Taxation Law: Income Tax Return, Deductions, and FCT v Cooke Analysis

VerifiedAdded on 2023/04/23

|13

|2786

|457

Homework Assignment

AI Summary

This assignment solution covers two main areas of taxation law. The first part involves calculating Jane Herman's income tax liability, considering various income sources like salary, allowances, financial controller awards, taxation service fees, rental income, and dividends. It also addresses permissible deductions, including registration fees, travel expenses, salary paid to secretary, telephone and internet expenses, motor vehicle running expenses, council rates, insurance, property agent commission, repair and maintenance, water rates, capital work allowance, and donations. The second part analyzes the FCT v Cooke & Sherdon (1980) case, focusing on whether holiday schemes awarded to retailers constitute assessable income. The analysis involves examining relevant provisions of the Income Tax Assessment Act, including sections related to ordinary income, benefits provided by employers, and non-convertible benefits.

Taxation law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1: Income Tax Return of Jane Herman.......................................................................3

Provisions...............................................................................................................................3

Income tax calculations..........................................................................................................3

Working notes........................................................................................................................3

Question 2: FCT v Cooke & Sherdon (1980)............................................................................3

Issue........................................................................................................................................3

Provisions...............................................................................................................................3

Applicability...........................................................................................................................4

Conclusion..............................................................................................................................4

References..................................................................................................................................5

Question 1: Income Tax Return of Jane Herman.......................................................................3

Provisions...............................................................................................................................3

Income tax calculations..........................................................................................................3

Working notes........................................................................................................................3

Question 2: FCT v Cooke & Sherdon (1980)............................................................................3

Issue........................................................................................................................................3

Provisions...............................................................................................................................3

Applicability...........................................................................................................................4

Conclusion..............................................................................................................................4

References..................................................................................................................................5

QUESTION 1: INCOME TAX RETURN OF JANE HERMAN

Provisions

In the given study, Jane Herman is a chartered accountant and engages in the part time

working as a financial controller of hotels in Sydney. He along with the receiving salary from

the hotel also generate the income by carrying out the sole taxation practice.

Employment income refers as the earning derived from the employment. The person should

include all the income generated from the employment whether it is received in cash or in any

manner subject to some norms (Martins, 2018).

In the term salary and wages, commission, bonus, parental leave, payment received under the

work compensation scheme, money received under casual work etc. is included (Shields and

et.al, 2015). Along with this, if the employer provides any other payment in the course of the

employment and allowances such as travel, clothing, car, laundry, and payment for the

services then also it is included in the assessable income of the employee.

Further the person can also claim for the deduction of the expenses, if it is directly related

with the generation of the income. For claiming the deduction there must be some condition

which is to be fulfilled by the assesse, such as –

The money which is spent is not reimbursed by any other person.

It must be directly related with the income.

The person who claiming the deduction must have the record for the evidence.

Capital allowance related with motor car

If an individual makes use of own car in carrying out their work-associated duties inclusive

of a car leased or owned, then they might be capable to claim for a deduction for related

expenditures. Further, if an individual gains an allowance from their employer for car

expenditures then it is considered as an assessable income and the same must be comprised in

their tax return (Knechel & Salterio, 2016). Further the allowance amount is generally is

reflected in their payment details. One can select one of the two key methods for the

calculation of car expenditure deductions which are namely: cents per kilometer method and

logbook method.

Provisions

In the given study, Jane Herman is a chartered accountant and engages in the part time

working as a financial controller of hotels in Sydney. He along with the receiving salary from

the hotel also generate the income by carrying out the sole taxation practice.

Employment income refers as the earning derived from the employment. The person should

include all the income generated from the employment whether it is received in cash or in any

manner subject to some norms (Martins, 2018).

In the term salary and wages, commission, bonus, parental leave, payment received under the

work compensation scheme, money received under casual work etc. is included (Shields and

et.al, 2015). Along with this, if the employer provides any other payment in the course of the

employment and allowances such as travel, clothing, car, laundry, and payment for the

services then also it is included in the assessable income of the employee.

Further the person can also claim for the deduction of the expenses, if it is directly related

with the generation of the income. For claiming the deduction there must be some condition

which is to be fulfilled by the assesse, such as –

The money which is spent is not reimbursed by any other person.

It must be directly related with the income.

The person who claiming the deduction must have the record for the evidence.

Capital allowance related with motor car

If an individual makes use of own car in carrying out their work-associated duties inclusive

of a car leased or owned, then they might be capable to claim for a deduction for related

expenditures. Further, if an individual gains an allowance from their employer for car

expenditures then it is considered as an assessable income and the same must be comprised in

their tax return (Knechel & Salterio, 2016). Further the allowance amount is generally is

reflected in their payment details. One can select one of the two key methods for the

calculation of car expenditure deductions which are namely: cents per kilometer method and

logbook method.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

An individual can make claim for deductions for a work-related car expenditures if they make

use of their own car in conducting their job performance as an employee, such as carrying

bulky tools and equipment that their employee needs to use for operation, attending meetings,

delivering supplies, conducting itinerant work, traveling among two different employment

places and traveling from usual workplace to an optional workplace (Australian Taxation

Office, 2019).

Provisions related with the rental income

If an individual made investment in a rental property or rented their existing property, then

they will be required to retain records from the starting basis, while working out for expenses

then they need to claim for deduction, and must announce all their rental associated income in

their tax return (Paris, 2017). The taxpayer can make claim for deduction for their associated

expenditures for the period when the property is rented out or is accessible for rent, then

include the management as well as maintenance costs inclusive of all interest on loans can

often be claimed on an immediate basis i.e. deducted in opposition to their present income

year. Borrowed expenditures, spending of capital works and depreciation can be deducted

for several years.

Capital work allowance

Capital works are employed to generate income, inclusive of structural developments and

buildings are written off above a longer period as compared to other depreciating assets.

Further, the taxpayer can make claim for deduction for the overall costs of the assumption in

the year it took place. The deduction is calculated by 2.5% or 4% of the construction based

expense based on the time construction started and how the usage of capital works is done.

According to the ITAA 1997 Div 43, a person paying tax can claim for a deduction for

capital expense occurred in construction of capital works which are employed for income

generating purposes (Australian Taxation Office, 2019). Further, the construction must be

done prior when there is accessibility of deduction. The capital work deduction is accessible

for buildings, alterations, developments or extensions, structural improvement for example

sealed driveways and holding ways and earthworks for protection for environment like

embankments.

Provisions related with the dividend

use of their own car in conducting their job performance as an employee, such as carrying

bulky tools and equipment that their employee needs to use for operation, attending meetings,

delivering supplies, conducting itinerant work, traveling among two different employment

places and traveling from usual workplace to an optional workplace (Australian Taxation

Office, 2019).

Provisions related with the rental income

If an individual made investment in a rental property or rented their existing property, then

they will be required to retain records from the starting basis, while working out for expenses

then they need to claim for deduction, and must announce all their rental associated income in

their tax return (Paris, 2017). The taxpayer can make claim for deduction for their associated

expenditures for the period when the property is rented out or is accessible for rent, then

include the management as well as maintenance costs inclusive of all interest on loans can

often be claimed on an immediate basis i.e. deducted in opposition to their present income

year. Borrowed expenditures, spending of capital works and depreciation can be deducted

for several years.

Capital work allowance

Capital works are employed to generate income, inclusive of structural developments and

buildings are written off above a longer period as compared to other depreciating assets.

Further, the taxpayer can make claim for deduction for the overall costs of the assumption in

the year it took place. The deduction is calculated by 2.5% or 4% of the construction based

expense based on the time construction started and how the usage of capital works is done.

According to the ITAA 1997 Div 43, a person paying tax can claim for a deduction for

capital expense occurred in construction of capital works which are employed for income

generating purposes (Australian Taxation Office, 2019). Further, the construction must be

done prior when there is accessibility of deduction. The capital work deduction is accessible

for buildings, alterations, developments or extensions, structural improvement for example

sealed driveways and holding ways and earthworks for protection for environment like

embankments.

Provisions related with the dividend

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation on dividends are done on different based on if or if not the shareholder is an

Australian resident or non-resident.

Franked

The base of the system is that if the payment made by the company or credited by the

company with dividends which have been franked then the taxpayer might be subjected to a

franking tax balanced to the tax the corporate has been payable on its income (Swan, 2018).

Unfranked

A resident corporate might pay or credit the taxpayer with an unfranked dividend, there is no

presence of attached franking credit to these dividends. If a taxpayer derives an unfranked

dividend announced to be conduit foreign income on either their dividend or distribution

statement, comprise that amount being as unfranked dividend on the taxpayer’s tax return

(Australian Taxation Office, 2019).

Income tax calculations

Computation of the income tax payable by the Jane for the year ending

30June 2018

Particulars Amount in

$

Income

Salary received 50000

Allowance related with clothing 4500

Financial controller award

received in cash

5000

Financial controller award HP

computer

Australian resident or non-resident.

Franked

The base of the system is that if the payment made by the company or credited by the

company with dividends which have been franked then the taxpayer might be subjected to a

franking tax balanced to the tax the corporate has been payable on its income (Swan, 2018).

Unfranked

A resident corporate might pay or credit the taxpayer with an unfranked dividend, there is no

presence of attached franking credit to these dividends. If a taxpayer derives an unfranked

dividend announced to be conduit foreign income on either their dividend or distribution

statement, comprise that amount being as unfranked dividend on the taxpayer’s tax return

(Australian Taxation Office, 2019).

Income tax calculations

Computation of the income tax payable by the Jane for the year ending

30June 2018

Particulars Amount in

$

Income

Salary received 50000

Allowance related with clothing 4500

Financial controller award

received in cash

5000

Financial controller award HP

computer

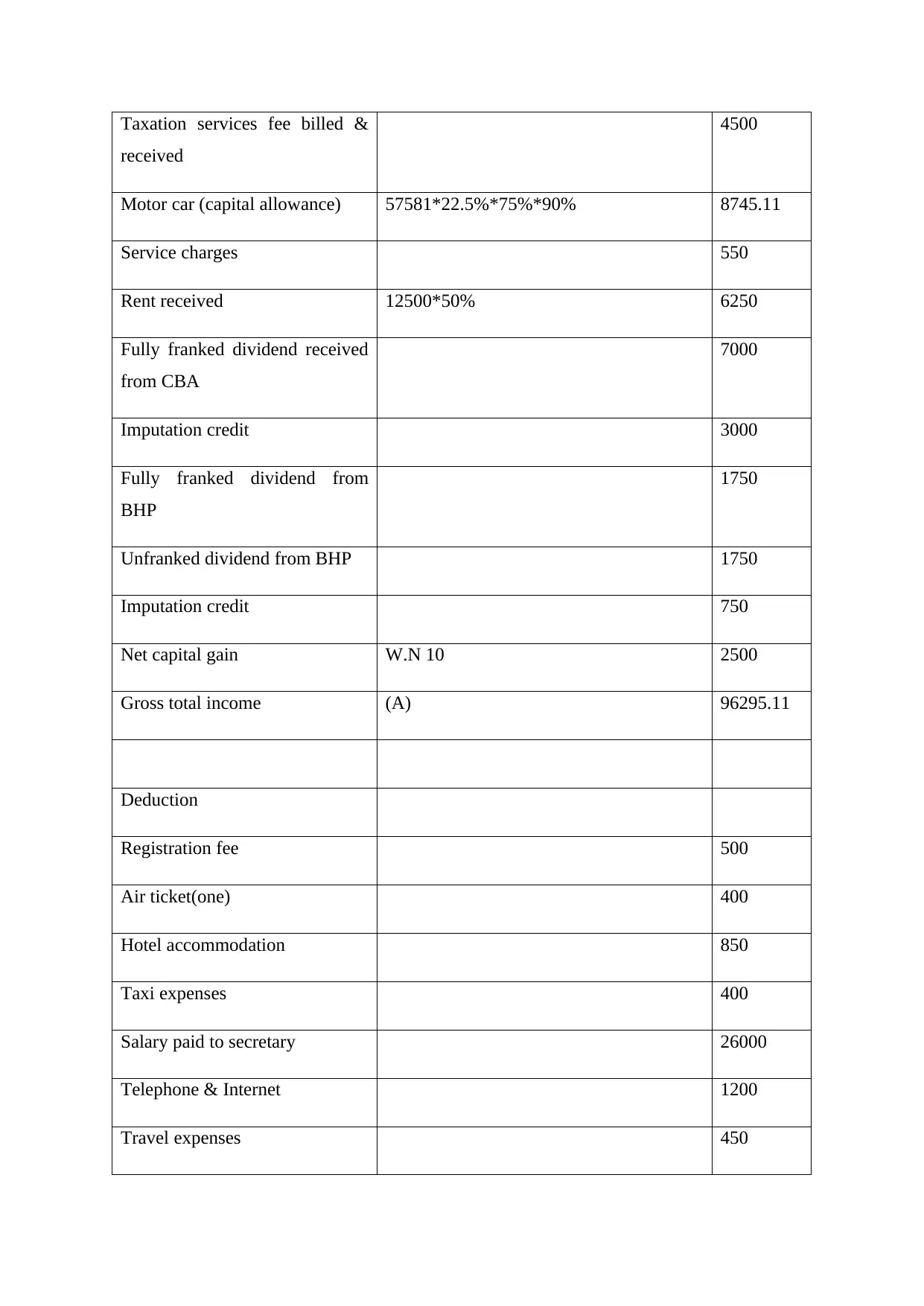

Taxation services fee billed &

received

4500

Motor car (capital allowance) 57581*22.5%*75%*90% 8745.11

Service charges 550

Rent received 12500*50% 6250

Fully franked dividend received

from CBA

7000

Imputation credit 3000

Fully franked dividend from

BHP

1750

Unfranked dividend from BHP 1750

Imputation credit 750

Net capital gain W.N 10 2500

Gross total income (A) 96295.11

Deduction

Registration fee 500

Air ticket(one) 400

Hotel accommodation 850

Taxi expenses 400

Salary paid to secretary 26000

Telephone & Internet 1200

Travel expenses 450

received

4500

Motor car (capital allowance) 57581*22.5%*75%*90% 8745.11

Service charges 550

Rent received 12500*50% 6250

Fully franked dividend received

from CBA

7000

Imputation credit 3000

Fully franked dividend from

BHP

1750

Unfranked dividend from BHP 1750

Imputation credit 750

Net capital gain W.N 10 2500

Gross total income (A) 96295.11

Deduction

Registration fee 500

Air ticket(one) 400

Hotel accommodation 850

Taxi expenses 400

Salary paid to secretary 26000

Telephone & Internet 1200

Travel expenses 450

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

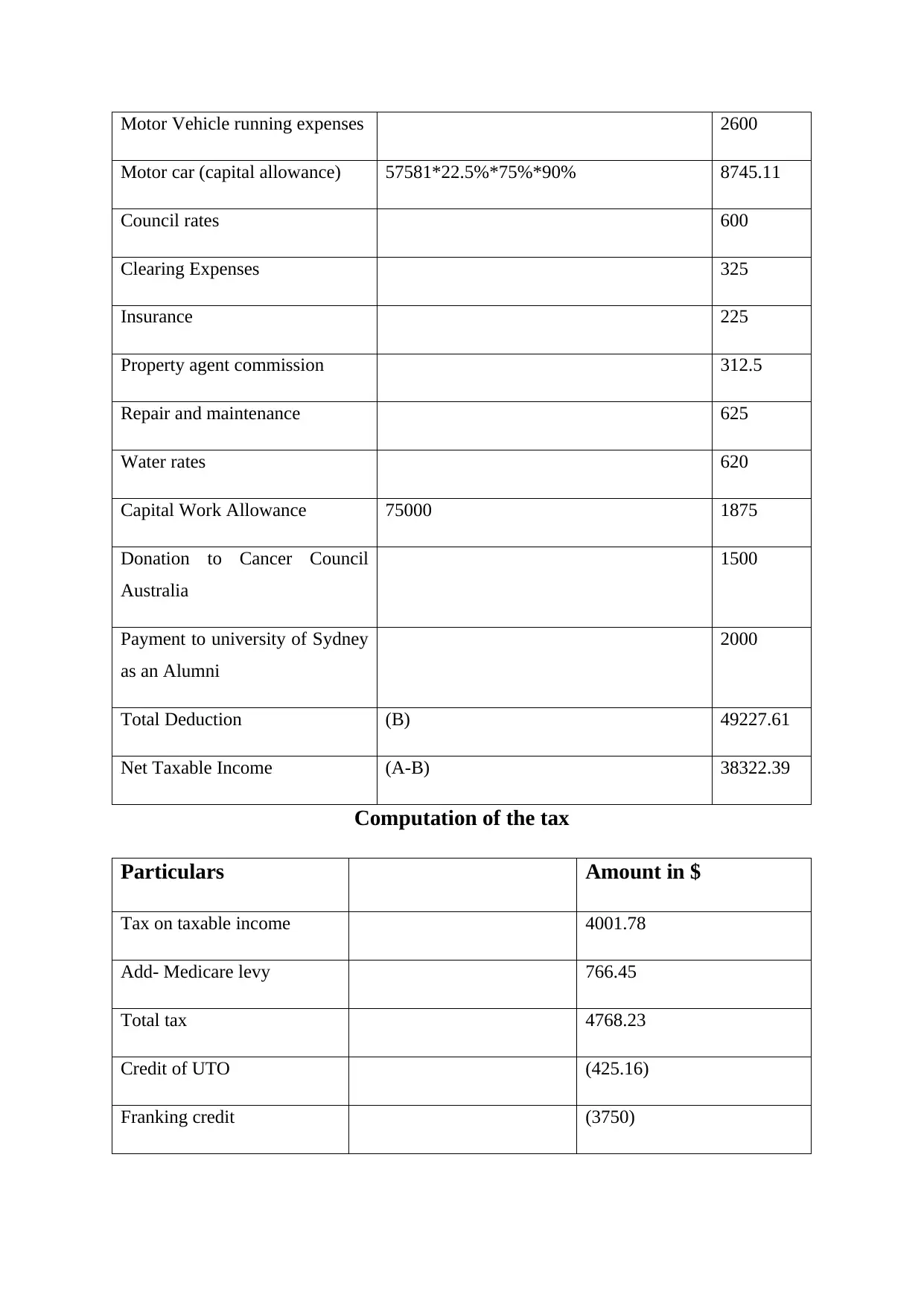

Motor Vehicle running expenses 2600

Motor car (capital allowance) 57581*22.5%*75%*90% 8745.11

Council rates 600

Clearing Expenses 325

Insurance 225

Property agent commission 312.5

Repair and maintenance 625

Water rates 620

Capital Work Allowance 75000 1875

Donation to Cancer Council

Australia

1500

Payment to university of Sydney

as an Alumni

2000

Total Deduction (B) 49227.61

Net Taxable Income (A-B) 38322.39

Computation of the tax

Particulars Amount in $

Tax on taxable income 4001.78

Add- Medicare levy 766.45

Total tax 4768.23

Credit of UTO (425.16)

Franking credit (3750)

Motor car (capital allowance) 57581*22.5%*75%*90% 8745.11

Council rates 600

Clearing Expenses 325

Insurance 225

Property agent commission 312.5

Repair and maintenance 625

Water rates 620

Capital Work Allowance 75000 1875

Donation to Cancer Council

Australia

1500

Payment to university of Sydney

as an Alumni

2000

Total Deduction (B) 49227.61

Net Taxable Income (A-B) 38322.39

Computation of the tax

Particulars Amount in $

Tax on taxable income 4001.78

Add- Medicare levy 766.45

Total tax 4768.23

Credit of UTO (425.16)

Franking credit (3750)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

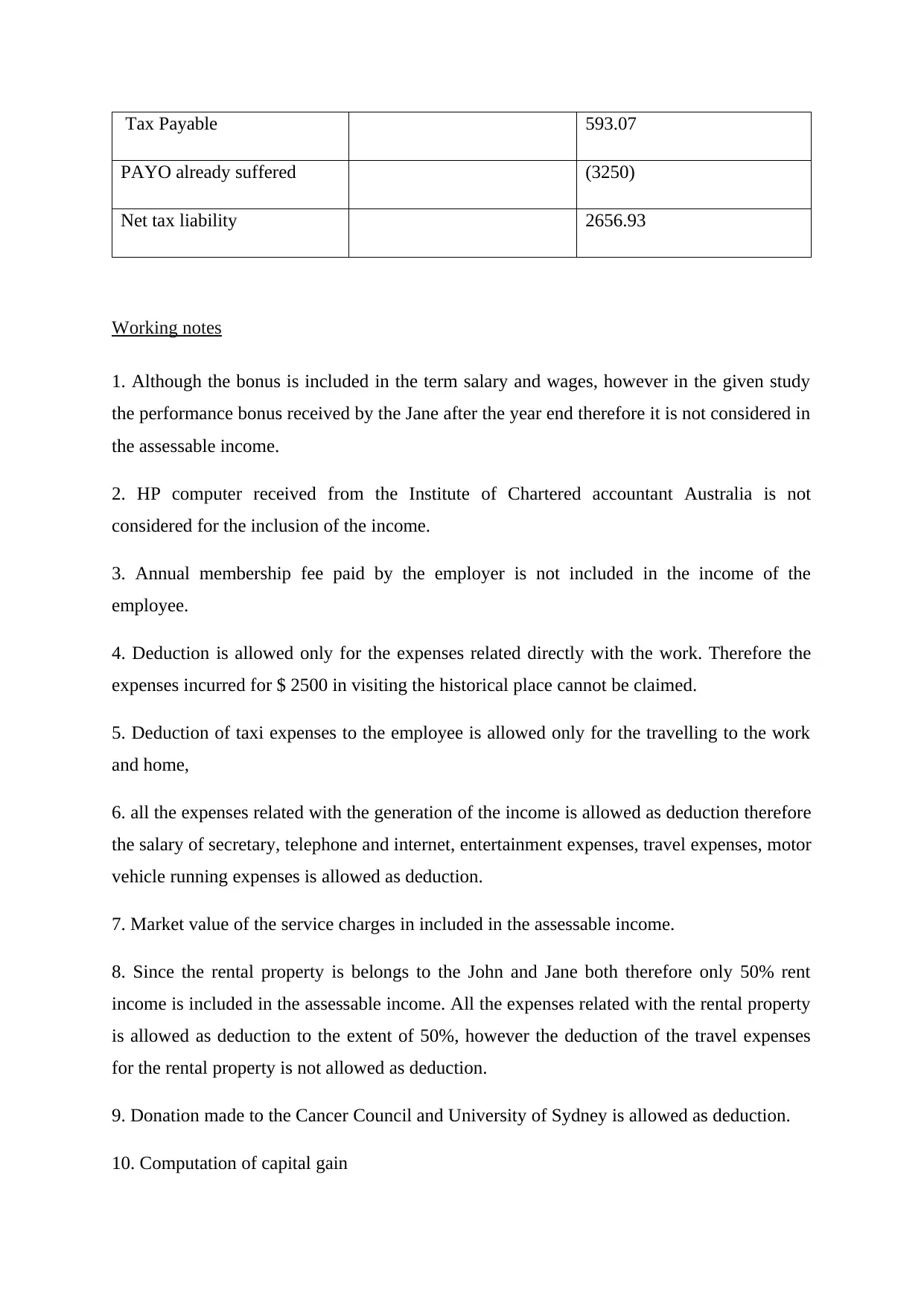

Tax Payable 593.07

PAYO already suffered (3250)

Net tax liability 2656.93

Working notes

1. Although the bonus is included in the term salary and wages, however in the given study

the performance bonus received by the Jane after the year end therefore it is not considered in

the assessable income.

2. HP computer received from the Institute of Chartered accountant Australia is not

considered for the inclusion of the income.

3. Annual membership fee paid by the employer is not included in the income of the

employee.

4. Deduction is allowed only for the expenses related directly with the work. Therefore the

expenses incurred for $ 2500 in visiting the historical place cannot be claimed.

5. Deduction of taxi expenses to the employee is allowed only for the travelling to the work

and home,

6. all the expenses related with the generation of the income is allowed as deduction therefore

the salary of secretary, telephone and internet, entertainment expenses, travel expenses, motor

vehicle running expenses is allowed as deduction.

7. Market value of the service charges in included in the assessable income.

8. Since the rental property is belongs to the John and Jane both therefore only 50% rent

income is included in the assessable income. All the expenses related with the rental property

is allowed as deduction to the extent of 50%, however the deduction of the travel expenses

for the rental property is not allowed as deduction.

9. Donation made to the Cancer Council and University of Sydney is allowed as deduction.

10. Computation of capital gain

PAYO already suffered (3250)

Net tax liability 2656.93

Working notes

1. Although the bonus is included in the term salary and wages, however in the given study

the performance bonus received by the Jane after the year end therefore it is not considered in

the assessable income.

2. HP computer received from the Institute of Chartered accountant Australia is not

considered for the inclusion of the income.

3. Annual membership fee paid by the employer is not included in the income of the

employee.

4. Deduction is allowed only for the expenses related directly with the work. Therefore the

expenses incurred for $ 2500 in visiting the historical place cannot be claimed.

5. Deduction of taxi expenses to the employee is allowed only for the travelling to the work

and home,

6. all the expenses related with the generation of the income is allowed as deduction therefore

the salary of secretary, telephone and internet, entertainment expenses, travel expenses, motor

vehicle running expenses is allowed as deduction.

7. Market value of the service charges in included in the assessable income.

8. Since the rental property is belongs to the John and Jane both therefore only 50% rent

income is included in the assessable income. All the expenses related with the rental property

is allowed as deduction to the extent of 50%, however the deduction of the travel expenses

for the rental property is not allowed as deduction.

9. Donation made to the Cancer Council and University of Sydney is allowed as deduction.

10. Computation of capital gain

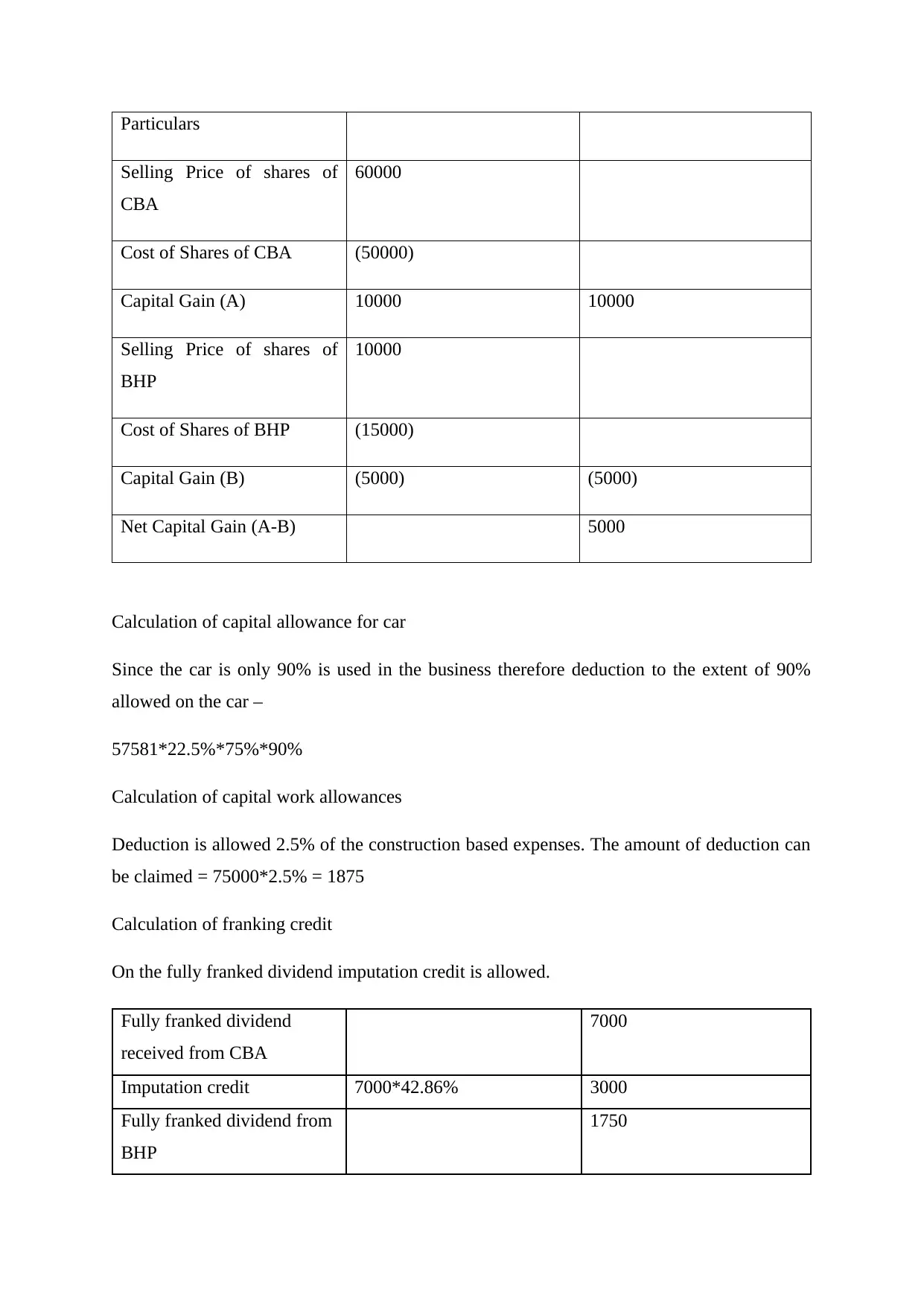

Particulars

Selling Price of shares of

CBA

60000

Cost of Shares of CBA (50000)

Capital Gain (A) 10000 10000

Selling Price of shares of

BHP

10000

Cost of Shares of BHP (15000)

Capital Gain (B) (5000) (5000)

Net Capital Gain (A-B) 5000

Calculation of capital allowance for car

Since the car is only 90% is used in the business therefore deduction to the extent of 90%

allowed on the car –

57581*22.5%*75%*90%

Calculation of capital work allowances

Deduction is allowed 2.5% of the construction based expenses. The amount of deduction can

be claimed = 75000*2.5% = 1875

Calculation of franking credit

On the fully franked dividend imputation credit is allowed.

Fully franked dividend

received from CBA

7000

Imputation credit 7000*42.86% 3000

Fully franked dividend from

BHP

1750

Selling Price of shares of

CBA

60000

Cost of Shares of CBA (50000)

Capital Gain (A) 10000 10000

Selling Price of shares of

BHP

10000

Cost of Shares of BHP (15000)

Capital Gain (B) (5000) (5000)

Net Capital Gain (A-B) 5000

Calculation of capital allowance for car

Since the car is only 90% is used in the business therefore deduction to the extent of 90%

allowed on the car –

57581*22.5%*75%*90%

Calculation of capital work allowances

Deduction is allowed 2.5% of the construction based expenses. The amount of deduction can

be claimed = 75000*2.5% = 1875

Calculation of franking credit

On the fully franked dividend imputation credit is allowed.

Fully franked dividend

received from CBA

7000

Imputation credit 7000*42.86% 3000

Fully franked dividend from

BHP

1750

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Imputation credit 1750*42.86% 750

QUESTION 2: FCT V COOKE & SHERDON (1980)

Issue

The present case is related with the determination of the ordinary income. In this case the

producer of the soft drinks is awarding the holiday scheme to its retailers. The reason behind

the allocation of the holiday scheme is to identify the efforts of the retailers who complete

their allotted criteria of the sales recognition. In this scheme the cost of the travelling and

fairs paid by the manufacturer (Wolters Kluwer, 2018). However the scheme is provided as

per the wish of the manufacture and it cannot be transferred to any other person, further no

cash in awarded in respect of the scheme. If the payment of specified number of bottles is

paid by the retailer to the manufacture then the manufacture give the award of holiday

scheme to the retailer. The issue is whether the award of the holiday scheme made to the

retailer, the value of the fares and accommodation which is paid by the manufacture is

included in the assessable income of the each retailer under section 21, 25(1) and 26(e).

Provisions

According to the section 6(1) of the Income Tax Assessment Act 1997, the tax is charged on

the income derived from the ordinary course of the business and on some income which is

specifically defined under the act (Lee, 2018).

Section 26(e) states that value to the taxpayer includes all benefits, bonuses, allowances,

gratuities, premiums which are provided by the employer, directly or indirectly in the course

of the employment or services provided by him (Buchanan & Consett, 2016).

Section 25(1) states that income includes any benefit even if it is not convertible into money;

it is depended on some facts. If the inconvertible benefits in the hands to recipients is related

with the goods and services which is normally required by the person in the ordinary course

of his/her life for the maintenance or ease for themselves or their dependent, so that it is

possible to benefit received by the person is recurring by which he would satisfy his

requirement, then it could be included in the income of the assesse (Burton, 2018).

Section 21 is applicable after determining the assessable income of the assesse.

QUESTION 2: FCT V COOKE & SHERDON (1980)

Issue

The present case is related with the determination of the ordinary income. In this case the

producer of the soft drinks is awarding the holiday scheme to its retailers. The reason behind

the allocation of the holiday scheme is to identify the efforts of the retailers who complete

their allotted criteria of the sales recognition. In this scheme the cost of the travelling and

fairs paid by the manufacturer (Wolters Kluwer, 2018). However the scheme is provided as

per the wish of the manufacture and it cannot be transferred to any other person, further no

cash in awarded in respect of the scheme. If the payment of specified number of bottles is

paid by the retailer to the manufacture then the manufacture give the award of holiday

scheme to the retailer. The issue is whether the award of the holiday scheme made to the

retailer, the value of the fares and accommodation which is paid by the manufacture is

included in the assessable income of the each retailer under section 21, 25(1) and 26(e).

Provisions

According to the section 6(1) of the Income Tax Assessment Act 1997, the tax is charged on

the income derived from the ordinary course of the business and on some income which is

specifically defined under the act (Lee, 2018).

Section 26(e) states that value to the taxpayer includes all benefits, bonuses, allowances,

gratuities, premiums which are provided by the employer, directly or indirectly in the course

of the employment or services provided by him (Buchanan & Consett, 2016).

Section 25(1) states that income includes any benefit even if it is not convertible into money;

it is depended on some facts. If the inconvertible benefits in the hands to recipients is related

with the goods and services which is normally required by the person in the ordinary course

of his/her life for the maintenance or ease for themselves or their dependent, so that it is

possible to benefit received by the person is recurring by which he would satisfy his

requirement, then it could be included in the income of the assesse (Burton, 2018).

Section 21 is applicable after determining the assessable income of the assesse.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Applicability

On the basis of the above provision it has been seen that, according to the section26 (e), it is

compulsory that benefit must be provided for the services rendered. However in the given

case, the manufacture only made the promise to retailers to sell the goods to them in

exchange of promises made by the retailer to sell those goods in a specified area. In this case,

there is no award given by the manufacture for the work of the retailer of selling the goods to

consumer. There is no promise to sell the goods to the retailer and for the performance of the

promise there is not any sale by the manufacture.

Further the requirement of the section 25(1) is also not satisfied because the holiday scheme

cannot be regarded as the expenditure which is required by the person for satisfying their

essential needs. As per the section 25(1), for considering the non-convertible benefits in the

meaning of income it is compulsory that the expenses reimburse by any other person must be

in the nature by which the requirement of the ordinary person or his dependent would be

satisfies. Therefore the section25 (1) is not applicable in the given case (Wolters Kluwer,

2018).

Moreover section 21 is applicable only after the assessable income determined; therefore it is

also not applicable in the given case.

Conclusion

It has been concluded that in the case of FCT v Cooke and Sherden, the value of holiday

scheme provided to the retailer is not considered as the ordinary income therefore not

included in the assessable income.

On the basis of the above provision it has been seen that, according to the section26 (e), it is

compulsory that benefit must be provided for the services rendered. However in the given

case, the manufacture only made the promise to retailers to sell the goods to them in

exchange of promises made by the retailer to sell those goods in a specified area. In this case,

there is no award given by the manufacture for the work of the retailer of selling the goods to

consumer. There is no promise to sell the goods to the retailer and for the performance of the

promise there is not any sale by the manufacture.

Further the requirement of the section 25(1) is also not satisfied because the holiday scheme

cannot be regarded as the expenditure which is required by the person for satisfying their

essential needs. As per the section 25(1), for considering the non-convertible benefits in the

meaning of income it is compulsory that the expenses reimburse by any other person must be

in the nature by which the requirement of the ordinary person or his dependent would be

satisfies. Therefore the section25 (1) is not applicable in the given case (Wolters Kluwer,

2018).

Moreover section 21 is applicable only after the assessable income determined; therefore it is

also not applicable in the given case.

Conclusion

It has been concluded that in the case of FCT v Cooke and Sherden, the value of holiday

scheme provided to the retailer is not considered as the ordinary income therefore not

included in the assessable income.

REFERENCES

Australian Taxation Office, (2019). Car expenses. Retrieved from

<https://www.ato.gov.au/individuals/income-and-deductions/deductions-you-can-

claim/vehicle-and-travel-expenses/car-expenses/#Calculating_your_deduction>.

Australian Taxation Office, (2019). Depreciation and capital expenses and allowances.

Retrieved from < https://www.ato.gov.au/business/depreciation-and-capital-expenses-

and-allowances/>.

Australian Taxation Office, (2019). Paying dividends and other distributions. Retrieved from

< https://www.ato.gov.au/business/imputation/paying-dividends-and-other-

distributions/>.

Buchanan, R., & Consett, E. (2016). Section 974-80 ITAA97: The current state of play. Tax

Specialist, 19(5), 217.

Burton, M. (2018). Interpreting the Australian Income Tax Definition of Ordinary Income:

Ritual Incantation Or Analysis, When Examined through the Lens of Early Twentieth

Century Linguistic Philosophy. eJTR, 16, 2.

Jones, D. (2018). Complexity of tax residency attracts review. Taxation in Australia, 53(6),

296.

Knechel, W. R., & Salterio, S. E. (2016). Taxation: Assurance and risk. Routledge.

Lee, J. (2018). The Effectiveness of Part IVA of the Income Tax Assessment Act 1936

(CTH): Time for a Not Merely Incidental'Purpose Test. J. Austl. Tax'n, 20, 1.

Martins, P. (2018). TD 2017/20. Taxation in Australia, 52(10), 562.

Paris, C. (2017). Housing Australia. Macmillan International Higher Education.

Shields, J., Brown, M., Kaine, S., Dolle-Samuel, C., North-Samardzic, A., McLean, P., ... &

Plimmer, G. (2015). Managing employee performance & reward: Concepts,

practices, strategies. Cambridge University Press.

Swan, P. L. (2018). Investment, the Corporate Tax Rate, and the Pricing of Franking Credits.

Australian Taxation Office, (2019). Car expenses. Retrieved from

<https://www.ato.gov.au/individuals/income-and-deductions/deductions-you-can-

claim/vehicle-and-travel-expenses/car-expenses/#Calculating_your_deduction>.

Australian Taxation Office, (2019). Depreciation and capital expenses and allowances.

Retrieved from < https://www.ato.gov.au/business/depreciation-and-capital-expenses-

and-allowances/>.

Australian Taxation Office, (2019). Paying dividends and other distributions. Retrieved from

< https://www.ato.gov.au/business/imputation/paying-dividends-and-other-

distributions/>.

Buchanan, R., & Consett, E. (2016). Section 974-80 ITAA97: The current state of play. Tax

Specialist, 19(5), 217.

Burton, M. (2018). Interpreting the Australian Income Tax Definition of Ordinary Income:

Ritual Incantation Or Analysis, When Examined through the Lens of Early Twentieth

Century Linguistic Philosophy. eJTR, 16, 2.

Jones, D. (2018). Complexity of tax residency attracts review. Taxation in Australia, 53(6),

296.

Knechel, W. R., & Salterio, S. E. (2016). Taxation: Assurance and risk. Routledge.

Lee, J. (2018). The Effectiveness of Part IVA of the Income Tax Assessment Act 1936

(CTH): Time for a Not Merely Incidental'Purpose Test. J. Austl. Tax'n, 20, 1.

Martins, P. (2018). TD 2017/20. Taxation in Australia, 52(10), 562.

Paris, C. (2017). Housing Australia. Macmillan International Higher Education.

Shields, J., Brown, M., Kaine, S., Dolle-Samuel, C., North-Samardzic, A., McLean, P., ... &

Plimmer, G. (2015). Managing employee performance & reward: Concepts,

practices, strategies. Cambridge University Press.

Swan, P. L. (2018). Investment, the Corporate Tax Rate, and the Pricing of Franking Credits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.