Job Costing System and Activity Based Costing for Voltus Communication

VerifiedAdded on 2022/11/09

|7

|1897

|70

AI Summary

This article discusses the use of Job Costing System and Activity Based Costing for Voltus Communication, including computation of pre-determined overhead rate, overhead applied, under/over applied overhead, and disposal methods. It also explores the possibility of using ABC for better costing and pricing.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Introduction

Voltus Communication currently uses Job Costing System. Job Costing

system is one of the most simple methods of costing where the company

accumulates all the cost in the production in heads of direct material,

direct labour and manufacturing overheads and applies it evenly to the

jobs of the company using a single pre determined overhead rate for

overheads which can be machine hours, labour hours, labour cost or any

other single means for allocation (Bragg, 2019).

Voltus Communication is using machine hours as a means for computing

the pre-determined overhead rate for applying manufacturing overheads

to the jobs of the company. It is given that the company estimates the

pre-determined overhead rate using and estimated overheads for the year

at $3,600,000 and a total of 80,000 machine hour.

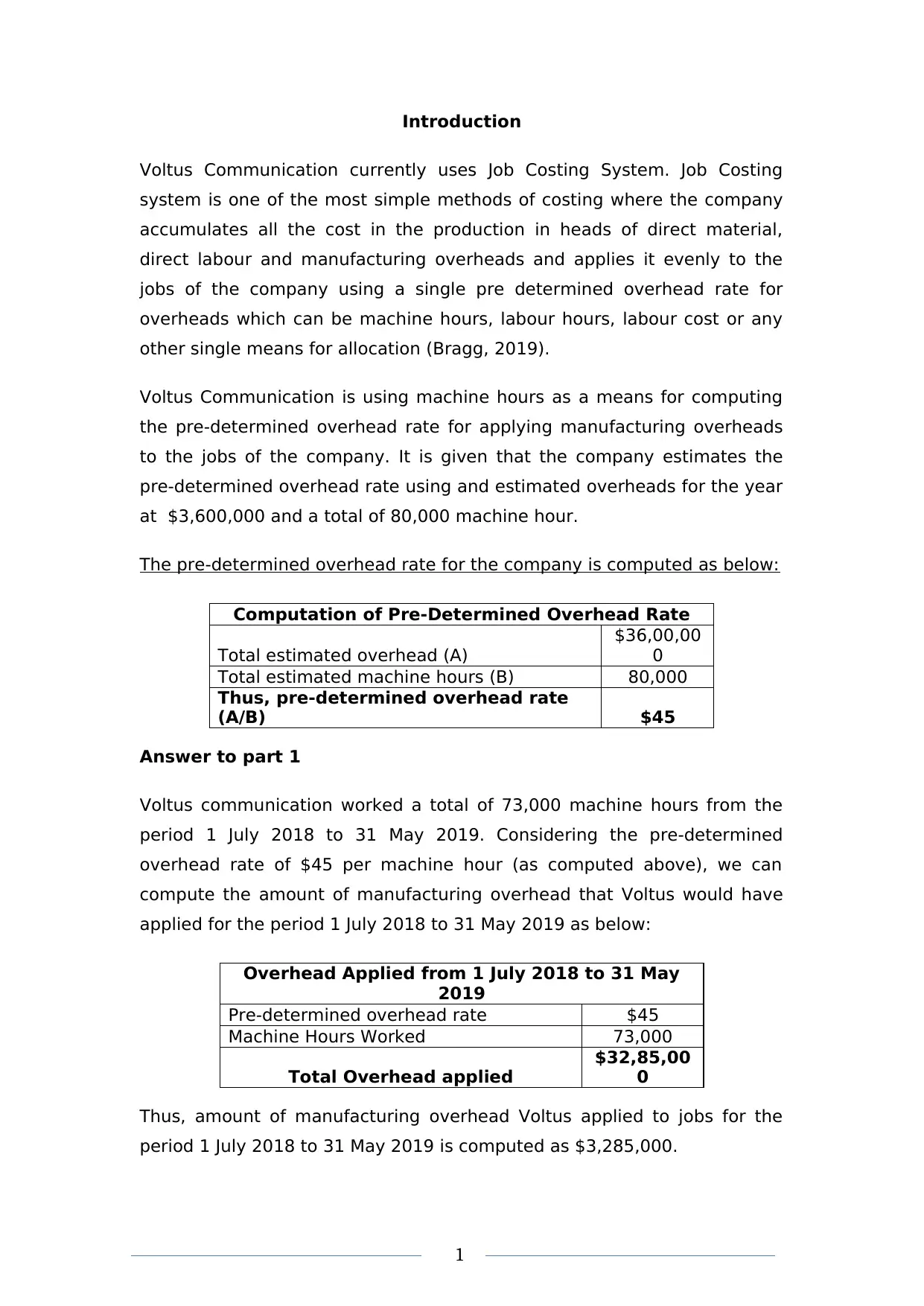

The pre-determined overhead rate for the company is computed as below:

Computation of Pre-Determined Overhead Rate

Total estimated overhead (A)

$36,00,00

0

Total estimated machine hours (B) 80,000

Thus, pre-determined overhead rate

(A/B) $45

Answer to part 1

Voltus communication worked a total of 73,000 machine hours from the

period 1 July 2018 to 31 May 2019. Considering the pre-determined

overhead rate of $45 per machine hour (as computed above), we can

compute the amount of manufacturing overhead that Voltus would have

applied for the period 1 July 2018 to 31 May 2019 as below:

Overhead Applied from 1 July 2018 to 31 May

2019

Pre-determined overhead rate $45

Machine Hours Worked 73,000

Total Overhead applied

$32,85,00

0

Thus, amount of manufacturing overhead Voltus applied to jobs for the

period 1 July 2018 to 31 May 2019 is computed as $3,285,000.

1

Voltus Communication currently uses Job Costing System. Job Costing

system is one of the most simple methods of costing where the company

accumulates all the cost in the production in heads of direct material,

direct labour and manufacturing overheads and applies it evenly to the

jobs of the company using a single pre determined overhead rate for

overheads which can be machine hours, labour hours, labour cost or any

other single means for allocation (Bragg, 2019).

Voltus Communication is using machine hours as a means for computing

the pre-determined overhead rate for applying manufacturing overheads

to the jobs of the company. It is given that the company estimates the

pre-determined overhead rate using and estimated overheads for the year

at $3,600,000 and a total of 80,000 machine hour.

The pre-determined overhead rate for the company is computed as below:

Computation of Pre-Determined Overhead Rate

Total estimated overhead (A)

$36,00,00

0

Total estimated machine hours (B) 80,000

Thus, pre-determined overhead rate

(A/B) $45

Answer to part 1

Voltus communication worked a total of 73,000 machine hours from the

period 1 July 2018 to 31 May 2019. Considering the pre-determined

overhead rate of $45 per machine hour (as computed above), we can

compute the amount of manufacturing overhead that Voltus would have

applied for the period 1 July 2018 to 31 May 2019 as below:

Overhead Applied from 1 July 2018 to 31 May

2019

Pre-determined overhead rate $45

Machine Hours Worked 73,000

Total Overhead applied

$32,85,00

0

Thus, amount of manufacturing overhead Voltus applied to jobs for the

period 1 July 2018 to 31 May 2019 is computed as $3,285,000.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

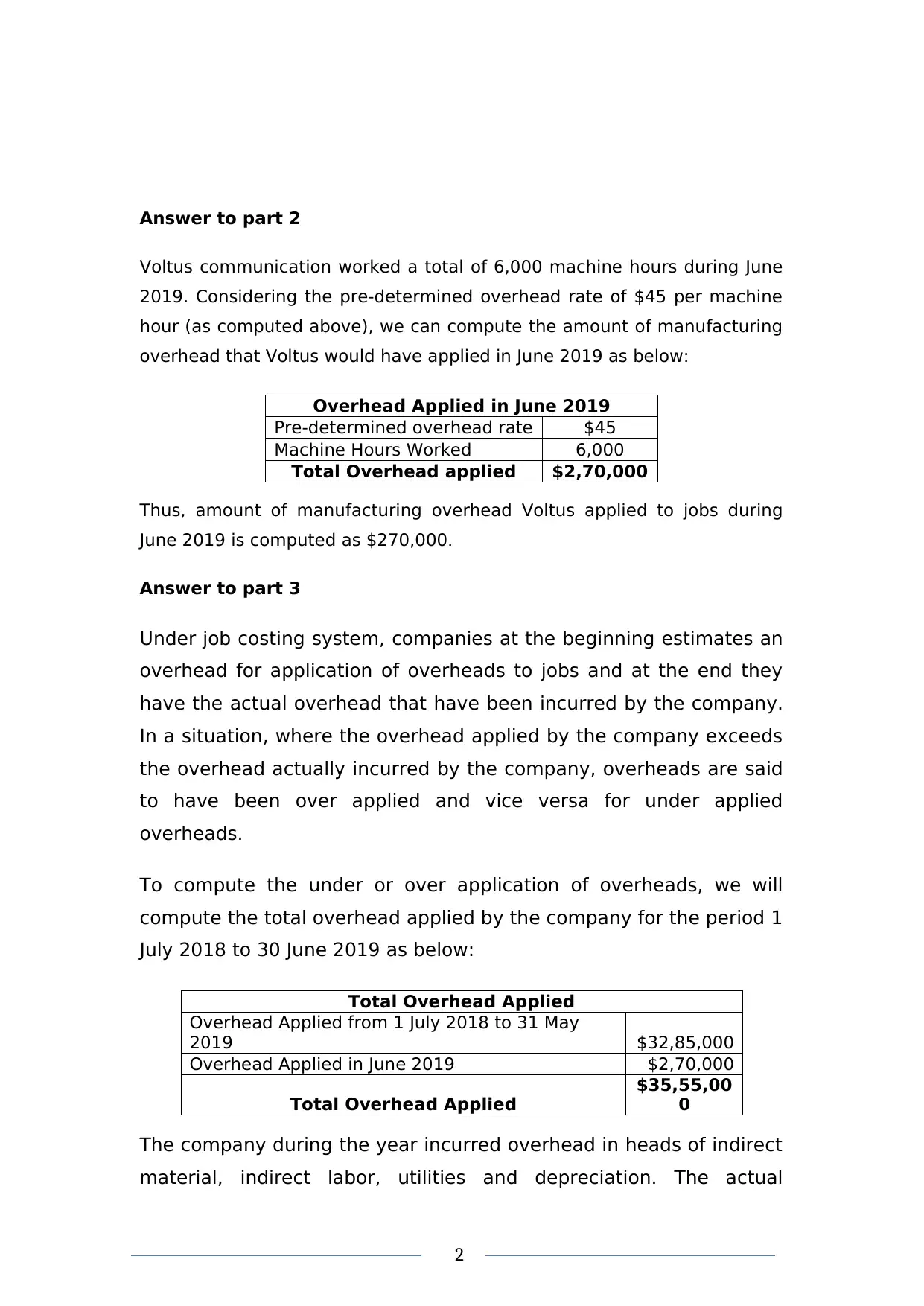

Answer to part 2

Voltus communication worked a total of 6,000 machine hours during June

2019. Considering the pre-determined overhead rate of $45 per machine

hour (as computed above), we can compute the amount of manufacturing

overhead that Voltus would have applied in June 2019 as below:

Overhead Applied in June 2019

Pre-determined overhead rate $45

Machine Hours Worked 6,000

Total Overhead applied $2,70,000

Thus, amount of manufacturing overhead Voltus applied to jobs during

June 2019 is computed as $270,000.

Answer to part 3

Under job costing system, companies at the beginning estimates an

overhead for application of overheads to jobs and at the end they

have the actual overhead that have been incurred by the company.

In a situation, where the overhead applied by the company exceeds

the overhead actually incurred by the company, overheads are said

to have been over applied and vice versa for under applied

overheads.

To compute the under or over application of overheads, we will

compute the total overhead applied by the company for the period 1

July 2018 to 30 June 2019 as below:

Total Overhead Applied

Overhead Applied from 1 July 2018 to 31 May

2019 $32,85,000

Overhead Applied in June 2019 $2,70,000

Total Overhead Applied

$35,55,00

0

The company during the year incurred overhead in heads of indirect

material, indirect labor, utilities and depreciation. The actual

2

Voltus communication worked a total of 6,000 machine hours during June

2019. Considering the pre-determined overhead rate of $45 per machine

hour (as computed above), we can compute the amount of manufacturing

overhead that Voltus would have applied in June 2019 as below:

Overhead Applied in June 2019

Pre-determined overhead rate $45

Machine Hours Worked 6,000

Total Overhead applied $2,70,000

Thus, amount of manufacturing overhead Voltus applied to jobs during

June 2019 is computed as $270,000.

Answer to part 3

Under job costing system, companies at the beginning estimates an

overhead for application of overheads to jobs and at the end they

have the actual overhead that have been incurred by the company.

In a situation, where the overhead applied by the company exceeds

the overhead actually incurred by the company, overheads are said

to have been over applied and vice versa for under applied

overheads.

To compute the under or over application of overheads, we will

compute the total overhead applied by the company for the period 1

July 2018 to 30 June 2019 as below:

Total Overhead Applied

Overhead Applied from 1 July 2018 to 31 May

2019 $32,85,000

Overhead Applied in June 2019 $2,70,000

Total Overhead Applied

$35,55,00

0

The company during the year incurred overhead in heads of indirect

material, indirect labor, utilities and depreciation. The actual

2

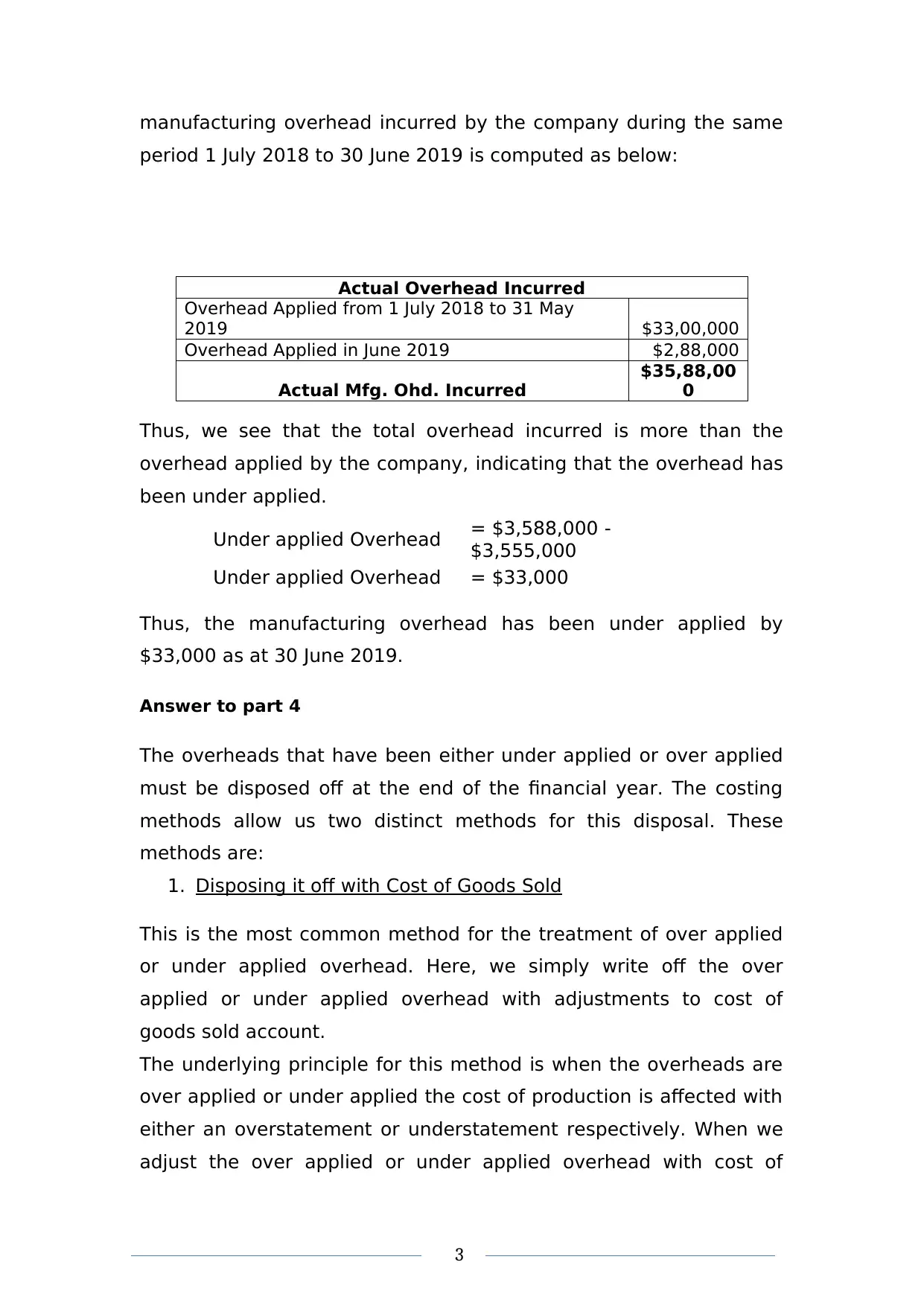

manufacturing overhead incurred by the company during the same

period 1 July 2018 to 30 June 2019 is computed as below:

Actual Overhead Incurred

Overhead Applied from 1 July 2018 to 31 May

2019 $33,00,000

Overhead Applied in June 2019 $2,88,000

Actual Mfg. Ohd. Incurred

$35,88,00

0

Thus, we see that the total overhead incurred is more than the

overhead applied by the company, indicating that the overhead has

been under applied.

Under applied Overhead = $3,588,000 -

$3,555,000

Under applied Overhead = $33,000

Thus, the manufacturing overhead has been under applied by

$33,000 as at 30 June 2019.

Answer to part 4

The overheads that have been either under applied or over applied

must be disposed off at the end of the financial year. The costing

methods allow us two distinct methods for this disposal. These

methods are:

1. Disposing it off with Cost of Goods Sold

This is the most common method for the treatment of over applied

or under applied overhead. Here, we simply write off the over

applied or under applied overhead with adjustments to cost of

goods sold account.

The underlying principle for this method is when the overheads are

over applied or under applied the cost of production is affected with

either an overstatement or understatement respectively. When we

adjust the over applied or under applied overhead with cost of

3

period 1 July 2018 to 30 June 2019 is computed as below:

Actual Overhead Incurred

Overhead Applied from 1 July 2018 to 31 May

2019 $33,00,000

Overhead Applied in June 2019 $2,88,000

Actual Mfg. Ohd. Incurred

$35,88,00

0

Thus, we see that the total overhead incurred is more than the

overhead applied by the company, indicating that the overhead has

been under applied.

Under applied Overhead = $3,588,000 -

$3,555,000

Under applied Overhead = $33,000

Thus, the manufacturing overhead has been under applied by

$33,000 as at 30 June 2019.

Answer to part 4

The overheads that have been either under applied or over applied

must be disposed off at the end of the financial year. The costing

methods allow us two distinct methods for this disposal. These

methods are:

1. Disposing it off with Cost of Goods Sold

This is the most common method for the treatment of over applied

or under applied overhead. Here, we simply write off the over

applied or under applied overhead with adjustments to cost of

goods sold account.

The underlying principle for this method is when the overheads are

over applied or under applied the cost of production is affected with

either an overstatement or understatement respectively. When we

adjust the over applied or under applied overhead with cost of

3

goods sold we actually equalize the cost of production for accuracy.

Transfer of over applied or under applied overhead to cost of goods

sold nullifies their balances.

This method is recommended for use when the amount of over

applied or under applied overhead is not very significant for the

company. When the over applied or under applied overhead are not

a very high value item, the company can simply adjust it with cost

of goods sold.

2. Dispose it off with all cost heads including WIP inventory,

Finished Goods and Cost of Goods Sold.

In a situation where the over applied or under applied overhead are

of significant value, simply adjusting it with the cost of goods sold is

not the best option. The over applied or under applied overhead in

this case is adjusted with all the cost heads that led to the

difference which includes the WIP (Work In Progress) Inventory,

Finished Goods, and Cost of Goods sold. The logic is that the over

applied or under applied overhead are adjusted to all the units of

the organization be it in their WIP stage, FG inventory or are sold to

customers.

When significant over applied or under applied overhead are

adjusted with cost of goods sold, it leads to misappropriated net

income and thus they are evenly distributed to all heads to avoid

this inflation of net income.

In the current situation, I would recommend Voltus Communication

to use the first method where we dispose it off with the cost of

goods sold. This is because the under applied overhead of $33,000

is only 0.9% of total overhead incurred $3,588,000, which makes it

very insignificant and the company can simply dispose it off with the

cost of goods sold for the company.

Answer to part 5

4

Transfer of over applied or under applied overhead to cost of goods

sold nullifies their balances.

This method is recommended for use when the amount of over

applied or under applied overhead is not very significant for the

company. When the over applied or under applied overhead are not

a very high value item, the company can simply adjust it with cost

of goods sold.

2. Dispose it off with all cost heads including WIP inventory,

Finished Goods and Cost of Goods Sold.

In a situation where the over applied or under applied overhead are

of significant value, simply adjusting it with the cost of goods sold is

not the best option. The over applied or under applied overhead in

this case is adjusted with all the cost heads that led to the

difference which includes the WIP (Work In Progress) Inventory,

Finished Goods, and Cost of Goods sold. The logic is that the over

applied or under applied overhead are adjusted to all the units of

the organization be it in their WIP stage, FG inventory or are sold to

customers.

When significant over applied or under applied overhead are

adjusted with cost of goods sold, it leads to misappropriated net

income and thus they are evenly distributed to all heads to avoid

this inflation of net income.

In the current situation, I would recommend Voltus Communication

to use the first method where we dispose it off with the cost of

goods sold. This is because the under applied overhead of $33,000

is only 0.9% of total overhead incurred $3,588,000, which makes it

very insignificant and the company can simply dispose it off with the

cost of goods sold for the company.

Answer to part 5

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

To explore the possibility of using ABC for Voltus Communication,

we will have to first understand what ABC is. The ABC also known as

the Activity Based Costing is a logical approach where the company

allocates the overhead costs to the products of the company on the

basis of the usage of the resources of the company.

Under ABC we start with identification of all the major activities that

the company has and their total costs. These total costs are then

are then allocated to the products based on their usage of the

activities that have been identified earlier (AccountingCoach.com,

2019).

With the use of ABC for allocation of the manufacturing overhead,

Voltus Communication would be able to eliminate the limitation of

job costing system which allocates the overheads based on one

single rate basis the machine hours worked.

Currently Voltus Communication uses a single pre determined

overhead rate based on the total machine hours worked and all the

overheads are applied evenly to all their products. This is not the

right approach as the company currently has various jobs in hand all

of which do not use the same resources. Some jobs are using more

resources as compared to others and thus their allocation of the

overhead should be more than the others. Job costing will never be

able to identify these differences and thus they should opt for ABC,

which will identify these differences in resources used, and provide

better costing leading to better pricing and profitability for the firm.

Recommendation: Voltus communication should opt for Activity

Based Costing as they have different jobs in hand, all of which uses

different resources and thus all of them should have different costs

and prices.

The use of Activity Based coting will eliminate the problem of equal

application of overheads to all jobs by identification of activities, and

5

we will have to first understand what ABC is. The ABC also known as

the Activity Based Costing is a logical approach where the company

allocates the overhead costs to the products of the company on the

basis of the usage of the resources of the company.

Under ABC we start with identification of all the major activities that

the company has and their total costs. These total costs are then

are then allocated to the products based on their usage of the

activities that have been identified earlier (AccountingCoach.com,

2019).

With the use of ABC for allocation of the manufacturing overhead,

Voltus Communication would be able to eliminate the limitation of

job costing system which allocates the overheads based on one

single rate basis the machine hours worked.

Currently Voltus Communication uses a single pre determined

overhead rate based on the total machine hours worked and all the

overheads are applied evenly to all their products. This is not the

right approach as the company currently has various jobs in hand all

of which do not use the same resources. Some jobs are using more

resources as compared to others and thus their allocation of the

overhead should be more than the others. Job costing will never be

able to identify these differences and thus they should opt for ABC,

which will identify these differences in resources used, and provide

better costing leading to better pricing and profitability for the firm.

Recommendation: Voltus communication should opt for Activity

Based Costing as they have different jobs in hand, all of which uses

different resources and thus all of them should have different costs

and prices.

The use of Activity Based coting will eliminate the problem of equal

application of overheads to all jobs by identification of activities, and

5

their usage by each jobs for appropriate allocation and thus correct

pricing.

Answer to part 6

The company had 2 jobs (B 12-008 and K 12-009) in WIP as at 31

May 2019 and worked on all the 5 jobs during June 2019. It is given

that the company was able to complete all the 5 tasks and further

sold off all the jobs except for K 12-009 that was unsold and thus

lying as finished goods inventory for the company.

The balance in the finished goods was the total costs blocked in the

job in terms of its WIP balance as on 31 May 2019 and all the

additions made to it during June 2019

Based on above, the balance in the finished goods account is

computed as below:

Computation of Finished goods Account - K 12 -009

Particular

Amoun

t Amount

Opening WIP (31 May 2019) $1,63,000

Additions made during June 2019:

Direct Material $14,000

Direct Labour $36,000

Manufacturing Overhead (1,000 @

$45) $45,000 $95,000

Finished Goods balance as on 30 June 2019

$2,58,00

0

Thus, Voltus communication had a balance of $258,000 in their

finished goods account as at 30 June 2019 against their unsold

finished inventory of their job No. K 12-009.

Conclusion

Thus we see how job costing leads to incorrect pricing as the single

rate allocates overhead evenly to all jobs of the company. If the

company opts for ABC they will be able to better estimate the costs

6

pricing.

Answer to part 6

The company had 2 jobs (B 12-008 and K 12-009) in WIP as at 31

May 2019 and worked on all the 5 jobs during June 2019. It is given

that the company was able to complete all the 5 tasks and further

sold off all the jobs except for K 12-009 that was unsold and thus

lying as finished goods inventory for the company.

The balance in the finished goods was the total costs blocked in the

job in terms of its WIP balance as on 31 May 2019 and all the

additions made to it during June 2019

Based on above, the balance in the finished goods account is

computed as below:

Computation of Finished goods Account - K 12 -009

Particular

Amoun

t Amount

Opening WIP (31 May 2019) $1,63,000

Additions made during June 2019:

Direct Material $14,000

Direct Labour $36,000

Manufacturing Overhead (1,000 @

$45) $45,000 $95,000

Finished Goods balance as on 30 June 2019

$2,58,00

0

Thus, Voltus communication had a balance of $258,000 in their

finished goods account as at 30 June 2019 against their unsold

finished inventory of their job No. K 12-009.

Conclusion

Thus we see how job costing leads to incorrect pricing as the single

rate allocates overhead evenly to all jobs of the company. If the

company opts for ABC they will be able to better estimate the costs

6

of the goods and thus will have better control over prices and

profitability of the company.

References

AccountingCoach.com. (2019). Activity Based Costing | Explanation |

AccountingCoach. Retrieved from

https://www.accountingcoach.com/activity-based-costing/explanation on

14 Apr. 2019

Bragg, S. (2019). Job costing. [online] AccountingTools. Retrieved from

https://www.accountingtools.com/articles/2017/5/14/job-costing on 14 Apr.

2019

Copeland, R. (2000). Managerial accounting. Houston, TX: Dame.

dummies. (2019). Cost Accounting: The Weighted Average Costing Method

- dummies. Retrieved from

https://www.dummies.com/business/accounting/cost-accounting-the-

weighted-average-costing-method/ on14 Apr. 2019].

Garrison, R., Noreen, E. and Brewer, P. (n.d.). Managerial accounting.

Horngren, C., Datar, S., Rajan, M., Maguire, W. and Tan, R. (n.d.). Cost

accounting.

Jiambalvo, J. (n.d.). Managerial accounting.

Lucey, T. (2009). Costing. Australia: South-Western Cengage Learning.

7

profitability of the company.

References

AccountingCoach.com. (2019). Activity Based Costing | Explanation |

AccountingCoach. Retrieved from

https://www.accountingcoach.com/activity-based-costing/explanation on

14 Apr. 2019

Bragg, S. (2019). Job costing. [online] AccountingTools. Retrieved from

https://www.accountingtools.com/articles/2017/5/14/job-costing on 14 Apr.

2019

Copeland, R. (2000). Managerial accounting. Houston, TX: Dame.

dummies. (2019). Cost Accounting: The Weighted Average Costing Method

- dummies. Retrieved from

https://www.dummies.com/business/accounting/cost-accounting-the-

weighted-average-costing-method/ on14 Apr. 2019].

Garrison, R., Noreen, E. and Brewer, P. (n.d.). Managerial accounting.

Horngren, C., Datar, S., Rajan, M., Maguire, W. and Tan, R. (n.d.). Cost

accounting.

Jiambalvo, J. (n.d.). Managerial accounting.

Lucey, T. (2009). Costing. Australia: South-Western Cengage Learning.

7

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.