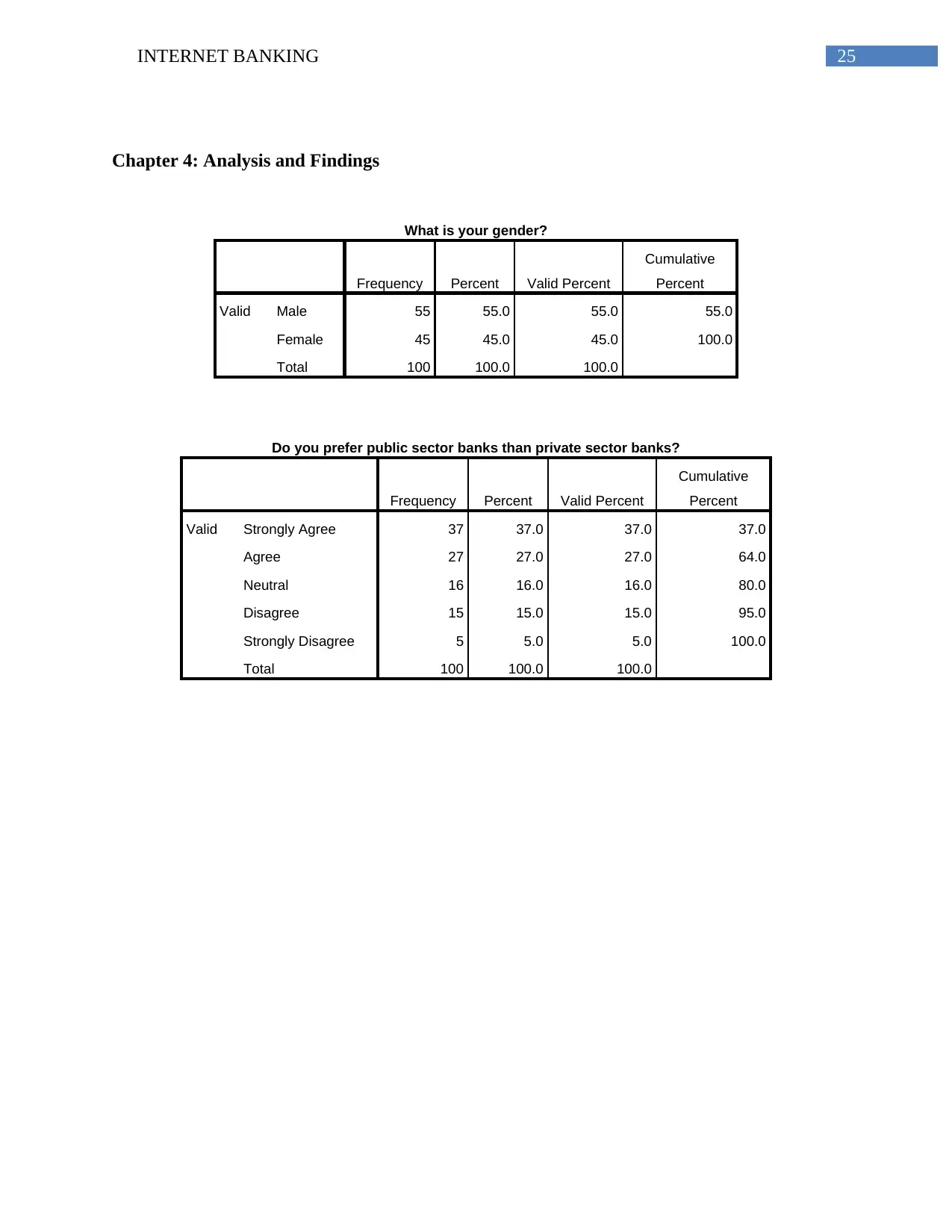

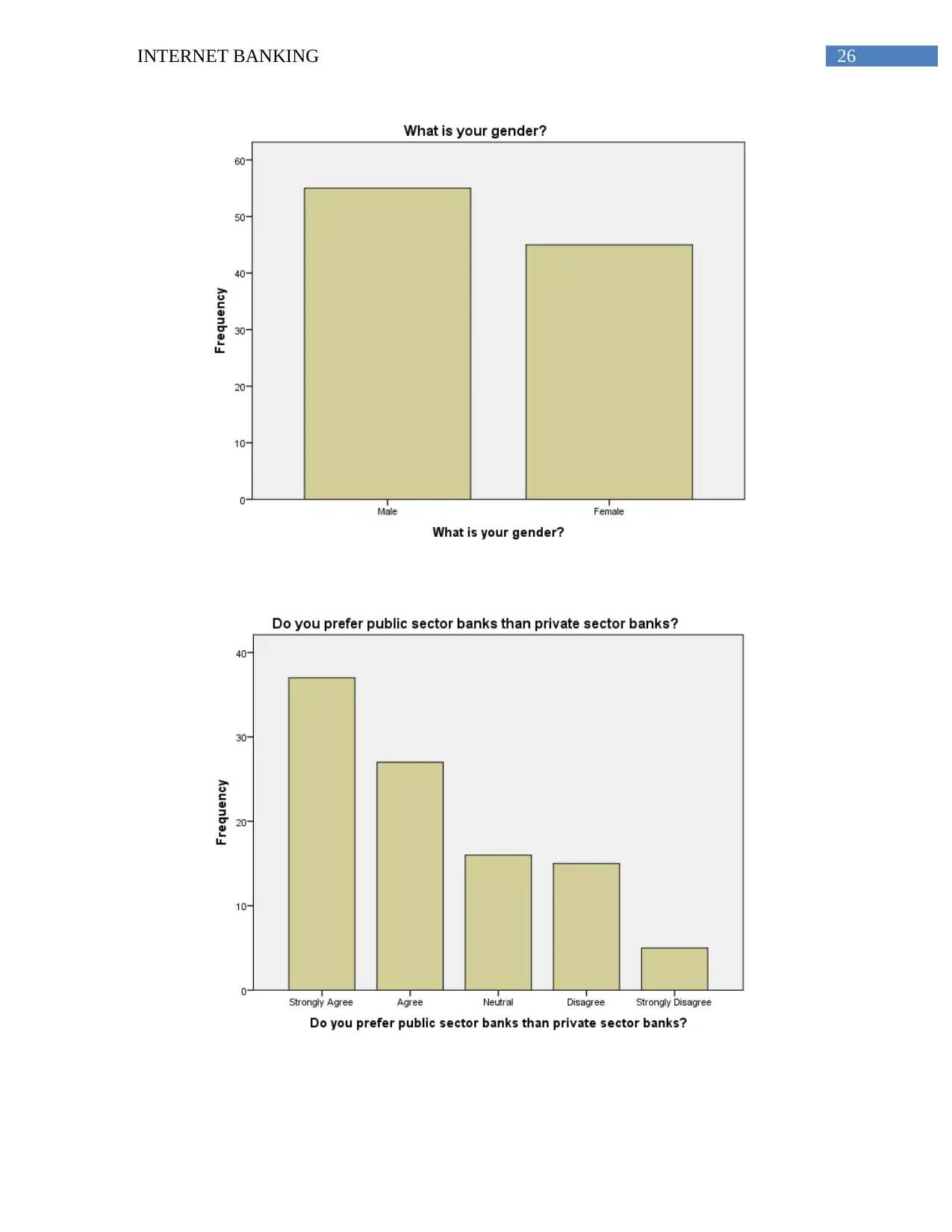

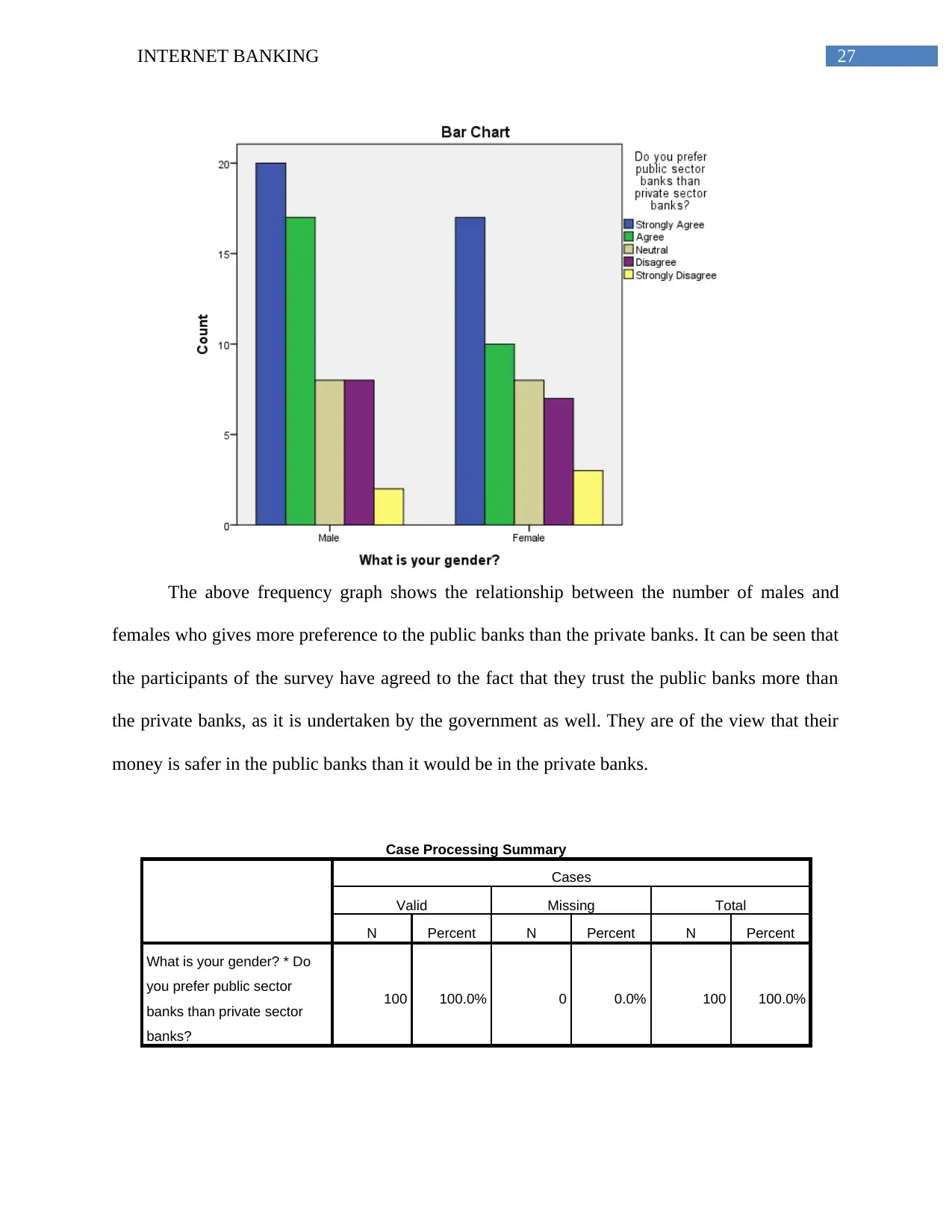

Impact of Internet Banking on Customers

VerifiedAdded on 2020/02/24

|60

|11205

|115

AI Summary

This assignment delves into the impact of internet banking on customers. It examines factors influencing customer adoption, explores the benefits and drawbacks of online banking, and analyzes customer satisfaction levels with internet banking services. The analysis draws upon research studies and empirical data to provide insights into this evolving financial landscape.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: INTERNET BANKING

Impact of Internet Banking System and Technology on Indian Banks

Name of the Student

Name of the University

Author Note

Impact of Internet Banking System and Technology on Indian Banks

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1INTERNET BANKING

Abstract

The banking sector will be successful and will survive if they can maintain their customers and

broaden their base of customers as well. The satisfaction of the customers also plays an

important part, as it will help the bank in retaining its customers, which will help in increasing

their profits and result in better performance for the banks. The use of technology has changed

the perception of the people, as it has helped them in carrying out their work in an easy manner.

The banking sector has also adopted the latest technologies that are available to them so that it

can make the work easy for the customers as well as for its employees. The customers in the

current scenario are shifting from the approaches that are present in traditional banking methods

to the modern day practices of banking systems. This has helped in reducing their costs and

being more effective towards the customers.

This study has been conducted in five chapters. The first chapter contains the background of the

study along with the aims and questions and hypothesis that will help in carrying out the research

in an efficient manner. The second chapter deals with the review of literature that has been

presented by different authors and scholars so that it can help the researcher in completing the

study in an appropriate manner. The third chapter contains the methods that have been used by

the researcher so that the process of research can be conducted in a better manner. The fourth

chapter contains the analysis, which has been conducted by the researcher so that it can provide a

better recommendation for the banks and its customers. The fifth chapter consists of the

recommendation and conclusion, which has been gathered after the researcher has got the

responses and conducting the test with the help of software.

Abstract

The banking sector will be successful and will survive if they can maintain their customers and

broaden their base of customers as well. The satisfaction of the customers also plays an

important part, as it will help the bank in retaining its customers, which will help in increasing

their profits and result in better performance for the banks. The use of technology has changed

the perception of the people, as it has helped them in carrying out their work in an easy manner.

The banking sector has also adopted the latest technologies that are available to them so that it

can make the work easy for the customers as well as for its employees. The customers in the

current scenario are shifting from the approaches that are present in traditional banking methods

to the modern day practices of banking systems. This has helped in reducing their costs and

being more effective towards the customers.

This study has been conducted in five chapters. The first chapter contains the background of the

study along with the aims and questions and hypothesis that will help in carrying out the research

in an efficient manner. The second chapter deals with the review of literature that has been

presented by different authors and scholars so that it can help the researcher in completing the

study in an appropriate manner. The third chapter contains the methods that have been used by

the researcher so that the process of research can be conducted in a better manner. The fourth

chapter contains the analysis, which has been conducted by the researcher so that it can provide a

better recommendation for the banks and its customers. The fifth chapter consists of the

recommendation and conclusion, which has been gathered after the researcher has got the

responses and conducting the test with the help of software.

2INTERNET BANKING

Acknowledgment

I would also like to take this opportunity to thank my professor without whose, constant support

and guidance, the research would not have been possible.

Firstly, I would like to thank God the Almighty in giving me the strength and courage without

which I could not have completed the entire study. Secondly, I would like to thank my family

and relatives who gave me constant support mentally and physically so that I can complete the

study on time. Lastly, I would like to give thanks to my peers and the friends who have helped

me in providing the appropriate information throughout the project and helped me in doing the

in-depth analysis of the research. Without their proper guidance, it is impossible for me to

complete the project.

Thanks and Regards,

Yours Sincerely,

Acknowledgment

I would also like to take this opportunity to thank my professor without whose, constant support

and guidance, the research would not have been possible.

Firstly, I would like to thank God the Almighty in giving me the strength and courage without

which I could not have completed the entire study. Secondly, I would like to thank my family

and relatives who gave me constant support mentally and physically so that I can complete the

study on time. Lastly, I would like to give thanks to my peers and the friends who have helped

me in providing the appropriate information throughout the project and helped me in doing the

in-depth analysis of the research. Without their proper guidance, it is impossible for me to

complete the project.

Thanks and Regards,

Yours Sincerely,

3INTERNET BANKING

Table of Contents

Chapter 1: Introduction....................................................................................................................5

Background of the study..............................................................................................................5

Aim of the project........................................................................................................................7

Details of the research.................................................................................................................7

Justification of the topic...............................................................................................................8

Assistance to the organization.....................................................................................................8

Research questions.......................................................................................................................8

Research Hypothesis....................................................................................................................8

Chapter 2: Literature Review.........................................................................................................10

Internet Banking........................................................................................................................10

Trust...........................................................................................................................................11

Quality of service.......................................................................................................................12

Perceived ease of use.................................................................................................................13

Perceived usefulness..................................................................................................................14

Customer satisfaction.................................................................................................................15

Impact of e-banking on the customers.......................................................................................16

Chapter 3: Research Methodology................................................................................................19

Approaches for the study...........................................................................................................19

Research method used...............................................................................................................20

Table of Contents

Chapter 1: Introduction....................................................................................................................5

Background of the study..............................................................................................................5

Aim of the project........................................................................................................................7

Details of the research.................................................................................................................7

Justification of the topic...............................................................................................................8

Assistance to the organization.....................................................................................................8

Research questions.......................................................................................................................8

Research Hypothesis....................................................................................................................8

Chapter 2: Literature Review.........................................................................................................10

Internet Banking........................................................................................................................10

Trust...........................................................................................................................................11

Quality of service.......................................................................................................................12

Perceived ease of use.................................................................................................................13

Perceived usefulness..................................................................................................................14

Customer satisfaction.................................................................................................................15

Impact of e-banking on the customers.......................................................................................16

Chapter 3: Research Methodology................................................................................................19

Approaches for the study...........................................................................................................19

Research method used...............................................................................................................20

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

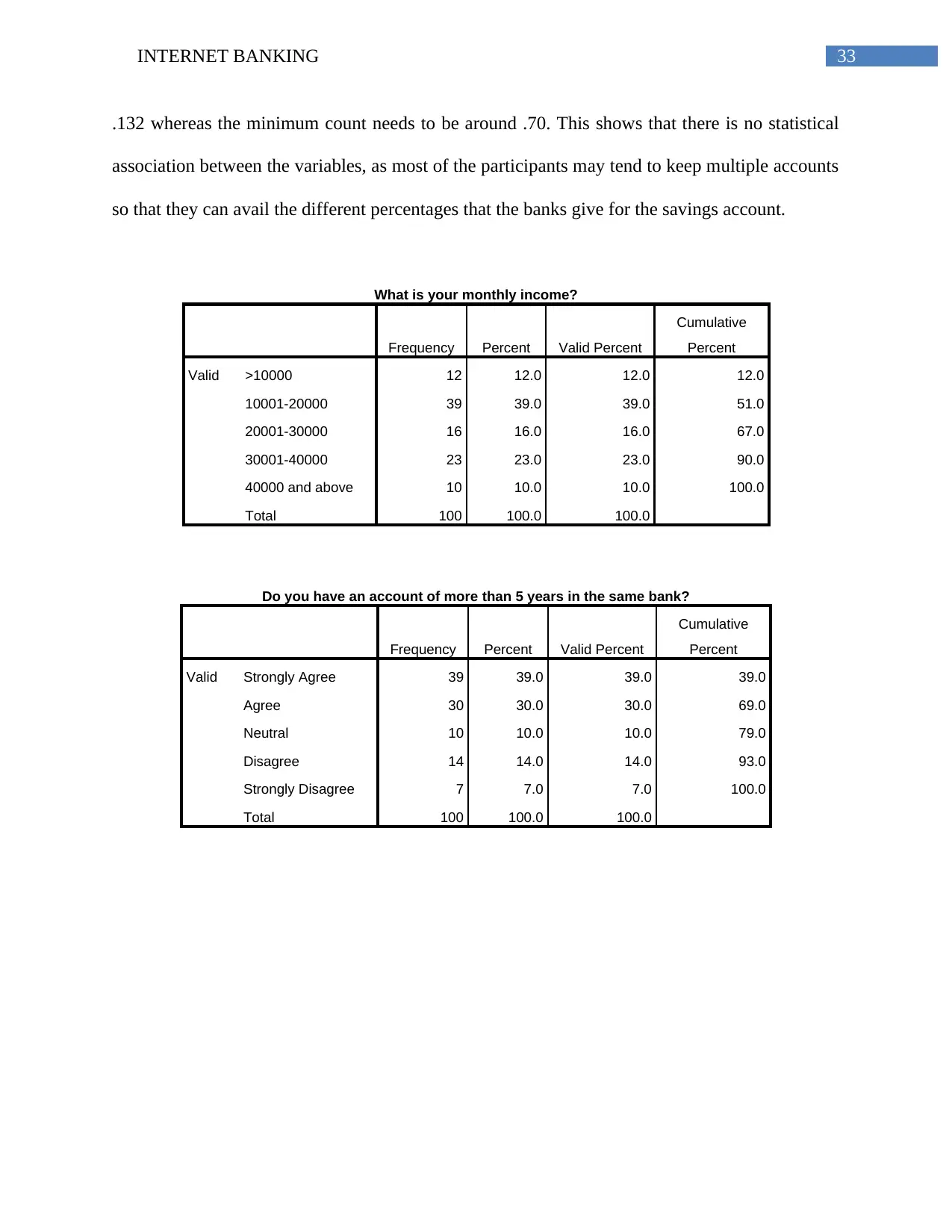

4INTERNET BANKING

Quantitative method...................................................................................................................20

Qualitative method.....................................................................................................................21

Project content...........................................................................................................................21

Data collection...........................................................................................................................21

Analysis of the data...................................................................................................................22

Types of investigation................................................................................................................22

Research Philosophy......................................................................................................................23

Justification of the investigation type used................................................................................24

Chapter 4: Analysis and Findings..................................................................................................25

Chapter 5: Conclusion and Recommendation...............................................................................49

Findings.....................................................................................................................................49

Limitations.................................................................................................................................50

Recommendations......................................................................................................................50

Reference List................................................................................................................................52

Appendix........................................................................................................................................56

Quantitative method...................................................................................................................20

Qualitative method.....................................................................................................................21

Project content...........................................................................................................................21

Data collection...........................................................................................................................21

Analysis of the data...................................................................................................................22

Types of investigation................................................................................................................22

Research Philosophy......................................................................................................................23

Justification of the investigation type used................................................................................24

Chapter 4: Analysis and Findings..................................................................................................25

Chapter 5: Conclusion and Recommendation...............................................................................49

Findings.....................................................................................................................................49

Limitations.................................................................................................................................50

Recommendations......................................................................................................................50

Reference List................................................................................................................................52

Appendix........................................................................................................................................56

5INTERNET BANKING

Chapter 1: Introduction

Background of the study

The introduction of the technological advances has helped in the field of information

technology with respect to the banking industries on a global basis, as it has reduced the degree

pressure up on the consumers. The development in the field of telecommunications along with

the electronic processes of data has also helped in adopting these changes by using the latest

technologies in the banking business. The level of competition has also increased, as the method

has proved to be cheaper and effective towards the services that are provided by the banks to its

customers, as they are in need to avail the services of the banks at a faster rate (Krishna 2015).

The health and prosperity of any nation depends on the system of banking that the

country has so that it can help the customers in investing their money and trusting the services of

the bank. The rise of the commercial banks started in India after the country became

independent, which led to the formation of the Reserve Bank of India (RBI) so that the services

of the banks can be monitored in an efficient manner (Charfeddine and Nasri 2015). The rise in

the private and foreign banks along with the public sector banks has helped the customers in

availing the systems such as e-banking, t-banking and m-banking suggests that the banks have

come a long way forward. The banking sector that is present in India has come up a long way

and is undergoing continuous changes in its systems so that it can provide better services to its

customers. This will help the banks in satisfying the customers, which may lead to the retention

of the customers by the bank (George and Kumar 2014).

During the past years, it can be seen that the banks used to have large queues for paying

the utility bills or for depositing and withdrawing the cash from the banks. This has been reduced

Chapter 1: Introduction

Background of the study

The introduction of the technological advances has helped in the field of information

technology with respect to the banking industries on a global basis, as it has reduced the degree

pressure up on the consumers. The development in the field of telecommunications along with

the electronic processes of data has also helped in adopting these changes by using the latest

technologies in the banking business. The level of competition has also increased, as the method

has proved to be cheaper and effective towards the services that are provided by the banks to its

customers, as they are in need to avail the services of the banks at a faster rate (Krishna 2015).

The health and prosperity of any nation depends on the system of banking that the

country has so that it can help the customers in investing their money and trusting the services of

the bank. The rise of the commercial banks started in India after the country became

independent, which led to the formation of the Reserve Bank of India (RBI) so that the services

of the banks can be monitored in an efficient manner (Charfeddine and Nasri 2015). The rise in

the private and foreign banks along with the public sector banks has helped the customers in

availing the systems such as e-banking, t-banking and m-banking suggests that the banks have

come a long way forward. The banking sector that is present in India has come up a long way

and is undergoing continuous changes in its systems so that it can provide better services to its

customers. This will help the banks in satisfying the customers, which may lead to the retention

of the customers by the bank (George and Kumar 2014).

During the past years, it can be seen that the banks used to have large queues for paying

the utility bills or for depositing and withdrawing the cash from the banks. This has been reduced

6INTERNET BANKING

considerably with the onset of the technological advances within the banking systems. The

consumers of the bank have reduced their waiting times by a considerable amount, as the

transactions of the bank have been made easy with the use of technology. The banks in the

current scenario have utilized the facilities that are present online, which has helped them in

reducing the paper work that resulted in giving better responses to the customers. The banking

industry was one of the first sectors that had a major impact due to the adoption of the latest

technologies, which changes there interactive interface with the customers (Varaprasad,

Sridharan and Unnithan 2015).

The main advantage that the banks get due to this technique is that they can be available

to serve the customers on a regular basis. The perception of the customers and the change in their

life style of the people has helped in the growth of the banking system. The analysis of the

attitudes of the customers towards the banking system has changed considerably because of the

use of advanced technologies (Kumar Sharma and Madhumohan Govindaluri 2014).

The banking sector has been undergoing the changes since the early 1990s with respect to

the use of information technology and the development that is being seen in the electronic

commerce as well. These developments have proved to be a threat regarding the operations that

have been managed by the bank in a traditional manner. It can be seen that the use of the

payment system that is electronic in nature may over emphasize the system of payments within

the country because of the vast changes due to the advancements in technology. It can also be

seen that with the onset of the new technologies can lead to the changes in digital monetary

system by replacing it with fiduciary currencies (Paul, Mittal and Srivastav 2016).

considerably with the onset of the technological advances within the banking systems. The

consumers of the bank have reduced their waiting times by a considerable amount, as the

transactions of the bank have been made easy with the use of technology. The banks in the

current scenario have utilized the facilities that are present online, which has helped them in

reducing the paper work that resulted in giving better responses to the customers. The banking

industry was one of the first sectors that had a major impact due to the adoption of the latest

technologies, which changes there interactive interface with the customers (Varaprasad,

Sridharan and Unnithan 2015).

The main advantage that the banks get due to this technique is that they can be available

to serve the customers on a regular basis. The perception of the customers and the change in their

life style of the people has helped in the growth of the banking system. The analysis of the

attitudes of the customers towards the banking system has changed considerably because of the

use of advanced technologies (Kumar Sharma and Madhumohan Govindaluri 2014).

The banking sector has been undergoing the changes since the early 1990s with respect to

the use of information technology and the development that is being seen in the electronic

commerce as well. These developments have proved to be a threat regarding the operations that

have been managed by the bank in a traditional manner. It can be seen that the use of the

payment system that is electronic in nature may over emphasize the system of payments within

the country because of the vast changes due to the advancements in technology. It can also be

seen that with the onset of the new technologies can lead to the changes in digital monetary

system by replacing it with fiduciary currencies (Paul, Mittal and Srivastav 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERNET BANKING

The rise in the multiple functions by the modern banks has helped them in providing

better and more products and services to its customers with the primary objective of satisfying

the customers and increasing its profit ratio. The process of innovation has helped the banks in

adopting new technologies along with better methods in serving the products and services, which

had started during the 1950s before most of the industries adopted it. The use of automatic

machines was started by the banks of United States of America, which led to the development of

most of the countries in the years to come (Mittal and Agarwal 2016).

Aim of the project

The aim of the project is to study the factors that are as follows:

The impact of internet banking offered by Indian banks to its customers

How much internet banking has penetrated in the minds of the customers

To gain insights about functioning of internet banking and technology

To explore the future prospects of internet banking and technology

Details of the research

The project will deal with the perceptions that the customers have regarding the adopting

of the technology in the banking system. The rise in the use of technological advances in the

banks have helped the customers in interacting with the services of the banks in an efficient

manner, which has helped the banks in establishing customer satisfaction by providing better

services. The research paper will be conducted to study the objective of the perceptions of the

customers regarding the services of the bank such as the e-banking system.

The rise in the multiple functions by the modern banks has helped them in providing

better and more products and services to its customers with the primary objective of satisfying

the customers and increasing its profit ratio. The process of innovation has helped the banks in

adopting new technologies along with better methods in serving the products and services, which

had started during the 1950s before most of the industries adopted it. The use of automatic

machines was started by the banks of United States of America, which led to the development of

most of the countries in the years to come (Mittal and Agarwal 2016).

Aim of the project

The aim of the project is to study the factors that are as follows:

The impact of internet banking offered by Indian banks to its customers

How much internet banking has penetrated in the minds of the customers

To gain insights about functioning of internet banking and technology

To explore the future prospects of internet banking and technology

Details of the research

The project will deal with the perceptions that the customers have regarding the adopting

of the technology in the banking system. The rise in the use of technological advances in the

banks have helped the customers in interacting with the services of the banks in an efficient

manner, which has helped the banks in establishing customer satisfaction by providing better

services. The research paper will be conducted to study the objective of the perceptions of the

customers regarding the services of the bank such as the e-banking system.

8INTERNET BANKING

Justification of the topic

This topic was chosen, as it will help the researcher in getting better insights about the

technologies that are being used in the Indian banks in providing better services to its customers,

which may help them in satisfying the customers with their services. The topic will also provide

valuable insights to the researcher regarding the impact of technological advancements on the

bank, which has resulted in serving the customers in a better manner.

Assistance to the organization

The research will be conducted taking in to consideration one of the public and private

banks and the customers of the banks, which will help in understanding the effectiveness of the

banks towards its customers. The private bank will be Housing Development Finance

Corporation (HDFC) and the public bank will be State Bank of India (SBI) along with some of

the customers of these banks who will help in conducting the research in an efficient manner.

Research questions

The research will be conducted based on the following questions:

What impact does the bank create on its customers by adopting new technologies?

What is the perception of the customers regarding the adoption of new technology in the

banks?

Research Hypothesis

The research will be conducted based on the following hypothesis:

H1: There is a relation between the banking services that are provided to the customer

based on gender, age, income and education

Justification of the topic

This topic was chosen, as it will help the researcher in getting better insights about the

technologies that are being used in the Indian banks in providing better services to its customers,

which may help them in satisfying the customers with their services. The topic will also provide

valuable insights to the researcher regarding the impact of technological advancements on the

bank, which has resulted in serving the customers in a better manner.

Assistance to the organization

The research will be conducted taking in to consideration one of the public and private

banks and the customers of the banks, which will help in understanding the effectiveness of the

banks towards its customers. The private bank will be Housing Development Finance

Corporation (HDFC) and the public bank will be State Bank of India (SBI) along with some of

the customers of these banks who will help in conducting the research in an efficient manner.

Research questions

The research will be conducted based on the following questions:

What impact does the bank create on its customers by adopting new technologies?

What is the perception of the customers regarding the adoption of new technology in the

banks?

Research Hypothesis

The research will be conducted based on the following hypothesis:

H1: There is a relation between the banking services that are provided to the customer

based on gender, age, income and education

9INTERNET BANKING

H2: The awareness levels among the customers of the public and the private banks have

no difference with respect to the banking services that are offered to them

H3: There is a significant difference in the usage of the banking services by the

customers based on gender, age, income and education

H2: The awareness levels among the customers of the public and the private banks have

no difference with respect to the banking services that are offered to them

H3: There is a significant difference in the usage of the banking services by the

customers based on gender, age, income and education

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10INTERNET BANKING

Chapter 2: Literature Review

Internet Banking

The lives of the individuals have been affected with the adoption of the latest

technologies in the current period in qualitative and quantitative ways respectively. The

expansion in the information technology has affected the lives of million people along with the

changes in the business and economic atmosphere all over the world. The adoption of these

technologies in the banking sector has helped them in communicating in a proper manner and the

process of transactions has sped up for the clients. The use of internet banking by the consumers

in the modern world is being adopted by the customers at a faster rate, as it has helped them in

minimizing their transaction process with the banks (Kaushik and Rahman 2015). The use of the

services provided by the banks has helped in creating a better channel so that the customers do

not need to visit the bank for any of their transactions, s it can be done while they are at work or

at home. This has helped in reducing the time of waiting, which has helped the consumers

significantly and has increased their trust towards their respective banks. The banks have been

able to eliminate their boundaries with respect to geographic and physical with the help of the

banking services. The traditional method of transactions in the bank was time consuming and

labor intensive, which is now replaced by the machines that is available at a cheaper price

(Chavan 2013).

The e-banking services that were adopted by the banks in India came in to effect from the

1990s with the rise in the usage of credit cards, telephone services and the Automatic Teller

Machine (ATM). The previous decade has shown that the banks have adopted the information

system, use of database and other latest technologies that have helped them in increasing the

Chapter 2: Literature Review

Internet Banking

The lives of the individuals have been affected with the adoption of the latest

technologies in the current period in qualitative and quantitative ways respectively. The

expansion in the information technology has affected the lives of million people along with the

changes in the business and economic atmosphere all over the world. The adoption of these

technologies in the banking sector has helped them in communicating in a proper manner and the

process of transactions has sped up for the clients. The use of internet banking by the consumers

in the modern world is being adopted by the customers at a faster rate, as it has helped them in

minimizing their transaction process with the banks (Kaushik and Rahman 2015). The use of the

services provided by the banks has helped in creating a better channel so that the customers do

not need to visit the bank for any of their transactions, s it can be done while they are at work or

at home. This has helped in reducing the time of waiting, which has helped the consumers

significantly and has increased their trust towards their respective banks. The banks have been

able to eliminate their boundaries with respect to geographic and physical with the help of the

banking services. The traditional method of transactions in the bank was time consuming and

labor intensive, which is now replaced by the machines that is available at a cheaper price

(Chavan 2013).

The e-banking services that were adopted by the banks in India came in to effect from the

1990s with the rise in the usage of credit cards, telephone services and the Automatic Teller

Machine (ATM). The previous decade has shown that the banks have adopted the information

system, use of database and other latest technologies that have helped them in increasing the

11INTERNET BANKING

services at various levels of the banks. The availability of the online facilities has helped the

services of the banks to be conducted through a secured website, which are operated by the

banks through the help of online enquiries, e-transfers and e-payments (Laudon and Laudon

2016).

Trust

The act of performance or the service that is provided to the bank and is intangible in

nature without acting as the owners of the service needs to be done in a careful manner. The

services that are intangible in nature may often result in problems among the customers, as they

might not be aware of the problems that they might face when availing the service. Therefore, it

is necessary for trust to be involved in managing the risks along with the vulnerability that the

customers may face with the respective services. The use of internet has led to increased

competition in the markets that are developed technologically, which makes it challenging for

the banks to maintain their relationships with the clients in a better manner. The factor of trust

and security that is provided by the banks to its customers helps in influencing the relationships

between the banks and its customers (Shaikh and Karjaluoto 2015). The banks try to maintain a

long-term relationship with the customers so that it helps them in developing their trust with the

customers. The perception of the customers is that they find it challenging in trusting the internet

banking options that are provided by the banks along with the other electronic commerce factors

that try to extract the information from the customers. Thus, it can be said that trust is a

multidimensional and complex phenomenon that may arise in the minds of the customers. It is

related to the factor of avoiding the risk and the security that the customers perceive about the

services that are being offered by the banks (Yadav, Chauhan and Pathak 2015).

services at various levels of the banks. The availability of the online facilities has helped the

services of the banks to be conducted through a secured website, which are operated by the

banks through the help of online enquiries, e-transfers and e-payments (Laudon and Laudon

2016).

Trust

The act of performance or the service that is provided to the bank and is intangible in

nature without acting as the owners of the service needs to be done in a careful manner. The

services that are intangible in nature may often result in problems among the customers, as they

might not be aware of the problems that they might face when availing the service. Therefore, it

is necessary for trust to be involved in managing the risks along with the vulnerability that the

customers may face with the respective services. The use of internet has led to increased

competition in the markets that are developed technologically, which makes it challenging for

the banks to maintain their relationships with the clients in a better manner. The factor of trust

and security that is provided by the banks to its customers helps in influencing the relationships

between the banks and its customers (Shaikh and Karjaluoto 2015). The banks try to maintain a

long-term relationship with the customers so that it helps them in developing their trust with the

customers. The perception of the customers is that they find it challenging in trusting the internet

banking options that are provided by the banks along with the other electronic commerce factors

that try to extract the information from the customers. Thus, it can be said that trust is a

multidimensional and complex phenomenon that may arise in the minds of the customers. It is

related to the factor of avoiding the risk and the security that the customers perceive about the

services that are being offered by the banks (Yadav, Chauhan and Pathak 2015).

12INTERNET BANKING

Therefore, the customers need to trust and be reliable towards the honesty that the banks

show with respect to the services that are being offered by them. The issues of security are very

crucial because of the direct involvement of the activities of the users regarding the tangible and

the intangible services that are being provided by the banks. Moreover, the trust that is present in

the transactions that are online is subjective in nature according to the profitability of the

customers and their expectations regarding the services of the banks. The beliefs on which the

customers can trust the banks depend on the factors of integrity, benevolence and competences

(Singh and Kumar 2014).

Quality of service

The rise in the revolution with respect to digitization has changed the vision on a regular

basis of the people in the current century. The empowerment of the World Wide Web along with

the e-commerce on a global basis has helped in increasing the number of people in being

connected with others on the internet. The advantages in adopting the these technologies by the

organizations has helped in the creation of barriers of entry, improvement in the level of

productivity along with the increased profits due to the generation of better revenues from the

renewed services (Hanafizadeh, Keating and Khedmatgozar 2014). The use of better

communication process along with the increased use of information technology has helped the

banks in developing and delivering the services, which is considered superior by the customers

with respect to the transactions in the banking system. The quality of service that is being

provided by the banks is one of the primary factors that help in determining the success of the

electronic commerce in the banking sector. The quality of service may be defined as the overall

impression of the consumers towards the organization for the services that are being provided by

them (Saffina, Kammani and Date 2014).

Therefore, the customers need to trust and be reliable towards the honesty that the banks

show with respect to the services that are being offered by them. The issues of security are very

crucial because of the direct involvement of the activities of the users regarding the tangible and

the intangible services that are being provided by the banks. Moreover, the trust that is present in

the transactions that are online is subjective in nature according to the profitability of the

customers and their expectations regarding the services of the banks. The beliefs on which the

customers can trust the banks depend on the factors of integrity, benevolence and competences

(Singh and Kumar 2014).

Quality of service

The rise in the revolution with respect to digitization has changed the vision on a regular

basis of the people in the current century. The empowerment of the World Wide Web along with

the e-commerce on a global basis has helped in increasing the number of people in being

connected with others on the internet. The advantages in adopting the these technologies by the

organizations has helped in the creation of barriers of entry, improvement in the level of

productivity along with the increased profits due to the generation of better revenues from the

renewed services (Hanafizadeh, Keating and Khedmatgozar 2014). The use of better

communication process along with the increased use of information technology has helped the

banks in developing and delivering the services, which is considered superior by the customers

with respect to the transactions in the banking system. The quality of service that is being

provided by the banks is one of the primary factors that help in determining the success of the

electronic commerce in the banking sector. The quality of service may be defined as the overall

impression of the consumers towards the organization for the services that are being provided by

them (Saffina, Kammani and Date 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13INTERNET BANKING

The quality of service according to the perception of the customers is based on the system

of online delivery and excludes the process where the service has been produced and developed.

It is also one of the factors based on which the customers try to evaluate the services that are

being provided by the banks to them. The concept of quality of service needs to be inclusive of

the delivery process and the outcomes that are associated with the service (Montazemi and

Qahri-Saremi 2015).

The Nodic model that was developed by Gronroos in the early 1980s had different

dimensions that were linked to the quality of services such as the quality of techniques, quality of

function and the corporate image. The other model was presented by Lehtinen, which showed

that the quality of service was based on three dimensions that are interactive, physical and

corporate. The physical quality of the products that are involved in the delivery of the service

helps in the consumption and the interaction between the employees of the organization and the

customers. The corporate quality is defined as the image of the organization that is perceived by

the customers (Namahoot and Laohavichien 2015).

Perceived ease of use

The rise in the World Wide Web along with the internet has helped the customers and the

bankers by providing them with the opportunity of an environment that is innovated in nature,

which helps in stimulating the operative and the learning process (Das et al. 2017). The intention

of the customers is to adopt the latest technologies that will help them in easing out the process

of transactions. The perceived ease of use is an important factor that helps in studying and

accepting the internet along with the World Wide Web so that it helps them in using the

processes in an easier manner. It is an extent to which the customers can use the technologies in

an easier manner. The online banking system of the banks with respect to the easiness in which it

The quality of service according to the perception of the customers is based on the system

of online delivery and excludes the process where the service has been produced and developed.

It is also one of the factors based on which the customers try to evaluate the services that are

being provided by the banks to them. The concept of quality of service needs to be inclusive of

the delivery process and the outcomes that are associated with the service (Montazemi and

Qahri-Saremi 2015).

The Nodic model that was developed by Gronroos in the early 1980s had different

dimensions that were linked to the quality of services such as the quality of techniques, quality of

function and the corporate image. The other model was presented by Lehtinen, which showed

that the quality of service was based on three dimensions that are interactive, physical and

corporate. The physical quality of the products that are involved in the delivery of the service

helps in the consumption and the interaction between the employees of the organization and the

customers. The corporate quality is defined as the image of the organization that is perceived by

the customers (Namahoot and Laohavichien 2015).

Perceived ease of use

The rise in the World Wide Web along with the internet has helped the customers and the

bankers by providing them with the opportunity of an environment that is innovated in nature,

which helps in stimulating the operative and the learning process (Das et al. 2017). The intention

of the customers is to adopt the latest technologies that will help them in easing out the process

of transactions. The perceived ease of use is an important factor that helps in studying and

accepting the internet along with the World Wide Web so that it helps them in using the

processes in an easier manner. It is an extent to which the customers can use the technologies in

an easier manner. The online banking system of the banks with respect to the easiness in which it

14INTERNET BANKING

can be used may be the attractiveness of the URL towards the customers along with the easy way

to navigate the sites and find out the proper informations with minimum of effort. Additionally,

it can be noted that the perception of easy usage will help the customers in accepting the

changes, as it will help them in accessing the information easily (Sikdar, Kumar and Makkad

2015).

It can also be stated that the factors that help in the growth of the system of electronic

banking can be determined with the easiness of its use, which combines the factor of

convenience with respect to the easy access to the internet and the availability of the functions

that are present in the banking services. The perceived use of ease helps in measuring the

satisfaction level of the customers regarding the adoption of the information system. This can be

applied in the concept of online banking as well, as the banks need to give more focus on the

navigation of the websites and the functions that are applicable so that it helps in catering to the

needs of the customers. The online medium for the transactions of the banks has to depend on the

proper techniques of communication failing which the customers may switch towards the

traditional methods of banking transactions (Khanna and Gupta 2015).

Perceived usefulness

The use of the information technology has helped in changing the growth of the

industries, as it has developed with the onset of internet banking, which has made it more

complex and diversified respectively. The speedy and the convenient services has been achieved

by the bank through the system of internet banking. The traditional system of banking that was

very much in practice in India posed many threats to the bankers, as the long queues made the

customers impatient (Bhasin 2015). The attitude towards the use of the internet facilities by the

banks depend on various factors such as the background of the customers and the behavior

can be used may be the attractiveness of the URL towards the customers along with the easy way

to navigate the sites and find out the proper informations with minimum of effort. Additionally,

it can be noted that the perception of easy usage will help the customers in accepting the

changes, as it will help them in accessing the information easily (Sikdar, Kumar and Makkad

2015).

It can also be stated that the factors that help in the growth of the system of electronic

banking can be determined with the easiness of its use, which combines the factor of

convenience with respect to the easy access to the internet and the availability of the functions

that are present in the banking services. The perceived use of ease helps in measuring the

satisfaction level of the customers regarding the adoption of the information system. This can be

applied in the concept of online banking as well, as the banks need to give more focus on the

navigation of the websites and the functions that are applicable so that it helps in catering to the

needs of the customers. The online medium for the transactions of the banks has to depend on the

proper techniques of communication failing which the customers may switch towards the

traditional methods of banking transactions (Khanna and Gupta 2015).

Perceived usefulness

The use of the information technology has helped in changing the growth of the

industries, as it has developed with the onset of internet banking, which has made it more

complex and diversified respectively. The speedy and the convenient services has been achieved

by the bank through the system of internet banking. The traditional system of banking that was

very much in practice in India posed many threats to the bankers, as the long queues made the

customers impatient (Bhasin 2015). The attitude towards the use of the internet facilities by the

banks depend on various factors such as the background of the customers and the behavior

15INTERNET BANKING

towards adopting the different technologies so that they can use the services of the bank in an

easier manner. The attitudes of the customers towards internet banking are influenced by the

level of experience that the customers have in using the computers and adopting the latest

technologies along with the environmental factors such as uninterrupted service of the internet

within a particular locality. The new channels of banking has to be adopted by the customers so

that it helps them in understanding the integration of the password, encryption of the data and the

techniques behind protection of data (Kaura 2013). Additionally, it can be said that that privacy

and security are the factors that influence the transactions of the bank by adopting the new online

methods. The usefulness of the Technology Acceptance Model (TAM) has helped in studying

the technologies that are available in the information system so that it helps in enhancing the

performance of the customers (Roy et al. 2017).

The usefulness of the users will help them in enhancing their decision about the use of

online banking, which will help them in reducing their efforts with the transfer, withdraw or

deposit of money in their respective bank accounts. It also helps in measuring the usefulness of

the perception of the customers that is related to the outcome of using the latest technologies. It

also helps the customers in boosting up their performance with respect to the service that are

offered by the banks to them (Shankar and Kumari 2016).

Customer satisfaction

In any of the business to customer (B2C) type of sector, the ultimate goal of the

organization is to satisfy the customers with their products and services. It is an important part in

theory as well as in practical, as the marketers along with the analysts of the organization can

understand the minds of the customers. This helps the organization in producing the goods and

services according to the tastes and preferences of the customers. The idea of customer

towards adopting the different technologies so that they can use the services of the bank in an

easier manner. The attitudes of the customers towards internet banking are influenced by the

level of experience that the customers have in using the computers and adopting the latest

technologies along with the environmental factors such as uninterrupted service of the internet

within a particular locality. The new channels of banking has to be adopted by the customers so

that it helps them in understanding the integration of the password, encryption of the data and the

techniques behind protection of data (Kaura 2013). Additionally, it can be said that that privacy

and security are the factors that influence the transactions of the bank by adopting the new online

methods. The usefulness of the Technology Acceptance Model (TAM) has helped in studying

the technologies that are available in the information system so that it helps in enhancing the

performance of the customers (Roy et al. 2017).

The usefulness of the users will help them in enhancing their decision about the use of

online banking, which will help them in reducing their efforts with the transfer, withdraw or

deposit of money in their respective bank accounts. It also helps in measuring the usefulness of

the perception of the customers that is related to the outcome of using the latest technologies. It

also helps the customers in boosting up their performance with respect to the service that are

offered by the banks to them (Shankar and Kumari 2016).

Customer satisfaction

In any of the business to customer (B2C) type of sector, the ultimate goal of the

organization is to satisfy the customers with their products and services. It is an important part in

theory as well as in practical, as the marketers along with the analysts of the organization can

understand the minds of the customers. This helps the organization in producing the goods and

services according to the tastes and preferences of the customers. The idea of customer

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16INTERNET BANKING

satisfaction is important for the organizations that are in to service, as their subscriptions depend

on the satisfaction that the customers get from the service, which in turn helps in increasing the

loyalty of the customers towards the organization (Yadav, Chauhan and Pathak 2015). The

increase in the customer loyalty helps in generating better revenues for the banks, as the

customers are likely to keep their money in the same organization n repeatedly. Customer

satisfaction is the concept that helps in understanding the purchase of the goods and services

from the organization and the level of satisfaction that they have derived after the use of the

products and the services. The satisfaction of the customers is also dependent on the attitude of

the customers towards the provider of the services along with the differences that the customers

can anticipate about the products or the services (Saffina, Kammani and Date 2014).

Impact of e-banking on the customers

According to the survey that was conducted by the Reserve Bank of India in India, it was

seen that the use of ATM cards were high among the young users of the bank. These young users

are comfortable in using the e-banking services that are provided to them by the banks, as they

find that it is easy and consumes less time. The concept of internet banking is becoming a

popular phenomenon in India, as more number of customers are trying to adopt to the systems

that are helping them in reducing their transaction times (Namahoot and Laohavichien 2015).

The six important features that are present with respect to the e-banking services are the

accuracy and convenience with which the consumers can access their accounts of their respective

banks along with the feedback that the customers can provide to the bank so that their services

can be improved in a better manner. The other dimensions were that it helped in increasing the

efficiency of the services of the bank, which resulted in the better performance of the banks

satisfaction is important for the organizations that are in to service, as their subscriptions depend

on the satisfaction that the customers get from the service, which in turn helps in increasing the

loyalty of the customers towards the organization (Yadav, Chauhan and Pathak 2015). The

increase in the customer loyalty helps in generating better revenues for the banks, as the

customers are likely to keep their money in the same organization n repeatedly. Customer

satisfaction is the concept that helps in understanding the purchase of the goods and services

from the organization and the level of satisfaction that they have derived after the use of the

products and the services. The satisfaction of the customers is also dependent on the attitude of

the customers towards the provider of the services along with the differences that the customers

can anticipate about the products or the services (Saffina, Kammani and Date 2014).

Impact of e-banking on the customers

According to the survey that was conducted by the Reserve Bank of India in India, it was

seen that the use of ATM cards were high among the young users of the bank. These young users

are comfortable in using the e-banking services that are provided to them by the banks, as they

find that it is easy and consumes less time. The concept of internet banking is becoming a

popular phenomenon in India, as more number of customers are trying to adopt to the systems

that are helping them in reducing their transaction times (Namahoot and Laohavichien 2015).

The six important features that are present with respect to the e-banking services are the

accuracy and convenience with which the consumers can access their accounts of their respective

banks along with the feedback that the customers can provide to the bank so that their services

can be improved in a better manner. The other dimensions were that it helped in increasing the

efficiency of the services of the bank, which resulted in the better performance of the banks

17INTERNET BANKING

towards its customers along with the easy access that the customers get by availing the

techniques that have been given by the banks (Das et al. 2017).

The concept of internet banking is an innovative channel of distribution that helps the

customers by providing them less waiting period and better convenience than the banking

methods that are present in the traditional approach. This has helped the banks in producing the

structure that are cost effective with respect to the channels of delivery. The banks also became

advantageous, as the adoption of the better services led to the reduction in the costs of operation

and increase in the satisfaction of the customers, which resulted in the retention of the customers.

The concept of internet banking has had a major impact on the banks and in the lives of the

customers, as most of them have accepted the technological advances, which has helped them in

managing the transactions in an efficient manner (Khanna and Gupta 2015).

The banks are able to provide better financial services to the customers by maintaining

lower cost in their operational methods. The banks are able to find out the strategies in a

comprehensive manner that is related to the banking services, which helps the banks in being

competitive in nature. The changes in the technology have created an impact on the lifestyles of

the people, which has helped them in changing their outlook towards the services that are being

offered by the banks (Bhasin 2015). The home banking services that have been supplied by the

banks is a significant strategy that has helped the banks in attracting the customers and even

retaining them. Almost 75 percent of the Indian banks had adopted the services of internet

banking between the periods of 1993-2000. This showed that the banks had extended their

activities to the customers so that they can avail the facilities, which will help them in easing out

their transactions (Sikdar, Kumar and Makkad 2015).

towards its customers along with the easy access that the customers get by availing the

techniques that have been given by the banks (Das et al. 2017).

The concept of internet banking is an innovative channel of distribution that helps the

customers by providing them less waiting period and better convenience than the banking

methods that are present in the traditional approach. This has helped the banks in producing the

structure that are cost effective with respect to the channels of delivery. The banks also became

advantageous, as the adoption of the better services led to the reduction in the costs of operation

and increase in the satisfaction of the customers, which resulted in the retention of the customers.

The concept of internet banking has had a major impact on the banks and in the lives of the

customers, as most of them have accepted the technological advances, which has helped them in

managing the transactions in an efficient manner (Khanna and Gupta 2015).

The banks are able to provide better financial services to the customers by maintaining

lower cost in their operational methods. The banks are able to find out the strategies in a

comprehensive manner that is related to the banking services, which helps the banks in being

competitive in nature. The changes in the technology have created an impact on the lifestyles of

the people, which has helped them in changing their outlook towards the services that are being

offered by the banks (Bhasin 2015). The home banking services that have been supplied by the

banks is a significant strategy that has helped the banks in attracting the customers and even

retaining them. Almost 75 percent of the Indian banks had adopted the services of internet

banking between the periods of 1993-2000. This showed that the banks had extended their

activities to the customers so that they can avail the facilities, which will help them in easing out

their transactions (Sikdar, Kumar and Makkad 2015).

18INTERNET BANKING

The advantages of using the internet banking provided improved security measures to the

customers regarding the access of the banks through the internet. It also helped the customers, as

the banks offered better services to them, which helped the banks in increasing the customer base

and maintain customer loyalty at the same time. According to a recent study, it was seen that the

customers have adopted the technologies that are present in the e-banking system in India, which

has resulted in a positive attitude among the customers (Kaura 2013).

The advantages of using the internet banking provided improved security measures to the

customers regarding the access of the banks through the internet. It also helped the customers, as

the banks offered better services to them, which helped the banks in increasing the customer base

and maintain customer loyalty at the same time. According to a recent study, it was seen that the

customers have adopted the technologies that are present in the e-banking system in India, which

has resulted in a positive attitude among the customers (Kaura 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19INTERNET BANKING

Theory Hypothesis Observation Confirmation/Rejection

Chapter 3: Research Methodology

Approaches for the study

The approach for the study of the research helps the researcher in conducting the research

process in an efficient manner. The different kinds of approaches will be analyzed by the

researcher in an in-depth manner.

The approach that is deductive in nature will be taken in to consideration by the

researcher for this particular study of research. the deductive approach helps the researcher in

deriving the conclusions, which will be based on different factors and objectives so that it can be

linked with the conclusion in a better way (Mackey and Gass 2015).

(Source: Created by Author)

The approach that is inductive in nature is almost the opposite of the deductive approach,

as it is based on the facts that are quantitative in nature. The quantitative study is the collection

of the data from the customers and the managers of the banking organization, which are based on

real time. The main aim of the approach for this study will be to analyze the impact on the

customers with respect to the e-banking services that are provided by the Indian banks (Taylor,

Bogdan and DeVault 2015).

Figure 1: Deductive Approach

Theory Hypothesis Observation Confirmation/Rejection

Chapter 3: Research Methodology

Approaches for the study

The approach for the study of the research helps the researcher in conducting the research

process in an efficient manner. The different kinds of approaches will be analyzed by the

researcher in an in-depth manner.

The approach that is deductive in nature will be taken in to consideration by the

researcher for this particular study of research. the deductive approach helps the researcher in

deriving the conclusions, which will be based on different factors and objectives so that it can be

linked with the conclusion in a better way (Mackey and Gass 2015).

(Source: Created by Author)

The approach that is inductive in nature is almost the opposite of the deductive approach,

as it is based on the facts that are quantitative in nature. The quantitative study is the collection

of the data from the customers and the managers of the banking organization, which are based on

real time. The main aim of the approach for this study will be to analyze the impact on the

customers with respect to the e-banking services that are provided by the Indian banks (Taylor,

Bogdan and DeVault 2015).

Figure 1: Deductive Approach

20INTERNET BANKING

Research method used

The research method helps in the submission of the datas that has been collected and

investigated in a proper manner. This particular study will be conducted by taking in to

consideration the primary and the secondary sources of data. The primary sources of data will be

taken care of by taking in to consideration the questionnaires that will be handed out to the

customers for gathering their responses. With respect to the secondary data, the information will

be extracted from the various journals, websites of the company and the books that have been

published by the various authors. The use of the secondary data will help in getting a better

insight about the different concepts that are present with the banking services in the banks. The

information that will be available on the website about the organization will help in completing

the study of the research in an appropriate manner (Flick 2015).

Quantitative method

The quantitative method is used when the objectives are formal in nature so that the

events can be measured and the numerical data can be analyzed with the help of the statistical

data. It is the method that helps in analyzing the numerical figures along with the variables,

which can be measured in a better manner. This method helps in the preparation of the

hypothesis in a better way so that the research can be conducted in an empirical manner.

The quantitative method also has some strength, as it helps in authenticating and testing

the published theories that are already present and the test of hypothesis that will help in gaining

a better level of reliability from the data that is collected by the interviews. This method also has

some weaknesses such as the researcher may ignore the phenomena that are basic and focus

more on the theories that are published already (Smith 2015).

Research method used

The research method helps in the submission of the datas that has been collected and

investigated in a proper manner. This particular study will be conducted by taking in to

consideration the primary and the secondary sources of data. The primary sources of data will be

taken care of by taking in to consideration the questionnaires that will be handed out to the

customers for gathering their responses. With respect to the secondary data, the information will

be extracted from the various journals, websites of the company and the books that have been

published by the various authors. The use of the secondary data will help in getting a better

insight about the different concepts that are present with the banking services in the banks. The

information that will be available on the website about the organization will help in completing

the study of the research in an appropriate manner (Flick 2015).

Quantitative method

The quantitative method is used when the objectives are formal in nature so that the

events can be measured and the numerical data can be analyzed with the help of the statistical

data. It is the method that helps in analyzing the numerical figures along with the variables,

which can be measured in a better manner. This method helps in the preparation of the

hypothesis in a better way so that the research can be conducted in an empirical manner.

The quantitative method also has some strength, as it helps in authenticating and testing

the published theories that are already present and the test of hypothesis that will help in gaining

a better level of reliability from the data that is collected by the interviews. This method also has

some weaknesses such as the researcher may ignore the phenomena that are basic and focus

more on the theories that are published already (Smith 2015).

21INTERNET BANKING

Qualitative method

The qualitative method that is used in the research process helps the researcher in taking

in to consideration the qualitative data that has been observed when the interviews were being

conducted by the researcher. The researcher will be able to study and get an in-depth knowledge

about the human activities within the organization along with the reasons for it when this method

is chosen for the study.

This method also has some strength, as the information that is collected through this

process is free from any biasness, as the reliability is very strong for the observer. The

information that is evaluated from this method is specific in nature. The method however has

some weakness as well, as it is unreliable because the materials that are qualitative in nature need

to be symbolized by submitting better techniques for the purpose of the measurement (Silverman

2016).

Project content

The project will be carried out based on the responses that will be collected from the

customers from the banks in India. The customers need to fill in the questions that have been put

by the researcher in the questionnaire. This will help the researcher in analyzing the responses of

the customers and provide better recommendation for the banks.

Data collection

The researcher will collect the response samples from 100 customers who has accounts in

private or in the public banks, which will help in the analysis of the data in a successful manner.

Qualitative method

The qualitative method that is used in the research process helps the researcher in taking

in to consideration the qualitative data that has been observed when the interviews were being

conducted by the researcher. The researcher will be able to study and get an in-depth knowledge

about the human activities within the organization along with the reasons for it when this method

is chosen for the study.

This method also has some strength, as the information that is collected through this

process is free from any biasness, as the reliability is very strong for the observer. The

information that is evaluated from this method is specific in nature. The method however has

some weakness as well, as it is unreliable because the materials that are qualitative in nature need

to be symbolized by submitting better techniques for the purpose of the measurement (Silverman

2016).

Project content

The project will be carried out based on the responses that will be collected from the

customers from the banks in India. The customers need to fill in the questions that have been put

by the researcher in the questionnaire. This will help the researcher in analyzing the responses of

the customers and provide better recommendation for the banks.

Data collection

The researcher will collect the response samples from 100 customers who has accounts in

private or in the public banks, which will help in the analysis of the data in a successful manner.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22INTERNET BANKING

Analysis of the data

The process of the research study will be based on the data sources, which are

quantitative and qualitative in nature. The use of the statistical methods will help in the analysis

of the data, which in turn will result in finding out the relationship between the different

variables. The responses will be collected in the excel work sheet and a Chi Square analysis will

be done, which was suggested by Pearson. This analysis will help in finding out the statistical

relationship between the variables that have been taken up for the process of research. The

primary survey will try to eliminate the errors, which may have occurred during the process of

collecting the samples, which will help in finding out the association based on statistics between

the independent and the dependent variables. Additionally, the study that is based on the

qualitative method will help in testing out the factors that are present in the hypothesis.

Types of investigation

There are different types of investigative processes that help in collecting the responses

from the managers, which can be classified as positivism, realism and interpretivism types of

investigation. These different types will help the researcher in taking in to account the analysis,

which needs to be done in an in-depth manner.

Analysis of the data

The process of the research study will be based on the data sources, which are

quantitative and qualitative in nature. The use of the statistical methods will help in the analysis

of the data, which in turn will result in finding out the relationship between the different

variables. The responses will be collected in the excel work sheet and a Chi Square analysis will

be done, which was suggested by Pearson. This analysis will help in finding out the statistical

relationship between the variables that have been taken up for the process of research. The

primary survey will try to eliminate the errors, which may have occurred during the process of

collecting the samples, which will help in finding out the association based on statistics between

the independent and the dependent variables. Additionally, the study that is based on the

qualitative method will help in testing out the factors that are present in the hypothesis.

Types of investigation

There are different types of investigative processes that help in collecting the responses

from the managers, which can be classified as positivism, realism and interpretivism types of