International Financial Management Assignment - University Name

VerifiedAdded on 2022/09/27

|13

|2972

|22

Homework Assignment

AI Summary

This assignment on International Financial Management (IFM) analyzes various financial concepts within a global context. Part A focuses on calculating exchange rates (EURUSD, GBPEUR), explaining triangular arbitrage, and assessing inflation's impact on currency values. It delves into the real value of the dollar, implications of exchange rate changes, and interest rate differentials between the US and Eurozone. Part B explores options and futures contracts. It calculates net payouts from call and put options, outlines advantages/disadvantages for MNCs, and explains how futures contracts can hedge against Euro interest rate increases. The assignment includes calculations for daily payments on futures contracts and explores interest rate swaps, along with explanations of market practices and risk mitigation strategies.

Running head: INTERNATIONAL FINANCIAL MANAGEMENT

International Financial Management

Name of the Student:

Name of the University:

Authors Note:

International Financial Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCIAL MANAGEMENT

1

Table of Contents

Part A:........................................................................................................................................3

1.a Calculating the new exchange rate EURUSD:.....................................................................3

1.b Calculating the exchange rate GBPEUR:............................................................................3

1.c Explaining the relationship and triangular arbitrage:...........................................................3

2.a Indicating which currency will have the higher rate of inflation in 2017:...........................4

2.b Calculating the change in real value of dollar, where relevant implications of the change:4

2.c Identifying the implications of a change in the real exchange rate of a currency:...............5

2.d Explaining the expect interest rate in the US to be higher than Euro:.................................5

2.e Explaining the why there is no difference in the interest rates of government bonds of any

two countries in the Euro:..........................................................................................................6

Part B:.........................................................................................................................................6

5.a Calculating the Net Pay-out from the purchased call option at the strike price of 67 pence

for the following possible maturity prices 55p, 60p,65p,70p,75p:............................................6

5.b Calculating the Net Pay-out from the purchased put option at the strike price of 67 pence

for the following possible maturity prices 55p, 60p,65p,70p,75p:............................................7

5c. Calculate the total cost of the dollar for the questions:........................................................7

5.d Outlining the advantages and disadvantages of purchasing a call and put for the MNCs

importing from the US:..............................................................................................................8

6.a Explaining why selling futures contract on French bonds would reduce the effect on an

increase in Euro interest rates:...................................................................................................8

6.b Calculating the daily payments and receipts on the future contract given on the bonds:....9

6.c Explaining the market insists on daily settlement:...............................................................9

6.d Explaining how it might work in an interest rate swap:.....................................................10

6.e Calculating the net profit or loss per unit on maturity prices:............................................10

1

Table of Contents

Part A:........................................................................................................................................3

1.a Calculating the new exchange rate EURUSD:.....................................................................3

1.b Calculating the exchange rate GBPEUR:............................................................................3

1.c Explaining the relationship and triangular arbitrage:...........................................................3

2.a Indicating which currency will have the higher rate of inflation in 2017:...........................4

2.b Calculating the change in real value of dollar, where relevant implications of the change:4

2.c Identifying the implications of a change in the real exchange rate of a currency:...............5

2.d Explaining the expect interest rate in the US to be higher than Euro:.................................5

2.e Explaining the why there is no difference in the interest rates of government bonds of any

two countries in the Euro:..........................................................................................................6

Part B:.........................................................................................................................................6

5.a Calculating the Net Pay-out from the purchased call option at the strike price of 67 pence

for the following possible maturity prices 55p, 60p,65p,70p,75p:............................................6

5.b Calculating the Net Pay-out from the purchased put option at the strike price of 67 pence

for the following possible maturity prices 55p, 60p,65p,70p,75p:............................................7

5c. Calculate the total cost of the dollar for the questions:........................................................7

5.d Outlining the advantages and disadvantages of purchasing a call and put for the MNCs

importing from the US:..............................................................................................................8

6.a Explaining why selling futures contract on French bonds would reduce the effect on an

increase in Euro interest rates:...................................................................................................8

6.b Calculating the daily payments and receipts on the future contract given on the bonds:....9

6.c Explaining the market insists on daily settlement:...............................................................9

6.d Explaining how it might work in an interest rate swap:.....................................................10

6.e Calculating the net profit or loss per unit on maturity prices:............................................10

INTERNATIONAL FINANCIAL MANAGEMENT

2

6.f Explaining how the option contract protects against the interest rate rise:........................11

References:...............................................................................................................................12

2

6.f Explaining how the option contract protects against the interest rate rise:........................11

References:...............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCIAL MANAGEMENT

3

Part A:

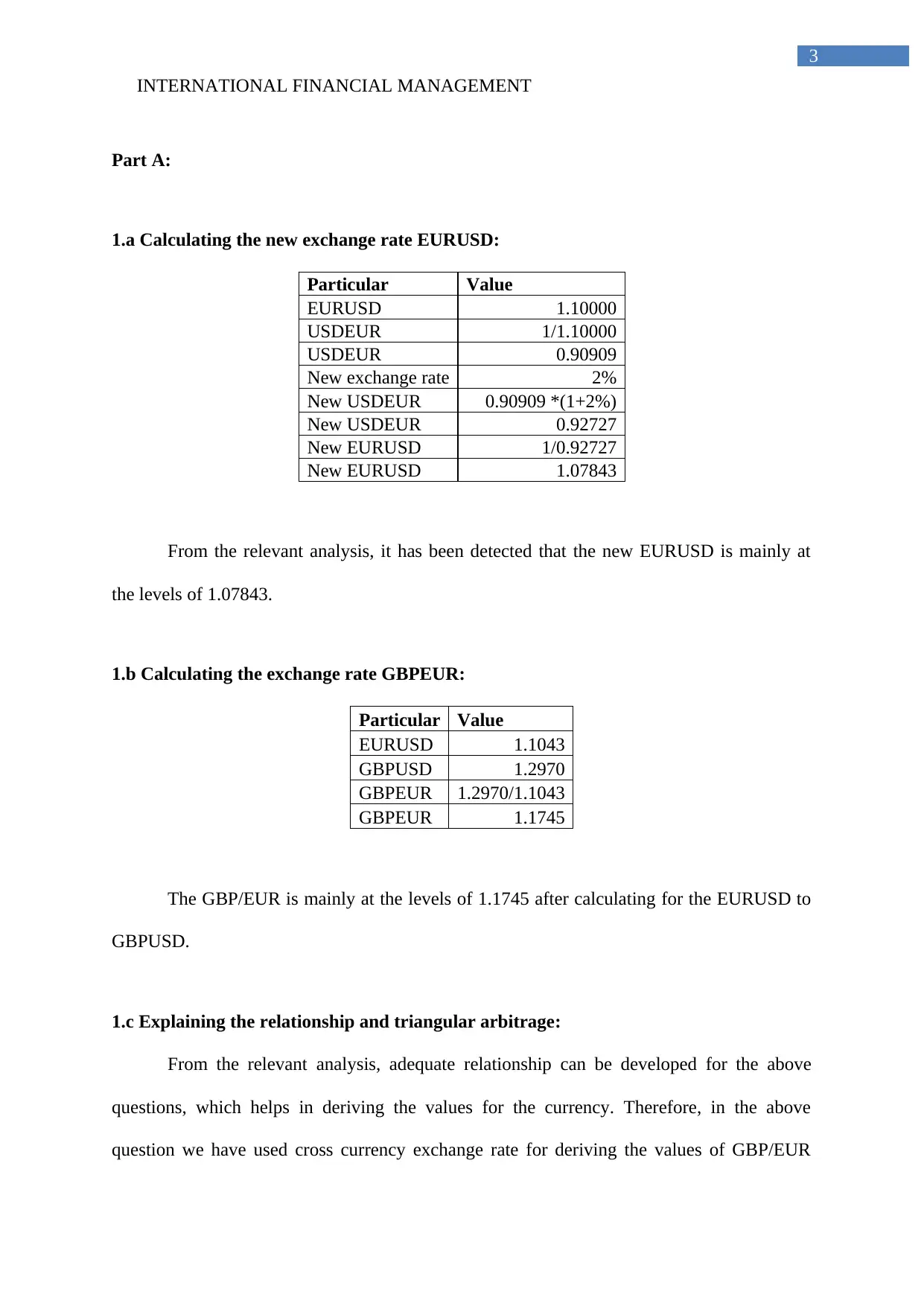

1.a Calculating the new exchange rate EURUSD:

Particular Value

EURUSD 1.10000

USDEUR 1/1.10000

USDEUR 0.90909

New exchange rate 2%

New USDEUR 0.90909 *(1+2%)

New USDEUR 0.92727

New EURUSD 1/0.92727

New EURUSD 1.07843

From the relevant analysis, it has been detected that the new EURUSD is mainly at

the levels of 1.07843.

1.b Calculating the exchange rate GBPEUR:

Particular Value

EURUSD 1.1043

GBPUSD 1.2970

GBPEUR 1.2970/1.1043

GBPEUR 1.1745

The GBP/EUR is mainly at the levels of 1.1745 after calculating for the EURUSD to

GBPUSD.

1.c Explaining the relationship and triangular arbitrage:

From the relevant analysis, adequate relationship can be developed for the above

questions, which helps in deriving the values for the currency. Therefore, in the above

question we have used cross currency exchange rate for deriving the values of GBP/EUR

3

Part A:

1.a Calculating the new exchange rate EURUSD:

Particular Value

EURUSD 1.10000

USDEUR 1/1.10000

USDEUR 0.90909

New exchange rate 2%

New USDEUR 0.90909 *(1+2%)

New USDEUR 0.92727

New EURUSD 1/0.92727

New EURUSD 1.07843

From the relevant analysis, it has been detected that the new EURUSD is mainly at

the levels of 1.07843.

1.b Calculating the exchange rate GBPEUR:

Particular Value

EURUSD 1.1043

GBPUSD 1.2970

GBPEUR 1.2970/1.1043

GBPEUR 1.1745

The GBP/EUR is mainly at the levels of 1.1745 after calculating for the EURUSD to

GBPUSD.

1.c Explaining the relationship and triangular arbitrage:

From the relevant analysis, adequate relationship can be developed for the above

questions, which helps in deriving the values for the currency. Therefore, in the above

question we have used cross currency exchange rate for deriving the values of GBP/EUR

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCIAL MANAGEMENT

4

after deriving the values from EURUSD and GBPUSD. The cross-currency values are mainly

calculated as there is a relationship between the values of EURUSD and GBPUSD., which

would help in deriving the appropriate valuation of the currency GBP/EUR. Thus, the

utilisation of the cross-currency calculation would eventually help in determining the third

currency value, which can be used in the calculation of triangular arbitrage. Consequently,

the method might help in determining the appropriate level of currency value over the period

of time. Therefore, from the relevant analysis, it has been detected that the Triangular

arbitrage can incur either profit or loss for the investors utilising the method for investments

in the currency market (Della, Ramadorai and Sarno 2016).

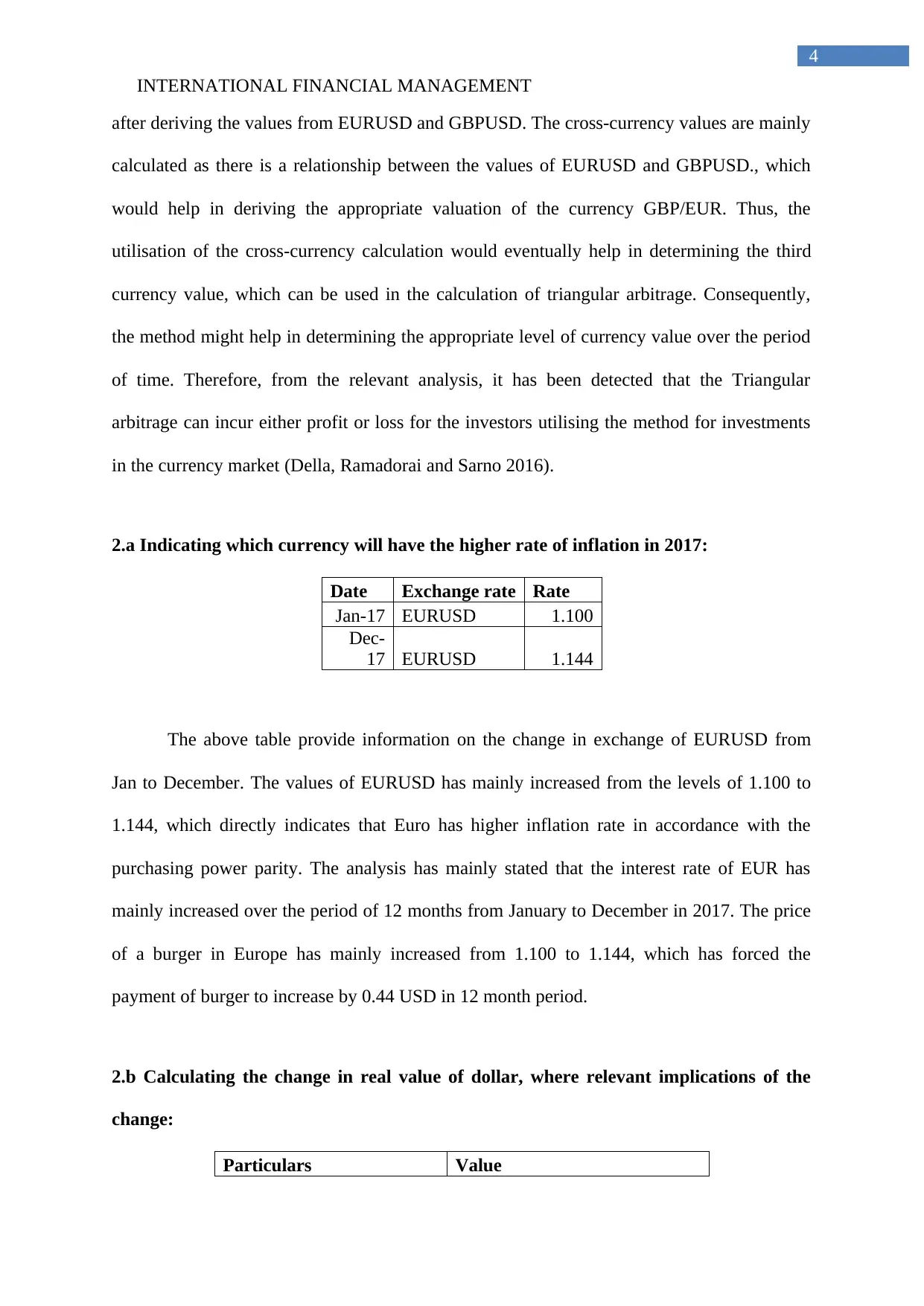

2.a Indicating which currency will have the higher rate of inflation in 2017:

Date Exchange rate Rate

Jan-17 EURUSD 1.100

Dec-

17 EURUSD 1.144

The above table provide information on the change in exchange of EURUSD from

Jan to December. The values of EURUSD has mainly increased from the levels of 1.100 to

1.144, which directly indicates that Euro has higher inflation rate in accordance with the

purchasing power parity. The analysis has mainly stated that the interest rate of EUR has

mainly increased over the period of 12 months from January to December in 2017. The price

of a burger in Europe has mainly increased from 1.100 to 1.144, which has forced the

payment of burger to increase by 0.44 USD in 12 month period.

2.b Calculating the change in real value of dollar, where relevant implications of the

change:

Particulars Value

4

after deriving the values from EURUSD and GBPUSD. The cross-currency values are mainly

calculated as there is a relationship between the values of EURUSD and GBPUSD., which

would help in deriving the appropriate valuation of the currency GBP/EUR. Thus, the

utilisation of the cross-currency calculation would eventually help in determining the third

currency value, which can be used in the calculation of triangular arbitrage. Consequently,

the method might help in determining the appropriate level of currency value over the period

of time. Therefore, from the relevant analysis, it has been detected that the Triangular

arbitrage can incur either profit or loss for the investors utilising the method for investments

in the currency market (Della, Ramadorai and Sarno 2016).

2.a Indicating which currency will have the higher rate of inflation in 2017:

Date Exchange rate Rate

Jan-17 EURUSD 1.100

Dec-

17 EURUSD 1.144

The above table provide information on the change in exchange of EURUSD from

Jan to December. The values of EURUSD has mainly increased from the levels of 1.100 to

1.144, which directly indicates that Euro has higher inflation rate in accordance with the

purchasing power parity. The analysis has mainly stated that the interest rate of EUR has

mainly increased over the period of 12 months from January to December in 2017. The price

of a burger in Europe has mainly increased from 1.100 to 1.144, which has forced the

payment of burger to increase by 0.44 USD in 12 month period.

2.b Calculating the change in real value of dollar, where relevant implications of the

change:

Particulars Value

INTERNATIONAL FINANCIAL MANAGEMENT

5

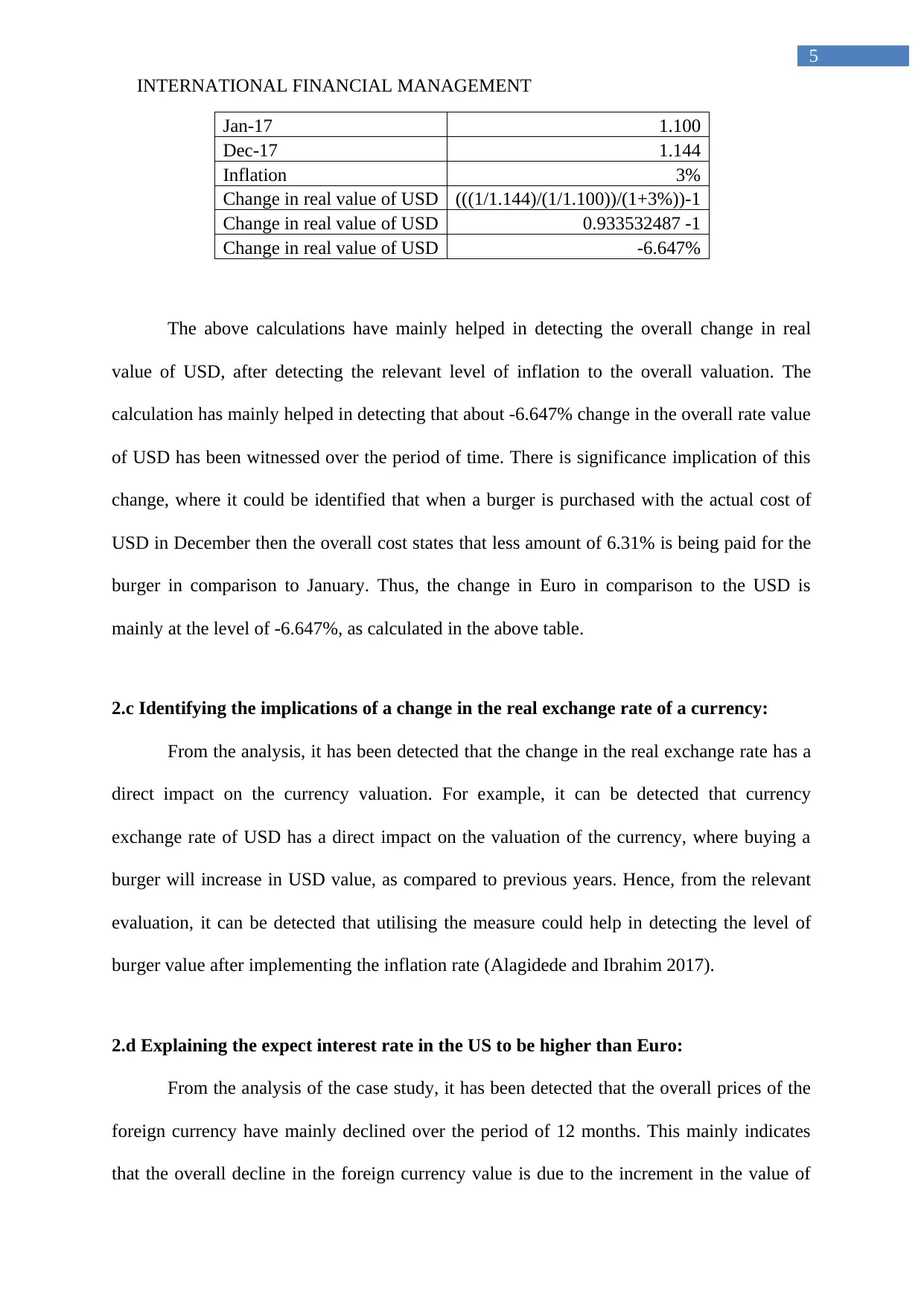

Jan-17 1.100

Dec-17 1.144

Inflation 3%

Change in real value of USD (((1/1.144)/(1/1.100))/(1+3%))-1

Change in real value of USD 0.933532487 -1

Change in real value of USD -6.647%

The above calculations have mainly helped in detecting the overall change in real

value of USD, after detecting the relevant level of inflation to the overall valuation. The

calculation has mainly helped in detecting that about -6.647% change in the overall rate value

of USD has been witnessed over the period of time. There is significance implication of this

change, where it could be identified that when a burger is purchased with the actual cost of

USD in December then the overall cost states that less amount of 6.31% is being paid for the

burger in comparison to January. Thus, the change in Euro in comparison to the USD is

mainly at the level of -6.647%, as calculated in the above table.

2.c Identifying the implications of a change in the real exchange rate of a currency:

From the analysis, it has been detected that the change in the real exchange rate has a

direct impact on the currency valuation. For example, it can be detected that currency

exchange rate of USD has a direct impact on the valuation of the currency, where buying a

burger will increase in USD value, as compared to previous years. Hence, from the relevant

evaluation, it can be detected that utilising the measure could help in detecting the level of

burger value after implementing the inflation rate (Alagidede and Ibrahim 2017).

2.d Explaining the expect interest rate in the US to be higher than Euro:

From the analysis of the case study, it has been detected that the overall prices of the

foreign currency have mainly declined over the period of 12 months. This mainly indicates

that the overall decline in the foreign currency value is due to the increment in the value of

5

Jan-17 1.100

Dec-17 1.144

Inflation 3%

Change in real value of USD (((1/1.144)/(1/1.100))/(1+3%))-1

Change in real value of USD 0.933532487 -1

Change in real value of USD -6.647%

The above calculations have mainly helped in detecting the overall change in real

value of USD, after detecting the relevant level of inflation to the overall valuation. The

calculation has mainly helped in detecting that about -6.647% change in the overall rate value

of USD has been witnessed over the period of time. There is significance implication of this

change, where it could be identified that when a burger is purchased with the actual cost of

USD in December then the overall cost states that less amount of 6.31% is being paid for the

burger in comparison to January. Thus, the change in Euro in comparison to the USD is

mainly at the level of -6.647%, as calculated in the above table.

2.c Identifying the implications of a change in the real exchange rate of a currency:

From the analysis, it has been detected that the change in the real exchange rate has a

direct impact on the currency valuation. For example, it can be detected that currency

exchange rate of USD has a direct impact on the valuation of the currency, where buying a

burger will increase in USD value, as compared to previous years. Hence, from the relevant

evaluation, it can be detected that utilising the measure could help in detecting the level of

burger value after implementing the inflation rate (Alagidede and Ibrahim 2017).

2.d Explaining the expect interest rate in the US to be higher than Euro:

From the analysis of the case study, it has been detected that the overall prices of the

foreign currency have mainly declined over the period of 12 months. This mainly indicates

that the overall decline in the foreign currency value is due to the increment in the value of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCIAL MANAGEMENT

6

local currency. This indicates that the USD has depreciated in comparison to the EUR, which

directly indicates that the inflation rate in US has increased during the period of 12 months.

This increment in the real interest rate has mainly declined the valuation of the currency,

which has led to the increment in the value of USD from 1.100 in January to 1.144 in

December.

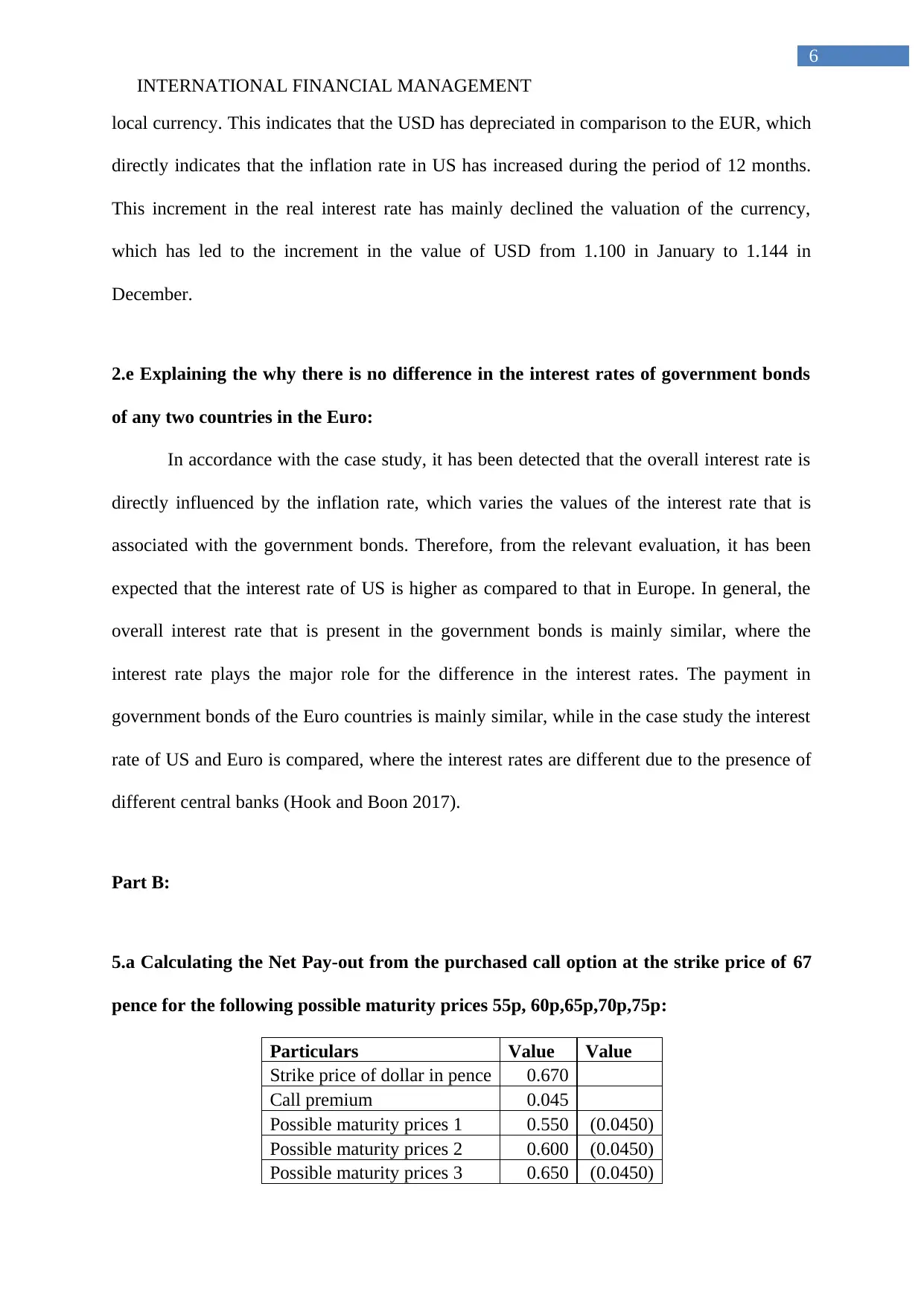

2.e Explaining the why there is no difference in the interest rates of government bonds

of any two countries in the Euro:

In accordance with the case study, it has been detected that the overall interest rate is

directly influenced by the inflation rate, which varies the values of the interest rate that is

associated with the government bonds. Therefore, from the relevant evaluation, it has been

expected that the interest rate of US is higher as compared to that in Europe. In general, the

overall interest rate that is present in the government bonds is mainly similar, where the

interest rate plays the major role for the difference in the interest rates. The payment in

government bonds of the Euro countries is mainly similar, while in the case study the interest

rate of US and Euro is compared, where the interest rates are different due to the presence of

different central banks (Hook and Boon 2017).

Part B:

5.a Calculating the Net Pay-out from the purchased call option at the strike price of 67

pence for the following possible maturity prices 55p, 60p,65p,70p,75p:

Particulars Value Value

Strike price of dollar in pence 0.670

Call premium 0.045

Possible maturity prices 1 0.550 (0.0450)

Possible maturity prices 2 0.600 (0.0450)

Possible maturity prices 3 0.650 (0.0450)

6

local currency. This indicates that the USD has depreciated in comparison to the EUR, which

directly indicates that the inflation rate in US has increased during the period of 12 months.

This increment in the real interest rate has mainly declined the valuation of the currency,

which has led to the increment in the value of USD from 1.100 in January to 1.144 in

December.

2.e Explaining the why there is no difference in the interest rates of government bonds

of any two countries in the Euro:

In accordance with the case study, it has been detected that the overall interest rate is

directly influenced by the inflation rate, which varies the values of the interest rate that is

associated with the government bonds. Therefore, from the relevant evaluation, it has been

expected that the interest rate of US is higher as compared to that in Europe. In general, the

overall interest rate that is present in the government bonds is mainly similar, where the

interest rate plays the major role for the difference in the interest rates. The payment in

government bonds of the Euro countries is mainly similar, while in the case study the interest

rate of US and Euro is compared, where the interest rates are different due to the presence of

different central banks (Hook and Boon 2017).

Part B:

5.a Calculating the Net Pay-out from the purchased call option at the strike price of 67

pence for the following possible maturity prices 55p, 60p,65p,70p,75p:

Particulars Value Value

Strike price of dollar in pence 0.670

Call premium 0.045

Possible maturity prices 1 0.550 (0.0450)

Possible maturity prices 2 0.600 (0.0450)

Possible maturity prices 3 0.650 (0.0450)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCIAL MANAGEMENT

7

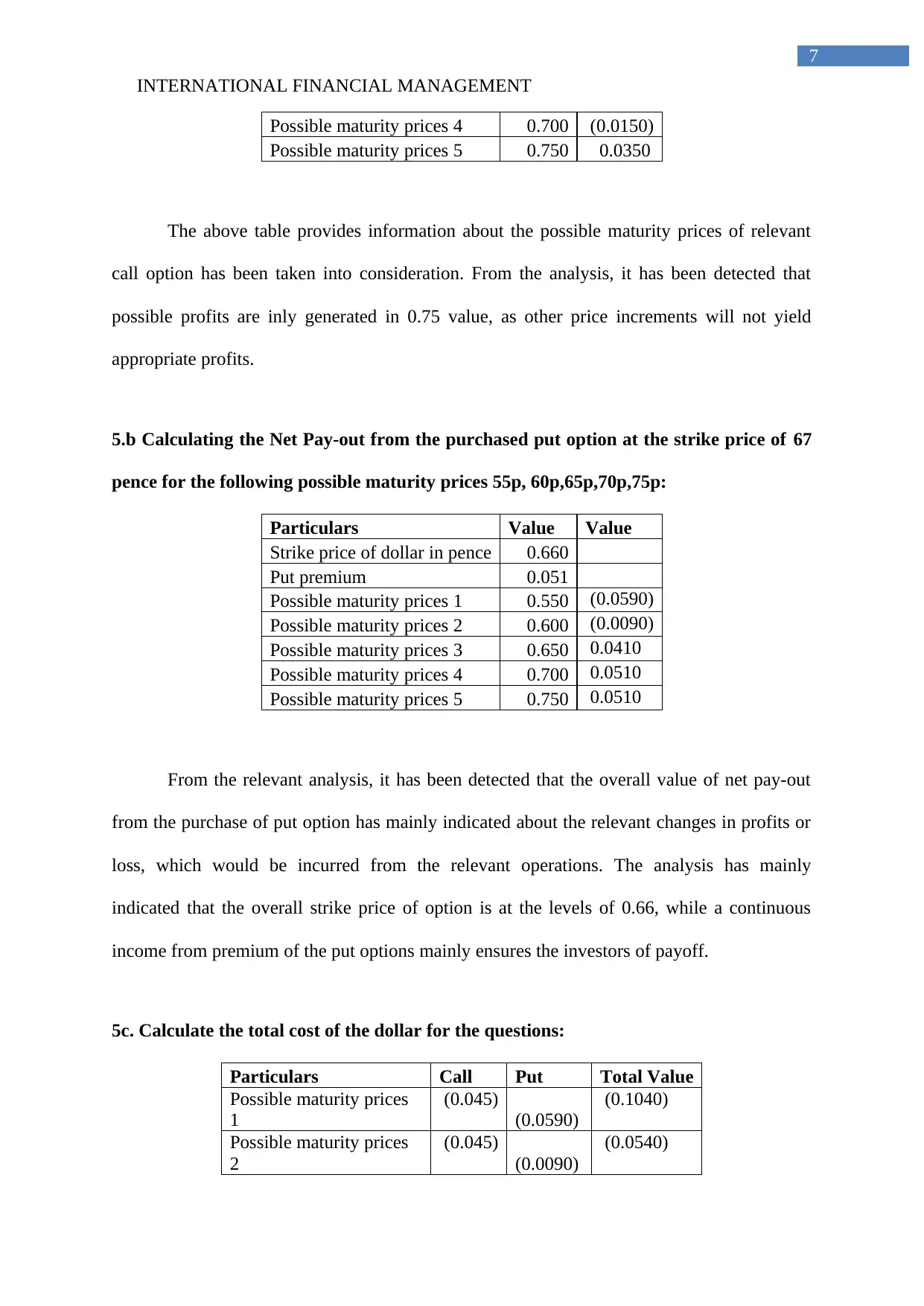

Possible maturity prices 4 0.700 (0.0150)

Possible maturity prices 5 0.750 0.0350

The above table provides information about the possible maturity prices of relevant

call option has been taken into consideration. From the analysis, it has been detected that

possible profits are inly generated in 0.75 value, as other price increments will not yield

appropriate profits.

5.b Calculating the Net Pay-out from the purchased put option at the strike price of 67

pence for the following possible maturity prices 55p, 60p,65p,70p,75p:

Particulars Value Value

Strike price of dollar in pence 0.660

Put premium 0.051

Possible maturity prices 1 0.550 (0.0590)

Possible maturity prices 2 0.600 (0.0090)

Possible maturity prices 3 0.650 0.0410

Possible maturity prices 4 0.700 0.0510

Possible maturity prices 5 0.750 0.0510

From the relevant analysis, it has been detected that the overall value of net pay-out

from the purchase of put option has mainly indicated about the relevant changes in profits or

loss, which would be incurred from the relevant operations. The analysis has mainly

indicated that the overall strike price of option is at the levels of 0.66, while a continuous

income from premium of the put options mainly ensures the investors of payoff.

5c. Calculate the total cost of the dollar for the questions:

Particulars Call Put Total Value

Possible maturity prices

1

(0.045)

(0.0590)

(0.1040)

Possible maturity prices

2

(0.045)

(0.0090)

(0.0540)

7

Possible maturity prices 4 0.700 (0.0150)

Possible maturity prices 5 0.750 0.0350

The above table provides information about the possible maturity prices of relevant

call option has been taken into consideration. From the analysis, it has been detected that

possible profits are inly generated in 0.75 value, as other price increments will not yield

appropriate profits.

5.b Calculating the Net Pay-out from the purchased put option at the strike price of 67

pence for the following possible maturity prices 55p, 60p,65p,70p,75p:

Particulars Value Value

Strike price of dollar in pence 0.660

Put premium 0.051

Possible maturity prices 1 0.550 (0.0590)

Possible maturity prices 2 0.600 (0.0090)

Possible maturity prices 3 0.650 0.0410

Possible maturity prices 4 0.700 0.0510

Possible maturity prices 5 0.750 0.0510

From the relevant analysis, it has been detected that the overall value of net pay-out

from the purchase of put option has mainly indicated about the relevant changes in profits or

loss, which would be incurred from the relevant operations. The analysis has mainly

indicated that the overall strike price of option is at the levels of 0.66, while a continuous

income from premium of the put options mainly ensures the investors of payoff.

5c. Calculate the total cost of the dollar for the questions:

Particulars Call Put Total Value

Possible maturity prices

1

(0.045)

(0.0590)

(0.1040)

Possible maturity prices

2

(0.045)

(0.0090)

(0.0540)

INTERNATIONAL FINANCIAL MANAGEMENT

8

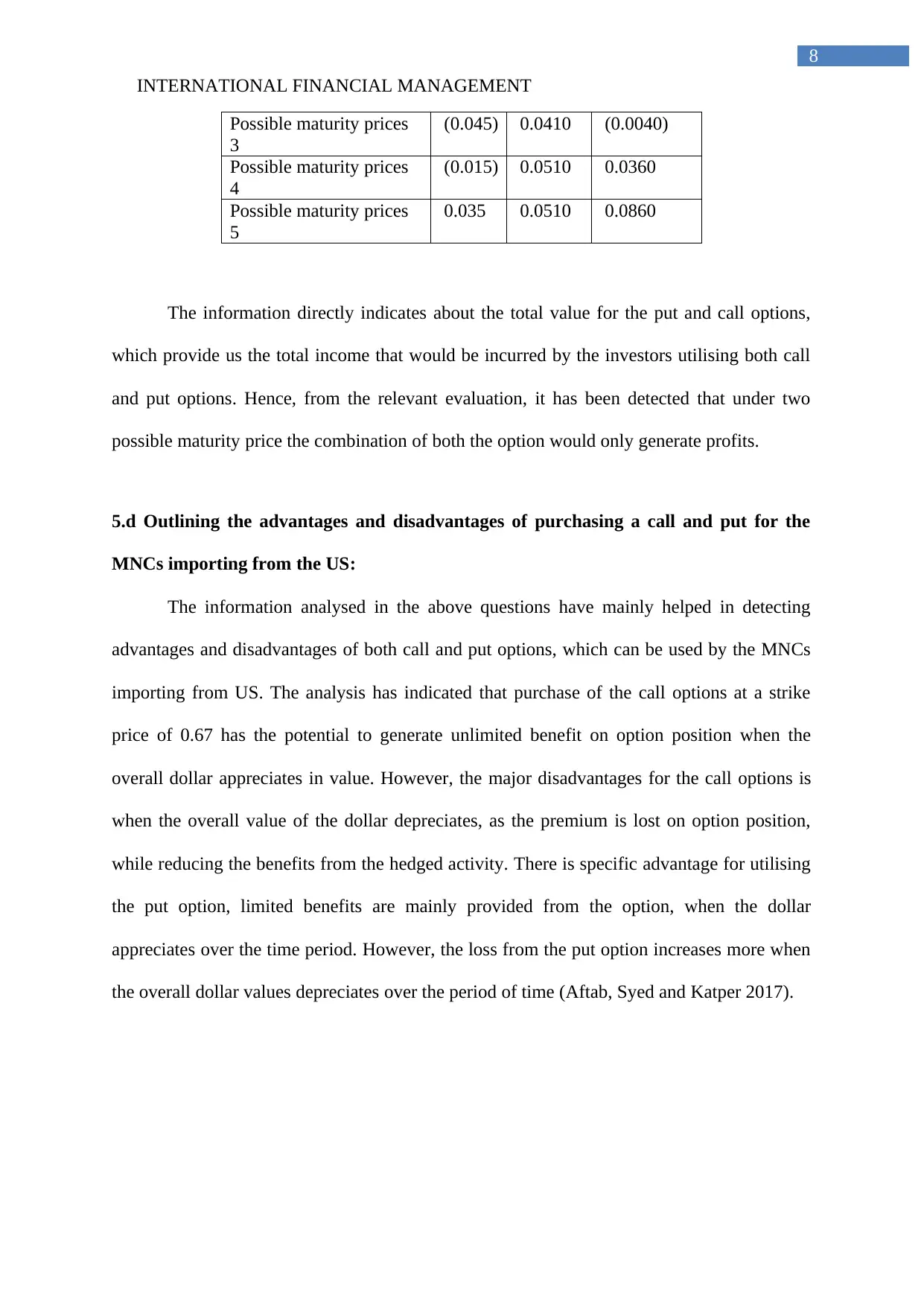

Possible maturity prices

3

(0.045) 0.0410 (0.0040)

Possible maturity prices

4

(0.015) 0.0510 0.0360

Possible maturity prices

5

0.035 0.0510 0.0860

The information directly indicates about the total value for the put and call options,

which provide us the total income that would be incurred by the investors utilising both call

and put options. Hence, from the relevant evaluation, it has been detected that under two

possible maturity price the combination of both the option would only generate profits.

5.d Outlining the advantages and disadvantages of purchasing a call and put for the

MNCs importing from the US:

The information analysed in the above questions have mainly helped in detecting

advantages and disadvantages of both call and put options, which can be used by the MNCs

importing from US. The analysis has indicated that purchase of the call options at a strike

price of 0.67 has the potential to generate unlimited benefit on option position when the

overall dollar appreciates in value. However, the major disadvantages for the call options is

when the overall value of the dollar depreciates, as the premium is lost on option position,

while reducing the benefits from the hedged activity. There is specific advantage for utilising

the put option, limited benefits are mainly provided from the option, when the dollar

appreciates over the time period. However, the loss from the put option increases more when

the overall dollar values depreciates over the period of time (Aftab, Syed and Katper 2017).

8

Possible maturity prices

3

(0.045) 0.0410 (0.0040)

Possible maturity prices

4

(0.015) 0.0510 0.0360

Possible maturity prices

5

0.035 0.0510 0.0860

The information directly indicates about the total value for the put and call options,

which provide us the total income that would be incurred by the investors utilising both call

and put options. Hence, from the relevant evaluation, it has been detected that under two

possible maturity price the combination of both the option would only generate profits.

5.d Outlining the advantages and disadvantages of purchasing a call and put for the

MNCs importing from the US:

The information analysed in the above questions have mainly helped in detecting

advantages and disadvantages of both call and put options, which can be used by the MNCs

importing from US. The analysis has indicated that purchase of the call options at a strike

price of 0.67 has the potential to generate unlimited benefit on option position when the

overall dollar appreciates in value. However, the major disadvantages for the call options is

when the overall value of the dollar depreciates, as the premium is lost on option position,

while reducing the benefits from the hedged activity. There is specific advantage for utilising

the put option, limited benefits are mainly provided from the option, when the dollar

appreciates over the time period. However, the loss from the put option increases more when

the overall dollar values depreciates over the period of time (Aftab, Syed and Katper 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCIAL MANAGEMENT

9

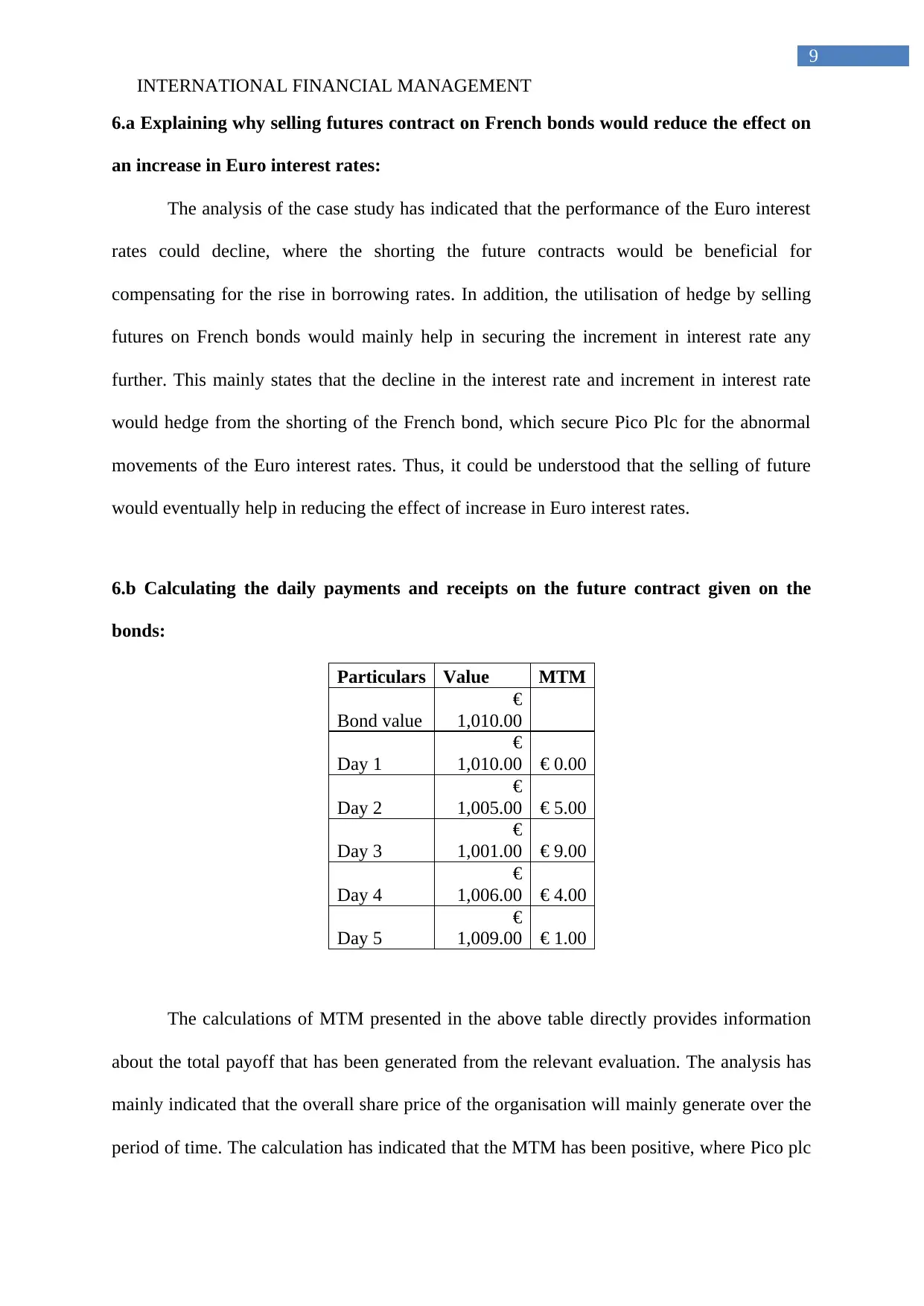

6.a Explaining why selling futures contract on French bonds would reduce the effect on

an increase in Euro interest rates:

The analysis of the case study has indicated that the performance of the Euro interest

rates could decline, where the shorting the future contracts would be beneficial for

compensating for the rise in borrowing rates. In addition, the utilisation of hedge by selling

futures on French bonds would mainly help in securing the increment in interest rate any

further. This mainly states that the decline in the interest rate and increment in interest rate

would hedge from the shorting of the French bond, which secure Pico Plc for the abnormal

movements of the Euro interest rates. Thus, it could be understood that the selling of future

would eventually help in reducing the effect of increase in Euro interest rates.

6.b Calculating the daily payments and receipts on the future contract given on the

bonds:

Particulars Value MTM

Bond value

€

1,010.00

Day 1

€

1,010.00 € 0.00

Day 2

€

1,005.00 € 5.00

Day 3

€

1,001.00 € 9.00

Day 4

€

1,006.00 € 4.00

Day 5

€

1,009.00 € 1.00

The calculations of MTM presented in the above table directly provides information

about the total payoff that has been generated from the relevant evaluation. The analysis has

mainly indicated that the overall share price of the organisation will mainly generate over the

period of time. The calculation has indicated that the MTM has been positive, where Pico plc

9

6.a Explaining why selling futures contract on French bonds would reduce the effect on

an increase in Euro interest rates:

The analysis of the case study has indicated that the performance of the Euro interest

rates could decline, where the shorting the future contracts would be beneficial for

compensating for the rise in borrowing rates. In addition, the utilisation of hedge by selling

futures on French bonds would mainly help in securing the increment in interest rate any

further. This mainly states that the decline in the interest rate and increment in interest rate

would hedge from the shorting of the French bond, which secure Pico Plc for the abnormal

movements of the Euro interest rates. Thus, it could be understood that the selling of future

would eventually help in reducing the effect of increase in Euro interest rates.

6.b Calculating the daily payments and receipts on the future contract given on the

bonds:

Particulars Value MTM

Bond value

€

1,010.00

Day 1

€

1,010.00 € 0.00

Day 2

€

1,005.00 € 5.00

Day 3

€

1,001.00 € 9.00

Day 4

€

1,006.00 € 4.00

Day 5

€

1,009.00 € 1.00

The calculations of MTM presented in the above table directly provides information

about the total payoff that has been generated from the relevant evaluation. The analysis has

mainly indicated that the overall share price of the organisation will mainly generate over the

period of time. The calculation has indicated that the MTM has been positive, where Pico plc

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCIAL MANAGEMENT

10

will only receive cash from the futures contract on bond rather paying anything during the 5-

day trade.

6.c Explaining the market insists on daily settlement:

The market insists on the daily settlement is relevantly positive, as it allows both the

exchange and investors to evaluate their current investment exposures and reduce the chance

of high debt. The daily settlement measure mainly reduces the chance of unethical measure

that might be conducted by investors while not providing relevant leverage for the loss

conducted from their trade.

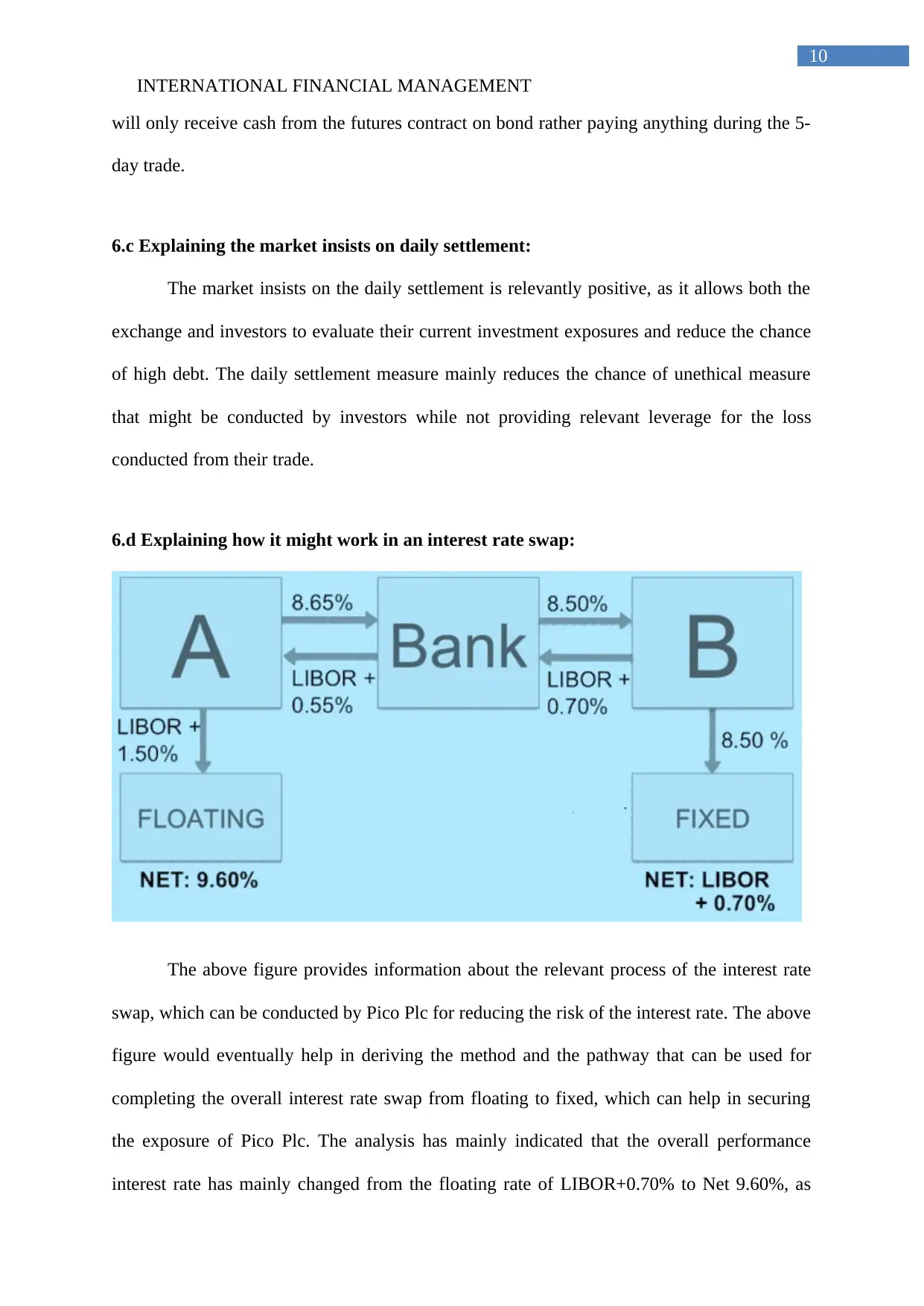

6.d Explaining how it might work in an interest rate swap:

The above figure provides information about the relevant process of the interest rate

swap, which can be conducted by Pico Plc for reducing the risk of the interest rate. The above

figure would eventually help in deriving the method and the pathway that can be used for

completing the overall interest rate swap from floating to fixed, which can help in securing

the exposure of Pico Plc. The analysis has mainly indicated that the overall performance

interest rate has mainly changed from the floating rate of LIBOR+0.70% to Net 9.60%, as

10

will only receive cash from the futures contract on bond rather paying anything during the 5-

day trade.

6.c Explaining the market insists on daily settlement:

The market insists on the daily settlement is relevantly positive, as it allows both the

exchange and investors to evaluate their current investment exposures and reduce the chance

of high debt. The daily settlement measure mainly reduces the chance of unethical measure

that might be conducted by investors while not providing relevant leverage for the loss

conducted from their trade.

6.d Explaining how it might work in an interest rate swap:

The above figure provides information about the relevant process of the interest rate

swap, which can be conducted by Pico Plc for reducing the risk of the interest rate. The above

figure would eventually help in deriving the method and the pathway that can be used for

completing the overall interest rate swap from floating to fixed, which can help in securing

the exposure of Pico Plc. The analysis has mainly indicated that the overall performance

interest rate has mainly changed from the floating rate of LIBOR+0.70% to Net 9.60%, as

INTERNATIONAL FINANCIAL MANAGEMENT

11

depicted in the above figure. The process can be done only with a help pf a bank, who needs

to behave as the intermediary between two companies. Thus, the process would ensure Pico

Plc to transfer their floating rate to other company with fixed rate (Benos, Payne and Vasios

2018).

6.e Calculating the net profit or loss per unit on maturity prices:

Particulars Value Value

Strike price of dollar in pence € 1,008.00

Put premium € 4.00

Possible maturity prices 1 € 985.00 19.0000

Possible maturity prices 2 € 1,000.00 4.0000

Possible maturity prices 3 € 1,015.00 (4.0000)

Possible maturity prices 4 € 1,020.00 (4.0000)

The information provided in the above table directly depicts about the put option that

has been taken into consideration for Pico Plc, where the organisation can secure the overall

risk exposure. The analysis has mainly indicated that the loss of € 4.00 is mainly indicated in

the above table. Therefore, it could be understood that the risk involved in put options can be

controlled, while the profits from the exposure is relevantly unlimited.

6.f Explaining how the option contract protects against the interest rate rise:

The put option contract mainly indicates about the level of risk exposure that can be

reduced from the exposure of the interest rates. The calculation of the bond directly includes

the valuation of the interest rate, which directly helps in determining the appropriate level of

bond price. In addition, the increment in interest rate directly reduces the overall bond prices

and vice versa. Thus, it is beneficial for buying the put option for appropriately protecting the

against the interest rate rise (Du, Tepper and Verdelhan 2018).

11

depicted in the above figure. The process can be done only with a help pf a bank, who needs

to behave as the intermediary between two companies. Thus, the process would ensure Pico

Plc to transfer their floating rate to other company with fixed rate (Benos, Payne and Vasios

2018).

6.e Calculating the net profit or loss per unit on maturity prices:

Particulars Value Value

Strike price of dollar in pence € 1,008.00

Put premium € 4.00

Possible maturity prices 1 € 985.00 19.0000

Possible maturity prices 2 € 1,000.00 4.0000

Possible maturity prices 3 € 1,015.00 (4.0000)

Possible maturity prices 4 € 1,020.00 (4.0000)

The information provided in the above table directly depicts about the put option that

has been taken into consideration for Pico Plc, where the organisation can secure the overall

risk exposure. The analysis has mainly indicated that the loss of € 4.00 is mainly indicated in

the above table. Therefore, it could be understood that the risk involved in put options can be

controlled, while the profits from the exposure is relevantly unlimited.

6.f Explaining how the option contract protects against the interest rate rise:

The put option contract mainly indicates about the level of risk exposure that can be

reduced from the exposure of the interest rates. The calculation of the bond directly includes

the valuation of the interest rate, which directly helps in determining the appropriate level of

bond price. In addition, the increment in interest rate directly reduces the overall bond prices

and vice versa. Thus, it is beneficial for buying the put option for appropriately protecting the

against the interest rate rise (Du, Tepper and Verdelhan 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.