Financial Resource Management and Decision Making for ABC Ltd (Report)

VerifiedAdded on 2020/01/16

|15

|5094

|267

Report

AI Summary

This report examines the financial requirements and management strategies of ABC Ltd, a small-sized retail store. It delves into identifying various sources of capital, including equity financing, bank loans, and asset sales, assessing their implications on the firm. The report highlights the significance of financial planning, budgeting, and investment appraisal techniques like payback period and discounted cash flow. It analyzes the impact of financing sources on financial statements, including the income statement and balance sheet. Furthermore, the report explores the preparation of budgets and their analysis for optimal decisions, alongside unit cost and pricing strategies. The financial performance of Hilton Hotel & Group is also examined and compared with Marriott. The report concludes with an analysis of financial statements using financial ratios to assess the financial health of the business.

MANAGING FINANCIAL

RESOURCES AND

DECISIONS

1

RESOURCES AND

DECISIONS

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTROUCTION...................................................................................................................................3

1.1 Available source for financing the business...............................................................................3

1.2 Assessing various implications of financing sources on firm....................................................4

1.3 Selection of the most appropriate retail store.............................................................................4

TASK 2.................................................................................................................................................5

2.1 Cost of various sources of finances............................................................................................5

2.2 Significance of financial planning in a business........................................................................5

2.3 Informations needed for financing decision makers..................................................................6

2.4 Impact of finance sources on the financial statements...............................................................6

TASK 3.................................................................................................................................................7

3.1 Preparing budgets and its analysis for the best decisions...........................................................7

3.2 Unit cost and pricing decisions..................................................................................................7

3.3 Investment appraisal techniques applications............................................................................8

TASK 4...............................................................................................................................................10

4.1 Types of financial statements...................................................................................................10

4.2 Final accounts differences in different organizations...............................................................11

4.3 Analysis financial statements using financial ratios.................................................................11

CONCLUSION..................................................................................................................................12

2

INTROUCTION...................................................................................................................................3

1.1 Available source for financing the business...............................................................................3

1.2 Assessing various implications of financing sources on firm....................................................4

1.3 Selection of the most appropriate retail store.............................................................................4

TASK 2.................................................................................................................................................5

2.1 Cost of various sources of finances............................................................................................5

2.2 Significance of financial planning in a business........................................................................5

2.3 Informations needed for financing decision makers..................................................................6

2.4 Impact of finance sources on the financial statements...............................................................6

TASK 3.................................................................................................................................................7

3.1 Preparing budgets and its analysis for the best decisions...........................................................7

3.2 Unit cost and pricing decisions..................................................................................................7

3.3 Investment appraisal techniques applications............................................................................8

TASK 4...............................................................................................................................................10

4.1 Types of financial statements...................................................................................................10

4.2 Final accounts differences in different organizations...............................................................11

4.3 Analysis financial statements using financial ratios.................................................................11

CONCLUSION..................................................................................................................................12

2

INTROUCTION

Now-a-days, financial decisions becomes the key or central element of the business success

which assist entrepreneurs to generate sufficient amount of capital and utilize it optimally for

accomplishing the goals. In UK, small and medium sized enterprises make substantial contribution

to the growth and success of the country. Therefore, the assignment is prepared here to examine the

financial requirement of a small sized retail store named ABC Ltd to deliver excellent retailing

services to the people. The report will emphasize on identifying distinguish sources of capital to

meet corporate funding needs. Furthermore, it will present the various key decisions like costing,

pricing, long-term investment decisions etc. for the proper functionality. Lastly, a well-established

and leading hotelier, Hilton Hotel & Group’s financial performance will be examined and compared

with the rivalry Marriott.

TASK 1

1.1 Available source for financing the business

In the corporate world, finance takes very important place and the corporations needs the

respective resources in proper and adequate manner. When the ABC Ltd. has not adequate finance

then there are various kinds of sources are available which provide such kind of services to it. In

context to this, various types of sources of finance which are available are such as follows:

Sale of assets: It is an internal source of finance where the company raise fund using

internal condition of the firm (Brigham and Ehrhardt, 2013). As per the source the ABC Ltd. sale

it's those assets and equipments which are unused and unproductive for the firm. After selling the

assets whatever sum of money comes is to be use in business expansion.

Equity financing: Another source of finance is equity which is mostly used external

financing source by the firms. In this the company issues it's shares in the stock market which are

purchased by the shareholders. Further, investment which is made by the investors is to be used by

the business entity for expanding the firm.

Bank loan: It is also external financing source which provides financial resources and

services to the company for expanding the firm in another market. Here the management has to

fulfil all the process of applying loan and then bank determine valuation of it. After that the ABC

Ltd. able to raise fund easily in the market. It is little costly and risky as compare to equity

financing.

3

Now-a-days, financial decisions becomes the key or central element of the business success

which assist entrepreneurs to generate sufficient amount of capital and utilize it optimally for

accomplishing the goals. In UK, small and medium sized enterprises make substantial contribution

to the growth and success of the country. Therefore, the assignment is prepared here to examine the

financial requirement of a small sized retail store named ABC Ltd to deliver excellent retailing

services to the people. The report will emphasize on identifying distinguish sources of capital to

meet corporate funding needs. Furthermore, it will present the various key decisions like costing,

pricing, long-term investment decisions etc. for the proper functionality. Lastly, a well-established

and leading hotelier, Hilton Hotel & Group’s financial performance will be examined and compared

with the rivalry Marriott.

TASK 1

1.1 Available source for financing the business

In the corporate world, finance takes very important place and the corporations needs the

respective resources in proper and adequate manner. When the ABC Ltd. has not adequate finance

then there are various kinds of sources are available which provide such kind of services to it. In

context to this, various types of sources of finance which are available are such as follows:

Sale of assets: It is an internal source of finance where the company raise fund using

internal condition of the firm (Brigham and Ehrhardt, 2013). As per the source the ABC Ltd. sale

it's those assets and equipments which are unused and unproductive for the firm. After selling the

assets whatever sum of money comes is to be use in business expansion.

Equity financing: Another source of finance is equity which is mostly used external

financing source by the firms. In this the company issues it's shares in the stock market which are

purchased by the shareholders. Further, investment which is made by the investors is to be used by

the business entity for expanding the firm.

Bank loan: It is also external financing source which provides financial resources and

services to the company for expanding the firm in another market. Here the management has to

fulfil all the process of applying loan and then bank determine valuation of it. After that the ABC

Ltd. able to raise fund easily in the market. It is little costly and risky as compare to equity

financing.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

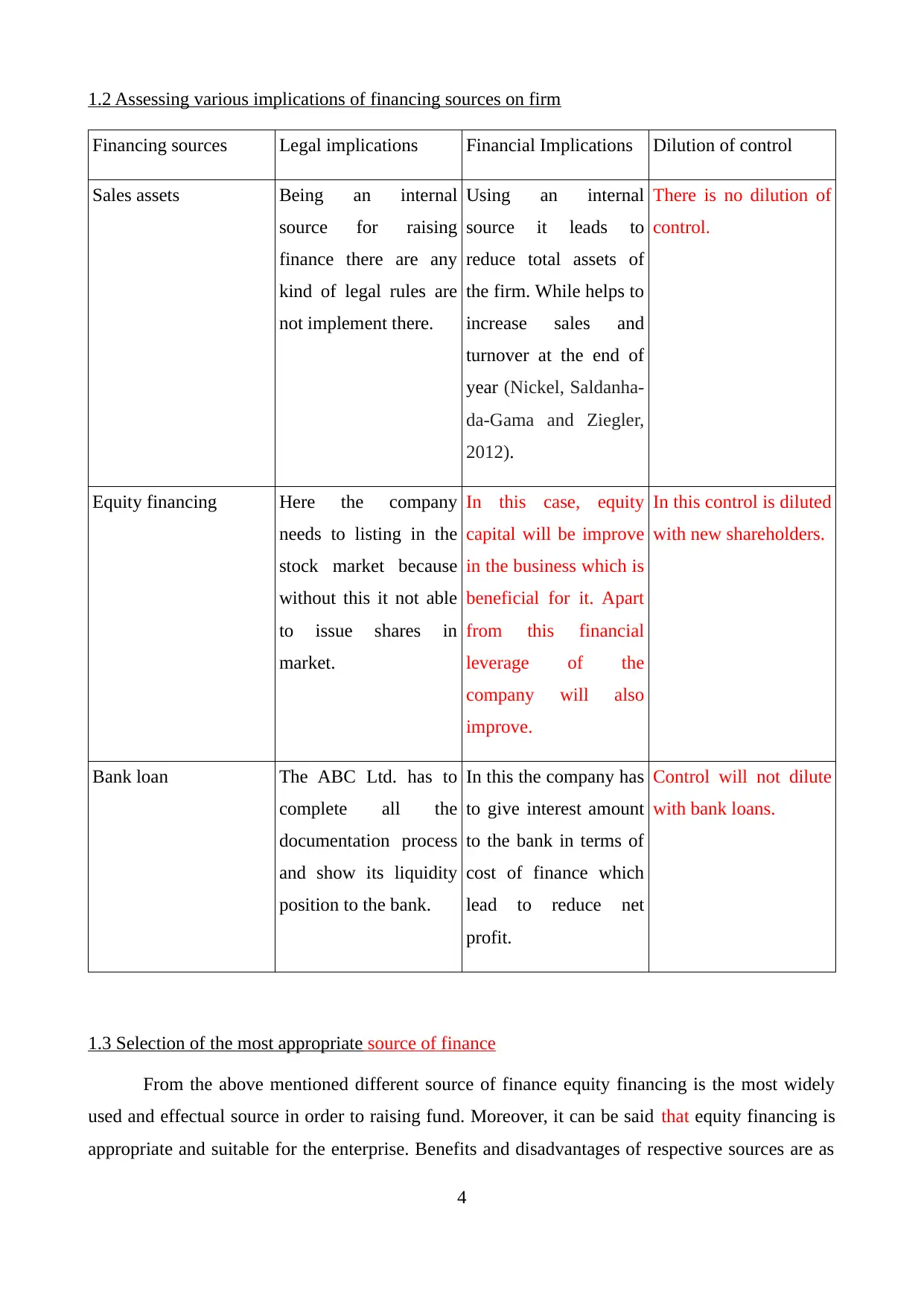

1.2 Assessing various implications of financing sources on firm

Financing sources Legal implications Financial Implications Dilution of control

Sales assets Being an internal

source for raising

finance there are any

kind of legal rules are

not implement there.

Using an internal

source it leads to

reduce total assets of

the firm. While helps to

increase sales and

turnover at the end of

year (Nickel, Saldanha-

da-Gama and Ziegler,

2012).

There is no dilution of

control.

Equity financing Here the company

needs to listing in the

stock market because

without this it not able

to issue shares in

market.

In this case, equity

capital will be improve

in the business which is

beneficial for it. Apart

from this financial

leverage of the

company will also

improve.

In this control is diluted

with new shareholders.

Bank loan The ABC Ltd. has to

complete all the

documentation process

and show its liquidity

position to the bank.

In this the company has

to give interest amount

to the bank in terms of

cost of finance which

lead to reduce net

profit.

Control will not dilute

with bank loans.

1.3 Selection of the most appropriate source of finance

From the above mentioned different source of finance equity financing is the most widely

used and effectual source in order to raising fund. Moreover, it can be said that equity financing is

appropriate and suitable for the enterprise. Benefits and disadvantages of respective sources are as

4

Financing sources Legal implications Financial Implications Dilution of control

Sales assets Being an internal

source for raising

finance there are any

kind of legal rules are

not implement there.

Using an internal

source it leads to

reduce total assets of

the firm. While helps to

increase sales and

turnover at the end of

year (Nickel, Saldanha-

da-Gama and Ziegler,

2012).

There is no dilution of

control.

Equity financing Here the company

needs to listing in the

stock market because

without this it not able

to issue shares in

market.

In this case, equity

capital will be improve

in the business which is

beneficial for it. Apart

from this financial

leverage of the

company will also

improve.

In this control is diluted

with new shareholders.

Bank loan The ABC Ltd. has to

complete all the

documentation process

and show its liquidity

position to the bank.

In this the company has

to give interest amount

to the bank in terms of

cost of finance which

lead to reduce net

profit.

Control will not dilute

with bank loans.

1.3 Selection of the most appropriate source of finance

From the above mentioned different source of finance equity financing is the most widely

used and effectual source in order to raising fund. Moreover, it can be said that equity financing is

appropriate and suitable for the enterprise. Benefits and disadvantages of respective sources are as

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

below:

Advantages: Very main benefit of the equity is that the company able to raise fund whenever

it wants without valuing firm in the retail industry of UK. Further, the ABC Ltd. Company is able to

increase market presence and enhance level of capital in the business. Along with this cost of

finance is very low as compare to another financing sources (Brigham and Ehrhardt, 2013).

Limitations: When the company going to issue shares then it needs to listing in the stock

market. Because without listing it cannot issue shares in the market which lead to reduce capital

raising. In addition to this, it has to provide dividend amount to the potential stockholders on yearly

basis by which profit level get affected.

TASK 2

2.1 Cost of various sources of finances

There are variety of sources that can be used by the business, every sources has some

financial cost towards the business. With reference to the selected retail business, it will incur

following financial cost on various financial sources, mentioned hereunder:

Bank borrowings: Getting loans from banks bring obligations to ABC ltd to pay a fixed

interest charge inclusive installment as the cost. It has one benefit that is tax benefit which offer

opportunity to ABC Ltd to minimize taxation burden.

Share capital: It bring dividend obligations to the business which is required to be paid by

ABC Ltd to investors for the risk undertaken by investing their capital. Unlike debt, it does not offer

any tax benefits to the ABC Ltd (Drechsler and Natter, 2012).

Hire purchase: Vendor provide flexible payment facilities to the buyer through deciding

periodical installments which includes some interest charges.

Leasing: On leasing, ABC Ltd needs to make interest payment to the lessor for the services

provided and it is the financial cost of leasing.

2.2 Significance of financial planning in a business

Financial planning is a process of devising plans, policies and financial strategies for

accomplishing financial targets. The significance of financial plan is provided here as under:

ABC Ltd managers can create the best capital structure through making a right combination

of fixed and fluctuating source of capital for the cost management and profit enhancement.

5

Advantages: Very main benefit of the equity is that the company able to raise fund whenever

it wants without valuing firm in the retail industry of UK. Further, the ABC Ltd. Company is able to

increase market presence and enhance level of capital in the business. Along with this cost of

finance is very low as compare to another financing sources (Brigham and Ehrhardt, 2013).

Limitations: When the company going to issue shares then it needs to listing in the stock

market. Because without listing it cannot issue shares in the market which lead to reduce capital

raising. In addition to this, it has to provide dividend amount to the potential stockholders on yearly

basis by which profit level get affected.

TASK 2

2.1 Cost of various sources of finances

There are variety of sources that can be used by the business, every sources has some

financial cost towards the business. With reference to the selected retail business, it will incur

following financial cost on various financial sources, mentioned hereunder:

Bank borrowings: Getting loans from banks bring obligations to ABC ltd to pay a fixed

interest charge inclusive installment as the cost. It has one benefit that is tax benefit which offer

opportunity to ABC Ltd to minimize taxation burden.

Share capital: It bring dividend obligations to the business which is required to be paid by

ABC Ltd to investors for the risk undertaken by investing their capital. Unlike debt, it does not offer

any tax benefits to the ABC Ltd (Drechsler and Natter, 2012).

Hire purchase: Vendor provide flexible payment facilities to the buyer through deciding

periodical installments which includes some interest charges.

Leasing: On leasing, ABC Ltd needs to make interest payment to the lessor for the services

provided and it is the financial cost of leasing.

2.2 Significance of financial planning in a business

Financial planning is a process of devising plans, policies and financial strategies for

accomplishing financial targets. The significance of financial plan is provided here as under:

ABC Ltd managers can create the best capital structure through making a right combination

of fixed and fluctuating source of capital for the cost management and profit enhancement.

5

Not only the collection of funds, but its effective and efficient utilization is too important,

therefore, through making an excellent plan, ABC Ltd can use their funds in an optimal

manner and minimize cost.

Budgetary planning is the part of it that enable ABC Ltd to get standard revenue & control

operations for the effective cost management (Greene, Brush and Brown, 2015).

It provide financial safety and security through maintaining surplus funds at each and every

point of time to meet urgencies.

It provide an assurance against dramatically and drastic change in market environment like

sudden market volatility, shortage of material, high cost of transportation and so on.

2.3 Informations needed for financing decision makers

When the ABC limited company raising fund from internal as well as external sources then

the respective sources needs different kinds of information data. Various decision makers require

several kinds of informations are such as related to company’s financial performance, valuation,

reputation etc. When performance of the firm is higher and better in the retail industry then decision

makers attract to invest more money in that firm which helps to expand organisation up to greater

extent. In regarding to this, external decision makers are needs to take data and informations

regarding financial conditions. Because higher the level of profit provide more return to the

investors (Healy and Palepu, 2012).

Key decision makers are such as partners, venture capitalists, banks, share or stock market

and those financials who provide finance and fund to the company. They require very basic and key

information of the company is such as its profitability and credibility in the industry. Further, the

bank seeks towards business valuation in the overall market and industry where it operates. In

addition to this, venture capitalist require information related to the return on investment ratio as

well as profit of the firm. Moreover, stock market need information which are related to the profit

and investor ratios. Because higher the profit and investor ratio provide more amount of return on

the investment made by shareholders.

2.4 Impact of finance sources on the financial statements

Every financial source is reported and properly disclosed in the financial statements,

therefore, it will impact the financial statements of the business in following manner:

Interest cost is shown under the income statement which in turn decrease net return of the

firm. ABC Ltd will need to disclose interest payment before deduction of tax liabilities, therefore, it

6

therefore, through making an excellent plan, ABC Ltd can use their funds in an optimal

manner and minimize cost.

Budgetary planning is the part of it that enable ABC Ltd to get standard revenue & control

operations for the effective cost management (Greene, Brush and Brown, 2015).

It provide financial safety and security through maintaining surplus funds at each and every

point of time to meet urgencies.

It provide an assurance against dramatically and drastic change in market environment like

sudden market volatility, shortage of material, high cost of transportation and so on.

2.3 Informations needed for financing decision makers

When the ABC limited company raising fund from internal as well as external sources then

the respective sources needs different kinds of information data. Various decision makers require

several kinds of informations are such as related to company’s financial performance, valuation,

reputation etc. When performance of the firm is higher and better in the retail industry then decision

makers attract to invest more money in that firm which helps to expand organisation up to greater

extent. In regarding to this, external decision makers are needs to take data and informations

regarding financial conditions. Because higher the level of profit provide more return to the

investors (Healy and Palepu, 2012).

Key decision makers are such as partners, venture capitalists, banks, share or stock market

and those financials who provide finance and fund to the company. They require very basic and key

information of the company is such as its profitability and credibility in the industry. Further, the

bank seeks towards business valuation in the overall market and industry where it operates. In

addition to this, venture capitalist require information related to the return on investment ratio as

well as profit of the firm. Moreover, stock market need information which are related to the profit

and investor ratios. Because higher the profit and investor ratio provide more amount of return on

the investment made by shareholders.

2.4 Impact of finance sources on the financial statements

Every financial source is reported and properly disclosed in the financial statements,

therefore, it will impact the financial statements of the business in following manner:

Interest cost is shown under the income statement which in turn decrease net return of the

firm. ABC Ltd will need to disclose interest payment before deduction of tax liabilities, therefore, it

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

minimizes the taxation burden and maximize net profitability. In balance sheet, it will reduce cash

& its equivalent as under the cash flow statement, it is shown as cash outflow from financing

activities because it is related to long-term fund collection like debt, lease, hire purchase and others.

On the other hand, debt collection is reported under long-term/non-current obligations and in assets,

cash balance improved.

In contrast, dividend payment is shown under the P&L account from the net profitability and

remainder is called retained profits. However, in the B/S, it is subtracted from the cash balance as it

reports as cash outflow from financing activities (Cambra-Fierro, Melero and Sese, 2015). In

against to this, share capital is reported under the head total equities which indicates excess of total

assets over liabilities.

Due to equity financing capital raises which lead to reduce gearing and debt to equity ratio

withing the company. On the basis of more finance financial stability of the business entity will be

imporve in the industry up to greater extent. Hence, it can be said that through equity financing firm

will be able to recover and fulfil amount of debt and create psoitive impact on the balance sheet.

Bank loan affects on the balance sheet in negative as well as positive both ways of the

company. When firm raise fund through the bank loan then long term debt will increase in the

balance sheet of the entity which lead to enhance total liabilities. On the other side capital will be

raise due to which total assets and financial stability improves and impact positively on the balance

sheet.

TASK 3

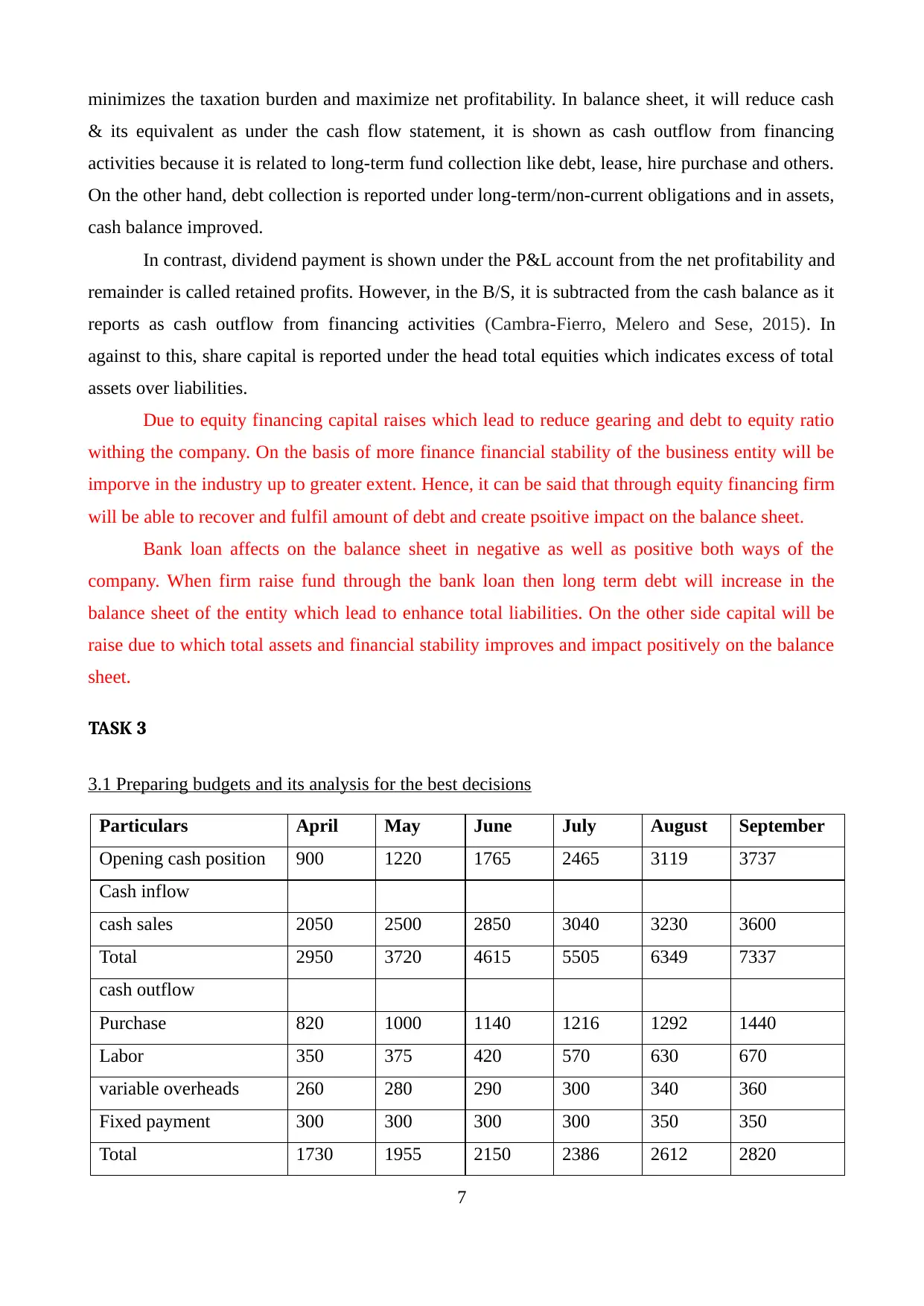

3.1 Preparing budgets and its analysis for the best decisions

Particulars April May June July August September

Opening cash position 900 1220 1765 2465 3119 3737

Cash inflow

cash sales 2050 2500 2850 3040 3230 3600

Total 2950 3720 4615 5505 6349 7337

cash outflow

Purchase 820 1000 1140 1216 1292 1440

Labor 350 375 420 570 630 670

variable overheads 260 280 290 300 340 360

Fixed payment 300 300 300 300 350 350

Total 1730 1955 2150 2386 2612 2820

7

& its equivalent as under the cash flow statement, it is shown as cash outflow from financing

activities because it is related to long-term fund collection like debt, lease, hire purchase and others.

On the other hand, debt collection is reported under long-term/non-current obligations and in assets,

cash balance improved.

In contrast, dividend payment is shown under the P&L account from the net profitability and

remainder is called retained profits. However, in the B/S, it is subtracted from the cash balance as it

reports as cash outflow from financing activities (Cambra-Fierro, Melero and Sese, 2015). In

against to this, share capital is reported under the head total equities which indicates excess of total

assets over liabilities.

Due to equity financing capital raises which lead to reduce gearing and debt to equity ratio

withing the company. On the basis of more finance financial stability of the business entity will be

imporve in the industry up to greater extent. Hence, it can be said that through equity financing firm

will be able to recover and fulfil amount of debt and create psoitive impact on the balance sheet.

Bank loan affects on the balance sheet in negative as well as positive both ways of the

company. When firm raise fund through the bank loan then long term debt will increase in the

balance sheet of the entity which lead to enhance total liabilities. On the other side capital will be

raise due to which total assets and financial stability improves and impact positively on the balance

sheet.

TASK 3

3.1 Preparing budgets and its analysis for the best decisions

Particulars April May June July August September

Opening cash position 900 1220 1765 2465 3119 3737

Cash inflow

cash sales 2050 2500 2850 3040 3230 3600

Total 2950 3720 4615 5505 6349 7337

cash outflow

Purchase 820 1000 1140 1216 1292 1440

Labor 350 375 420 570 630 670

variable overheads 260 280 290 300 340 360

Fixed payment 300 300 300 300 350 350

Total 1730 1955 2150 2386 2612 2820

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net cash position 1220 1765 2465 3119 3737 4517

Above cash budget analyzed that ABC Ltd’s cash inflow shows a rising trend as it goes from

2050 to 3600 in the last month. It happens because of high availability of disposable income to the

public, growing lifestyle and larger demand. In contrast, under the cash outflow, purchase remains

constant to 40% of turnover, it goes increased from 820 to 1440. However, labor’s wages shows a

sudden and drastic increase in July to 570 whereas variable shows increasing trend with the increase

in sales and fixed payments gone up in last two months to 350. Total cash outflow goes up from

1730 to 2820, and net cash position depicts a surplus plus growing trend throughout the years from

1220 to 4517.

Surplus cash indicates that expected revenue will exceed the total expenditures and enable

firm to meet their urgent financial requirement. ABC Ltd can utilize such cash availability in

prodcutive purpose like it can invest the capital in profitable investment opportunity to get favorable

return on it.

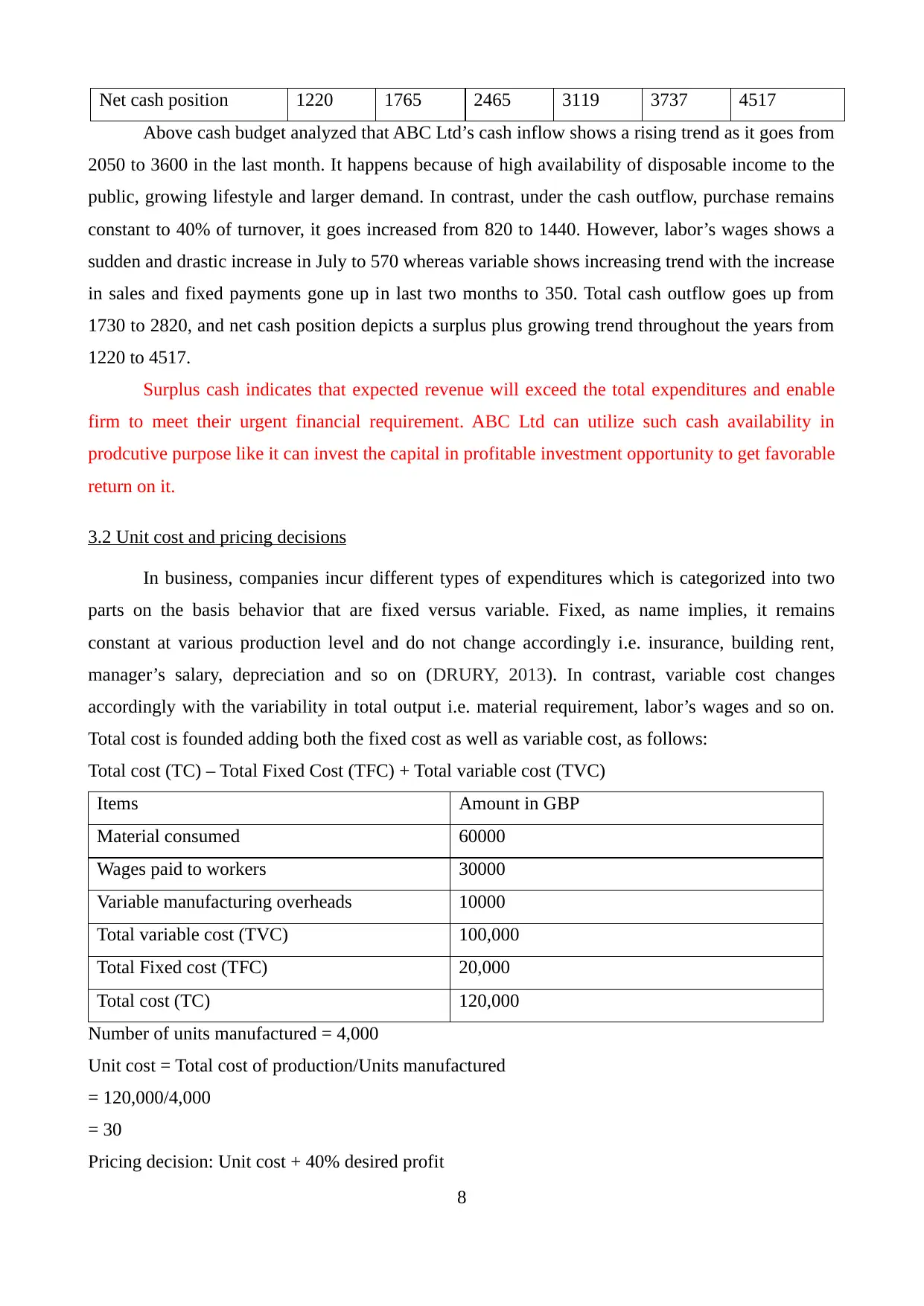

3.2 Unit cost and pricing decisions

In business, companies incur different types of expenditures which is categorized into two

parts on the basis behavior that are fixed versus variable. Fixed, as name implies, it remains

constant at various production level and do not change accordingly i.e. insurance, building rent,

manager’s salary, depreciation and so on (DRURY, 2013). In contrast, variable cost changes

accordingly with the variability in total output i.e. material requirement, labor’s wages and so on.

Total cost is founded adding both the fixed cost as well as variable cost, as follows:

Total cost (TC) – Total Fixed Cost (TFC) + Total variable cost (TVC)

Items Amount in GBP

Material consumed 60000

Wages paid to workers 30000

Variable manufacturing overheads 10000

Total variable cost (TVC) 100,000

Total Fixed cost (TFC) 20,000

Total cost (TC) 120,000

Number of units manufactured = 4,000

Unit cost = Total cost of production/Units manufactured

= 120,000/4,000

= 30

Pricing decision: Unit cost + 40% desired profit

8

Above cash budget analyzed that ABC Ltd’s cash inflow shows a rising trend as it goes from

2050 to 3600 in the last month. It happens because of high availability of disposable income to the

public, growing lifestyle and larger demand. In contrast, under the cash outflow, purchase remains

constant to 40% of turnover, it goes increased from 820 to 1440. However, labor’s wages shows a

sudden and drastic increase in July to 570 whereas variable shows increasing trend with the increase

in sales and fixed payments gone up in last two months to 350. Total cash outflow goes up from

1730 to 2820, and net cash position depicts a surplus plus growing trend throughout the years from

1220 to 4517.

Surplus cash indicates that expected revenue will exceed the total expenditures and enable

firm to meet their urgent financial requirement. ABC Ltd can utilize such cash availability in

prodcutive purpose like it can invest the capital in profitable investment opportunity to get favorable

return on it.

3.2 Unit cost and pricing decisions

In business, companies incur different types of expenditures which is categorized into two

parts on the basis behavior that are fixed versus variable. Fixed, as name implies, it remains

constant at various production level and do not change accordingly i.e. insurance, building rent,

manager’s salary, depreciation and so on (DRURY, 2013). In contrast, variable cost changes

accordingly with the variability in total output i.e. material requirement, labor’s wages and so on.

Total cost is founded adding both the fixed cost as well as variable cost, as follows:

Total cost (TC) – Total Fixed Cost (TFC) + Total variable cost (TVC)

Items Amount in GBP

Material consumed 60000

Wages paid to workers 30000

Variable manufacturing overheads 10000

Total variable cost (TVC) 100,000

Total Fixed cost (TFC) 20,000

Total cost (TC) 120,000

Number of units manufactured = 4,000

Unit cost = Total cost of production/Units manufactured

= 120,000/4,000

= 30

Pricing decision: Unit cost + 40% desired profit

8

= 30 + (30*40%)

= 30 + 12

= 42

Justification behind using 40% mark-up

Here, 40% desired target return has been taken using various components such as profit-

maximization objectives, customers willingness to pay, their economic situation, market trend,

growth in demand and competitors product pricing also. With the stated case, consumers are ready

to pay high prices for the quality offerings and has strong financail position. In addition, managers

are targeted to gain maximum return therefore, 40% desired profit mark-up is founded suitable.

At 40% mark-up on the total cost, retailer will have to charge 42 GBP for each unit. If entity

wish to earn greater return then he needs to charge higher rate than 40% or vice-versa for getting

adequate return and high success.

3.3 Investment appraisal techniques applications

Capital budgeting is one of the key technique that is used by the financial managers for the

financial planning & success. This tools will help retailer, ABC Ltd to determine that whether a firm

must invest or deny available investment opportunity for the business growth, expansion and

success.

Payback period:

This technique is the simplest method that find out the recovery period of beginning cost of

investment in a project. While dealing with mutually-exclusive projects, an investor must prefers a

project with shorter payback period or vice-versa (Greene, Brush and Brown, 2015).

Accounting rate of return;

This method just computes or quantifies the return percentage on the total initial investment.

Company always needs high return, therefore, prefers greater ARR.

Net present value:

It is the modern and also the best way of investment appraisal which discounts the cash flow

to address the impact of market uncertainties. Total of discounted cash flows over the beginning

cost of capital is called net present value.

Internal rate of return:

This method just find out the rate at where NPV does not exists, henceforth, there is neither

any return nor loss exists at that rate.

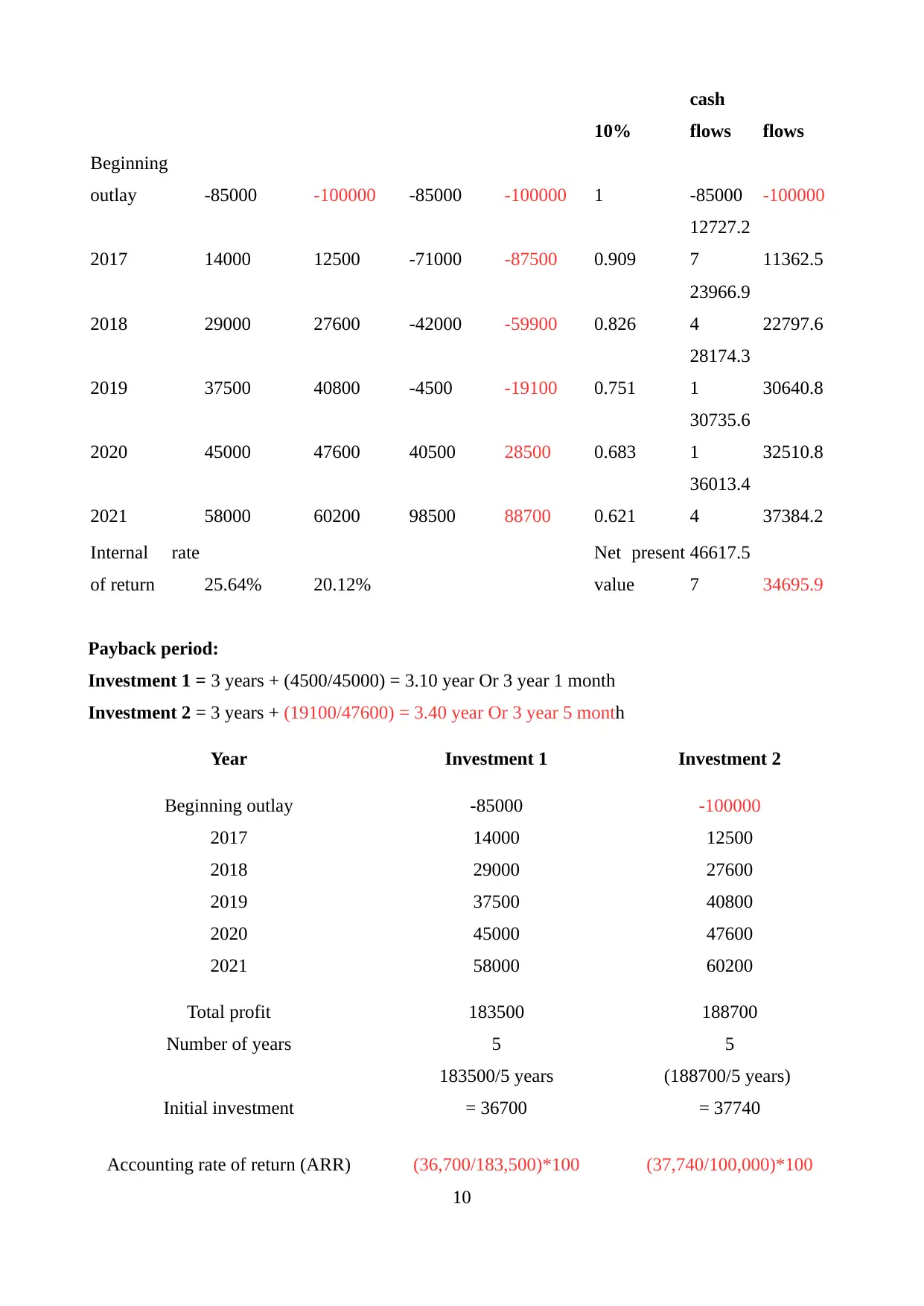

Year Investment 1

Investment

2 CCF (1st) CCF (2nd)

Discounted

factor @

Cumula

tive

Cumulat

ive cash

9

= 30 + 12

= 42

Justification behind using 40% mark-up

Here, 40% desired target return has been taken using various components such as profit-

maximization objectives, customers willingness to pay, their economic situation, market trend,

growth in demand and competitors product pricing also. With the stated case, consumers are ready

to pay high prices for the quality offerings and has strong financail position. In addition, managers

are targeted to gain maximum return therefore, 40% desired profit mark-up is founded suitable.

At 40% mark-up on the total cost, retailer will have to charge 42 GBP for each unit. If entity

wish to earn greater return then he needs to charge higher rate than 40% or vice-versa for getting

adequate return and high success.

3.3 Investment appraisal techniques applications

Capital budgeting is one of the key technique that is used by the financial managers for the

financial planning & success. This tools will help retailer, ABC Ltd to determine that whether a firm

must invest or deny available investment opportunity for the business growth, expansion and

success.

Payback period:

This technique is the simplest method that find out the recovery period of beginning cost of

investment in a project. While dealing with mutually-exclusive projects, an investor must prefers a

project with shorter payback period or vice-versa (Greene, Brush and Brown, 2015).

Accounting rate of return;

This method just computes or quantifies the return percentage on the total initial investment.

Company always needs high return, therefore, prefers greater ARR.

Net present value:

It is the modern and also the best way of investment appraisal which discounts the cash flow

to address the impact of market uncertainties. Total of discounted cash flows over the beginning

cost of capital is called net present value.

Internal rate of return:

This method just find out the rate at where NPV does not exists, henceforth, there is neither

any return nor loss exists at that rate.

Year Investment 1

Investment

2 CCF (1st) CCF (2nd)

Discounted

factor @

Cumula

tive

Cumulat

ive cash

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10%

cash

flows flows

Beginning

outlay -85000 -100000 -85000 -100000 1 -85000 -100000

2017 14000 12500 -71000 -87500 0.909

12727.2

7 11362.5

2018 29000 27600 -42000 -59900 0.826

23966.9

4 22797.6

2019 37500 40800 -4500 -19100 0.751

28174.3

1 30640.8

2020 45000 47600 40500 28500 0.683

30735.6

1 32510.8

2021 58000 60200 98500 88700 0.621

36013.4

4 37384.2

Internal rate

of return 25.64% 20.12%

Net present

value

46617.5

7 34695.9

Payback period:

Investment 1 = 3 years + (4500/45000) = 3.10 year Or 3 year 1 month

Investment 2 = 3 years + (19100/47600) = 3.40 year Or 3 year 5 month

Year Investment 1 Investment 2

Beginning outlay -85000 -100000

2017 14000 12500

2018 29000 27600

2019 37500 40800

2020 45000 47600

2021 58000 60200

Total profit 183500 188700

Number of years 5 5

Initial investment

183500/5 years

= 36700

(188700/5 years)

= 37740

Accounting rate of return (ARR) (36,700/183,500)*100 (37,740/100,000)*100

10

cash

flows flows

Beginning

outlay -85000 -100000 -85000 -100000 1 -85000 -100000

2017 14000 12500 -71000 -87500 0.909

12727.2

7 11362.5

2018 29000 27600 -42000 -59900 0.826

23966.9

4 22797.6

2019 37500 40800 -4500 -19100 0.751

28174.3

1 30640.8

2020 45000 47600 40500 28500 0.683

30735.6

1 32510.8

2021 58000 60200 98500 88700 0.621

36013.4

4 37384.2

Internal rate

of return 25.64% 20.12%

Net present

value

46617.5

7 34695.9

Payback period:

Investment 1 = 3 years + (4500/45000) = 3.10 year Or 3 year 1 month

Investment 2 = 3 years + (19100/47600) = 3.40 year Or 3 year 5 month

Year Investment 1 Investment 2

Beginning outlay -85000 -100000

2017 14000 12500

2018 29000 27600

2019 37500 40800

2020 45000 47600

2021 58000 60200

Total profit 183500 188700

Number of years 5 5

Initial investment

183500/5 years

= 36700

(188700/5 years)

= 37740

Accounting rate of return (ARR) (36,700/183,500)*100 (37,740/100,000)*100

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 43.18% = 37.74%

Recommendations

Investment 1 has shorter payback duration to 3 year 1 month hence, it is clear that recovery

period of this project is smaller. Moreover, this project has greater ARR to 43.18% whilst in another

one, it is derived to 37.74% hence, project A will give higher accounting period. However, under the

discounting techniques, both the IRR & NPV gives favorable esults for the first project. Project A's

NPV & IRR are comparatively greater to 25.64% & 46,617.57, in contrast, in the second one, it is

derived to 20.12% and 34,695.9 which is comparatively lower. Thus, the results favors investment

in first project and consider it more viable and should be undertaken by the management (Altenburg

and Pegels, 2012).

TASK 4

4.1 Types of financial statements

All the corporations or establishments needs to prepare their financial accounts adhering

with the accounting standards, UK GAAP. It is important to construct final accounts on a regular

period incorporating the results of all the monetary business transactions and activities. The

important annual accounts that an organization needs to prepare are stated here as under:

Income Statement

This statements provides an overview of organizational revenues and incurred payments in

connection with the regular transactions. The main target of making income statement is to

determine the profitability performance by subtracting total expenditures from the generated

revenues (Julian and Ofori‐dankwa, 2013). Income comprises sales, however, payments includes

purchase, rent, salary, wages, insurance and others.

Balance sheet

It provides a snapshot of liabilities, assets and shareholder’s equity and mainly targeted at

identifying the financial status of the firm. Analysts mainly use it to determine capital structure &

working capital for assessing solvency & liquidity and managerial efficiency too to evaluable

business performance.

Cash Flow Statement

This statement reconciles cash inflow and its disposal in operating, investing and financing

activities to keep track of cash position of the firm over the period. It enables a business to identify

the closing cash balance with the reasons behind change in cash balances at two different balance

11

Recommendations

Investment 1 has shorter payback duration to 3 year 1 month hence, it is clear that recovery

period of this project is smaller. Moreover, this project has greater ARR to 43.18% whilst in another

one, it is derived to 37.74% hence, project A will give higher accounting period. However, under the

discounting techniques, both the IRR & NPV gives favorable esults for the first project. Project A's

NPV & IRR are comparatively greater to 25.64% & 46,617.57, in contrast, in the second one, it is

derived to 20.12% and 34,695.9 which is comparatively lower. Thus, the results favors investment

in first project and consider it more viable and should be undertaken by the management (Altenburg

and Pegels, 2012).

TASK 4

4.1 Types of financial statements

All the corporations or establishments needs to prepare their financial accounts adhering

with the accounting standards, UK GAAP. It is important to construct final accounts on a regular

period incorporating the results of all the monetary business transactions and activities. The

important annual accounts that an organization needs to prepare are stated here as under:

Income Statement

This statements provides an overview of organizational revenues and incurred payments in

connection with the regular transactions. The main target of making income statement is to

determine the profitability performance by subtracting total expenditures from the generated

revenues (Julian and Ofori‐dankwa, 2013). Income comprises sales, however, payments includes

purchase, rent, salary, wages, insurance and others.

Balance sheet

It provides a snapshot of liabilities, assets and shareholder’s equity and mainly targeted at

identifying the financial status of the firm. Analysts mainly use it to determine capital structure &

working capital for assessing solvency & liquidity and managerial efficiency too to evaluable

business performance.

Cash Flow Statement

This statement reconciles cash inflow and its disposal in operating, investing and financing

activities to keep track of cash position of the firm over the period. It enables a business to identify

the closing cash balance with the reasons behind change in cash balances at two different balance

11

sheet dates (Fassin, 2012).

4.2 Final accounts differences in different organizations

Sole trader prepares income statement by reporting their revenues through trading activities

like supply of goods and services, purchase, wages, salaries and other payments. As per this, excess

of income over expenditures is called net profit or net loss which is totally available for the

proprietor. However, partnership construct profit and loss account and net profit is being distributed

among all the partners in their profit/loss sharing ratio. It also prepares partner's current account for

the distribution of interest on capital, interest on loan, partner’s commission and so on. In contrast,

companies and sole proprietor do not construct such type of account for the distribution of profit.

On the other hand, companies prepare income statement as per the rules of company act and

international accounting standards as well. It is prepared in decided format and every item is

recorded in structure manner to know gross profit, operational return and net profitability (Keupp,

Palmié and Gassmann, 2012). Unlike sole proprietor and partnership, they distribute a part of net

return to the investors which is known as dividend, therefore, it is reported as earning per share and

remainder as retained profits.

On the other side, sole proprietor’s balance sheet reported owner’s capital as investment, in

partnership, every partner’s capital contribution is clearly disclosed in the B/S whilst in company, it

comprises equity shareholder investment, share premium and retained profits. It also needs to

prepare it as per the schedules for the harmonization accounting practices. In addition, sole trader &

partnership do not require to construct statement of cash flow whilst companies are legally obliged

to prepare it for knowing the reasons for change in cash. Partnership construct partner capital

account to determine their total investment whereas companies prepare statement of change in

equity for the same.

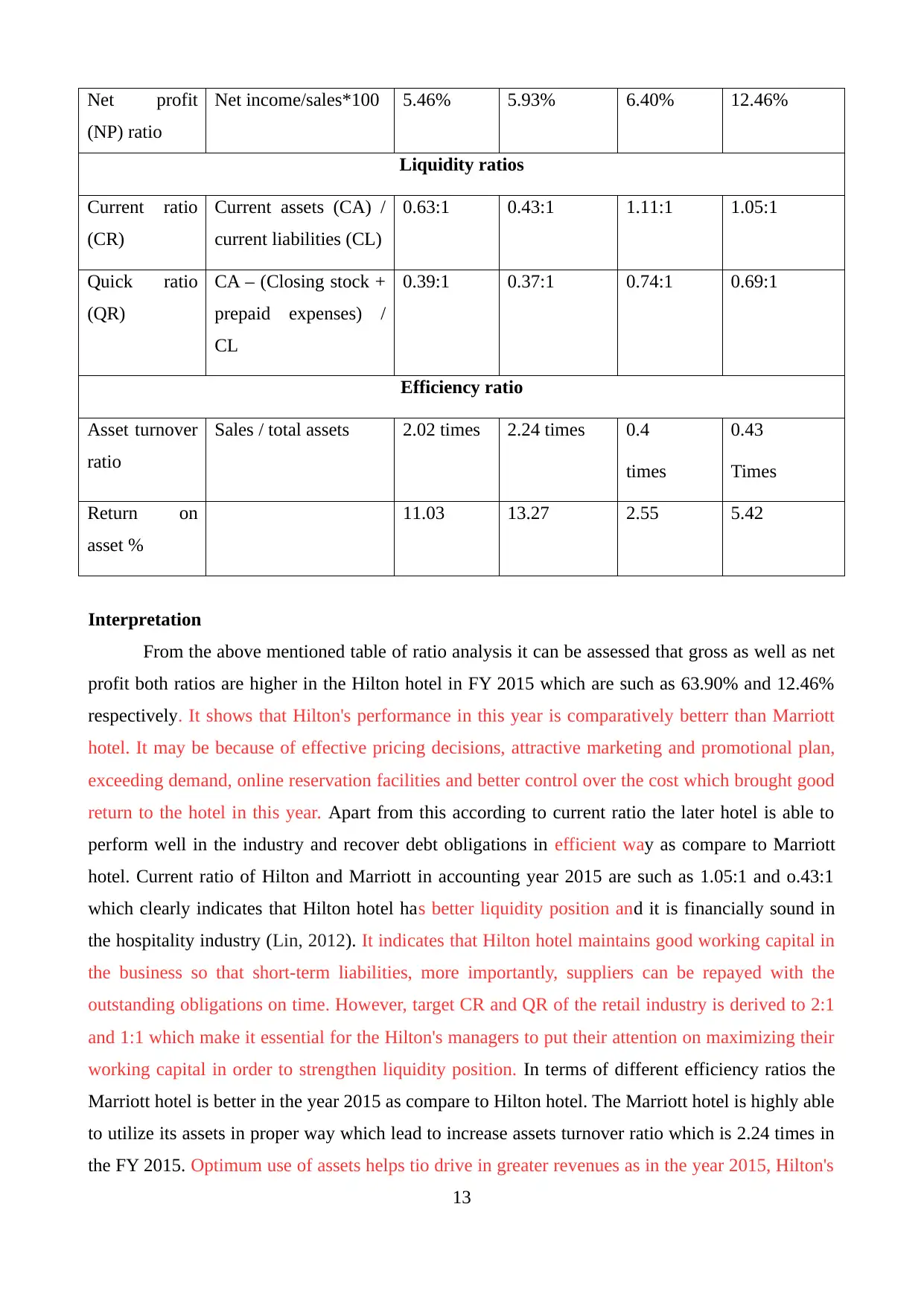

4.3 Analysis financial statements using financial ratios

Name of ratio Formula Hotel Marriott Hotel Hilton

2014 2015 2014 2015

Profitability ratios

Gross income 1966 2123 6483 7207

Net income 753 859 673 1404

Revenue 13796 14486 10502 11272

Gross profit

(GP) ratio

Gross

income/sales*100

14.25% 14.66% 61.70% 63.90%

12

4.2 Final accounts differences in different organizations

Sole trader prepares income statement by reporting their revenues through trading activities

like supply of goods and services, purchase, wages, salaries and other payments. As per this, excess

of income over expenditures is called net profit or net loss which is totally available for the

proprietor. However, partnership construct profit and loss account and net profit is being distributed

among all the partners in their profit/loss sharing ratio. It also prepares partner's current account for

the distribution of interest on capital, interest on loan, partner’s commission and so on. In contrast,

companies and sole proprietor do not construct such type of account for the distribution of profit.

On the other hand, companies prepare income statement as per the rules of company act and

international accounting standards as well. It is prepared in decided format and every item is

recorded in structure manner to know gross profit, operational return and net profitability (Keupp,

Palmié and Gassmann, 2012). Unlike sole proprietor and partnership, they distribute a part of net

return to the investors which is known as dividend, therefore, it is reported as earning per share and

remainder as retained profits.

On the other side, sole proprietor’s balance sheet reported owner’s capital as investment, in

partnership, every partner’s capital contribution is clearly disclosed in the B/S whilst in company, it

comprises equity shareholder investment, share premium and retained profits. It also needs to

prepare it as per the schedules for the harmonization accounting practices. In addition, sole trader &

partnership do not require to construct statement of cash flow whilst companies are legally obliged

to prepare it for knowing the reasons for change in cash. Partnership construct partner capital

account to determine their total investment whereas companies prepare statement of change in

equity for the same.

4.3 Analysis financial statements using financial ratios

Name of ratio Formula Hotel Marriott Hotel Hilton

2014 2015 2014 2015

Profitability ratios

Gross income 1966 2123 6483 7207

Net income 753 859 673 1404

Revenue 13796 14486 10502 11272

Gross profit

(GP) ratio

Gross

income/sales*100

14.25% 14.66% 61.70% 63.90%

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net profit

(NP) ratio

Net income/sales*100 5.46% 5.93% 6.40% 12.46%

Liquidity ratios

Current ratio

(CR)

Current assets (CA) /

current liabilities (CL)

0.63:1 0.43:1 1.11:1 1.05:1

Quick ratio

(QR)

CA – (Closing stock +

prepaid expenses) /

CL

0.39:1 0.37:1 0.74:1 0.69:1

Efficiency ratio

Asset turnover

ratio

Sales / total assets 2.02 times 2.24 times 0.4

times

0.43

Times

Return on

asset %

11.03 13.27 2.55 5.42

Interpretation

From the above mentioned table of ratio analysis it can be assessed that gross as well as net

profit both ratios are higher in the Hilton hotel in FY 2015 which are such as 63.90% and 12.46%

respectively. It shows that Hilton's performance in this year is comparatively betterr than Marriott

hotel. It may be because of effective pricing decisions, attractive marketing and promotional plan,

exceeding demand, online reservation facilities and better control over the cost which brought good

return to the hotel in this year. Apart from this according to current ratio the later hotel is able to

perform well in the industry and recover debt obligations in efficient way as compare to Marriott

hotel. Current ratio of Hilton and Marriott in accounting year 2015 are such as 1.05:1 and o.43:1

which clearly indicates that Hilton hotel has better liquidity position and it is financially sound in

the hospitality industry (Lin, 2012). It indicates that Hilton hotel maintains good working capital in

the business so that short-term liabilities, more importantly, suppliers can be repayed with the

outstanding obligations on time. However, target CR and QR of the retail industry is derived to 2:1

and 1:1 which make it essential for the Hilton's managers to put their attention on maximizing their

working capital in order to strengthen liquidity position. In terms of different efficiency ratios the

Marriott hotel is better in the year 2015 as compare to Hilton hotel. The Marriott hotel is highly able

to utilize its assets in proper way which lead to increase assets turnover ratio which is 2.24 times in

the FY 2015. Optimum use of assets helps tio drive in greater revenues as in the year 2015, Hilton's

13

(NP) ratio

Net income/sales*100 5.46% 5.93% 6.40% 12.46%

Liquidity ratios

Current ratio

(CR)

Current assets (CA) /

current liabilities (CL)

0.63:1 0.43:1 1.11:1 1.05:1

Quick ratio

(QR)

CA – (Closing stock +

prepaid expenses) /

CL

0.39:1 0.37:1 0.74:1 0.69:1

Efficiency ratio

Asset turnover

ratio

Sales / total assets 2.02 times 2.24 times 0.4

times

0.43

Times

Return on

asset %

11.03 13.27 2.55 5.42

Interpretation

From the above mentioned table of ratio analysis it can be assessed that gross as well as net

profit both ratios are higher in the Hilton hotel in FY 2015 which are such as 63.90% and 12.46%

respectively. It shows that Hilton's performance in this year is comparatively betterr than Marriott

hotel. It may be because of effective pricing decisions, attractive marketing and promotional plan,

exceeding demand, online reservation facilities and better control over the cost which brought good

return to the hotel in this year. Apart from this according to current ratio the later hotel is able to

perform well in the industry and recover debt obligations in efficient way as compare to Marriott

hotel. Current ratio of Hilton and Marriott in accounting year 2015 are such as 1.05:1 and o.43:1

which clearly indicates that Hilton hotel has better liquidity position and it is financially sound in

the hospitality industry (Lin, 2012). It indicates that Hilton hotel maintains good working capital in

the business so that short-term liabilities, more importantly, suppliers can be repayed with the

outstanding obligations on time. However, target CR and QR of the retail industry is derived to 2:1

and 1:1 which make it essential for the Hilton's managers to put their attention on maximizing their

working capital in order to strengthen liquidity position. In terms of different efficiency ratios the

Marriott hotel is better in the year 2015 as compare to Hilton hotel. The Marriott hotel is highly able

to utilize its assets in proper way which lead to increase assets turnover ratio which is 2.24 times in

the FY 2015. Optimum use of assets helps tio drive in greater revenues as in the year 2015, Hilton's

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

total revenues exceeded by 11.16%.

CONCLUSION

After completing the above report, it becomes clear that every source has a different

implication, therefore, ABC Ltd must choose a right combination of source for meeting out their

financial need. Budgeting analysis founded that ABC Ltd needs to put stronger control over cash

disposal and make policies in relation with increase in revenues for having a successful growth.

Lastly, investment appraisal technique founded 2nd proposal highly suitable due to maximum NPV.

Further, ratio analysis techniques founded that appropriate and right pricing mechanism, cost

controlling measures, capital structure and working capital decisions helps to strengthen the

financial performance for a successful business.

14

CONCLUSION

After completing the above report, it becomes clear that every source has a different

implication, therefore, ABC Ltd must choose a right combination of source for meeting out their

financial need. Budgeting analysis founded that ABC Ltd needs to put stronger control over cash

disposal and make policies in relation with increase in revenues for having a successful growth.

Lastly, investment appraisal technique founded 2nd proposal highly suitable due to maximum NPV.

Further, ratio analysis techniques founded that appropriate and right pricing mechanism, cost

controlling measures, capital structure and working capital decisions helps to strengthen the

financial performance for a successful business.

14

REFERENCES

Books and Journals

Altenburg, T. and Pegels, A., 2012. Sustainability-oriented innovation systems–managing the green

transformation. Innovation and Development. 2(1). pp. 5-22.

Brigham, E. F. and Ehrhardt, M. C., 2013. Financial management: Theory & practice. Cengage

Learning.

Brigham, E. F. and Ehrhardt, M. C., 2013. Financial management: Theory & practice. Cengage

Learning.

Cambra-Fierro, J., Melero, I. and Sese, F. J., 2015. Managing complaints to improve customer

profitability. Journal of Retailing. 91(1). pp. 109-124.

Drechsler, W. and Natter, M., 2012. Understanding a firm's openness decisions in innovation.

Journal of Business Research. 65(3). pp. 438-445.

DRURY, C. M., 2013. Management and cost accounting. Springer.

Fassin, Y., 2012. Stakeholder management, reciprocity and stakeholder responsibility. Journal of

Business Ethics. 109(1). pp. 83-96.

Greene, P. G., Brush, C. G. and Brown, T. E., 2015. Resources in small firms: an exploratory study.

Journal of Small Business Strategy. 8(2). pp. 25-40.

Greene, P. G., Brush, C. G. and Brown, T. E., 2015. Resources in small firms: an exploratory

study. Journal of Small Business Strategy. 8(2). pp. 25-40.

Healy, P. M. and Palepu, K. G., 2012. Business analysis valuation: Using financial statements.

Cengage Learning.

Julian, S. D. and Ofori‐dankwa, J. C., 2013. Financial resource availability and corporate social

responsibility expenditures in a sub‐Saharan economy: The institutional difference

hypothesis. Strategic Management Journal. 34(11). pp. 1314-1330.

Keupp, M. M., Palmié, M. and Gassmann, O., 2012. The strategic management of innovation: A

systematic review and paths for future research. International Journal of Management

Reviews. 14(4). pp. 367-390.

Lin, W. T., 2012. Family ownership and internationalization processes: Internationalization pace,

internationalization scope, and internationalization rhythm. European Management

Journal. 30(1). pp. 47-56.

15

Books and Journals

Altenburg, T. and Pegels, A., 2012. Sustainability-oriented innovation systems–managing the green

transformation. Innovation and Development. 2(1). pp. 5-22.

Brigham, E. F. and Ehrhardt, M. C., 2013. Financial management: Theory & practice. Cengage

Learning.

Brigham, E. F. and Ehrhardt, M. C., 2013. Financial management: Theory & practice. Cengage

Learning.

Cambra-Fierro, J., Melero, I. and Sese, F. J., 2015. Managing complaints to improve customer

profitability. Journal of Retailing. 91(1). pp. 109-124.

Drechsler, W. and Natter, M., 2012. Understanding a firm's openness decisions in innovation.

Journal of Business Research. 65(3). pp. 438-445.

DRURY, C. M., 2013. Management and cost accounting. Springer.

Fassin, Y., 2012. Stakeholder management, reciprocity and stakeholder responsibility. Journal of

Business Ethics. 109(1). pp. 83-96.

Greene, P. G., Brush, C. G. and Brown, T. E., 2015. Resources in small firms: an exploratory study.

Journal of Small Business Strategy. 8(2). pp. 25-40.

Greene, P. G., Brush, C. G. and Brown, T. E., 2015. Resources in small firms: an exploratory

study. Journal of Small Business Strategy. 8(2). pp. 25-40.

Healy, P. M. and Palepu, K. G., 2012. Business analysis valuation: Using financial statements.

Cengage Learning.

Julian, S. D. and Ofori‐dankwa, J. C., 2013. Financial resource availability and corporate social

responsibility expenditures in a sub‐Saharan economy: The institutional difference

hypothesis. Strategic Management Journal. 34(11). pp. 1314-1330.

Keupp, M. M., Palmié, M. and Gassmann, O., 2012. The strategic management of innovation: A

systematic review and paths for future research. International Journal of Management

Reviews. 14(4). pp. 367-390.

Lin, W. T., 2012. Family ownership and internationalization processes: Internationalization pace,

internationalization scope, and internationalization rhythm. European Management

Journal. 30(1). pp. 47-56.

15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.