Indirect Tax: VAT Report - Comprehensive Analysis and Assessment

VerifiedAdded on 2021/01/01

|14

|4014

|480

Report

AI Summary

This report provides a comprehensive overview of Value Added Tax (VAT) in the UK, exploring its significance as a major source of government revenue. It delves into various aspects of VAT, including sources of information like purchase and sales registers, the role of government agencies such as HMRC, and VAT registration requirements. The report outlines the information required on business documents, different VAT schemes like annual accounting and flat-rate schemes, and the importance of staying updated with changes in regulations. Furthermore, it demonstrates the extraction and calculation of VAT for a specific accounting period, covering inputs, outputs, and the calculation of VAT due. The report also addresses the implications of non-compliance with VAT regulations and the communication of VAT-related information to management, offering advice on the impact of VAT payments on cash flow and financial forecasts. Overall, this report serves as a detailed guide to understanding and managing VAT compliance.

Indirect tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of VAT information.................................................................................................1

1.2 The way in which an organisation should interact with the relevant government agency....2

1.3 VAT registration requirements..............................................................................................2

1.4 Information that must be included on business documents of VAT registered businesses...3

1.5 Requirements and frequency of reporting for VAT schemes................................................3

1.6 Maintaining an up-to-date knowledge of changes to code of practice, regulation or

legislation.....................................................................................................................................4

TASK 2............................................................................................................................................4

2.1 Extraction of relevant data for a specific period of accounting period..................................4

2.2 Calculation of relevant inputs and outputs.............................................................................5

2.3 Calculation of the VAT due to or from the relevant tax authority.........................................7

2.4 VAT Return with associated payment within the statutory time limits.................................7

TASK 3............................................................................................................................................8

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations....................................................................................................................................8

3.2 Adjustments and declarations for any errors or omission identified in previous VAT period

......................................................................................................................................................9

TASK 4............................................................................................................................................9

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts.........................................................................................................9

4.2 Advise for changes in VAT legislation which would have an effect on an organisation’s

recording systems.......................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of VAT information.................................................................................................1

1.2 The way in which an organisation should interact with the relevant government agency....2

1.3 VAT registration requirements..............................................................................................2

1.4 Information that must be included on business documents of VAT registered businesses...3

1.5 Requirements and frequency of reporting for VAT schemes................................................3

1.6 Maintaining an up-to-date knowledge of changes to code of practice, regulation or

legislation.....................................................................................................................................4

TASK 2............................................................................................................................................4

2.1 Extraction of relevant data for a specific period of accounting period..................................4

2.2 Calculation of relevant inputs and outputs.............................................................................5

2.3 Calculation of the VAT due to or from the relevant tax authority.........................................7

2.4 VAT Return with associated payment within the statutory time limits.................................7

TASK 3............................................................................................................................................8

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations....................................................................................................................................8

3.2 Adjustments and declarations for any errors or omission identified in previous VAT period

......................................................................................................................................................9

TASK 4............................................................................................................................................9

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts.........................................................................................................9

4.2 Advise for changes in VAT legislation which would have an effect on an organisation’s

recording systems.......................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Indirect tax is one of the major source of revenue for government in UK. Indirect Tax

refers to Indirect tax refers to tax on on consumable products not directly levied on income or

property such as excise duties, custom duties, value added tax etc. Ultimate consumer of goods

or services bears burden of indirect tax. Indirect tax leads to an significant increase in the price of

goods and products for the consumers (Adema, Fron and Ladaique, 2014). In all indirect taxes

VAT is most important due to various implications and procedures. In UK, value added tax is

largest source of government revenue among all indirect taxes. In UK, VAT is paid by retailers,

whole-sellers or other intermediaries to government but consumers are ultimate bearer of tax.

This report exhibits a complete understanding of VAT while covering various aspects like

sources of information under VAT, registration requirements, information required for business

documentation and other VAT related compliances. In this report all regulations concerned with

VAT, accurate and timely VAT return , VAT implications and penalties and communication of

VAT information is discussed.

TASK 1

1.1 Sources of VAT information

VAT is mainly associated with goods and consumable products. VAT is levied on a

product as the value is added at different stages of the supply chain, from production to retail

sale. For intermediaries like whole-sellers, retailers and other relevant intermediaries, sources of

information for VAT calculation are purchase register, sales registers, credit notes, debit notes,

inventory registers and other manual register related with selling and purchasing activities. In

case of sales return a credit note is used which helps organisation to adjust VAT input and output

and also a Debit note is used for purchase return (Bargain and et.al., 2015). As a good practice in

order to classify and mange value added tax for various products, an inventory register is

maintained by business organisations. Some entity for simplification of process of VAT

calculation maintains a memorandum VAT register in which input credits and input credits

availed are recorded by entities which also helps to avoid any error or difficulties. Therefore in

order to calculate VAT amount payable, consideration of purchase register, sales registers, credit

notes, debit notes, inventory registers and other manual register related with selling and

purchasing activities are necessary. All of these are major sources on VAT information.

Indirect tax is one of the major source of revenue for government in UK. Indirect Tax

refers to Indirect tax refers to tax on on consumable products not directly levied on income or

property such as excise duties, custom duties, value added tax etc. Ultimate consumer of goods

or services bears burden of indirect tax. Indirect tax leads to an significant increase in the price of

goods and products for the consumers (Adema, Fron and Ladaique, 2014). In all indirect taxes

VAT is most important due to various implications and procedures. In UK, value added tax is

largest source of government revenue among all indirect taxes. In UK, VAT is paid by retailers,

whole-sellers or other intermediaries to government but consumers are ultimate bearer of tax.

This report exhibits a complete understanding of VAT while covering various aspects like

sources of information under VAT, registration requirements, information required for business

documentation and other VAT related compliances. In this report all regulations concerned with

VAT, accurate and timely VAT return , VAT implications and penalties and communication of

VAT information is discussed.

TASK 1

1.1 Sources of VAT information

VAT is mainly associated with goods and consumable products. VAT is levied on a

product as the value is added at different stages of the supply chain, from production to retail

sale. For intermediaries like whole-sellers, retailers and other relevant intermediaries, sources of

information for VAT calculation are purchase register, sales registers, credit notes, debit notes,

inventory registers and other manual register related with selling and purchasing activities. In

case of sales return a credit note is used which helps organisation to adjust VAT input and output

and also a Debit note is used for purchase return (Bargain and et.al., 2015). As a good practice in

order to classify and mange value added tax for various products, an inventory register is

maintained by business organisations. Some entity for simplification of process of VAT

calculation maintains a memorandum VAT register in which input credits and input credits

availed are recorded by entities which also helps to avoid any error or difficulties. Therefore in

order to calculate VAT amount payable, consideration of purchase register, sales registers, credit

notes, debit notes, inventory registers and other manual register related with selling and

purchasing activities are necessary. All of these are major sources on VAT information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.2 The way in which an organisation should interact with the relevant government agency

For proper compliance of rules and regulations, an regulatory authority some times

known as government agency, is established by government for particular field and such relevant

government agency ensures proper compliance of rules and regulations (Duclos and Makdissi,

2014). Under UK's tax regulatory system HMRC act as government agency which regulates the

compliance of indirect taxes. HMRC act as intermediary between government and business

organisations. Beside HMRC there are many councils and units which acts as intermediaries.

These agencies provides various online and offline services to taxpayers and also provides some

experts to solve difficulties related with indirect taxes.

1.3 VAT registration requirements

In UK registration of VAT registration is compulsory for organisations having total

turnover exceeding £85,000 however an organisation can register voluntarily if turnover is less

than above threshold limit. In case of distance-selling this limit is £70000. The turnover

mentioned in threshold is VAT taxable turnover that incudes total amount of products or goods

sold which is not exempt under VAT (Tagkalakis, 2014). Here Distance selling refers to selling

of goods by registered business of one European Union country sells goods to other country in

European Union. Following are the major documents required for VAT registration, as follows -

Relevant documents related with incorporation such as Certificate of incorporation, Firm

registration certificate.

National Insurance (NI) number

Specific Tax identifier code i.e. Unique Taxpayer's reference (UTR) number

Details related to Business banks

Information of associated businesses within last two years

After registration of business under VAT, a certificate indicating unique VAT

registration is provided to business organisation. For Companies, doing business within UK but

not having any registered office in UK; registration under VAT is necessary. Insurance and

education business are not required to registered under VAT because such business sell goods or

services that are exempt from VAT.

For proper compliance of rules and regulations, an regulatory authority some times

known as government agency, is established by government for particular field and such relevant

government agency ensures proper compliance of rules and regulations (Duclos and Makdissi,

2014). Under UK's tax regulatory system HMRC act as government agency which regulates the

compliance of indirect taxes. HMRC act as intermediary between government and business

organisations. Beside HMRC there are many councils and units which acts as intermediaries.

These agencies provides various online and offline services to taxpayers and also provides some

experts to solve difficulties related with indirect taxes.

1.3 VAT registration requirements

In UK registration of VAT registration is compulsory for organisations having total

turnover exceeding £85,000 however an organisation can register voluntarily if turnover is less

than above threshold limit. In case of distance-selling this limit is £70000. The turnover

mentioned in threshold is VAT taxable turnover that incudes total amount of products or goods

sold which is not exempt under VAT (Tagkalakis, 2014). Here Distance selling refers to selling

of goods by registered business of one European Union country sells goods to other country in

European Union. Following are the major documents required for VAT registration, as follows -

Relevant documents related with incorporation such as Certificate of incorporation, Firm

registration certificate.

National Insurance (NI) number

Specific Tax identifier code i.e. Unique Taxpayer's reference (UTR) number

Details related to Business banks

Information of associated businesses within last two years

After registration of business under VAT, a certificate indicating unique VAT

registration is provided to business organisation. For Companies, doing business within UK but

not having any registered office in UK; registration under VAT is necessary. Insurance and

education business are not required to registered under VAT because such business sell goods or

services that are exempt from VAT.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

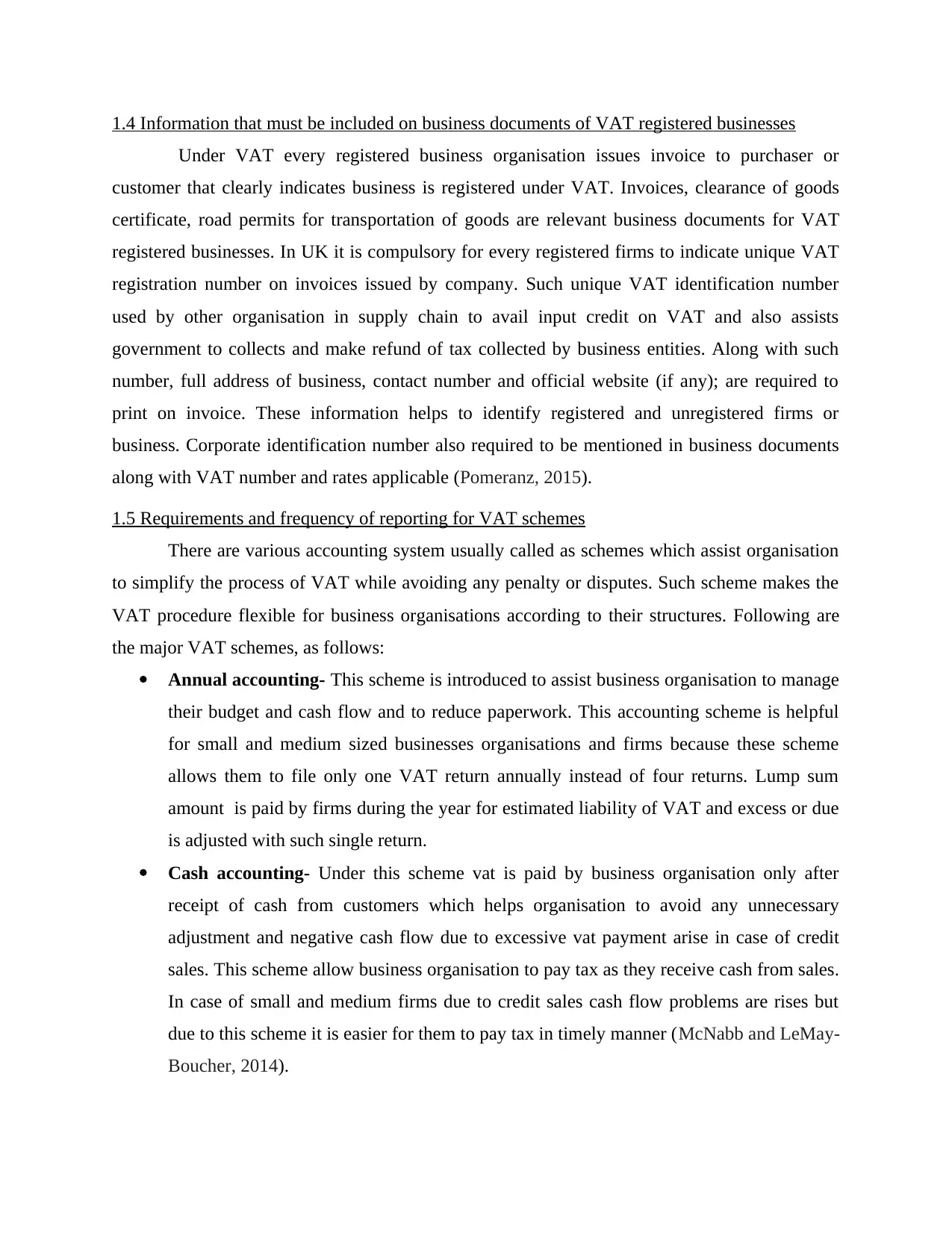

1.4 Information that must be included on business documents of VAT registered businesses

Under VAT every registered business organisation issues invoice to purchaser or

customer that clearly indicates business is registered under VAT. Invoices, clearance of goods

certificate, road permits for transportation of goods are relevant business documents for VAT

registered businesses. In UK it is compulsory for every registered firms to indicate unique VAT

registration number on invoices issued by company. Such unique VAT identification number

used by other organisation in supply chain to avail input credit on VAT and also assists

government to collects and make refund of tax collected by business entities. Along with such

number, full address of business, contact number and official website (if any); are required to

print on invoice. These information helps to identify registered and unregistered firms or

business. Corporate identification number also required to be mentioned in business documents

along with VAT number and rates applicable (Pomeranz, 2015).

1.5 Requirements and frequency of reporting for VAT schemes

There are various accounting system usually called as schemes which assist organisation

to simplify the process of VAT while avoiding any penalty or disputes. Such scheme makes the

VAT procedure flexible for business organisations according to their structures. Following are

the major VAT schemes, as follows:

Annual accounting- This scheme is introduced to assist business organisation to manage

their budget and cash flow and to reduce paperwork. This accounting scheme is helpful

for small and medium sized businesses organisations and firms because these scheme

allows them to file only one VAT return annually instead of four returns. Lump sum

amount is paid by firms during the year for estimated liability of VAT and excess or due

is adjusted with such single return.

Cash accounting- Under this scheme vat is paid by business organisation only after

receipt of cash from customers which helps organisation to avoid any unnecessary

adjustment and negative cash flow due to excessive vat payment arise in case of credit

sales. This scheme allow business organisation to pay tax as they receive cash from sales.

In case of small and medium firms due to credit sales cash flow problems are rises but

due to this scheme it is easier for them to pay tax in timely manner (McNabb and LeMay-

Boucher, 2014).

Under VAT every registered business organisation issues invoice to purchaser or

customer that clearly indicates business is registered under VAT. Invoices, clearance of goods

certificate, road permits for transportation of goods are relevant business documents for VAT

registered businesses. In UK it is compulsory for every registered firms to indicate unique VAT

registration number on invoices issued by company. Such unique VAT identification number

used by other organisation in supply chain to avail input credit on VAT and also assists

government to collects and make refund of tax collected by business entities. Along with such

number, full address of business, contact number and official website (if any); are required to

print on invoice. These information helps to identify registered and unregistered firms or

business. Corporate identification number also required to be mentioned in business documents

along with VAT number and rates applicable (Pomeranz, 2015).

1.5 Requirements and frequency of reporting for VAT schemes

There are various accounting system usually called as schemes which assist organisation

to simplify the process of VAT while avoiding any penalty or disputes. Such scheme makes the

VAT procedure flexible for business organisations according to their structures. Following are

the major VAT schemes, as follows:

Annual accounting- This scheme is introduced to assist business organisation to manage

their budget and cash flow and to reduce paperwork. This accounting scheme is helpful

for small and medium sized businesses organisations and firms because these scheme

allows them to file only one VAT return annually instead of four returns. Lump sum

amount is paid by firms during the year for estimated liability of VAT and excess or due

is adjusted with such single return.

Cash accounting- Under this scheme vat is paid by business organisation only after

receipt of cash from customers which helps organisation to avoid any unnecessary

adjustment and negative cash flow due to excessive vat payment arise in case of credit

sales. This scheme allow business organisation to pay tax as they receive cash from sales.

In case of small and medium firms due to credit sales cash flow problems are rises but

due to this scheme it is easier for them to pay tax in timely manner (McNabb and LeMay-

Boucher, 2014).

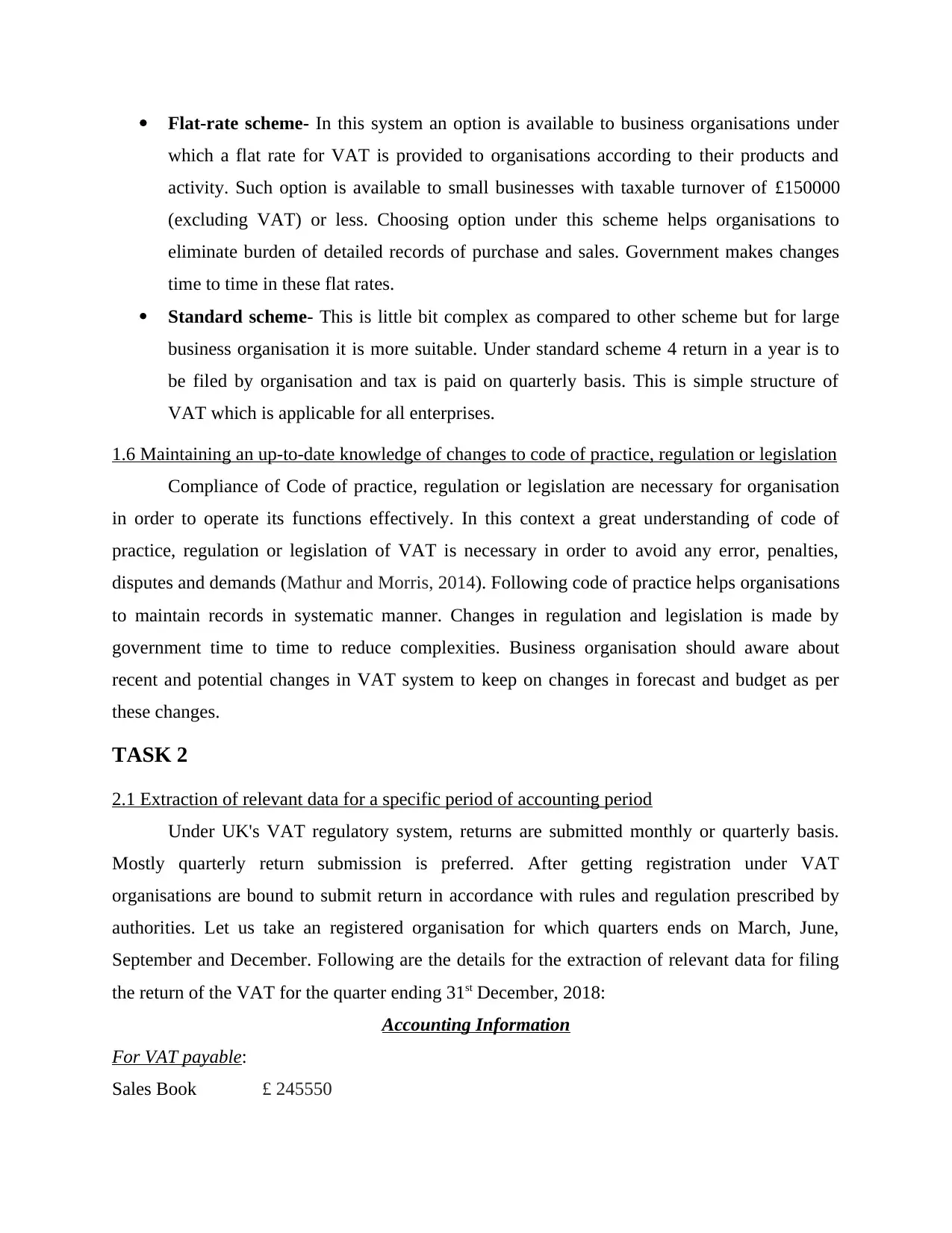

Flat-rate scheme- In this system an option is available to business organisations under

which a flat rate for VAT is provided to organisations according to their products and

activity. Such option is available to small businesses with taxable turnover of £150000

(excluding VAT) or less. Choosing option under this scheme helps organisations to

eliminate burden of detailed records of purchase and sales. Government makes changes

time to time in these flat rates.

Standard scheme- This is little bit complex as compared to other scheme but for large

business organisation it is more suitable. Under standard scheme 4 return in a year is to

be filed by organisation and tax is paid on quarterly basis. This is simple structure of

VAT which is applicable for all enterprises.

1.6 Maintaining an up-to-date knowledge of changes to code of practice, regulation or legislation

Compliance of Code of practice, regulation or legislation are necessary for organisation

in order to operate its functions effectively. In this context a great understanding of code of

practice, regulation or legislation of VAT is necessary in order to avoid any error, penalties,

disputes and demands (Mathur and Morris, 2014). Following code of practice helps organisations

to maintain records in systematic manner. Changes in regulation and legislation is made by

government time to time to reduce complexities. Business organisation should aware about

recent and potential changes in VAT system to keep on changes in forecast and budget as per

these changes.

TASK 2

2.1 Extraction of relevant data for a specific period of accounting period

Under UK's VAT regulatory system, returns are submitted monthly or quarterly basis.

Mostly quarterly return submission is preferred. After getting registration under VAT

organisations are bound to submit return in accordance with rules and regulation prescribed by

authorities. Let us take an registered organisation for which quarters ends on March, June,

September and December. Following are the details for the extraction of relevant data for filing

the return of the VAT for the quarter ending 31st December, 2018:

Accounting Information

For VAT payable:

Sales Book £ 245550

which a flat rate for VAT is provided to organisations according to their products and

activity. Such option is available to small businesses with taxable turnover of £150000

(excluding VAT) or less. Choosing option under this scheme helps organisations to

eliminate burden of detailed records of purchase and sales. Government makes changes

time to time in these flat rates.

Standard scheme- This is little bit complex as compared to other scheme but for large

business organisation it is more suitable. Under standard scheme 4 return in a year is to

be filed by organisation and tax is paid on quarterly basis. This is simple structure of

VAT which is applicable for all enterprises.

1.6 Maintaining an up-to-date knowledge of changes to code of practice, regulation or legislation

Compliance of Code of practice, regulation or legislation are necessary for organisation

in order to operate its functions effectively. In this context a great understanding of code of

practice, regulation or legislation of VAT is necessary in order to avoid any error, penalties,

disputes and demands (Mathur and Morris, 2014). Following code of practice helps organisations

to maintain records in systematic manner. Changes in regulation and legislation is made by

government time to time to reduce complexities. Business organisation should aware about

recent and potential changes in VAT system to keep on changes in forecast and budget as per

these changes.

TASK 2

2.1 Extraction of relevant data for a specific period of accounting period

Under UK's VAT regulatory system, returns are submitted monthly or quarterly basis.

Mostly quarterly return submission is preferred. After getting registration under VAT

organisations are bound to submit return in accordance with rules and regulation prescribed by

authorities. Let us take an registered organisation for which quarters ends on March, June,

September and December. Following are the details for the extraction of relevant data for filing

the return of the VAT for the quarter ending 31st December, 2018:

Accounting Information

For VAT payable:

Sales Book £ 245550

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

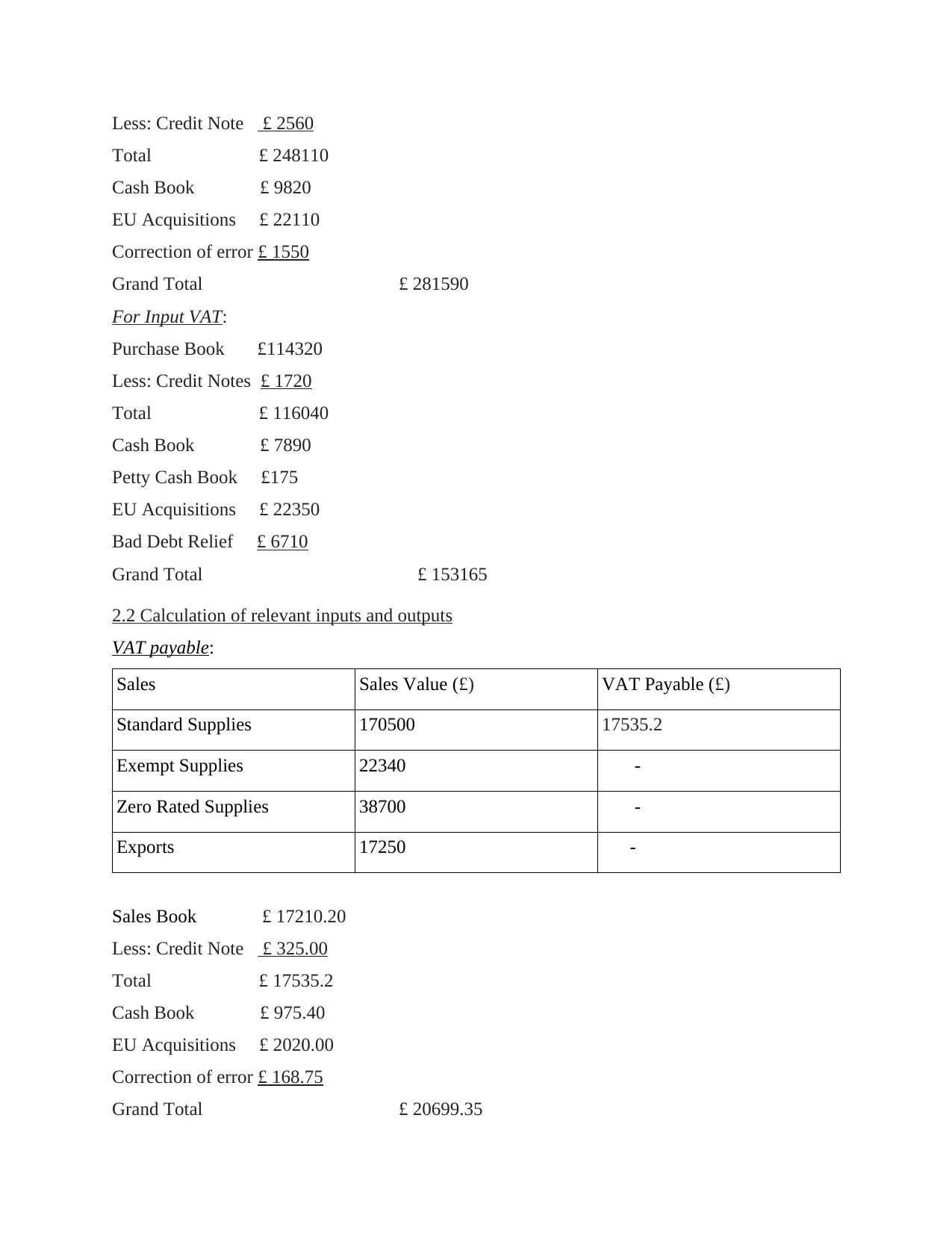

Less: Credit Note £ 2560

Total £ 248110

Cash Book £ 9820

EU Acquisitions £ 22110

Correction of error £ 1550

Grand Total £ 281590

For Input VAT:

Purchase Book £114320

Less: Credit Notes £ 1720

Total £ 116040

Cash Book £ 7890

Petty Cash Book £175

EU Acquisitions £ 22350

Bad Debt Relief £ 6710

Grand Total £ 153165

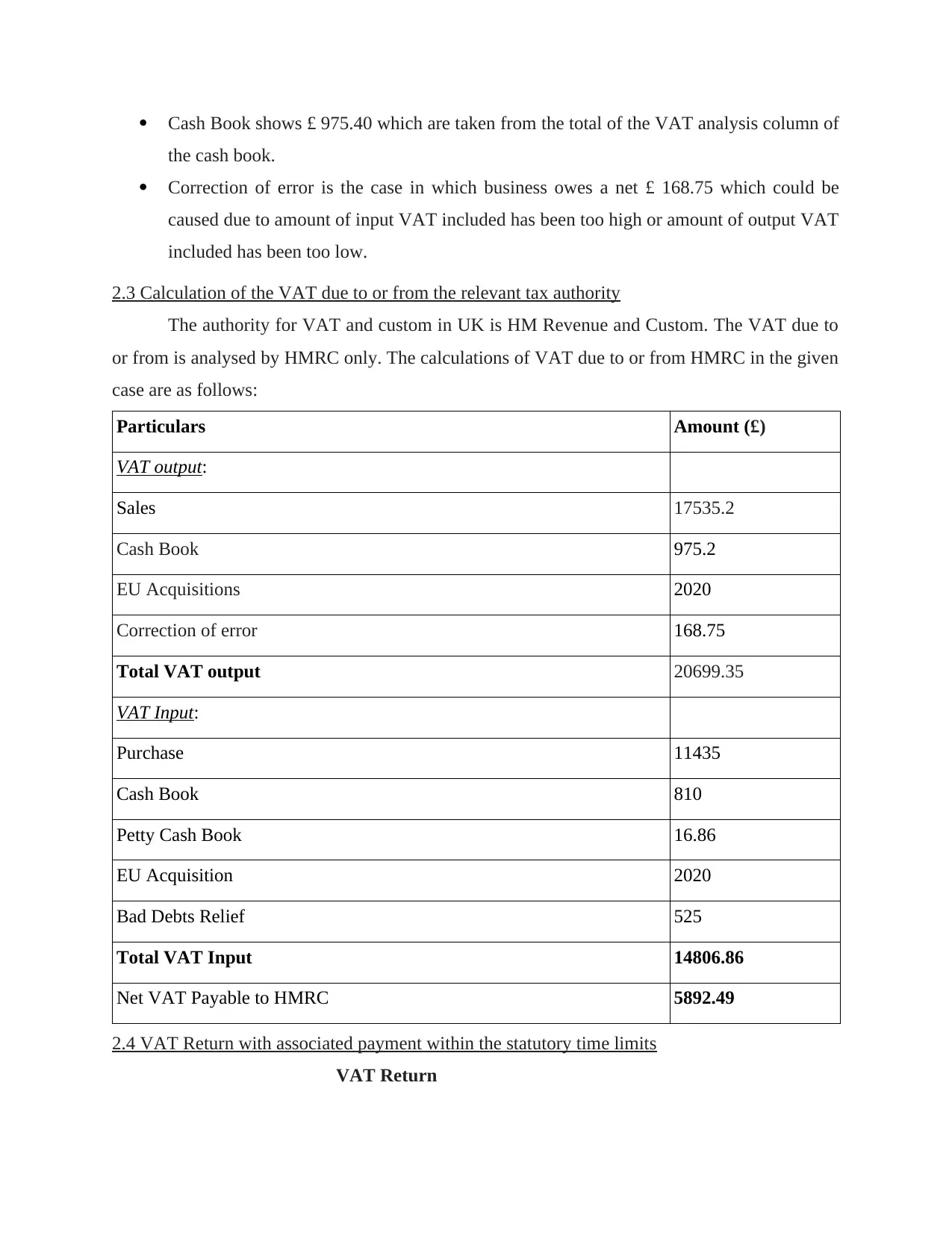

2.2 Calculation of relevant inputs and outputs

VAT payable:

Sales Sales Value (£) VAT Payable (£)

Standard Supplies 170500 17535.2

Exempt Supplies 22340 -

Zero Rated Supplies 38700 -

Exports 17250 -

Sales Book £ 17210.20

Less: Credit Note £ 325.00

Total £ 17535.2

Cash Book £ 975.40

EU Acquisitions £ 2020.00

Correction of error £ 168.75

Grand Total £ 20699.35

Total £ 248110

Cash Book £ 9820

EU Acquisitions £ 22110

Correction of error £ 1550

Grand Total £ 281590

For Input VAT:

Purchase Book £114320

Less: Credit Notes £ 1720

Total £ 116040

Cash Book £ 7890

Petty Cash Book £175

EU Acquisitions £ 22350

Bad Debt Relief £ 6710

Grand Total £ 153165

2.2 Calculation of relevant inputs and outputs

VAT payable:

Sales Sales Value (£) VAT Payable (£)

Standard Supplies 170500 17535.2

Exempt Supplies 22340 -

Zero Rated Supplies 38700 -

Exports 17250 -

Sales Book £ 17210.20

Less: Credit Note £ 325.00

Total £ 17535.2

Cash Book £ 975.40

EU Acquisitions £ 2020.00

Correction of error £ 168.75

Grand Total £ 20699.35

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

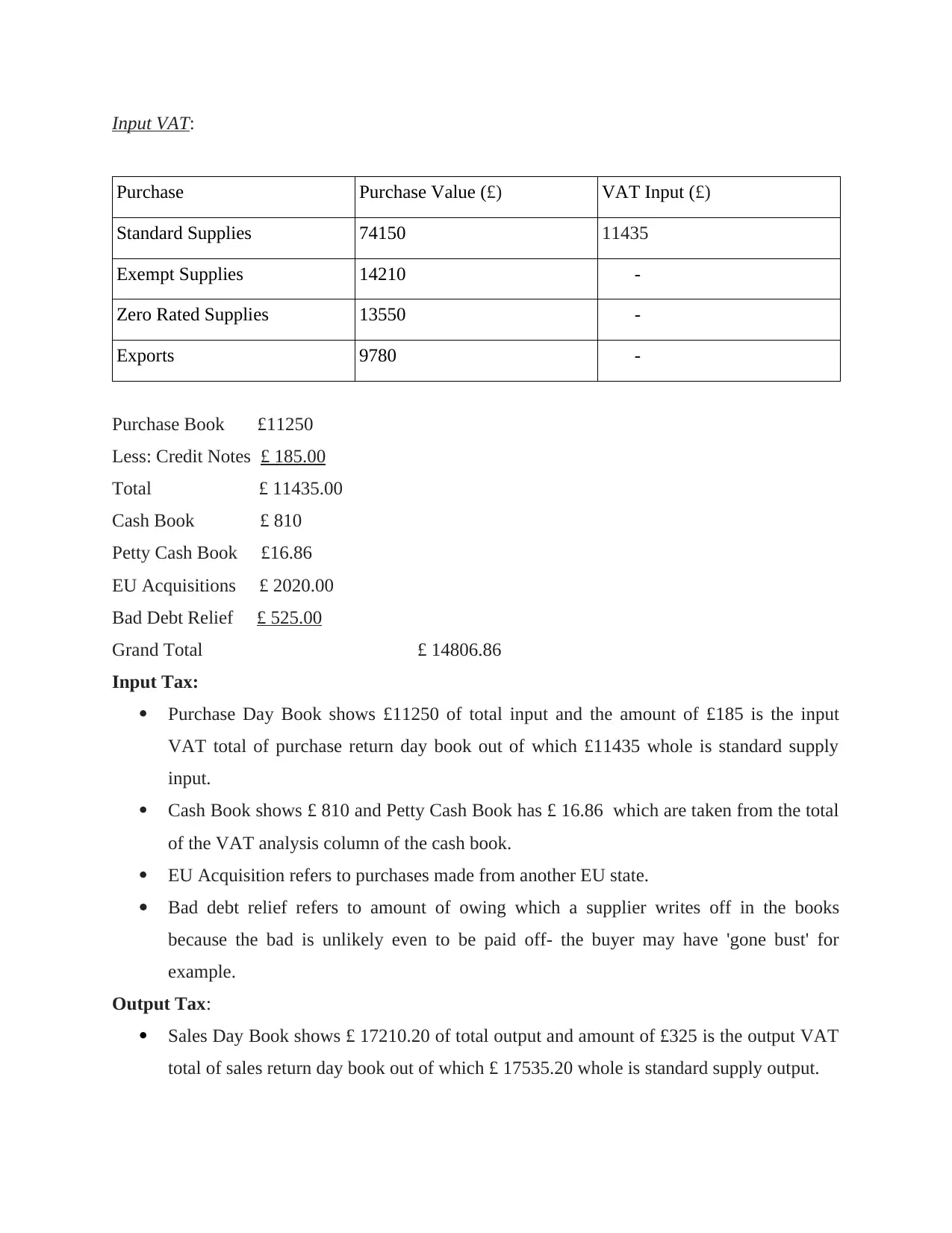

Input VAT:

Purchase Purchase Value (£) VAT Input (£)

Standard Supplies 74150 11435

Exempt Supplies 14210 -

Zero Rated Supplies 13550 -

Exports 9780 -

Purchase Book £11250

Less: Credit Notes £ 185.00

Total £ 11435.00

Cash Book £ 810

Petty Cash Book £16.86

EU Acquisitions £ 2020.00

Bad Debt Relief £ 525.00

Grand Total £ 14806.86

Input Tax:

Purchase Day Book shows £11250 of total input and the amount of £185 is the input

VAT total of purchase return day book out of which £11435 whole is standard supply

input.

Cash Book shows £ 810 and Petty Cash Book has £ 16.86 which are taken from the total

of the VAT analysis column of the cash book.

EU Acquisition refers to purchases made from another EU state.

Bad debt relief refers to amount of owing which a supplier writes off in the books

because the bad is unlikely even to be paid off- the buyer may have 'gone bust' for

example.

Output Tax:

Sales Day Book shows £ 17210.20 of total output and amount of £325 is the output VAT

total of sales return day book out of which £ 17535.20 whole is standard supply output.

Purchase Purchase Value (£) VAT Input (£)

Standard Supplies 74150 11435

Exempt Supplies 14210 -

Zero Rated Supplies 13550 -

Exports 9780 -

Purchase Book £11250

Less: Credit Notes £ 185.00

Total £ 11435.00

Cash Book £ 810

Petty Cash Book £16.86

EU Acquisitions £ 2020.00

Bad Debt Relief £ 525.00

Grand Total £ 14806.86

Input Tax:

Purchase Day Book shows £11250 of total input and the amount of £185 is the input

VAT total of purchase return day book out of which £11435 whole is standard supply

input.

Cash Book shows £ 810 and Petty Cash Book has £ 16.86 which are taken from the total

of the VAT analysis column of the cash book.

EU Acquisition refers to purchases made from another EU state.

Bad debt relief refers to amount of owing which a supplier writes off in the books

because the bad is unlikely even to be paid off- the buyer may have 'gone bust' for

example.

Output Tax:

Sales Day Book shows £ 17210.20 of total output and amount of £325 is the output VAT

total of sales return day book out of which £ 17535.20 whole is standard supply output.

Cash Book shows £ 975.40 which are taken from the total of the VAT analysis column of

the cash book.

Correction of error is the case in which business owes a net £ 168.75 which could be

caused due to amount of input VAT included has been too high or amount of output VAT

included has been too low.

2.3 Calculation of the VAT due to or from the relevant tax authority

The authority for VAT and custom in UK is HM Revenue and Custom. The VAT due to

or from is analysed by HMRC only. The calculations of VAT due to or from HMRC in the given

case are as follows:

Particulars Amount (£)

VAT output:

Sales 17535.2

Cash Book 975.2

EU Acquisitions 2020

Correction of error 168.75

Total VAT output 20699.35

VAT Input:

Purchase 11435

Cash Book 810

Petty Cash Book 16.86

EU Acquisition 2020

Bad Debts Relief 525

Total VAT Input 14806.86

Net VAT Payable to HMRC 5892.49

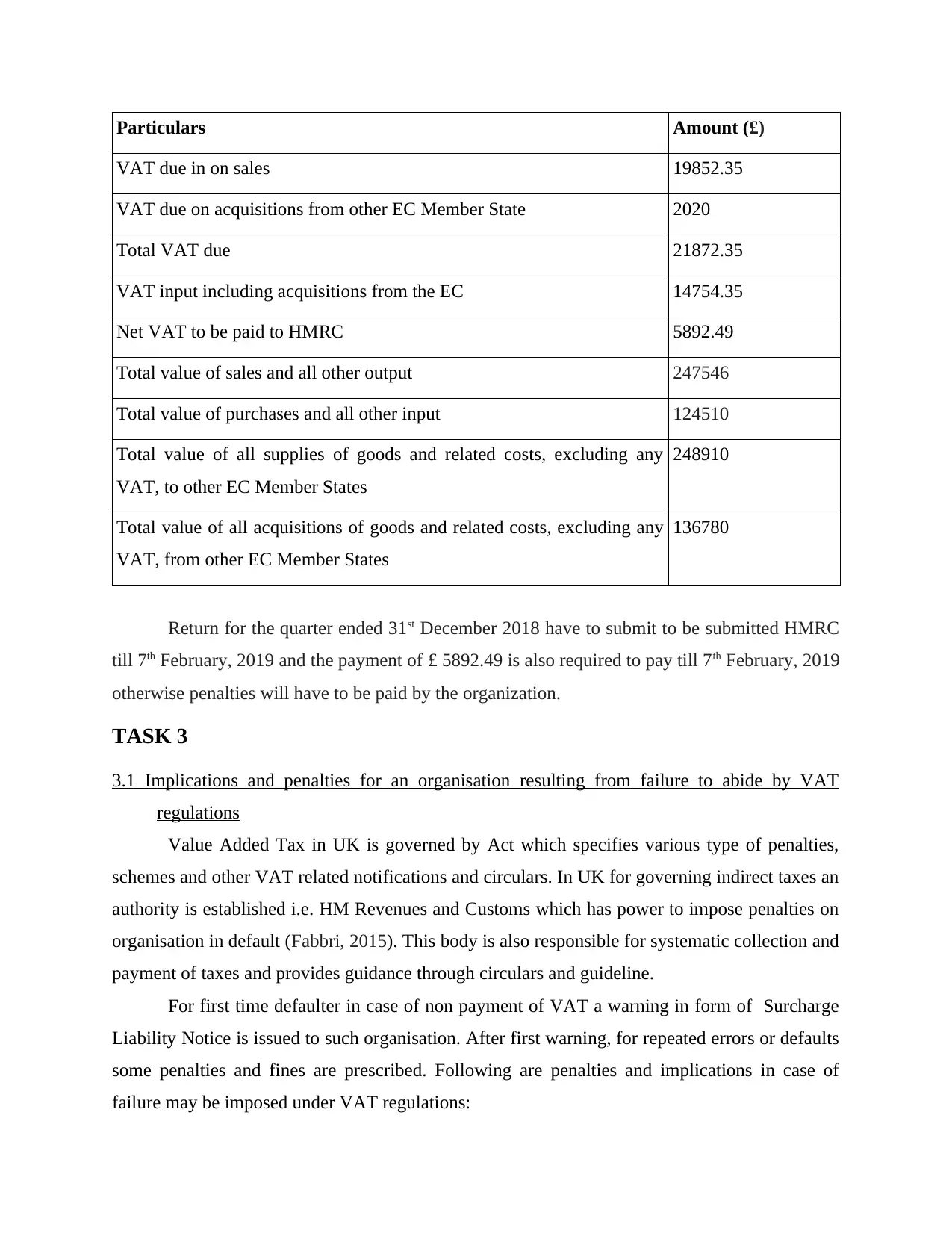

2.4 VAT Return with associated payment within the statutory time limits

VAT Return

the cash book.

Correction of error is the case in which business owes a net £ 168.75 which could be

caused due to amount of input VAT included has been too high or amount of output VAT

included has been too low.

2.3 Calculation of the VAT due to or from the relevant tax authority

The authority for VAT and custom in UK is HM Revenue and Custom. The VAT due to

or from is analysed by HMRC only. The calculations of VAT due to or from HMRC in the given

case are as follows:

Particulars Amount (£)

VAT output:

Sales 17535.2

Cash Book 975.2

EU Acquisitions 2020

Correction of error 168.75

Total VAT output 20699.35

VAT Input:

Purchase 11435

Cash Book 810

Petty Cash Book 16.86

EU Acquisition 2020

Bad Debts Relief 525

Total VAT Input 14806.86

Net VAT Payable to HMRC 5892.49

2.4 VAT Return with associated payment within the statutory time limits

VAT Return

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Amount (£)

VAT due in on sales 19852.35

VAT due on acquisitions from other EC Member State 2020

Total VAT due 21872.35

VAT input including acquisitions from the EC 14754.35

Net VAT to be paid to HMRC 5892.49

Total value of sales and all other output 247546

Total value of purchases and all other input 124510

Total value of all supplies of goods and related costs, excluding any

VAT, to other EC Member States

248910

Total value of all acquisitions of goods and related costs, excluding any

VAT, from other EC Member States

136780

Return for the quarter ended 31st December 2018 have to submit to be submitted HMRC

till 7th February, 2019 and the payment of £ 5892.49 is also required to pay till 7th February, 2019

otherwise penalties will have to be paid by the organization.

TASK 3

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations

Value Added Tax in UK is governed by Act which specifies various type of penalties,

schemes and other VAT related notifications and circulars. In UK for governing indirect taxes an

authority is established i.e. HM Revenues and Customs which has power to impose penalties on

organisation in default (Fabbri, 2015). This body is also responsible for systematic collection and

payment of taxes and provides guidance through circulars and guideline.

For first time defaulter in case of non payment of VAT a warning in form of Surcharge

Liability Notice is issued to such organisation. After first warning, for repeated errors or defaults

some penalties and fines are prescribed. Following are penalties and implications in case of

failure may be imposed under VAT regulations:

VAT due in on sales 19852.35

VAT due on acquisitions from other EC Member State 2020

Total VAT due 21872.35

VAT input including acquisitions from the EC 14754.35

Net VAT to be paid to HMRC 5892.49

Total value of sales and all other output 247546

Total value of purchases and all other input 124510

Total value of all supplies of goods and related costs, excluding any

VAT, to other EC Member States

248910

Total value of all acquisitions of goods and related costs, excluding any

VAT, from other EC Member States

136780

Return for the quarter ended 31st December 2018 have to submit to be submitted HMRC

till 7th February, 2019 and the payment of £ 5892.49 is also required to pay till 7th February, 2019

otherwise penalties will have to be paid by the organization.

TASK 3

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations

Value Added Tax in UK is governed by Act which specifies various type of penalties,

schemes and other VAT related notifications and circulars. In UK for governing indirect taxes an

authority is established i.e. HM Revenues and Customs which has power to impose penalties on

organisation in default (Fabbri, 2015). This body is also responsible for systematic collection and

payment of taxes and provides guidance through circulars and guideline.

For first time defaulter in case of non payment of VAT a warning in form of Surcharge

Liability Notice is issued to such organisation. After first warning, for repeated errors or defaults

some penalties and fines are prescribed. Following are penalties and implications in case of

failure may be imposed under VAT regulations:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In case of Late filing: No specific penalties are prescribed for late filing of VAT return

but penalty is prescribed for non payment or late payment of VAT payable.

In case of Late payment: In this case Surcharge Liability Notice is issued as discussed

above and in case conditions of Surcharge Liability Notice are not fulfilled than a

surcharge of 2% of the VAT due will apply and this gone be increased to 5%, 10% or

15% in case mistake is repeated or an extended Surcharge Liability Notice will be issued

(Madden, 2015).

Late registration: No specific penalties are prescribed in case of late VAT registration.

However if an organisation met the threshold and there is an obligation has been arsed

then penalties are levied for delay, In case Less than 9 months of delay: 5% of VAT due,

9 to 18 months delay: 10% of VAT due and more than 18 months delay: 15% of VAT

due.

3.2 Adjustments and declarations for any errors or omission identified in previous VAT period

Following are the criteria for adjustments for any errors or omission identified in

previous VAT period :

Error or omission should below the reporting threshold.

Error or omission should not be deliberated(mistake made on a purpose).

Error or omission should be for an accounting period that ends less then 4 years ago

(Jiang and Shao, 2014).

Following are the major facts that helps to make adjustments and declarations in case of

any errors or omission identified in previous VAT period:

From VAT 652 is used for Error correction in any previous year return, Official site of

government provides this forms through its official website after filling business details

on website along with VAT registration number.

Transitional arrangements are introduced by HMRC which for rectification of error in

relation to mismatch regarding input credit.

HMRC also provide relief from difficulties of error correction by launching specific

schemes for correction.

but penalty is prescribed for non payment or late payment of VAT payable.

In case of Late payment: In this case Surcharge Liability Notice is issued as discussed

above and in case conditions of Surcharge Liability Notice are not fulfilled than a

surcharge of 2% of the VAT due will apply and this gone be increased to 5%, 10% or

15% in case mistake is repeated or an extended Surcharge Liability Notice will be issued

(Madden, 2015).

Late registration: No specific penalties are prescribed in case of late VAT registration.

However if an organisation met the threshold and there is an obligation has been arsed

then penalties are levied for delay, In case Less than 9 months of delay: 5% of VAT due,

9 to 18 months delay: 10% of VAT due and more than 18 months delay: 15% of VAT

due.

3.2 Adjustments and declarations for any errors or omission identified in previous VAT period

Following are the criteria for adjustments for any errors or omission identified in

previous VAT period :

Error or omission should below the reporting threshold.

Error or omission should not be deliberated(mistake made on a purpose).

Error or omission should be for an accounting period that ends less then 4 years ago

(Jiang and Shao, 2014).

Following are the major facts that helps to make adjustments and declarations in case of

any errors or omission identified in previous VAT period:

From VAT 652 is used for Error correction in any previous year return, Official site of

government provides this forms through its official website after filling business details

on website along with VAT registration number.

Transitional arrangements are introduced by HMRC which for rectification of error in

relation to mismatch regarding input credit.

HMRC also provide relief from difficulties of error correction by launching specific

schemes for correction.

TASK 4

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts

There is huge impact on company's cash flow due to payment of VAT. However,VAT

rates change as time passes by to retain its effect and efficiency. These changes have impact on

all financial accounts across an organisation which eventually affect the VAT control account.

The factors which affect the cash flow and financial forecasts due to VAT payment are explained

as follows:

Imposition of penalty by the tax departments for the error done by the organisation and

management are unknown about these errors can affect cash flow or financial forecast of

the organisation.

Sudden increase in VAT rate by the government on the products which the organisation

is engaged can affect financial forecast of managers.

If the company is dealing in credit sales and purchase the goods in cash, then this will

adversely affect the cash flow position of the company because of late payment or receipt

from the parties (Thuronyi and Cui, 2015).

Sudden demand notice received by the tax authorities of UK can also increases the

payment towards consultants and legal charges which affects cash flow of the entity

adversely.

Payment of VAT may impact the working capital requirement and due to which

organisation requires more cash, it will reduce the cash flow in the business.

4.2 Advise for changes in VAT legislation which would have an effect on an organisation’s

recording systems

By implementing the changes by the government time to time by issuing circulars or

notification etc. which affects various interested person in an organisation like mangers,

accountant, supplier, related parties etc. Changes in the VAT legislation will effect the

organisational recording system such as making tax digital or removing offline forms for VAT

registration. Organisation faced many challenges for implementing these legislation changes in

the organisation. These are as follows:

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts

There is huge impact on company's cash flow due to payment of VAT. However,VAT

rates change as time passes by to retain its effect and efficiency. These changes have impact on

all financial accounts across an organisation which eventually affect the VAT control account.

The factors which affect the cash flow and financial forecasts due to VAT payment are explained

as follows:

Imposition of penalty by the tax departments for the error done by the organisation and

management are unknown about these errors can affect cash flow or financial forecast of

the organisation.

Sudden increase in VAT rate by the government on the products which the organisation

is engaged can affect financial forecast of managers.

If the company is dealing in credit sales and purchase the goods in cash, then this will

adversely affect the cash flow position of the company because of late payment or receipt

from the parties (Thuronyi and Cui, 2015).

Sudden demand notice received by the tax authorities of UK can also increases the

payment towards consultants and legal charges which affects cash flow of the entity

adversely.

Payment of VAT may impact the working capital requirement and due to which

organisation requires more cash, it will reduce the cash flow in the business.

4.2 Advise for changes in VAT legislation which would have an effect on an organisation’s

recording systems

By implementing the changes by the government time to time by issuing circulars or

notification etc. which affects various interested person in an organisation like mangers,

accountant, supplier, related parties etc. Changes in the VAT legislation will effect the

organisational recording system such as making tax digital or removing offline forms for VAT

registration. Organisation faced many challenges for implementing these legislation changes in

the organisation. These are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.