Input Tax Credit and GST Rulings

VerifiedAdded on 2020/04/07

|12

|1982

|33

AI Summary

The assignment delves into the complexities of input tax credit within the Goods and Services Tax (GST) framework. It examines GSTR 2006/3, a taxation ruling that clarifies methods for determining input tax credit eligibility under the new GST Act 1999. The analysis focuses on 'extent' and 'to the extent' doctrines applied in interpreting GST legislation, using the case of Ronpibon Tin NL v. FC of T as an example. It further explores how advertising expenses incurred by Big Bank Ltd for creditable acquisitions can be claimed as input tax credit based on GSTR 2006/13.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of Student:

Name of University:

Author’s Note:

Taxation Law

Name of Student:

Name of University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Answer 1:

Answer to requirement 1:

Issue:

The situation at present considers the fact that the cost incurred in moving machinery to a

new site can be thought of as permissible deductions or not in compliance with the section 8(1)

of the ITAA 1997.

Laws:

a. “Section 8-1 of the Income Tax Assessment Act 1997”

b. “British Insulated & Helsby Cables”

Application:

In compliance with the of -1 of the Income Tax Assessment Act 1997, the cost which is

incurred in the location of the machinery to a new site represents the nature of the capital nature

and no sort of permissible deductions is allowed in case of this particular scenario. Due to

depreciation reasons, the movement of the machinery represents a small change cost and it is

stated that it will be allowed as permissible deductions under the section 8(1) of the Income Tax

Assessment Act 1997.

The major reason for putting importance in the expe4nses for the purpose of permissible

deductions results from the daily business operations.

Answer 1:

Answer to requirement 1:

Issue:

The situation at present considers the fact that the cost incurred in moving machinery to a

new site can be thought of as permissible deductions or not in compliance with the section 8(1)

of the ITAA 1997.

Laws:

a. “Section 8-1 of the Income Tax Assessment Act 1997”

b. “British Insulated & Helsby Cables”

Application:

In compliance with the of -1 of the Income Tax Assessment Act 1997, the cost which is

incurred in the location of the machinery to a new site represents the nature of the capital nature

and no sort of permissible deductions is allowed in case of this particular scenario. Due to

depreciation reasons, the movement of the machinery represents a small change cost and it is

stated that it will be allowed as permissible deductions under the section 8(1) of the Income Tax

Assessment Act 1997.

The major reason for putting importance in the expe4nses for the purpose of permissible

deductions results from the daily business operations.

2TAXATION LAW

Based on the British Insulated & Helsby Cables verdict the involved cost in the

transportation is characteristic of the increasing benefit on the business related premises due to

shift of the depreciable assets.

According to the Taxation Ruling of TD 93/126, the machinery installation and the

beginning of the business functions the occurrence cost in bringing the machine for the complete

operation is to be considered as revenue. It is clearly inferred from the above situation that the

locating of the machine to the new site is to be treated as non-allowable deductions (Reaves and

Bauer 2012).

Conclusion:

The obtained cost in movement of the machine to a new site is representative of the

movement of an asset from a particular place to another. It is also noted that it is to be considered

as capital expenditure (Posner 2014). In connection to this the permissible deductions will be

allowed in compliance with section 8(1) of the Income Tax Assessment Act 1997.

Answer to requirement 2:

Issue:

The situation helps in understanding if the revaluation of the assets to affect the cover of

insurance would be viewed as allowable deductions in compliance with the “section 8(1) of the

Income Tax Assessment Act 1997”.

Laws:

a. “Section 8-1 of the Income Tax Assessment Act 1997”

Based on the British Insulated & Helsby Cables verdict the involved cost in the

transportation is characteristic of the increasing benefit on the business related premises due to

shift of the depreciable assets.

According to the Taxation Ruling of TD 93/126, the machinery installation and the

beginning of the business functions the occurrence cost in bringing the machine for the complete

operation is to be considered as revenue. It is clearly inferred from the above situation that the

locating of the machine to the new site is to be treated as non-allowable deductions (Reaves and

Bauer 2012).

Conclusion:

The obtained cost in movement of the machine to a new site is representative of the

movement of an asset from a particular place to another. It is also noted that it is to be considered

as capital expenditure (Posner 2014). In connection to this the permissible deductions will be

allowed in compliance with section 8(1) of the Income Tax Assessment Act 1997.

Answer to requirement 2:

Issue:

The situation helps in understanding if the revaluation of the assets to affect the cover of

insurance would be viewed as allowable deductions in compliance with the “section 8(1) of the

Income Tax Assessment Act 1997”.

Laws:

a. “Section 8-1 of the Income Tax Assessment Act 1997”

3TAXATION LAW

Application:

It is evident from the discussed scenario at present that the expense possessing

association with the fixed assets makes it necessary to determine whether such expenditures have

occurred in the revelation acquired in increasing the revenue producing capacity while

determining the deductions. It is also to be seen whether it is used in just the asset protection

(Scholes 2015).

In case the latter helps in the benefit of the temporary nature it is possible that the

expenditure is probably repetitive and needs to be treated as allowable deductions. This should

be considered in compliance with the section 8-1 of the Income Tax Assessment Act 1997. This

is done usually as the occurred expenses are basically repetitive in nature (Zelenak 2012).

Conclusion:

It can be concluded that the cost that leads to the cover of the insurance is to be

considered ads permissible deductions and it is to be considered so under the “section 8-1 of the

ITAA 1997”.

Answer to requirement 3:

Issue:

The situation helps in bringing to the fore the issue of whether the legal expenditures

incurred by the company in opposing the petition for the winding up would be considered with

deductions with reference to the “section 8(1) of the ITAA 1997”.

Application:

It is evident from the discussed scenario at present that the expense possessing

association with the fixed assets makes it necessary to determine whether such expenditures have

occurred in the revelation acquired in increasing the revenue producing capacity while

determining the deductions. It is also to be seen whether it is used in just the asset protection

(Scholes 2015).

In case the latter helps in the benefit of the temporary nature it is possible that the

expenditure is probably repetitive and needs to be treated as allowable deductions. This should

be considered in compliance with the section 8-1 of the Income Tax Assessment Act 1997. This

is done usually as the occurred expenses are basically repetitive in nature (Zelenak 2012).

Conclusion:

It can be concluded that the cost that leads to the cover of the insurance is to be

considered ads permissible deductions and it is to be considered so under the “section 8-1 of the

ITAA 1997”.

Answer to requirement 3:

Issue:

The situation helps in bringing to the fore the issue of whether the legal expenditures

incurred by the company in opposing the petition for the winding up would be considered with

deductions with reference to the “section 8(1) of the ITAA 1997”.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

Laws:

a. “Section 8-1 of the Income Tax Assessment Act 1997”

b. “FC of T v Snowden and Wilson Pty Ltd (1958) 99 CLR 431)”

Application:

In the case of FC of T v Snowden and Wilson Pty Ltd (1958) those expenditures which

are not usual are given notice and in no previous situation the taxpayer is required to commence

the lawful actions as in no situations it helps in the prevention of the expenditure to qualify as a

deductable expenditure.

As mentioned under “section 8-1 of the Income Tax Assessment Act 1997”, cost

incurred in the business windup is usually incurred in the operations of the business and are not

accountable as permissible deductions. The “taxation ruling of ID 2004/367”represents that

legal cost will be considered for deductions if the cost is for carrying out the business operation

through which an individual produces the taxable proceeds (Lang 2014).

The situations in which the legal expenditure occurs for the differences in the winding up

of the petition cannot be allowed as deductions. This is due to the fact that they re[present the

characteristics of the capitalistic nature and the expenditures are in connection to that of the

business operations.

Conclusion:

It is clearly understood form the situation that the cost incurred in the opposing of

the petition of the winding up is to be treated ads non-allowable deductions which is under the

“section 8(1) of the ITAA 1997”.

Laws:

a. “Section 8-1 of the Income Tax Assessment Act 1997”

b. “FC of T v Snowden and Wilson Pty Ltd (1958) 99 CLR 431)”

Application:

In the case of FC of T v Snowden and Wilson Pty Ltd (1958) those expenditures which

are not usual are given notice and in no previous situation the taxpayer is required to commence

the lawful actions as in no situations it helps in the prevention of the expenditure to qualify as a

deductable expenditure.

As mentioned under “section 8-1 of the Income Tax Assessment Act 1997”, cost

incurred in the business windup is usually incurred in the operations of the business and are not

accountable as permissible deductions. The “taxation ruling of ID 2004/367”represents that

legal cost will be considered for deductions if the cost is for carrying out the business operation

through which an individual produces the taxable proceeds (Lang 2014).

The situations in which the legal expenditure occurs for the differences in the winding up

of the petition cannot be allowed as deductions. This is due to the fact that they re[present the

characteristics of the capitalistic nature and the expenditures are in connection to that of the

business operations.

Conclusion:

It is clearly understood form the situation that the cost incurred in the opposing of

the petition of the winding up is to be treated ads non-allowable deductions which is under the

“section 8(1) of the ITAA 1997”.

5TAXATION LAW

Answer to requirement 4:

Issue:

The current scenario determines whether or not the legal expenditure which is occurred

for the solicitor services with regard to the numerous business operation of the clients that will be

viewed as allowable for deductions under the “section 8(1) of the ITAA 1997”.

Laws:

a. “section 8-1 of the Income Tax Assessment Act 1997”

Application:

Based on the “section 8-1 of the Income Tax Assessment Act 1997”, in case a legal

expense takes place in respect of the business operations in order to produce the revenue it is to

be treated as allowable deductions.

Certain exceptions are there however in cases of legal expenses which symbolizes capital

domestic as also private in nature. This is in case the particularly incurred producing the exempt

as well as non-chargeable non-exempt goods (Bodie 2013).

Based on the above discussion, in case an individual incurs a legal fees may not be

treated as allowable deductions given that there is not any sort of relation in the taxable income

generation (Graetz and Schenk 2009).

According to the section “8(1) of the ITAA 1997”, the legal expense obtained by the

taxpayer in the laying down of the fact that it has a connection with the business in the

production of the chargeable income will be allowed in the form of permissible deductions.

Answer to requirement 4:

Issue:

The current scenario determines whether or not the legal expenditure which is occurred

for the solicitor services with regard to the numerous business operation of the clients that will be

viewed as allowable for deductions under the “section 8(1) of the ITAA 1997”.

Laws:

a. “section 8-1 of the Income Tax Assessment Act 1997”

Application:

Based on the “section 8-1 of the Income Tax Assessment Act 1997”, in case a legal

expense takes place in respect of the business operations in order to produce the revenue it is to

be treated as allowable deductions.

Certain exceptions are there however in cases of legal expenses which symbolizes capital

domestic as also private in nature. This is in case the particularly incurred producing the exempt

as well as non-chargeable non-exempt goods (Bodie 2013).

Based on the above discussion, in case an individual incurs a legal fees may not be

treated as allowable deductions given that there is not any sort of relation in the taxable income

generation (Graetz and Schenk 2009).

According to the section “8(1) of the ITAA 1997”, the legal expense obtained by the

taxpayer in the laying down of the fact that it has a connection with the business in the

production of the chargeable income will be allowed in the form of permissible deductions.

6TAXATION LAW

Conclusion:

The entire situation is enlightening regarding the business aspects and their operations. It

helps to understand that the production of the taxable income needs to be treated ad permissible

deductions in compliance with “section 8-1 of the ITAA 1997” .

Answer to question 2:

Issue:

The current scenario of the Big Bank is related to the determining the input tax credit

with respect to the expenditure of the advertisement is incurred. This is in connection to the

GSTR Act 1999.

Legislation:

a. “GST Act 1999”

b. “paragraphs 11-5 and 15-5”

c. “subsection 15-25”

d. “Goods and Service taxation ruling of GSTR 2006/3”

e. “Ronpibon Tin NL v. FC of T”

Application:

The Situation of the Big Bank is extremely enlightening regarding the situation. Big Bank

Ltd has incurred an expense of $1,650,000 as GST was inclusive of the advertisement in the

previous year. With connection to the situation the taxation ruling of Goods and Service taxation

Conclusion:

The entire situation is enlightening regarding the business aspects and their operations. It

helps to understand that the production of the taxable income needs to be treated ad permissible

deductions in compliance with “section 8-1 of the ITAA 1997” .

Answer to question 2:

Issue:

The current scenario of the Big Bank is related to the determining the input tax credit

with respect to the expenditure of the advertisement is incurred. This is in connection to the

GSTR Act 1999.

Legislation:

a. “GST Act 1999”

b. “paragraphs 11-5 and 15-5”

c. “subsection 15-25”

d. “Goods and Service taxation ruling of GSTR 2006/3”

e. “Ronpibon Tin NL v. FC of T”

Application:

The Situation of the Big Bank is extremely enlightening regarding the situation. Big Bank

Ltd has incurred an expense of $1,650,000 as GST was inclusive of the advertisement in the

previous year. With connection to the situation the taxation ruling of Goods and Service taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

ruling of GSTR 2006/3 is applicable. This is due to the reason that the company is eligible or the

input tax credit.

The taxation ruling of the Goods and Service of GSTR 2006/3 gives an insight regarding

the methods needed to be implemented in order to determine the input tax credit. This is also in

connection to changes needed for the administration for the change in requirement of the fiscal

supplies. This is under the new tax system GST Act 1999.

It includes the extent of the creditable purpose and also the actual ruling applications

under division 11,15 and 129 of the GST Act. The rules apply to those cases where registration is

required for the obtaining of the registration as it is necessary to acquire those economic supplies

that exceed the financial acquisition’s threshold limt.

In the case of Ronpibon Tin NL v. FC of T the doctrine of “extent” and “to the extent” is

applied in analysing the legislation of GST. This involves the obligations in which the adoption

method needs to be genuine and just. As in the under the paragraph 11-5 and 15-5 to qualify an

acquisition as the creditable acquisition it must be creditable either entirely or in parts.

The scheme of the GST legislation provides that an entity or an individual needs to claim

input tax credit for the GST inclusive supplies that is acquired or import for the entity. If an

individual making a financial supplies and goes past the financial acquisition threshold, they will

not be entitled to recover all the GST charged to them however a part of such GST can be

recovered by the company.

The paragraphs 11-5 and 15-5 (a), clearly states the concepts of creditability as well as

creditable importation. The acquisition needs to be creditable. In regard to section 11-15 or 15-

10 an acquisition qualifies to be creditable if an entity makes the supplies for the purpose of

ruling of GSTR 2006/3 is applicable. This is due to the reason that the company is eligible or the

input tax credit.

The taxation ruling of the Goods and Service of GSTR 2006/3 gives an insight regarding

the methods needed to be implemented in order to determine the input tax credit. This is also in

connection to changes needed for the administration for the change in requirement of the fiscal

supplies. This is under the new tax system GST Act 1999.

It includes the extent of the creditable purpose and also the actual ruling applications

under division 11,15 and 129 of the GST Act. The rules apply to those cases where registration is

required for the obtaining of the registration as it is necessary to acquire those economic supplies

that exceed the financial acquisition’s threshold limt.

In the case of Ronpibon Tin NL v. FC of T the doctrine of “extent” and “to the extent” is

applied in analysing the legislation of GST. This involves the obligations in which the adoption

method needs to be genuine and just. As in the under the paragraph 11-5 and 15-5 to qualify an

acquisition as the creditable acquisition it must be creditable either entirely or in parts.

The scheme of the GST legislation provides that an entity or an individual needs to claim

input tax credit for the GST inclusive supplies that is acquired or import for the entity. If an

individual making a financial supplies and goes past the financial acquisition threshold, they will

not be entitled to recover all the GST charged to them however a part of such GST can be

recovered by the company.

The paragraphs 11-5 and 15-5 (a), clearly states the concepts of creditability as well as

creditable importation. The acquisition needs to be creditable. In regard to section 11-15 or 15-

10 an acquisition qualifies to be creditable if an entity makes the supplies for the purpose of

8TAXATION LAW

claiming input tax credit. It needs to be mentioned that the advertising expenditure incurred by

the Big Bank Ltd, for the purpose of the creditable acquisitions. With references to GSTR ruling

of 2006/3, the Big Bank Ltd has gone past the financial acquisition threshold limit and the

invoice that is issued to Big Bank Ltd will be entitled for input tax credit for the GST supplies

made. This needs to be understood that the situation is crucial.

Conclusion:

It helps to arrive at the conclusion that Bi Bank is eligible to claim the income tax credit

with regard to the GSTR 2006/13 this is for the amount incurred in the expenses related to

advertising due to the creditable acquisition purposes.

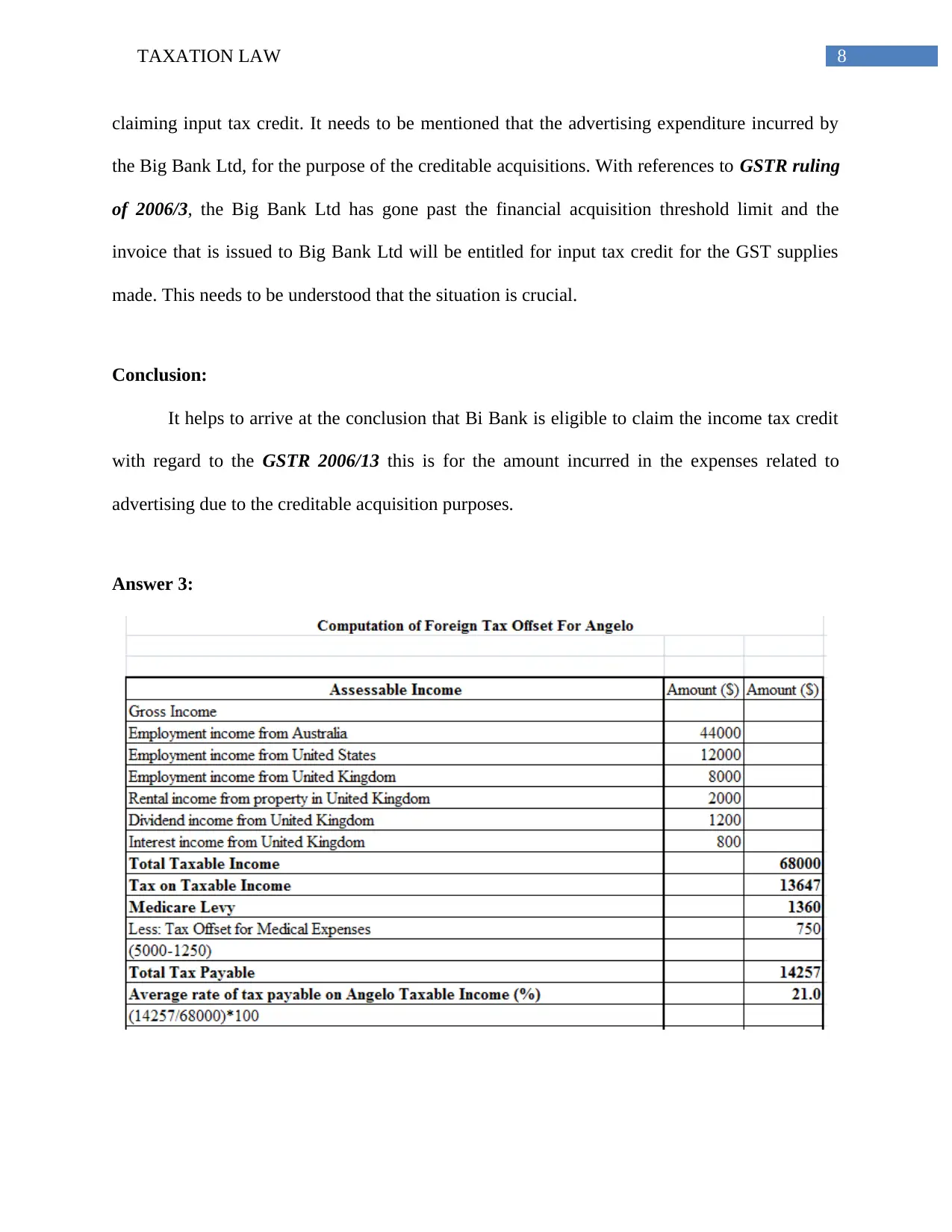

Answer 3:

claiming input tax credit. It needs to be mentioned that the advertising expenditure incurred by

the Big Bank Ltd, for the purpose of the creditable acquisitions. With references to GSTR ruling

of 2006/3, the Big Bank Ltd has gone past the financial acquisition threshold limit and the

invoice that is issued to Big Bank Ltd will be entitled for input tax credit for the GST supplies

made. This needs to be understood that the situation is crucial.

Conclusion:

It helps to arrive at the conclusion that Bi Bank is eligible to claim the income tax credit

with regard to the GSTR 2006/13 this is for the amount incurred in the expenses related to

advertising due to the creditable acquisition purposes.

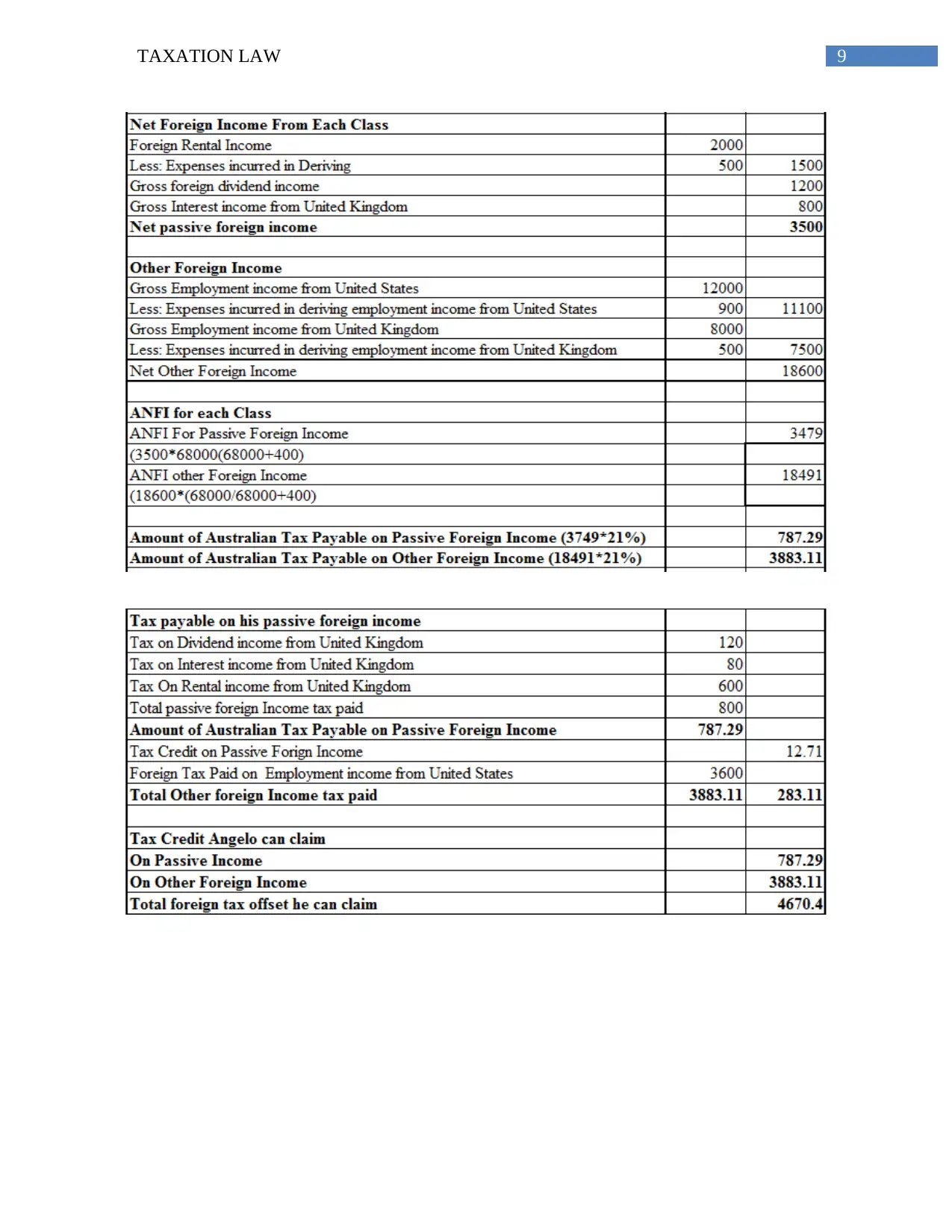

Answer 3:

9TAXATION LAW

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

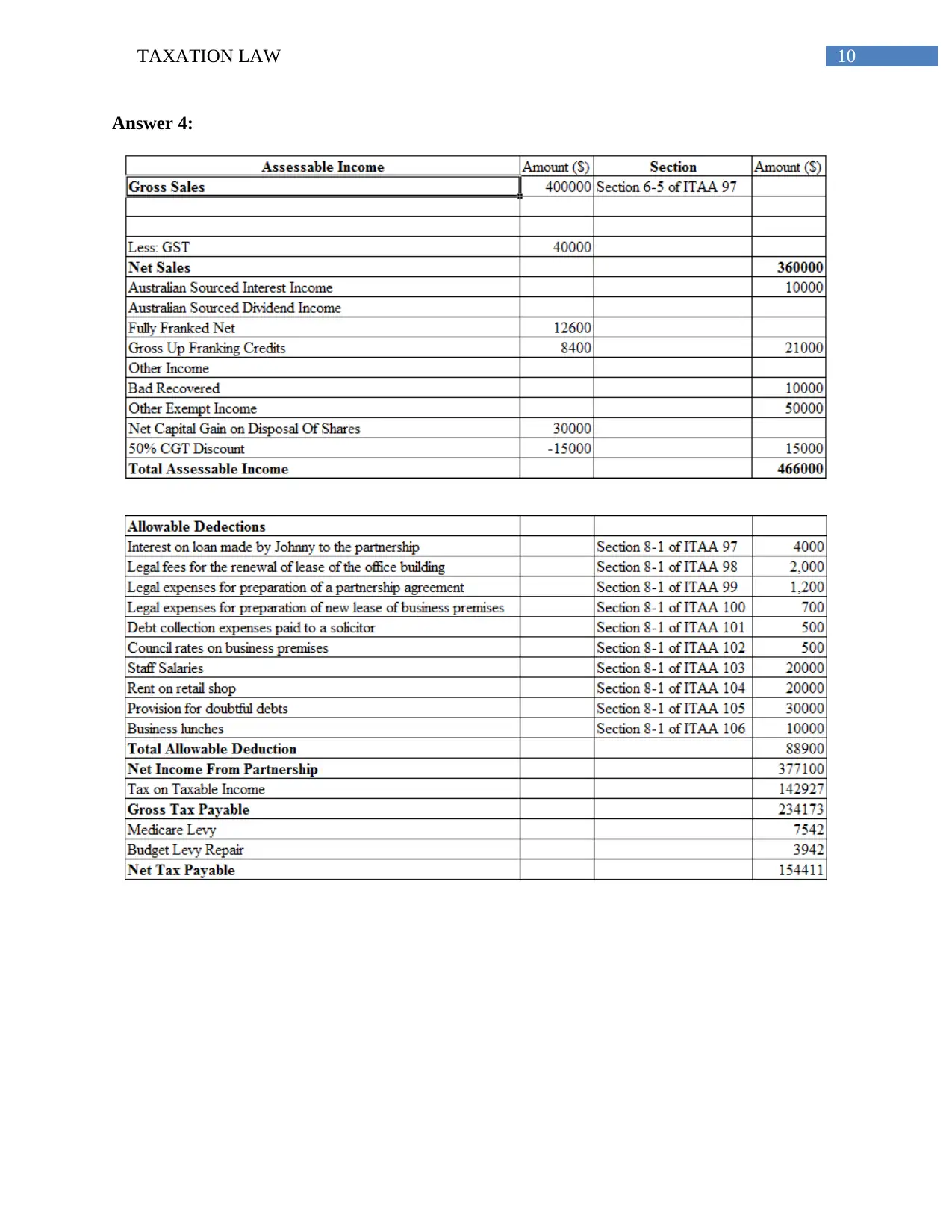

Answer 4:

Answer 4:

11TAXATION LAW

References:

Bodie, Z., 2013. Investments. McGraw-Hill.

Graetz, M.J. and Schenk, D.H., 2009. Federal Income Taxation: Principles and Policies.

Foundation Press.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Posner, R.A., 2014. Economic analysis of law. Wolters Kluwer Law & Business.

Reaves, B.A. and Bauer, L.M., 2012. Federal law enforcement officers, 2008. BiblioGov.

Scholes, M.S., 2015. Taxes and business strategy. Prentice Hall.

Zelenak, L., 2012. Custom and the Rule of Law in the Administration of the Income Tax. Duke

LJ, 62, p.829.

References:

Bodie, Z., 2013. Investments. McGraw-Hill.

Graetz, M.J. and Schenk, D.H., 2009. Federal Income Taxation: Principles and Policies.

Foundation Press.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Posner, R.A., 2014. Economic analysis of law. Wolters Kluwer Law & Business.

Reaves, B.A. and Bauer, L.M., 2012. Federal law enforcement officers, 2008. BiblioGov.

Scholes, M.S., 2015. Taxes and business strategy. Prentice Hall.

Zelenak, L., 2012. Custom and the Rule of Law in the Administration of the Income Tax. Duke

LJ, 62, p.829.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.