Financial Accounting and Management Report for Collins Colman

VerifiedAdded on 2023/01/07

|17

|3935

|59

Report

AI Summary

This report provides a comprehensive financial analysis of Collins Colman Ltd, covering various aspects of financial and management accounting. It begins with the preparation of financial statements, including the income statement and statement of financial position for the year ended December 31, 2019. The report then delves into management accounting concepts such as break-even analysis and margin of safety, calculating these metrics for the company's microwave sales. It assesses the profitability of different sales scenarios and evaluates the impact of a new sales strategy. Furthermore, the report explores investment appraisal techniques, including payback period, accounting rate of return, and net present value, to determine the viability of purchasing a new machine. It provides recommendations based on these calculations and discusses the merits and demerits of different investment appraisal methods and the use of budgets for strategic planning. The analysis highlights the company's financial position, liquidity, and profitability, offering insights for improved financial management and strategic decision-making.

INTRODUCTION TO

ACCOUNTING AND FINANCE

ACCOUNTING AND FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

PART A...........................................................................................................................................1

a. Statement of Income for the year ended 31st December 2019................................................1

b. Statement of Financial Position for the year ended 31st December 2019................................3

PART B...........................................................................................................................................5

a. Contribution of the microwave towards covering the fixed costs...........................................5

b. Breakeven point and the margin of safety in the terms of both the units of the microwaves

and the revenues on selling the microwaves for 40.....................................................................5

c. Profits made by Parksmead Limited if produced and selling 60000 of the microwaves.........6

d. Analysing the new strategy of Parksmead limited increasing the sales units by 15% and

sales price by 8% for making advertisement expenses of 135000..............................................7

e. Explanation underpinning the assumptions attached with break even models including its

implementation for the business..................................................................................................8

PART C...........................................................................................................................................9

a. Calculating Payback period, Accounting rate of return and Net Present Value of machine

and recommendations for purchase of machine..........................................................................9

b. Report analysing and explaining merits and demerits of different investment appraisal

techniques..................................................................................................................................11

c. Report identifying and explaining key benefits and limitations of using budget as the tool

for strategic planning.................................................................................................................12

REFERENCES..............................................................................................................................14

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

PART A...........................................................................................................................................1

a. Statement of Income for the year ended 31st December 2019................................................1

b. Statement of Financial Position for the year ended 31st December 2019................................3

PART B...........................................................................................................................................5

a. Contribution of the microwave towards covering the fixed costs...........................................5

b. Breakeven point and the margin of safety in the terms of both the units of the microwaves

and the revenues on selling the microwaves for 40.....................................................................5

c. Profits made by Parksmead Limited if produced and selling 60000 of the microwaves.........6

d. Analysing the new strategy of Parksmead limited increasing the sales units by 15% and

sales price by 8% for making advertisement expenses of 135000..............................................7

e. Explanation underpinning the assumptions attached with break even models including its

implementation for the business..................................................................................................8

PART C...........................................................................................................................................9

a. Calculating Payback period, Accounting rate of return and Net Present Value of machine

and recommendations for purchase of machine..........................................................................9

b. Report analysing and explaining merits and demerits of different investment appraisal

techniques..................................................................................................................................11

c. Report identifying and explaining key benefits and limitations of using budget as the tool

for strategic planning.................................................................................................................12

REFERENCES..............................................................................................................................14

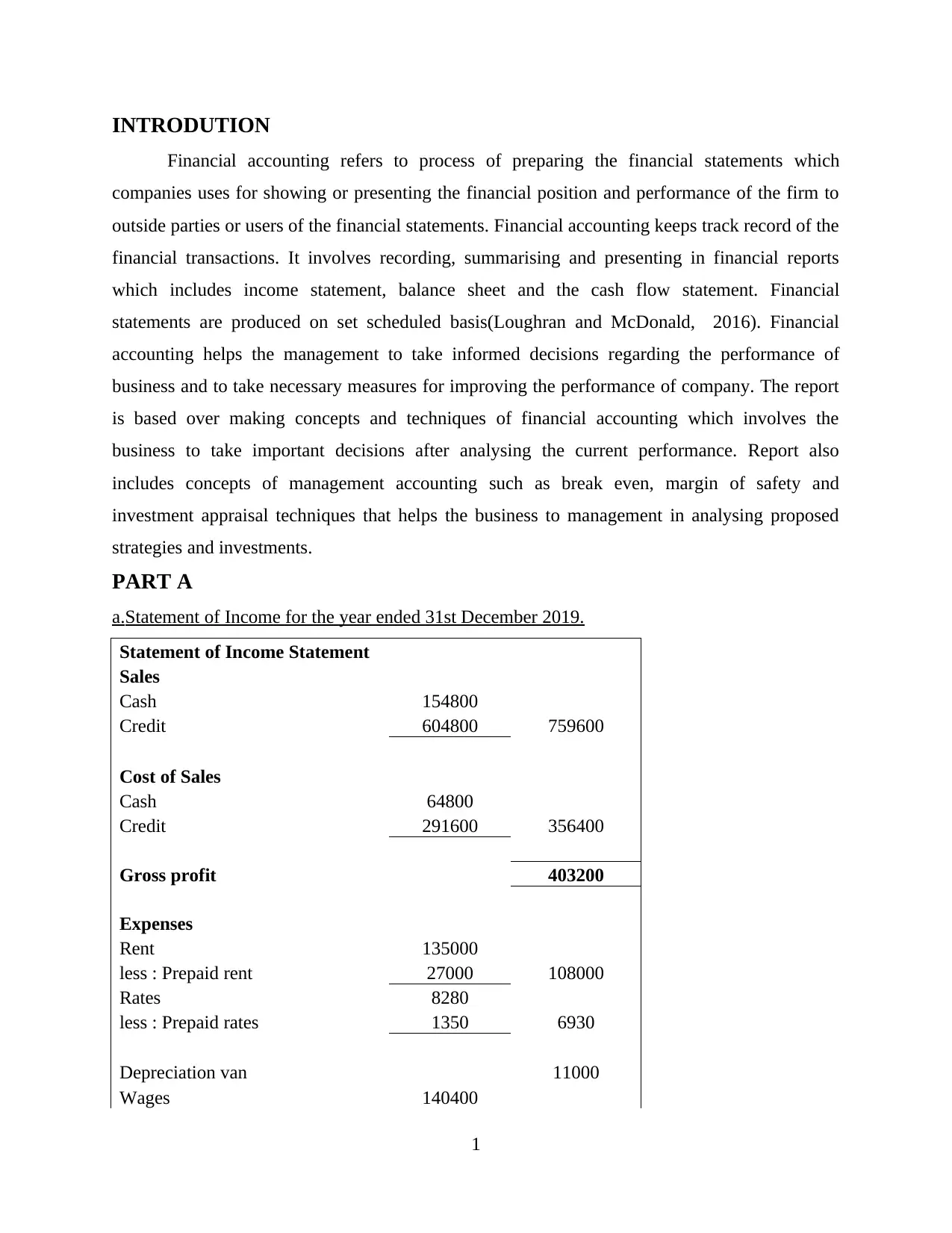

INTRODUTION

Financial accounting refers to process of preparing the financial statements which

companies uses for showing or presenting the financial position and performance of the firm to

outside parties or users of the financial statements. Financial accounting keeps track record of the

financial transactions. It involves recording, summarising and presenting in financial reports

which includes income statement, balance sheet and the cash flow statement. Financial

statements are produced on set scheduled basis(Loughran and McDonald, 2016). Financial

accounting helps the management to take informed decisions regarding the performance of

business and to take necessary measures for improving the performance of company. The report

is based over making concepts and techniques of financial accounting which involves the

business to take important decisions after analysing the current performance. Report also

includes concepts of management accounting such as break even, margin of safety and

investment appraisal techniques that helps the business to management in analysing proposed

strategies and investments.

PART A

a.Statement of Income for the year ended 31st December 2019.

Statement of Income Statement

Sales

Cash 154800

Credit 604800 759600

Cost of Sales

Cash 64800

Credit 291600 356400

Gross profit 403200

Expenses

Rent 135000

less : Prepaid rent 27000 108000

Rates 8280

less : Prepaid rates 1350 6930

Depreciation van 11000

Wages 140400

1

Financial accounting refers to process of preparing the financial statements which

companies uses for showing or presenting the financial position and performance of the firm to

outside parties or users of the financial statements. Financial accounting keeps track record of the

financial transactions. It involves recording, summarising and presenting in financial reports

which includes income statement, balance sheet and the cash flow statement. Financial

statements are produced on set scheduled basis(Loughran and McDonald, 2016). Financial

accounting helps the management to take informed decisions regarding the performance of

business and to take necessary measures for improving the performance of company. The report

is based over making concepts and techniques of financial accounting which involves the

business to take important decisions after analysing the current performance. Report also

includes concepts of management accounting such as break even, margin of safety and

investment appraisal techniques that helps the business to management in analysing proposed

strategies and investments.

PART A

a.Statement of Income for the year ended 31st December 2019.

Statement of Income Statement

Sales

Cash 154800

Credit 604800 759600

Cost of Sales

Cash 64800

Credit 291600 356400

Gross profit 403200

Expenses

Rent 135000

less : Prepaid rent 27000 108000

Rates 8280

less : Prepaid rates 1350 6930

Depreciation van 11000

Wages 140400

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Add ; Outstanding Wages 2610 143010

Electricity Bills 6840

Van Expenses 40320

Total Expenses 316100

Net Profit 87100

Workings

Rent

Annual Rent 108000

Rent Paid 135000

Prepaid Rent -27000

Rate

Jan - March 2019 2880

April - December 5400 * (9/12)

4050

Total rates for the year 6930

Prepaid 5400-4050

Jan - March 2020 1350

Van

Cost of van 72000

Useful Life 6

Residual value 6000

Depreciation

(72000-

6000)/6

11000

Trade Receivables

Sales 604800

Cash Collections 525600

Bad Debts 1800

Tr Receivables at year

end 77400

Trade Payables

2

Electricity Bills 6840

Van Expenses 40320

Total Expenses 316100

Net Profit 87100

Workings

Rent

Annual Rent 108000

Rent Paid 135000

Prepaid Rent -27000

Rate

Jan - March 2019 2880

April - December 5400 * (9/12)

4050

Total rates for the year 6930

Prepaid 5400-4050

Jan - March 2020 1350

Van

Cost of van 72000

Useful Life 6

Residual value 6000

Depreciation

(72000-

6000)/6

11000

Trade Receivables

Sales 604800

Cash Collections 525600

Bad Debts 1800

Tr Receivables at year

end 77400

Trade Payables

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

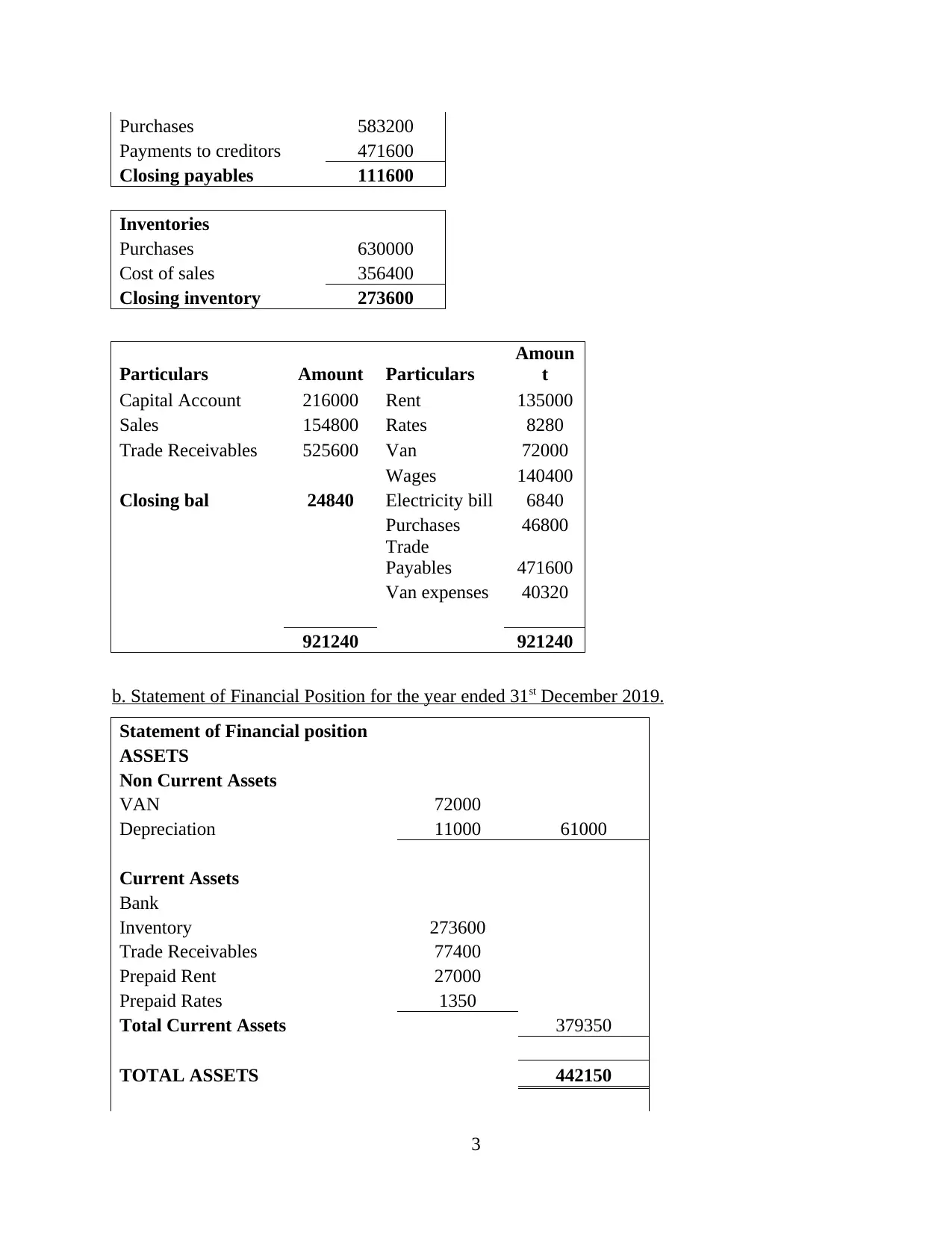

Purchases 583200

Payments to creditors 471600

Closing payables 111600

Inventories

Purchases 630000

Cost of sales 356400

Closing inventory 273600

Particulars Amount Particulars

Amoun

t

Capital Account 216000 Rent 135000

Sales 154800 Rates 8280

Trade Receivables 525600 Van 72000

Wages 140400

Closing bal 24840 Electricity bill 6840

Purchases 46800

Trade

Payables 471600

Van expenses 40320

921240 921240

b. Statement of Financial Position for the year ended 31st December 2019.

Statement of Financial position

ASSETS

Non Current Assets

VAN 72000

Depreciation 11000 61000

Current Assets

Bank

Inventory 273600

Trade Receivables 77400

Prepaid Rent 27000

Prepaid Rates 1350

Total Current Assets 379350

TOTAL ASSETS 442150

3

Payments to creditors 471600

Closing payables 111600

Inventories

Purchases 630000

Cost of sales 356400

Closing inventory 273600

Particulars Amount Particulars

Amoun

t

Capital Account 216000 Rent 135000

Sales 154800 Rates 8280

Trade Receivables 525600 Van 72000

Wages 140400

Closing bal 24840 Electricity bill 6840

Purchases 46800

Trade

Payables 471600

Van expenses 40320

921240 921240

b. Statement of Financial Position for the year ended 31st December 2019.

Statement of Financial position

ASSETS

Non Current Assets

VAN 72000

Depreciation 11000 61000

Current Assets

Bank

Inventory 273600

Trade Receivables 77400

Prepaid Rent 27000

Prepaid Rates 1350

Total Current Assets 379350

TOTAL ASSETS 442150

3

EQUITY AND LIABILITIES

Equity 216000

Retained Earnings 87100

Total Equity 303100

LIABILITIES

Non Current Liabilities

Borrowings 0 0

Current Liabilities

Bank Overdraft 24840

Trade Payables 111600

Outstanding wages 2610 139050

TOTAL EQUITY &

LIABILITIES 442150

Analysis

Collins Colman limited has started new business which began trading from 1st January

2019. Financial position of the company does not seem to be strong. It could be analysed that

liquidity position of the company is very weak. It is having negative cash balance in the first

year. The income statement shows profits where the cash position of company is negative which

shows that it is very essential to analyse both income and position statement of company. The

situation can cause significant implications over the stakeholders and people planning to invest

in the company. Colman limited is required to take considerable steps for improving the

performance of business so that it could manage the operations of business by bringing the

liquidity position to positive (Atrill and McLaney, 2006). It has to increase the current assets and

control over expenses. It could also loans for meeting the working capital requirements of the

business. This will enable the company to run its operations properly.

PART B

a. Contribution of the microwave towards covering the fixed costs

Selling Price 40

Variable Costs

Materials 15.75

Labour 8.85

4

Equity 216000

Retained Earnings 87100

Total Equity 303100

LIABILITIES

Non Current Liabilities

Borrowings 0 0

Current Liabilities

Bank Overdraft 24840

Trade Payables 111600

Outstanding wages 2610 139050

TOTAL EQUITY &

LIABILITIES 442150

Analysis

Collins Colman limited has started new business which began trading from 1st January

2019. Financial position of the company does not seem to be strong. It could be analysed that

liquidity position of the company is very weak. It is having negative cash balance in the first

year. The income statement shows profits where the cash position of company is negative which

shows that it is very essential to analyse both income and position statement of company. The

situation can cause significant implications over the stakeholders and people planning to invest

in the company. Colman limited is required to take considerable steps for improving the

performance of business so that it could manage the operations of business by bringing the

liquidity position to positive (Atrill and McLaney, 2006). It has to increase the current assets and

control over expenses. It could also loans for meeting the working capital requirements of the

business. This will enable the company to run its operations properly.

PART B

a. Contribution of the microwave towards covering the fixed costs

Selling Price 40

Variable Costs

Materials 15.75

Labour 8.85

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

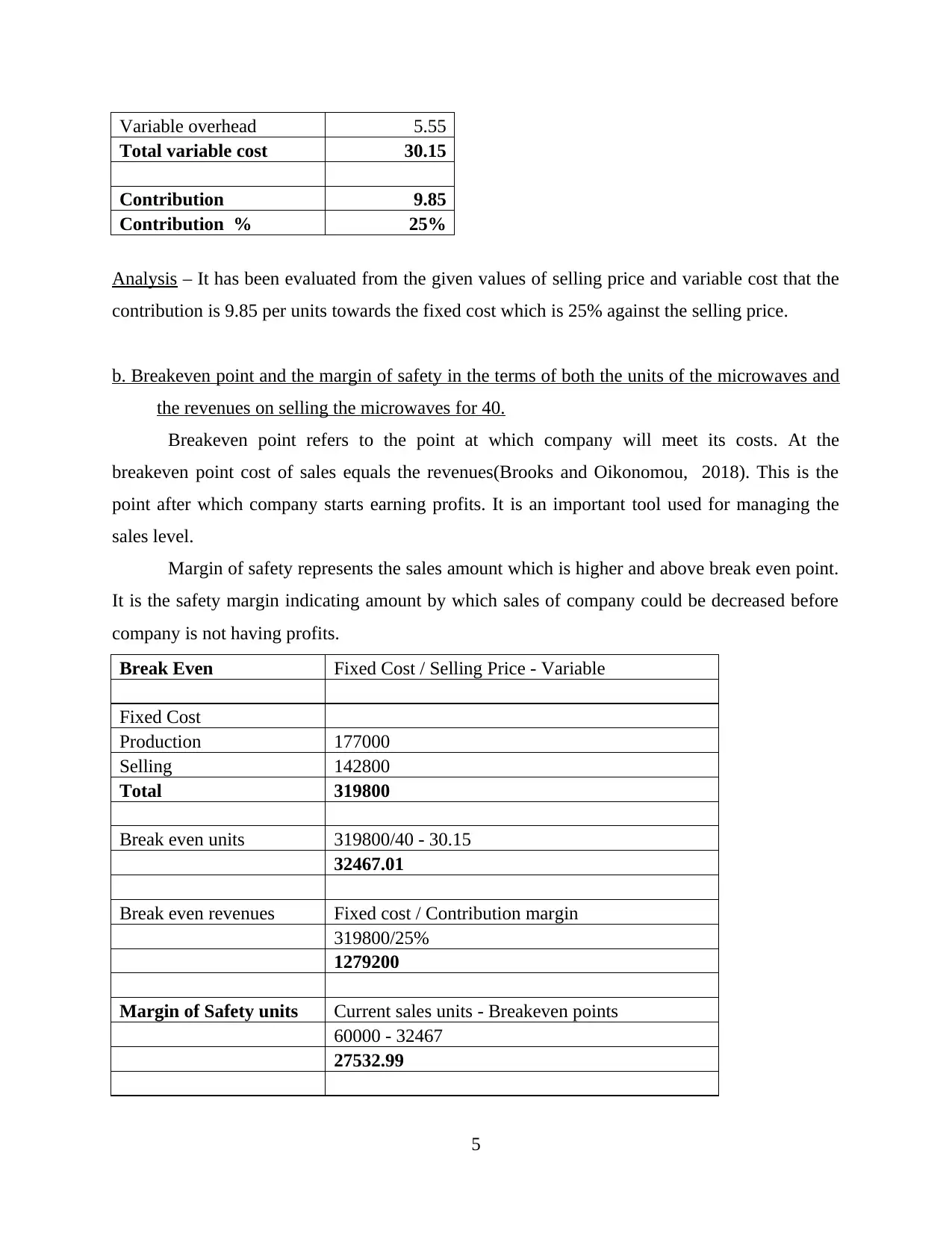

Variable overhead 5.55

Total variable cost 30.15

Contribution 9.85

Contribution % 25%

Analysis – It has been evaluated from the given values of selling price and variable cost that the

contribution is 9.85 per units towards the fixed cost which is 25% against the selling price.

b. Breakeven point and the margin of safety in the terms of both the units of the microwaves and

the revenues on selling the microwaves for 40.

Breakeven point refers to the point at which company will meet its costs. At the

breakeven point cost of sales equals the revenues(Brooks and Oikonomou, 2018). This is the

point after which company starts earning profits. It is an important tool used for managing the

sales level.

Margin of safety represents the sales amount which is higher and above break even point.

It is the safety margin indicating amount by which sales of company could be decreased before

company is not having profits.

Break Even Fixed Cost / Selling Price - Variable

Fixed Cost

Production 177000

Selling 142800

Total 319800

Break even units 319800/40 - 30.15

32467.01

Break even revenues Fixed cost / Contribution margin

319800/25%

1279200

Margin of Safety units Current sales units - Breakeven points

60000 - 32467

27532.99

5

Total variable cost 30.15

Contribution 9.85

Contribution % 25%

Analysis – It has been evaluated from the given values of selling price and variable cost that the

contribution is 9.85 per units towards the fixed cost which is 25% against the selling price.

b. Breakeven point and the margin of safety in the terms of both the units of the microwaves and

the revenues on selling the microwaves for 40.

Breakeven point refers to the point at which company will meet its costs. At the

breakeven point cost of sales equals the revenues(Brooks and Oikonomou, 2018). This is the

point after which company starts earning profits. It is an important tool used for managing the

sales level.

Margin of safety represents the sales amount which is higher and above break even point.

It is the safety margin indicating amount by which sales of company could be decreased before

company is not having profits.

Break Even Fixed Cost / Selling Price - Variable

Fixed Cost

Production 177000

Selling 142800

Total 319800

Break even units 319800/40 - 30.15

32467.01

Break even revenues Fixed cost / Contribution margin

319800/25%

1279200

Margin of Safety units Current sales units - Breakeven points

60000 - 32467

27532.99

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Margin of safety in units Current sales - Break even sales

Current sales 2400000

Break even sales 1279200

Margin of safety 1120800

Analysis – It could be analysed that the company is presently having selling price of 40 and

variable costs of 30.15. The fixed cost of company from production and selling totalled to

319800. The break even units of company are 32467 microwaves and in revenues is 1,279,200.

On the other margin of safety is in units is 27532 microwaves and in revenues is

1,120,800. This is the amount that could be decreased if company do not have any profit.

c. Profits made by Parksmead Limited if produced and selling 60000 of the microwaves

Calculation of Profits

Units 60000

Sales 40 2400000

Variable Cost

Materials 15.75 945000

Labour 8.85 531000

Variable overhead 5.55 333000

Contribution 591000

Fixed Cost

Production 177000

Selling plc 142800

Profit 271200

Analysis –

It could be analysed that at the sales and production level of 60000 microwaves will be

earning profits of 271,200 after meeting all the variable and fixed costs. The variable cost per

unit is 30.15 and for 60000 units it has totalled to 1809000 and fixed costs are 319,800.

6

Current sales 2400000

Break even sales 1279200

Margin of safety 1120800

Analysis – It could be analysed that the company is presently having selling price of 40 and

variable costs of 30.15. The fixed cost of company from production and selling totalled to

319800. The break even units of company are 32467 microwaves and in revenues is 1,279,200.

On the other margin of safety is in units is 27532 microwaves and in revenues is

1,120,800. This is the amount that could be decreased if company do not have any profit.

c. Profits made by Parksmead Limited if produced and selling 60000 of the microwaves

Calculation of Profits

Units 60000

Sales 40 2400000

Variable Cost

Materials 15.75 945000

Labour 8.85 531000

Variable overhead 5.55 333000

Contribution 591000

Fixed Cost

Production 177000

Selling plc 142800

Profit 271200

Analysis –

It could be analysed that at the sales and production level of 60000 microwaves will be

earning profits of 271,200 after meeting all the variable and fixed costs. The variable cost per

unit is 30.15 and for 60000 units it has totalled to 1809000 and fixed costs are 319,800.

6

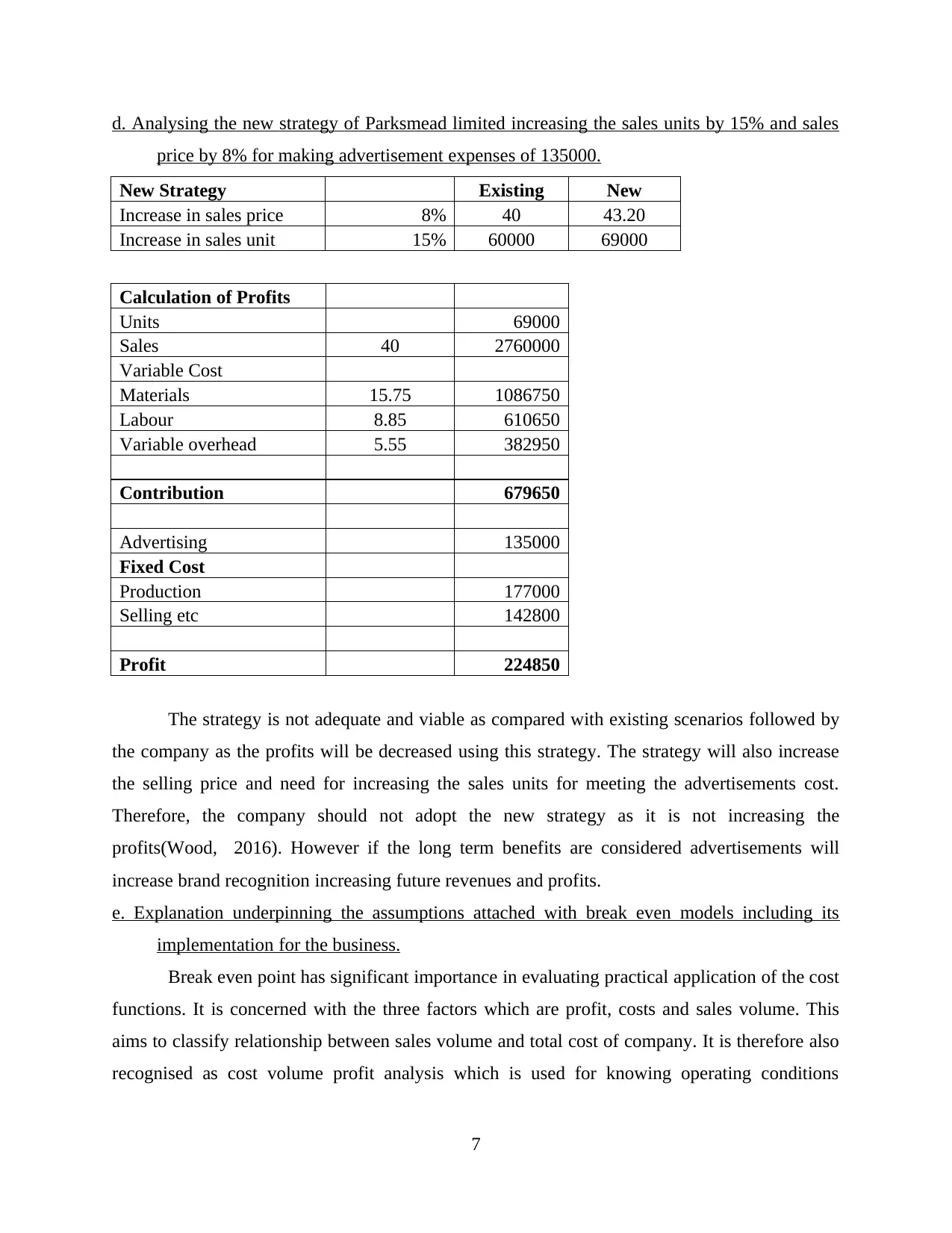

d. Analysing the new strategy of Parksmead limited increasing the sales units by 15% and sales

price by 8% for making advertisement expenses of 135000.

New Strategy Existing New

Increase in sales price 8% 40 43.20

Increase in sales unit 15% 60000 69000

Calculation of Profits

Units 69000

Sales 40 2760000

Variable Cost

Materials 15.75 1086750

Labour 8.85 610650

Variable overhead 5.55 382950

Contribution 679650

Advertising 135000

Fixed Cost

Production 177000

Selling etc 142800

Profit 224850

The strategy is not adequate and viable as compared with existing scenarios followed by

the company as the profits will be decreased using this strategy. The strategy will also increase

the selling price and need for increasing the sales units for meeting the advertisements cost.

Therefore, the company should not adopt the new strategy as it is not increasing the

profits(Wood, 2016). However if the long term benefits are considered advertisements will

increase brand recognition increasing future revenues and profits.

e. Explanation underpinning the assumptions attached with break even models including its

implementation for the business.

Break even point has significant importance in evaluating practical application of the cost

functions. It is concerned with the three factors which are profit, costs and sales volume. This

aims to classify relationship between sales volume and total cost of company. It is therefore also

recognised as cost volume profit analysis which is used for knowing operating conditions

7

price by 8% for making advertisement expenses of 135000.

New Strategy Existing New

Increase in sales price 8% 40 43.20

Increase in sales unit 15% 60000 69000

Calculation of Profits

Units 69000

Sales 40 2760000

Variable Cost

Materials 15.75 1086750

Labour 8.85 610650

Variable overhead 5.55 382950

Contribution 679650

Advertising 135000

Fixed Cost

Production 177000

Selling etc 142800

Profit 224850

The strategy is not adequate and viable as compared with existing scenarios followed by

the company as the profits will be decreased using this strategy. The strategy will also increase

the selling price and need for increasing the sales units for meeting the advertisements cost.

Therefore, the company should not adopt the new strategy as it is not increasing the

profits(Wood, 2016). However if the long term benefits are considered advertisements will

increase brand recognition increasing future revenues and profits.

e. Explanation underpinning the assumptions attached with break even models including its

implementation for the business.

Break even point has significant importance in evaluating practical application of the cost

functions. It is concerned with the three factors which are profit, costs and sales volume. This

aims to classify relationship between sales volume and total cost of company. It is therefore also

recognised as cost volume profit analysis which is used for knowing operating conditions

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

existing when company breaks even. There are number of assumptions taken in the break even

analysis which are ;

All costs are classified in variable and fixed costs and does not considers semi – variable

costs.

Behaviour of different costs is linear which means costs shown on graph will form

straight line.

Total amount of the fixed cost remains constant at every output level and the variable

costs fluctuate in proportion of the output.

Selling price will be constant at every level of output that means prices of units will not

be changing at different sales level.

Price for the inputs such as material, labour, etc remains constant for the calculations.

No change will be there for efficiency of the men & machines and the technological

methods will be constant.

Output or sales volume is the only factor affecting the cost.

The break even could be applied successfully by the range of differing businesses. It

enables the business to decide the sales which is required to be achieved for covering the cost

and for earning desirable profits. It could be used for different types of businesses to make the

strategies regarding their sales level and also for the purpose of controlling the costs(Goodacre,

Gaunt and Henry, 2017). It could be used by both manufacturing and service companies as both

industries have variable cost and fixed cost that could be used for identifying breakeven point for

covering cost and earning profit.

PART C

a. Calculating Payback period, Accounting rate of return and Net Present Value of machine and

recommendations for purchase of machine

Cost of new machine 8000000

Cash Flows

Cash Inflows 3400000

Cash Outflow -1280000

less : Depreciation -1400000

Cash Flows 720000

Add : depreciation 1400000

8

analysis which are ;

All costs are classified in variable and fixed costs and does not considers semi – variable

costs.

Behaviour of different costs is linear which means costs shown on graph will form

straight line.

Total amount of the fixed cost remains constant at every output level and the variable

costs fluctuate in proportion of the output.

Selling price will be constant at every level of output that means prices of units will not

be changing at different sales level.

Price for the inputs such as material, labour, etc remains constant for the calculations.

No change will be there for efficiency of the men & machines and the technological

methods will be constant.

Output or sales volume is the only factor affecting the cost.

The break even could be applied successfully by the range of differing businesses. It

enables the business to decide the sales which is required to be achieved for covering the cost

and for earning desirable profits. It could be used for different types of businesses to make the

strategies regarding their sales level and also for the purpose of controlling the costs(Goodacre,

Gaunt and Henry, 2017). It could be used by both manufacturing and service companies as both

industries have variable cost and fixed cost that could be used for identifying breakeven point for

covering cost and earning profit.

PART C

a. Calculating Payback period, Accounting rate of return and Net Present Value of machine and

recommendations for purchase of machine

Cost of new machine 8000000

Cash Flows

Cash Inflows 3400000

Cash Outflow -1280000

less : Depreciation -1400000

Cash Flows 720000

Add : depreciation 1400000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

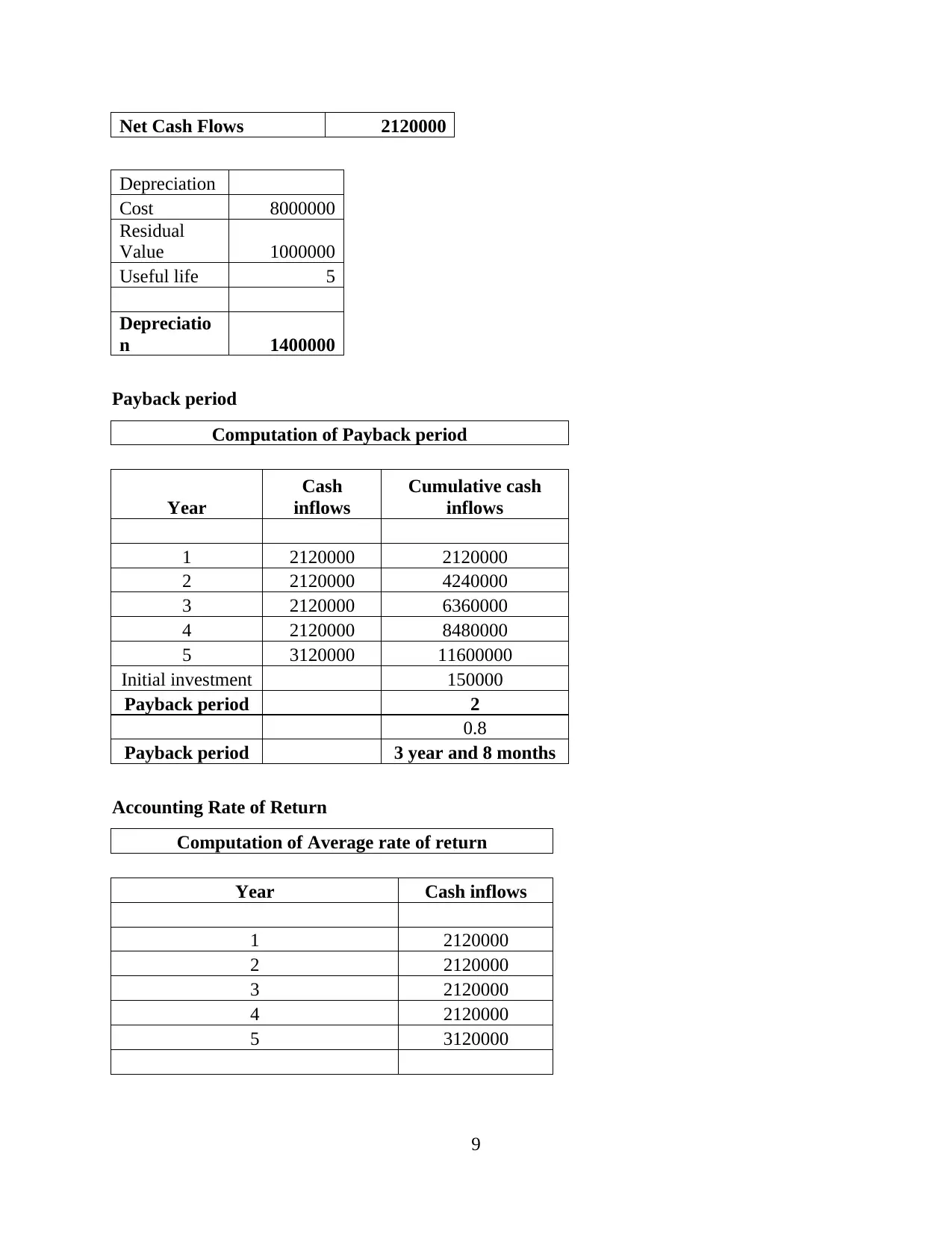

Net Cash Flows 2120000

Depreciation

Cost 8000000

Residual

Value 1000000

Useful life 5

Depreciatio

n 1400000

Payback period

Computation of Payback period

Year

Cash

inflows

Cumulative cash

inflows

1 2120000 2120000

2 2120000 4240000

3 2120000 6360000

4 2120000 8480000

5 3120000 11600000

Initial investment 150000

Payback period 2

0.8

Payback period 3 year and 8 months

Accounting Rate of Return

Computation of Average rate of return

Year Cash inflows

1 2120000

2 2120000

3 2120000

4 2120000

5 3120000

9

Depreciation

Cost 8000000

Residual

Value 1000000

Useful life 5

Depreciatio

n 1400000

Payback period

Computation of Payback period

Year

Cash

inflows

Cumulative cash

inflows

1 2120000 2120000

2 2120000 4240000

3 2120000 6360000

4 2120000 8480000

5 3120000 11600000

Initial investment 150000

Payback period 2

0.8

Payback period 3 year and 8 months

Accounting Rate of Return

Computation of Average rate of return

Year Cash inflows

1 2120000

2 2120000

3 2120000

4 2120000

5 3120000

9

Average profit or cash inflow 2320000

Average initial investment 8000000

average initial investment [(initial

investment + scrap value) / 2]

ARR 29%

Net Present Value

Computation of NPV

Year

Cash

inflows

PV

factor @

9%

Discounted

cash inflows

1 2120000 0.917 1944954

2 2120000 0.842 1784362

3 2120000 0.772 1637029

4 2120000 0.708 1501861

5 3120000 0.650 2027786

Total discounted cash inflow 8895992

Initial investment 8000000

NPV (Total discounted cash

inflows - initial investment) 895992

Recommendation

It could be evaluated from the above analysis that the project of machine is viable as the

NPV of the project is positive. The ARR of the project is 29% that adequate and high. Payback

period of the machine is 3 years and 8 months which is higher. NPV and ARR suggests the

project to be viable and acceptable where the longer payback period reduces the profits that

could be generated from the project(Chang and Chow, 2019). Outcomes of investment appraisals

shows that the project is viable and the cash flows from the machine will cover the cost and also

allow company to earn profits for one year. Therefore the project should be accepted by the

company.

10

Average initial investment 8000000

average initial investment [(initial

investment + scrap value) / 2]

ARR 29%

Net Present Value

Computation of NPV

Year

Cash

inflows

PV

factor @

9%

Discounted

cash inflows

1 2120000 0.917 1944954

2 2120000 0.842 1784362

3 2120000 0.772 1637029

4 2120000 0.708 1501861

5 3120000 0.650 2027786

Total discounted cash inflow 8895992

Initial investment 8000000

NPV (Total discounted cash

inflows - initial investment) 895992

Recommendation

It could be evaluated from the above analysis that the project of machine is viable as the

NPV of the project is positive. The ARR of the project is 29% that adequate and high. Payback

period of the machine is 3 years and 8 months which is higher. NPV and ARR suggests the

project to be viable and acceptable where the longer payback period reduces the profits that

could be generated from the project(Chang and Chow, 2019). Outcomes of investment appraisals

shows that the project is viable and the cash flows from the machine will cover the cost and also

allow company to earn profits for one year. Therefore the project should be accepted by the

company.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.