Introduction to Financial Accounting Assignment Solution

VerifiedAdded on 2023/01/07

|15

|3525

|73

Homework Assignment

AI Summary

This document presents a comprehensive solution to an Introduction to Financial Accounting assignment. The solution includes the preparation of a trading account, profit and loss account, and a statement of financial position based on a provided trial balance. It also evaluates the key features of financial information for users, explaining their importance and benefits. Additionally, the assignment covers ratio analysis, including gross profit margin, return on capital employed, current ratio, and trade payables/receivables periods, with interpretations. Furthermore, it addresses the creation of bank accounts, purchase accounts, and other relevant accounts, along with a trial balance. Finally, it delves into depreciation methods (straight-line and reducing balance), and explains significant accounting concepts.

Introduction to

Financial Accounting

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Q1a...................................................................................................................................................3

a. Prepare Trading account..........................................................................................................3

b. Prepare profit and loss account................................................................................................3

c. Draft statement of financial position........................................................................................3

Q1b. Evaluate six of main features of information for users of financial statements. Explain why

they are important and the benefits they will bring to the users......................................................4

Q2a...................................................................................................................................................7

Gross profit Margin.....................................................................................................................7

Return on capital employed.........................................................................................................8

Current ratio.................................................................................................................................8

Trade payables period in days.....................................................................................................8

Trade receivable in days..............................................................................................................9

Q2b................................................................................................................................................10

a. Bank account..........................................................................................................................10

b. All other accounts..................................................................................................................10

c. Trial balance...........................................................................................................................11

Q2c.................................................................................................................................................11

i. Straight-line method at 12.5% per annum..............................................................................11

ii. Reducing balance method at 15% per annum.......................................................................12

iii. Explain the meaning and significance of the following accounting concepts.....................12

References......................................................................................................................................15

Q1a...................................................................................................................................................3

a. Prepare Trading account..........................................................................................................3

b. Prepare profit and loss account................................................................................................3

c. Draft statement of financial position........................................................................................3

Q1b. Evaluate six of main features of information for users of financial statements. Explain why

they are important and the benefits they will bring to the users......................................................4

Q2a...................................................................................................................................................7

Gross profit Margin.....................................................................................................................7

Return on capital employed.........................................................................................................8

Current ratio.................................................................................................................................8

Trade payables period in days.....................................................................................................8

Trade receivable in days..............................................................................................................9

Q2b................................................................................................................................................10

a. Bank account..........................................................................................................................10

b. All other accounts..................................................................................................................10

c. Trial balance...........................................................................................................................11

Q2c.................................................................................................................................................11

i. Straight-line method at 12.5% per annum..............................................................................11

ii. Reducing balance method at 15% per annum.......................................................................12

iii. Explain the meaning and significance of the following accounting concepts.....................12

References......................................................................................................................................15

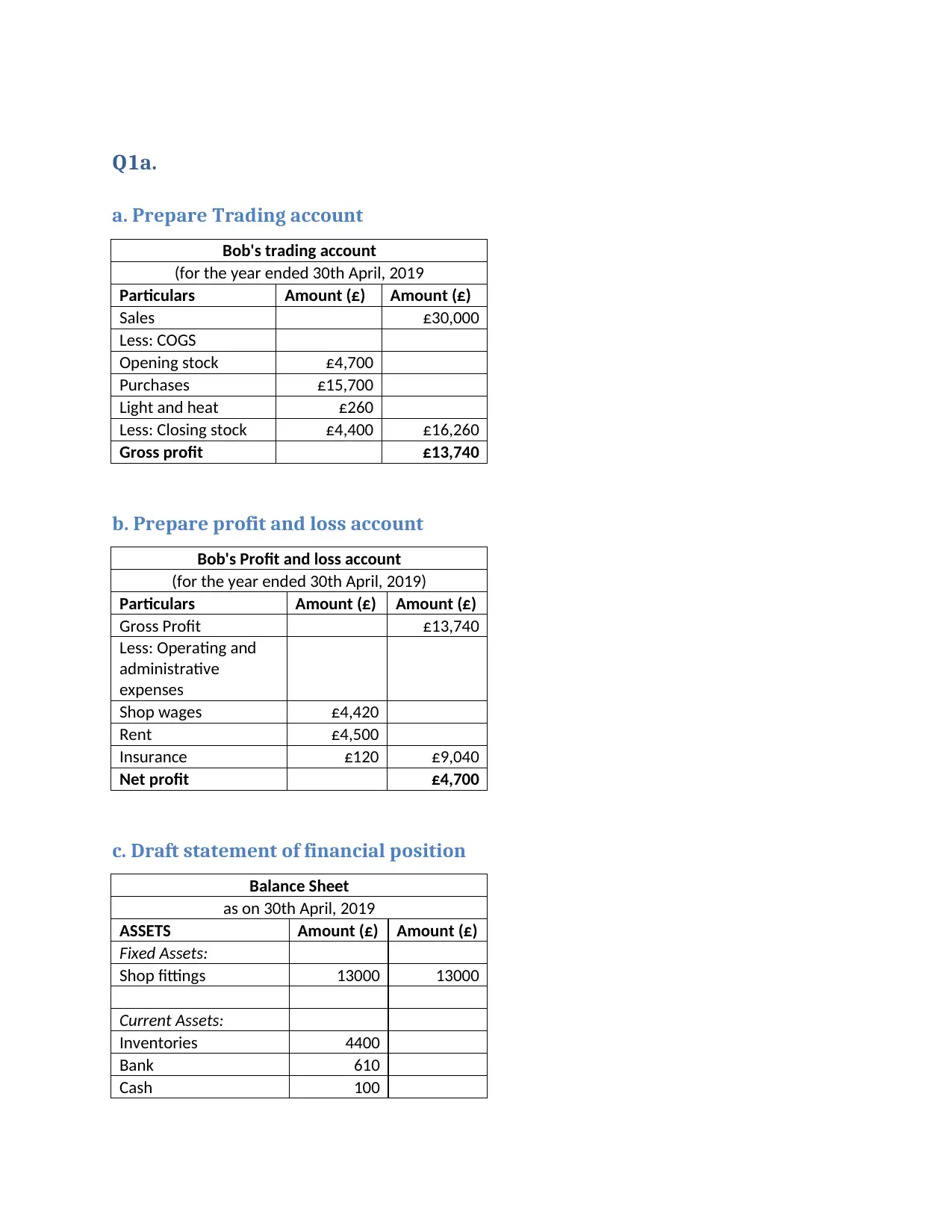

Q1a.

a. Prepare Trading account

Bob's trading account

(for the year ended 30th April, 2019

Particulars Amount (£) Amount (£)

Sales £30,000

Less: COGS

Opening stock £4,700

Purchases £15,700

Light and heat £260

Less: Closing stock £4,400 £16,260

Gross profit £13,740

b. Prepare profit and loss account

Bob's Profit and loss account

(for the year ended 30th April, 2019)

Particulars Amount (£) Amount (£)

Gross Profit £13,740

Less: Operating and

administrative

expenses

Shop wages £4,420

Rent £4,500

Insurance £120 £9,040

Net profit £4,700

c. Draft statement of financial position

Balance Sheet

as on 30th April, 2019

ASSETS Amount (£) Amount (£)

Fixed Assets:

Shop fittings 13000 13000

Current Assets:

Inventories 4400

Bank 610

Cash 100

a. Prepare Trading account

Bob's trading account

(for the year ended 30th April, 2019

Particulars Amount (£) Amount (£)

Sales £30,000

Less: COGS

Opening stock £4,700

Purchases £15,700

Light and heat £260

Less: Closing stock £4,400 £16,260

Gross profit £13,740

b. Prepare profit and loss account

Bob's Profit and loss account

(for the year ended 30th April, 2019)

Particulars Amount (£) Amount (£)

Gross Profit £13,740

Less: Operating and

administrative

expenses

Shop wages £4,420

Rent £4,500

Insurance £120 £9,040

Net profit £4,700

c. Draft statement of financial position

Balance Sheet

as on 30th April, 2019

ASSETS Amount (£) Amount (£)

Fixed Assets:

Shop fittings 13000 13000

Current Assets:

Inventories 4400

Bank 610

Cash 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

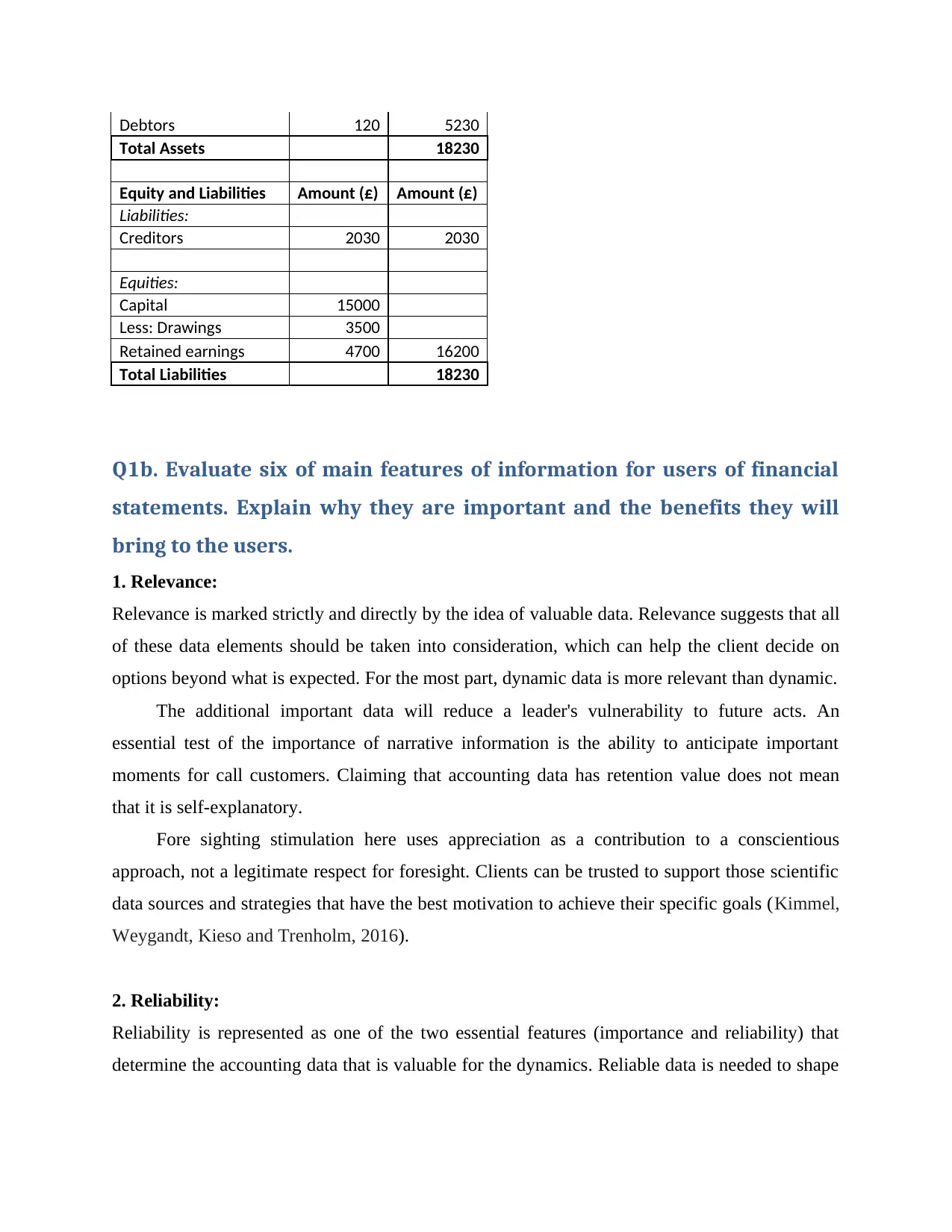

Debtors 120 5230

Total Assets 18230

Equity and Liabilities Amount (£) Amount (£)

Liabilities:

Creditors 2030 2030

Equities:

Capital 15000

Less: Drawings 3500

Retained earnings 4700 16200

Total Liabilities 18230

Q1b. Evaluate six of main features of information for users of financial

statements. Explain why they are important and the benefits they will

bring to the users.

1. Relevance:

Relevance is marked strictly and directly by the idea of valuable data. Relevance suggests that all

of these data elements should be taken into consideration, which can help the client decide on

options beyond what is expected. For the most part, dynamic data is more relevant than dynamic.

The additional important data will reduce a leader's vulnerability to future acts. An

essential test of the importance of narrative information is the ability to anticipate important

moments for call customers. Claiming that accounting data has retention value does not mean

that it is self-explanatory.

Fore sighting stimulation here uses appreciation as a contribution to a conscientious

approach, not a legitimate respect for foresight. Clients can be trusted to support those scientific

data sources and strategies that have the best motivation to achieve their specific goals (Kimmel,

Weygandt, Kieso and Trenholm, 2016).

2. Reliability:

Reliability is represented as one of the two essential features (importance and reliability) that

determine the accounting data that is valuable for the dynamics. Reliable data is needed to shape

Total Assets 18230

Equity and Liabilities Amount (£) Amount (£)

Liabilities:

Creditors 2030 2030

Equities:

Capital 15000

Less: Drawings 3500

Retained earnings 4700 16200

Total Liabilities 18230

Q1b. Evaluate six of main features of information for users of financial

statements. Explain why they are important and the benefits they will

bring to the users.

1. Relevance:

Relevance is marked strictly and directly by the idea of valuable data. Relevance suggests that all

of these data elements should be taken into consideration, which can help the client decide on

options beyond what is expected. For the most part, dynamic data is more relevant than dynamic.

The additional important data will reduce a leader's vulnerability to future acts. An

essential test of the importance of narrative information is the ability to anticipate important

moments for call customers. Claiming that accounting data has retention value does not mean

that it is self-explanatory.

Fore sighting stimulation here uses appreciation as a contribution to a conscientious

approach, not a legitimate respect for foresight. Clients can be trusted to support those scientific

data sources and strategies that have the best motivation to achieve their specific goals (Kimmel,

Weygandt, Kieso and Trenholm, 2016).

2. Reliability:

Reliability is represented as one of the two essential features (importance and reliability) that

determine the accounting data that is valuable for the dynamics. Reliable data is needed to shape

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decisions about a company’s purchasing power and financial position. Trust varies from what to

what.

Some data included in an annual report may be more robust than others. For example, plant

and equipment data may not be as robust as some conventional storage data due to conflicts in

identity vulnerabilities. Reliability is the quality that ensures that customers can rely on reliable

information as an example of what it means to talk to.

3. Understandability:

Understanding the nature of the data is what will allow consumers to see how critical they are.

The benefits of data can be extended by making it more rational and therefore useful for a larger

movement of customers. By incorporating data that is uniquely seen by today's customers and

not others, it makes predictions that go against satisfactory publication standards.

Incentive data should be introduced as well as to refrain from incorrect translation of tax

reports. In this way, money data retention data includes information that customers understand

the data and communicate in a structured and formulated way that is widely accessible to the

customer.

4. Comparability:

The money option requires you to decide between potential asset courses. In making a decision,

the director establishes a relationship between options, which is motivated by the financial data.

The same thing means that similar items are published in this way and not similar items that

were unexpectedly mentioned.

Tantamount balance sheet accounting data reveals similarities and differences arising from

the appearance and fundamental differences in the enterprise or in efforts and exchanges of them,

and not just from the difference in them. the cash-related accounting treatment (Kimmel,

Weygandt, Kieso and Trenholm, 2016).

The data, if any, will help the boss to decide on the characteristics of money, deficits and

future opportunities, between at least two companies or between periods in a lone venture.

5. Consistency:

what.

Some data included in an annual report may be more robust than others. For example, plant

and equipment data may not be as robust as some conventional storage data due to conflicts in

identity vulnerabilities. Reliability is the quality that ensures that customers can rely on reliable

information as an example of what it means to talk to.

3. Understandability:

Understanding the nature of the data is what will allow consumers to see how critical they are.

The benefits of data can be extended by making it more rational and therefore useful for a larger

movement of customers. By incorporating data that is uniquely seen by today's customers and

not others, it makes predictions that go against satisfactory publication standards.

Incentive data should be introduced as well as to refrain from incorrect translation of tax

reports. In this way, money data retention data includes information that customers understand

the data and communicate in a structured and formulated way that is widely accessible to the

customer.

4. Comparability:

The money option requires you to decide between potential asset courses. In making a decision,

the director establishes a relationship between options, which is motivated by the financial data.

The same thing means that similar items are published in this way and not similar items that

were unexpectedly mentioned.

Tantamount balance sheet accounting data reveals similarities and differences arising from

the appearance and fundamental differences in the enterprise or in efforts and exchanges of them,

and not just from the difference in them. the cash-related accounting treatment (Kimmel,

Weygandt, Kieso and Trenholm, 2016).

The data, if any, will help the boss to decide on the characteristics of money, deficits and

future opportunities, between at least two companies or between periods in a lone venture.

5. Consistency:

Consistency of strategy over time is an important quality that makes accounting numbers more

useful. Consistent use of accounting standards begins with a single accounting period and is then

updated on tax summaries for clients encouraging the study and understanding of similar

accounting information.

It is usually not appropriate for the financial expert what standards or disclosures an

organization adopts in its tax return, if they happen to understand how it is followed and will

surely be followed reliably from year to year.

The absence of texture gives it a similar appearance. The estimate between group

correlations is significantly reduced when material differences in payrolls are determined by

types in accounting forecasts.

6. Neutrality:

The nature of opportunity with bias or independence is called non-participation. The lack of bias

means that, in detailing or implementing guidelines, the essential concern should be the

importance and reliability of the resulting data, not the impact which the new status may have on

the mind on user.

Impartial decision-making between accounting options is freed from the bias toward a

preset result. The (mostly useful) money-related information destinations serve a wide range of

award-winning data clients, and none of the pre-ordered results tend to respond on all the biases

and motives of a messenger (Kimmel, Weygandt, Kieso and Trenholm, 2016).

Importance of accounting informations:

The accounting information is important in estimating the presentation of various business

activities. Although budget reports are the accounting data tool used to evaluate business

activities, business owners can examine this data more rigorously when evaluating business

activities. Cash allowances using accounting data represented tax summaries and segmented

them into driving signals.

Business owners regularly use accounting data to create financial plans for their

organizations. Authenticated money laundering data provides business owners with an in-

depth analysis of how their organizations have burned money on specific business

useful. Consistent use of accounting standards begins with a single accounting period and is then

updated on tax summaries for clients encouraging the study and understanding of similar

accounting information.

It is usually not appropriate for the financial expert what standards or disclosures an

organization adopts in its tax return, if they happen to understand how it is followed and will

surely be followed reliably from year to year.

The absence of texture gives it a similar appearance. The estimate between group

correlations is significantly reduced when material differences in payrolls are determined by

types in accounting forecasts.

6. Neutrality:

The nature of opportunity with bias or independence is called non-participation. The lack of bias

means that, in detailing or implementing guidelines, the essential concern should be the

importance and reliability of the resulting data, not the impact which the new status may have on

the mind on user.

Impartial decision-making between accounting options is freed from the bias toward a

preset result. The (mostly useful) money-related information destinations serve a wide range of

award-winning data clients, and none of the pre-ordered results tend to respond on all the biases

and motives of a messenger (Kimmel, Weygandt, Kieso and Trenholm, 2016).

Importance of accounting informations:

The accounting information is important in estimating the presentation of various business

activities. Although budget reports are the accounting data tool used to evaluate business

activities, business owners can examine this data more rigorously when evaluating business

activities. Cash allowances using accounting data represented tax summaries and segmented

them into driving signals.

Business owners regularly use accounting data to create financial plans for their

organizations. Authenticated money laundering data provides business owners with an in-

depth analysis of how their organizations have burned money on specific business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

capabilities. Business owners often take this accounting data and create future spending

plans to ensure money management for their organizations. These financial plans can also be

balanced by relying on standard accounting data to ensure that a business owner does not

limit spending on the underlying funds.

Accounting data is typically used to make business decisions. For budget management, the

definition of payroll and expense accounting provides a meaningful review for the industry.

Options may include growing a conventional asset, using various cash resources, purchasing

new hardware or offices, valuing future contracts, or testing it new business openings.

External trading partners often use accounting data to make speculative choices. Banks,

lending experts, financial speculators or private speculators often analyze group accounting

data to determine financial quality and operational productivity. This suggests that an

independent company is a speculative option (Yu, Lin and Tang, 2018).

Benefits of accounting information:

1. Increased automation - more consistent output and fewer resources (people) needs

2. Better information - this is important for strategic decision-making

3. Faster turnaround times - this is important for compliance filing as well as

management reporting. For the latter, stale data is not helpful in making strategic

decisions (Kolitz, 2016).

4. Connectivity & flexibility - this allows for increased automation, greater flexibility in

data gathering and reporting and the ability to connect financial and non-financial data

(Kolitz, 2016).

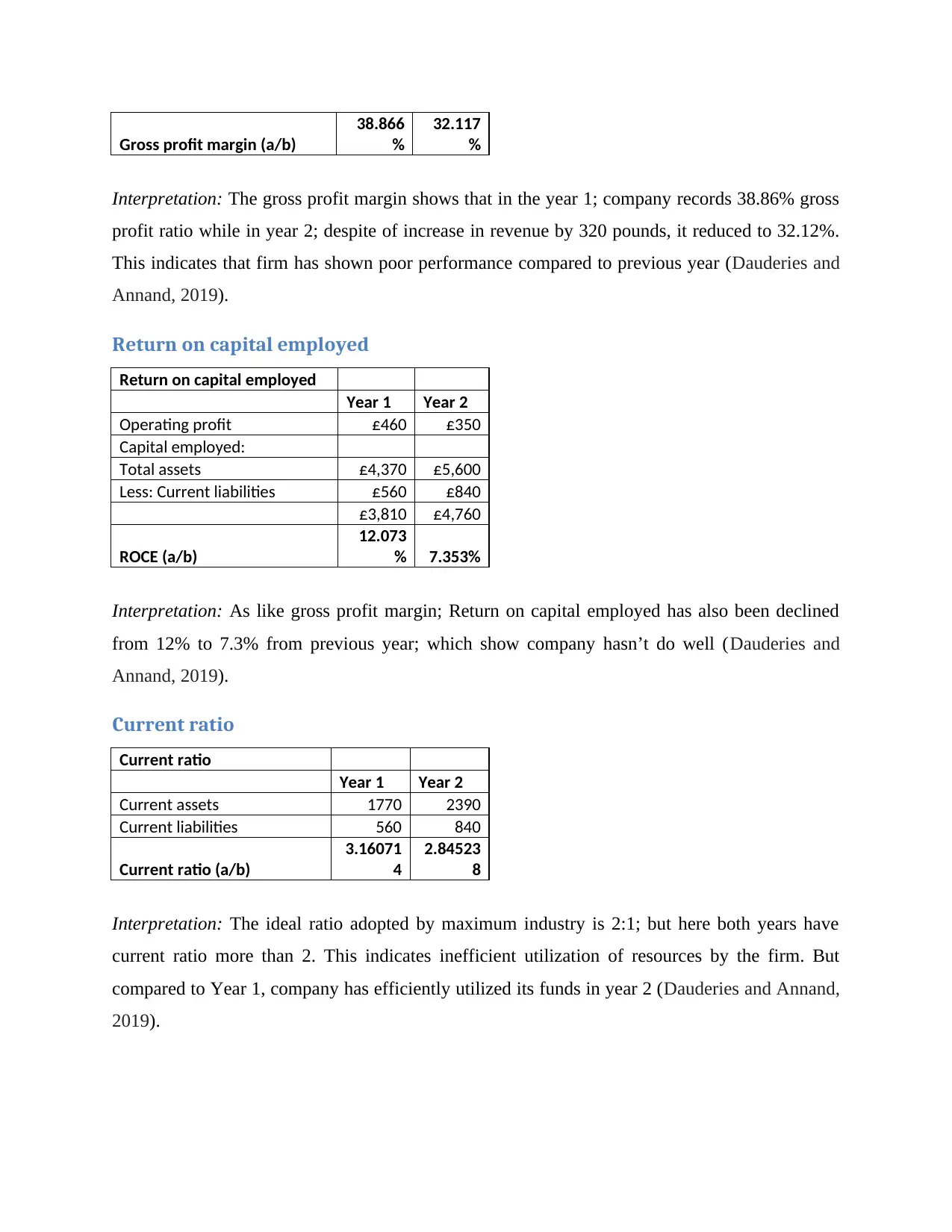

Q2a.

Gross profit Margin

Gross profit margin

Year 1 Year 2

Gross profit £1,920 £2,200

Net Sales £4,940 £6,850

plans to ensure money management for their organizations. These financial plans can also be

balanced by relying on standard accounting data to ensure that a business owner does not

limit spending on the underlying funds.

Accounting data is typically used to make business decisions. For budget management, the

definition of payroll and expense accounting provides a meaningful review for the industry.

Options may include growing a conventional asset, using various cash resources, purchasing

new hardware or offices, valuing future contracts, or testing it new business openings.

External trading partners often use accounting data to make speculative choices. Banks,

lending experts, financial speculators or private speculators often analyze group accounting

data to determine financial quality and operational productivity. This suggests that an

independent company is a speculative option (Yu, Lin and Tang, 2018).

Benefits of accounting information:

1. Increased automation - more consistent output and fewer resources (people) needs

2. Better information - this is important for strategic decision-making

3. Faster turnaround times - this is important for compliance filing as well as

management reporting. For the latter, stale data is not helpful in making strategic

decisions (Kolitz, 2016).

4. Connectivity & flexibility - this allows for increased automation, greater flexibility in

data gathering and reporting and the ability to connect financial and non-financial data

(Kolitz, 2016).

Q2a.

Gross profit Margin

Gross profit margin

Year 1 Year 2

Gross profit £1,920 £2,200

Net Sales £4,940 £6,850

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gross profit margin (a/b)

38.866

%

32.117

%

Interpretation: The gross profit margin shows that in the year 1; company records 38.86% gross

profit ratio while in year 2; despite of increase in revenue by 320 pounds, it reduced to 32.12%.

This indicates that firm has shown poor performance compared to previous year (Dauderies and

Annand, 2019).

Return on capital employed

Return on capital employed

Year 1 Year 2

Operating profit £460 £350

Capital employed:

Total assets £4,370 £5,600

Less: Current liabilities £560 £840

£3,810 £4,760

ROCE (a/b)

12.073

% 7.353%

Interpretation: As like gross profit margin; Return on capital employed has also been declined

from 12% to 7.3% from previous year; which show company hasn’t do well (Dauderies and

Annand, 2019).

Current ratio

Current ratio

Year 1 Year 2

Current assets 1770 2390

Current liabilities 560 840

Current ratio (a/b)

3.16071

4

2.84523

8

Interpretation: The ideal ratio adopted by maximum industry is 2:1; but here both years have

current ratio more than 2. This indicates inefficient utilization of resources by the firm. But

compared to Year 1, company has efficiently utilized its funds in year 2 (Dauderies and Annand,

2019).

38.866

%

32.117

%

Interpretation: The gross profit margin shows that in the year 1; company records 38.86% gross

profit ratio while in year 2; despite of increase in revenue by 320 pounds, it reduced to 32.12%.

This indicates that firm has shown poor performance compared to previous year (Dauderies and

Annand, 2019).

Return on capital employed

Return on capital employed

Year 1 Year 2

Operating profit £460 £350

Capital employed:

Total assets £4,370 £5,600

Less: Current liabilities £560 £840

£3,810 £4,760

ROCE (a/b)

12.073

% 7.353%

Interpretation: As like gross profit margin; Return on capital employed has also been declined

from 12% to 7.3% from previous year; which show company hasn’t do well (Dauderies and

Annand, 2019).

Current ratio

Current ratio

Year 1 Year 2

Current assets 1770 2390

Current liabilities 560 840

Current ratio (a/b)

3.16071

4

2.84523

8

Interpretation: The ideal ratio adopted by maximum industry is 2:1; but here both years have

current ratio more than 2. This indicates inefficient utilization of resources by the firm. But

compared to Year 1, company has efficiently utilized its funds in year 2 (Dauderies and Annand,

2019).

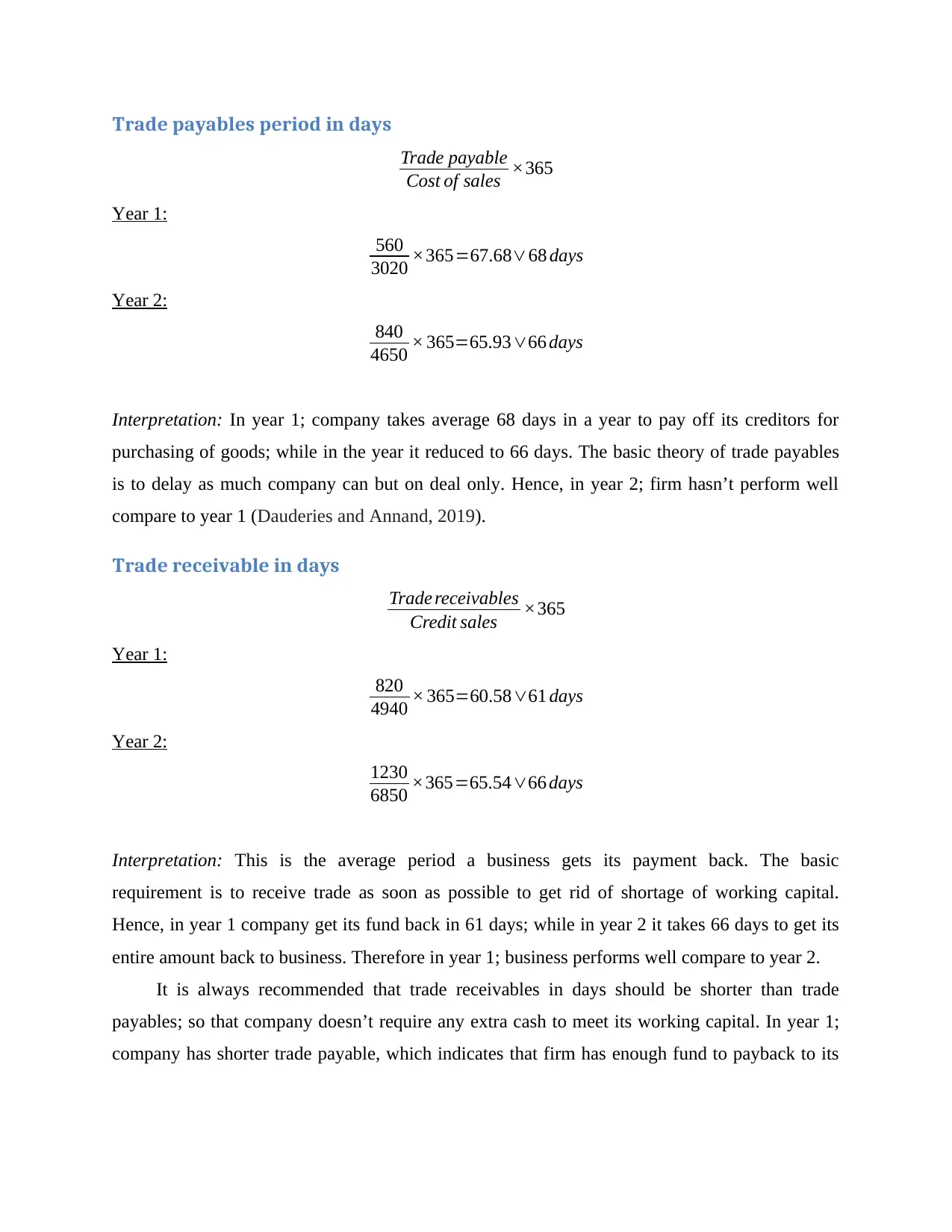

Trade payables period in days

Trade payable

Cost of sales ×365

Year 1:

560

3020 ×365=67.68∨68 days

Year 2:

840

4650 × 365=65.93∨66 days

Interpretation: In year 1; company takes average 68 days in a year to pay off its creditors for

purchasing of goods; while in the year it reduced to 66 days. The basic theory of trade payables

is to delay as much company can but on deal only. Hence, in year 2; firm hasn’t perform well

compare to year 1 (Dauderies and Annand, 2019).

Trade receivable in days

Trade receivables

Credit sales ×365

Year 1:

820

4940 × 365=60.58∨61 days

Year 2:

1230

6850 ×365=65.54∨66 days

Interpretation: This is the average period a business gets its payment back. The basic

requirement is to receive trade as soon as possible to get rid of shortage of working capital.

Hence, in year 1 company get its fund back in 61 days; while in year 2 it takes 66 days to get its

entire amount back to business. Therefore in year 1; business performs well compare to year 2.

It is always recommended that trade receivables in days should be shorter than trade

payables; so that company doesn’t require any extra cash to meet its working capital. In year 1;

company has shorter trade payable, which indicates that firm has enough fund to payback to its

Trade payable

Cost of sales ×365

Year 1:

560

3020 ×365=67.68∨68 days

Year 2:

840

4650 × 365=65.93∨66 days

Interpretation: In year 1; company takes average 68 days in a year to pay off its creditors for

purchasing of goods; while in the year it reduced to 66 days. The basic theory of trade payables

is to delay as much company can but on deal only. Hence, in year 2; firm hasn’t perform well

compare to year 1 (Dauderies and Annand, 2019).

Trade receivable in days

Trade receivables

Credit sales ×365

Year 1:

820

4940 × 365=60.58∨61 days

Year 2:

1230

6850 ×365=65.54∨66 days

Interpretation: This is the average period a business gets its payment back. The basic

requirement is to receive trade as soon as possible to get rid of shortage of working capital.

Hence, in year 1 company get its fund back in 61 days; while in year 2 it takes 66 days to get its

entire amount back to business. Therefore in year 1; business performs well compare to year 2.

It is always recommended that trade receivables in days should be shorter than trade

payables; so that company doesn’t require any extra cash to meet its working capital. In year 1;

company has shorter trade payable, which indicates that firm has enough fund to payback to its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

creditors without arranging for any extra fund from the market; while in year 2 both days are

same (Ainsworth and Deines, 2019).

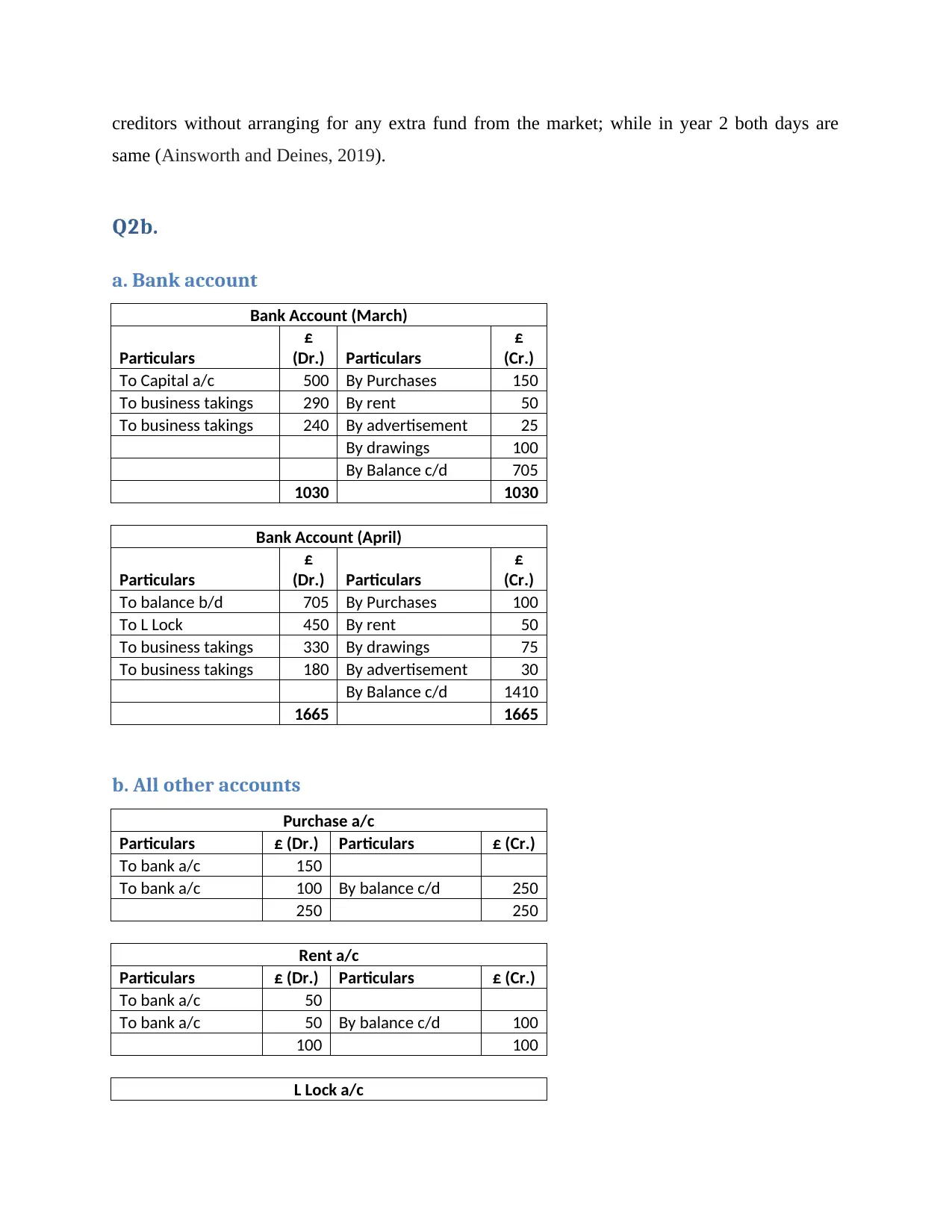

Q2b.

a. Bank account

Bank Account (March)

Particulars

£

(Dr.) Particulars

£

(Cr.)

To Capital a/c 500 By Purchases 150

To business takings 290 By rent 50

To business takings 240 By advertisement 25

By drawings 100

By Balance c/d 705

1030 1030

Bank Account (April)

Particulars

£

(Dr.) Particulars

£

(Cr.)

To balance b/d 705 By Purchases 100

To L Lock 450 By rent 50

To business takings 330 By drawings 75

To business takings 180 By advertisement 30

By Balance c/d 1410

1665 1665

b. All other accounts

Purchase a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To bank a/c 150

To bank a/c 100 By balance c/d 250

250 250

Rent a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To bank a/c 50

To bank a/c 50 By balance c/d 100

100 100

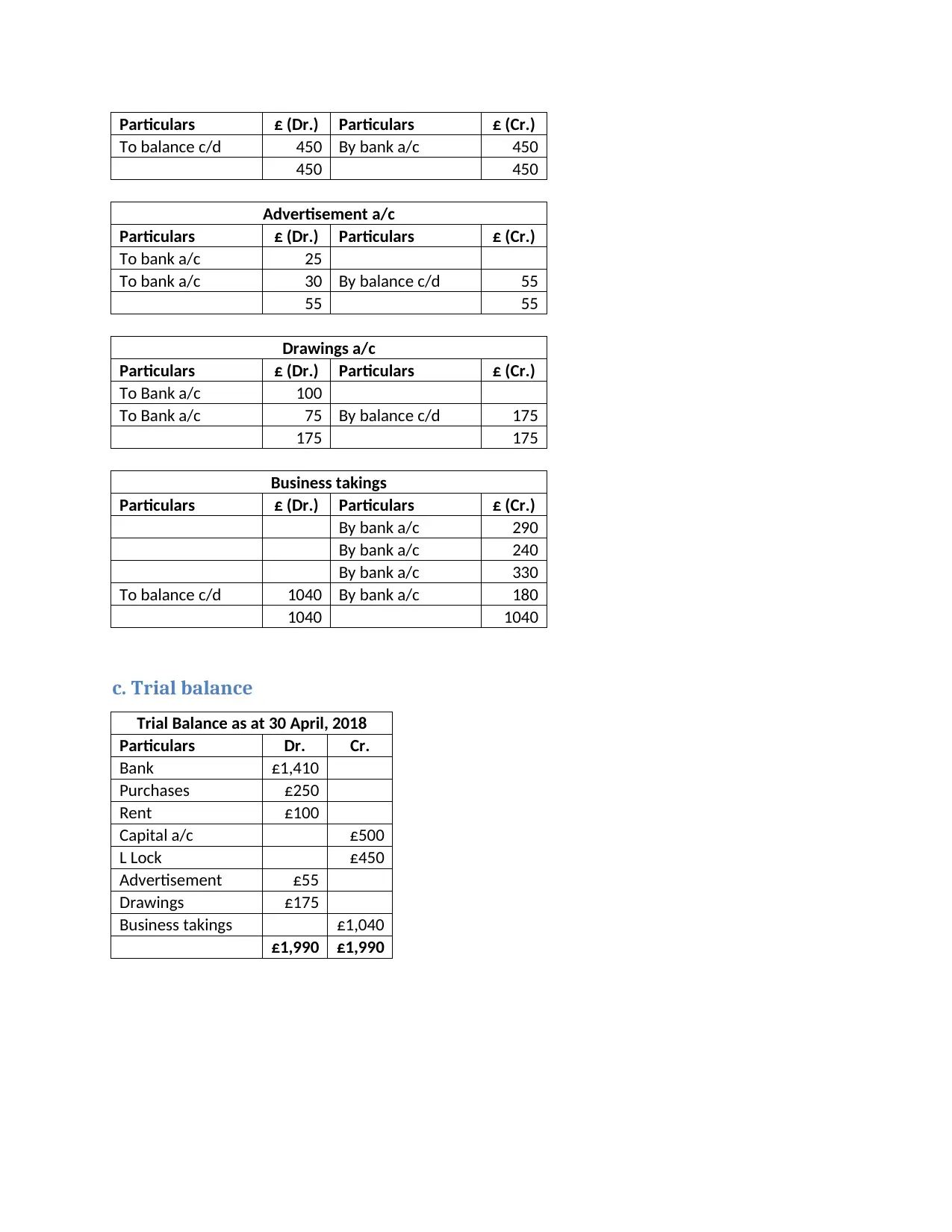

L Lock a/c

same (Ainsworth and Deines, 2019).

Q2b.

a. Bank account

Bank Account (March)

Particulars

£

(Dr.) Particulars

£

(Cr.)

To Capital a/c 500 By Purchases 150

To business takings 290 By rent 50

To business takings 240 By advertisement 25

By drawings 100

By Balance c/d 705

1030 1030

Bank Account (April)

Particulars

£

(Dr.) Particulars

£

(Cr.)

To balance b/d 705 By Purchases 100

To L Lock 450 By rent 50

To business takings 330 By drawings 75

To business takings 180 By advertisement 30

By Balance c/d 1410

1665 1665

b. All other accounts

Purchase a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To bank a/c 150

To bank a/c 100 By balance c/d 250

250 250

Rent a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To bank a/c 50

To bank a/c 50 By balance c/d 100

100 100

L Lock a/c

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars £ (Dr.) Particulars £ (Cr.)

To balance c/d 450 By bank a/c 450

450 450

Advertisement a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To bank a/c 25

To bank a/c 30 By balance c/d 55

55 55

Drawings a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To Bank a/c 100

To Bank a/c 75 By balance c/d 175

175 175

Business takings

Particulars £ (Dr.) Particulars £ (Cr.)

By bank a/c 290

By bank a/c 240

By bank a/c 330

To balance c/d 1040 By bank a/c 180

1040 1040

c. Trial balance

Trial Balance as at 30 April, 2018

Particulars Dr. Cr.

Bank £1,410

Purchases £250

Rent £100

Capital a/c £500

L Lock £450

Advertisement £55

Drawings £175

Business takings £1,040

£1,990 £1,990

To balance c/d 450 By bank a/c 450

450 450

Advertisement a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To bank a/c 25

To bank a/c 30 By balance c/d 55

55 55

Drawings a/c

Particulars £ (Dr.) Particulars £ (Cr.)

To Bank a/c 100

To Bank a/c 75 By balance c/d 175

175 175

Business takings

Particulars £ (Dr.) Particulars £ (Cr.)

By bank a/c 290

By bank a/c 240

By bank a/c 330

To balance c/d 1040 By bank a/c 180

1040 1040

c. Trial balance

Trial Balance as at 30 April, 2018

Particulars Dr. Cr.

Bank £1,410

Purchases £250

Rent £100

Capital a/c £500

L Lock £450

Advertisement £55

Drawings £175

Business takings £1,040

£1,990 £1,990

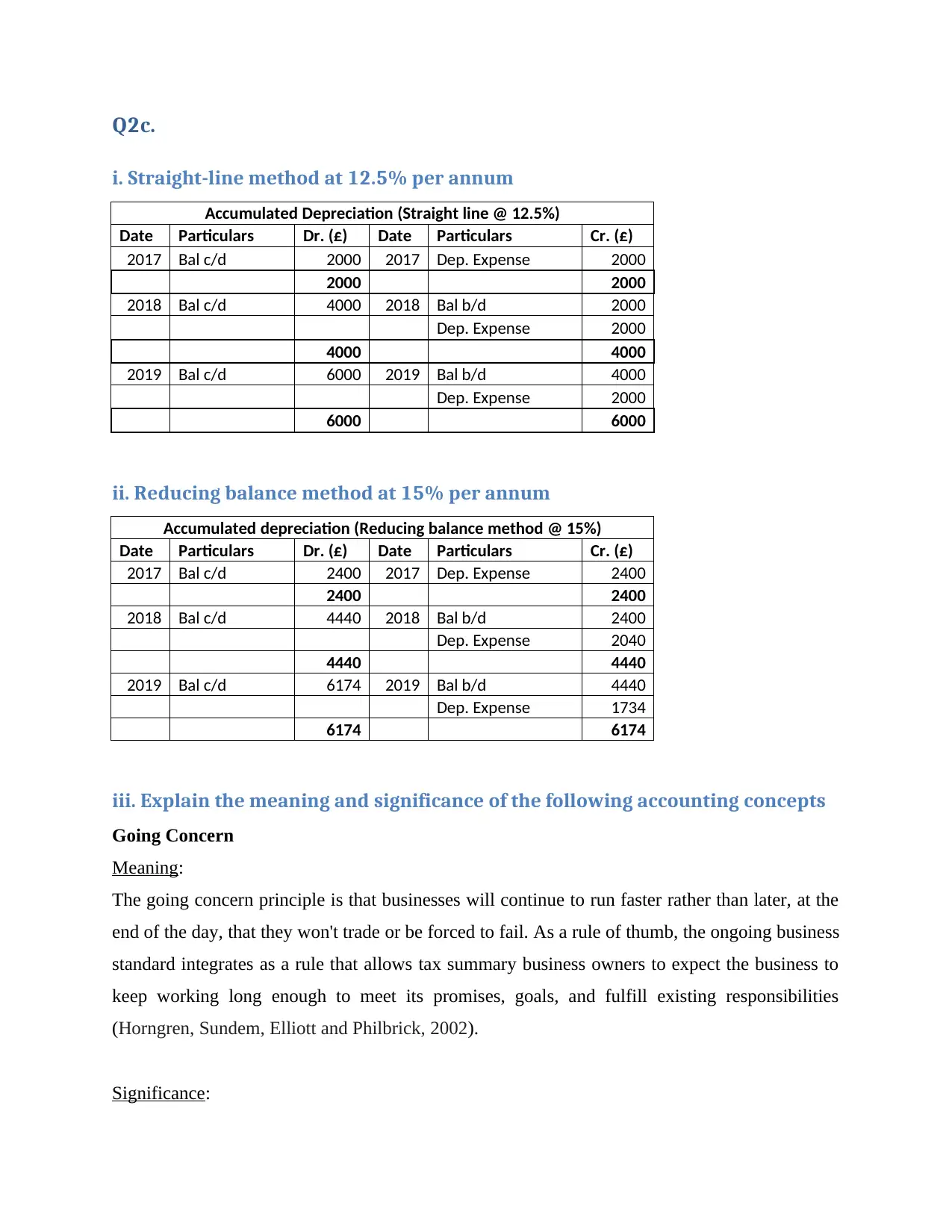

Q2c.

i. Straight-line method at 12.5% per annum

Accumulated Depreciation (Straight line @ 12.5%)

Date Particulars Dr. (£) Date Particulars Cr. (£)

2017 Bal c/d 2000 2017 Dep. Expense 2000

2000 2000

2018 Bal c/d 4000 2018 Bal b/d 2000

Dep. Expense 2000

4000 4000

2019 Bal c/d 6000 2019 Bal b/d 4000

Dep. Expense 2000

6000 6000

ii. Reducing balance method at 15% per annum

Accumulated depreciation (Reducing balance method @ 15%)

Date Particulars Dr. (£) Date Particulars Cr. (£)

2017 Bal c/d 2400 2017 Dep. Expense 2400

2400 2400

2018 Bal c/d 4440 2018 Bal b/d 2400

Dep. Expense 2040

4440 4440

2019 Bal c/d 6174 2019 Bal b/d 4440

Dep. Expense 1734

6174 6174

iii. Explain the meaning and significance of the following accounting concepts

Going Concern

Meaning:

The going concern principle is that businesses will continue to run faster rather than later, at the

end of the day, that they won't trade or be forced to fail. As a rule of thumb, the ongoing business

standard integrates as a rule that allows tax summary business owners to expect the business to

keep working long enough to meet its promises, goals, and fulfill existing responsibilities

(Horngren, Sundem, Elliott and Philbrick, 2002).

Significance:

i. Straight-line method at 12.5% per annum

Accumulated Depreciation (Straight line @ 12.5%)

Date Particulars Dr. (£) Date Particulars Cr. (£)

2017 Bal c/d 2000 2017 Dep. Expense 2000

2000 2000

2018 Bal c/d 4000 2018 Bal b/d 2000

Dep. Expense 2000

4000 4000

2019 Bal c/d 6000 2019 Bal b/d 4000

Dep. Expense 2000

6000 6000

ii. Reducing balance method at 15% per annum

Accumulated depreciation (Reducing balance method @ 15%)

Date Particulars Dr. (£) Date Particulars Cr. (£)

2017 Bal c/d 2400 2017 Dep. Expense 2400

2400 2400

2018 Bal c/d 4440 2018 Bal b/d 2400

Dep. Expense 2040

4440 4440

2019 Bal c/d 6174 2019 Bal b/d 4440

Dep. Expense 1734

6174 6174

iii. Explain the meaning and significance of the following accounting concepts

Going Concern

Meaning:

The going concern principle is that businesses will continue to run faster rather than later, at the

end of the day, that they won't trade or be forced to fail. As a rule of thumb, the ongoing business

standard integrates as a rule that allows tax summary business owners to expect the business to

keep working long enough to meet its promises, goals, and fulfill existing responsibilities

(Horngren, Sundem, Elliott and Philbrick, 2002).

Significance:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.