Fraud Risk Mitigation in Auditing

VerifiedAdded on 2020/02/24

|9

|2103

|108

AI Summary

This assignment focuses on analyzing fraud risk factors within a company using two case studies. It examines the auditor's responsibility in identifying, mitigating, and reporting these risks. The analysis covers issues like inadequate segregation of duties, hasty implementation of new IT systems, and potential for management bias. The assignment emphasizes the importance of proper internal controls, expert opinions, and timely account checks to minimize fraud risk and ensure accurate financial reporting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

By student name

Professor

University

Date: 28 August 2017.

Professor

University

Date: 28 August 2017.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

Contents

Question no 1…………………………………………………………………...2

Question no 2…………………………………………………………………...6

Question no 3…………………………………………………………….....….7

Refrences.....……………………………………………………………….......8

1 | P a g e

Contents

Question no 1…………………………………………………………………...2

Question no 2…………………………………………………………………...6

Question no 3…………………………………………………………….....….7

Refrences.....……………………………………………………………….......8

1 | P a g e

2

Question no 1

Audit is an independent examination of the books of accounts of an entity conducted by the

auditors with the view to express an opinion on the financial statements whether they are prepared on

an unbiased and true basis and whether they can be relied upon to take the critical and significant

business and financial statements. It gives reasonable assurance to the users of the financial statements,

both internal and external, including government, shareholders, banks, financial institutions, creditors,

etc. to help them take decision on their investments. The regulation on audit on the entities has

increased over time by ACCA and other regulatory bodies. There has been many guidance’s being issued

by the IFRS committee for recording the transaction and maintenance of the books which needs to be

verified by the auditors while conducting the audit of the entity. The requirements of audit do not end

here and audited report is required in the stock exchanges in which the company’s shares are listed. To

conduct an audit, the auditor 1st needs to understand the business and it environment, the industry in

which it is operating, the government regulation, other economic and political factor, if any, affecting

the business and several other micro and macro economic factors to give a proper audit report. Auditors

also need to validate and comment upon the estimates and management judgements being taken upon

in preparation of the accounts such that they are viable (Raiborn, Butler & Martin 2016). They also need

to check on the materiality, going concern assumption and whether or not the basic concept of

consistency has been followed or not. With all this objectives in mind, the auditor audits the books of

accounts using substantive and analytical audit procedures. Substantive audit procedures include

vouching of the incomes and expenses recorded in the books falling above the materiality level for

whether they actually exist or not, whether they have been completely recorded, reconciling the same

from the supporting evidences in the form of vouchers, bills, invoices, etc. Substantive procedures are

usually given effect to using inspection of records, observation of processes and procedures being

followed, taking external confirmations from the parties dealing with the business or company like

debtors, creditors, banks, etc., verifying the related party transactions, etc. They also check the

arithmetical accuracy in some cases to check whether this has been taken care of or not. Besides all this,

a check is also made on the assets and liabilities recorded in the books for their actual existence and

reporting to check substance over form (Knechel & Salterio 2016).

Once all this is given effect to and still the auditor is not able to express his / her opinion, then

he/she resorts to the analytical audit procedures, which include ratio analysis of certain specific ratios,

comparison of the actual from the budgeted and expected figures, trend analysis with respect to the

2 | P a g e

Question no 1

Audit is an independent examination of the books of accounts of an entity conducted by the

auditors with the view to express an opinion on the financial statements whether they are prepared on

an unbiased and true basis and whether they can be relied upon to take the critical and significant

business and financial statements. It gives reasonable assurance to the users of the financial statements,

both internal and external, including government, shareholders, banks, financial institutions, creditors,

etc. to help them take decision on their investments. The regulation on audit on the entities has

increased over time by ACCA and other regulatory bodies. There has been many guidance’s being issued

by the IFRS committee for recording the transaction and maintenance of the books which needs to be

verified by the auditors while conducting the audit of the entity. The requirements of audit do not end

here and audited report is required in the stock exchanges in which the company’s shares are listed. To

conduct an audit, the auditor 1st needs to understand the business and it environment, the industry in

which it is operating, the government regulation, other economic and political factor, if any, affecting

the business and several other micro and macro economic factors to give a proper audit report. Auditors

also need to validate and comment upon the estimates and management judgements being taken upon

in preparation of the accounts such that they are viable (Raiborn, Butler & Martin 2016). They also need

to check on the materiality, going concern assumption and whether or not the basic concept of

consistency has been followed or not. With all this objectives in mind, the auditor audits the books of

accounts using substantive and analytical audit procedures. Substantive audit procedures include

vouching of the incomes and expenses recorded in the books falling above the materiality level for

whether they actually exist or not, whether they have been completely recorded, reconciling the same

from the supporting evidences in the form of vouchers, bills, invoices, etc. Substantive procedures are

usually given effect to using inspection of records, observation of processes and procedures being

followed, taking external confirmations from the parties dealing with the business or company like

debtors, creditors, banks, etc., verifying the related party transactions, etc. They also check the

arithmetical accuracy in some cases to check whether this has been taken care of or not. Besides all this,

a check is also made on the assets and liabilities recorded in the books for their actual existence and

reporting to check substance over form (Knechel & Salterio 2016).

Once all this is given effect to and still the auditor is not able to express his / her opinion, then

he/she resorts to the analytical audit procedures, which include ratio analysis of certain specific ratios,

comparison of the actual from the budgeted and expected figures, trend analysis with respect to the

2 | P a g e

3

industry and the past period, etc. Before further steps, the auditor generally checks on the level of

internal control being maintained in the entity before making further audit plan and determining the

nature, extent of checking and time of audit procedures to be undertaken. If the internal control is

strong, it implies less risk, and therefore less of routine checking can be done on the other hand, if the

internal control itself is weak, the risk of material misstatements rises and in such a case the auditor

needs to increase the extent of checking (Jones 2017).

In the given case, a printing press is to be audited and the new auditor is taking over from the

old one. Besides this, as per the records, the company has had several accounting changes having huge

bearing on the results like changes in the depreciation policy, a loan being taken with some conditions,

the management being changed at the top level and the new IT system being introduced without any

proper checking and back up. All these financial and non-financial data asks for an audit, which can

justify the accounts prepared and point out the material misstatements, if any to the management. For

this, a detailed ratio analysis has been shown below from the perspective of debt management,

liquidity, asset management and profitability. Furthermore, industry ratios are missing and hence the

same has been ignored in workings (Grenier 2017).

3 | P a g e

industry and the past period, etc. Before further steps, the auditor generally checks on the level of

internal control being maintained in the entity before making further audit plan and determining the

nature, extent of checking and time of audit procedures to be undertaken. If the internal control is

strong, it implies less risk, and therefore less of routine checking can be done on the other hand, if the

internal control itself is weak, the risk of material misstatements rises and in such a case the auditor

needs to increase the extent of checking (Jones 2017).

In the given case, a printing press is to be audited and the new auditor is taking over from the

old one. Besides this, as per the records, the company has had several accounting changes having huge

bearing on the results like changes in the depreciation policy, a loan being taken with some conditions,

the management being changed at the top level and the new IT system being introduced without any

proper checking and back up. All these financial and non-financial data asks for an audit, which can

justify the accounts prepared and point out the material misstatements, if any to the management. For

this, a detailed ratio analysis has been shown below from the perspective of debt management,

liquidity, asset management and profitability. Furthermore, industry ratios are missing and hence the

same has been ignored in workings (Grenier 2017).

3 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

2013 2014 2015

Total current assets 5,385,938 7,509,150 9,600,929

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 1.42 1.47 1.50

2013 2014 2015

Total current assets - Inventory - Prepaid expenses 3,129,750 4,837,788 5,420,429

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 0.83 0.94 0.85

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total Assets 5,120,250 15,903,900 26,147,991

Result 74% 32% 53%

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 41% 47% 113%

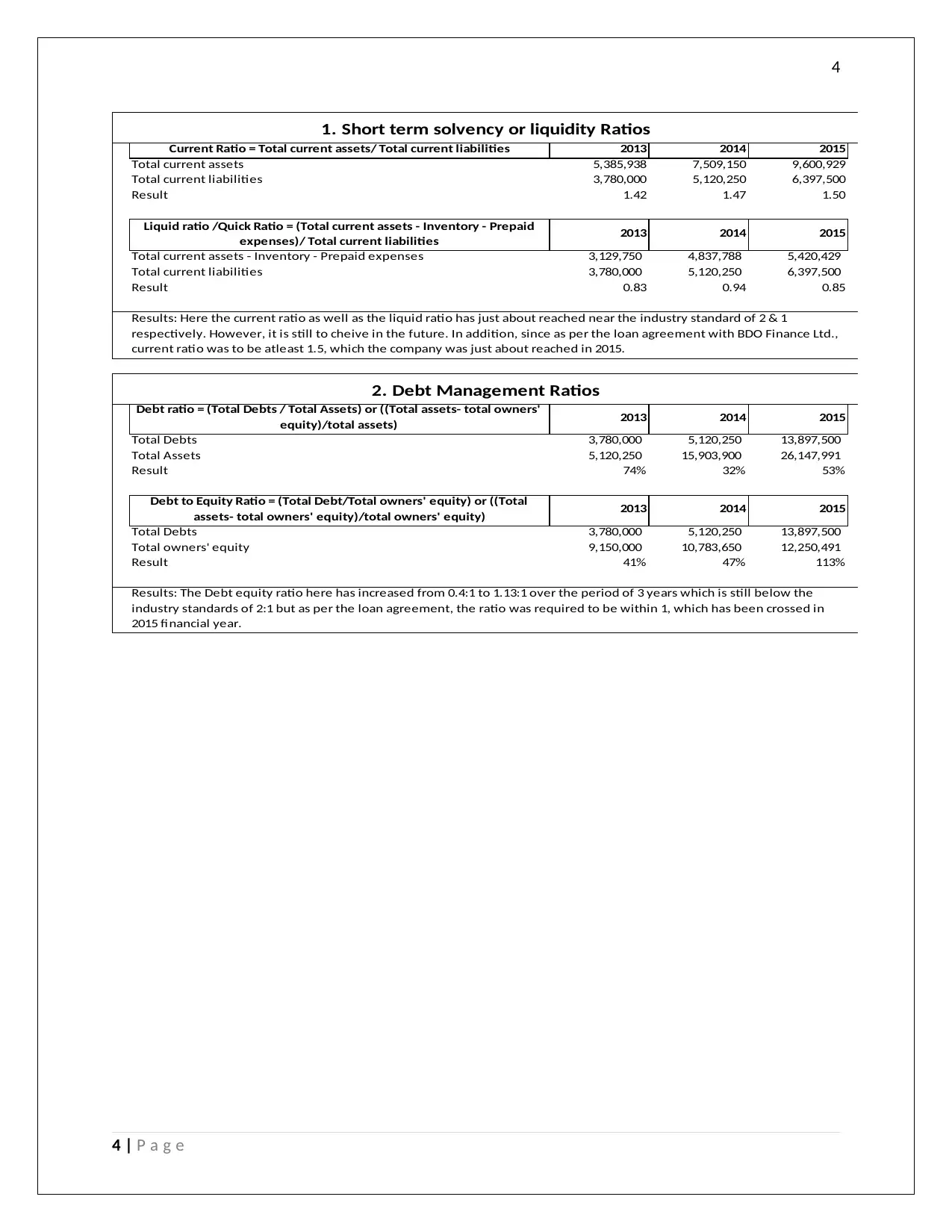

Results: Here the current ratio as well as the liquid ratio has just about reached near the industry standard of 2 & 1

respectively. However, it is still to cheive in the future. In addition, since as per the loan agreement with BDO Finance Ltd.,

current ratio was to be atleast 1.5, which the company was just about reached in 2015.

1. Short term solvency or liquidity Ratios

2. Debt Management Ratios

Results: The Debt equity ratio here has increased from 0.4:1 to 1.13:1 over the period of 3 years which is still below the

industry standards of 2:1 but as per the loan agreement, the ratio was required to be within 1, which has been crossed in

2015 financial year.

Current Ratio = Total current assets/ Total current liabilities

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets)

Debt to Equity Ratio = (Total Debt/Total owners' equity) or ((Total

assets- total owners' equity)/total owners' equity)

4 | P a g e

2013 2014 2015

Total current assets 5,385,938 7,509,150 9,600,929

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 1.42 1.47 1.50

2013 2014 2015

Total current assets - Inventory - Prepaid expenses 3,129,750 4,837,788 5,420,429

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 0.83 0.94 0.85

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total Assets 5,120,250 15,903,900 26,147,991

Result 74% 32% 53%

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 41% 47% 113%

Results: Here the current ratio as well as the liquid ratio has just about reached near the industry standard of 2 & 1

respectively. However, it is still to cheive in the future. In addition, since as per the loan agreement with BDO Finance Ltd.,

current ratio was to be atleast 1.5, which the company was just about reached in 2015.

1. Short term solvency or liquidity Ratios

2. Debt Management Ratios

Results: The Debt equity ratio here has increased from 0.4:1 to 1.13:1 over the period of 3 years which is still below the

industry standards of 2:1 but as per the loan agreement, the ratio was required to be within 1, which has been crossed in

2015 financial year.

Current Ratio = Total current assets/ Total current liabilities

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets)

Debt to Equity Ratio = (Total Debt/Total owners' equity) or ((Total

assets- total owners' equity)/total owners' equity)

4 | P a g e

5

2013 2014 2015

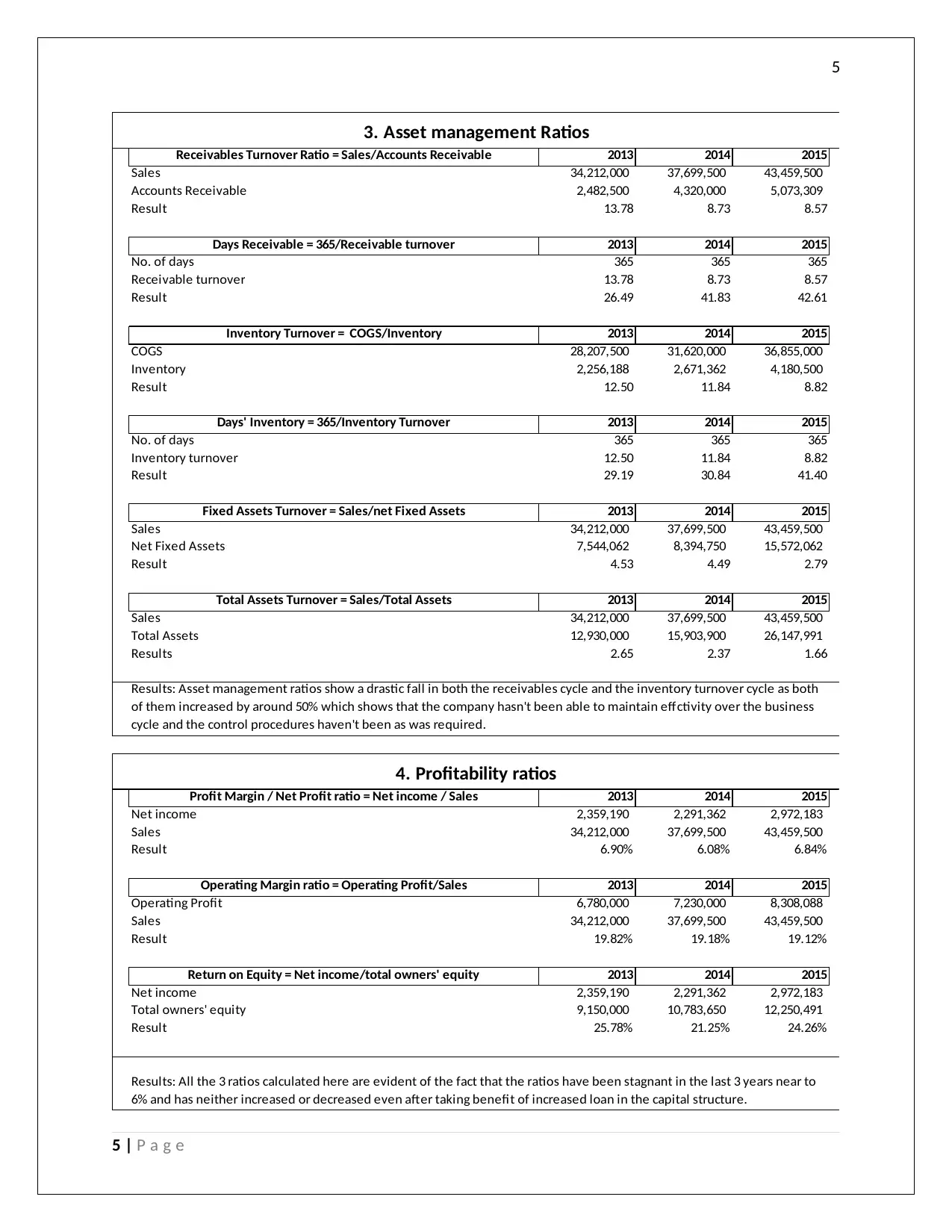

Sales 34,212,000 37,699,500 43,459,500

Accounts Receivable 2,482,500 4,320,000 5,073,309

Result 13.78 8.73 8.57

2013 2014 2015

No. of days 365 365 365

Receivable turnover 13.78 8.73 8.57

Result 26.49 41.83 42.61

2013 2014 2015

COGS 28,207,500 31,620,000 36,855,000

Inventory 2,256,188 2,671,362 4,180,500

Result 12.50 11.84 8.82

2013 2014 2015

No. of days 365 365 365

Inventory turnover 12.50 11.84 8.82

Result 29.19 30.84 41.40

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Net Fixed Assets 7,544,062 8,394,750 15,572,062

Result 4.53 4.49 2.79

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Total Assets 12,930,000 15,903,900 26,147,991

Results 2.65 2.37 1.66

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Sales 34,212,000 37,699,500 43,459,500

Result 6.90% 6.08% 6.84%

2013 2014 2015

Operating Profit 6,780,000 7,230,000 8,308,088

Sales 34,212,000 37,699,500 43,459,500

Result 19.82% 19.18% 19.12%

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 25.78% 21.25% 24.26%

Results: Asset management ratios show a drastic fall in both the receivables cycle and the inventory turnover cycle as both

of them increased by around 50% which shows that the company hasn't been able to maintain effctivity over the business

cycle and the control procedures haven't been as was required.

3. Asset management Ratios

Results: All the 3 ratios calculated here are evident of the fact that the ratios have been stagnant in the last 3 years near to

6% and has neither increased or decreased even after taking benefit of increased loan in the capital structure.

Inventory Turnover = COGS/Inventory

Days' Inventory = 365/Inventory Turnover

Fixed Assets Turnover = Sales/net Fixed Assets

Total Assets Turnover = Sales/Total Assets

Profit Margin / Net Profit ratio = Net income / Sales

Operating Margin ratio = Operating Profit/Sales

Return on Equity = Net income/total owners' equity

Receivables Turnover Ratio = Sales/Accounts Receivable

Days Receivable = 365/Receivable turnover

4. Profitability ratios

5 | P a g e

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Accounts Receivable 2,482,500 4,320,000 5,073,309

Result 13.78 8.73 8.57

2013 2014 2015

No. of days 365 365 365

Receivable turnover 13.78 8.73 8.57

Result 26.49 41.83 42.61

2013 2014 2015

COGS 28,207,500 31,620,000 36,855,000

Inventory 2,256,188 2,671,362 4,180,500

Result 12.50 11.84 8.82

2013 2014 2015

No. of days 365 365 365

Inventory turnover 12.50 11.84 8.82

Result 29.19 30.84 41.40

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Net Fixed Assets 7,544,062 8,394,750 15,572,062

Result 4.53 4.49 2.79

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Total Assets 12,930,000 15,903,900 26,147,991

Results 2.65 2.37 1.66

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Sales 34,212,000 37,699,500 43,459,500

Result 6.90% 6.08% 6.84%

2013 2014 2015

Operating Profit 6,780,000 7,230,000 8,308,088

Sales 34,212,000 37,699,500 43,459,500

Result 19.82% 19.18% 19.12%

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 25.78% 21.25% 24.26%

Results: Asset management ratios show a drastic fall in both the receivables cycle and the inventory turnover cycle as both

of them increased by around 50% which shows that the company hasn't been able to maintain effctivity over the business

cycle and the control procedures haven't been as was required.

3. Asset management Ratios

Results: All the 3 ratios calculated here are evident of the fact that the ratios have been stagnant in the last 3 years near to

6% and has neither increased or decreased even after taking benefit of increased loan in the capital structure.

Inventory Turnover = COGS/Inventory

Days' Inventory = 365/Inventory Turnover

Fixed Assets Turnover = Sales/net Fixed Assets

Total Assets Turnover = Sales/Total Assets

Profit Margin / Net Profit ratio = Net income / Sales

Operating Margin ratio = Operating Profit/Sales

Return on Equity = Net income/total owners' equity

Receivables Turnover Ratio = Sales/Accounts Receivable

Days Receivable = 365/Receivable turnover

4. Profitability ratios

5 | P a g e

6

Solution 2

Risk assessment and analysis is an important part of auditing. It is important for the auditor to apply all

kinds of procedures to identify all the probable risk factors. There are generally three types of risk

associated with an audit, inherent risk, control risk and detection risk. Inherent risk occurs when things

are not in the hands of the management even after applying all the possible control measures. Control

risk occurs when the management fail to ascertain proper control level in the organisation and detection

risk occurs in situation where the auditor fails on his part to detect the major risks and errors (Fay &

Negangard 2017). The main implication of the same is that it is the duty of the auditor to make sure that

proper judgement is established on his part. In case of DIPL, there are two cases of inherent risk and the

same has been explained here under-

First case is where the management is considering changing the methods of valuation and adopting new

procedures that are deviation from the normal routine matters. In these cases, it becomes difficult for

the auditor to ascertain the proper trail of work. The CEO of the company wants to change the method

of calculation of depreciation by taking the life of asset to be twenty years, whereas as per the industry

standards the life must be thirty years. Therefore, this is a deviation from the normal procedures and

the company has taken no research before applying them. The second case is the installation of the new

It system without proper research, oat may be possible that it leads to overvaluation of the accounts.

The new system has been installed without any reconciliation; any research, and in case it fails it might

affect the overall profitability of the company. Thus, it is important for the auditor of the company, to

make sure that the management is providing proper disclosure for any kind of changes they are

incorporating (Sonu, Ahn & Choi 2017).The results after implementation must also be monitored so that

any case of misevaluation may be ascertained. This in these areas there are no proper control by the

management and thus leads to inherent risk on part of the company The management should provide

the auditor with all the proper details that might be needed. The auditor must do its own research

before commenting on the validation of the new IT system. It is important that expert opinion must be

taken before such changes are made. Strong control measures should also be incorporated, so that risk

is reduced. These are the few ways by which risk can be identified and mitigated (Bae 2017).

6 | P a g e

Solution 2

Risk assessment and analysis is an important part of auditing. It is important for the auditor to apply all

kinds of procedures to identify all the probable risk factors. There are generally three types of risk

associated with an audit, inherent risk, control risk and detection risk. Inherent risk occurs when things

are not in the hands of the management even after applying all the possible control measures. Control

risk occurs when the management fail to ascertain proper control level in the organisation and detection

risk occurs in situation where the auditor fails on his part to detect the major risks and errors (Fay &

Negangard 2017). The main implication of the same is that it is the duty of the auditor to make sure that

proper judgement is established on his part. In case of DIPL, there are two cases of inherent risk and the

same has been explained here under-

First case is where the management is considering changing the methods of valuation and adopting new

procedures that are deviation from the normal routine matters. In these cases, it becomes difficult for

the auditor to ascertain the proper trail of work. The CEO of the company wants to change the method

of calculation of depreciation by taking the life of asset to be twenty years, whereas as per the industry

standards the life must be thirty years. Therefore, this is a deviation from the normal procedures and

the company has taken no research before applying them. The second case is the installation of the new

It system without proper research, oat may be possible that it leads to overvaluation of the accounts.

The new system has been installed without any reconciliation; any research, and in case it fails it might

affect the overall profitability of the company. Thus, it is important for the auditor of the company, to

make sure that the management is providing proper disclosure for any kind of changes they are

incorporating (Sonu, Ahn & Choi 2017).The results after implementation must also be monitored so that

any case of misevaluation may be ascertained. This in these areas there are no proper control by the

management and thus leads to inherent risk on part of the company The management should provide

the auditor with all the proper details that might be needed. The auditor must do its own research

before commenting on the validation of the new IT system. It is important that expert opinion must be

taken before such changes are made. Strong control measures should also be incorporated, so that risk

is reduced. These are the few ways by which risk can be identified and mitigated (Bae 2017).

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Solution 3

Fraud occurs when the management or the employee of the company indulges in certain

activities for their own personal gains that are harmful for the working of the organisation. It occurs

when the internal controls are not strong which gives the employees to do such activities. Often the

management might be the culprit, the auditor should not rely on what the management portrays and

should apply his own research techniques before reaching a conclusion In case of DIPL, and there are

two cases where we see that fraud risk factor is present.

First case is in the non-segregation of important work, which gives the employees a chance to

easily defalcate the money. In case of DIPL, a single person has been given the responsibility to manage

the accounts and reconcile the same. This shows that the management of the company is lacking proper

internal control measures. The auditor should make sure that the work is properly segregated between

the employees, proper authority must be established and in any case the employees indulges in any kind

of fraud they must be penalised. The second case of fraud is the installation of the new It system by the

management. The management has undertaken the same in allot of haste. It has not applied any

research before doing the same. There are high chances that personal motives of the magemnt might be

involved in the same. In this case, we see that before installation of the system no reconciliation of the

cost and the result was done, it may be possible that the new system fails. This will affect the overall

profitability of the company. In all cases the management should make sure that, the accounts are not

under or overvalued. In any case, the auditor finds that there are certain fraud risk factors involved, the

auditor can question the management and then can modify the audit report. . Expert opinion of the

outsiders must be taken in case of the same. Thus, it is important that the auditor must see that proper

records must be checked in relation to the new system .The main job here is to make sure that the

books of account shows the true state of affairs and any kind of fraud risk factors must be identified and

must be eliminated. In these few ways, the auditor can help I identification and mitigation of the overall

fraud risk factors that might be associated with the company. It is the duty of the auditor and the

management to make sure that suppose visits and timely checking of the accounts are done to keep a

check on the sincerity of the employees. In addition, the management must establish proper controls.

All these will help in mitigation of the major fraud risk factors in the company and support the auditor in

conducting his audit properly (DeZoort & Harrison 2016).

References

7 | P a g e

Solution 3

Fraud occurs when the management or the employee of the company indulges in certain

activities for their own personal gains that are harmful for the working of the organisation. It occurs

when the internal controls are not strong which gives the employees to do such activities. Often the

management might be the culprit, the auditor should not rely on what the management portrays and

should apply his own research techniques before reaching a conclusion In case of DIPL, and there are

two cases where we see that fraud risk factor is present.

First case is in the non-segregation of important work, which gives the employees a chance to

easily defalcate the money. In case of DIPL, a single person has been given the responsibility to manage

the accounts and reconcile the same. This shows that the management of the company is lacking proper

internal control measures. The auditor should make sure that the work is properly segregated between

the employees, proper authority must be established and in any case the employees indulges in any kind

of fraud they must be penalised. The second case of fraud is the installation of the new It system by the

management. The management has undertaken the same in allot of haste. It has not applied any

research before doing the same. There are high chances that personal motives of the magemnt might be

involved in the same. In this case, we see that before installation of the system no reconciliation of the

cost and the result was done, it may be possible that the new system fails. This will affect the overall

profitability of the company. In all cases the management should make sure that, the accounts are not

under or overvalued. In any case, the auditor finds that there are certain fraud risk factors involved, the

auditor can question the management and then can modify the audit report. . Expert opinion of the

outsiders must be taken in case of the same. Thus, it is important that the auditor must see that proper

records must be checked in relation to the new system .The main job here is to make sure that the

books of account shows the true state of affairs and any kind of fraud risk factors must be identified and

must be eliminated. In these few ways, the auditor can help I identification and mitigation of the overall

fraud risk factors that might be associated with the company. It is the duty of the auditor and the

management to make sure that suppose visits and timely checking of the accounts are done to keep a

check on the sincerity of the employees. In addition, the management must establish proper controls.

All these will help in mitigation of the major fraud risk factors in the company and support the auditor in

conducting his audit properly (DeZoort & Harrison 2016).

References

7 | P a g e

8

Bae, SH 2017, 'The Association Between Corporate Tax Avoidance And Audit Efforts: Evidence From

Korea', Journal of Applied Business Research, vol 33, no. 1, pp. 153-172.

DeZoort, FT & Harrison, PD 2016, 'Understanding Auditors sense of Responsibility for detecting fraud

within organization', Journal of Business Ethics, pp. 1-18.

Fay, R & Negangard, EM 2017, 'Manual journal entry testing : Data analytics and the risk of fraud',

Journal of Accounting Education, vol 38, pp. 37-49.

Grenier, J 2017, 'Encouraging Professional Skepticism in the Industry Specialization Era', Journal of

Business Ethics, vol 142, no. 2, pp. 241-256.

Jones, P 2017, Statistical Sampling and Risk Analysis in Auditing, Routledge, NY.

Knechel, WB & Salterio, SE 2016, Auditing:Assurance and Risk, 4th edn, Routledge, New York.

Raiborn, C, Butler, JB & Martin, K 2016, 'The internal audit function: A prerequisite for Good

Governance', Journal of Corporate Accounting and Finance, vol 28, no. 2, pp. 10-21.

Sonu, CH, Ahn, H & Choi, A 2017, 'Audit fee pressure and audit risk: evidence from the financial crisis of

2008', Asia-Pacific Journal of Accounting & Economics , vol 24, no. 1-2, pp. 127-144.

8 | P a g e

Bae, SH 2017, 'The Association Between Corporate Tax Avoidance And Audit Efforts: Evidence From

Korea', Journal of Applied Business Research, vol 33, no. 1, pp. 153-172.

DeZoort, FT & Harrison, PD 2016, 'Understanding Auditors sense of Responsibility for detecting fraud

within organization', Journal of Business Ethics, pp. 1-18.

Fay, R & Negangard, EM 2017, 'Manual journal entry testing : Data analytics and the risk of fraud',

Journal of Accounting Education, vol 38, pp. 37-49.

Grenier, J 2017, 'Encouraging Professional Skepticism in the Industry Specialization Era', Journal of

Business Ethics, vol 142, no. 2, pp. 241-256.

Jones, P 2017, Statistical Sampling and Risk Analysis in Auditing, Routledge, NY.

Knechel, WB & Salterio, SE 2016, Auditing:Assurance and Risk, 4th edn, Routledge, New York.

Raiborn, C, Butler, JB & Martin, K 2016, 'The internal audit function: A prerequisite for Good

Governance', Journal of Corporate Accounting and Finance, vol 28, no. 2, pp. 10-21.

Sonu, CH, Ahn, H & Choi, A 2017, 'Audit fee pressure and audit risk: evidence from the financial crisis of

2008', Asia-Pacific Journal of Accounting & Economics , vol 24, no. 1-2, pp. 127-144.

8 | P a g e

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.