Introduction to Australian Income Tax Law: Cases and Concepts

VerifiedAdded on 2021/02/20

|9

|2263

|35

Homework Assignment

AI Summary

This assignment provides an overview of Australian income tax law, covering key concepts such as residency, assessable income, and deductions. It examines the tax implications for both Australian residents and foreign residents, including the relevant sections of the Income Tax Assessment Act. The assignment includes analysis of case studies like Federal Commissioner of Taxation v. Applegate and Hayes v. Federal Commissioner of Taxation, to illustrate the application of tax laws to real-world scenarios. It also explores specific deductions, capital gains tax, and the impact of international employment and migration on tax obligations. The document concludes with a discussion of taxation concepts through case studies and reference to relevant articles.

Introduction to income

tax law

tax law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

QUESTION 1...................................................................................................................................1

QUESTION 2...................................................................................................................................1

QUESTION 3...................................................................................................................................1

QUESTION 4...................................................................................................................................1

QUESTION 5...................................................................................................................................2

CONCLUSION................................................................................................................................3

REFERENCES................................................................................................................................4

INTRODUCTION ..........................................................................................................................1

QUESTION 1...................................................................................................................................1

QUESTION 2...................................................................................................................................1

QUESTION 3...................................................................................................................................1

QUESTION 4...................................................................................................................................1

QUESTION 5...................................................................................................................................2

CONCLUSION................................................................................................................................3

REFERENCES................................................................................................................................4

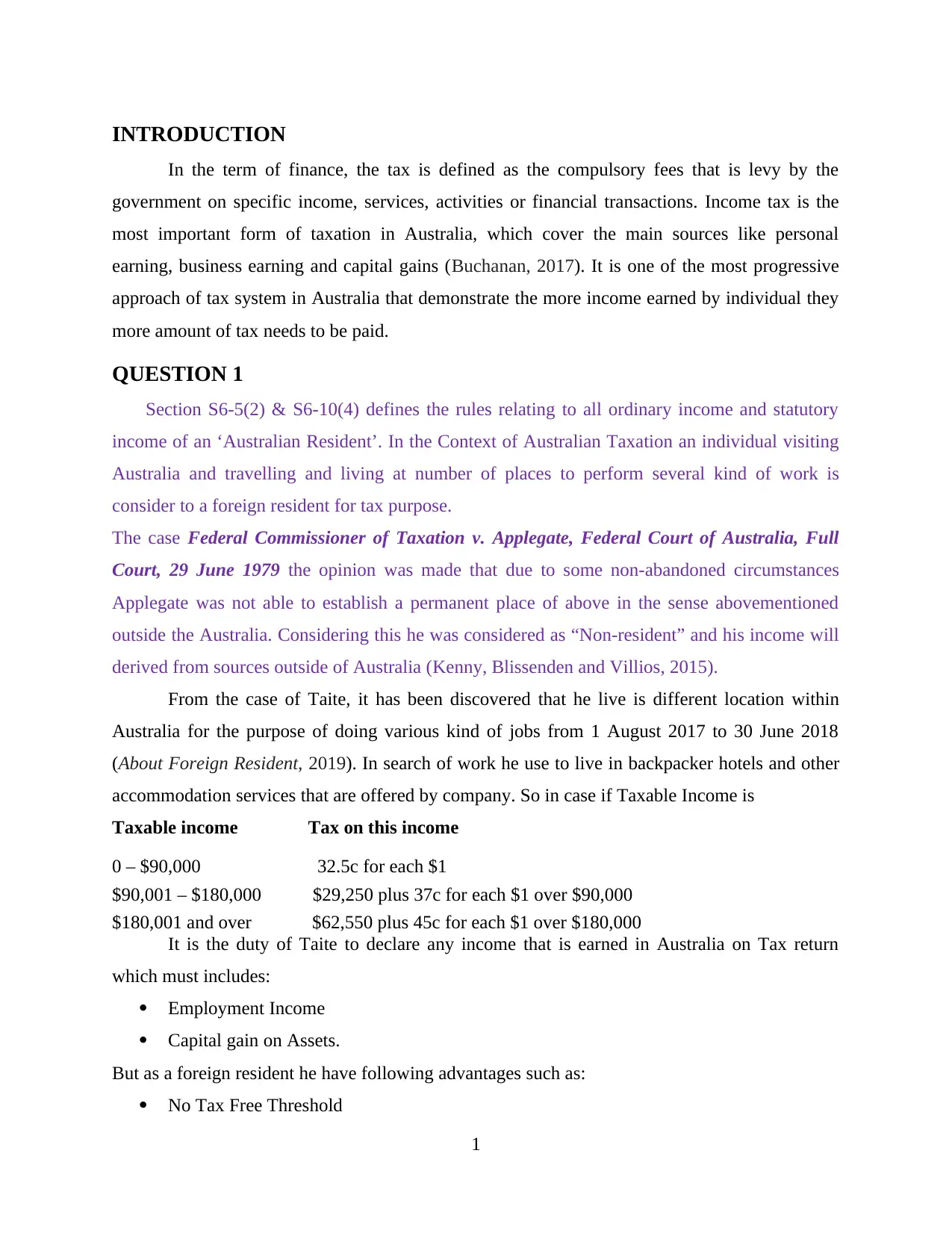

INTRODUCTION

In the term of finance, the tax is defined as the compulsory fees that is levy by the

government on specific income, services, activities or financial transactions. Income tax is the

most important form of taxation in Australia, which cover the main sources like personal

earning, business earning and capital gains (Buchanan, 2017). It is one of the most progressive

approach of tax system in Australia that demonstrate the more income earned by individual they

more amount of tax needs to be paid.

QUESTION 1

Section S6-5(2) & S6-10(4) defines the rules relating to all ordinary income and statutory

income of an ‘Australian Resident’. In the Context of Australian Taxation an individual visiting

Australia and travelling and living at number of places to perform several kind of work is

consider to a foreign resident for tax purpose.

The case Federal Commissioner of Taxation v. Applegate, Federal Court of Australia, Full

Court, 29 June 1979 the opinion was made that due to some non-abandoned circumstances

Applegate was not able to establish a permanent place of above in the sense abovementioned

outside the Australia. Considering this he was considered as “Non-resident” and his income will

derived from sources outside of Australia (Kenny, Blissenden and Villios, 2015).

From the case of Taite, it has been discovered that he live is different location within

Australia for the purpose of doing various kind of jobs from 1 August 2017 to 30 June 2018

(About Foreign Resident, 2019). In search of work he use to live in backpacker hotels and other

accommodation services that are offered by company. So in case if Taxable Income is

Taxable income Tax on this income

0 – $90,000 32.5c for each $1

$90,001 – $180,000 $29,250 plus 37c for each $1 over $90,000

$180,001 and over $62,550 plus 45c for each $1 over $180,000

It is the duty of Taite to declare any income that is earned in Australia on Tax return

which must includes:

Employment Income

Capital gain on Assets.

But as a foreign resident he have following advantages such as:

No Tax Free Threshold

1

In the term of finance, the tax is defined as the compulsory fees that is levy by the

government on specific income, services, activities or financial transactions. Income tax is the

most important form of taxation in Australia, which cover the main sources like personal

earning, business earning and capital gains (Buchanan, 2017). It is one of the most progressive

approach of tax system in Australia that demonstrate the more income earned by individual they

more amount of tax needs to be paid.

QUESTION 1

Section S6-5(2) & S6-10(4) defines the rules relating to all ordinary income and statutory

income of an ‘Australian Resident’. In the Context of Australian Taxation an individual visiting

Australia and travelling and living at number of places to perform several kind of work is

consider to a foreign resident for tax purpose.

The case Federal Commissioner of Taxation v. Applegate, Federal Court of Australia, Full

Court, 29 June 1979 the opinion was made that due to some non-abandoned circumstances

Applegate was not able to establish a permanent place of above in the sense abovementioned

outside the Australia. Considering this he was considered as “Non-resident” and his income will

derived from sources outside of Australia (Kenny, Blissenden and Villios, 2015).

From the case of Taite, it has been discovered that he live is different location within

Australia for the purpose of doing various kind of jobs from 1 August 2017 to 30 June 2018

(About Foreign Resident, 2019). In search of work he use to live in backpacker hotels and other

accommodation services that are offered by company. So in case if Taxable Income is

Taxable income Tax on this income

0 – $90,000 32.5c for each $1

$90,001 – $180,000 $29,250 plus 37c for each $1 over $90,000

$180,001 and over $62,550 plus 45c for each $1 over $180,000

It is the duty of Taite to declare any income that is earned in Australia on Tax return

which must includes:

Employment Income

Capital gain on Assets.

But as a foreign resident he have following advantages such as:

No Tax Free Threshold

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Not need to pay any levy on Medicare

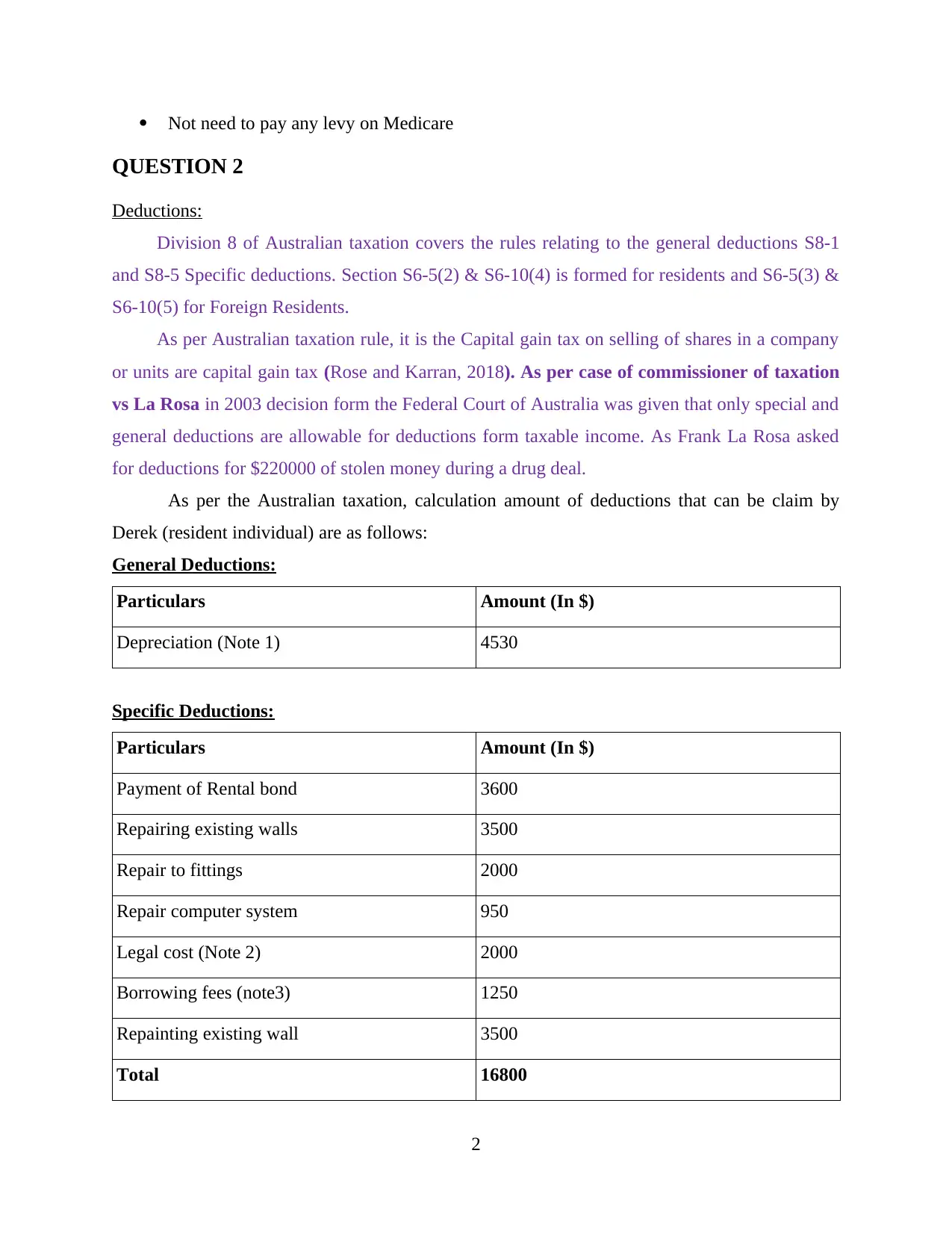

QUESTION 2

Deductions:

Division 8 of Australian taxation covers the rules relating to the general deductions S8-1

and S8-5 Specific deductions. Section S6-5(2) & S6-10(4) is formed for residents and S6-5(3) &

S6-10(5) for Foreign Residents.

As per Australian taxation rule, it is the Capital gain tax on selling of shares in a company

or units are capital gain tax (Rose and Karran, 2018). As per case of commissioner of taxation

vs La Rosa in 2003 decision form the Federal Court of Australia was given that only special and

general deductions are allowable for deductions form taxable income. As Frank La Rosa asked

for deductions for $220000 of stolen money during a drug deal.

As per the Australian taxation, calculation amount of deductions that can be claim by

Derek (resident individual) are as follows:

General Deductions:

Particulars Amount (In $)

Depreciation (Note 1) 4530

Specific Deductions:

Particulars Amount (In $)

Payment of Rental bond 3600

Repairing existing walls 3500

Repair to fittings 2000

Repair computer system 950

Legal cost (Note 2) 2000

Borrowing fees (note3) 1250

Repainting existing wall 3500

Total 16800

2

QUESTION 2

Deductions:

Division 8 of Australian taxation covers the rules relating to the general deductions S8-1

and S8-5 Specific deductions. Section S6-5(2) & S6-10(4) is formed for residents and S6-5(3) &

S6-10(5) for Foreign Residents.

As per Australian taxation rule, it is the Capital gain tax on selling of shares in a company

or units are capital gain tax (Rose and Karran, 2018). As per case of commissioner of taxation

vs La Rosa in 2003 decision form the Federal Court of Australia was given that only special and

general deductions are allowable for deductions form taxable income. As Frank La Rosa asked

for deductions for $220000 of stolen money during a drug deal.

As per the Australian taxation, calculation amount of deductions that can be claim by

Derek (resident individual) are as follows:

General Deductions:

Particulars Amount (In $)

Depreciation (Note 1) 4530

Specific Deductions:

Particulars Amount (In $)

Payment of Rental bond 3600

Repairing existing walls 3500

Repair to fittings 2000

Repair computer system 950

Legal cost (Note 2) 2000

Borrowing fees (note3) 1250

Repainting existing wall 3500

Total 16800

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Note1: As per Australian income tax act, depreciation rate on fixed assets which are given in the

questions is 15 percentage (Tax Deductions, 2019). Therefore, this rate of depreciation is to be

apply.

Note2: Legal cost paid for business is a business expense and deduction of this shall be given to

the individual assesses.

Note3: borrowing cost paid for taking business loan falls in the category of specific deduction

subject to some condition as may be provided in act. There specific deduction shall be given in

this respect.

Note4: Repair to existing walls and computer system is not capitalised because it does not

provide the any economical benefits in future. Therefore, specific deduction is to be given for

this.

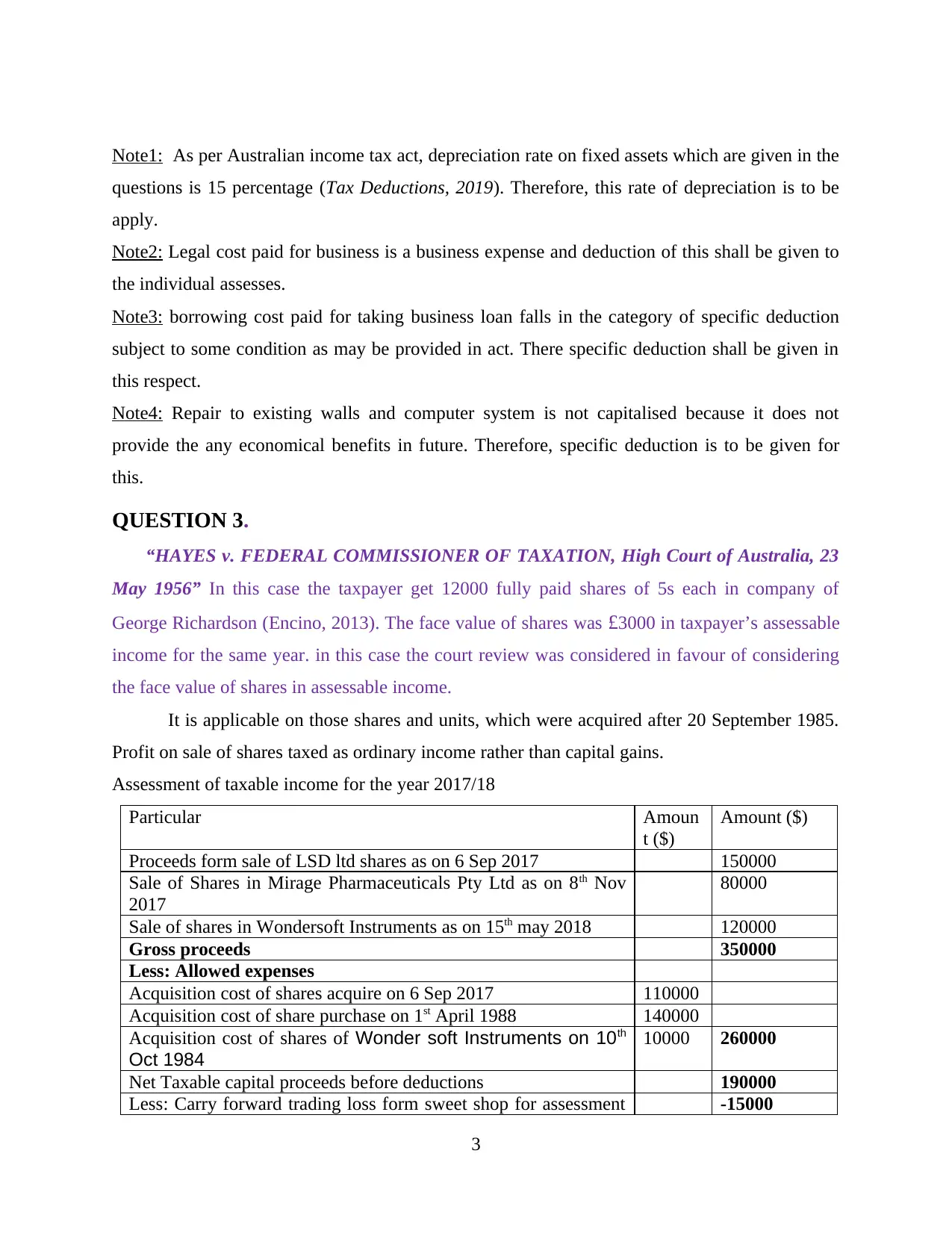

QUESTION 3.

“HAYES v. FEDERAL COMMISSIONER OF TAXATION, High Court of Australia, 23

May 1956” In this case the taxpayer get 12000 fully paid shares of 5s each in company of

George Richardson (Encino, 2013). The face value of shares was £3000 in taxpayer’s assessable

income for the same year. in this case the court review was considered in favour of considering

the face value of shares in assessable income.

It is applicable on those shares and units, which were acquired after 20 September 1985.

Profit on sale of shares taxed as ordinary income rather than capital gains.

Assessment of taxable income for the year 2017/18

Particular Amoun

t ($)

Amount ($)

Proceeds form sale of LSD ltd shares as on 6 Sep 2017 150000

Sale of Shares in Mirage Pharmaceuticals Pty Ltd as on 8th Nov

2017

80000

Sale of shares in Wondersoft Instruments as on 15th may 2018 120000

Gross proceeds 350000

Less: Allowed expenses

Acquisition cost of shares acquire on 6 Sep 2017 110000

Acquisition cost of share purchase on 1st April 1988 140000

Acquisition cost of shares of Wonder soft Instruments on 10th

Oct 1984

10000 260000

Net Taxable capital proceeds before deductions 190000

Less: Carry forward trading loss form sweet shop for assessment -15000

3

questions is 15 percentage (Tax Deductions, 2019). Therefore, this rate of depreciation is to be

apply.

Note2: Legal cost paid for business is a business expense and deduction of this shall be given to

the individual assesses.

Note3: borrowing cost paid for taking business loan falls in the category of specific deduction

subject to some condition as may be provided in act. There specific deduction shall be given in

this respect.

Note4: Repair to existing walls and computer system is not capitalised because it does not

provide the any economical benefits in future. Therefore, specific deduction is to be given for

this.

QUESTION 3.

“HAYES v. FEDERAL COMMISSIONER OF TAXATION, High Court of Australia, 23

May 1956” In this case the taxpayer get 12000 fully paid shares of 5s each in company of

George Richardson (Encino, 2013). The face value of shares was £3000 in taxpayer’s assessable

income for the same year. in this case the court review was considered in favour of considering

the face value of shares in assessable income.

It is applicable on those shares and units, which were acquired after 20 September 1985.

Profit on sale of shares taxed as ordinary income rather than capital gains.

Assessment of taxable income for the year 2017/18

Particular Amoun

t ($)

Amount ($)

Proceeds form sale of LSD ltd shares as on 6 Sep 2017 150000

Sale of Shares in Mirage Pharmaceuticals Pty Ltd as on 8th Nov

2017

80000

Sale of shares in Wondersoft Instruments as on 15th may 2018 120000

Gross proceeds 350000

Less: Allowed expenses

Acquisition cost of shares acquire on 6 Sep 2017 110000

Acquisition cost of share purchase on 1st April 1988 140000

Acquisition cost of shares of Wonder soft Instruments on 10th

Oct 1984

10000 260000

Net Taxable capital proceeds before deductions 190000

Less: Carry forward trading loss form sweet shop for assessment -15000

3

year 2017/18

Net taxable capital gain 175000

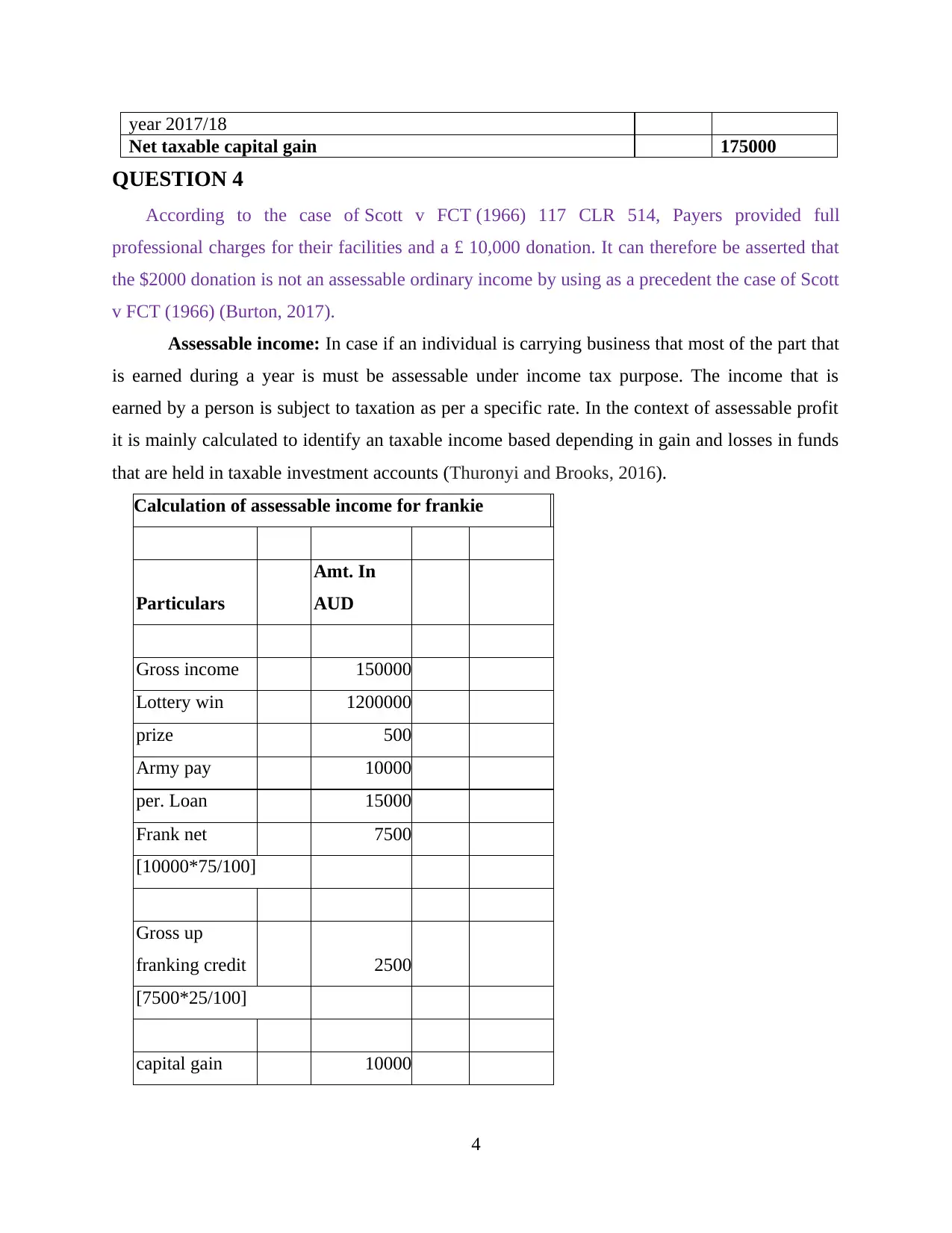

QUESTION 4

According to the case of Scott v FCT (1966) 117 CLR 514, Payers provided full

professional charges for their facilities and a £ 10,000 donation. It can therefore be asserted that

the $2000 donation is not an assessable ordinary income by using as a precedent the case of Scott

v FCT (1966) (Burton, 2017).

Assessable income: In case if an individual is carrying business that most of the part that

is earned during a year is must be assessable under income tax purpose. The income that is

earned by a person is subject to taxation as per a specific rate. In the context of assessable profit

it is mainly calculated to identify an taxable income based depending in gain and losses in funds

that are held in taxable investment accounts (Thuronyi and Brooks, 2016).

Calculation of assessable income for frankie

Particulars

Amt. In

AUD

Gross income 150000

Lottery win 1200000

prize 500

Army pay 10000

per. Loan 15000

Frank net 7500

[10000*75/100]

Gross up

franking credit 2500

[7500*25/100]

capital gain 10000

4

Net taxable capital gain 175000

QUESTION 4

According to the case of Scott v FCT (1966) 117 CLR 514, Payers provided full

professional charges for their facilities and a £ 10,000 donation. It can therefore be asserted that

the $2000 donation is not an assessable ordinary income by using as a precedent the case of Scott

v FCT (1966) (Burton, 2017).

Assessable income: In case if an individual is carrying business that most of the part that

is earned during a year is must be assessable under income tax purpose. The income that is

earned by a person is subject to taxation as per a specific rate. In the context of assessable profit

it is mainly calculated to identify an taxable income based depending in gain and losses in funds

that are held in taxable investment accounts (Thuronyi and Brooks, 2016).

Calculation of assessable income for frankie

Particulars

Amt. In

AUD

Gross income 150000

Lottery win 1200000

prize 500

Army pay 10000

per. Loan 15000

Frank net 7500

[10000*75/100]

Gross up

franking credit 2500

[7500*25/100]

capital gain 10000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 5

There are some useful articles from different sources related with taxation are discussed

below (Articles related to taxation concepts, 2019).

Simon- A migrant from England Changed his Mind.

A) Facts

Simon was to lived with his family in England and decided to shift Australia on

permanent basis (Pogge and Mehta, 2016). They arrived in Sydney where he find a respective

job in accounting firm and bought house and children start going to private school. As time

passes, his family was not happy while living in Australia and decided to return England. They

live for only 4 months therefore they will still be treated as British Citizens.

B) Taxation concept

The tax legislative related with Simon case will be according to Taxation Ruling TR

98/17 which states that calculation of income tax is on the basis of resident status of individual

entering in Australia shows the circumstances in which a person is considered as residing in

Australia (Taxation Ruling TR 98/17, 2019). This law mainly have different factors that

determine the living of an individual such as:

Intention of presence

Family and business or employment ties

Maintenance and location of assets

social and living arrangements.

As Simon and his family lives for short duration and they comes in the factors intention

or purpose of presence thus they are not be consider an Australian resident for income Tax

Purpose.

C) In the article the taxation concept states that Simon was not liable to any income Tax as they

he and his family live only for 4 months, which is, not long enough to qualify for citizenship.

Bronwyn- An Extended job Overseas.

A) Facts

Bronwyn is an Australian resident have a job offer to work in other country for three

years with the option to get extension for more 3 years. They have house in Australia and

decided to come back one day and move with her husband and three children. She is not ready to

make extension decision as she wanted to first look weather her family is ready to live or not. To

5

There are some useful articles from different sources related with taxation are discussed

below (Articles related to taxation concepts, 2019).

Simon- A migrant from England Changed his Mind.

A) Facts

Simon was to lived with his family in England and decided to shift Australia on

permanent basis (Pogge and Mehta, 2016). They arrived in Sydney where he find a respective

job in accounting firm and bought house and children start going to private school. As time

passes, his family was not happy while living in Australia and decided to return England. They

live for only 4 months therefore they will still be treated as British Citizens.

B) Taxation concept

The tax legislative related with Simon case will be according to Taxation Ruling TR

98/17 which states that calculation of income tax is on the basis of resident status of individual

entering in Australia shows the circumstances in which a person is considered as residing in

Australia (Taxation Ruling TR 98/17, 2019). This law mainly have different factors that

determine the living of an individual such as:

Intention of presence

Family and business or employment ties

Maintenance and location of assets

social and living arrangements.

As Simon and his family lives for short duration and they comes in the factors intention

or purpose of presence thus they are not be consider an Australian resident for income Tax

Purpose.

C) In the article the taxation concept states that Simon was not liable to any income Tax as they

he and his family live only for 4 months, which is, not long enough to qualify for citizenship.

Bronwyn- An Extended job Overseas.

A) Facts

Bronwyn is an Australian resident have a job offer to work in other country for three

years with the option to get extension for more 3 years. They have house in Australia and

decided to come back one day and move with her husband and three children. She is not ready to

make extension decision as she wanted to first look weather her family is ready to live or not. To

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

live in other country they have rent a house with an accommodation allowance that is provided in

contract (Mares and Queralt, 2015).

B) Taxation concept

From the income tax prospectus, the total amount received by Bronwyn from her house

that is given on rent will be computed as a part of taxable income. She also took a overseas house

for rent which allowances are paid by company so she will not be able to get any redemption in

case of income generated from house in Australia.

C) There is a connection between taxation concept and indicators of good tax policy as there are

five basic situation that can be maximized to the superlative extent accomplishment.

CONCLUSION

From the above report it has been calculated that income tax is mainly paid on total

revenue that is received by an individual like salary, wages, investments, interest, profit and

payments from rent. An individual can get deduction from paying tax in case if they are eligible

for specific tac offsets and government rebates. There are different treatment for an individual

that is visit Australia for work and business purpose.

6

contract (Mares and Queralt, 2015).

B) Taxation concept

From the income tax prospectus, the total amount received by Bronwyn from her house

that is given on rent will be computed as a part of taxable income. She also took a overseas house

for rent which allowances are paid by company so she will not be able to get any redemption in

case of income generated from house in Australia.

C) There is a connection between taxation concept and indicators of good tax policy as there are

five basic situation that can be maximized to the superlative extent accomplishment.

CONCLUSION

From the above report it has been calculated that income tax is mainly paid on total

revenue that is received by an individual like salary, wages, investments, interest, profit and

payments from rent. An individual can get deduction from paying tax in case if they are eligible

for specific tac offsets and government rebates. There are different treatment for an individual

that is visit Australia for work and business purpose.

6

REFERENCES

Books and Journals:

Kenny, P., Blissenden, M. and Villios, S., 2015. Residency and Australians working overseas:

can be an expensive lesson in tax Law.

Encino, M., 2013. Holy Profits: How Federal Law Allows for the Abuse of the Church Tax-

Exempt Status. Hous. Bus. & Tax LJ. 14. p.78.

Burton, M., 2017. A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the

Purposes of the Australian Income Tax. J. Austl. Tax'n. 19. p.50.

Buchanan, A., 2017. A critical introduction to Rawls’ theory of justice. In Distributive Justice

(pp. 175-211). Routledge.

Mares, I. and Queralt, D., 2015. The non-democratic origins of income taxation. Comparative

Political Studies. 48(14). pp.1974-2009.

Pogge, T. and Mehta, K. eds., 2016. Global tax fairness. Oxford University Press.

Rose, R. and Karran, T., 2018. Taxation by political inertia: Financing the growth of

government in Britain. Routledge.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International BV.

Online

Taxation Ruling TR 98/17. 2019. [Online] Available Through:

<https://www.ato.gov.au/Individuals/International-tax-for-individuals/In-detail/

Residency/Examples-of-residents-and-foreign-residents/>.

Articles related to taxation concepts. 2019. [Online] Available Through:

<https://economictimes.indiatimes.com/nri/nri-tax/are-you-earning-abroad-know-the-

tax-rules/slideshow/59860408.cms>.

Tax Deductions. 2019. [Online] Available Through:

<http://taxsummaries.pwc.com/ID/Australia-Individual-Deductions>.

7

Books and Journals:

Kenny, P., Blissenden, M. and Villios, S., 2015. Residency and Australians working overseas:

can be an expensive lesson in tax Law.

Encino, M., 2013. Holy Profits: How Federal Law Allows for the Abuse of the Church Tax-

Exempt Status. Hous. Bus. & Tax LJ. 14. p.78.

Burton, M., 2017. A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the

Purposes of the Australian Income Tax. J. Austl. Tax'n. 19. p.50.

Buchanan, A., 2017. A critical introduction to Rawls’ theory of justice. In Distributive Justice

(pp. 175-211). Routledge.

Mares, I. and Queralt, D., 2015. The non-democratic origins of income taxation. Comparative

Political Studies. 48(14). pp.1974-2009.

Pogge, T. and Mehta, K. eds., 2016. Global tax fairness. Oxford University Press.

Rose, R. and Karran, T., 2018. Taxation by political inertia: Financing the growth of

government in Britain. Routledge.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International BV.

Online

Taxation Ruling TR 98/17. 2019. [Online] Available Through:

<https://www.ato.gov.au/Individuals/International-tax-for-individuals/In-detail/

Residency/Examples-of-residents-and-foreign-residents/>.

Articles related to taxation concepts. 2019. [Online] Available Through:

<https://economictimes.indiatimes.com/nri/nri-tax/are-you-earning-abroad-know-the-

tax-rules/slideshow/59860408.cms>.

Tax Deductions. 2019. [Online] Available Through:

<http://taxsummaries.pwc.com/ID/Australia-Individual-Deductions>.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.