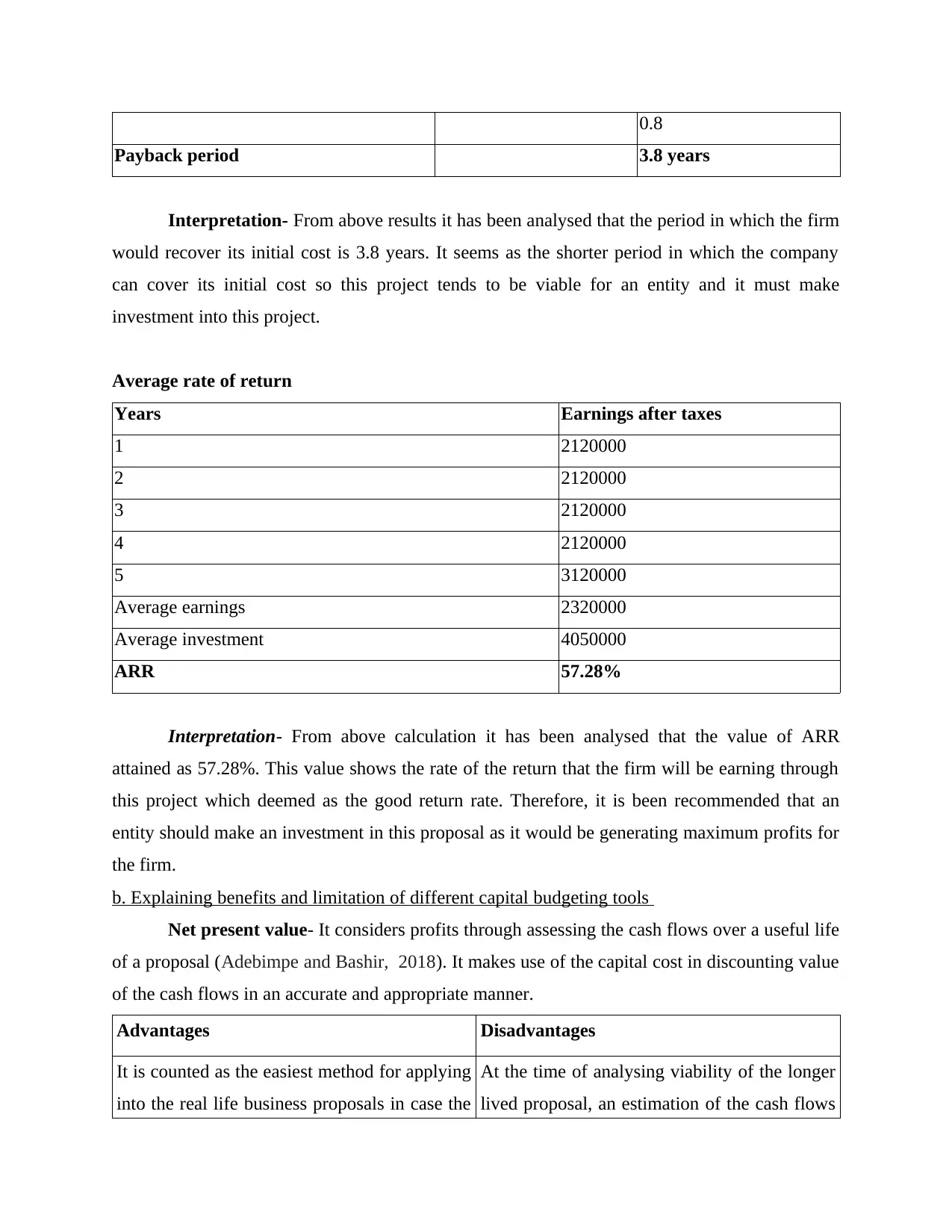

Introduction to Accounting and Finance

VerifiedAdded on 2023/01/07

|20

|3983

|67

AI Summary

This document provides an introduction to accounting and finance. It covers topics such as income statements, break-even analysis, and evaluating business strategies. The document also includes calculations for payback, ARR, and NPV. Suitable for students studying accounting and finance courses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Introduction to Accounting and

Finance

Finance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

PART A...........................................................................................................................................3

PART B............................................................................................................................................7

a. Determining the contribution of the each microwave in regard to covering the fixed cost....7

b. Computation of BEP and the margin of safety if microwave is sold at the price of £40........7

c. Computation of profit that Parks mead Ltd would make by selling 60000 units of

microwaves at the price of £40...................................................................................................8

d. Evaluating and analysing the new strategy of Parksmead Ltd................................................9

e. Underpinning assumptions attached to the BEP model........................................................10

Part C.............................................................................................................................................11

a. Computing payback, ARR, and NPV of the firm .................................................................11

b. Explaining benefits and limitation of different capital budgeting tools ...............................13

c. Explaining main advantages and disadvantages of making use of the budget as the strategic

technique ..................................................................................................................................15

REFERENCES .............................................................................................................................17

PART A...........................................................................................................................................3

PART B............................................................................................................................................7

a. Determining the contribution of the each microwave in regard to covering the fixed cost....7

b. Computation of BEP and the margin of safety if microwave is sold at the price of £40........7

c. Computation of profit that Parks mead Ltd would make by selling 60000 units of

microwaves at the price of £40...................................................................................................8

d. Evaluating and analysing the new strategy of Parksmead Ltd................................................9

e. Underpinning assumptions attached to the BEP model........................................................10

Part C.............................................................................................................................................11

a. Computing payback, ARR, and NPV of the firm .................................................................11

b. Explaining benefits and limitation of different capital budgeting tools ...............................13

c. Explaining main advantages and disadvantages of making use of the budget as the strategic

technique ..................................................................................................................................15

REFERENCES .............................................................................................................................17

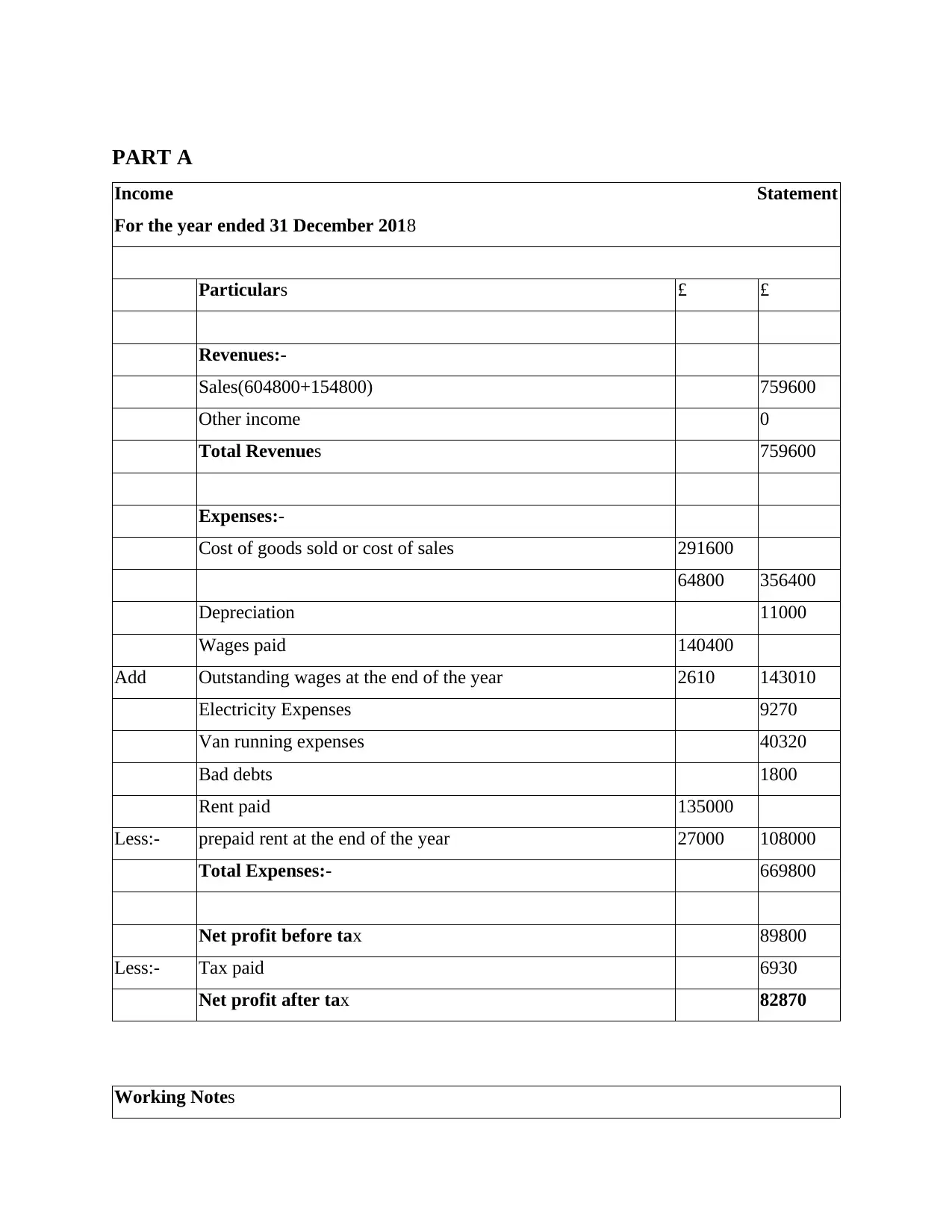

PART A

Income Statement

For the year ended 31 December 2018

Particulars £ £

Revenues:-

Sales(604800+154800) 759600

Other income 0

Total Revenues 759600

Expenses:-

Cost of goods sold or cost of sales 291600

64800 356400

Depreciation 11000

Wages paid 140400

Add Outstanding wages at the end of the year 2610 143010

Electricity Expenses 9270

Van running expenses 40320

Bad debts 1800

Rent paid 135000

Less:- prepaid rent at the end of the year 27000 108000

Total Expenses:- 669800

Net profit before tax 89800

Less:- Tax paid 6930

Net profit after tax 82870

Working Notes

Income Statement

For the year ended 31 December 2018

Particulars £ £

Revenues:-

Sales(604800+154800) 759600

Other income 0

Total Revenues 759600

Expenses:-

Cost of goods sold or cost of sales 291600

64800 356400

Depreciation 11000

Wages paid 140400

Add Outstanding wages at the end of the year 2610 143010

Electricity Expenses 9270

Van running expenses 40320

Bad debts 1800

Rent paid 135000

Less:- prepaid rent at the end of the year 27000 108000

Total Expenses:- 669800

Net profit before tax 89800

Less:- Tax paid 6930

Net profit after tax 82870

Working Notes

1 Total Sales

credit sales 604800

cash sales 154800

759600

2 Depreciation

Purchase Price of Van 72000

scarp value 6000

life in years 6

Depreciation 11000

3 Tax Computation

Tax upto 31 march 2018 2880

Add:- Tax from 1 april 2018 to 31 march 2019 5400

Less:- prepaid tax of 3 months

(from 1january 2019 to 31 march 2019) 1350

6930

4 Electricity Expenses:-

Expenses paid 6840

Add:- Outstanding expenses at the end of the year 2430

9270

Balance Sheet

For the year ended 31 December 2018

credit sales 604800

cash sales 154800

759600

2 Depreciation

Purchase Price of Van 72000

scarp value 6000

life in years 6

Depreciation 11000

3 Tax Computation

Tax upto 31 march 2018 2880

Add:- Tax from 1 april 2018 to 31 march 2019 5400

Less:- prepaid tax of 3 months

(from 1january 2019 to 31 march 2019) 1350

6930

4 Electricity Expenses:-

Expenses paid 6840

Add:- Outstanding expenses at the end of the year 2430

9270

Balance Sheet

For the year ended 31 December 2018

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

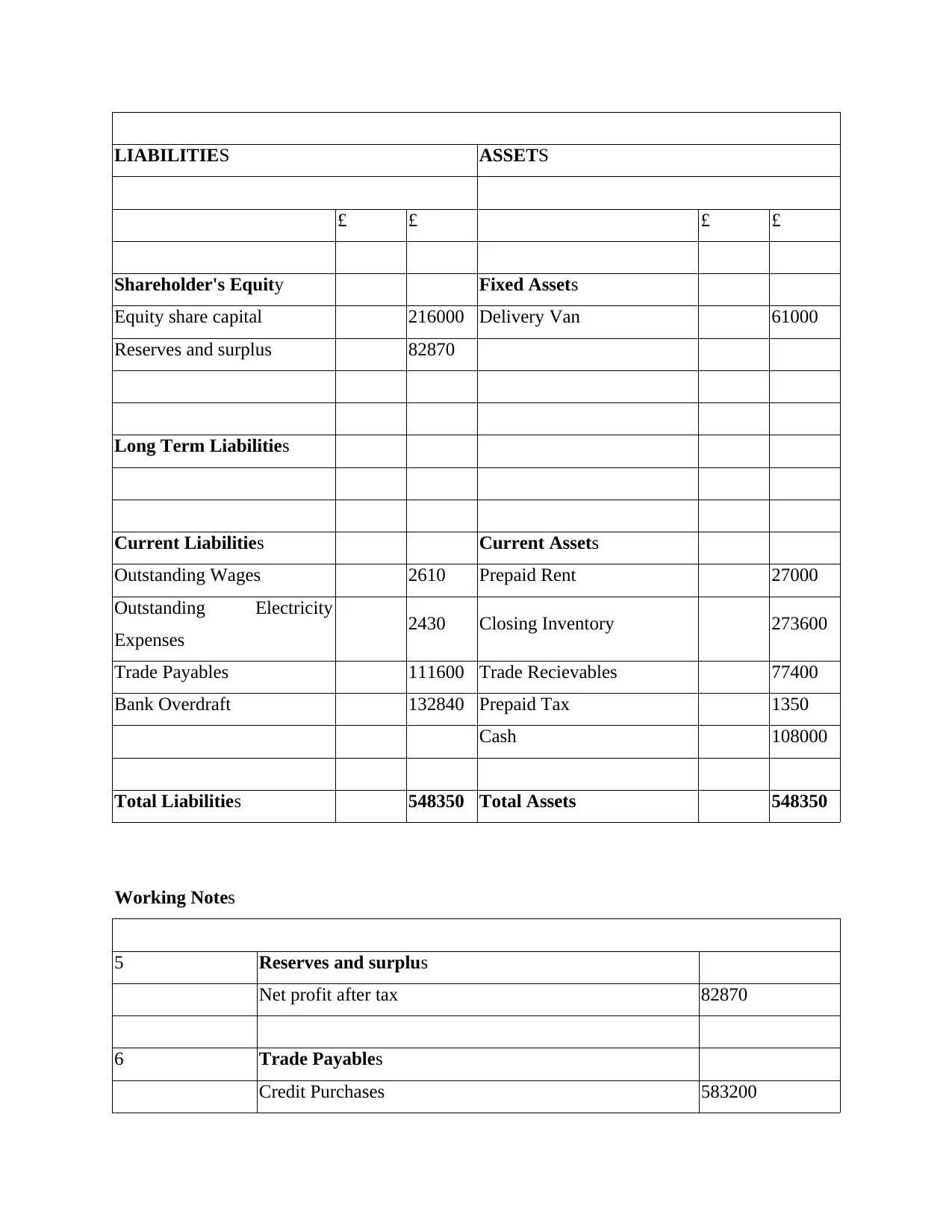

LIABILITIES ASSETS

£ £ £ £

Shareholder's Equity Fixed Assets

Equity share capital 216000 Delivery Van 61000

Reserves and surplus 82870

Long Term Liabilities

Current Liabilities Current Assets

Outstanding Wages 2610 Prepaid Rent 27000

Outstanding Electricity

Expenses 2430 Closing Inventory 273600

Trade Payables 111600 Trade Recievables 77400

Bank Overdraft 132840 Prepaid Tax 1350

Cash 108000

Total Liabilities 548350 Total Assets 548350

Working Notes

5 Reserves and surplus

Net profit after tax 82870

6 Trade Payables

Credit Purchases 583200

£ £ £ £

Shareholder's Equity Fixed Assets

Equity share capital 216000 Delivery Van 61000

Reserves and surplus 82870

Long Term Liabilities

Current Liabilities Current Assets

Outstanding Wages 2610 Prepaid Rent 27000

Outstanding Electricity

Expenses 2430 Closing Inventory 273600

Trade Payables 111600 Trade Recievables 77400

Bank Overdraft 132840 Prepaid Tax 1350

Cash 108000

Total Liabilities 548350 Total Assets 548350

Working Notes

5 Reserves and surplus

Net profit after tax 82870

6 Trade Payables

Credit Purchases 583200

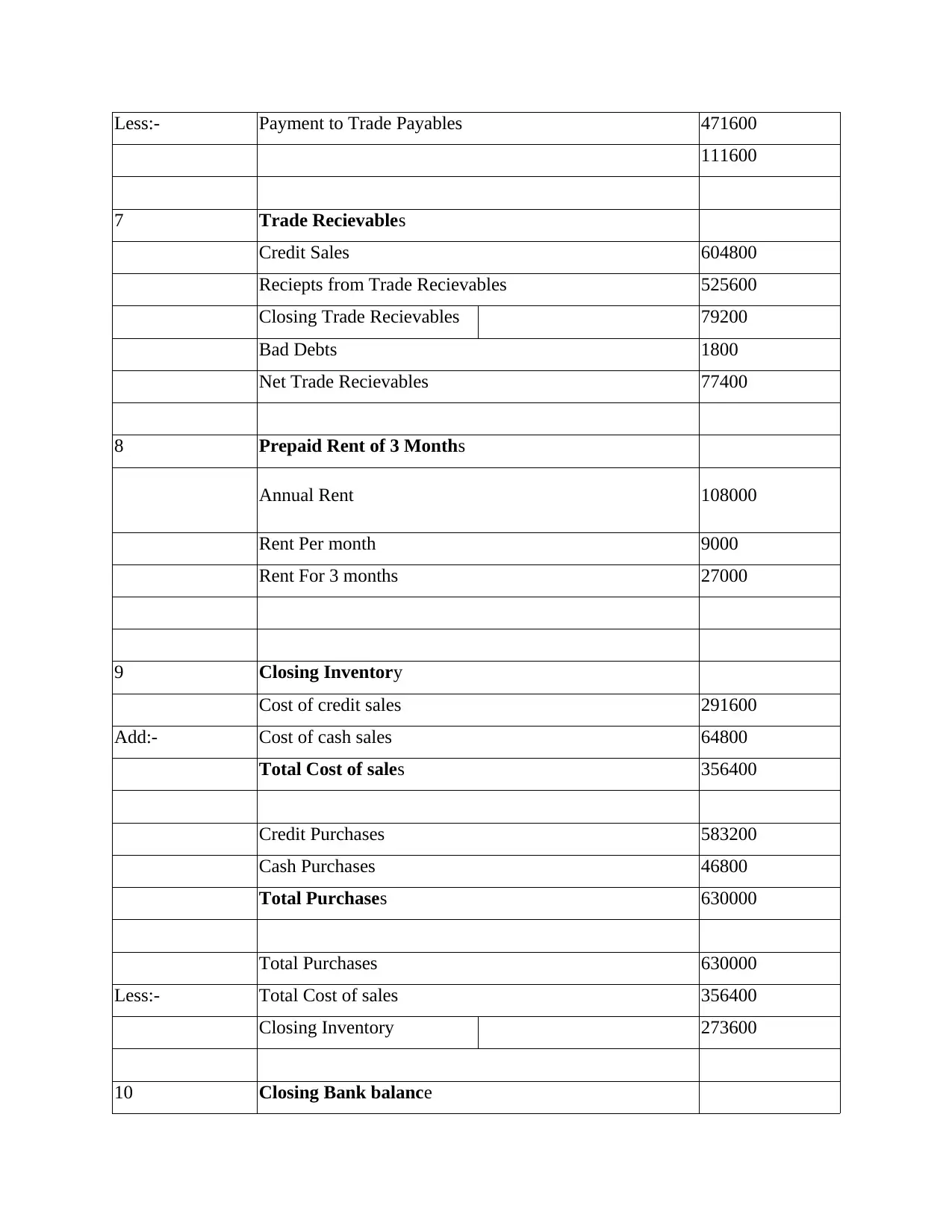

Less:- Payment to Trade Payables 471600

111600

7 Trade Recievables

Credit Sales 604800

Reciepts from Trade Recievables 525600

Closing Trade Recievables 79200

Bad Debts 1800

Net Trade Recievables 77400

8 Prepaid Rent of 3 Months

Annual Rent 108000

Rent Per month 9000

Rent For 3 months 27000

9 Closing Inventory

Cost of credit sales 291600

Add:- Cost of cash sales 64800

Total Cost of sales 356400

Credit Purchases 583200

Cash Purchases 46800

Total Purchases 630000

Total Purchases 630000

Less:- Total Cost of sales 356400

Closing Inventory 273600

10 Closing Bank balance

111600

7 Trade Recievables

Credit Sales 604800

Reciepts from Trade Recievables 525600

Closing Trade Recievables 79200

Bad Debts 1800

Net Trade Recievables 77400

8 Prepaid Rent of 3 Months

Annual Rent 108000

Rent Per month 9000

Rent For 3 months 27000

9 Closing Inventory

Cost of credit sales 291600

Add:- Cost of cash sales 64800

Total Cost of sales 356400

Credit Purchases 583200

Cash Purchases 46800

Total Purchases 630000

Total Purchases 630000

Less:- Total Cost of sales 356400

Closing Inventory 273600

10 Closing Bank balance

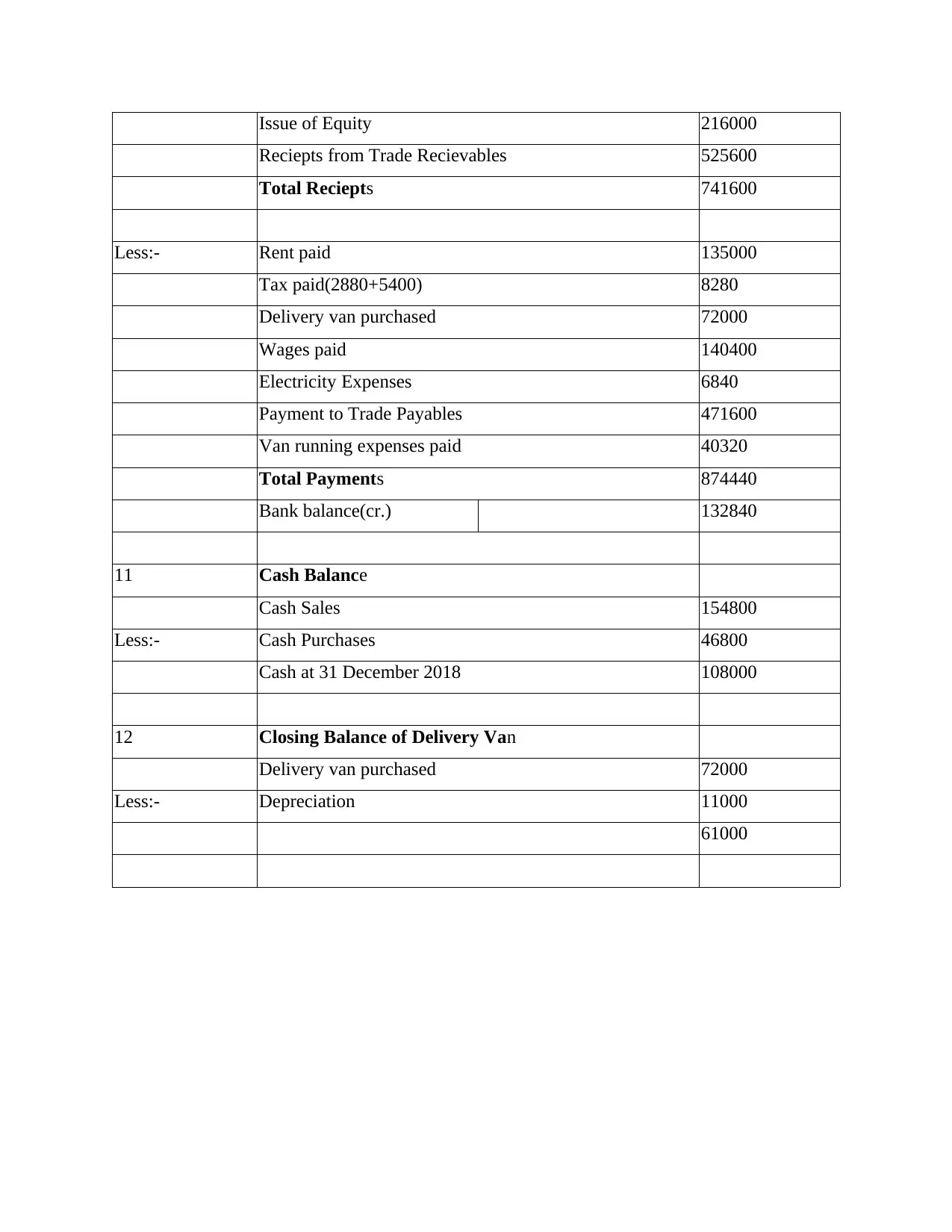

Issue of Equity 216000

Reciepts from Trade Recievables 525600

Total Reciepts 741600

Less:- Rent paid 135000

Tax paid(2880+5400) 8280

Delivery van purchased 72000

Wages paid 140400

Electricity Expenses 6840

Payment to Trade Payables 471600

Van running expenses paid 40320

Total Payments 874440

Bank balance(cr.) 132840

11 Cash Balance

Cash Sales 154800

Less:- Cash Purchases 46800

Cash at 31 December 2018 108000

12 Closing Balance of Delivery Van

Delivery van purchased 72000

Less:- Depreciation 11000

61000

Reciepts from Trade Recievables 525600

Total Reciepts 741600

Less:- Rent paid 135000

Tax paid(2880+5400) 8280

Delivery van purchased 72000

Wages paid 140400

Electricity Expenses 6840

Payment to Trade Payables 471600

Van running expenses paid 40320

Total Payments 874440

Bank balance(cr.) 132840

11 Cash Balance

Cash Sales 154800

Less:- Cash Purchases 46800

Cash at 31 December 2018 108000

12 Closing Balance of Delivery Van

Delivery van purchased 72000

Less:- Depreciation 11000

61000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART B

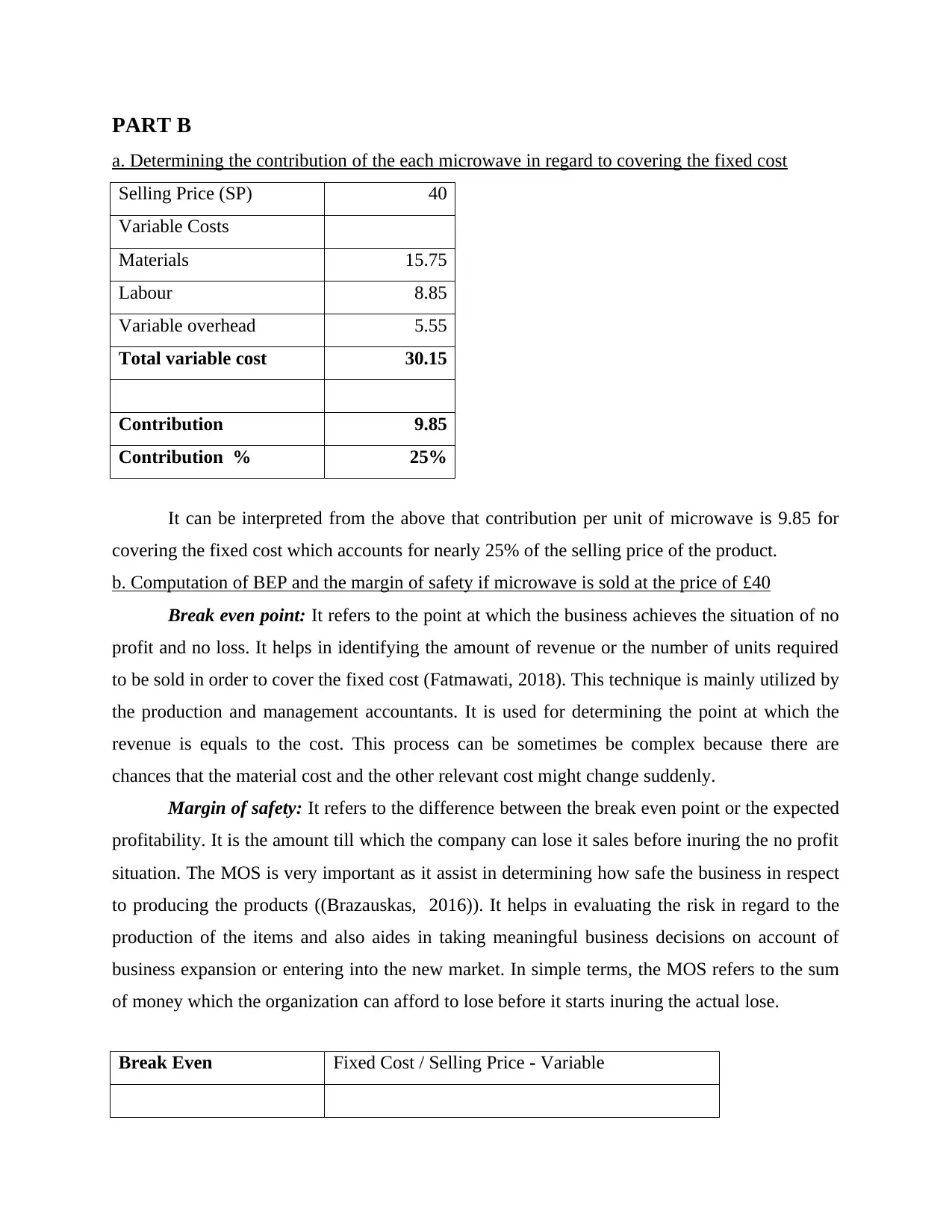

a. Determining the contribution of the each microwave in regard to covering the fixed cost

Selling Price (SP) 40

Variable Costs

Materials 15.75

Labour 8.85

Variable overhead 5.55

Total variable cost 30.15

Contribution 9.85

Contribution % 25%

It can be interpreted from the above that contribution per unit of microwave is 9.85 for

covering the fixed cost which accounts for nearly 25% of the selling price of the product.

b. Computation of BEP and the margin of safety if microwave is sold at the price of £40

Break even point: It refers to the point at which the business achieves the situation of no

profit and no loss. It helps in identifying the amount of revenue or the number of units required

to be sold in order to cover the fixed cost (Fatmawati, 2018). This technique is mainly utilized by

the production and management accountants. It is used for determining the point at which the

revenue is equals to the cost. This process can be sometimes be complex because there are

chances that the material cost and the other relevant cost might change suddenly.

Margin of safety: It refers to the difference between the break even point or the expected

profitability. It is the amount till which the company can lose it sales before inuring the no profit

situation. The MOS is very important as it assist in determining how safe the business in respect

to producing the products ((Brazauskas, 2016)). It helps in evaluating the risk in regard to the

production of the items and also aides in taking meaningful business decisions on account of

business expansion or entering into the new market. In simple terms, the MOS refers to the sum

of money which the organization can afford to lose before it starts inuring the actual lose.

Break Even Fixed Cost / Selling Price - Variable

a. Determining the contribution of the each microwave in regard to covering the fixed cost

Selling Price (SP) 40

Variable Costs

Materials 15.75

Labour 8.85

Variable overhead 5.55

Total variable cost 30.15

Contribution 9.85

Contribution % 25%

It can be interpreted from the above that contribution per unit of microwave is 9.85 for

covering the fixed cost which accounts for nearly 25% of the selling price of the product.

b. Computation of BEP and the margin of safety if microwave is sold at the price of £40

Break even point: It refers to the point at which the business achieves the situation of no

profit and no loss. It helps in identifying the amount of revenue or the number of units required

to be sold in order to cover the fixed cost (Fatmawati, 2018). This technique is mainly utilized by

the production and management accountants. It is used for determining the point at which the

revenue is equals to the cost. This process can be sometimes be complex because there are

chances that the material cost and the other relevant cost might change suddenly.

Margin of safety: It refers to the difference between the break even point or the expected

profitability. It is the amount till which the company can lose it sales before inuring the no profit

situation. The MOS is very important as it assist in determining how safe the business in respect

to producing the products ((Brazauskas, 2016)). It helps in evaluating the risk in regard to the

production of the items and also aides in taking meaningful business decisions on account of

business expansion or entering into the new market. In simple terms, the MOS refers to the sum

of money which the organization can afford to lose before it starts inuring the actual lose.

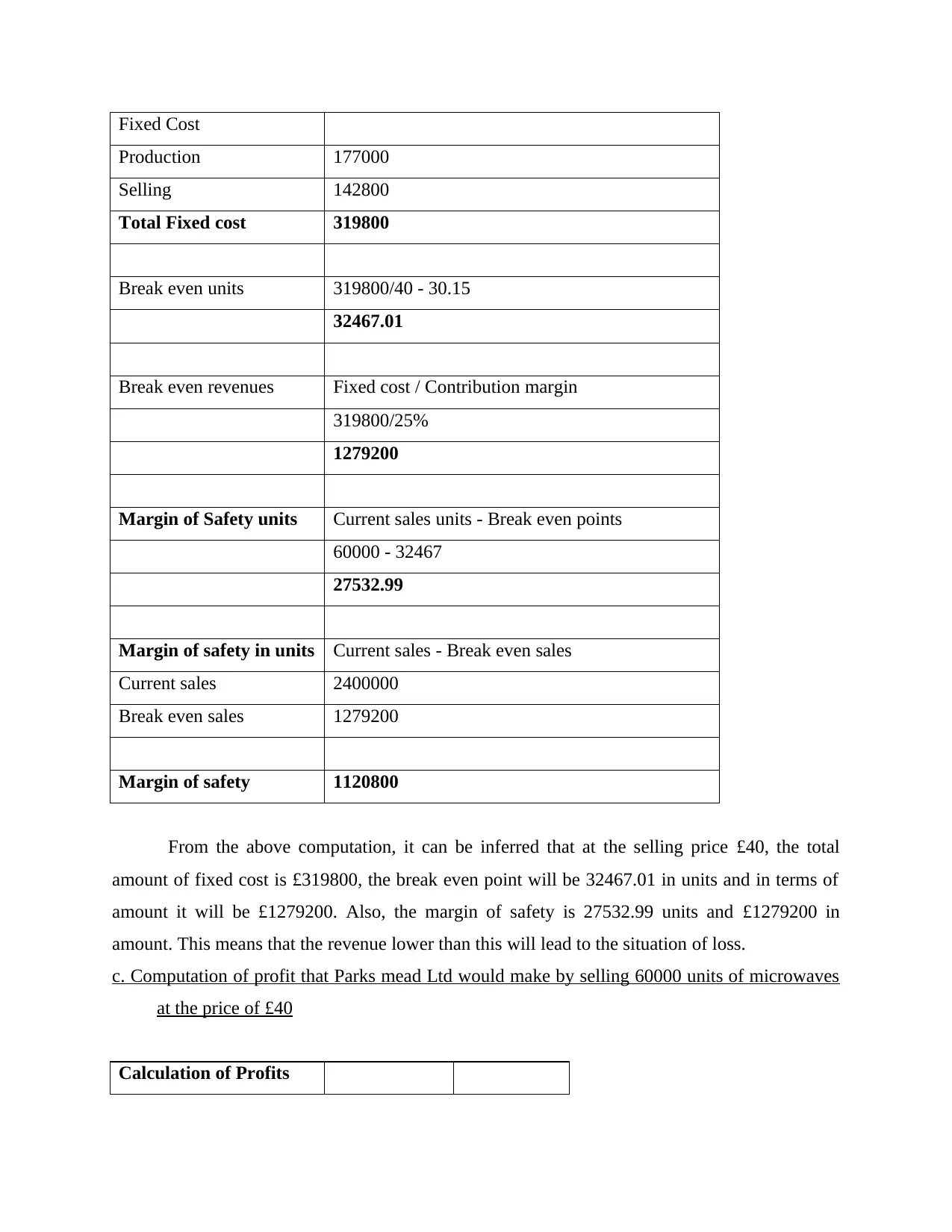

Break Even Fixed Cost / Selling Price - Variable

Fixed Cost

Production 177000

Selling 142800

Total Fixed cost 319800

Break even units 319800/40 - 30.15

32467.01

Break even revenues Fixed cost / Contribution margin

319800/25%

1279200

Margin of Safety units Current sales units - Break even points

60000 - 32467

27532.99

Margin of safety in units Current sales - Break even sales

Current sales 2400000

Break even sales 1279200

Margin of safety 1120800

From the above computation, it can be inferred that at the selling price £40, the total

amount of fixed cost is £319800, the break even point will be 32467.01 in units and in terms of

amount it will be £1279200. Also, the margin of safety is 27532.99 units and £1279200 in

amount. This means that the revenue lower than this will lead to the situation of loss.

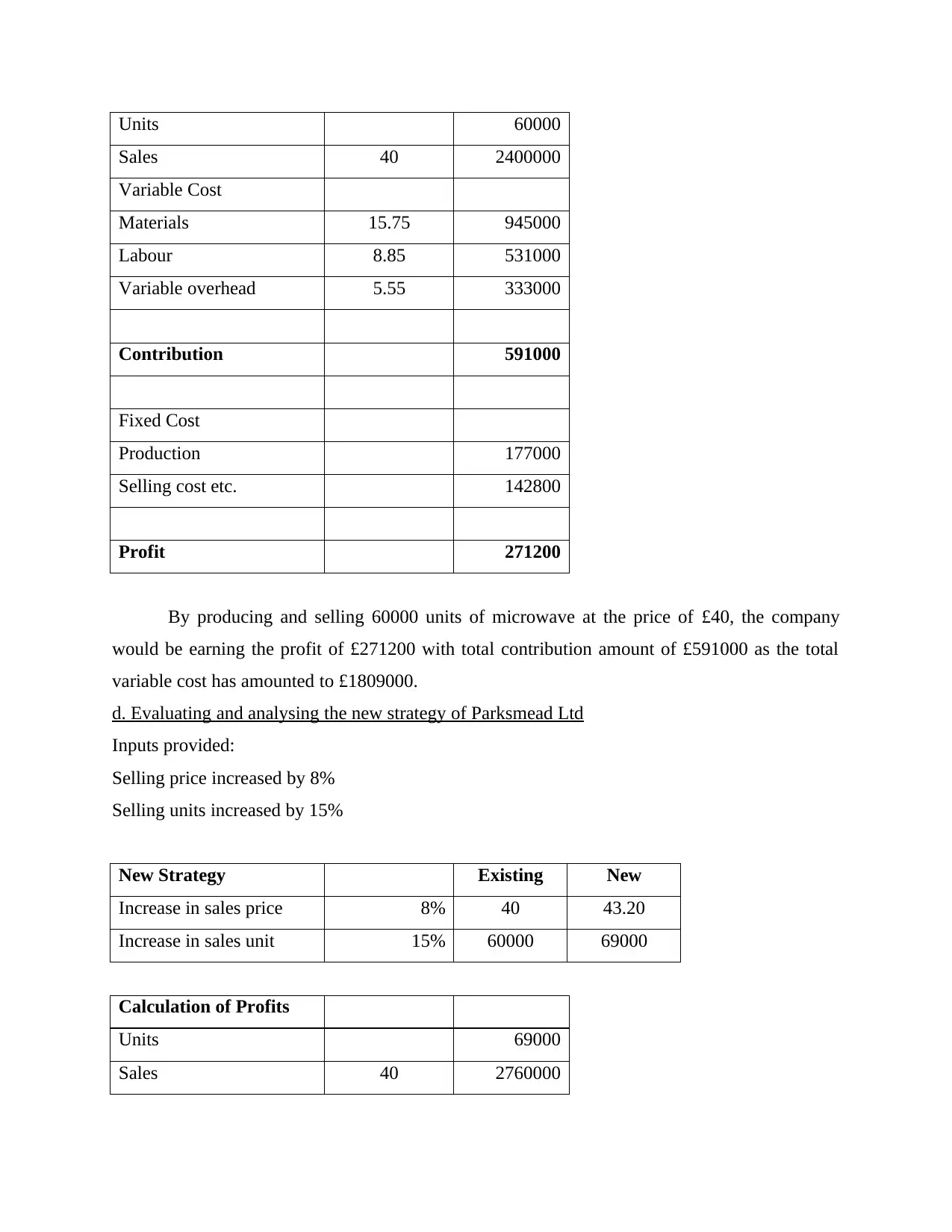

c. Computation of profit that Parks mead Ltd would make by selling 60000 units of microwaves

at the price of £40

Calculation of Profits

Production 177000

Selling 142800

Total Fixed cost 319800

Break even units 319800/40 - 30.15

32467.01

Break even revenues Fixed cost / Contribution margin

319800/25%

1279200

Margin of Safety units Current sales units - Break even points

60000 - 32467

27532.99

Margin of safety in units Current sales - Break even sales

Current sales 2400000

Break even sales 1279200

Margin of safety 1120800

From the above computation, it can be inferred that at the selling price £40, the total

amount of fixed cost is £319800, the break even point will be 32467.01 in units and in terms of

amount it will be £1279200. Also, the margin of safety is 27532.99 units and £1279200 in

amount. This means that the revenue lower than this will lead to the situation of loss.

c. Computation of profit that Parks mead Ltd would make by selling 60000 units of microwaves

at the price of £40

Calculation of Profits

Units 60000

Sales 40 2400000

Variable Cost

Materials 15.75 945000

Labour 8.85 531000

Variable overhead 5.55 333000

Contribution 591000

Fixed Cost

Production 177000

Selling cost etc. 142800

Profit 271200

By producing and selling 60000 units of microwave at the price of £40, the company

would be earning the profit of £271200 with total contribution amount of £591000 as the total

variable cost has amounted to £1809000.

d. Evaluating and analysing the new strategy of Parksmead Ltd

Inputs provided:

Selling price increased by 8%

Selling units increased by 15%

New Strategy Existing New

Increase in sales price 8% 40 43.20

Increase in sales unit 15% 60000 69000

Calculation of Profits

Units 69000

Sales 40 2760000

Sales 40 2400000

Variable Cost

Materials 15.75 945000

Labour 8.85 531000

Variable overhead 5.55 333000

Contribution 591000

Fixed Cost

Production 177000

Selling cost etc. 142800

Profit 271200

By producing and selling 60000 units of microwave at the price of £40, the company

would be earning the profit of £271200 with total contribution amount of £591000 as the total

variable cost has amounted to £1809000.

d. Evaluating and analysing the new strategy of Parksmead Ltd

Inputs provided:

Selling price increased by 8%

Selling units increased by 15%

New Strategy Existing New

Increase in sales price 8% 40 43.20

Increase in sales unit 15% 60000 69000

Calculation of Profits

Units 69000

Sales 40 2760000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

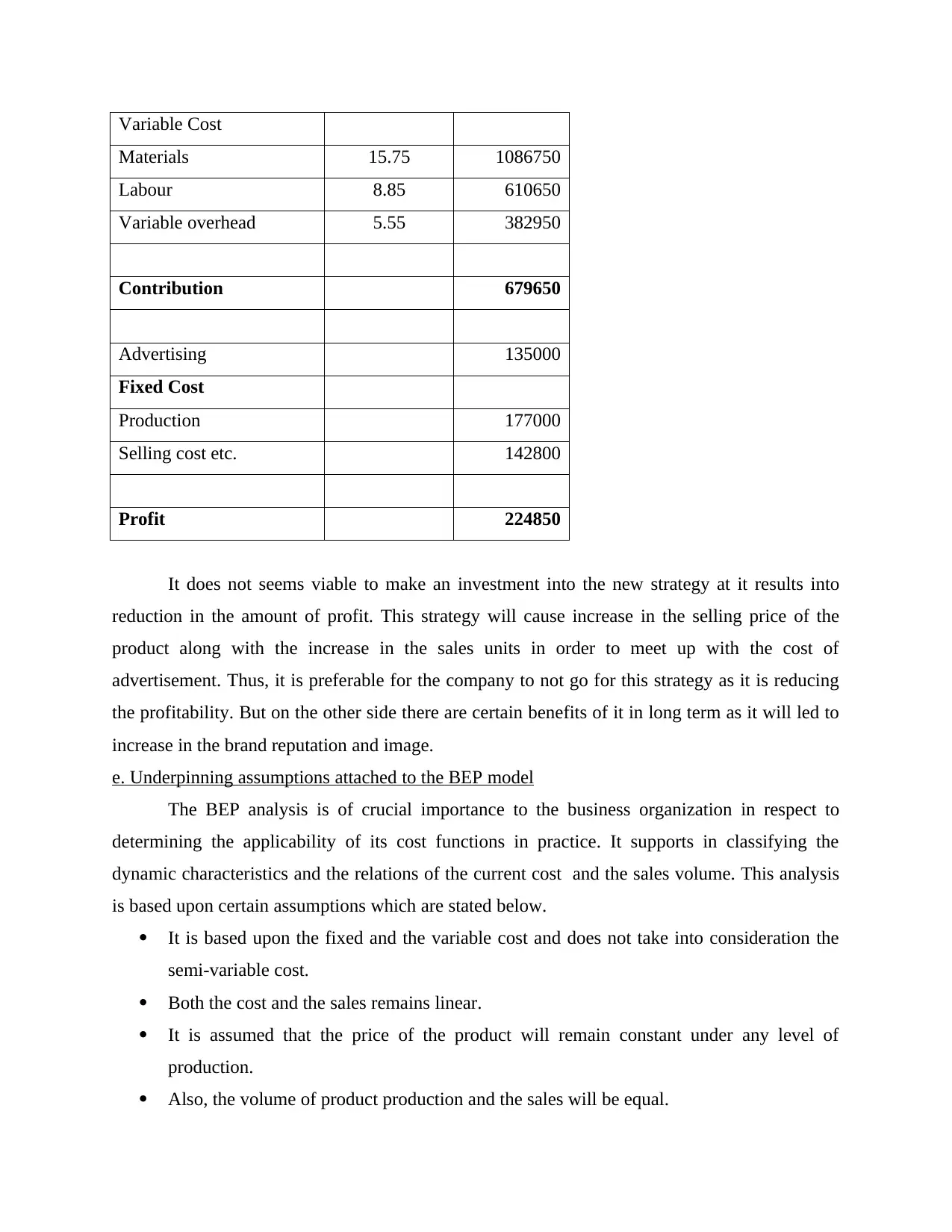

Variable Cost

Materials 15.75 1086750

Labour 8.85 610650

Variable overhead 5.55 382950

Contribution 679650

Advertising 135000

Fixed Cost

Production 177000

Selling cost etc. 142800

Profit 224850

It does not seems viable to make an investment into the new strategy at it results into

reduction in the amount of profit. This strategy will cause increase in the selling price of the

product along with the increase in the sales units in order to meet up with the cost of

advertisement. Thus, it is preferable for the company to not go for this strategy as it is reducing

the profitability. But on the other side there are certain benefits of it in long term as it will led to

increase in the brand reputation and image.

e. Underpinning assumptions attached to the BEP model

The BEP analysis is of crucial importance to the business organization in respect to

determining the applicability of its cost functions in practice. It supports in classifying the

dynamic characteristics and the relations of the current cost and the sales volume. This analysis

is based upon certain assumptions which are stated below.

It is based upon the fixed and the variable cost and does not take into consideration the

semi-variable cost.

Both the cost and the sales remains linear.

It is assumed that the price of the product will remain constant under any level of

production.

Also, the volume of product production and the sales will be equal.

Materials 15.75 1086750

Labour 8.85 610650

Variable overhead 5.55 382950

Contribution 679650

Advertising 135000

Fixed Cost

Production 177000

Selling cost etc. 142800

Profit 224850

It does not seems viable to make an investment into the new strategy at it results into

reduction in the amount of profit. This strategy will cause increase in the selling price of the

product along with the increase in the sales units in order to meet up with the cost of

advertisement. Thus, it is preferable for the company to not go for this strategy as it is reducing

the profitability. But on the other side there are certain benefits of it in long term as it will led to

increase in the brand reputation and image.

e. Underpinning assumptions attached to the BEP model

The BEP analysis is of crucial importance to the business organization in respect to

determining the applicability of its cost functions in practice. It supports in classifying the

dynamic characteristics and the relations of the current cost and the sales volume. This analysis

is based upon certain assumptions which are stated below.

It is based upon the fixed and the variable cost and does not take into consideration the

semi-variable cost.

Both the cost and the sales remains linear.

It is assumed that the price of the product will remain constant under any level of

production.

Also, the volume of product production and the sales will be equal.

The fixed cost will remain constant under the certain level of production.

It is also assumed that the technological change and any enhancement in the efficiency of

the labour will be constant.

The price of the item is assumed to remain constant.

Under the situation of the multiple product, the product mix is taken as constant.

The break even point analysis can be utilized by the range of businesses. It will assist the

business organization irrespective of nature, occupation, field or size in determining the point

where it will achieve the situation of no profit no loss. It also supports the businesses in

determining the selling price of the product in order to attain maximum profitability (Messer,

2020). It can only be used if the organization is having cost bifurcated into fixed and variable as

these are very important in for deriving the contribution and then the break even point as well.

Therefore, this is useful in every types of business organization which helps in taking valuable

business decisions in order to accomplish the targets more effectively.

Part C

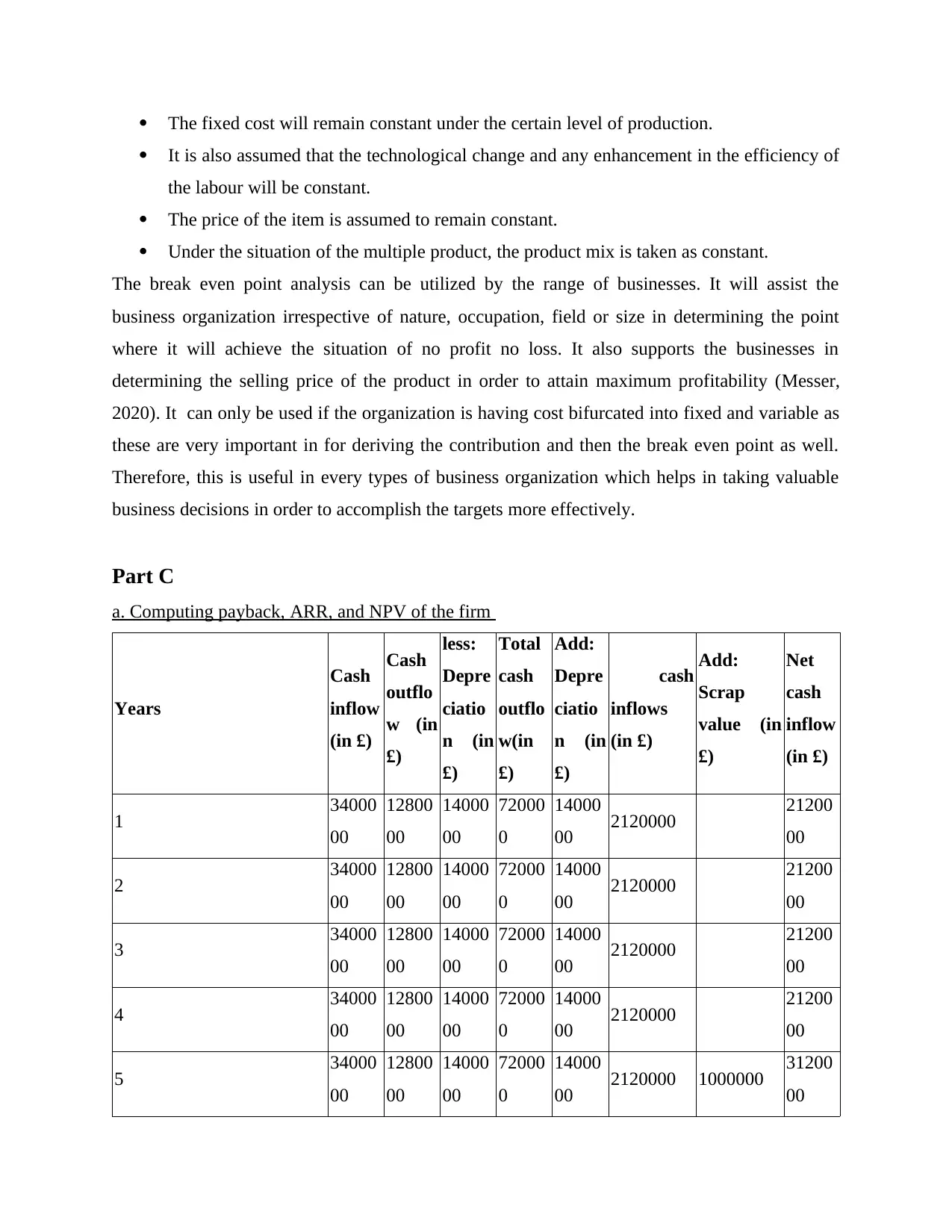

a. Computing payback, ARR, and NPV of the firm

Years

Cash

inflow

(in £)

Cash

outflo

w (in

£)

less:

Depre

ciatio

n (in

£)

Total

cash

outflo

w(in

£)

Add:

Depre

ciatio

n (in

£)

cash

inflows

(in £)

Add:

Scrap

value (in

£)

Net

cash

inflow

(in £)

1 34000

00

12800

00

14000

00

72000

0

14000

00 2120000 21200

00

2 34000

00

12800

00

14000

00

72000

0

14000

00 2120000 21200

00

3 34000

00

12800

00

14000

00

72000

0

14000

00 2120000 21200

00

4 34000

00

12800

00

14000

00

72000

0

14000

00 2120000 21200

00

5 34000

00

12800

00

14000

00

72000

0

14000

00 2120000 1000000 31200

00

It is also assumed that the technological change and any enhancement in the efficiency of

the labour will be constant.

The price of the item is assumed to remain constant.

Under the situation of the multiple product, the product mix is taken as constant.

The break even point analysis can be utilized by the range of businesses. It will assist the

business organization irrespective of nature, occupation, field or size in determining the point

where it will achieve the situation of no profit no loss. It also supports the businesses in

determining the selling price of the product in order to attain maximum profitability (Messer,

2020). It can only be used if the organization is having cost bifurcated into fixed and variable as

these are very important in for deriving the contribution and then the break even point as well.

Therefore, this is useful in every types of business organization which helps in taking valuable

business decisions in order to accomplish the targets more effectively.

Part C

a. Computing payback, ARR, and NPV of the firm

Years

Cash

inflow

(in £)

Cash

outflo

w (in

£)

less:

Depre

ciatio

n (in

£)

Total

cash

outflo

w(in

£)

Add:

Depre

ciatio

n (in

£)

cash

inflows

(in £)

Add:

Scrap

value (in

£)

Net

cash

inflow

(in £)

1 34000

00

12800

00

14000

00

72000

0

14000

00 2120000 21200

00

2 34000

00

12800

00

14000

00

72000

0

14000

00 2120000 21200

00

3 34000

00

12800

00

14000

00

72000

0

14000

00 2120000 21200

00

4 34000

00

12800

00

14000

00

72000

0

14000

00 2120000 21200

00

5 34000

00

12800

00

14000

00

72000

0

14000

00 2120000 1000000 31200

00

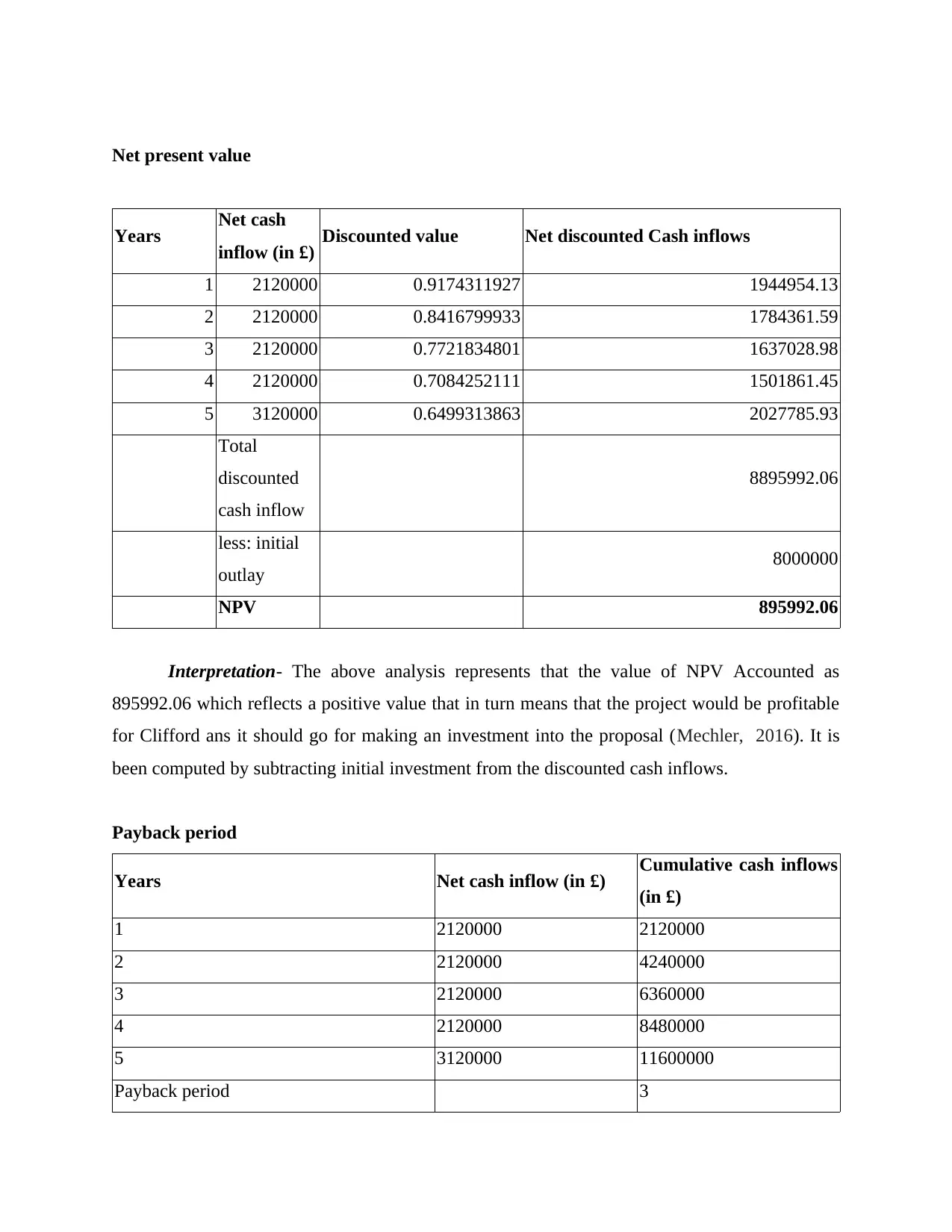

Net present value

Years Net cash

inflow (in £) Discounted value Net discounted Cash inflows

1 2120000 0.9174311927 1944954.13

2 2120000 0.8416799933 1784361.59

3 2120000 0.7721834801 1637028.98

4 2120000 0.7084252111 1501861.45

5 3120000 0.6499313863 2027785.93

Total

discounted

cash inflow

8895992.06

less: initial

outlay 8000000

NPV 895992.06

Interpretation- The above analysis represents that the value of NPV Accounted as

895992.06 which reflects a positive value that in turn means that the project would be profitable

for Clifford ans it should go for making an investment into the proposal (Mechler, 2016). It is

been computed by subtracting initial investment from the discounted cash inflows.

Payback period

Years Net cash inflow (in £) Cumulative cash inflows

(in £)

1 2120000 2120000

2 2120000 4240000

3 2120000 6360000

4 2120000 8480000

5 3120000 11600000

Payback period 3

Years Net cash

inflow (in £) Discounted value Net discounted Cash inflows

1 2120000 0.9174311927 1944954.13

2 2120000 0.8416799933 1784361.59

3 2120000 0.7721834801 1637028.98

4 2120000 0.7084252111 1501861.45

5 3120000 0.6499313863 2027785.93

Total

discounted

cash inflow

8895992.06

less: initial

outlay 8000000

NPV 895992.06

Interpretation- The above analysis represents that the value of NPV Accounted as

895992.06 which reflects a positive value that in turn means that the project would be profitable

for Clifford ans it should go for making an investment into the proposal (Mechler, 2016). It is

been computed by subtracting initial investment from the discounted cash inflows.

Payback period

Years Net cash inflow (in £) Cumulative cash inflows

(in £)

1 2120000 2120000

2 2120000 4240000

3 2120000 6360000

4 2120000 8480000

5 3120000 11600000

Payback period 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.8

Payback period 3.8 years

Interpretation- From above results it has been analysed that the period in which the firm

would recover its initial cost is 3.8 years. It seems as the shorter period in which the company

can cover its initial cost so this project tends to be viable for an entity and it must make

investment into this project.

Average rate of return

Years Earnings after taxes

1 2120000

2 2120000

3 2120000

4 2120000

5 3120000

Average earnings 2320000

Average investment 4050000

ARR 57.28%

Interpretation- From above calculation it has been analysed that the value of ARR

attained as 57.28%. This value shows the rate of the return that the firm will be earning through

this project which deemed as the good return rate. Therefore, it is been recommended that an

entity should make an investment in this proposal as it would be generating maximum profits for

the firm.

b. Explaining benefits and limitation of different capital budgeting tools

Net present value- It considers profits through assessing the cash flows over a useful life

of a proposal (Adebimpe and Bashir, 2018). It makes use of the capital cost in discounting value

of the cash flows in an accurate and appropriate manner.

Advantages Disadvantages

It is counted as the easiest method for applying

into the real life business proposals in case the

At the time of analysing viability of the longer

lived proposal, an estimation of the cash flows

Payback period 3.8 years

Interpretation- From above results it has been analysed that the period in which the firm

would recover its initial cost is 3.8 years. It seems as the shorter period in which the company

can cover its initial cost so this project tends to be viable for an entity and it must make

investment into this project.

Average rate of return

Years Earnings after taxes

1 2120000

2 2120000

3 2120000

4 2120000

5 3120000

Average earnings 2320000

Average investment 4050000

ARR 57.28%

Interpretation- From above calculation it has been analysed that the value of ARR

attained as 57.28%. This value shows the rate of the return that the firm will be earning through

this project which deemed as the good return rate. Therefore, it is been recommended that an

entity should make an investment in this proposal as it would be generating maximum profits for

the firm.

b. Explaining benefits and limitation of different capital budgeting tools

Net present value- It considers profits through assessing the cash flows over a useful life

of a proposal (Adebimpe and Bashir, 2018). It makes use of the capital cost in discounting value

of the cash flows in an accurate and appropriate manner.

Advantages Disadvantages

It is counted as the easiest method for applying

into the real life business proposals in case the

At the time of analysing viability of the longer

lived proposal, an estimation of the cash flows

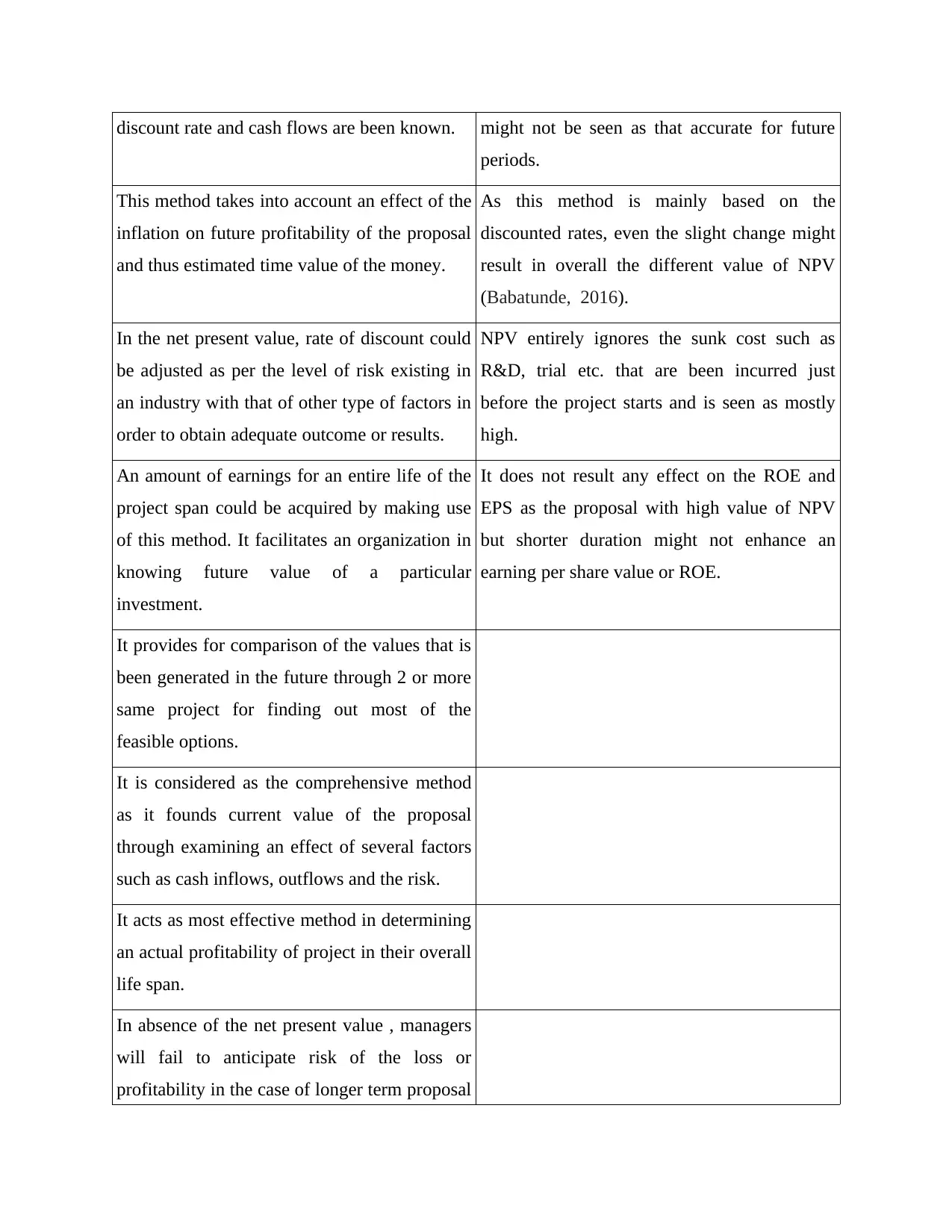

discount rate and cash flows are been known. might not be seen as that accurate for future

periods.

This method takes into account an effect of the

inflation on future profitability of the proposal

and thus estimated time value of the money.

As this method is mainly based on the

discounted rates, even the slight change might

result in overall the different value of NPV

(Babatunde, 2016).

In the net present value, rate of discount could

be adjusted as per the level of risk existing in

an industry with that of other type of factors in

order to obtain adequate outcome or results.

NPV entirely ignores the sunk cost such as

R&D, trial etc. that are been incurred just

before the project starts and is seen as mostly

high.

An amount of earnings for an entire life of the

project span could be acquired by making use

of this method. It facilitates an organization in

knowing future value of a particular

investment.

It does not result any effect on the ROE and

EPS as the proposal with high value of NPV

but shorter duration might not enhance an

earning per share value or ROE.

It provides for comparison of the values that is

been generated in the future through 2 or more

same project for finding out most of the

feasible options.

It is considered as the comprehensive method

as it founds current value of the proposal

through examining an effect of several factors

such as cash inflows, outflows and the risk.

It acts as most effective method in determining

an actual profitability of project in their overall

life span.

In absence of the net present value , managers

will fail to anticipate risk of the loss or

profitability in the case of longer term proposal

periods.

This method takes into account an effect of the

inflation on future profitability of the proposal

and thus estimated time value of the money.

As this method is mainly based on the

discounted rates, even the slight change might

result in overall the different value of NPV

(Babatunde, 2016).

In the net present value, rate of discount could

be adjusted as per the level of risk existing in

an industry with that of other type of factors in

order to obtain adequate outcome or results.

NPV entirely ignores the sunk cost such as

R&D, trial etc. that are been incurred just

before the project starts and is seen as mostly

high.

An amount of earnings for an entire life of the

project span could be acquired by making use

of this method. It facilitates an organization in

knowing future value of a particular

investment.

It does not result any effect on the ROE and

EPS as the proposal with high value of NPV

but shorter duration might not enhance an

earning per share value or ROE.

It provides for comparison of the values that is

been generated in the future through 2 or more

same project for finding out most of the

feasible options.

It is considered as the comprehensive method

as it founds current value of the proposal

through examining an effect of several factors

such as cash inflows, outflows and the risk.

It acts as most effective method in determining

an actual profitability of project in their overall

life span.

In absence of the net present value , managers

will fail to anticipate risk of the loss or

profitability in the case of longer term proposal

(Hopkinson, 2016). On other side, it is

possible through determining a proposal with

zero and negative value of NPV.

This method is counted as quite logical as here

the value of cash flows are not been expected

to reinvest in financial market.

Payback period- It means as the non-discounted tool that provides an anticipation

regarding an amount of the time that the project will take for covering the investment cost which

is been expressed in terms of years.

Advantages Disadvantages

It is very simple for understanding this method

as it does not need particular knowledge and

the accounting rules for applying. Therefore,

this tool is applied as universal method of

evaluating the proposals.

This technique ignores the time value of the

money factor which is seen as major limitation.

It is very easy to choose the most suitable

project with help of this method (Smit and

Trigeorgis, 2017).

It entirely ignores the aspect of profitability

and focus only on liquidity.

This technique focuses on risk factor so it is

adequate for those companies who do not take

any risk.

This tool provides focus on cash flow before

the payback period and do not consider the

cash flow generated after payback period.

It is the tool that emphasize on the liquidity

which helps in speedy recovery of an

investment.

It emphasizes only on capital cost and ignores

the interest factor.

possible through determining a proposal with

zero and negative value of NPV.

This method is counted as quite logical as here

the value of cash flows are not been expected

to reinvest in financial market.

Payback period- It means as the non-discounted tool that provides an anticipation

regarding an amount of the time that the project will take for covering the investment cost which

is been expressed in terms of years.

Advantages Disadvantages

It is very simple for understanding this method

as it does not need particular knowledge and

the accounting rules for applying. Therefore,

this tool is applied as universal method of

evaluating the proposals.

This technique ignores the time value of the

money factor which is seen as major limitation.

It is very easy to choose the most suitable

project with help of this method (Smit and

Trigeorgis, 2017).

It entirely ignores the aspect of profitability

and focus only on liquidity.

This technique focuses on risk factor so it is

adequate for those companies who do not take

any risk.

This tool provides focus on cash flow before

the payback period and do not consider the

cash flow generated after payback period.

It is the tool that emphasize on the liquidity

which helps in speedy recovery of an

investment.

It emphasizes only on capital cost and ignores

the interest factor.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

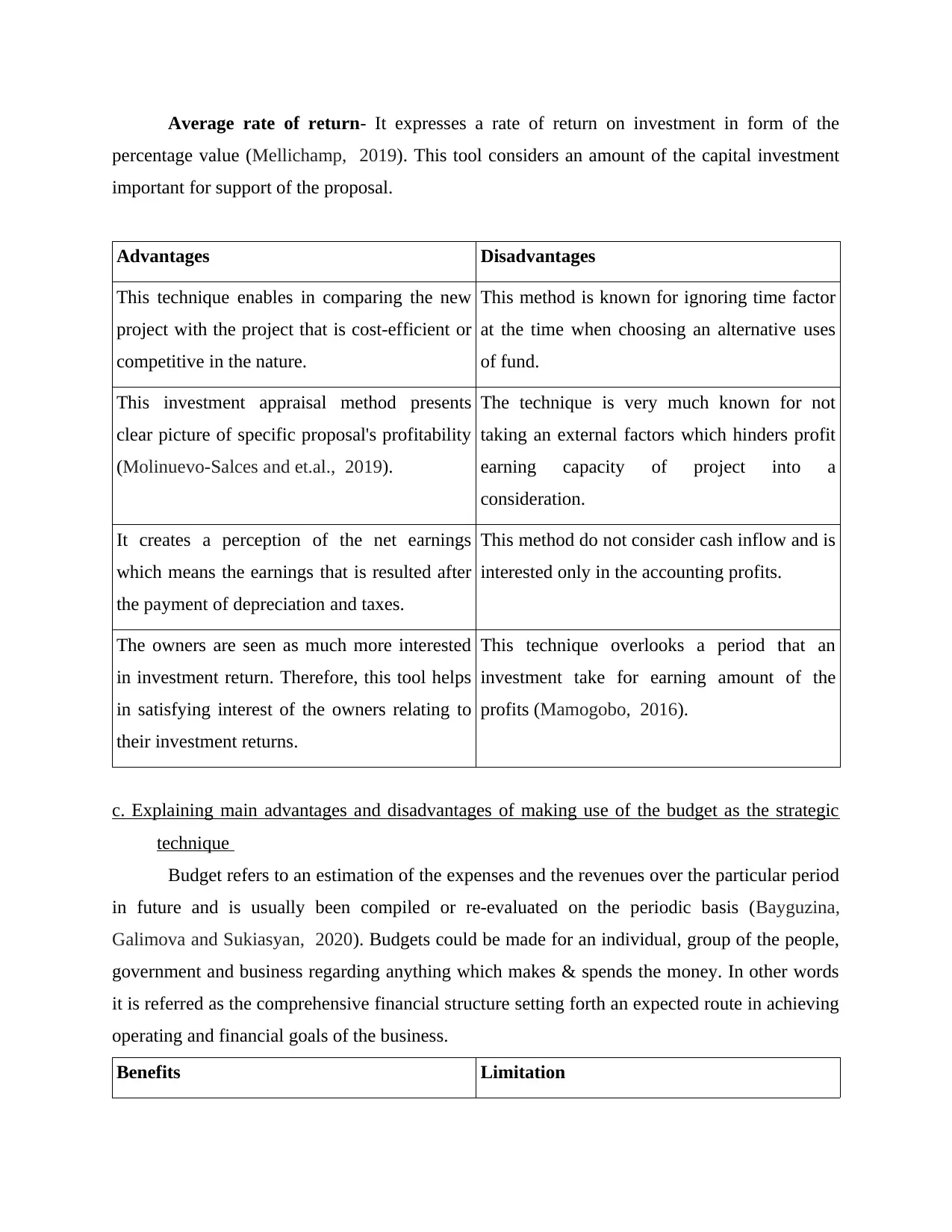

Average rate of return- It expresses a rate of return on investment in form of the

percentage value (Mellichamp, 2019). This tool considers an amount of the capital investment

important for support of the proposal.

Advantages Disadvantages

This technique enables in comparing the new

project with the project that is cost-efficient or

competitive in the nature.

This method is known for ignoring time factor

at the time when choosing an alternative uses

of fund.

This investment appraisal method presents

clear picture of specific proposal's profitability

(Molinuevo-Salces and et.al., 2019).

The technique is very much known for not

taking an external factors which hinders profit

earning capacity of project into a

consideration.

It creates a perception of the net earnings

which means the earnings that is resulted after

the payment of depreciation and taxes.

This method do not consider cash inflow and is

interested only in the accounting profits.

The owners are seen as much more interested

in investment return. Therefore, this tool helps

in satisfying interest of the owners relating to

their investment returns.

This technique overlooks a period that an

investment take for earning amount of the

profits (Mamogobo, 2016).

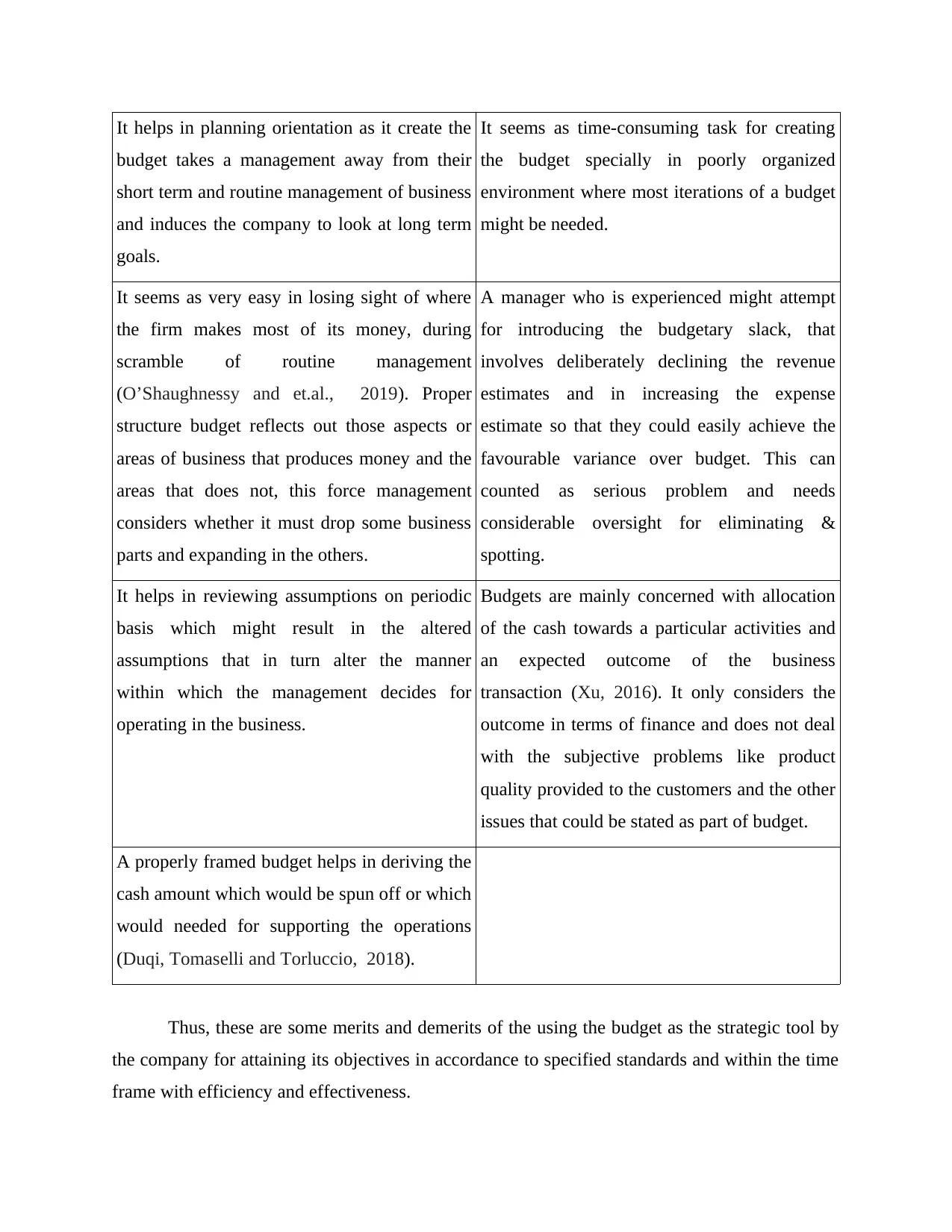

c. Explaining main advantages and disadvantages of making use of the budget as the strategic

technique

Budget refers to an estimation of the expenses and the revenues over the particular period

in future and is usually been compiled or re-evaluated on the periodic basis (Bayguzina,

Galimova and Sukiasyan, 2020). Budgets could be made for an individual, group of the people,

government and business regarding anything which makes & spends the money. In other words

it is referred as the comprehensive financial structure setting forth an expected route in achieving

operating and financial goals of the business.

Benefits Limitation

percentage value (Mellichamp, 2019). This tool considers an amount of the capital investment

important for support of the proposal.

Advantages Disadvantages

This technique enables in comparing the new

project with the project that is cost-efficient or

competitive in the nature.

This method is known for ignoring time factor

at the time when choosing an alternative uses

of fund.

This investment appraisal method presents

clear picture of specific proposal's profitability

(Molinuevo-Salces and et.al., 2019).

The technique is very much known for not

taking an external factors which hinders profit

earning capacity of project into a

consideration.

It creates a perception of the net earnings

which means the earnings that is resulted after

the payment of depreciation and taxes.

This method do not consider cash inflow and is

interested only in the accounting profits.

The owners are seen as much more interested

in investment return. Therefore, this tool helps

in satisfying interest of the owners relating to

their investment returns.

This technique overlooks a period that an

investment take for earning amount of the

profits (Mamogobo, 2016).

c. Explaining main advantages and disadvantages of making use of the budget as the strategic

technique

Budget refers to an estimation of the expenses and the revenues over the particular period

in future and is usually been compiled or re-evaluated on the periodic basis (Bayguzina,

Galimova and Sukiasyan, 2020). Budgets could be made for an individual, group of the people,

government and business regarding anything which makes & spends the money. In other words

it is referred as the comprehensive financial structure setting forth an expected route in achieving

operating and financial goals of the business.

Benefits Limitation

It helps in planning orientation as it create the

budget takes a management away from their

short term and routine management of business

and induces the company to look at long term

goals.

It seems as time-consuming task for creating

the budget specially in poorly organized

environment where most iterations of a budget

might be needed.

It seems as very easy in losing sight of where

the firm makes most of its money, during

scramble of routine management

(O’Shaughnessy and et.al., 2019). Proper

structure budget reflects out those aspects or

areas of business that produces money and the

areas that does not, this force management

considers whether it must drop some business

parts and expanding in the others.

A manager who is experienced might attempt

for introducing the budgetary slack, that

involves deliberately declining the revenue

estimates and in increasing the expense

estimate so that they could easily achieve the

favourable variance over budget. This can

counted as serious problem and needs

considerable oversight for eliminating &

spotting.

It helps in reviewing assumptions on periodic

basis which might result in the altered

assumptions that in turn alter the manner

within which the management decides for

operating in the business.

Budgets are mainly concerned with allocation

of the cash towards a particular activities and

an expected outcome of the business

transaction (Xu, 2016). It only considers the

outcome in terms of finance and does not deal

with the subjective problems like product

quality provided to the customers and the other

issues that could be stated as part of budget.

A properly framed budget helps in deriving the

cash amount which would be spun off or which

would needed for supporting the operations

(Duqi, Tomaselli and Torluccio, 2018).

Thus, these are some merits and demerits of the using the budget as the strategic tool by

the company for attaining its objectives in accordance to specified standards and within the time

frame with efficiency and effectiveness.

budget takes a management away from their

short term and routine management of business

and induces the company to look at long term

goals.

It seems as time-consuming task for creating

the budget specially in poorly organized

environment where most iterations of a budget

might be needed.

It seems as very easy in losing sight of where

the firm makes most of its money, during

scramble of routine management

(O’Shaughnessy and et.al., 2019). Proper

structure budget reflects out those aspects or

areas of business that produces money and the

areas that does not, this force management

considers whether it must drop some business

parts and expanding in the others.

A manager who is experienced might attempt

for introducing the budgetary slack, that

involves deliberately declining the revenue

estimates and in increasing the expense

estimate so that they could easily achieve the

favourable variance over budget. This can

counted as serious problem and needs

considerable oversight for eliminating &

spotting.

It helps in reviewing assumptions on periodic

basis which might result in the altered

assumptions that in turn alter the manner

within which the management decides for

operating in the business.

Budgets are mainly concerned with allocation

of the cash towards a particular activities and

an expected outcome of the business

transaction (Xu, 2016). It only considers the

outcome in terms of finance and does not deal

with the subjective problems like product

quality provided to the customers and the other

issues that could be stated as part of budget.

A properly framed budget helps in deriving the

cash amount which would be spun off or which

would needed for supporting the operations

(Duqi, Tomaselli and Torluccio, 2018).

Thus, these are some merits and demerits of the using the budget as the strategic tool by

the company for attaining its objectives in accordance to specified standards and within the time

frame with efficiency and effectiveness.

REFERENCES

Books and journal

Adebimpe, O. A. and Bashir, O., 2018. Modern Approach to Property Development

Appraisal. Covenant Journal of Research in the Built Environment.

Babatunde, S. P., 2016. Linear Programming and Investment Appraisal: A Review of

Literature. American Journal of Management Science and Engineering. 1(2). pp.61-66.

Bayguzina, L. Z., Galimova, G. A. and Sukiasyan, A. A., 2020, March. Tools for Estimating the

Risk Effect on the Investment Project Efficiency. In International Scientific Conference"

Far East Con"(ISCFEC 2020) (pp. 529-536). Atlantis Press.

Brazauskas, M., 2016. Alternative risk measurement methods: theoretical aspects of the margin

of safety. Socialiniai tyrimai. 39(1). pp.5-12.

Duqi, A., Tomaselli, A. and Torluccio, G., 2018. Is relationship lending still a mixed blessing?

A review of advantages and disadvantages for lenders and borrowers. Journal of Economic

Surveys. 32(5). pp.1446-1482.

Fatmawati, K. N., 2018. PROFIT PLANNING WITH BREAK EVEN POINT (BEP)

METHOD. JOSAR (Journal of Students Academic Research). 3(1). pp.52-65.

Hopkinson, M., 2016. The Case for Project Net Present Value (NPV) and NPV Risk

Models. PM World Journal.

Mamogobo, S. M., 2016. A comparison of financial evaluation methods used in

projects (Doctoral dissertation, University of Johannesburg).

Mechler, R., 2016. Reviewing estimates of the economic efficiency of disaster risk management:

opportunities and limitations of using risk-based cost–benefit analysis. Natural

Hazards. 81(3). pp.2121-2147.

Mellichamp, D. A., 2019. Profitability, risk, and investment in conceptual plant design:

Optimizing key financial parameters rigorously using NPV%. Computers & Chemical

Engineering. 128. pp.450-467.

Messer, R., 2020. Break Even Decisions. In Financial Modeling for Decision Making: Using

MS-Excel in Accounting and Finance. Emerald Publishing Limited.

Molinuevo-Salces, B. and et.al., 2019. Microalgae and wastewater treatment: advantages and

disadvantages. In Microalgae biotechnology for development of biofuel and wastewater

treatment (pp. 505-533). Springer, Singapore.

O’Shaughnessy, S. A. and et.al., 2019. Identifying advantages and disadvantages of variable

rate irrigation: An updated review. Applied Engineering in Agriculture. 35(6). pp.837-852.

Books and journal

Adebimpe, O. A. and Bashir, O., 2018. Modern Approach to Property Development

Appraisal. Covenant Journal of Research in the Built Environment.

Babatunde, S. P., 2016. Linear Programming and Investment Appraisal: A Review of

Literature. American Journal of Management Science and Engineering. 1(2). pp.61-66.

Bayguzina, L. Z., Galimova, G. A. and Sukiasyan, A. A., 2020, March. Tools for Estimating the

Risk Effect on the Investment Project Efficiency. In International Scientific Conference"

Far East Con"(ISCFEC 2020) (pp. 529-536). Atlantis Press.

Brazauskas, M., 2016. Alternative risk measurement methods: theoretical aspects of the margin

of safety. Socialiniai tyrimai. 39(1). pp.5-12.

Duqi, A., Tomaselli, A. and Torluccio, G., 2018. Is relationship lending still a mixed blessing?

A review of advantages and disadvantages for lenders and borrowers. Journal of Economic

Surveys. 32(5). pp.1446-1482.

Fatmawati, K. N., 2018. PROFIT PLANNING WITH BREAK EVEN POINT (BEP)

METHOD. JOSAR (Journal of Students Academic Research). 3(1). pp.52-65.

Hopkinson, M., 2016. The Case for Project Net Present Value (NPV) and NPV Risk

Models. PM World Journal.

Mamogobo, S. M., 2016. A comparison of financial evaluation methods used in

projects (Doctoral dissertation, University of Johannesburg).

Mechler, R., 2016. Reviewing estimates of the economic efficiency of disaster risk management:

opportunities and limitations of using risk-based cost–benefit analysis. Natural

Hazards. 81(3). pp.2121-2147.

Mellichamp, D. A., 2019. Profitability, risk, and investment in conceptual plant design:

Optimizing key financial parameters rigorously using NPV%. Computers & Chemical

Engineering. 128. pp.450-467.

Messer, R., 2020. Break Even Decisions. In Financial Modeling for Decision Making: Using

MS-Excel in Accounting and Finance. Emerald Publishing Limited.

Molinuevo-Salces, B. and et.al., 2019. Microalgae and wastewater treatment: advantages and

disadvantages. In Microalgae biotechnology for development of biofuel and wastewater

treatment (pp. 505-533). Springer, Singapore.

O’Shaughnessy, S. A. and et.al., 2019. Identifying advantages and disadvantages of variable

rate irrigation: An updated review. Applied Engineering in Agriculture. 35(6). pp.837-852.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Smit, H. T. and Trigeorgis, L., 2017. Strategic NPV: Real options and strategic games under

different information structures. Strategic Management Journal. 38(13). pp.2555-2578.

Xu, Z., 2016. Premium Payback Period Model and its Application in Stock Investment (Doctoral

dissertation, Durham University).

different information structures. Strategic Management Journal. 38(13). pp.2555-2578.

Xu, Z., 2016. Premium Payback Period Model and its Application in Stock Investment (Doctoral

dissertation, Durham University).

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.