313LON - Analyzing Implications of Mark & Spencer's FDI in Australia

VerifiedAdded on 2023/04/12

|20

|3286

|273

Report

AI Summary

This report examines the implications of Mark & Spencer's proposed foreign direct investment (FDI) in Australia. It covers critical aspects such as the capital outlay required, assessing whether it presents an additional burden or offers sufficient return on investment. The report contrasts corporate governance practices in the UK and Australia, highlighting key differences that could affect the project's overall success and reliability. It also addresses the risks associated with foreign exchange fluctuations between the two countries and explores strategies for managing these risks, focusing on widely accepted mitigation methods. The analysis incorporates balance of payment data, and concludes with a summary of key considerations for Mark & Spencer's FDI strategy in Australia.

Running head: IMPLICATIONS OF ESTABLISHING FDI ABROAD.

Implications of establishing FDI abroad.

Name of the student:

Name of the university:

Author Note:

Implications of establishing FDI abroad.

Name of the student:

Name of the university:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Executive Summary:

The whole assignment is prepared to show the implications of foreign direct

investment proposal made by the Mark & Spencer. The assignment is prepared in such a

way that after the study of the assignment the person will be able to find the major area of

concern affecting the said proposal. The report is concerned with the main implications of

capital outlay required to finance the project of the Mark & Spencer whether it is in the form

of additional burden or the required return on the capital. The report is also concerned with

the corporate governance practice adopted in the UK and Australia with stating key areas of

differences, which may affect the overall project and the return or reliability of the project.

The focus is also on the risk that may arise due to fluctuation of foreign exchange between

both the countries with mentioning the ways to manage such risks. Although there are

several ways to mitigate the risk associated with foreign exchange but the focus is on the

main ways and widely accepted ways to mitigate the same risk.

Executive Summary:

The whole assignment is prepared to show the implications of foreign direct

investment proposal made by the Mark & Spencer. The assignment is prepared in such a

way that after the study of the assignment the person will be able to find the major area of

concern affecting the said proposal. The report is concerned with the main implications of

capital outlay required to finance the project of the Mark & Spencer whether it is in the form

of additional burden or the required return on the capital. The report is also concerned with

the corporate governance practice adopted in the UK and Australia with stating key areas of

differences, which may affect the overall project and the return or reliability of the project.

The focus is also on the risk that may arise due to fluctuation of foreign exchange between

both the countries with mentioning the ways to manage such risks. Although there are

several ways to mitigate the risk associated with foreign exchange but the focus is on the

main ways and widely accepted ways to mitigate the same risk.

2

Table of Contents

1. Introduction:...........................................................................................................................3

3. Balance of payment:...............................................................................................................6

3.1 Significance of Balance of payments:..............................................................................6

4. The key differences between Corporate Governance of UK and Australia:..........................9

5.1 Foreign exchange risk:...................................................................................................12

5.2 Foreign exchange risk management:..............................................................................13

6. Conclusion:..........................................................................................................................14

7. References:...........................................................................................................................15

Table of Contents

1. Introduction:...........................................................................................................................3

3. Balance of payment:...............................................................................................................6

3.1 Significance of Balance of payments:..............................................................................6

4. The key differences between Corporate Governance of UK and Australia:..........................9

5.1 Foreign exchange risk:...................................................................................................12

5.2 Foreign exchange risk management:..............................................................................13

6. Conclusion:..........................................................................................................................14

7. References:...........................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

1. Introduction:

The foreign direct investment and the implication of such investment on the financial

health of Mark & Spencer depends upon various factors, which directly or indirectly affects

the return from such investment. These factors are the trade and political relation between

both country, the corporate governance policy of that government, the foreign exchange risk

and effect of sourcing of such investment on the financial health of the Mark & Spencer.

The main emphasize has been given to introduce the problems that may be faced during the

process of implementation of such investment proposal. The project of foreign direct

investment has several factors to consider and several studies on the microeconomic

conditions of that country, which is necessary for successful implementation of the project

otherwise, the project can be produce undesirable result.

1. Introduction:

The foreign direct investment and the implication of such investment on the financial

health of Mark & Spencer depends upon various factors, which directly or indirectly affects

the return from such investment. These factors are the trade and political relation between

both country, the corporate governance policy of that government, the foreign exchange risk

and effect of sourcing of such investment on the financial health of the Mark & Spencer.

The main emphasize has been given to introduce the problems that may be faced during the

process of implementation of such investment proposal. The project of foreign direct

investment has several factors to consider and several studies on the microeconomic

conditions of that country, which is necessary for successful implementation of the project

otherwise, the project can be produce undesirable result.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

2. Implications of Firm’s additional capital requirement:

To establish a FDI abroad, the Mark & Spencer will need significant amount of

capital. For this purpose, Mark & Spencer may adopt different financing policy based on

which the impacts of such funding can be analyzed. There are two types of Capital financing

such as Debt financing and equity funding. These two methods of financing and their impact

on the company is explained below:

1. Internal financing: it refers to the use of retained profits for financing of the project

capital requirement instead of distributing it to the shareholders. This method is most

acceptable when there is huge fund available. This funding is not tax deductible and

neither do appreciation in the value of the capital. Internal sources of finances

generally includes fund generated through sale of assets, through reducing working

capital requirement and through operational activity of the company.

2. External financing: it is the way of financing business projects from outside

sources of the organizations such as debt financing, equity financing and short-term

borrowings. This type of financing will generally results into interest obligation to

the Mark & Spencer. If equity financing is involved then there will be proportionate

transfer of ownership. This type of financing is most commonly financing and it is

suitable for financing projects with huge capital requirements. However, the major

drawback of such financing is the interest burden to the Mark & Spencer, which is

the charge against the profit.

When an organization uses equity as means to finance its project, it is termed as

equity financing. In this consideration by issuing fresh equity of the Mark & Spencer

to the extent, it is required for project financing. However, this type of financing

does not have any effect on the profitability of the Mark & Spencer but it dilutes the

2. Implications of Firm’s additional capital requirement:

To establish a FDI abroad, the Mark & Spencer will need significant amount of

capital. For this purpose, Mark & Spencer may adopt different financing policy based on

which the impacts of such funding can be analyzed. There are two types of Capital financing

such as Debt financing and equity funding. These two methods of financing and their impact

on the company is explained below:

1. Internal financing: it refers to the use of retained profits for financing of the project

capital requirement instead of distributing it to the shareholders. This method is most

acceptable when there is huge fund available. This funding is not tax deductible and

neither do appreciation in the value of the capital. Internal sources of finances

generally includes fund generated through sale of assets, through reducing working

capital requirement and through operational activity of the company.

2. External financing: it is the way of financing business projects from outside

sources of the organizations such as debt financing, equity financing and short-term

borrowings. This type of financing will generally results into interest obligation to

the Mark & Spencer. If equity financing is involved then there will be proportionate

transfer of ownership. This type of financing is most commonly financing and it is

suitable for financing projects with huge capital requirements. However, the major

drawback of such financing is the interest burden to the Mark & Spencer, which is

the charge against the profit.

When an organization uses equity as means to finance its project, it is termed as

equity financing. In this consideration by issuing fresh equity of the Mark & Spencer

to the extent, it is required for project financing. However, this type of financing

does not have any effect on the profitability of the Mark & Spencer but it dilutes the

5

ownership of the company. When an organization uses debt as a way of financing

then it is called as debt financing and it has serious impact on the debt equity ratio of

the company. Debt financing also results into a reduction in the profit of the

company. The company should have to pay interest even if there has been loss in the

financial year. (Gorton, and Winton, 2016).

ownership of the company. When an organization uses debt as a way of financing

then it is called as debt financing and it has serious impact on the debt equity ratio of

the company. Debt financing also results into a reduction in the profit of the

company. The company should have to pay interest even if there has been loss in the

financial year. (Gorton, and Winton, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

3. Balance of payment:

Balance of payment also known as BOP is the record of all economic transactions

between a country and the rest of world. It shows the relationship between the export and

import of that particular country. It provide detailed information of the demand and supply

of the currency of a specific country in terms of their export and import. Balance of payment

plays a key role in valuing currency of that country because it shows how much foreign

currency is required and how much foreign currency they are holding to import goods.

Country with more import requirements as compared to the export requirement will slightly

have higher foreign currency demand due to which the home currency depreciate against

foreign currency and vice-versa. The Balance of payment statement shows whether the

company has surplus or deficit of funds. If the country’s export is more than its imports then

the said country is said to be in surplus resulting into an increase to the currency of that

particular country and vice-versa.

3.1 Significance of Balance of payments:

There are no. of uses and importance of the data of balance of payment. It can be

used to evaluate Australia’s specific policy regarding export and import with the rest of the

world. The data can be analyzed to evaluate the relationship of the country with the foreign

company based on which decisions regarding investment can be made. There are following

points mentioning the significance of balance of payment:

a. It reveals financial as well as economic health of a particular country i.e. Australia

through use of import and export data of that country. Understanding financial status

of Australia is more important to analyze for making investment proposals in

Australia or establishing any FDI in that country because the financial and economic

3. Balance of payment:

Balance of payment also known as BOP is the record of all economic transactions

between a country and the rest of world. It shows the relationship between the export and

import of that particular country. It provide detailed information of the demand and supply

of the currency of a specific country in terms of their export and import. Balance of payment

plays a key role in valuing currency of that country because it shows how much foreign

currency is required and how much foreign currency they are holding to import goods.

Country with more import requirements as compared to the export requirement will slightly

have higher foreign currency demand due to which the home currency depreciate against

foreign currency and vice-versa. The Balance of payment statement shows whether the

company has surplus or deficit of funds. If the country’s export is more than its imports then

the said country is said to be in surplus resulting into an increase to the currency of that

particular country and vice-versa.

3.1 Significance of Balance of payments:

There are no. of uses and importance of the data of balance of payment. It can be

used to evaluate Australia’s specific policy regarding export and import with the rest of the

world. The data can be analyzed to evaluate the relationship of the country with the foreign

company based on which decisions regarding investment can be made. There are following

points mentioning the significance of balance of payment:

a. It reveals financial as well as economic health of a particular country i.e. Australia

through use of import and export data of that country. Understanding financial status

of Australia is more important to analyze for making investment proposals in

Australia or establishing any FDI in that country because the financial and economic

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

status will provide potential signals regarding the expected return, growth

opportunities and risks associated with such investment proposals whether it is in

form of FDI or in any other means. (Médici, and Panigo, 2015.)

b. It used to determine whether the value of the currency of that particular country is

appreciating or deprecating. The appreciation and depreciation in the value of

Australia is mainly dependent upon the value of the import and export made by

Australia within a year. The benefit from the changes in the value of the currency is

mainly dependent on the nature of funding made by Australia. As mentioned, Mark

& Spencer wants to establish a FDI in Australia. If the value of the AUD appreciates

then it will somehow will increase return to Mark & Spencer and if the value of

currency of Australia i.e. Australian dollar is depreciating then the return from

foreign direct investment will automatically fall down affecting into overall

investment decision of Mark & Spencer.

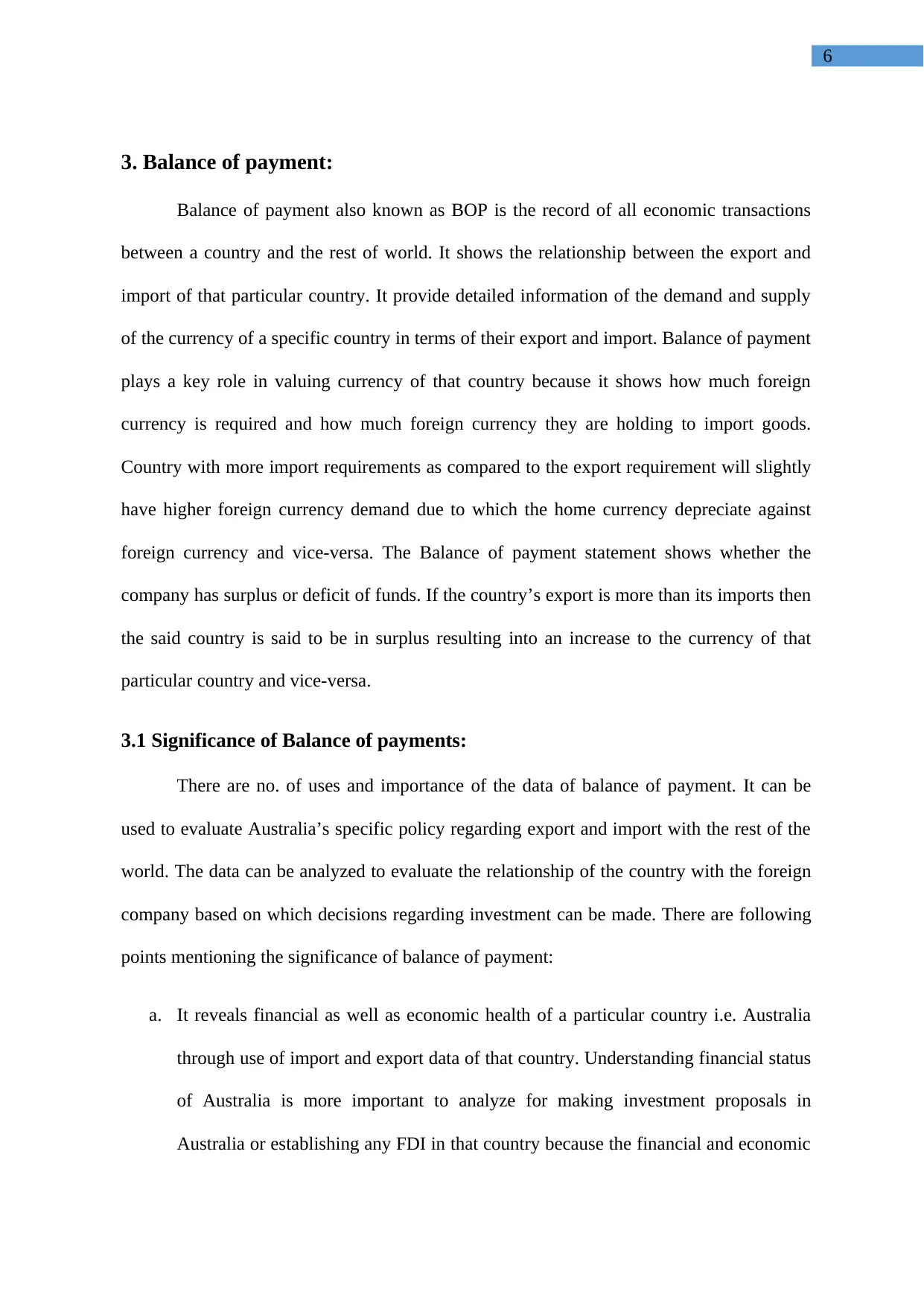

The chart given below shows the balance of payment of Australia:

(Fig. 1.1- chart showing export data of Australia)

status will provide potential signals regarding the expected return, growth

opportunities and risks associated with such investment proposals whether it is in

form of FDI or in any other means. (Médici, and Panigo, 2015.)

b. It used to determine whether the value of the currency of that particular country is

appreciating or deprecating. The appreciation and depreciation in the value of

Australia is mainly dependent upon the value of the import and export made by

Australia within a year. The benefit from the changes in the value of the currency is

mainly dependent on the nature of funding made by Australia. As mentioned, Mark

& Spencer wants to establish a FDI in Australia. If the value of the AUD appreciates

then it will somehow will increase return to Mark & Spencer and if the value of

currency of Australia i.e. Australian dollar is depreciating then the return from

foreign direct investment will automatically fall down affecting into overall

investment decision of Mark & Spencer.

The chart given below shows the balance of payment of Australia:

(Fig. 1.1- chart showing export data of Australia)

8

(Source: https://www.rba.gov.au/chart-pack/balance-payments.html)

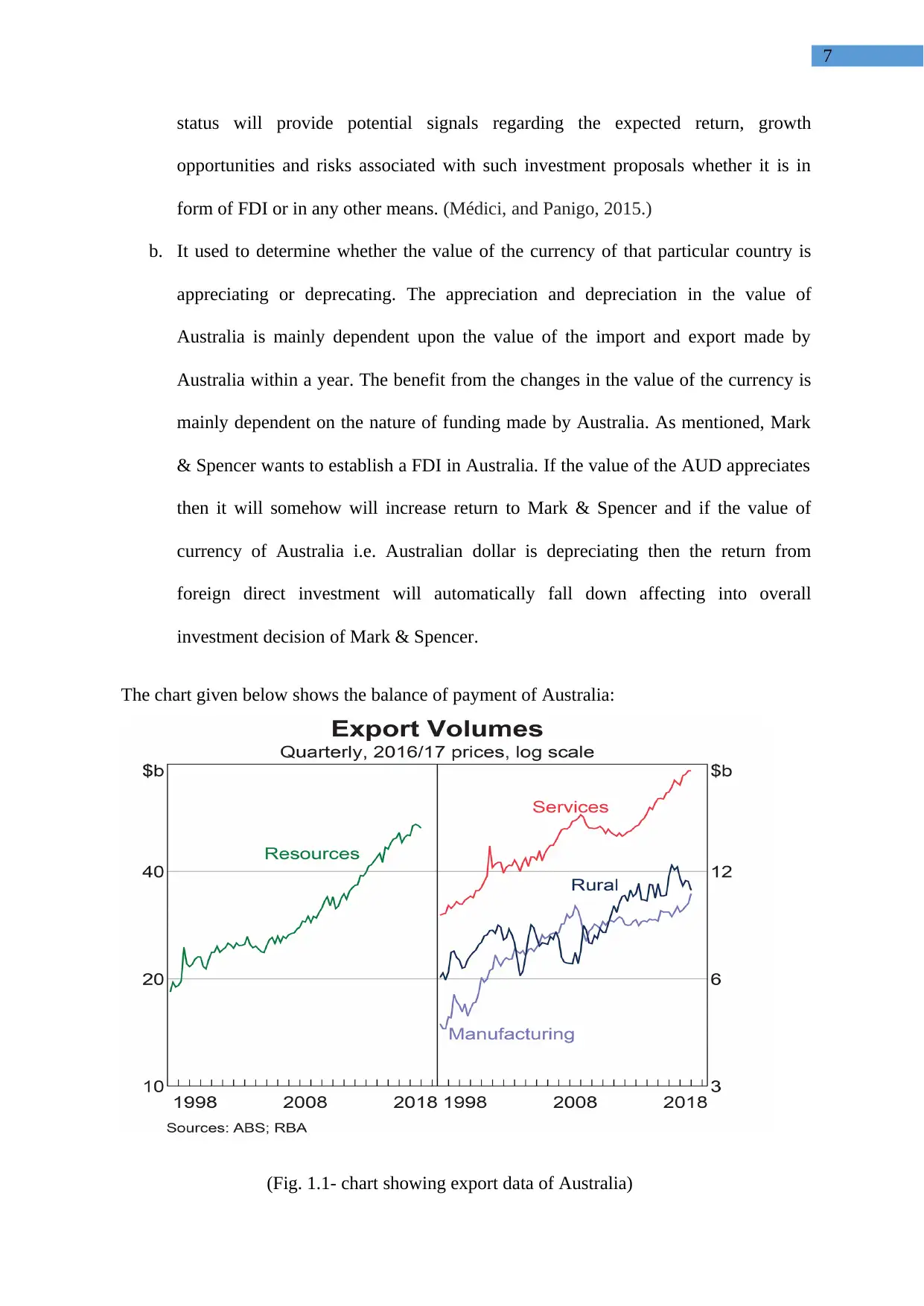

(Fig.1.2- chart showing import data of Australia,

(Source: https://www.rba.gov.au/chart-pack/balance-payments.html)

(Source: https://www.rba.gov.au/chart-pack/balance-payments.html)

(Fig.1.2- chart showing import data of Australia,

(Source: https://www.rba.gov.au/chart-pack/balance-payments.html)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

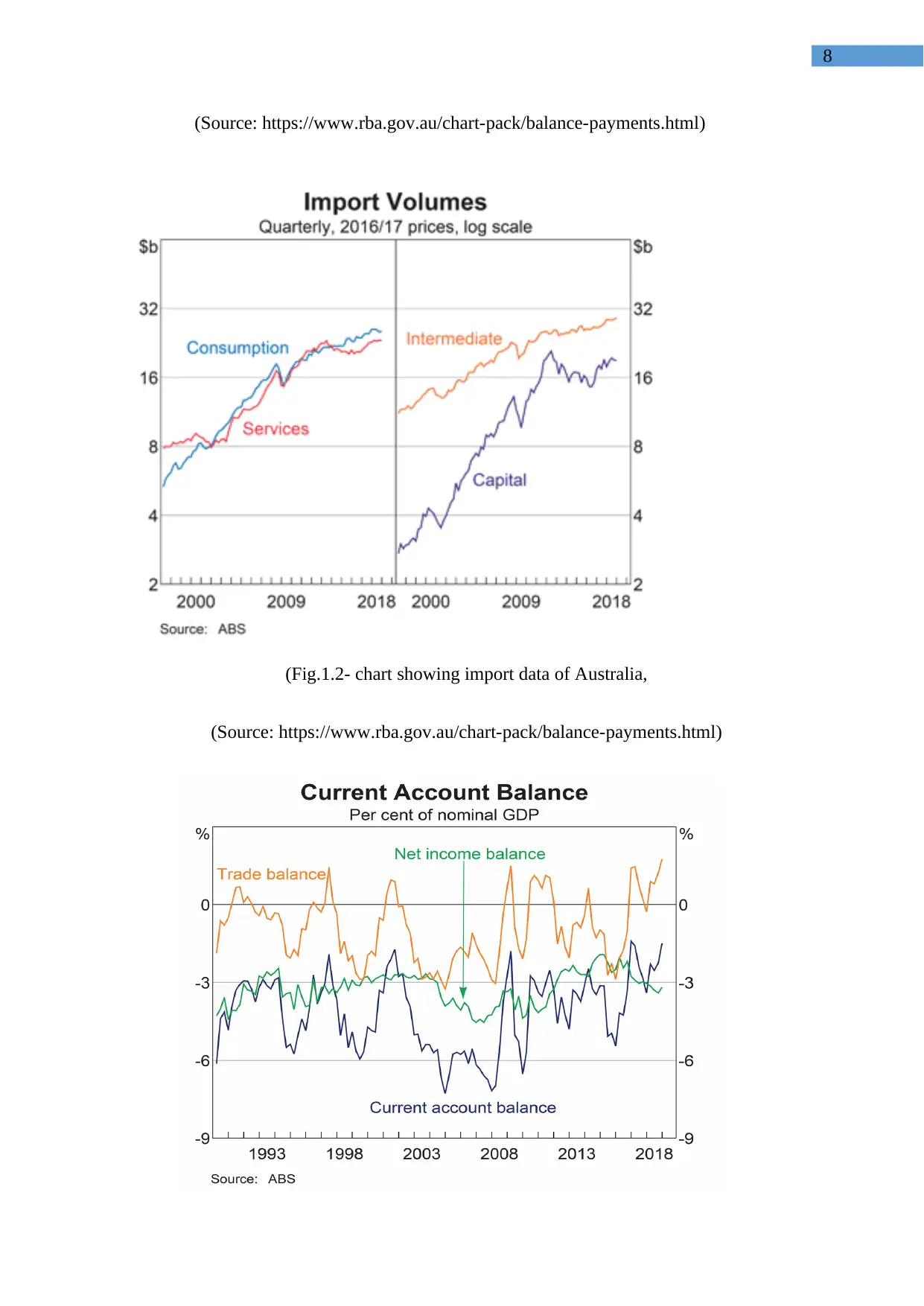

(Fig.1.2- chart showing import data of Australia)

(Source: https://www.rba.gov.au/chart-pack/balance-payments.html)

As observed from above data, it can be concluded that the trade deficit of Australia

has been increased throughout the year due to increased imports and decreased exports. It

has been increased to 4.81 billion in the month of April 2019 from 4.35 billion in the

previous month beating the market consensus of AUD 3.8 billion surplus. The increase in

import of goods or services and decrease in export of goods or services has led the overall

trade deficit for the Australian balance of payment.

(Fig.1.2- chart showing import data of Australia)

(Source: https://www.rba.gov.au/chart-pack/balance-payments.html)

As observed from above data, it can be concluded that the trade deficit of Australia

has been increased throughout the year due to increased imports and decreased exports. It

has been increased to 4.81 billion in the month of April 2019 from 4.35 billion in the

previous month beating the market consensus of AUD 3.8 billion surplus. The increase in

import of goods or services and decrease in export of goods or services has led the overall

trade deficit for the Australian balance of payment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

4. The key differences between Corporate Governance of UK and

Australia:

The corporate governance establish the relationship between the stakeholders or the

owner of the company and the management of the company. It increases the degree of

transparency between the management and the owner of the company with proper allocation

of accountability to the management of the company. The importance of corporate

governance is such that it can reveal major frauds and hidden facts about the health of the

company whether it is beneficial for the company or not. The corporate governance of UK

and Australia has designed based on the business environment and the laws and regulations

covering the business environment of both the country. The structure of the corporate

governance differs of both the country differs from following points:

a) The structure of Board: The structure of board differs from the composition of

Independent directors and managing directors in the board of both the country. The

board under Australian corporate governance consists of majority of independent

directors and chairmen should be independent director. The responsibility of

chairperson and chief executive officer of the board should not be exercised by same

person. The structure of board of UK corporate governance is having one committee

of both non-executive as well as executive directors; the presence of majority

independent director is main concern for the board. (Wickham and Backhouse,

2017.)

b) Leadership structure: under the UK corporate governance code, it is mentioned

that the chairperson and the CEO of the company should not be same. This means

that the company should have different persons for both the position. If the company

does not have different person for both the position then it has to disclose the reason

4. The key differences between Corporate Governance of UK and

Australia:

The corporate governance establish the relationship between the stakeholders or the

owner of the company and the management of the company. It increases the degree of

transparency between the management and the owner of the company with proper allocation

of accountability to the management of the company. The importance of corporate

governance is such that it can reveal major frauds and hidden facts about the health of the

company whether it is beneficial for the company or not. The corporate governance of UK

and Australia has designed based on the business environment and the laws and regulations

covering the business environment of both the country. The structure of the corporate

governance differs of both the country differs from following points:

a) The structure of Board: The structure of board differs from the composition of

Independent directors and managing directors in the board of both the country. The

board under Australian corporate governance consists of majority of independent

directors and chairmen should be independent director. The responsibility of

chairperson and chief executive officer of the board should not be exercised by same

person. The structure of board of UK corporate governance is having one committee

of both non-executive as well as executive directors; the presence of majority

independent director is main concern for the board. (Wickham and Backhouse,

2017.)

b) Leadership structure: under the UK corporate governance code, it is mentioned

that the chairperson and the CEO of the company should not be same. This means

that the company should have different persons for both the position. If the company

does not have different person for both the position then it has to disclose the reason

11

behind of not doing so. Whereas in Australia, the Board is not be chaired by the

chief executive person and this provision is compulsory in nature. (Shrives, and

Brennan, 2015.)

c) The role and liability of Directors:

The role and responsibility of Directors is the main point to consider the

difference between the corporate governance between the UK and Australia. In

Australia, the Directors’ liability is not only limited to the company assets but it also

expended to the personal liability of the director. This means that in case of

misconduct resulting into loss to the shareholders, the director will have to

compensate that loss through their personal capacity. The directors usually have the

entire insider Information of the company and they can use to make personal

advantage for themselves. Therefore, this provision generally binds directors’

responsibility not only limited but also expended to their personal assets as in the

case if they had made any profit through use of insider information resulting into

loss to the shareholders, said loss can be recovered from the directors personal

assets.

The UK code of corporate governance has outlined the liability of Directors only to

their capacity in the company i.e. limited to their remunerations only. However, if

the director has been found to be guilty on the ground that they have been using

some means to have advantages for their personal benefits then the company may

exercise their right to recover such from the personal assets of the company. (Al‐

Hadi et al. 2017).

d) Structure of Corporate governance policy:

behind of not doing so. Whereas in Australia, the Board is not be chaired by the

chief executive person and this provision is compulsory in nature. (Shrives, and

Brennan, 2015.)

c) The role and liability of Directors:

The role and responsibility of Directors is the main point to consider the

difference between the corporate governance between the UK and Australia. In

Australia, the Directors’ liability is not only limited to the company assets but it also

expended to the personal liability of the director. This means that in case of

misconduct resulting into loss to the shareholders, the director will have to

compensate that loss through their personal capacity. The directors usually have the

entire insider Information of the company and they can use to make personal

advantage for themselves. Therefore, this provision generally binds directors’

responsibility not only limited but also expended to their personal assets as in the

case if they had made any profit through use of insider information resulting into

loss to the shareholders, said loss can be recovered from the directors personal

assets.

The UK code of corporate governance has outlined the liability of Directors only to

their capacity in the company i.e. limited to their remunerations only. However, if

the director has been found to be guilty on the ground that they have been using

some means to have advantages for their personal benefits then the company may

exercise their right to recover such from the personal assets of the company. (Al‐

Hadi et al. 2017).

d) Structure of Corporate governance policy:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.