Oil & Gas M&A: Influencing Factors and Strategic Analysis (2014-2016)

VerifiedAdded on 2023/06/19

|13

|3848

|434

Case Study

AI Summary

This case study examines the merger and acquisition (M&A) strategies employed by the oil and gas industry between 2014 and 2016, a period marked by significant fluctuations in oil prices. It identifies both external factors, such as the sharp decline in oil prices, rapid oil production, the development of energy-efficient vehicles, and the lifting of sanctions on Iran, and internal factors, including oil company bankruptcies, negligence in anticipating market shifts, intense competition, and misperceptions about investment returns, that influenced these strategies. The study highlights significant M&A deals, including Royal Dutch Shell's acquisition of BG Group and Noble Energy's acquisition of Rosetta Resources, analyzing the benefits and challenges associated with each. The analysis provides insights into how companies sought to reset, leverage inorganic growth, and achieve synergistic merging in response to the challenging market conditions.

Table of Contents

1. Introduction:........................................................................................................................2

2. Internal and External factors that influenced Oil and Gas Industries to use Merger and

Acquisition strategy during 2014-2016......................................................................................2

2.1. External Factors:..........................................................................................................2

2.1.1. Oil Price Dropping:..............................................................................................2

2.1.2. Rapid production of Oil in massive amount:.......................................................3

2.1.3. Development of Energy Efficient Cars:...............................................................3

2.1.4. Lifting of International Sanction placed on Iran:.................................................3

2.2. Internal Factors:...........................................................................................................4

2.2.1. Oil companies going bankrupt:............................................................................4

2.2.2. Negligence:..........................................................................................................4

2.2.3. Competition among companies:...........................................................................4

2.2.4. Wrong Perception:...............................................................................................5

3. Merger and Acquisition strategy used by Oil and Gas Industries during 2014-2016........5

3.1. Introduction:................................................................................................................5

3.2. One of the Biggest Acquisition of the decade came in year 2015: Royal Dutch Shell

bought BG Group:..................................................................................................................5

3.2.1. Benefits of this Acquisition for Royal Dutch Shell Plc:......................................6

3.2.2. Challenges of this acquisition to the merger (Royal Dutch Shell PLC):.............8

3.3. Noble Energy Acquisition of Rosetta Resources:.......................................................9

3.3.1. Benefit of this deal to Merger (Noble Energy):.................................................10

3.3.2. Challenges of this deal to the Merger (Noble Energy):.....................................10

4. Summary:.........................................................................................................................11

5. References........................................................................................................................11

1. Introduction:........................................................................................................................2

2. Internal and External factors that influenced Oil and Gas Industries to use Merger and

Acquisition strategy during 2014-2016......................................................................................2

2.1. External Factors:..........................................................................................................2

2.1.1. Oil Price Dropping:..............................................................................................2

2.1.2. Rapid production of Oil in massive amount:.......................................................3

2.1.3. Development of Energy Efficient Cars:...............................................................3

2.1.4. Lifting of International Sanction placed on Iran:.................................................3

2.2. Internal Factors:...........................................................................................................4

2.2.1. Oil companies going bankrupt:............................................................................4

2.2.2. Negligence:..........................................................................................................4

2.2.3. Competition among companies:...........................................................................4

2.2.4. Wrong Perception:...............................................................................................5

3. Merger and Acquisition strategy used by Oil and Gas Industries during 2014-2016........5

3.1. Introduction:................................................................................................................5

3.2. One of the Biggest Acquisition of the decade came in year 2015: Royal Dutch Shell

bought BG Group:..................................................................................................................5

3.2.1. Benefits of this Acquisition for Royal Dutch Shell Plc:......................................6

3.2.2. Challenges of this acquisition to the merger (Royal Dutch Shell PLC):.............8

3.3. Noble Energy Acquisition of Rosetta Resources:.......................................................9

3.3.1. Benefit of this deal to Merger (Noble Energy):.................................................10

3.3.2. Challenges of this deal to the Merger (Noble Energy):.....................................10

4. Summary:.........................................................................................................................11

5. References........................................................................................................................11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Introduction:

The intense fall of both natural gas and crude oil prices across the year 2014-2015, joint with

a high level of ambiguity about their future curve challenged oil and gas merger and

acquisition (M&A) activity in 2015. Crude oil prices began the year 2015 at US$55 per barrel

which declined sharply to US$37 per barrel by December that year. This was the lowermost

level since 2004. The natural gas prices also shared the same story. Since the production of

crude oil continued to overtake need of consumer by 2 million barrels per day and also there

is no clear sign when the global oil and gas market will rebalance, prices of crude oil and

natural gas have been continuously declining (Ernst & Young Global Limited, 2015).

This severe decline in oil prices in 2014 has put a discouragement on many big energy

companies. Having said that, this has not kept these companies from mergers and acquisitions

activities (Mattioli & D, 2015).

2. Internal and External factors that influenced Oil and

Gas Industries to use Merger and Acquisition strategy

during 2014-2016.

Merger and Acquisition activity in the oil and gas industry might recover its drive mainly by

big energy industries looking for some method of “reset”. This could be through financial

recapitalizations, asset sales, restructurings, and other forms of monetization. Also, these big

companies with the financial capability are looking to hunt inorganic growth opportunities at

reduced values, and are looking for synergistic merging (Deloitte Center, 2014).

2.1. External Factors:

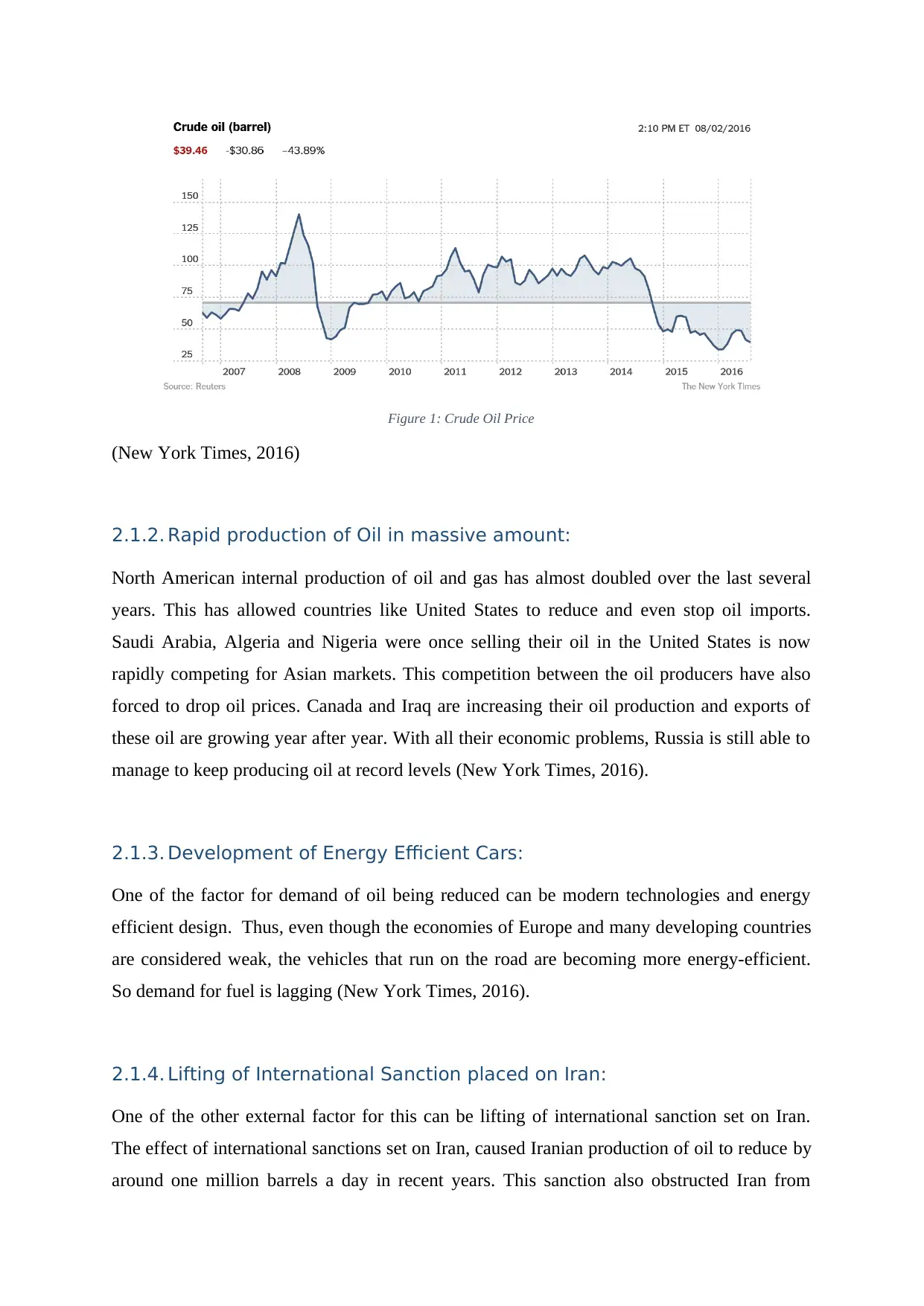

2.1.1. Oil Price Dropping:

Crude oil prices began the year 2015 at US$55 per barrel which declined sharply to US$37

per barrel by December that year. This oil prices was over US$100 a barrel in mid-2014 has

fallen dramatically below $27 by February 2016. Not only crude oil but there is a significant

price drop in natural gas prices, which are near 14-year lows (Egan, 2016).

The intense fall of both natural gas and crude oil prices across the year 2014-2015, joint with

a high level of ambiguity about their future curve challenged oil and gas merger and

acquisition (M&A) activity in 2015. Crude oil prices began the year 2015 at US$55 per barrel

which declined sharply to US$37 per barrel by December that year. This was the lowermost

level since 2004. The natural gas prices also shared the same story. Since the production of

crude oil continued to overtake need of consumer by 2 million barrels per day and also there

is no clear sign when the global oil and gas market will rebalance, prices of crude oil and

natural gas have been continuously declining (Ernst & Young Global Limited, 2015).

This severe decline in oil prices in 2014 has put a discouragement on many big energy

companies. Having said that, this has not kept these companies from mergers and acquisitions

activities (Mattioli & D, 2015).

2. Internal and External factors that influenced Oil and

Gas Industries to use Merger and Acquisition strategy

during 2014-2016.

Merger and Acquisition activity in the oil and gas industry might recover its drive mainly by

big energy industries looking for some method of “reset”. This could be through financial

recapitalizations, asset sales, restructurings, and other forms of monetization. Also, these big

companies with the financial capability are looking to hunt inorganic growth opportunities at

reduced values, and are looking for synergistic merging (Deloitte Center, 2014).

2.1. External Factors:

2.1.1. Oil Price Dropping:

Crude oil prices began the year 2015 at US$55 per barrel which declined sharply to US$37

per barrel by December that year. This oil prices was over US$100 a barrel in mid-2014 has

fallen dramatically below $27 by February 2016. Not only crude oil but there is a significant

price drop in natural gas prices, which are near 14-year lows (Egan, 2016).

Figure 1: Crude Oil Price

(New York Times, 2016)

2.1.2. Rapid production of Oil in massive amount:

North American internal production of oil and gas has almost doubled over the last several

years. This has allowed countries like United States to reduce and even stop oil imports.

Saudi Arabia, Algeria and Nigeria were once selling their oil in the United States is now

rapidly competing for Asian markets. This competition between the oil producers have also

forced to drop oil prices. Canada and Iraq are increasing their oil production and exports of

these oil are growing year after year. With all their economic problems, Russia is still able to

manage to keep producing oil at record levels (New York Times, 2016).

2.1.3. Development of Energy Efficient Cars:

One of the factor for demand of oil being reduced can be modern technologies and energy

efficient design. Thus, even though the economies of Europe and many developing countries

are considered weak, the vehicles that run on the road are becoming more energy-efficient.

So demand for fuel is lagging (New York Times, 2016).

2.1.4. Lifting of International Sanction placed on Iran:

One of the other external factor for this can be lifting of international sanction set on Iran.

The effect of international sanctions set on Iran, caused Iranian production of oil to reduce by

around one million barrels a day in recent years. This sanction also obstructed Iran from

(New York Times, 2016)

2.1.2. Rapid production of Oil in massive amount:

North American internal production of oil and gas has almost doubled over the last several

years. This has allowed countries like United States to reduce and even stop oil imports.

Saudi Arabia, Algeria and Nigeria were once selling their oil in the United States is now

rapidly competing for Asian markets. This competition between the oil producers have also

forced to drop oil prices. Canada and Iraq are increasing their oil production and exports of

these oil are growing year after year. With all their economic problems, Russia is still able to

manage to keep producing oil at record levels (New York Times, 2016).

2.1.3. Development of Energy Efficient Cars:

One of the factor for demand of oil being reduced can be modern technologies and energy

efficient design. Thus, even though the economies of Europe and many developing countries

are considered weak, the vehicles that run on the road are becoming more energy-efficient.

So demand for fuel is lagging (New York Times, 2016).

2.1.4. Lifting of International Sanction placed on Iran:

One of the other external factor for this can be lifting of international sanction set on Iran.

The effect of international sanctions set on Iran, caused Iranian production of oil to reduce by

around one million barrels a day in recent years. This sanction also obstructed Iran from

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

buying the latest international oil field technology and equipment. With this sanctions now

being lifted, the oil industry in Iran is also actively participating oil and gas production (New

York Times, 2016).

2.2. Internal Factors:

2.2.1. Oil companies going bankrupt:

There was a time, when oil prices were comfortably in the $90 to $100 a barrel and this is the

time when shale oil boom took off in North America. With the shale oil production booming,

oil and gas companies took on loads of debt to fund these expensive drilling for finding oil

and gas. But the subsequent flood in U.S. oil production created an epic supply surplus which

has now caused crude oil prices to crash badly (Egan, 2016).

Because of this, revenues have dropped. This has also choked off cash flows and making it

challenging for companies to pay off all their debt. To deal with this situation, oil companies

have countered by cutting jobs and reducing spending. Even though, some of the more

leveraged companies have been forced to the option of bankruptcy (Egan, 2016).

2.2.2. Negligence:

The Oil companies around the world, neglected the price drop in early 2014 and they thought

it was not a long term (England, 2016). This negligence from Oil and Gas companies

regarding the initial price drop lead the price to drop further and the companies to panic and

develop strategies such as Merger and Acquisition.

2.2.3. Competition among companies:

OPEC countries started to compete with US oil industries to take over the Asian market.

Also, this competition lead to the production of oil in a very high volume from both side.

This growth in production allowed the price of oil to drop and ultimately, the companies that

were producing had to suffer from loss. Also, in April 2016, Exxon company had

reported record low quarterly profits, and they were, therefore, recently stripped of its top

AAA credit rating (KRAUSS, 2016).

being lifted, the oil industry in Iran is also actively participating oil and gas production (New

York Times, 2016).

2.2. Internal Factors:

2.2.1. Oil companies going bankrupt:

There was a time, when oil prices were comfortably in the $90 to $100 a barrel and this is the

time when shale oil boom took off in North America. With the shale oil production booming,

oil and gas companies took on loads of debt to fund these expensive drilling for finding oil

and gas. But the subsequent flood in U.S. oil production created an epic supply surplus which

has now caused crude oil prices to crash badly (Egan, 2016).

Because of this, revenues have dropped. This has also choked off cash flows and making it

challenging for companies to pay off all their debt. To deal with this situation, oil companies

have countered by cutting jobs and reducing spending. Even though, some of the more

leveraged companies have been forced to the option of bankruptcy (Egan, 2016).

2.2.2. Negligence:

The Oil companies around the world, neglected the price drop in early 2014 and they thought

it was not a long term (England, 2016). This negligence from Oil and Gas companies

regarding the initial price drop lead the price to drop further and the companies to panic and

develop strategies such as Merger and Acquisition.

2.2.3. Competition among companies:

OPEC countries started to compete with US oil industries to take over the Asian market.

Also, this competition lead to the production of oil in a very high volume from both side.

This growth in production allowed the price of oil to drop and ultimately, the companies that

were producing had to suffer from loss. Also, in April 2016, Exxon company had

reported record low quarterly profits, and they were, therefore, recently stripped of its top

AAA credit rating (KRAUSS, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.2.4. Wrong Perception:

Oil and Gas companies tried to grow their business and invested more on growing their

business rather than investing for returns (England, 2016).

There was a time, when oil prices were comfortably in the $90 to $100 a barrel and this is the

time when shale oil boom took off in North America. With the shale oil production booming,

oil and gas companies took on loads of debt to fund these expensive drilling for finding oil

and gas. But the subsequent flood in U.S. oil production created an epic supply surplus which

has now caused crude oil prices to crash badly (Egan, 2016).

3. Merger and Acquisition strategy used by Oil and Gas

Industries during 2014-2016.

3.1. Introduction:

The traditional definition of Merger and Acquisition states to the unification of two

companies to form a new business entity (merger) or the acquiring of one company by

another company (acquisition). In the Oil and Gas industry, especially in the upstream

sectors, Merger and Acquisition activities are usually more generally defined to include the

acquisition of Oil and Gas assets such as properties and reserves, and does not certainly be

just the acquisition of the entire business entity (Hsu, et al., 2015).

3.2. One of the Biggest Acquisition of the decade came in year

2015: Royal Dutch Shell bought BG Group:

One of the biggest acquisition of the whole decade was in year 2015 when Royal Dutch

Shell bought gas group BG for £47bn once a plunging oil price urged a leap on its long

wanted takeover target (Kollewe & Farrell, 2015).

This acquisition of BG Group (BG) by Royal Dutch Shell (Shell) was one of the biggest

international deal accounted. This US$80 billion acquisition was mainly intended to

strategically grow a dominant position in global LNG and also to bring Shell a superior

presence in high-potential offshore fields in Brazil (Deloitte Center, 2015).

Oil and Gas companies tried to grow their business and invested more on growing their

business rather than investing for returns (England, 2016).

There was a time, when oil prices were comfortably in the $90 to $100 a barrel and this is the

time when shale oil boom took off in North America. With the shale oil production booming,

oil and gas companies took on loads of debt to fund these expensive drilling for finding oil

and gas. But the subsequent flood in U.S. oil production created an epic supply surplus which

has now caused crude oil prices to crash badly (Egan, 2016).

3. Merger and Acquisition strategy used by Oil and Gas

Industries during 2014-2016.

3.1. Introduction:

The traditional definition of Merger and Acquisition states to the unification of two

companies to form a new business entity (merger) or the acquiring of one company by

another company (acquisition). In the Oil and Gas industry, especially in the upstream

sectors, Merger and Acquisition activities are usually more generally defined to include the

acquisition of Oil and Gas assets such as properties and reserves, and does not certainly be

just the acquisition of the entire business entity (Hsu, et al., 2015).

3.2. One of the Biggest Acquisition of the decade came in year

2015: Royal Dutch Shell bought BG Group:

One of the biggest acquisition of the whole decade was in year 2015 when Royal Dutch

Shell bought gas group BG for £47bn once a plunging oil price urged a leap on its long

wanted takeover target (Kollewe & Farrell, 2015).

This acquisition of BG Group (BG) by Royal Dutch Shell (Shell) was one of the biggest

international deal accounted. This US$80 billion acquisition was mainly intended to

strategically grow a dominant position in global LNG and also to bring Shell a superior

presence in high-potential offshore fields in Brazil (Deloitte Center, 2015).

3.2.1. Benefits of this Acquisition for Royal Dutch Shell Plc:

a. Getting an edge over it Rival and expanding:

Royal Dutch Shell Plc after finishing its largest acquisition of BG Group, has become bigger

than it rival Chevron Corp. This company, thus, has become the second largest non-state oil

company in the world. This acquisition of has allowed Shell company to grow dominant

especially in global LNG and it has taken Shell company to a greater presence in high-

potential offshore fields in Brazil.

This takeover of BG Group Plc by Shell has raised Shell company’s market value close to

US$175 billion. This acquisition will also add to cash flow, increase flagging reserves and

production, and strengthen its capability to pay dividends. (Bloomberg, 2016)

Shell, which is already one of the main non-state manufacturer of Liquefied Natural Gas

(LNG), after the acquisition, has become nearly twice the size of its closest competitor, which

is Exxon Mobil Corp. Purchasing of BG group gave Shell company admission to liquefaction

terminals from Trinidad and Tobago to Australia, a fleet of tankers in order to carry the fuel

and an global team of traders (Bloomberg, 2016).

b. Getting Stronger in LNG market:

One of the prime strategy of Shell company to acquire BG Group was there were some first-

class assets which BG Group had struggled to progress them as easily as they had expected.

Since, Shell company had a broader group of expertise and considerably better access to

investment capital, it could be able to use these resources from BG Group. This also provides

Shell company with an existence in the productive zone which is off the coast of Brazil, and

would safeguard that Shell company’s own production is continued over the medium term.

This has taken away the obligation of making huge discoveries to offset natural depletion

(Kollewe, 2015).

After having acquired the BG Group, the company got coverage to vast Santos basin

reserves in Brazil, and additional participation in the LNG market (Kollewe, 2015).

a. Getting an edge over it Rival and expanding:

Royal Dutch Shell Plc after finishing its largest acquisition of BG Group, has become bigger

than it rival Chevron Corp. This company, thus, has become the second largest non-state oil

company in the world. This acquisition of has allowed Shell company to grow dominant

especially in global LNG and it has taken Shell company to a greater presence in high-

potential offshore fields in Brazil.

This takeover of BG Group Plc by Shell has raised Shell company’s market value close to

US$175 billion. This acquisition will also add to cash flow, increase flagging reserves and

production, and strengthen its capability to pay dividends. (Bloomberg, 2016)

Shell, which is already one of the main non-state manufacturer of Liquefied Natural Gas

(LNG), after the acquisition, has become nearly twice the size of its closest competitor, which

is Exxon Mobil Corp. Purchasing of BG group gave Shell company admission to liquefaction

terminals from Trinidad and Tobago to Australia, a fleet of tankers in order to carry the fuel

and an global team of traders (Bloomberg, 2016).

b. Getting Stronger in LNG market:

One of the prime strategy of Shell company to acquire BG Group was there were some first-

class assets which BG Group had struggled to progress them as easily as they had expected.

Since, Shell company had a broader group of expertise and considerably better access to

investment capital, it could be able to use these resources from BG Group. This also provides

Shell company with an existence in the productive zone which is off the coast of Brazil, and

would safeguard that Shell company’s own production is continued over the medium term.

This has taken away the obligation of making huge discoveries to offset natural depletion

(Kollewe, 2015).

After having acquired the BG Group, the company got coverage to vast Santos basin

reserves in Brazil, and additional participation in the LNG market (Kollewe, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 2: BG and Shell combined LNG production prediction till 2018

(Bloomberg, 2016)

BG groups liquefied natural gas( LNG portfolio) joined with Shell company’s would

symbolise c40mtpa [circa 40 million tonnes per annum] or which is approximately 16% of

the global LNG market, further pushing Shell company’s spot as a leader in this LNG area. In

addition to this, Shell has acquired important progress options containing Tanzania and Lake

Charles LNG. BG Group’s assets has given Shell an additional grip in one of the lowest cost

basins in the world, and has potential added synergies with Shell’s Libra assets (Kollewe,

2015).

a. Having a Bigger Reserves of Oil and Gas:

Royal Dutch Shell company’s reserves have dropped in continuously, whereas BG’s have

increased in most of the years. The volume of oil and gas these companies hold under the

ground shows the value of the company. Shell company’s reserves have dropped by 563

million barrels since the year 2010, whereas BG has added 796 million to reserves.

(Bloomberg, 2016)

(Bloomberg, 2016)

BG groups liquefied natural gas( LNG portfolio) joined with Shell company’s would

symbolise c40mtpa [circa 40 million tonnes per annum] or which is approximately 16% of

the global LNG market, further pushing Shell company’s spot as a leader in this LNG area. In

addition to this, Shell has acquired important progress options containing Tanzania and Lake

Charles LNG. BG Group’s assets has given Shell an additional grip in one of the lowest cost

basins in the world, and has potential added synergies with Shell’s Libra assets (Kollewe,

2015).

a. Having a Bigger Reserves of Oil and Gas:

Royal Dutch Shell company’s reserves have dropped in continuously, whereas BG’s have

increased in most of the years. The volume of oil and gas these companies hold under the

ground shows the value of the company. Shell company’s reserves have dropped by 563

million barrels since the year 2010, whereas BG has added 796 million to reserves.

(Bloomberg, 2016)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 3: Shell Company Oil and Gas Reserve are dropping while BG's was increasing in year 2014

(Bloomberg, 2016)

3.2.2. Challenges of this acquisition to the merger (Royal Dutch Shell PLC):

a. Risk of Shares falling:

Shares of BG Group had dropped by almost a third in the year 2014, primarily because of its

experience to a sequence of distressed projects in Brazil and the price that were connected

with the start-up of a new LNG project in Australia.

Royal Dutch Shell is attracting more risk by allotting additional shares and also by paying out

cash to shareholders of BG Groups Therefore, balance sheet of them would have become

overextended. This possibly kept some kind of tension on the dividend as they send cash

flows for paying the debt before growing of their dividend (Kollewe, 2015).

b. Risk of Market Worsening and loosing Investors:

Shell company has amplified its estimation for operating-cost savings from the merger. It also

had plans to cut off 2,800 jobs from the united company and had reduced expenditure

predictions in an effort to secure and win backing from its shareholders (Bloomberg, 2016).

However, it can be seen that, it has failed to convince some of these shareholders. Standard

Life Investments which is Shell companies 11th- largest shareholder, had to vote against the

(Bloomberg, 2016)

3.2.2. Challenges of this acquisition to the merger (Royal Dutch Shell PLC):

a. Risk of Shares falling:

Shares of BG Group had dropped by almost a third in the year 2014, primarily because of its

experience to a sequence of distressed projects in Brazil and the price that were connected

with the start-up of a new LNG project in Australia.

Royal Dutch Shell is attracting more risk by allotting additional shares and also by paying out

cash to shareholders of BG Groups Therefore, balance sheet of them would have become

overextended. This possibly kept some kind of tension on the dividend as they send cash

flows for paying the debt before growing of their dividend (Kollewe, 2015).

b. Risk of Market Worsening and loosing Investors:

Shell company has amplified its estimation for operating-cost savings from the merger. It also

had plans to cut off 2,800 jobs from the united company and had reduced expenditure

predictions in an effort to secure and win backing from its shareholders (Bloomberg, 2016).

However, it can be seen that, it has failed to convince some of these shareholders. Standard

Life Investments which is Shell companies 11th- largest shareholder, had to vote against the

tie-up, quoting “downside risks” to the Shell company’s oil-price expectations amongst other

concerns (Bloomberg, 2016).

While Shell company has ensured buying BG Group would improve its aptitude to keep the

pay-out safe, the downfall in oil prices has compelled its dividend yield to the uppermost in at

least 30 years. Although Shell has secured backing for the transaction from a major

shareholder advisory firm, it can be seen that some of these investors still don’t completely

believe these initiates (Deloitte Center, 2015).

c. LNG market slowing down:

Shell company would certainly have to deal with an LNG market which is also going through

the process of slowdown. According to assessments by New York-based World Gas

Intelligence, the price of Liquefied Natural Gas (LNG) for short-term distributions to

Northeast Asia had gone down more than 26 percent in the past year 2014 to about $7.10 per

million British thermal units.(Bloomberg, 2016).

3.3. Noble Energy Acquisition of Rosetta Resources:

Noble Energy, Inc. proclaimed that it had accomplished the acquisition of Rosetta

Resources, Inc., after the latter’s shareholders approved the transaction in 2015. Thus,

Rosetta Resources became a solely owned subsidiary of Noble Energy (Zacks Equity

Research, 2015).

The deal states that for each Rosetta Resources share, its stockholder would receive 0.542

share of Noble Energy shared stock. Noble Energy will issue around 41 million shares of

common stock and take on Rosetta Resources’ net debt of $1.8 billion as a part of the

transaction.

This acquisition was a $2.1 billion acquisition which was announced May 2015. The

transaction for the acquisition was completed well in time (Zacks Equity Research, 2015).

3.3.1. Benefit of this deal to Merger (Noble Energy):

a. Eagle Ford Oil Field:

Noble will add 1,800 drilling sites in two of the three biggest U.S. shale oil fields with the

acquisition of Rosetta Resources. Rosetta’s assets contain 56,000 acres in the Permian and

concerns (Bloomberg, 2016).

While Shell company has ensured buying BG Group would improve its aptitude to keep the

pay-out safe, the downfall in oil prices has compelled its dividend yield to the uppermost in at

least 30 years. Although Shell has secured backing for the transaction from a major

shareholder advisory firm, it can be seen that some of these investors still don’t completely

believe these initiates (Deloitte Center, 2015).

c. LNG market slowing down:

Shell company would certainly have to deal with an LNG market which is also going through

the process of slowdown. According to assessments by New York-based World Gas

Intelligence, the price of Liquefied Natural Gas (LNG) for short-term distributions to

Northeast Asia had gone down more than 26 percent in the past year 2014 to about $7.10 per

million British thermal units.(Bloomberg, 2016).

3.3. Noble Energy Acquisition of Rosetta Resources:

Noble Energy, Inc. proclaimed that it had accomplished the acquisition of Rosetta

Resources, Inc., after the latter’s shareholders approved the transaction in 2015. Thus,

Rosetta Resources became a solely owned subsidiary of Noble Energy (Zacks Equity

Research, 2015).

The deal states that for each Rosetta Resources share, its stockholder would receive 0.542

share of Noble Energy shared stock. Noble Energy will issue around 41 million shares of

common stock and take on Rosetta Resources’ net debt of $1.8 billion as a part of the

transaction.

This acquisition was a $2.1 billion acquisition which was announced May 2015. The

transaction for the acquisition was completed well in time (Zacks Equity Research, 2015).

3.3.1. Benefit of this deal to Merger (Noble Energy):

a. Eagle Ford Oil Field:

Noble will add 1,800 drilling sites in two of the three biggest U.S. shale oil fields with the

acquisition of Rosetta Resources. Rosetta’s assets contain 56,000 acres in the Permian and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

50,000 acres in the Eagle Ford. Rosetta manufactured 66,000 barrels a day of oil and gas in

the first quarter of 2015 from these two sites. Over 60 percent of the production were liquids

(Olson & Polson, 2015).

b. Merger and Acquisition is the cheapest way to growth

Noble Energy now has set other acquisition targets are probable to have productions in West

Texas’s Permian Basin, including Matador Resources Co., Carrizo Oil & Gas Inc., Callon

Petroleum Co., and other minor companies parallel to Rosetta.

Martijn Rats who is an oil analyst at Morgan Stanley, said in a report that Merger and

Acquisition was perhaps an inexpensive choice for growth. Upstream Merger and Acquisition

is bound to grow; as big companies show interest on taking over small companies.

Shale oil giants from EOG Resources Inc. to Exxon Mobil Corp. have all indicated their

curiosity in taking advantage of lower evaluations in order to enhance to their North

American shale resources (Olson & Polson, 2015).

3.3.2. Challenges of this deal to the Merger (Noble Energy):

a. Risk of Share falling:

The Noble-Rosetta deal made by Noble Energy in best interest of acquisition of Rosetta

Resource, received firstly negative reply from investors, with Noble’s shares being reduced

around 5 per cent in early 2015 (Financial Times, 2015). By November 2015, Noble Energy's

stock price dropped nearly 6 percent to $45.31 (Menton, 2015).

b. Dept Consolidation of Rosetta Resources and its shareholders:

Noble had to obtain Rosetta in an all-stock deal and accept $1.8 billion in net debt. Also,

Rosetta resources’ shareholders would obtain 0.542 of a Noble share for every Rosetta share

they hold.

4. Summary:

Merger and Acquisition activity seem to have grown in the year 2014-2016 despite the oil

price dropping and no one knowing when it would recover. There are various internal and

external factors that have led companies to use Merge and Acquisition activity.

the first quarter of 2015 from these two sites. Over 60 percent of the production were liquids

(Olson & Polson, 2015).

b. Merger and Acquisition is the cheapest way to growth

Noble Energy now has set other acquisition targets are probable to have productions in West

Texas’s Permian Basin, including Matador Resources Co., Carrizo Oil & Gas Inc., Callon

Petroleum Co., and other minor companies parallel to Rosetta.

Martijn Rats who is an oil analyst at Morgan Stanley, said in a report that Merger and

Acquisition was perhaps an inexpensive choice for growth. Upstream Merger and Acquisition

is bound to grow; as big companies show interest on taking over small companies.

Shale oil giants from EOG Resources Inc. to Exxon Mobil Corp. have all indicated their

curiosity in taking advantage of lower evaluations in order to enhance to their North

American shale resources (Olson & Polson, 2015).

3.3.2. Challenges of this deal to the Merger (Noble Energy):

a. Risk of Share falling:

The Noble-Rosetta deal made by Noble Energy in best interest of acquisition of Rosetta

Resource, received firstly negative reply from investors, with Noble’s shares being reduced

around 5 per cent in early 2015 (Financial Times, 2015). By November 2015, Noble Energy's

stock price dropped nearly 6 percent to $45.31 (Menton, 2015).

b. Dept Consolidation of Rosetta Resources and its shareholders:

Noble had to obtain Rosetta in an all-stock deal and accept $1.8 billion in net debt. Also,

Rosetta resources’ shareholders would obtain 0.542 of a Noble share for every Rosetta share

they hold.

4. Summary:

Merger and Acquisition activity seem to have grown in the year 2014-2016 despite the oil

price dropping and no one knowing when it would recover. There are various internal and

external factors that have led companies to use Merge and Acquisition activity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From two big Merge and Acquisition that took place between 2014-2016, one can see that big

companies are highly interested in taking over small companies as these companies are

struggling with capital and existence. Thus, big companies are trying to get these small

companies as a bargin. The other reason dominant for this activity can be oil reserves and

other assets. As one can see Royal Shell Dutch company took the BG company primarily

because of it dominant presence in LNG and shores of Brazil. Similarly, the Noble Energy

also took the Rosetta Resource for its presence in Permian and England Ford.

Similarily, one can see the main challenges these companies are facing is falling of share

market values of the companies. Also, share distribution and shareholder distribution can be a

challenge to the merger.

5. References

1. Bloomberg, 2016. Deal or No Deal? The Numbers That Matter for Shell's BG Takeover.

[Online]

Available at: http://www.bloomberg.com/news/articles/2016-01-11/deal-or-no-deal-the-

numbers-that-matter-for-shell-s-bg-takeover

[Accessed 30 July 2016].

2. Deloitte Center, 2014. Oil & Gas Mergers and Acquisitions Report: Year-end 2014.

[Online]

Available at: http://www2.deloitte.com/us/en/pages/energy-and-resources/articles/oil-and-

gas-mergers-and-acquisitions-report-year-end-2014.html

[Accessed 18 07 2016].

3. Deloitte Center, 2015. Deloitte Oil & Gas Mergers and Acquisitions Report –2015

Update. [Online]

Available at: http://www2.deloitte.com/us/en/pages/energy-and-resources/articles/oil-and-

gas-mergers-and-acquisitions-update.html

[Accessed 20 August 2016].

4. Egan, M., 2016. U.S. oil bankruptcies spike 379%. [Online]

Available at: http://money.cnn.com/2016/02/11/investing/oil-prices-bankruptcies-spike/

[Accessed 24 07 2016].

5. England, J., 2016. 2016 Outlook on the Oil and Gas industry. [Online]

Available at: http://www2.deloitte.com/us/en/pages/energy-and-resources/articles/oil-and-

gas-industry-outlook.html

[Accessed 28 July 2016].

6. Ernst & Young Global Limited, 2015. Global oil and transactions review 2015. [Online]

Available at: http://www.ey.com/Publication/vwLUAssets/EY-global-oil-and-gas-

companies are highly interested in taking over small companies as these companies are

struggling with capital and existence. Thus, big companies are trying to get these small

companies as a bargin. The other reason dominant for this activity can be oil reserves and

other assets. As one can see Royal Shell Dutch company took the BG company primarily

because of it dominant presence in LNG and shores of Brazil. Similarly, the Noble Energy

also took the Rosetta Resource for its presence in Permian and England Ford.

Similarily, one can see the main challenges these companies are facing is falling of share

market values of the companies. Also, share distribution and shareholder distribution can be a

challenge to the merger.

5. References

1. Bloomberg, 2016. Deal or No Deal? The Numbers That Matter for Shell's BG Takeover.

[Online]

Available at: http://www.bloomberg.com/news/articles/2016-01-11/deal-or-no-deal-the-

numbers-that-matter-for-shell-s-bg-takeover

[Accessed 30 July 2016].

2. Deloitte Center, 2014. Oil & Gas Mergers and Acquisitions Report: Year-end 2014.

[Online]

Available at: http://www2.deloitte.com/us/en/pages/energy-and-resources/articles/oil-and-

gas-mergers-and-acquisitions-report-year-end-2014.html

[Accessed 18 07 2016].

3. Deloitte Center, 2015. Deloitte Oil & Gas Mergers and Acquisitions Report –2015

Update. [Online]

Available at: http://www2.deloitte.com/us/en/pages/energy-and-resources/articles/oil-and-

gas-mergers-and-acquisitions-update.html

[Accessed 20 August 2016].

4. Egan, M., 2016. U.S. oil bankruptcies spike 379%. [Online]

Available at: http://money.cnn.com/2016/02/11/investing/oil-prices-bankruptcies-spike/

[Accessed 24 07 2016].

5. England, J., 2016. 2016 Outlook on the Oil and Gas industry. [Online]

Available at: http://www2.deloitte.com/us/en/pages/energy-and-resources/articles/oil-and-

gas-industry-outlook.html

[Accessed 28 July 2016].

6. Ernst & Young Global Limited, 2015. Global oil and transactions review 2015. [Online]

Available at: http://www.ey.com/Publication/vwLUAssets/EY-global-oil-and-gas-

transactions-review-2015/$FILE/EY-global-oil-and-gas-transactions-review-2015.pdf

[Accessed 29 July 2016].

7. Financial Times, 2015. Noble Energy to buy Rosetta Resources in $3.7bn shale deal.

[Online]

Available at: http://www.ft.com/cms/s/0/e00e29c0-f7da-11e4-9beb-

00144feab7de.html#axzz4GIpy5zJd

[Accessed 31 July 2016].

8. Hsu, K.-C., Wright, M. & Zhu, Z., 2015. What Motivates Merger and Acquisition

Activities in the Upstream Oil & Gas Sectors in the U.S.?. [Online]

Available at: http://www.usaee.org/usaee2015/submissions/OnlineProceedings/M&A

%20Hsu-Wright-Zhu.pdf

[Accessed 23 July 2016].

9. Kollewe, J., 2015. Shell takeover of BG: what the analysts say. [Online]

Available at: https://www.theguardian.com/business/2015/apr/08/shell-takeover-of-bg-

what-the-analysts-say

[Accessed 01 August 2016].

10. Kollewe, J. & Farrell, S., 2015. Shell agrees to buy BG Group for £47bn. [Online]

Available at: https://www.theguardian.com/business/2015/apr/08/shell-bg-group-47bn-

takeover-oil-industry

[Accessed 22 July 2016].

11. KRAUSS, C., 2016. Exxon Mobil’s Sterling Credit Is Downgraded by Standard &

Poor’s. [Online]

Available at: http://www.nytimes.com/2016/04/27/business/energy-environment/exxon-

mobils-sterling-credit-is-downgraded-by-standard-poors.html

[Accessed 29 July 2016].

12. Mattioli, D. & D, C., 2015. Energy M&A Surges Despite Oil Slump. The Wall Street

Journal.

13. Menton, J., 2015. Rosetta Resources Inc (ROSE) Stock Price Soars 28% On $2B Noble

Energy Inc (NBL) Deal. [Online]

Available at: http://www.ibtimes.com/rosetta-resources-inc-rose-stock-price-soars-28-2b-

noble-energy-inc-nbl-deal-1916881

[Accessed 28 July 2016].

14. New York Times, 2016. Oil Prices: What’s Behind the Drop? Simple Economics.

[Online]

Available at: http://www.nytimes.com/interactive/2016/business/energy-environment/oil-

prices.html

[Accessed 28 July 2016].

15. Olson, B. & Polson, J., 2015. This $2.1 Billion Shale Deal Will Be the First of Many.

[Online]

Available at: http://www.bloomberg.com/news/articles/2015-05-11/noble-energy-buys-

[Accessed 29 July 2016].

7. Financial Times, 2015. Noble Energy to buy Rosetta Resources in $3.7bn shale deal.

[Online]

Available at: http://www.ft.com/cms/s/0/e00e29c0-f7da-11e4-9beb-

00144feab7de.html#axzz4GIpy5zJd

[Accessed 31 July 2016].

8. Hsu, K.-C., Wright, M. & Zhu, Z., 2015. What Motivates Merger and Acquisition

Activities in the Upstream Oil & Gas Sectors in the U.S.?. [Online]

Available at: http://www.usaee.org/usaee2015/submissions/OnlineProceedings/M&A

%20Hsu-Wright-Zhu.pdf

[Accessed 23 July 2016].

9. Kollewe, J., 2015. Shell takeover of BG: what the analysts say. [Online]

Available at: https://www.theguardian.com/business/2015/apr/08/shell-takeover-of-bg-

what-the-analysts-say

[Accessed 01 August 2016].

10. Kollewe, J. & Farrell, S., 2015. Shell agrees to buy BG Group for £47bn. [Online]

Available at: https://www.theguardian.com/business/2015/apr/08/shell-bg-group-47bn-

takeover-oil-industry

[Accessed 22 July 2016].

11. KRAUSS, C., 2016. Exxon Mobil’s Sterling Credit Is Downgraded by Standard &

Poor’s. [Online]

Available at: http://www.nytimes.com/2016/04/27/business/energy-environment/exxon-

mobils-sterling-credit-is-downgraded-by-standard-poors.html

[Accessed 29 July 2016].

12. Mattioli, D. & D, C., 2015. Energy M&A Surges Despite Oil Slump. The Wall Street

Journal.

13. Menton, J., 2015. Rosetta Resources Inc (ROSE) Stock Price Soars 28% On $2B Noble

Energy Inc (NBL) Deal. [Online]

Available at: http://www.ibtimes.com/rosetta-resources-inc-rose-stock-price-soars-28-2b-

noble-energy-inc-nbl-deal-1916881

[Accessed 28 July 2016].

14. New York Times, 2016. Oil Prices: What’s Behind the Drop? Simple Economics.

[Online]

Available at: http://www.nytimes.com/interactive/2016/business/energy-environment/oil-

prices.html

[Accessed 28 July 2016].

15. Olson, B. & Polson, J., 2015. This $2.1 Billion Shale Deal Will Be the First of Many.

[Online]

Available at: http://www.bloomberg.com/news/articles/2015-05-11/noble-energy-buys-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.