Comparison of Traditional and Activity-Based Costing

VerifiedAdded on 2019/11/26

|7

|930

|313

Essay

AI Summary

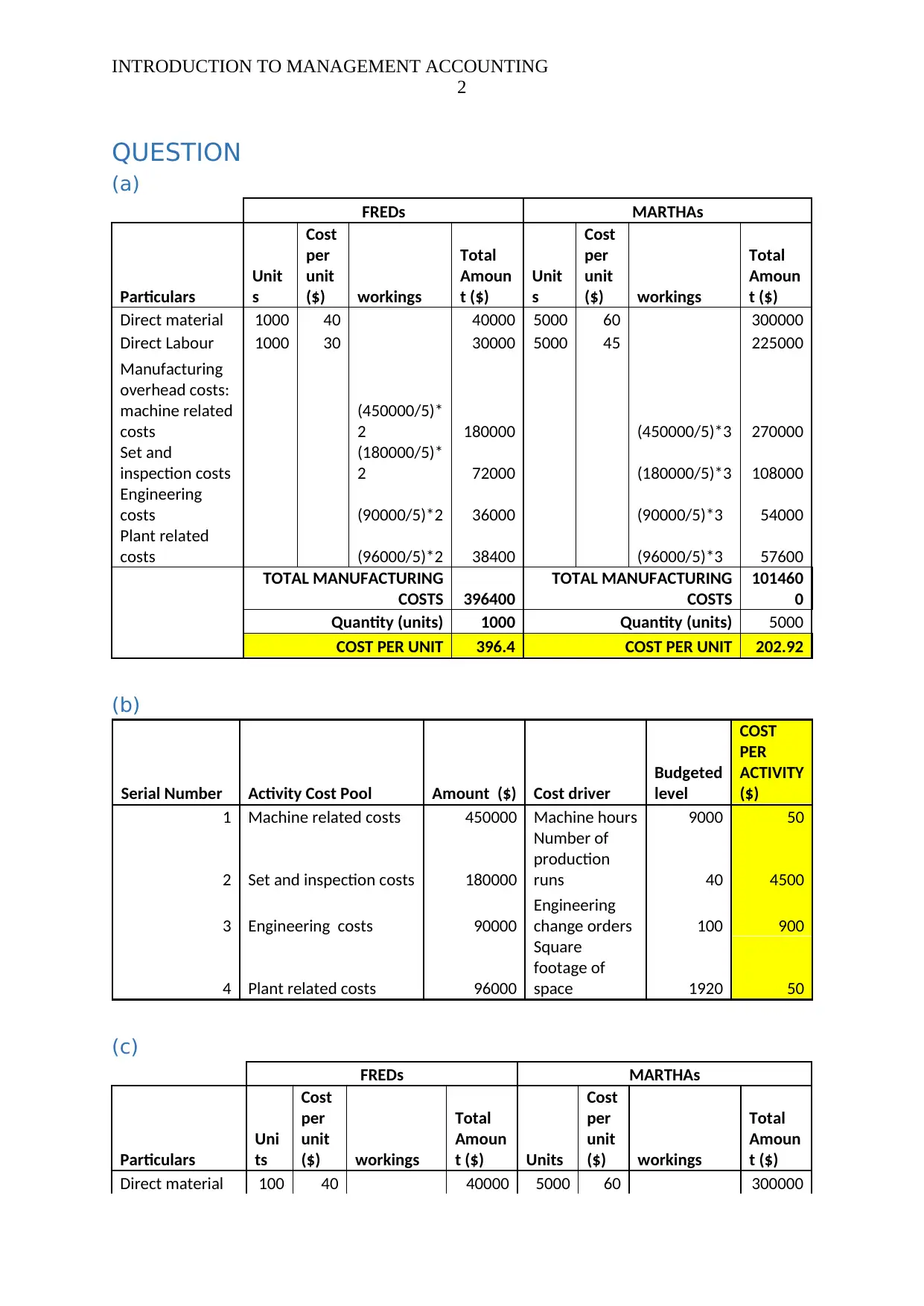

The provided content discusses the concept of plant-related costs and manufacturing overhead costs, highlighting the importance of Activity-Based Costing (ABC) in today's environment. The traditional costing system is criticized for its limitations, such as ignoring non-manufacturing costs and apportioning overhead costs based on direct labor hours. In contrast, ABC provides greater accuracy in costing, eliminates immaterial costs, facilitates benchmarking, and promotes continuous improvement through total quality control. However, the implementation of ABC can be long and time-consuming, and it requires caution when making decisions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.