International Financial Management

VerifiedAdded on 2023/01/09

|9

|2096

|32

AI Summary

This study covers the critical evaluation of multiple techniques of investment appraisals along with practice tasks. It also discusses non-financial factors in the organizational context. The study provides insights into evaluating the financial viability of investment projects using methods like Payback Method, ARR, and IRR. It also explores the advantages and disadvantages of these methods. Additionally, it discusses several non-financial variables that companies should consider in investment appraisal, such as legislation, industry standards, relationships with suppliers and customers, and external factors like inflation.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

International Financial

Management

Management

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Evaluating financial viability of investment project:...................................................................3

Critical appraise use of Payback Method, ARR and IRR as methods of investment appraisal:..5

Discussion about several non-financial variables a company should regard in investment

appraisal:......................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES ...............................................................................................................................9

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Evaluating financial viability of investment project:...................................................................3

Critical appraise use of Payback Method, ARR and IRR as methods of investment appraisal:..5

Discussion about several non-financial variables a company should regard in investment

appraisal:......................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES ...............................................................................................................................9

INTRODUCTION

Faster globalization, financial turmoil and an ever-changing market climate combined to

make current financial management problems more important than before. And these same

factors make effective financial controls quite necessary, as international financial management

(IFM) works, through decisions of financial nature made, at the time of global business (Madura,

2020). In this regard, the study covers critical evaluation of multiple techniques of investment

appraisals along with practice task. Further this study cover comprehensive discussion about

non-financial factors in organisational context.

MAIN BODY

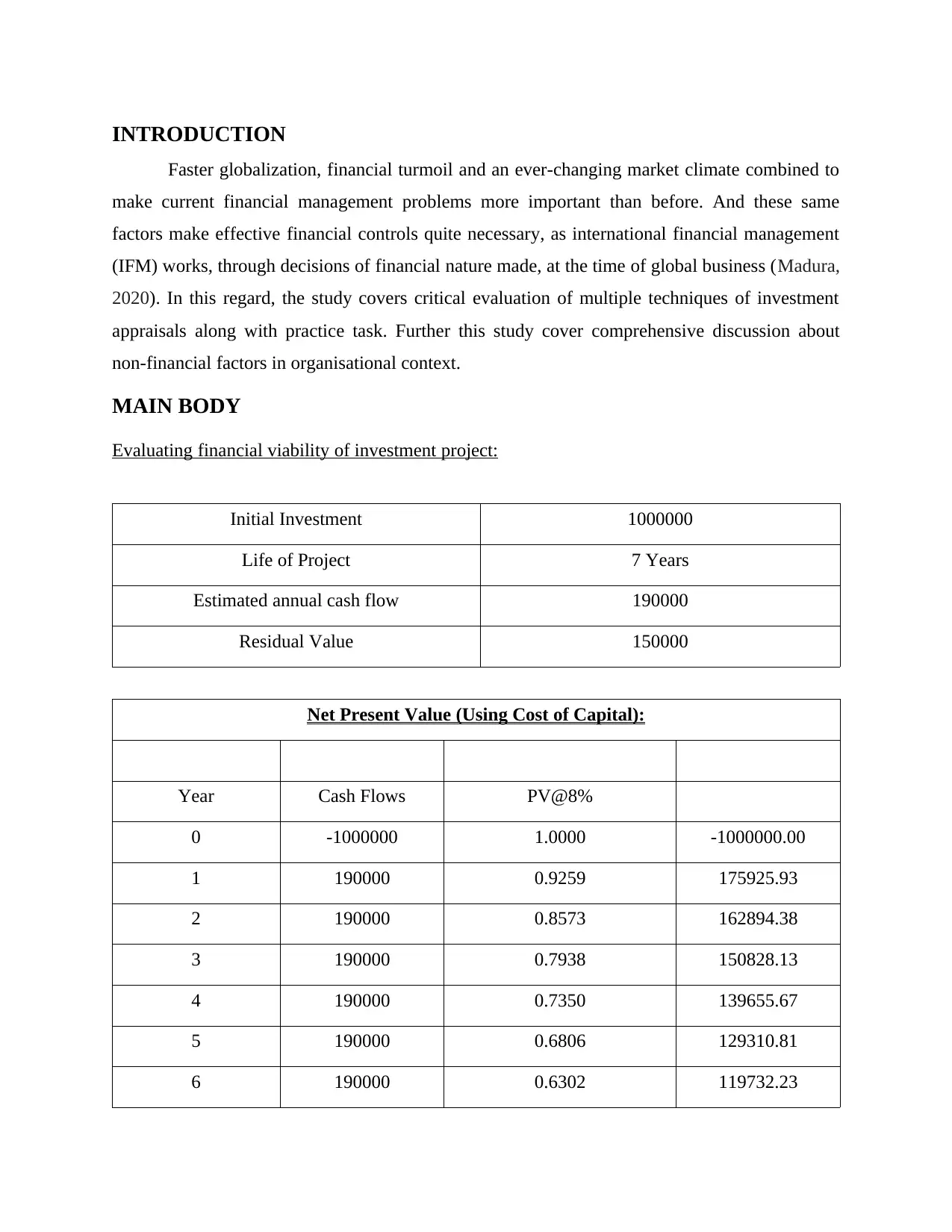

Evaluating financial viability of investment project:

Initial Investment 1000000

Life of Project 7 Years

Estimated annual cash flow 190000

Residual Value 150000

Net Present Value (Using Cost of Capital):

Year Cash Flows PV@8%

0 -1000000 1.0000 -1000000.00

1 190000 0.9259 175925.93

2 190000 0.8573 162894.38

3 190000 0.7938 150828.13

4 190000 0.7350 139655.67

5 190000 0.6806 129310.81

6 190000 0.6302 119732.23

Faster globalization, financial turmoil and an ever-changing market climate combined to

make current financial management problems more important than before. And these same

factors make effective financial controls quite necessary, as international financial management

(IFM) works, through decisions of financial nature made, at the time of global business (Madura,

2020). In this regard, the study covers critical evaluation of multiple techniques of investment

appraisals along with practice task. Further this study cover comprehensive discussion about

non-financial factors in organisational context.

MAIN BODY

Evaluating financial viability of investment project:

Initial Investment 1000000

Life of Project 7 Years

Estimated annual cash flow 190000

Residual Value 150000

Net Present Value (Using Cost of Capital):

Year Cash Flows PV@8%

0 -1000000 1.0000 -1000000.00

1 190000 0.9259 175925.93

2 190000 0.8573 162894.38

3 190000 0.7938 150828.13

4 190000 0.7350 139655.67

5 190000 0.6806 129310.81

6 190000 0.6302 119732.23

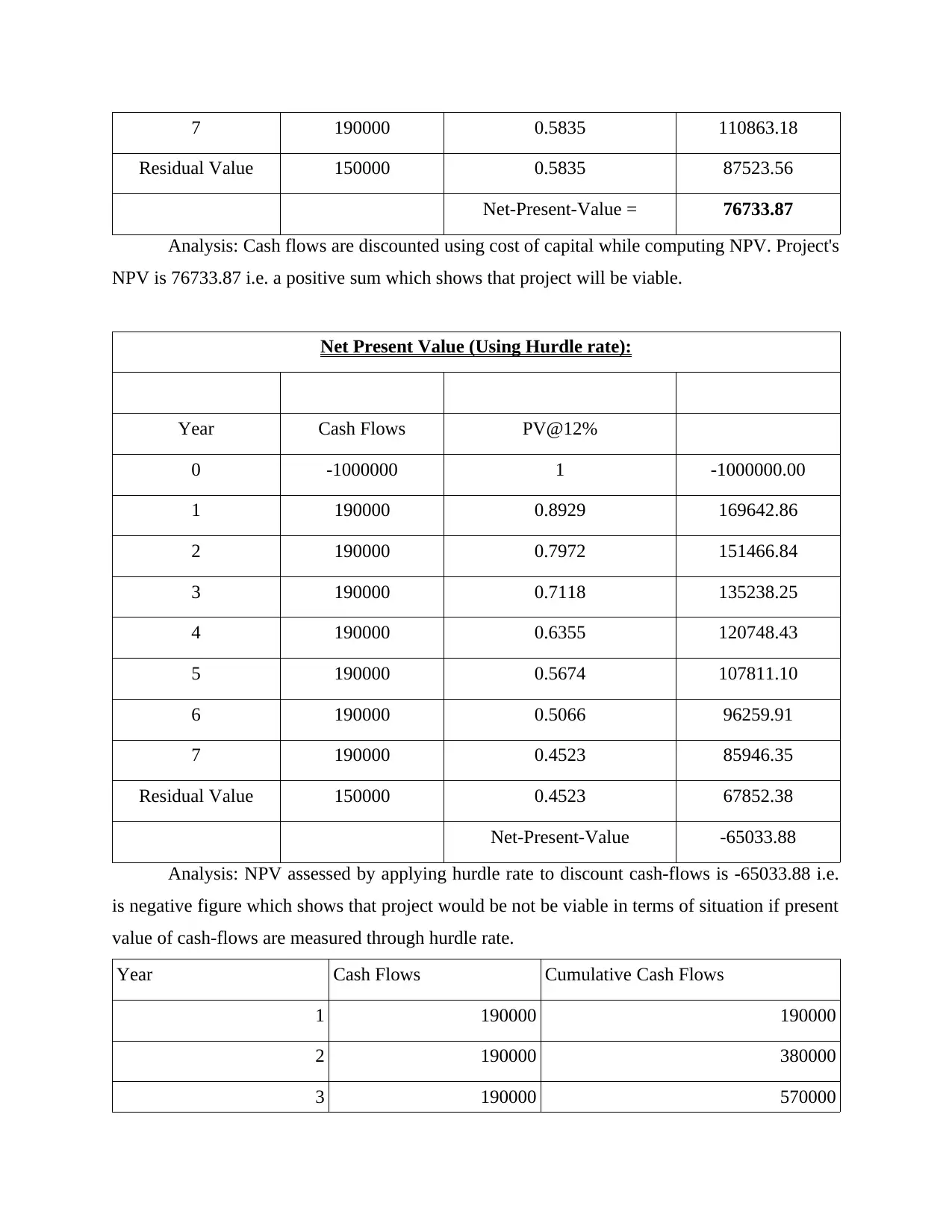

7 190000 0.5835 110863.18

Residual Value 150000 0.5835 87523.56

Net-Present-Value = 76733.87

Analysis: Cash flows are discounted using cost of capital while computing NPV. Project's

NPV is 76733.87 i.e. a positive sum which shows that project will be viable.

Net Present Value (Using Hurdle rate):

Year Cash Flows PV@12%

0 -1000000 1 -1000000.00

1 190000 0.8929 169642.86

2 190000 0.7972 151466.84

3 190000 0.7118 135238.25

4 190000 0.6355 120748.43

5 190000 0.5674 107811.10

6 190000 0.5066 96259.91

7 190000 0.4523 85946.35

Residual Value 150000 0.4523 67852.38

Net-Present-Value -65033.88

Analysis: NPV assessed by applying hurdle rate to discount cash-flows is -65033.88 i.e.

is negative figure which shows that project would be not be viable in terms of situation if present

value of cash-flows are measured through hurdle rate.

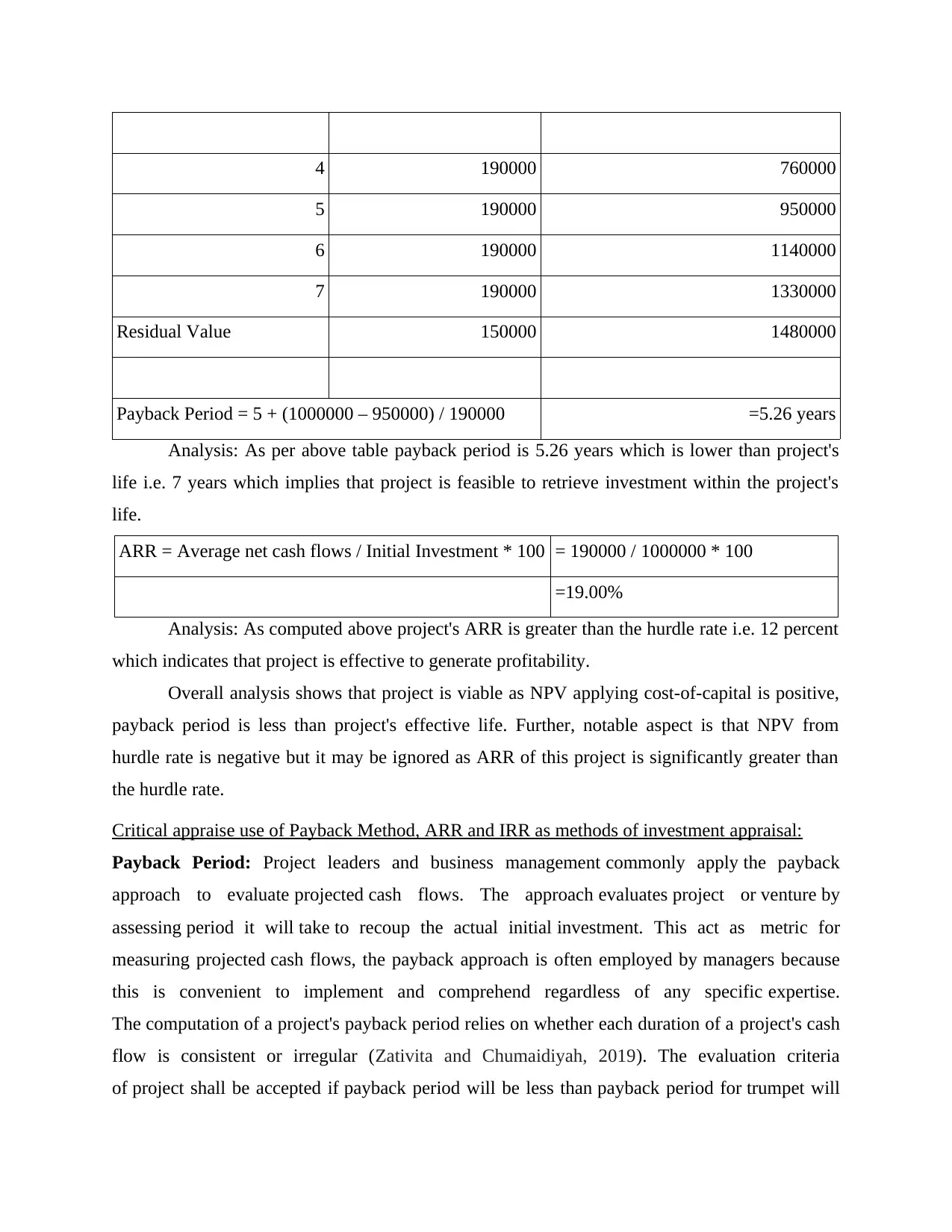

Year Cash Flows Cumulative Cash Flows

1 190000 190000

2 190000 380000

3 190000 570000

Residual Value 150000 0.5835 87523.56

Net-Present-Value = 76733.87

Analysis: Cash flows are discounted using cost of capital while computing NPV. Project's

NPV is 76733.87 i.e. a positive sum which shows that project will be viable.

Net Present Value (Using Hurdle rate):

Year Cash Flows PV@12%

0 -1000000 1 -1000000.00

1 190000 0.8929 169642.86

2 190000 0.7972 151466.84

3 190000 0.7118 135238.25

4 190000 0.6355 120748.43

5 190000 0.5674 107811.10

6 190000 0.5066 96259.91

7 190000 0.4523 85946.35

Residual Value 150000 0.4523 67852.38

Net-Present-Value -65033.88

Analysis: NPV assessed by applying hurdle rate to discount cash-flows is -65033.88 i.e.

is negative figure which shows that project would be not be viable in terms of situation if present

value of cash-flows are measured through hurdle rate.

Year Cash Flows Cumulative Cash Flows

1 190000 190000

2 190000 380000

3 190000 570000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4 190000 760000

5 190000 950000

6 190000 1140000

7 190000 1330000

Residual Value 150000 1480000

Payback Period = 5 + (1000000 – 950000) / 190000 =5.26 years

Analysis: As per above table payback period is 5.26 years which is lower than project's

life i.e. 7 years which implies that project is feasible to retrieve investment within the project's

life.

ARR = Average net cash flows / Initial Investment * 100 = 190000 / 1000000 * 100

=19.00%

Analysis: As computed above project's ARR is greater than the hurdle rate i.e. 12 percent

which indicates that project is effective to generate profitability.

Overall analysis shows that project is viable as NPV applying cost-of-capital is positive,

payback period is less than project's effective life. Further, notable aspect is that NPV from

hurdle rate is negative but it may be ignored as ARR of this project is significantly greater than

the hurdle rate.

Critical appraise use of Payback Method, ARR and IRR as methods of investment appraisal:

Payback Period: Project leaders and business management commonly apply the payback

approach to evaluate projected cash flows. The approach evaluates project or venture by

assessing period it will take to recoup the actual initial investment. This act as metric for

measuring projected cash flows, the payback approach is often employed by managers because

this is convenient to implement and comprehend regardless of any specific expertise.

The computation of a project's payback period relies on whether each duration of a project's cash

flow is consistent or irregular (Zativita and Chumaidiyah, 2019). The evaluation criteria

of project shall be accepted if payback period will be less than payback period for trumpet will

5 190000 950000

6 190000 1140000

7 190000 1330000

Residual Value 150000 1480000

Payback Period = 5 + (1000000 – 950000) / 190000 =5.26 years

Analysis: As per above table payback period is 5.26 years which is lower than project's

life i.e. 7 years which implies that project is feasible to retrieve investment within the project's

life.

ARR = Average net cash flows / Initial Investment * 100 = 190000 / 1000000 * 100

=19.00%

Analysis: As computed above project's ARR is greater than the hurdle rate i.e. 12 percent

which indicates that project is effective to generate profitability.

Overall analysis shows that project is viable as NPV applying cost-of-capital is positive,

payback period is less than project's effective life. Further, notable aspect is that NPV from

hurdle rate is negative but it may be ignored as ARR of this project is significantly greater than

the hurdle rate.

Critical appraise use of Payback Method, ARR and IRR as methods of investment appraisal:

Payback Period: Project leaders and business management commonly apply the payback

approach to evaluate projected cash flows. The approach evaluates project or venture by

assessing period it will take to recoup the actual initial investment. This act as metric for

measuring projected cash flows, the payback approach is often employed by managers because

this is convenient to implement and comprehend regardless of any specific expertise.

The computation of a project's payback period relies on whether each duration of a project's cash

flow is consistent or irregular (Zativita and Chumaidiyah, 2019). The evaluation criteria

of project shall be accepted if payback period will be less than payback period for trumpet will

be less than a targeted payback period. Here are several key benefits and drawbacks of this

method, as follows:

Advantages: The payback approach provide benefits in situations where an entity has

some time criteria as to how longer a project would take to repay itself off as well as

simple to assess. Due to its emphasis towards cost returns, businesses should use payback

method as an initial evaluation method when evaluating two or even more

projects choices. Understanding how longer an undertaking would require paying for

itself often comes in very handy in situations where project funding ties vast sums of

capital over lengthy stretches of time.

Disadvantages: Since distinct capital budgeting approaches demonstrate varying key

elements of project investment, weakness of payback method is due to its emphasis

only on paying-back period. Certain other relevant considerations to be included in

project evaluation include the project's generating potential, total return-on-investment

and time-frame contrasts. Projects which involve a longer payback period can actually

generate better returns than project with shorter payback period. The payback

methodology offers little and no detail on rate of return while evaluating two or maybe

more project alternatives, suggesting that project may yield improved returns over a

longer time-period.

ARR: The ARR or Accounting-return-rate is proportion of accounting profits to investment

made in a project, represented as percentage. When the ARR is higher than or exactly equivalent

to a project's hurdle rate, project will be accepted. "This approach is based on the estimated

accounting operating income produced by investment and calculated as a ratio of total

investment generated over entire life of project (Meta, 2016). Here following are some key

advantages and drawbacks of this method:

Advantages: It's very quick to quantify as well as quite simple to comprehend ARR. This

shall take into account total profits or benefits generated over the whole productive life of

a project. This recognizes key concept of net profit, i.e. profit after taxation and

depreciation. That is a crucial consideration in the determination under investment

proposal evaluation. This approach makes it possible to equate the new design proposal

with the cost-reduction proposal or other programs of a similar nature. This approach

provides a clear view of the feasibility of the enterprise. Each calls, on its own, the

method, as follows:

Advantages: The payback approach provide benefits in situations where an entity has

some time criteria as to how longer a project would take to repay itself off as well as

simple to assess. Due to its emphasis towards cost returns, businesses should use payback

method as an initial evaluation method when evaluating two or even more

projects choices. Understanding how longer an undertaking would require paying for

itself often comes in very handy in situations where project funding ties vast sums of

capital over lengthy stretches of time.

Disadvantages: Since distinct capital budgeting approaches demonstrate varying key

elements of project investment, weakness of payback method is due to its emphasis

only on paying-back period. Certain other relevant considerations to be included in

project evaluation include the project's generating potential, total return-on-investment

and time-frame contrasts. Projects which involve a longer payback period can actually

generate better returns than project with shorter payback period. The payback

methodology offers little and no detail on rate of return while evaluating two or maybe

more project alternatives, suggesting that project may yield improved returns over a

longer time-period.

ARR: The ARR or Accounting-return-rate is proportion of accounting profits to investment

made in a project, represented as percentage. When the ARR is higher than or exactly equivalent

to a project's hurdle rate, project will be accepted. "This approach is based on the estimated

accounting operating income produced by investment and calculated as a ratio of total

investment generated over entire life of project (Meta, 2016). Here following are some key

advantages and drawbacks of this method:

Advantages: It's very quick to quantify as well as quite simple to comprehend ARR. This

shall take into account total profits or benefits generated over the whole productive life of

a project. This recognizes key concept of net profit, i.e. profit after taxation and

depreciation. That is a crucial consideration in the determination under investment

proposal evaluation. This approach makes it possible to equate the new design proposal

with the cost-reduction proposal or other programs of a similar nature. This approach

provides a clear view of the feasibility of the enterprise. Each calls, on its own, the

accounting definition of income and the estimation of the rate of return. In fact, the

financial income can be accurately estimated from accounting reports.

Disadvantages: The outcomes are distinctive when one measures ROI and other

computes ARR. It causes a problem while taking decisions. This approach disregards the

factor of time. The main disadvantage of ARR method for selecting option applies of

funds would be that time value of such funds is disregarded. It is not possible to

ascertain fair return rate on grounds of ARR. This is discretion of the administration. This

approach does not take into account external variables which often influence the

competitiveness of project. It's doesn't consider cash inflows that are more crucial

than accounting-profits.

IRR: An IRR approach assesses the value of project or cash flows. This approach act as interest

rate where NPV of cash flows of investment/project is zero. When IRR of project

exceeds required return rate, then project would be desirable. In most cases , project executives

chose the IRR approach because it provides a quick overview of projects which would lend as

much as potential Cash flows (Kulakov and Kastro, 2017). Even so, this method concentrates

only projected cash flows which originate through capital investments. As a consequence, it

disregards prospective future costs which ultimately affect returns.

Advantages: This method's basic advantage is that it consider time factor which enhance

the usefulness and creditability of this approach. Interpretation of outcomes under this

method is very simple and help to assess the effectiveness of an investment.

Disadvantage: This method is basically relies on management's and enterprise's

assumptions which some time leads to misinterpretation of outcomes. In the case of such

projects, the contractor might also be expected to participate in such dependent projects.

But the IRR lacks these added costs. A IRR recommend the purchasing of an asset,

but gains obtained by that investment could be washed out by the expense of a contingent

investment.

Discussion about several non-financial variables a company should regard in investment

appraisal:

While financial case for investing money is a crucial part of decision-making process,

non-financial considerations may also be significant. Non financial factors are key consideration

in investment appraisal as they also directly or indirectly influence the decision-making with

financial income can be accurately estimated from accounting reports.

Disadvantages: The outcomes are distinctive when one measures ROI and other

computes ARR. It causes a problem while taking decisions. This approach disregards the

factor of time. The main disadvantage of ARR method for selecting option applies of

funds would be that time value of such funds is disregarded. It is not possible to

ascertain fair return rate on grounds of ARR. This is discretion of the administration. This

approach does not take into account external variables which often influence the

competitiveness of project. It's doesn't consider cash inflows that are more crucial

than accounting-profits.

IRR: An IRR approach assesses the value of project or cash flows. This approach act as interest

rate where NPV of cash flows of investment/project is zero. When IRR of project

exceeds required return rate, then project would be desirable. In most cases , project executives

chose the IRR approach because it provides a quick overview of projects which would lend as

much as potential Cash flows (Kulakov and Kastro, 2017). Even so, this method concentrates

only projected cash flows which originate through capital investments. As a consequence, it

disregards prospective future costs which ultimately affect returns.

Advantages: This method's basic advantage is that it consider time factor which enhance

the usefulness and creditability of this approach. Interpretation of outcomes under this

method is very simple and help to assess the effectiveness of an investment.

Disadvantage: This method is basically relies on management's and enterprise's

assumptions which some time leads to misinterpretation of outcomes. In the case of such

projects, the contractor might also be expected to participate in such dependent projects.

But the IRR lacks these added costs. A IRR recommend the purchasing of an asset,

but gains obtained by that investment could be washed out by the expense of a contingent

investment.

Discussion about several non-financial variables a company should regard in investment

appraisal:

While financial case for investing money is a crucial part of decision-making process,

non-financial considerations may also be significant. Non financial factors are key consideration

in investment appraisal as they also directly or indirectly influence the decision-making with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

respect to the selection of most effective and viable investment. Here following is discussion

about major non-financial factors, as follows:

Current and future legislation: Rules, laws and legislations whether current or

proposed are key variable in investment appraisal as they determine legal viability of

such investment in practical life. Management must consider existing and potential

legislation as well as their compliance to while selecting a best investment option as to

avoid any future complexities.

Industry Standards: Comparison with industry standards is significant to as to deal with

competitive business environmental factors. As if an investment proposal meets all the

criteria but not as per industry's standards then in real life, selection of such investment

would not be viable (Li, F.G. and Trutnevyte, 2017).

Relationships with suppliers and customers: Most often a investment's viability is

dependent on success in market which depends on customer's responses thus healthy

relationship with customers is crucial factor to consider in investment appraisal. Also

suppliers are most influential player within a market sector who have direct control over

each enterprise product cost as well as investment decisions. Thus effective relationship

with suppliers is quite essential in process of investment appraisal.

Inflation and other extremal Factors: Economic inflation rate directly impact buying

power of customers, borrowing rate and other variables thus while selecting an

investment proposal management must consider effect of inflation rate on investment.

Also there are some other external factors which are necessary to consider in investment

appraisal like organisation's market position, geographical location, social factors and so

on (Fokkema, Buijs and Vis, 2017).

CONCLUSION

From above study this has been articulated that different investment appraisal techniques

are quite essential for enterprise to take financial and investment decisions. However, here

certain non-financial exists which may affect enterprise decision-making in relation to

investment appraisal as discussed above thus consideration of such variable makes decision more

relevant.

about major non-financial factors, as follows:

Current and future legislation: Rules, laws and legislations whether current or

proposed are key variable in investment appraisal as they determine legal viability of

such investment in practical life. Management must consider existing and potential

legislation as well as their compliance to while selecting a best investment option as to

avoid any future complexities.

Industry Standards: Comparison with industry standards is significant to as to deal with

competitive business environmental factors. As if an investment proposal meets all the

criteria but not as per industry's standards then in real life, selection of such investment

would not be viable (Li, F.G. and Trutnevyte, 2017).

Relationships with suppliers and customers: Most often a investment's viability is

dependent on success in market which depends on customer's responses thus healthy

relationship with customers is crucial factor to consider in investment appraisal. Also

suppliers are most influential player within a market sector who have direct control over

each enterprise product cost as well as investment decisions. Thus effective relationship

with suppliers is quite essential in process of investment appraisal.

Inflation and other extremal Factors: Economic inflation rate directly impact buying

power of customers, borrowing rate and other variables thus while selecting an

investment proposal management must consider effect of inflation rate on investment.

Also there are some other external factors which are necessary to consider in investment

appraisal like organisation's market position, geographical location, social factors and so

on (Fokkema, Buijs and Vis, 2017).

CONCLUSION

From above study this has been articulated that different investment appraisal techniques

are quite essential for enterprise to take financial and investment decisions. However, here

certain non-financial exists which may affect enterprise decision-making in relation to

investment appraisal as discussed above thus consideration of such variable makes decision more

relevant.

REFERENCES

Books and Journals:

Madura, J., 2020. International financial management. Cengage Learning.

Zativita, F.I. and Chumaidiyah, E., 2019, May. Feasibility analysis of Rumah Tempe Zanada

establishment in Bandung using net present value, internal rate of return, and payback

period. In IOP Conference Series: Materials Science and Engineering (Vol. 505, No. 1,

p. 012007). IOP Publishing.

Meta, M., 2016. Relationship of the capital investment coefficient, accounting and internal rate

of return. Ekonomski izazovi, 5(9), pp.62-76.

Kulakov, N.Y. and Kastro, A.N.B., 2017. New applications of the IRR Method in the Evaluation

of investment Projects. In IIE Annual Conference. Proceedings (pp. 464-469). Institute

of Industrial and Systems Engineers (IISE).

Li, F.G. and Trutnevyte, E., 2017. Investment appraisal of cost-optimal and near-optimal

pathways for the UK electricity sector transition to 2050. Applied energy, 189, pp.89-

109.

Fokkema, J.E., Buijs, P. and Vis, I.F., 2017. An investment appraisal method to compare LNG-

fueled and conventional vessels. Transportation Research Part D: Transport and

Environment, 56, pp.229-240.

Books and Journals:

Madura, J., 2020. International financial management. Cengage Learning.

Zativita, F.I. and Chumaidiyah, E., 2019, May. Feasibility analysis of Rumah Tempe Zanada

establishment in Bandung using net present value, internal rate of return, and payback

period. In IOP Conference Series: Materials Science and Engineering (Vol. 505, No. 1,

p. 012007). IOP Publishing.

Meta, M., 2016. Relationship of the capital investment coefficient, accounting and internal rate

of return. Ekonomski izazovi, 5(9), pp.62-76.

Kulakov, N.Y. and Kastro, A.N.B., 2017. New applications of the IRR Method in the Evaluation

of investment Projects. In IIE Annual Conference. Proceedings (pp. 464-469). Institute

of Industrial and Systems Engineers (IISE).

Li, F.G. and Trutnevyte, E., 2017. Investment appraisal of cost-optimal and near-optimal

pathways for the UK electricity sector transition to 2050. Applied energy, 189, pp.89-

109.

Fokkema, J.E., Buijs, P. and Vis, I.F., 2017. An investment appraisal method to compare LNG-

fueled and conventional vessels. Transportation Research Part D: Transport and

Environment, 56, pp.229-240.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.