Detailed Management Accounting Report for Zylla Company's Performance

VerifiedAdded on 2020/10/22

|17

|4643

|387

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Zylla Company. It begins with an introduction to management accounting, its importance, and the different types of accounting methods, including cost accounting, price optimization, inventory management, and job costing. The report then delves into various management accounting reporting methods, such as segmental reports, performance reports, inventory management reports, job costing reports, and accounts receivables aging reports. The benefits of implementing management accounting systems are highlighted, emphasizing cost control, improved decision-making, and customer demand analysis. Furthermore, the report includes computations for marginal and absorption costing, providing practical examples. It also explores different planning tools, their merits and demerits, and how management accounting systems are used to respond to financial problems, ultimately leading to organizational success. The report concludes by summarizing the key findings and the overall impact of management accounting on Zylla Company's performance and financial health.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

P1 Meaning of management accounting and requirements and types of accounting.............1

P2 Different methods of management accounting reporting..................................................3

M1 Benefits of management accounting systems..................................................................5

P3 Computation of marginal and absorption costing.............................................................5

M2 Range of management accounting techniques.................................................................6

P4 Different types of planning tools and merits and demerits...............................................7

M3 Use of various planning tools..........................................................................................8

P5 How management accounting system used to respond to financial problems..................9

M4 Management accounting system leads to organisation success.....................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

P1 Meaning of management accounting and requirements and types of accounting.............1

P2 Different methods of management accounting reporting..................................................3

M1 Benefits of management accounting systems..................................................................5

P3 Computation of marginal and absorption costing.............................................................5

M2 Range of management accounting techniques.................................................................6

P4 Different types of planning tools and merits and demerits...............................................7

M3 Use of various planning tools..........................................................................................8

P5 How management accounting system used to respond to financial problems..................9

M4 Management accounting system leads to organisation success.....................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting information is crucial for organisation to resolve various issues

and improve upon its performance. Present report deals with importance of management

accounting to Zylla Company by which performance may be enhanced in a better way. Types of

management accounting and methods of reporting are also discussed. Moreover, calculation of

marginal and absorption costing are done. Various planning tools are explained along with

advantages and disadvantages of the same. Furthermore, management accounting systems are

explained which could be used to adapt to respond to financial problems. Thus, such type of

accounting information strengthens internal operations of the company.

P1 Meaning of management accounting and requirements and types of accounting

Management accounting is a useful branch of accounting for the managerial personnel of

the firm so that they may be able to take enhanced decisions in effective manner. This is

essentially required as business operates in dynamic environment where changes takes place now

and often. In such scenario, costs may be increased for manufacturing particular product and as

such, revenue would be impacted significantly. Thus, business needs to make better decisions so

that changes can be handled in effective way and this can be possible because of implementation

of management accounting in the organisation. It refers to that part of management where the

managers look out the needs of the business in relation to it operations, preparing financial

reports i.e. to be used by the management, helps in decision-making and helping them in

planning policies and strategies.

Management of firm relies on financial information which is provided to them with the

help of financial accounting and from this, managerial reports are prepared and imparted to

management in order to take better decision for the firm. Zylla Company also uses such

accounting as it provides clarity from where it has to improve upon and initiate control upon

expenses for injecting profits. Another essence of such accounting is that business can easily

analyse costs incurred on activities which can be reduced up to a high extent (Aykan and

Aksoylu, 2013). It helps organisation to effectively make decisions with much ease. In relation to

this, requirements of different types of management accounting are as follows-

1. Cost accounting-

1

Management accounting information is crucial for organisation to resolve various issues

and improve upon its performance. Present report deals with importance of management

accounting to Zylla Company by which performance may be enhanced in a better way. Types of

management accounting and methods of reporting are also discussed. Moreover, calculation of

marginal and absorption costing are done. Various planning tools are explained along with

advantages and disadvantages of the same. Furthermore, management accounting systems are

explained which could be used to adapt to respond to financial problems. Thus, such type of

accounting information strengthens internal operations of the company.

P1 Meaning of management accounting and requirements and types of accounting

Management accounting is a useful branch of accounting for the managerial personnel of

the firm so that they may be able to take enhanced decisions in effective manner. This is

essentially required as business operates in dynamic environment where changes takes place now

and often. In such scenario, costs may be increased for manufacturing particular product and as

such, revenue would be impacted significantly. Thus, business needs to make better decisions so

that changes can be handled in effective way and this can be possible because of implementation

of management accounting in the organisation. It refers to that part of management where the

managers look out the needs of the business in relation to it operations, preparing financial

reports i.e. to be used by the management, helps in decision-making and helping them in

planning policies and strategies.

Management of firm relies on financial information which is provided to them with the

help of financial accounting and from this, managerial reports are prepared and imparted to

management in order to take better decision for the firm. Zylla Company also uses such

accounting as it provides clarity from where it has to improve upon and initiate control upon

expenses for injecting profits. Another essence of such accounting is that business can easily

analyse costs incurred on activities which can be reduced up to a high extent (Aykan and

Aksoylu, 2013). It helps organisation to effectively make decisions with much ease. In relation to

this, requirements of different types of management accounting are as follows-

1. Cost accounting-

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting is effective method as it analyse costs and then make attempt to reduce

overall expenditures of the firm incurred on manufacturing commodities. This is quite useful

accounting method as overall costs are assessed and unnecessary expenses are carried out which

are not benefiting in the process and as such, they are reduced up too much extent. Zylla

Company can be benefited by cost accounting as expenditures can be eradicated by cost reports

imparted to management. It is essentially required by the firm so that expenses may not exceed

total revenue. There are different types of costs such as variable, fixed, semi-variable, indirect

and direct which are incurred and management can make enhanced decisions to initiate control

upon the same. Thus, cost accounting is essentially needed in the company to minimise expenses

and maximise profits.

2. Price optimisation technique-

Price optimisation is another useful method which is used to carry out how demand varies

with the change in price of the firm in the best possible manner (Burritt, Schaltegger and

Zvezdov, 2011). It is mathematical model which is utilised to know how customer's behaviour

changes when there is increase or decrease in price of particular commodity. This is used to

assess whether customers are willing to purchase at the prevailing price or not. It helps

organisation to quote price with regards to preferences of consumers and as such, price is quoted

in relation to customer's demand. Thus, company can easily sell its products without any

difficulty. Zylla Company should also rely on the price optimisation technique so that customers

may be able to purchase goods in effective manner. It is important as when prices are high, rivals

may drive away customers and when price are set low, profits cannot be garnered. Thus, through

this method, firm can easily quote price which will be beneficial in every aspect.

3. Inventory management-

Production is required so that company may be able to sell products in effective way.

Customer demand can be easily met by the organisation in effective manner (Cadez and

Guilding, 2012). For accomplishing desired production, inventory is needed in optimum

quantum to achieve production. It is required in adequate quantity so that no spoilage may

occur. Wastage is made when excess quantity is ordered by the production department and as

such, extra costs of handling in the warehouse is incurred. On the other hand, if less stock is

ordered, demand of production department cannot be accomplished. Thus, inventory requirement

2

overall expenditures of the firm incurred on manufacturing commodities. This is quite useful

accounting method as overall costs are assessed and unnecessary expenses are carried out which

are not benefiting in the process and as such, they are reduced up too much extent. Zylla

Company can be benefited by cost accounting as expenditures can be eradicated by cost reports

imparted to management. It is essentially required by the firm so that expenses may not exceed

total revenue. There are different types of costs such as variable, fixed, semi-variable, indirect

and direct which are incurred and management can make enhanced decisions to initiate control

upon the same. Thus, cost accounting is essentially needed in the company to minimise expenses

and maximise profits.

2. Price optimisation technique-

Price optimisation is another useful method which is used to carry out how demand varies

with the change in price of the firm in the best possible manner (Burritt, Schaltegger and

Zvezdov, 2011). It is mathematical model which is utilised to know how customer's behaviour

changes when there is increase or decrease in price of particular commodity. This is used to

assess whether customers are willing to purchase at the prevailing price or not. It helps

organisation to quote price with regards to preferences of consumers and as such, price is quoted

in relation to customer's demand. Thus, company can easily sell its products without any

difficulty. Zylla Company should also rely on the price optimisation technique so that customers

may be able to purchase goods in effective manner. It is important as when prices are high, rivals

may drive away customers and when price are set low, profits cannot be garnered. Thus, through

this method, firm can easily quote price which will be beneficial in every aspect.

3. Inventory management-

Production is required so that company may be able to sell products in effective way.

Customer demand can be easily met by the organisation in effective manner (Cadez and

Guilding, 2012). For accomplishing desired production, inventory is needed in optimum

quantum to achieve production. It is required in adequate quantity so that no spoilage may

occur. Wastage is made when excess quantity is ordered by the production department and as

such, extra costs of handling in the warehouse is incurred. On the other hand, if less stock is

ordered, demand of production department cannot be accomplished. Thus, inventory requirement

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

related managerial report is prepared and desired quantity is ordered which fulfills demand in the

best possible manner. JIT approach is required so that no wastage may occur as inventory is used

only when it is actually needed in production department. EOQ is useful tool to minimise

ordering and carrying cost and purchase desired quantity.

4. Job costing-

Manufacturing of products is done in order to achieve desired production and meet the

demand of customers in effective way. When production is attained, various costs of

manufacturing are incurred. Job costing is a method based on jobs performed by overheads

which are incurred when production is accomplished. This is essentially required so that costs

incurred on various jobs can be analysed and as such, reduction of expenses may be done in

order to achieve maximum efficiency in the best possible way. It helps organisation to

effectively minimise expenditures on jobs so that maximum production can be attained without

incurring more manufacturing overheads. Zylla Organisation can easily attain production by

controlling upon expenses in effective manner (Lachmann, Trapp and Trapp, 2017).

P2 Different methods of management accounting reporting

Various management accounting reports are described below-

1. Segmental report-

There are various units in the company which performs daily operational tasks. Such

units are also called as segments and are assessed by the management and report is provided to

them regarding performances of varied segments in the best possible manner. The segmental

report is also attached in financial statements which can be effectively utilised by users of

accounting information to interpret financial health of the firm and take better decisions. This

report is helpful for investors which may easily carry out whether investment should be made in

the firm or not. On the other hand, creditors are benefited with regards to solvency position of

company whether loan may be provided to organisation or not. The report includes revenue

generated from operating segments. Moreover, it is made available by public entities and not

private ones.

2. Performance report-

3

best possible manner. JIT approach is required so that no wastage may occur as inventory is used

only when it is actually needed in production department. EOQ is useful tool to minimise

ordering and carrying cost and purchase desired quantity.

4. Job costing-

Manufacturing of products is done in order to achieve desired production and meet the

demand of customers in effective way. When production is attained, various costs of

manufacturing are incurred. Job costing is a method based on jobs performed by overheads

which are incurred when production is accomplished. This is essentially required so that costs

incurred on various jobs can be analysed and as such, reduction of expenses may be done in

order to achieve maximum efficiency in the best possible way. It helps organisation to

effectively minimise expenditures on jobs so that maximum production can be attained without

incurring more manufacturing overheads. Zylla Organisation can easily attain production by

controlling upon expenses in effective manner (Lachmann, Trapp and Trapp, 2017).

P2 Different methods of management accounting reporting

Various management accounting reports are described below-

1. Segmental report-

There are various units in the company which performs daily operational tasks. Such

units are also called as segments and are assessed by the management and report is provided to

them regarding performances of varied segments in the best possible manner. The segmental

report is also attached in financial statements which can be effectively utilised by users of

accounting information to interpret financial health of the firm and take better decisions. This

report is helpful for investors which may easily carry out whether investment should be made in

the firm or not. On the other hand, creditors are benefited with regards to solvency position of

company whether loan may be provided to organisation or not. The report includes revenue

generated from operating segments. Moreover, it is made available by public entities and not

private ones.

2. Performance report-

3

This report is prepared to assess performance of something which is directly or indirectly

helping organisation to achieve goals in effective manner. Usually, employees' performance is

judged with the help of this report (Types of Managerial Accounting Reports, 2016). It means

that performance can be evaluated by preparation of the report. Management of Zylla Company

is easily benefited by this report as performance of employee's can be judged in effective manner

and if it is not up to the mark, then improvement may be initiated so that performance can be

maximised with much ease. Thus, variances found in actual results and planned one, corrective

action can be taken so that lost productivity of employees may be attained.

3. Inventory management report-

Inventory is required to be ordered in desired quantity as per the needs and requirements

of the production department so that maximum manufacturing can be achieved in the best

possible manner. This is required in optimum and adequate quantity so that it leads to no

wastage. It occurs when more than required quantum of stocks are purchased, it increases

handling expenses as it is needed to be stored in the warehouse. When the same is available in

less quantity, desired production cannot be accomplished. In order to overcome this situation,

inventory management report is prepared (Leotta, Rizza and Ruggeri, 2017). The production

department provides clarity to the management regarding the requirement of inventory in order

to accomplish customer's needs. This report is then provided to Zylla Company's management so

that they may analyse demand and as such, required quantity is purchased and supplied to

production department. Thus, spoilage of resources is eradicated as inventory is managed

effectually.

4. Job costing report-

Job costing is effective way of analysing expenses incurred on various manufacturing

jobs engaged in the production process. In relation to this, job costing report and imparted to

management so that costs on specific jobs can be assessed and measures can be taken to initiate

control upon expenditures in the best possible manner which are not benefiting in overall

production and reducing profits. Thus, with the help of job costing report, expenses on overheads

can be controlled in a better way. Hence, Zylla Company can reduce expenditures on those jobs

which are underperforming and direct those funds to good performing overheads helping in

maximising level of production (MONEM and SAEIDI, 2017).

4

helping organisation to achieve goals in effective manner. Usually, employees' performance is

judged with the help of this report (Types of Managerial Accounting Reports, 2016). It means

that performance can be evaluated by preparation of the report. Management of Zylla Company

is easily benefited by this report as performance of employee's can be judged in effective manner

and if it is not up to the mark, then improvement may be initiated so that performance can be

maximised with much ease. Thus, variances found in actual results and planned one, corrective

action can be taken so that lost productivity of employees may be attained.

3. Inventory management report-

Inventory is required to be ordered in desired quantity as per the needs and requirements

of the production department so that maximum manufacturing can be achieved in the best

possible manner. This is required in optimum and adequate quantity so that it leads to no

wastage. It occurs when more than required quantum of stocks are purchased, it increases

handling expenses as it is needed to be stored in the warehouse. When the same is available in

less quantity, desired production cannot be accomplished. In order to overcome this situation,

inventory management report is prepared (Leotta, Rizza and Ruggeri, 2017). The production

department provides clarity to the management regarding the requirement of inventory in order

to accomplish customer's needs. This report is then provided to Zylla Company's management so

that they may analyse demand and as such, required quantity is purchased and supplied to

production department. Thus, spoilage of resources is eradicated as inventory is managed

effectually.

4. Job costing report-

Job costing is effective way of analysing expenses incurred on various manufacturing

jobs engaged in the production process. In relation to this, job costing report and imparted to

management so that costs on specific jobs can be assessed and measures can be taken to initiate

control upon expenditures in the best possible manner which are not benefiting in overall

production and reducing profits. Thus, with the help of job costing report, expenses on overheads

can be controlled in a better way. Hence, Zylla Company can reduce expenditures on those jobs

which are underperforming and direct those funds to good performing overheads helping in

maximising level of production (MONEM and SAEIDI, 2017).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5. Accounts receivables ageing report-

Customers are provided with goods on cash or credit basis. When goods are imparted to

customers on credit, payment for the same is received afterwards within credit policy formulated

by the firm. In relation to this, accounts receivables ageing report is prepared by the company so

that it may be able to clarify how much amount is pending to be collected from the debtors. This

report is formulated in which unpaid invoices of consumers are carried out along with their

names and outstanding amount is listed as well. This help organisation to effectively extract how

much money remains outstanding and as such, company can collect the same from the

customers. If more amount is pending, firm needs to implement strict strategies so that payment

may be recovered within stipulated time.

Benefits of management accounting systems

The management accounting systems have immense benefits to organisation. Costs can

be analysed and controlled in a better way because of cost accounting. It is helpful as company is

able to initiate control upon expenses in the best possible manner. Furthermore, enhanced

decisions can be taken with the help of management accounting systems. On the other hand, firm

is able to assess demand of customers by forecasting their requirements and as such, demand can

be analysed and as a result, profits may be garnered with much ease.

P3 Computation of marginal and absorption costing

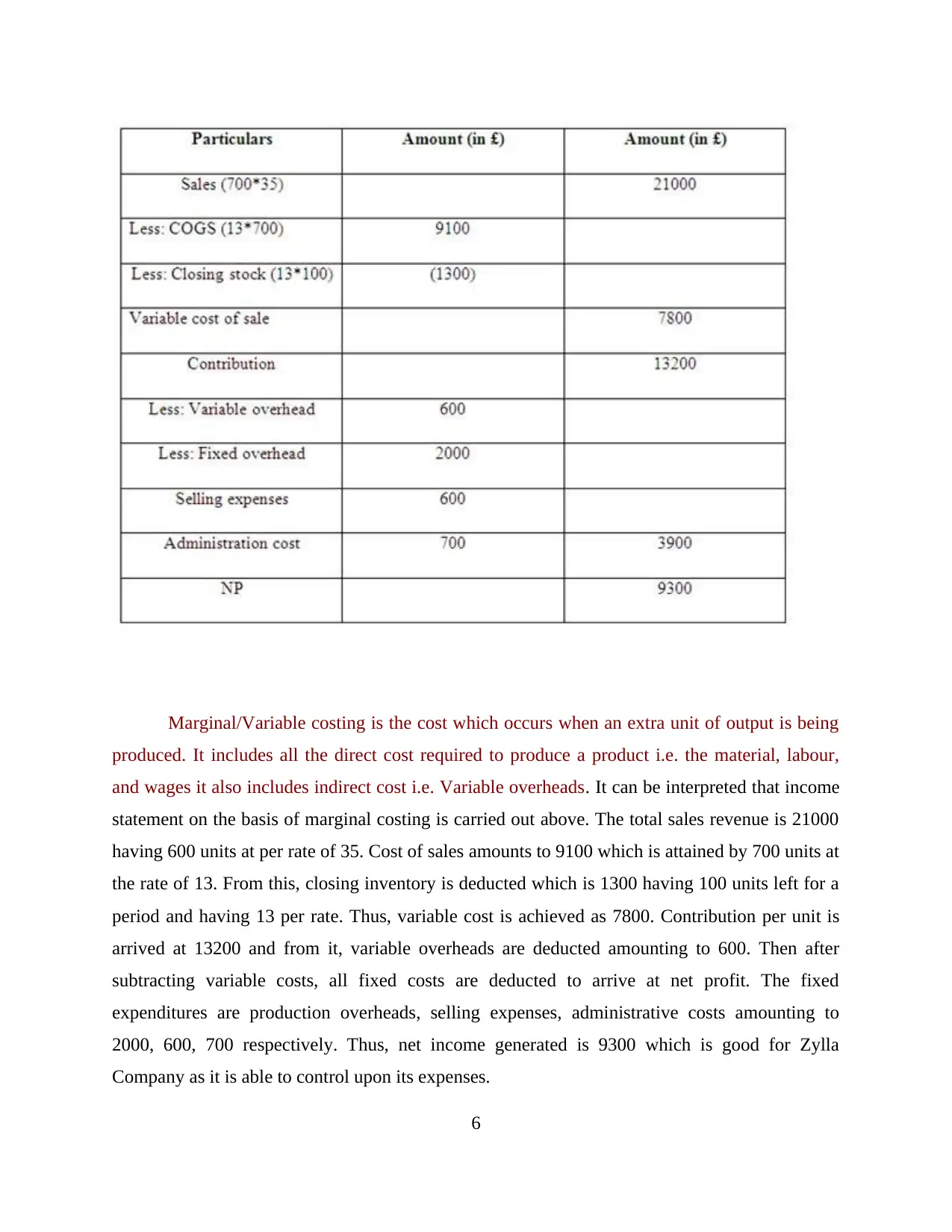

Marginal Costing income statement

5

Customers are provided with goods on cash or credit basis. When goods are imparted to

customers on credit, payment for the same is received afterwards within credit policy formulated

by the firm. In relation to this, accounts receivables ageing report is prepared by the company so

that it may be able to clarify how much amount is pending to be collected from the debtors. This

report is formulated in which unpaid invoices of consumers are carried out along with their

names and outstanding amount is listed as well. This help organisation to effectively extract how

much money remains outstanding and as such, company can collect the same from the

customers. If more amount is pending, firm needs to implement strict strategies so that payment

may be recovered within stipulated time.

Benefits of management accounting systems

The management accounting systems have immense benefits to organisation. Costs can

be analysed and controlled in a better way because of cost accounting. It is helpful as company is

able to initiate control upon expenses in the best possible manner. Furthermore, enhanced

decisions can be taken with the help of management accounting systems. On the other hand, firm

is able to assess demand of customers by forecasting their requirements and as such, demand can

be analysed and as a result, profits may be garnered with much ease.

P3 Computation of marginal and absorption costing

Marginal Costing income statement

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal/Variable costing is the cost which occurs when an extra unit of output is being

produced. It includes all the direct cost required to produce a product i.e. the material, labour,

and wages it also includes indirect cost i.e. Variable overheads. It can be interpreted that income

statement on the basis of marginal costing is carried out above. The total sales revenue is 21000

having 600 units at per rate of 35. Cost of sales amounts to 9100 which is attained by 700 units at

the rate of 13. From this, closing inventory is deducted which is 1300 having 100 units left for a

period and having 13 per rate. Thus, variable cost is achieved as 7800. Contribution per unit is

arrived at 13200 and from it, variable overheads are deducted amounting to 600. Then after

subtracting variable costs, all fixed costs are deducted to arrive at net profit. The fixed

expenditures are production overheads, selling expenses, administrative costs amounting to

2000, 600, 700 respectively. Thus, net income generated is 9300 which is good for Zylla

Company as it is able to control upon its expenses.

6

produced. It includes all the direct cost required to produce a product i.e. the material, labour,

and wages it also includes indirect cost i.e. Variable overheads. It can be interpreted that income

statement on the basis of marginal costing is carried out above. The total sales revenue is 21000

having 600 units at per rate of 35. Cost of sales amounts to 9100 which is attained by 700 units at

the rate of 13. From this, closing inventory is deducted which is 1300 having 100 units left for a

period and having 13 per rate. Thus, variable cost is achieved as 7800. Contribution per unit is

arrived at 13200 and from it, variable overheads are deducted amounting to 600. Then after

subtracting variable costs, all fixed costs are deducted to arrive at net profit. The fixed

expenditures are production overheads, selling expenses, administrative costs amounting to

2000, 600, 700 respectively. Thus, net income generated is 9300 which is good for Zylla

Company as it is able to control upon its expenses.

6

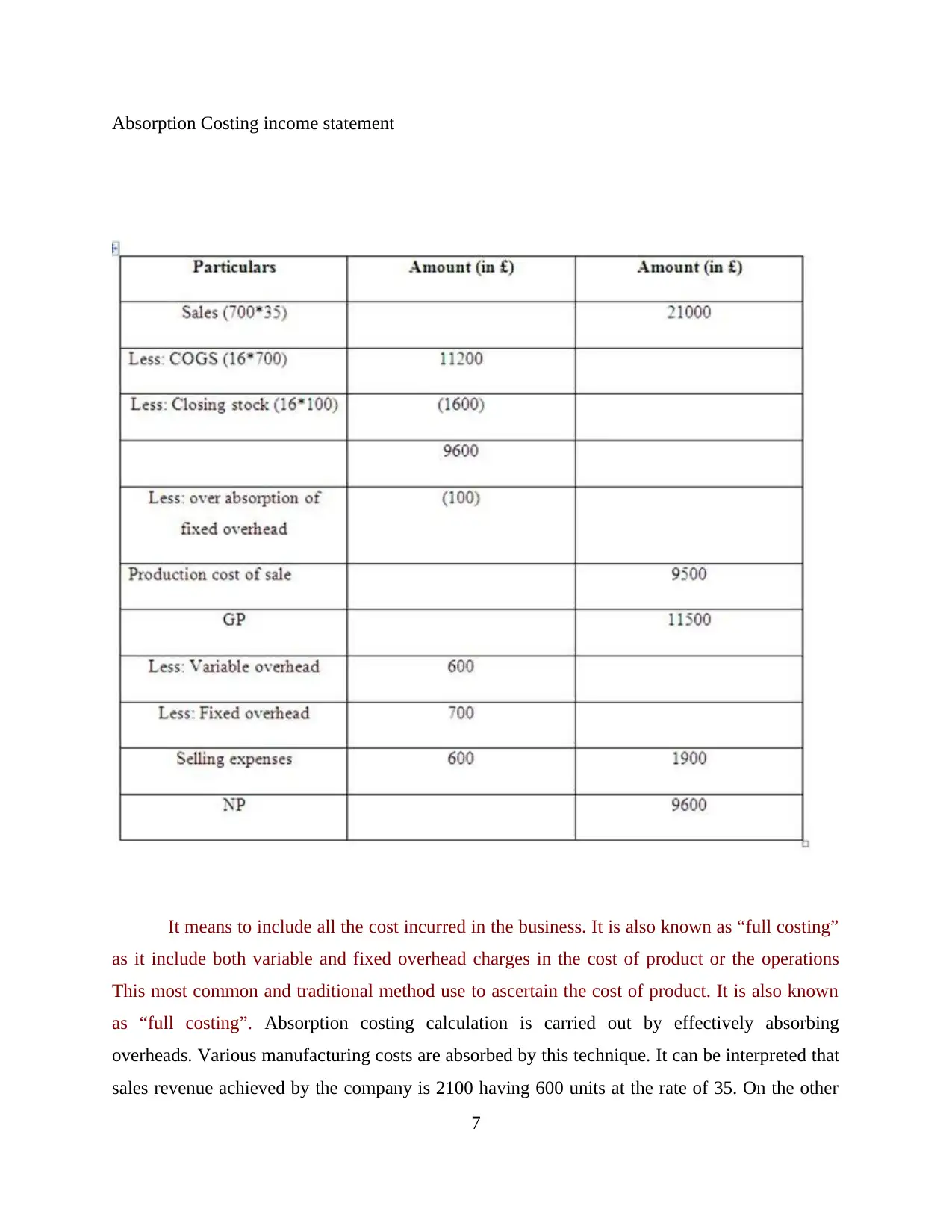

Absorption Costing income statement

It means to include all the cost incurred in the business. It is also known as “full costing”

as it include both variable and fixed overhead charges in the cost of product or the operations

This most common and traditional method use to ascertain the cost of product. It is also known

as “full costing”. Absorption costing calculation is carried out by effectively absorbing

overheads. Various manufacturing costs are absorbed by this technique. It can be interpreted that

sales revenue achieved by the company is 2100 having 600 units at the rate of 35. On the other

7

It means to include all the cost incurred in the business. It is also known as “full costing”

as it include both variable and fixed overhead charges in the cost of product or the operations

This most common and traditional method use to ascertain the cost of product. It is also known

as “full costing”. Absorption costing calculation is carried out by effectively absorbing

overheads. Various manufacturing costs are absorbed by this technique. It can be interpreted that

sales revenue achieved by the company is 2100 having 600 units at the rate of 35. On the other

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

hand, cost of production is 11200 which can be further bifurcated as 700 units at rate of 16. The

closing stock is 1600 and accounting to fixed production overheads is 100. Thus, total cost of

production is 9500 and as such, contribution per unit is 11500. On the other hand, variable cost

of 600 is deducted. Furthermore, all fixed costs are deducted such as selling and administrative

ones. Thus, profit arrived is 9600 which means that Zylla Company has gained good net income

after effectively absorbing manufacturing expenses (Turner and et.al, 2017).

Range of management accounting techniques

There are various techniques which are helpful to the organisation to improve upon its

performance. Among this is cost variance which is the difference between actual and planned

costs. It can be said that such technique is helpful for producing financial documents quite

effectually. Another technique is revaluation accounting which implies that revaluation of assets

is done so that book value and market value can be adjusted. This help Zylla Company to

effectively prepare financial documents.

P4 Different types of planning tools and merits and demerits

The various planning tools and advantages and disadvantages are listed below-

1. IRR-

IRR (Internal Rate of Return) is another effective method used to judge potentiality of the

investment in effectual manner. It is uses discounting rate which makes NPV (Net Present

Value) of cash inflows of new project to zero. This means that return that will be generated from

internal operations is carried out by this planning tool. Higher the IRR, better for Zylla Company

to invest in the project (Fourie, Opperman, Scott and Kumar, 2015).

Merits

1. One of the main advantage of IRR is that it takes into consideration time value of

concept in effective manner. Moreover, it analyses cash flows that will generate internal returns.

2. Another merit of this planning tool is that calculating IRR by taking discounting rate is

an easier task to be accomplished. Thus, potentiality and effectiveness of project can be judged

with much ease.

Demerits

1. The main disadvantage of IRR project size is not taken into account. Thus, cash flows

are analysed and compared with the capital invested in the new project.

8

closing stock is 1600 and accounting to fixed production overheads is 100. Thus, total cost of

production is 9500 and as such, contribution per unit is 11500. On the other hand, variable cost

of 600 is deducted. Furthermore, all fixed costs are deducted such as selling and administrative

ones. Thus, profit arrived is 9600 which means that Zylla Company has gained good net income

after effectively absorbing manufacturing expenses (Turner and et.al, 2017).

Range of management accounting techniques

There are various techniques which are helpful to the organisation to improve upon its

performance. Among this is cost variance which is the difference between actual and planned

costs. It can be said that such technique is helpful for producing financial documents quite

effectually. Another technique is revaluation accounting which implies that revaluation of assets

is done so that book value and market value can be adjusted. This help Zylla Company to

effectively prepare financial documents.

P4 Different types of planning tools and merits and demerits

The various planning tools and advantages and disadvantages are listed below-

1. IRR-

IRR (Internal Rate of Return) is another effective method used to judge potentiality of the

investment in effectual manner. It is uses discounting rate which makes NPV (Net Present

Value) of cash inflows of new project to zero. This means that return that will be generated from

internal operations is carried out by this planning tool. Higher the IRR, better for Zylla Company

to invest in the project (Fourie, Opperman, Scott and Kumar, 2015).

Merits

1. One of the main advantage of IRR is that it takes into consideration time value of

concept in effective manner. Moreover, it analyses cash flows that will generate internal returns.

2. Another merit of this planning tool is that calculating IRR by taking discounting rate is

an easier task to be accomplished. Thus, potentiality and effectiveness of project can be judged

with much ease.

Demerits

1. The main disadvantage of IRR project size is not taken into account. Thus, cash flows

are analysed and compared with the capital invested in the new project.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. IRR is not suitable as future expenditures are not focused at all. This method only takes

into account present value.

2. NPV-

NPV is one of the commonly used planning tool by the business in order to judge how

much profitable is the new project (Maher, Fakhar and Karimi, 2018). This means that

profitability aspect of project is analysed and as such, firm is able to take decision whether

investment should be made or not. Higher the NPV, better for the organisation as investing in

project is worthwhile. NPV is difference between cash inflows and outflows for a particular

period.

Merits

1. One of the main advantage of NPV is that time value concept of money is considered

while evaluating profitability aspect of the project.

2. It is useful as cost of capital and risk associated while making estimations regarding

future is ascertained in effective manner.

Demerits

1. It is disadvantageous as it relies on discounting rate which is difficult to ascertain.

Moreover, projections on such basis may lead to inaccurate decisions.

2. This method is not useful as cost of capital is obtained with much of guesswork and as

such, results drawn on this basis may outweigh good investment and wrong conclusion can be

drawn (Quattrone, 2016).

3. Forecasting- It is effective planning tool as it is used to predict future sales of entity.

Merits

Predicts future sales in effective way.

Expenditures can be analysed easily.

Demerits

Dependent on judgement of experts which are not correct sometimes.

Proper analysis cannot be accomplished as it is based on assumption

4. Variance analysis – It is used to figure out deviations between planned and actual results.

Merits

It is useful and simple to analyse variances

Corrective action is taken for improvement

9

into account present value.

2. NPV-

NPV is one of the commonly used planning tool by the business in order to judge how

much profitable is the new project (Maher, Fakhar and Karimi, 2018). This means that

profitability aspect of project is analysed and as such, firm is able to take decision whether

investment should be made or not. Higher the NPV, better for the organisation as investing in

project is worthwhile. NPV is difference between cash inflows and outflows for a particular

period.

Merits

1. One of the main advantage of NPV is that time value concept of money is considered

while evaluating profitability aspect of the project.

2. It is useful as cost of capital and risk associated while making estimations regarding

future is ascertained in effective manner.

Demerits

1. It is disadvantageous as it relies on discounting rate which is difficult to ascertain.

Moreover, projections on such basis may lead to inaccurate decisions.

2. This method is not useful as cost of capital is obtained with much of guesswork and as

such, results drawn on this basis may outweigh good investment and wrong conclusion can be

drawn (Quattrone, 2016).

3. Forecasting- It is effective planning tool as it is used to predict future sales of entity.

Merits

Predicts future sales in effective way.

Expenditures can be analysed easily.

Demerits

Dependent on judgement of experts which are not correct sometimes.

Proper analysis cannot be accomplished as it is based on assumption

4. Variance analysis – It is used to figure out deviations between planned and actual results.

Merits

It is useful and simple to analyse variances

Corrective action is taken for improvement

9

Demerits

It takes lot of time to assess differences

Routine work is hampered of personnels and productivity is reduced.

5. Standard costing- It is used to take difference between actual and expected costs if any.

Merits

Cost variances are removed instantly

Reduction in cost can be attained.

Demerits

It is difficult to carry out variances

It is time consuming technique

Use of various planning tools

The planning tools such as zero-based budgeting, NPV and IRR are effective planning

tools which are helpful in preparing forecasts and budgets. Zero-based budgeting help to prepare

budget from scratch base and as such, no historical figure of previous budgets are taken and as

such, fresh budget is prepared. This planning tool is widely used in the business to formulate

budget. Moreover, IRR is used to test potentiality of investment so that project may be analysed

whether adequate returns will be generated by investment or not. On the other hand, NPV is

widely used to check whether new project would be profitable for the firm or not. Moreover,

concept of time value of money is utilised by NPV. Thus, planning tools are effective way to

forecast budgets.

P5 How management accounting system used to respond to financial problems

Financial problems can be easily resolved by Zylla Company by taking into consideration

management accounting systems. These are described below-

1. Balanced Scorecard-

The balanced scorecard is one of the effective system to respond to financial problems of

firm (Renz and Herman, 2016). This system measures viability of internal functions and as such,

external results can be generated in the best possible manner. If external outcome is not good,

feedback is provided to company to improve upon and strengthen internal functions for desired

results. With the help of this system, improvement is done which is effectively strengthens

organisation's internally and as such, financial issues can be resolved in effectual way.

10

It takes lot of time to assess differences

Routine work is hampered of personnels and productivity is reduced.

5. Standard costing- It is used to take difference between actual and expected costs if any.

Merits

Cost variances are removed instantly

Reduction in cost can be attained.

Demerits

It is difficult to carry out variances

It is time consuming technique

Use of various planning tools

The planning tools such as zero-based budgeting, NPV and IRR are effective planning

tools which are helpful in preparing forecasts and budgets. Zero-based budgeting help to prepare

budget from scratch base and as such, no historical figure of previous budgets are taken and as

such, fresh budget is prepared. This planning tool is widely used in the business to formulate

budget. Moreover, IRR is used to test potentiality of investment so that project may be analysed

whether adequate returns will be generated by investment or not. On the other hand, NPV is

widely used to check whether new project would be profitable for the firm or not. Moreover,

concept of time value of money is utilised by NPV. Thus, planning tools are effective way to

forecast budgets.

P5 How management accounting system used to respond to financial problems

Financial problems can be easily resolved by Zylla Company by taking into consideration

management accounting systems. These are described below-

1. Balanced Scorecard-

The balanced scorecard is one of the effective system to respond to financial problems of

firm (Renz and Herman, 2016). This system measures viability of internal functions and as such,

external results can be generated in the best possible manner. If external outcome is not good,

feedback is provided to company to improve upon and strengthen internal functions for desired

results. With the help of this system, improvement is done which is effectively strengthens

organisation's internally and as such, financial issues can be resolved in effectual way.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.