main intention behind taking the loan for the business is to finance the requirement of a

machinery which will improve the efficiency of operations. The machine is to be imported from

outside the country and so appropriate funding is necessary. The loan will help Ray and Steve to

purchase the machinery and also provide some stability to the liquidity situation of the business.

Funding Position

The requirement of loan is for the purpose of purchasing the machinery for the business and also

improving the liquidity situation of the business. The loan down payments are to be made in

instalments and therefore the same does not affect the liquidity position of the business. In order to

maintain the liquidity position, rate of interest, operating expenditure also play a vital role.

Security

The data which is provided by the business are checked by NCCP for viability purposes and also

provide a basis for the lenders to assess whether they should provide loan facilities or not to the

client based on the credit rating of the client. NCCP takes enquiry of loan amounts and also check

track record for servicing of loan for Pallets-R-Us Pty Ltd.

Description of Machinery

The purchase price of the Machinery is estimated to be $ 800,000 for which the owners intend to

take financial assistance from a lender. The machine is to be imported from a foreign country. This

machine can be programmed to rapidly fabricate multiple components. The machine has an

expected commercial lifespan of at least 15 years with operating software to be updated every

three years. The machine is needed to be imported from the US. Initial enquiries with the US

supplier have indicated that they will require a letter of credit for the import of the machine.

Repayment structure of the New Entity

The loan repayment structure focuses on different requirement of the loan which the business

needs to fulfil. Some of the requirement which needs to be fulfilled are OSR requirement, ATO

Consideration, State Legislations. These requirements are applicable to the business and therefore

must be fulfilled

OSR requirements: The OSR helps in making distinction between the instruments

which are used for the purpose of recognizing the duty

payables which are there on agreement of loans.

Furthermore, the OSR additionally helps in distinguishing the

proceedings of the court and loan, which may be given to the

moneylenders.

It likewise helps in having agreements of loan and the same is

also helpful in property valuation.

The choices which are made relating to OSR helps in

demonstrating the legitimacy of loan offerings to clients..

ATO Considerations: The ATO considerations viably give relative rules, which

could be utilized by financial institutions to decide on

Page 18 of 27

Purpose of the loan

The main intention behind taking the loan for the business is to finance the requirement of a

machinery which will improve the efficiency of operations. The machine is to be imported from

outside the country and so appropriate funding is necessary. The loan will help Ray and Steve to

purchase the machinery and also provide some stability to the liquidity situation of the business.

Funding Position

The requirement of loan is for the purpose of purchasing the machinery for the business and also

improving the liquidity situation of the business. The loan down payments are to be made in

instalments and therefore the same does not affect the liquidity position of the business. In order to

maintain the liquidity position, rate of interest, operating expenditure also play a vital role.

Security

The data which is provided by the business are checked by NCCP for viability purposes and also

provide a basis for the lenders to assess whether they should provide loan facilities or not to the

client based on the credit rating of the client. NCCP takes enquiry of loan amounts and also check

track record for servicing of loan for Pallets-R-Us Pty Ltd.

Description of Machinery

The purchase price of the Machinery is estimated to be $ 800,000 for which the owners intend to

take financial assistance from a lender. The machine is to be imported from a foreign country. This

machine can be programmed to rapidly fabricate multiple components. The machine has an

expected commercial lifespan of at least 15 years with operating software to be updated every

three years. The machine is needed to be imported from the US. Initial enquiries with the US

supplier have indicated that they will require a letter of credit for the import of the machine.

Repayment structure of the New Entity

The loan repayment structure focuses on different requirement of the loan which the business

needs to fulfil. Some of the requirement which needs to be fulfilled are OSR requirement, ATO

Consideration, State Legislations. These requirements are applicable to the business and therefore

must be fulfilled

OSR requirements: The OSR helps in making distinction between the instruments

which are used for the purpose of recognizing the duty

payables which are there on agreement of loans.

Furthermore, the OSR additionally helps in distinguishing the

proceedings of the court and loan, which may be given to the

moneylenders.

It likewise helps in having agreements of loan and the same is

also helpful in property valuation.

The choices which are made relating to OSR helps in

demonstrating the legitimacy of loan offerings to clients..

ATO Considerations: The ATO considerations viably give relative rules, which

could be utilized by financial institutions to decide on

Page 18 of 27

sufficient advances of loans.

It likewise incorporates relative standards, which may be

considered while assessing the loan credibility of the

lenders.

Particulars LVR Property 1

ANZ EMI Payment 80% = 621760 * 80%

= 497408 loan amount

SUNCORP Bank

EMI Payment t

60% = 621760* 60%

= 373056 loan amount

BOQ EMI Payment 65% = 621760* 65%

= 404144 loan amount

Commercial Bank

EMI Payment

85% = 621760* 85%

= 528496 loan amount

Serviceability Calculations:

The serviceability calculations consider the loan amount which is paid and in relation to the same

the various fees which is incurred by the client business.

Sale Price: $800,000

Stamp Duty: $38800

Lodgement fee: $6500

Transaction fee: $10

Property Valuation review fees: 200

Total: $45,510

Recommendation

The business which is operated by Ray and Steve can utilize the loan option and take the same

from ANZ bank on a instalment payment basis. This loan taken will help the management to

purchase the machinery which will definitely improve the efficiency of the business and also the

production capacity of the business which implies that the profitability of the business will also

increase. It is recommended that the management should move forward with its plan and select

instalment loan system.

Assessor feedback for Task 3a:

Resubmission required?

No

Page 19 of 27

It likewise incorporates relative standards, which may be

considered while assessing the loan credibility of the

lenders.

Particulars LVR Property 1

ANZ EMI Payment 80% = 621760 * 80%