Management Accounting: Overhead Allocation and Cost Computation

Added on 2022-11-19

12 Pages2903 Words500 Views

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

1MANAGEMENT ACCOUNTING

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................4

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................7

Answer to question 6:.................................................................................................................8

References and bibliography:...................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................4

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................7

Answer to question 6:.................................................................................................................8

References and bibliography:...................................................................................................10

2MANAGEMENT ACCOUNTING

Answer to question 1:

Production of any goods or rendering of any service require certain inputs. All the

costs related to the prime input factors constitute the prime cost of the product or services. In

other words, all the direct expenses are the part of prime costs and all the indirect expenses

are collectively called overhead. Therefore, indirect materials used in production, indirect

labour incurred in relation to the production or manufacturing of goods and any other indirect

expenses are collectively called manufacturing overhead. In the same way, indirect materials

indirect labour and indirect expenses related to selling and distribution of goods are known as

selling and distribution overhead. Similarly all the period expenses related to the office and

administration are known as office and administrative overhead (Anderson and Dekker

2014).

Overhead expenses are those expenses which cannot be directly linked with the

production unit and hence, it needs to be allocated or absorbed to the production unit using

certain appropriate basis. The system of allocation of overhead to the production unit is called

the overhead allocation or overhead absorption. There are various methods of overhead

allocation or overhead absorption. The traditional method of overhead allocation uses a single

base for allocation of all the overhead expenses and that is why it is called the volume based

overhead allocation system (Kaplan and Atkinson 2015). There are various disadvantages of

overhead allocation using a single base which makes it an unscientific and inappropriate

method of overhead allocation in the modern revolutionary business era. In this system, a

predetermined overhead rate is computed based on the estimated total overhead and total use

of a single activity. Using that rate all the overhead is allocated to the production units

(Kamal 2015).

Answer to question 1:

Production of any goods or rendering of any service require certain inputs. All the

costs related to the prime input factors constitute the prime cost of the product or services. In

other words, all the direct expenses are the part of prime costs and all the indirect expenses

are collectively called overhead. Therefore, indirect materials used in production, indirect

labour incurred in relation to the production or manufacturing of goods and any other indirect

expenses are collectively called manufacturing overhead. In the same way, indirect materials

indirect labour and indirect expenses related to selling and distribution of goods are known as

selling and distribution overhead. Similarly all the period expenses related to the office and

administration are known as office and administrative overhead (Anderson and Dekker

2014).

Overhead expenses are those expenses which cannot be directly linked with the

production unit and hence, it needs to be allocated or absorbed to the production unit using

certain appropriate basis. The system of allocation of overhead to the production unit is called

the overhead allocation or overhead absorption. There are various methods of overhead

allocation or overhead absorption. The traditional method of overhead allocation uses a single

base for allocation of all the overhead expenses and that is why it is called the volume based

overhead allocation system (Kaplan and Atkinson 2015). There are various disadvantages of

overhead allocation using a single base which makes it an unscientific and inappropriate

method of overhead allocation in the modern revolutionary business era. In this system, a

predetermined overhead rate is computed based on the estimated total overhead and total use

of a single activity. Using that rate all the overhead is allocated to the production units

(Kamal 2015).

3MANAGEMENT ACCOUNTING

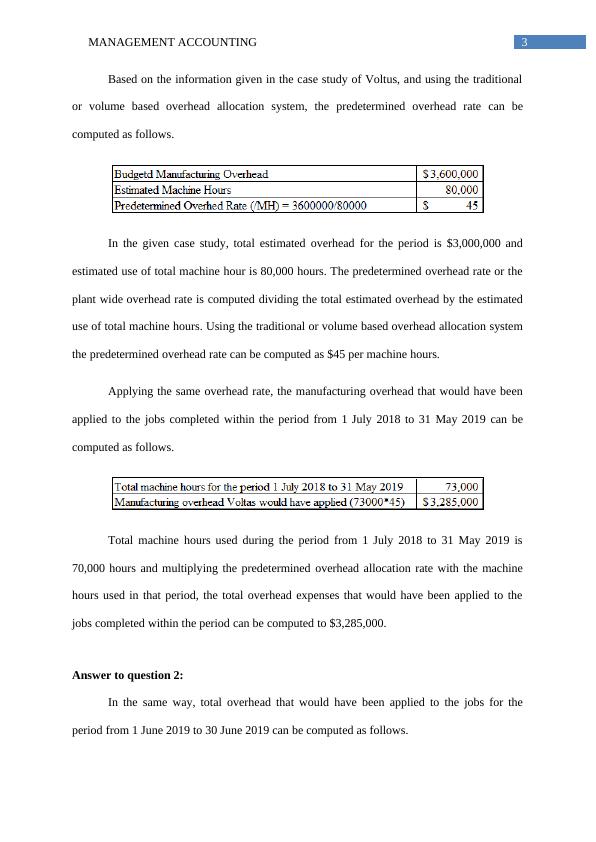

Based on the information given in the case study of Voltus, and using the traditional

or volume based overhead allocation system, the predetermined overhead rate can be

computed as follows.

In the given case study, total estimated overhead for the period is $3,000,000 and

estimated use of total machine hour is 80,000 hours. The predetermined overhead rate or the

plant wide overhead rate is computed dividing the total estimated overhead by the estimated

use of total machine hours. Using the traditional or volume based overhead allocation system

the predetermined overhead rate can be computed as $45 per machine hours.

Applying the same overhead rate, the manufacturing overhead that would have been

applied to the jobs completed within the period from 1 July 2018 to 31 May 2019 can be

computed as follows.

Total machine hours used during the period from 1 July 2018 to 31 May 2019 is

70,000 hours and multiplying the predetermined overhead allocation rate with the machine

hours used in that period, the total overhead expenses that would have been applied to the

jobs completed within the period can be computed to $3,285,000.

Answer to question 2:

In the same way, total overhead that would have been applied to the jobs for the

period from 1 June 2019 to 30 June 2019 can be computed as follows.

Based on the information given in the case study of Voltus, and using the traditional

or volume based overhead allocation system, the predetermined overhead rate can be

computed as follows.

In the given case study, total estimated overhead for the period is $3,000,000 and

estimated use of total machine hour is 80,000 hours. The predetermined overhead rate or the

plant wide overhead rate is computed dividing the total estimated overhead by the estimated

use of total machine hours. Using the traditional or volume based overhead allocation system

the predetermined overhead rate can be computed as $45 per machine hours.

Applying the same overhead rate, the manufacturing overhead that would have been

applied to the jobs completed within the period from 1 July 2018 to 31 May 2019 can be

computed as follows.

Total machine hours used during the period from 1 July 2018 to 31 May 2019 is

70,000 hours and multiplying the predetermined overhead allocation rate with the machine

hours used in that period, the total overhead expenses that would have been applied to the

jobs completed within the period can be computed to $3,285,000.

Answer to question 2:

In the same way, total overhead that would have been applied to the jobs for the

period from 1 June 2019 to 30 June 2019 can be computed as follows.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting 2022 Question Answerlg...

|7

|1173

|11

Management Accounting | Assignment -3lg...

|8

|1368

|19

Management Accounting Assesment Reportlg...

|7

|1327

|18

Strategic Management Accountinglg...

|7

|779

|58

Management Accounting- Assignment (Doc)lg...

|8

|2993

|224

ACC200 Activity Based-Costing Method vs Traditional Costinglg...

|7

|1654

|41