International Financial Management Assignment Report Analysis

VerifiedAdded on 2023/01/09

|11

|2364

|69

Report

AI Summary

This report delves into key aspects of international financial management, offering a comprehensive analysis of various techniques and concepts. It begins with a detailed examination of financial ratios for Green plc and Blue plc, including profitability, efficiency, and investor ratios, followed by a comparative analysis and recommendations. The report then moves on to the calculation of both market-value and book-value WACC for ART Co, highlighting the differences between the two and discussing the circumstances and limitations of WACC in investment appraisal. Finally, the report explores the objectives of working capital management and its central role in financial management, including optimization strategies for different products. The report is supported by references to relevant academic sources, providing a robust foundation for the analysis and conclusions presented.

International financial

management

management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

a) Computation of Ratios For Green plc and Blue plc:..............................................................3

(b): Comment on Ratios Computed and Recommendation:.......................................................5

(c). Limitation of Ratio analysis:................................................................................................5

TASK 2............................................................................................................................................6

(a). Computation of market-value WACC and book-value WACC of ART Co and comment

briefly on difference between the two values:............................................................................6

(b). Circumstances under which WACC used in investment appraisal and its limitations as a

discount rate could be overcome:...............................................................................................7

TASK 3............................................................................................................................................8

Objectives of working capital management and central role of it in financial management:....8

CONCLUSION...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

a) Computation of Ratios For Green plc and Blue plc:..............................................................3

(b): Comment on Ratios Computed and Recommendation:.......................................................5

(c). Limitation of Ratio analysis:................................................................................................5

TASK 2............................................................................................................................................6

(a). Computation of market-value WACC and book-value WACC of ART Co and comment

briefly on difference between the two values:............................................................................6

(b). Circumstances under which WACC used in investment appraisal and its limitations as a

discount rate could be overcome:...............................................................................................7

TASK 3............................................................................................................................................8

Objectives of working capital management and central role of it in financial management:....8

CONCLUSION...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

International financial management is wider field which covers multiple techniques and

methods to assess the actual performance of a corporation operating at international level.

Methods and techniques covered in it also help investors take feasible investment decisions

(Madura, 2020). The study coves multiple numerical and discussion about different aspects of

financial management like Ratios computation, analysis and is limitations, computation of

WACC etc. Further it covers discussion on objectives and aims of working-capital management

and its roles in financial management based on given case scenario.

MAIN BODY

TASK 1

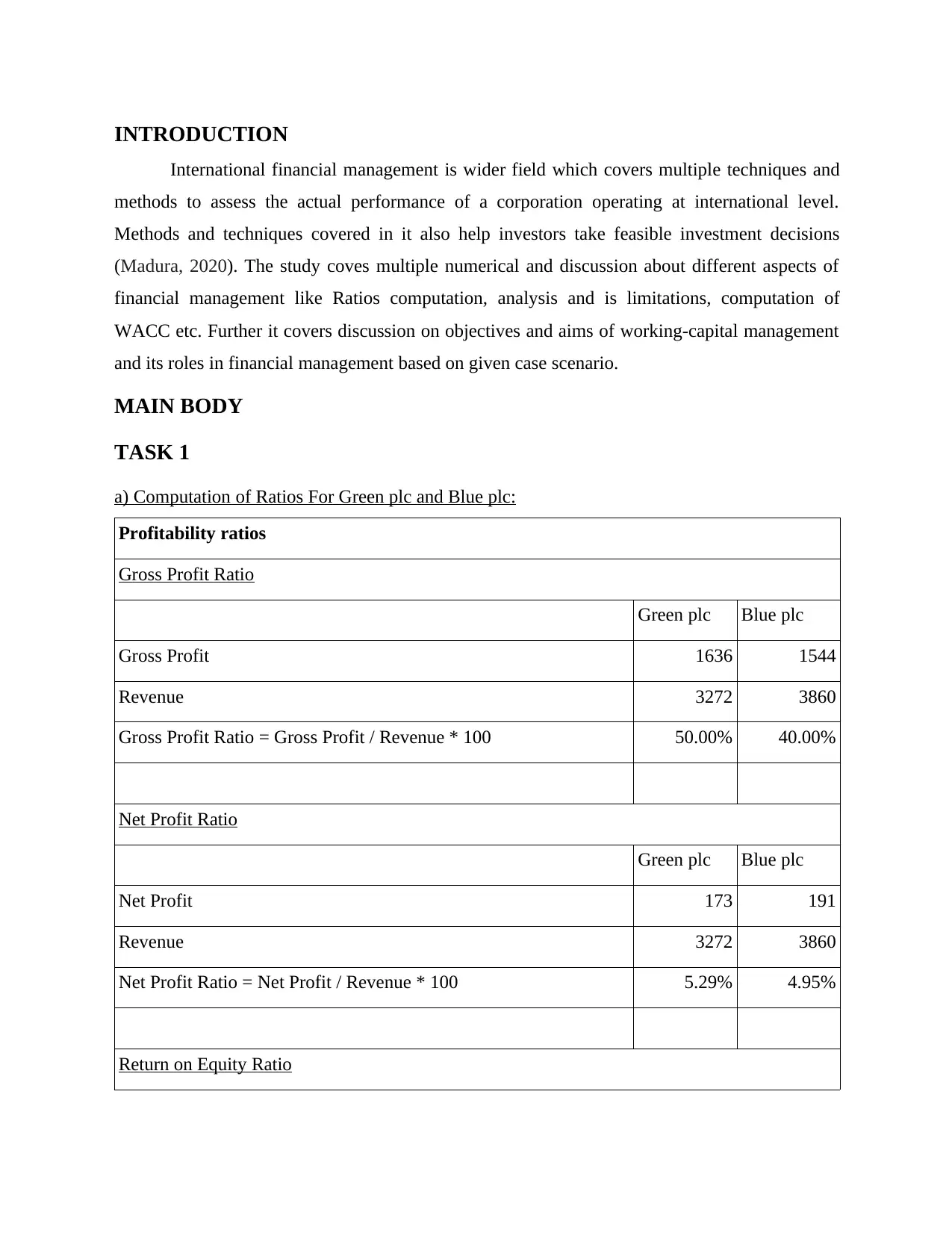

a) Computation of Ratios For Green plc and Blue plc:

Profitability ratios

Gross Profit Ratio

Green plc Blue plc

Gross Profit 1636 1544

Revenue 3272 3860

Gross Profit Ratio = Gross Profit / Revenue * 100 50.00% 40.00%

Net Profit Ratio

Green plc Blue plc

Net Profit 173 191

Revenue 3272 3860

Net Profit Ratio = Net Profit / Revenue * 100 5.29% 4.95%

Return on Equity Ratio

International financial management is wider field which covers multiple techniques and

methods to assess the actual performance of a corporation operating at international level.

Methods and techniques covered in it also help investors take feasible investment decisions

(Madura, 2020). The study coves multiple numerical and discussion about different aspects of

financial management like Ratios computation, analysis and is limitations, computation of

WACC etc. Further it covers discussion on objectives and aims of working-capital management

and its roles in financial management based on given case scenario.

MAIN BODY

TASK 1

a) Computation of Ratios For Green plc and Blue plc:

Profitability ratios

Gross Profit Ratio

Green plc Blue plc

Gross Profit 1636 1544

Revenue 3272 3860

Gross Profit Ratio = Gross Profit / Revenue * 100 50.00% 40.00%

Net Profit Ratio

Green plc Blue plc

Net Profit 173 191

Revenue 3272 3860

Net Profit Ratio = Net Profit / Revenue * 100 5.29% 4.95%

Return on Equity Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

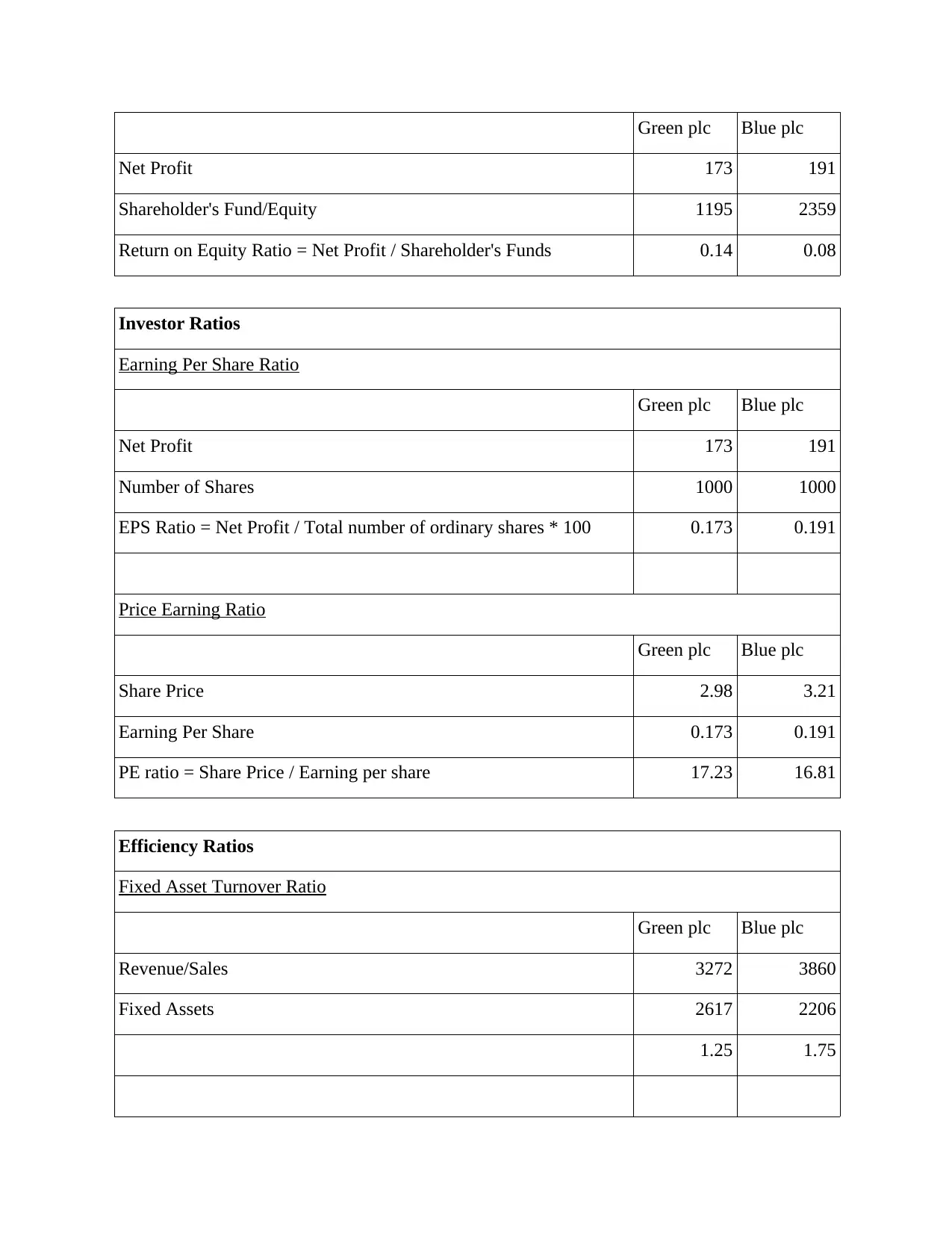

Green plc Blue plc

Net Profit 173 191

Shareholder's Fund/Equity 1195 2359

Return on Equity Ratio = Net Profit / Shareholder's Funds 0.14 0.08

Investor Ratios

Earning Per Share Ratio

Green plc Blue plc

Net Profit 173 191

Number of Shares 1000 1000

EPS Ratio = Net Profit / Total number of ordinary shares * 100 0.173 0.191

Price Earning Ratio

Green plc Blue plc

Share Price 2.98 3.21

Earning Per Share 0.173 0.191

PE ratio = Share Price / Earning per share 17.23 16.81

Efficiency Ratios

Fixed Asset Turnover Ratio

Green plc Blue plc

Revenue/Sales 3272 3860

Fixed Assets 2617 2206

1.25 1.75

Net Profit 173 191

Shareholder's Fund/Equity 1195 2359

Return on Equity Ratio = Net Profit / Shareholder's Funds 0.14 0.08

Investor Ratios

Earning Per Share Ratio

Green plc Blue plc

Net Profit 173 191

Number of Shares 1000 1000

EPS Ratio = Net Profit / Total number of ordinary shares * 100 0.173 0.191

Price Earning Ratio

Green plc Blue plc

Share Price 2.98 3.21

Earning Per Share 0.173 0.191

PE ratio = Share Price / Earning per share 17.23 16.81

Efficiency Ratios

Fixed Asset Turnover Ratio

Green plc Blue plc

Revenue/Sales 3272 3860

Fixed Assets 2617 2206

1.25 1.75

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

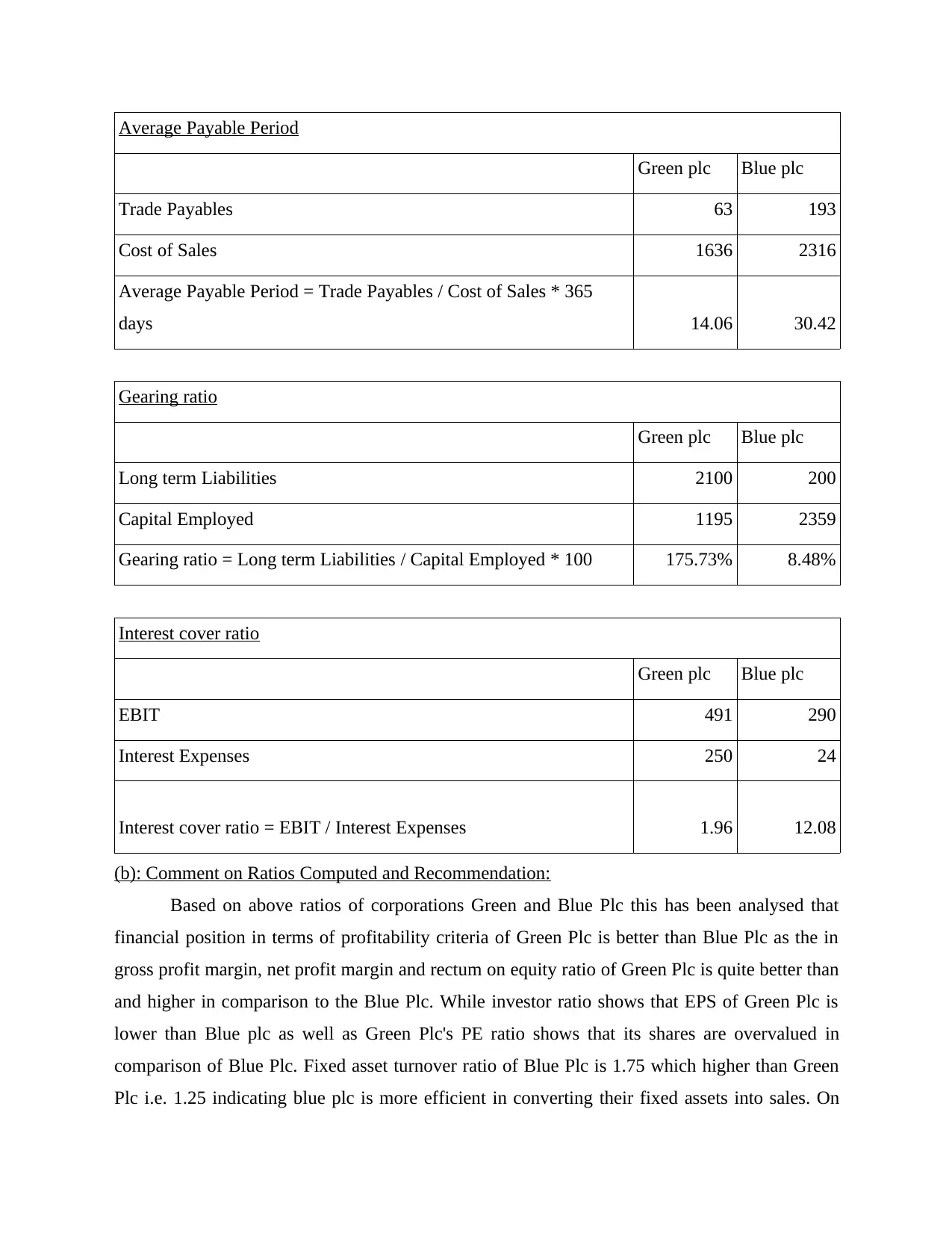

Average Payable Period

Green plc Blue plc

Trade Payables 63 193

Cost of Sales 1636 2316

Average Payable Period = Trade Payables / Cost of Sales * 365

days 14.06 30.42

Gearing ratio

Green plc Blue plc

Long term Liabilities 2100 200

Capital Employed 1195 2359

Gearing ratio = Long term Liabilities / Capital Employed * 100 175.73% 8.48%

Interest cover ratio

Green plc Blue plc

EBIT 491 290

Interest Expenses 250 24

Interest cover ratio = EBIT / Interest Expenses 1.96 12.08

(b): Comment on Ratios Computed and Recommendation:

Based on above ratios of corporations Green and Blue Plc this has been analysed that

financial position in terms of profitability criteria of Green Plc is better than Blue Plc as the in

gross profit margin, net profit margin and rectum on equity ratio of Green Plc is quite better than

and higher in comparison to the Blue Plc. While investor ratio shows that EPS of Green Plc is

lower than Blue plc as well as Green Plc's PE ratio shows that its shares are overvalued in

comparison of Blue Plc. Fixed asset turnover ratio of Blue Plc is 1.75 which higher than Green

Plc i.e. 1.25 indicating blue plc is more efficient in converting their fixed assets into sales. On

Green plc Blue plc

Trade Payables 63 193

Cost of Sales 1636 2316

Average Payable Period = Trade Payables / Cost of Sales * 365

days 14.06 30.42

Gearing ratio

Green plc Blue plc

Long term Liabilities 2100 200

Capital Employed 1195 2359

Gearing ratio = Long term Liabilities / Capital Employed * 100 175.73% 8.48%

Interest cover ratio

Green plc Blue plc

EBIT 491 290

Interest Expenses 250 24

Interest cover ratio = EBIT / Interest Expenses 1.96 12.08

(b): Comment on Ratios Computed and Recommendation:

Based on above ratios of corporations Green and Blue Plc this has been analysed that

financial position in terms of profitability criteria of Green Plc is better than Blue Plc as the in

gross profit margin, net profit margin and rectum on equity ratio of Green Plc is quite better than

and higher in comparison to the Blue Plc. While investor ratio shows that EPS of Green Plc is

lower than Blue plc as well as Green Plc's PE ratio shows that its shares are overvalued in

comparison of Blue Plc. Fixed asset turnover ratio of Blue Plc is 1.75 which higher than Green

Plc i.e. 1.25 indicating blue plc is more efficient in converting their fixed assets into sales. On

other hand average payable of Green Plc (14 days) is around half of the Blue Plc i.e. 30 days

indicating more better liquidity position of Green Plc. At last gearing and interest cover ratio

shows that Green Plc is too much rely on long term debt financing which is indicator of adverse

solvency position.

Therefore, based on above analysis this has been recommend to Blue Plc that company

should emphasise towards their profitability position and optimise expenses to enhance profits.

On other hand, Green Plc should control and strengthen their solvency and liquidity position by

reducing long term debts and loans obligation (Robinson, 2020).

(c). Limitation of Ratio analysis:

Major limitation of above analysis is that here only quantitative aspect has been covered

since ratios only deal with numbers – these do not discuss concerns such as product value ,

customer satisfaction, employee productivity, and many more (although these variables play a

major importance in financial results/outcomes. Another key limitation here is that in ratio

analysis only one year data has been used to make comparison of performance of Green and

Blue plc which does not provide true and fair picture of comparative financial performance of

both companies. Also, in fixed turnover ratio there generally average value of fixed assets are

used but due to lack of information current year's fixed assets value has been used (Septria and

Heryanto, 2019).

TASK 2

(a). Computation of market-value WACC and book-value WACC of ART Co and comment

briefly on difference between the two values:

Risk Free rate 4.00%

Equity Risk Premium 6.00%

Re = Rf + (Rm – Rf) * Bata = 4 + 6 * 1.15 = 10.9%

Cost of Debt (%) = kd * ( 1 – tax rate) = 6% ( 1- .25) = 4.50%

indicating more better liquidity position of Green Plc. At last gearing and interest cover ratio

shows that Green Plc is too much rely on long term debt financing which is indicator of adverse

solvency position.

Therefore, based on above analysis this has been recommend to Blue Plc that company

should emphasise towards their profitability position and optimise expenses to enhance profits.

On other hand, Green Plc should control and strengthen their solvency and liquidity position by

reducing long term debts and loans obligation (Robinson, 2020).

(c). Limitation of Ratio analysis:

Major limitation of above analysis is that here only quantitative aspect has been covered

since ratios only deal with numbers – these do not discuss concerns such as product value ,

customer satisfaction, employee productivity, and many more (although these variables play a

major importance in financial results/outcomes. Another key limitation here is that in ratio

analysis only one year data has been used to make comparison of performance of Green and

Blue plc which does not provide true and fair picture of comparative financial performance of

both companies. Also, in fixed turnover ratio there generally average value of fixed assets are

used but due to lack of information current year's fixed assets value has been used (Septria and

Heryanto, 2019).

TASK 2

(a). Computation of market-value WACC and book-value WACC of ART Co and comment

briefly on difference between the two values:

Risk Free rate 4.00%

Equity Risk Premium 6.00%

Re = Rf + (Rm – Rf) * Bata = 4 + 6 * 1.15 = 10.9%

Cost of Debt (%) = kd * ( 1 – tax rate) = 6% ( 1- .25) = 4.50%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

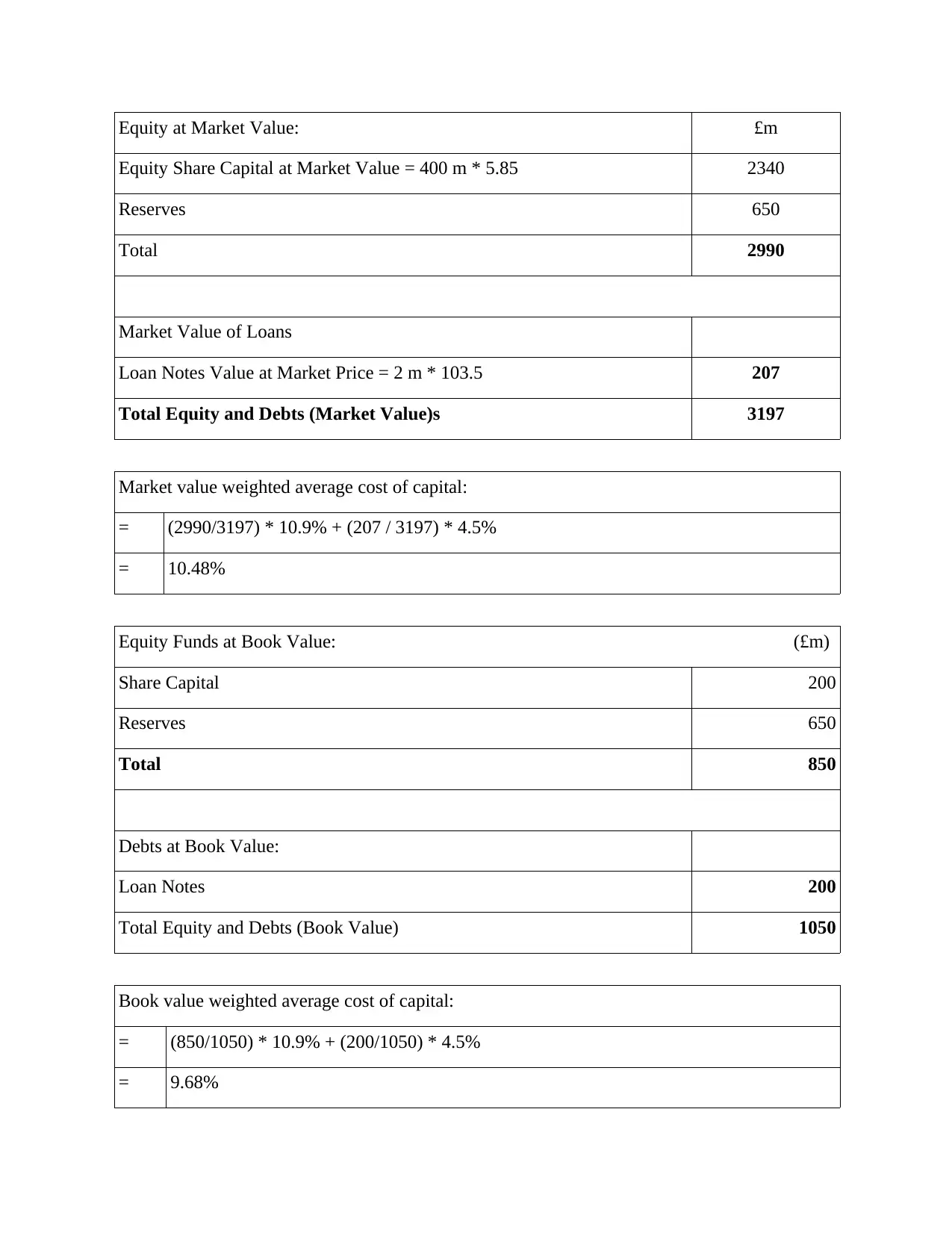

Equity at Market Value: £m

Equity Share Capital at Market Value = 400 m * 5.85 2340

Reserves 650

Total 2990

Market Value of Loans

Loan Notes Value at Market Price = 2 m * 103.5 207

Total Equity and Debts (Market Value)s 3197

Market value weighted average cost of capital:

= (2990/3197) * 10.9% + (207 / 3197) * 4.5%

= 10.48%

Equity Funds at Book Value: (£m)

Share Capital 200

Reserves 650

Total 850

Debts at Book Value:

Loan Notes 200

Total Equity and Debts (Book Value) 1050

Book value weighted average cost of capital:

= (850/1050) * 10.9% + (200/1050) * 4.5%

= 9.68%

Equity Share Capital at Market Value = 400 m * 5.85 2340

Reserves 650

Total 2990

Market Value of Loans

Loan Notes Value at Market Price = 2 m * 103.5 207

Total Equity and Debts (Market Value)s 3197

Market value weighted average cost of capital:

= (2990/3197) * 10.9% + (207 / 3197) * 4.5%

= 10.48%

Equity Funds at Book Value: (£m)

Share Capital 200

Reserves 650

Total 850

Debts at Book Value:

Loan Notes 200

Total Equity and Debts (Book Value) 1050

Book value weighted average cost of capital:

= (850/1050) * 10.9% + (200/1050) * 4.5%

= 9.68%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The weights of book values are easily accessible from financial statement for all kinds of

enterprises and are quite simple to compute. But at other side, for the market-

value weights, market prices/values have to be calculated but it is very difficult task to obtain

reliable data for same, in particular the value of equity whenever the company isn't listed. Still

Market Value WACC is deemed acceptable by analysts as the investor will claim market-

required rate of return on market value of capital and not book-value of capital (Nipa,

Kermanshachi and Ramaji, 2019).

(b). Circumstances under which WACC used in investment appraisal and its limitations as a

discount rate could be overcome:

WACC reflects investor's potential cost of having risk of bringing capital into a

corporation. Securities analysts use WACC to analyse and choose securities for investments. For

example, WACC is often used in discounting cash flow analysis as discounting rate extended to

expected cash flows in attempt to measure net-present-value of a company. WACC may be

viewed as hurdle rate against that to test the efficiency of ROIC. This also serves a crucial role in

the measurement of economic-value-added (EVA). Investors are using WACC as a method to

determine whether to make investment. The WAAC describes the minimal return rate at which a

corporation creates value for investors/shareholders (Mari and Marra, 2019).

One major circumstance that is likely keep business risk unchanged is that investment

project was an extension of established business operations. WACC can also be considered

as discount rate in appraisal of investment project that aimed to extend existing business

activities. Although, business risk relies on size and range of business operations as well as on

their existence, and any other investment project that extends current business operations must

be limited in comparison to size of existing company. Financial risk would remain constant

if investment project is funded in such manner that relative weighting of current sources of

funding remains constant, leaving current capital structure of investment business unchanged.

Although this is impossible in practice, a business will fund investment projects with target

capital structure in view that allow for minor variation. In case business risk shifts as a

consequence of investment project in such a way that it is not acceptable to use the corporation's

WACC for investment evaluation, a project-specific discounting rate should be measured

(Budhathoki and Rai, 2020).

enterprises and are quite simple to compute. But at other side, for the market-

value weights, market prices/values have to be calculated but it is very difficult task to obtain

reliable data for same, in particular the value of equity whenever the company isn't listed. Still

Market Value WACC is deemed acceptable by analysts as the investor will claim market-

required rate of return on market value of capital and not book-value of capital (Nipa,

Kermanshachi and Ramaji, 2019).

(b). Circumstances under which WACC used in investment appraisal and its limitations as a

discount rate could be overcome:

WACC reflects investor's potential cost of having risk of bringing capital into a

corporation. Securities analysts use WACC to analyse and choose securities for investments. For

example, WACC is often used in discounting cash flow analysis as discounting rate extended to

expected cash flows in attempt to measure net-present-value of a company. WACC may be

viewed as hurdle rate against that to test the efficiency of ROIC. This also serves a crucial role in

the measurement of economic-value-added (EVA). Investors are using WACC as a method to

determine whether to make investment. The WAAC describes the minimal return rate at which a

corporation creates value for investors/shareholders (Mari and Marra, 2019).

One major circumstance that is likely keep business risk unchanged is that investment

project was an extension of established business operations. WACC can also be considered

as discount rate in appraisal of investment project that aimed to extend existing business

activities. Although, business risk relies on size and range of business operations as well as on

their existence, and any other investment project that extends current business operations must

be limited in comparison to size of existing company. Financial risk would remain constant

if investment project is funded in such manner that relative weighting of current sources of

funding remains constant, leaving current capital structure of investment business unchanged.

Although this is impossible in practice, a business will fund investment projects with target

capital structure in view that allow for minor variation. In case business risk shifts as a

consequence of investment project in such a way that it is not acceptable to use the corporation's

WACC for investment evaluation, a project-specific discounting rate should be measured

(Budhathoki and Rai, 2020).

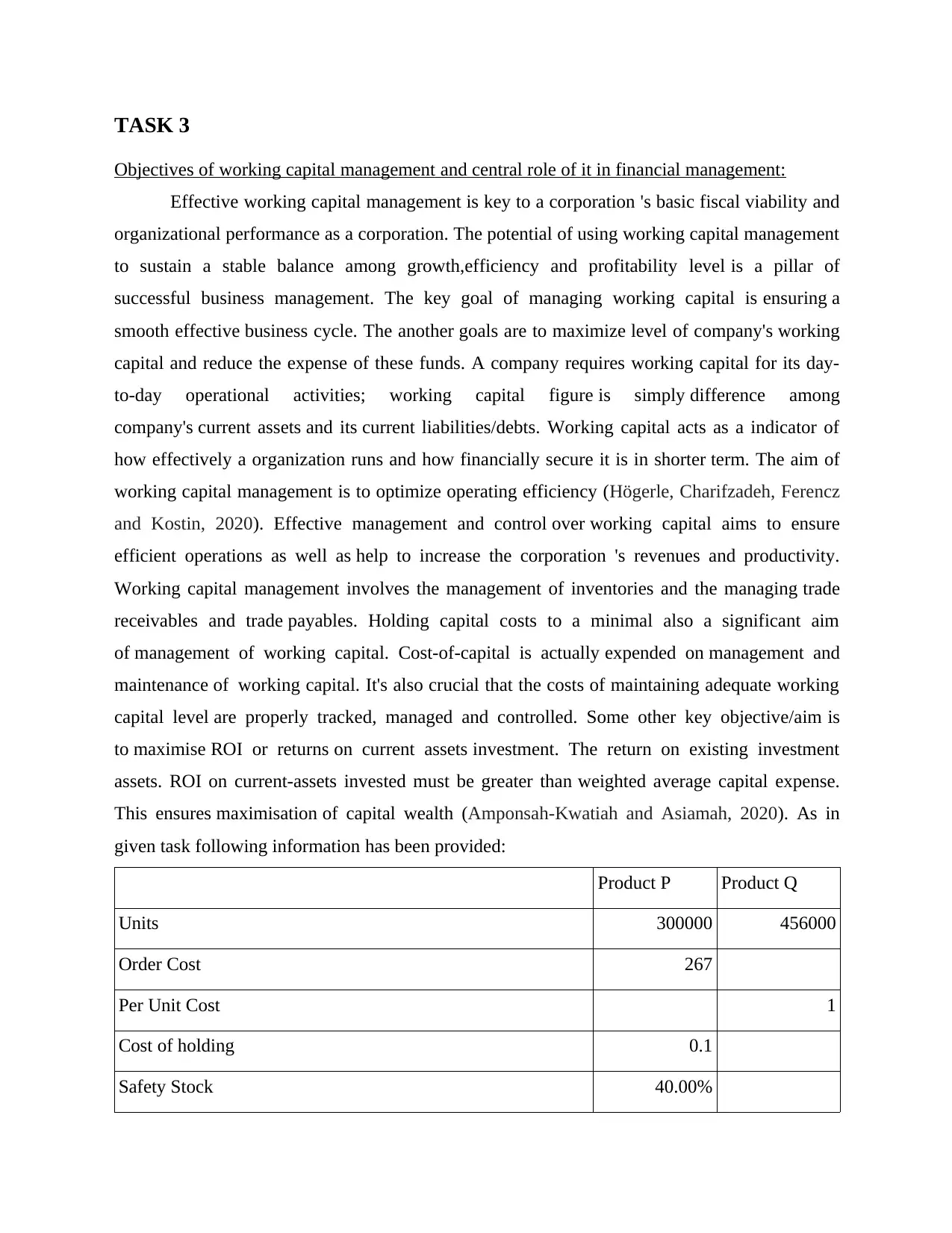

TASK 3

Objectives of working capital management and central role of it in financial management:

Effective working capital management is key to a corporation 's basic fiscal viability and

organizational performance as a corporation. The potential of using working capital management

to sustain a stable balance among growth,efficiency and profitability level is a pillar of

successful business management. The key goal of managing working capital is ensuring a

smooth effective business cycle. The another goals are to maximize level of company's working

capital and reduce the expense of these funds. A company requires working capital for its day-

to-day operational activities; working capital figure is simply difference among

company's current assets and its current liabilities/debts. Working capital acts as a indicator of

how effectively a organization runs and how financially secure it is in shorter term. The aim of

working capital management is to optimize operating efficiency (Högerle, Charifzadeh, Ferencz

and Kostin, 2020). Effective management and control over working capital aims to ensure

efficient operations as well as help to increase the corporation 's revenues and productivity.

Working capital management involves the management of inventories and the managing trade

receivables and trade payables. Holding capital costs to a minimal also a significant aim

of management of working capital. Cost-of-capital is actually expended on management and

maintenance of working capital. It's also crucial that the costs of maintaining adequate working

capital level are properly tracked, managed and controlled. Some other key objective/aim is

to maximise ROI or returns on current assets investment. The return on existing investment

assets. ROI on current-assets invested must be greater than weighted average capital expense.

This ensures maximisation of capital wealth (Amponsah-Kwatiah and Asiamah, 2020). As in

given task following information has been provided:

Product P Product Q

Units 300000 456000

Order Cost 267

Per Unit Cost 1

Cost of holding 0.1

Safety Stock 40.00%

Objectives of working capital management and central role of it in financial management:

Effective working capital management is key to a corporation 's basic fiscal viability and

organizational performance as a corporation. The potential of using working capital management

to sustain a stable balance among growth,efficiency and profitability level is a pillar of

successful business management. The key goal of managing working capital is ensuring a

smooth effective business cycle. The another goals are to maximize level of company's working

capital and reduce the expense of these funds. A company requires working capital for its day-

to-day operational activities; working capital figure is simply difference among

company's current assets and its current liabilities/debts. Working capital acts as a indicator of

how effectively a organization runs and how financially secure it is in shorter term. The aim of

working capital management is to optimize operating efficiency (Högerle, Charifzadeh, Ferencz

and Kostin, 2020). Effective management and control over working capital aims to ensure

efficient operations as well as help to increase the corporation 's revenues and productivity.

Working capital management involves the management of inventories and the managing trade

receivables and trade payables. Holding capital costs to a minimal also a significant aim

of management of working capital. Cost-of-capital is actually expended on management and

maintenance of working capital. It's also crucial that the costs of maintaining adequate working

capital level are properly tracked, managed and controlled. Some other key objective/aim is

to maximise ROI or returns on current assets investment. The return on existing investment

assets. ROI on current-assets invested must be greater than weighted average capital expense.

This ensures maximisation of capital wealth (Amponsah-Kwatiah and Asiamah, 2020). As in

given task following information has been provided:

Product P Product Q

Units 300000 456000

Order Cost 267

Per Unit Cost 1

Cost of holding 0.1

Safety Stock 40.00%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

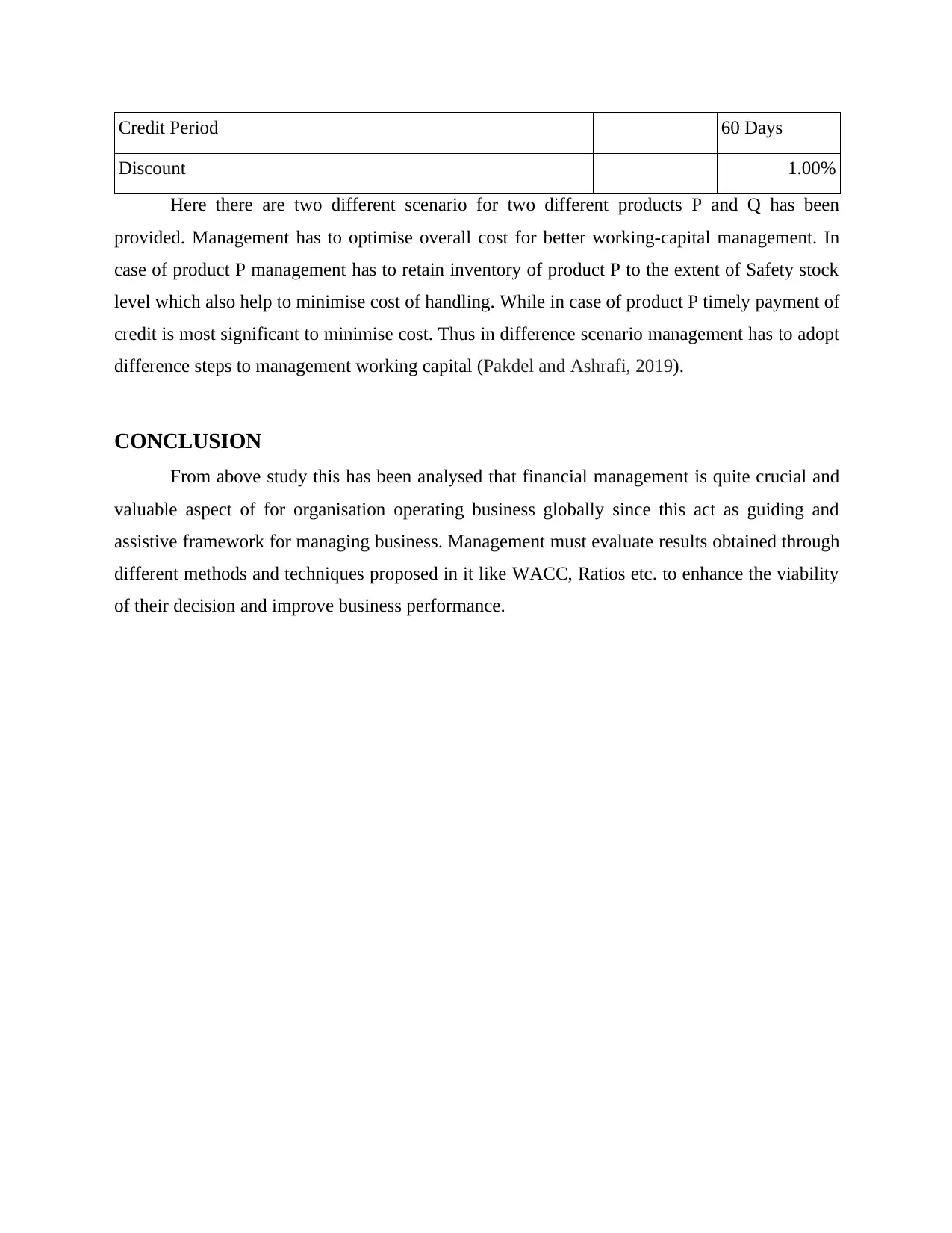

Credit Period 60 Days

Discount 1.00%

Here there are two different scenario for two different products P and Q has been

provided. Management has to optimise overall cost for better working-capital management. In

case of product P management has to retain inventory of product P to the extent of Safety stock

level which also help to minimise cost of handling. While in case of product P timely payment of

credit is most significant to minimise cost. Thus in difference scenario management has to adopt

difference steps to management working capital (Pakdel and Ashrafi, 2019).

CONCLUSION

From above study this has been analysed that financial management is quite crucial and

valuable aspect of for organisation operating business globally since this act as guiding and

assistive framework for managing business. Management must evaluate results obtained through

different methods and techniques proposed in it like WACC, Ratios etc. to enhance the viability

of their decision and improve business performance.

Discount 1.00%

Here there are two different scenario for two different products P and Q has been

provided. Management has to optimise overall cost for better working-capital management. In

case of product P management has to retain inventory of product P to the extent of Safety stock

level which also help to minimise cost of handling. While in case of product P timely payment of

credit is most significant to minimise cost. Thus in difference scenario management has to adopt

difference steps to management working capital (Pakdel and Ashrafi, 2019).

CONCLUSION

From above study this has been analysed that financial management is quite crucial and

valuable aspect of for organisation operating business globally since this act as guiding and

assistive framework for managing business. Management must evaluate results obtained through

different methods and techniques proposed in it like WACC, Ratios etc. to enhance the viability

of their decision and improve business performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Madura, J., 2020. International financial management. Cengage Learning.

Robinson, T.R., 2020. International financial statement analysis. John Wiley & Sons.

Septria, D. and Heryanto, H., 2019. Performance Capability Analysis and Regional Budget

Evaluation in Implementing Regional Autonomy in Dharmasraya District. Archives of

Business Research, 7(7), pp.180-187.

Nipa, T.J., Kermanshachi, S. and Ramaji, I., 2019, June. Comparative analysis of strengths and

limitations of infrastructure resilience measurement methods. In 7th CSCE

International Construction Specialty Conference (ICSC) (pp. 12-15).

Mari, C. and Marra, M., 2019. Valuing firm’s financial flexibility under default risk and

bankruptcy costs: a WACC based approach. International Journal of Managerial

Finance.

Budhathoki, P.B. and Rai, C.K., 2020. The Impact of the Debt Ratio, Total Assets, and Earning

Growth Rate on WACC: Evidence from Nepalese Commercial Banks. Asian Journal of

Economics, Business and Accounting, pp.16-23.

Högerle, B., Charifzadeh, M., Ferencz, M. and Kostin, K.B., 2020. The development of working

capital management and its impact on profitability and shareholder value: evidence

from Germany. Strategic Management, 25(2), pp.27-39.

Pakdel, M. and Ashrafi, M., 2019. Relationship between Working Capital Management and the

Performance of Firm in Different Business Cycles. Dutch Journal of Finance and

Management, 3(1), p.em0057.

Amponsah-Kwatiah, K. and Asiamah, M., 2020. Working capital management and profitability

of listed manufacturing firms in Ghana. International Journal of Productivity and

Performance Management.

Books and Journals:

Madura, J., 2020. International financial management. Cengage Learning.

Robinson, T.R., 2020. International financial statement analysis. John Wiley & Sons.

Septria, D. and Heryanto, H., 2019. Performance Capability Analysis and Regional Budget

Evaluation in Implementing Regional Autonomy in Dharmasraya District. Archives of

Business Research, 7(7), pp.180-187.

Nipa, T.J., Kermanshachi, S. and Ramaji, I., 2019, June. Comparative analysis of strengths and

limitations of infrastructure resilience measurement methods. In 7th CSCE

International Construction Specialty Conference (ICSC) (pp. 12-15).

Mari, C. and Marra, M., 2019. Valuing firm’s financial flexibility under default risk and

bankruptcy costs: a WACC based approach. International Journal of Managerial

Finance.

Budhathoki, P.B. and Rai, C.K., 2020. The Impact of the Debt Ratio, Total Assets, and Earning

Growth Rate on WACC: Evidence from Nepalese Commercial Banks. Asian Journal of

Economics, Business and Accounting, pp.16-23.

Högerle, B., Charifzadeh, M., Ferencz, M. and Kostin, K.B., 2020. The development of working

capital management and its impact on profitability and shareholder value: evidence

from Germany. Strategic Management, 25(2), pp.27-39.

Pakdel, M. and Ashrafi, M., 2019. Relationship between Working Capital Management and the

Performance of Firm in Different Business Cycles. Dutch Journal of Finance and

Management, 3(1), p.em0057.

Amponsah-Kwatiah, K. and Asiamah, M., 2020. Working capital management and profitability

of listed manufacturing firms in Ghana. International Journal of Productivity and

Performance Management.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.