Ireland Taxation System

VerifiedAdded on 2023/06/10

|20

|3969

|334

AI Summary

This article discusses tax residency, rental income, and Schedule D Case I Tax Adjusted Profits in Ireland. It covers the tax compliance implications of having an Irish rental source of income and allowable expenses that can be deducted from gross rents. It also explains the impact of tax residency position on income tax and the commencement rules for the first three years. The article includes a calculation of Sean's Schedule D Case I Tax Adjusted Profits and Capital Allowances for 2016 and 2017.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Ireland Taxation System

Contents

Tax Residency Position of Austin...................................................................................................2

Impact of Austin’s Tax Residency Position on his Income Tax.....................................................4

The tax compliance implications of having an Irish rental source of income.................................6

Allowable expenses that can be deducted from gross rents............................................................7

Commencement Rules for first three years.....................................................................................9

Calculation of Sean’s Schedule D Case I Tax Adjusted Profits and Capital Allowances for 2016

and 2017.........................................................................................................................................10

Table 2: Calculation of Sean & Helen's Taxable Income..............................................................12

VAT Treatment..............................................................................................................................13

Two-Thirds Rule, Composite and Multiple Supply......................................................................15

References......................................................................................................................................17

Contents

Tax Residency Position of Austin...................................................................................................2

Impact of Austin’s Tax Residency Position on his Income Tax.....................................................4

The tax compliance implications of having an Irish rental source of income.................................6

Allowable expenses that can be deducted from gross rents............................................................7

Commencement Rules for first three years.....................................................................................9

Calculation of Sean’s Schedule D Case I Tax Adjusted Profits and Capital Allowances for 2016

and 2017.........................................................................................................................................10

Table 2: Calculation of Sean & Helen's Taxable Income..............................................................12

VAT Treatment..............................................................................................................................13

Two-Thirds Rule, Composite and Multiple Supply......................................................................15

References......................................................................................................................................17

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Ireland Taxation System

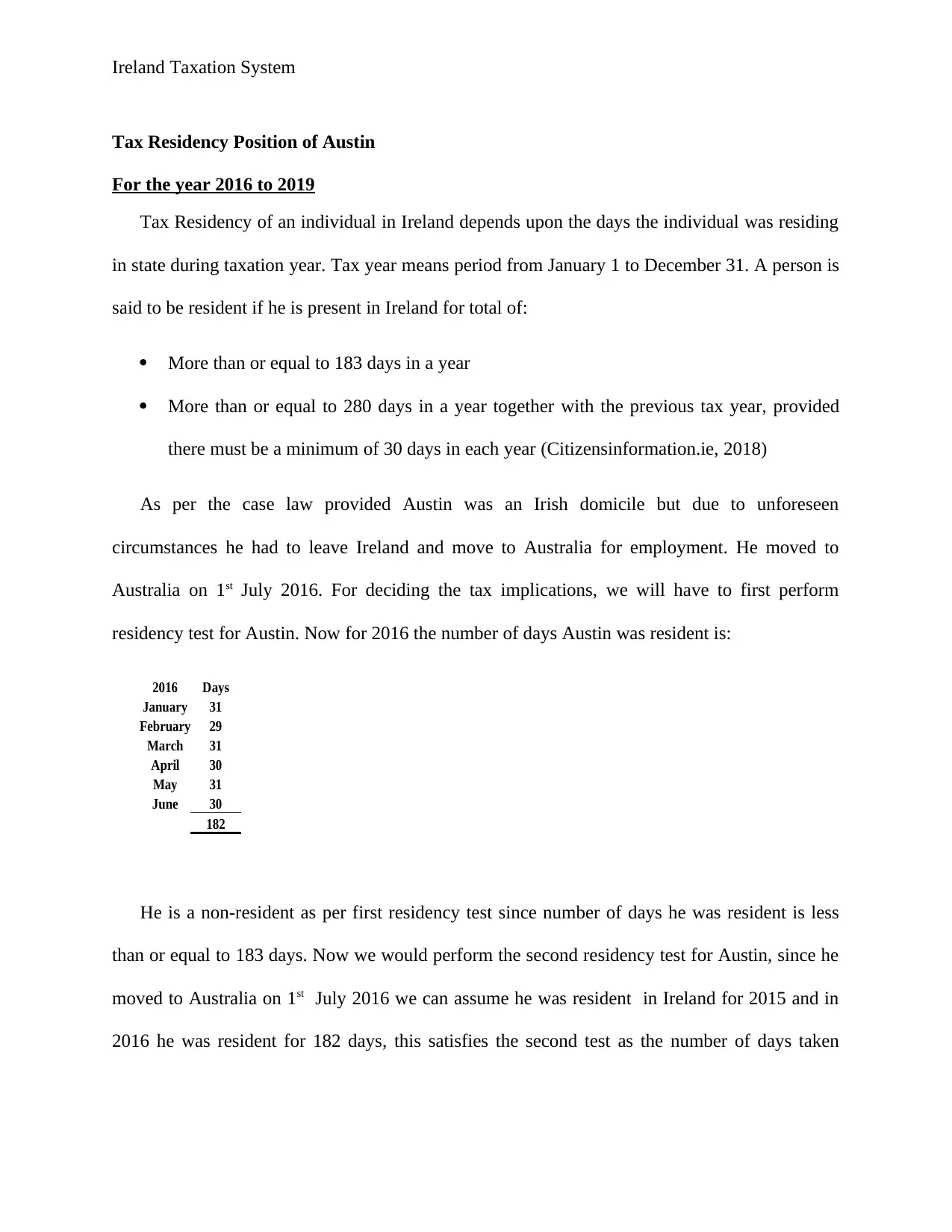

Tax Residency Position of Austin

For the year 2016 to 2019

Tax Residency of an individual in Ireland depends upon the days the individual was residing

in state during taxation year. Tax year means period from January 1 to December 31. A person is

said to be resident if he is present in Ireland for total of:

More than or equal to 183 days in a year

More than or equal to 280 days in a year together with the previous tax year, provided

there must be a minimum of 30 days in each year (Citizensinformation.ie, 2018)

As per the case law provided Austin was an Irish domicile but due to unforeseen

circumstances he had to leave Ireland and move to Australia for employment. He moved to

Australia on 1st July 2016. For deciding the tax implications, we will have to first perform

residency test for Austin. Now for 2016 the number of days Austin was resident is:

2016 Days

January 31

February 29

March 31

April 30

May 31

June 30

182

He is a non-resident as per first residency test since number of days he was resident is less

than or equal to 183 days. Now we would perform the second residency test for Austin, since he

moved to Australia on 1st July 2016 we can assume he was resident in Ireland for 2015 and in

2016 he was resident for 182 days, this satisfies the second test as the number of days taken

Tax Residency Position of Austin

For the year 2016 to 2019

Tax Residency of an individual in Ireland depends upon the days the individual was residing

in state during taxation year. Tax year means period from January 1 to December 31. A person is

said to be resident if he is present in Ireland for total of:

More than or equal to 183 days in a year

More than or equal to 280 days in a year together with the previous tax year, provided

there must be a minimum of 30 days in each year (Citizensinformation.ie, 2018)

As per the case law provided Austin was an Irish domicile but due to unforeseen

circumstances he had to leave Ireland and move to Australia for employment. He moved to

Australia on 1st July 2016. For deciding the tax implications, we will have to first perform

residency test for Austin. Now for 2016 the number of days Austin was resident is:

2016 Days

January 31

February 29

March 31

April 30

May 31

June 30

182

He is a non-resident as per first residency test since number of days he was resident is less

than or equal to 183 days. Now we would perform the second residency test for Austin, since he

moved to Australia on 1st July 2016 we can assume he was resident in Ireland for 2015 and in

2016 he was resident for 182 days, this satisfies the second test as the number of days taken

Ireland Taxation System

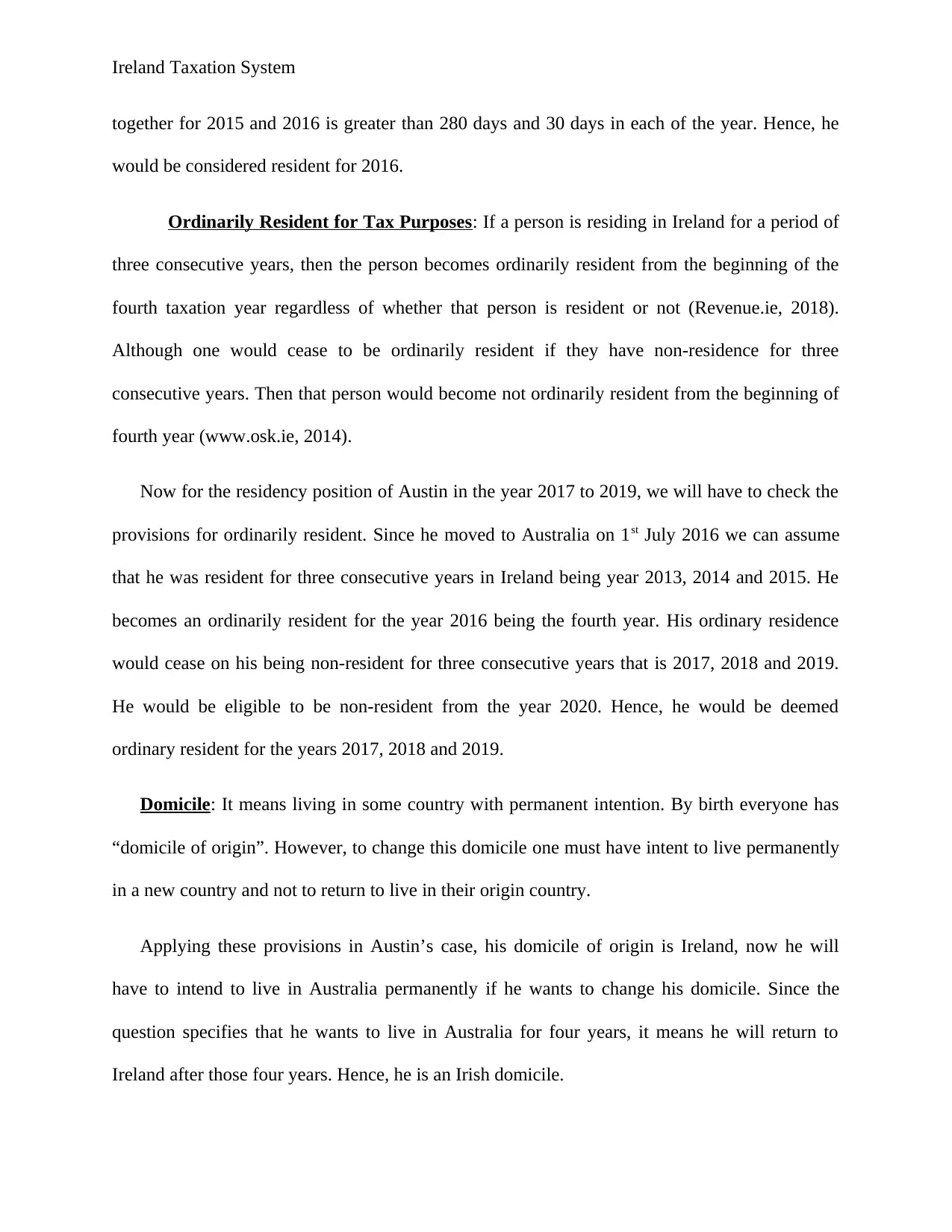

together for 2015 and 2016 is greater than 280 days and 30 days in each of the year. Hence, he

would be considered resident for 2016.

Ordinarily Resident for Tax Purposes: If a person is residing in Ireland for a period of

three consecutive years, then the person becomes ordinarily resident from the beginning of the

fourth taxation year regardless of whether that person is resident or not (Revenue.ie, 2018).

Although one would cease to be ordinarily resident if they have non-residence for three

consecutive years. Then that person would become not ordinarily resident from the beginning of

fourth year (www.osk.ie, 2014).

Now for the residency position of Austin in the year 2017 to 2019, we will have to check the

provisions for ordinarily resident. Since he moved to Australia on 1st July 2016 we can assume

that he was resident for three consecutive years in Ireland being year 2013, 2014 and 2015. He

becomes an ordinarily resident for the year 2016 being the fourth year. His ordinary residence

would cease on his being non-resident for three consecutive years that is 2017, 2018 and 2019.

He would be eligible to be non-resident from the year 2020. Hence, he would be deemed

ordinary resident for the years 2017, 2018 and 2019.

Domicile: It means living in some country with permanent intention. By birth everyone has

“domicile of origin”. However, to change this domicile one must have intent to live permanently

in a new country and not to return to live in their origin country.

Applying these provisions in Austin’s case, his domicile of origin is Ireland, now he will

have to intend to live in Australia permanently if he wants to change his domicile. Since the

question specifies that he wants to live in Australia for four years, it means he will return to

Ireland after those four years. Hence, he is an Irish domicile.

together for 2015 and 2016 is greater than 280 days and 30 days in each of the year. Hence, he

would be considered resident for 2016.

Ordinarily Resident for Tax Purposes: If a person is residing in Ireland for a period of

three consecutive years, then the person becomes ordinarily resident from the beginning of the

fourth taxation year regardless of whether that person is resident or not (Revenue.ie, 2018).

Although one would cease to be ordinarily resident if they have non-residence for three

consecutive years. Then that person would become not ordinarily resident from the beginning of

fourth year (www.osk.ie, 2014).

Now for the residency position of Austin in the year 2017 to 2019, we will have to check the

provisions for ordinarily resident. Since he moved to Australia on 1st July 2016 we can assume

that he was resident for three consecutive years in Ireland being year 2013, 2014 and 2015. He

becomes an ordinarily resident for the year 2016 being the fourth year. His ordinary residence

would cease on his being non-resident for three consecutive years that is 2017, 2018 and 2019.

He would be eligible to be non-resident from the year 2020. Hence, he would be deemed

ordinary resident for the years 2017, 2018 and 2019.

Domicile: It means living in some country with permanent intention. By birth everyone has

“domicile of origin”. However, to change this domicile one must have intent to live permanently

in a new country and not to return to live in their origin country.

Applying these provisions in Austin’s case, his domicile of origin is Ireland, now he will

have to intend to live in Australia permanently if he wants to change his domicile. Since the

question specifies that he wants to live in Australia for four years, it means he will return to

Ireland after those four years. Hence, he is an Irish domicile.

Ireland Taxation System

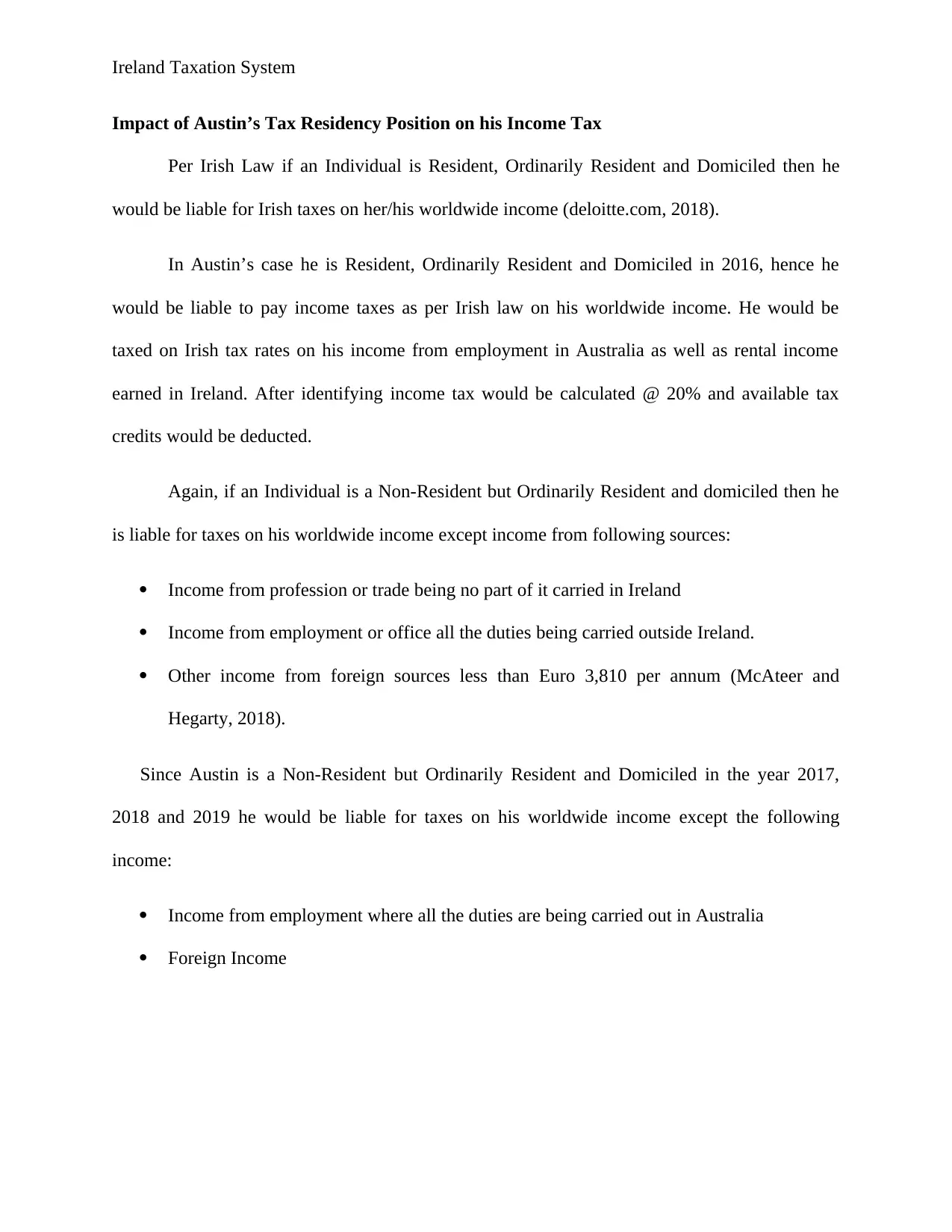

Impact of Austin’s Tax Residency Position on his Income Tax

Per Irish Law if an Individual is Resident, Ordinarily Resident and Domiciled then he

would be liable for Irish taxes on her/his worldwide income (deloitte.com, 2018).

In Austin’s case he is Resident, Ordinarily Resident and Domiciled in 2016, hence he

would be liable to pay income taxes as per Irish law on his worldwide income. He would be

taxed on Irish tax rates on his income from employment in Australia as well as rental income

earned in Ireland. After identifying income tax would be calculated @ 20% and available tax

credits would be deducted.

Again, if an Individual is a Non-Resident but Ordinarily Resident and domiciled then he

is liable for taxes on his worldwide income except income from following sources:

Income from profession or trade being no part of it carried in Ireland

Income from employment or office all the duties being carried outside Ireland.

Other income from foreign sources less than Euro 3,810 per annum (McAteer and

Hegarty, 2018).

Since Austin is a Non-Resident but Ordinarily Resident and Domiciled in the year 2017,

2018 and 2019 he would be liable for taxes on his worldwide income except the following

income:

Income from employment where all the duties are being carried out in Australia

Foreign Income

Impact of Austin’s Tax Residency Position on his Income Tax

Per Irish Law if an Individual is Resident, Ordinarily Resident and Domiciled then he

would be liable for Irish taxes on her/his worldwide income (deloitte.com, 2018).

In Austin’s case he is Resident, Ordinarily Resident and Domiciled in 2016, hence he

would be liable to pay income taxes as per Irish law on his worldwide income. He would be

taxed on Irish tax rates on his income from employment in Australia as well as rental income

earned in Ireland. After identifying income tax would be calculated @ 20% and available tax

credits would be deducted.

Again, if an Individual is a Non-Resident but Ordinarily Resident and domiciled then he

is liable for taxes on his worldwide income except income from following sources:

Income from profession or trade being no part of it carried in Ireland

Income from employment or office all the duties being carried outside Ireland.

Other income from foreign sources less than Euro 3,810 per annum (McAteer and

Hegarty, 2018).

Since Austin is a Non-Resident but Ordinarily Resident and Domiciled in the year 2017,

2018 and 2019 he would be liable for taxes on his worldwide income except the following

income:

Income from employment where all the duties are being carried out in Australia

Foreign Income

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ireland Taxation System

Besides these other levies would be:

Universal Social Charge if gross income would exceed Euro 13,000 p.a (KPMG, 2018).

Local tax on property for residential property owned in Ireland. The tax would be levied

based on the market value of residential property.

Domicile levy if worldwide income is exceeding Euro 1m or property located in Ireland

is worth Euro 5m and more or Irish income tax liability is less than Euro 200,000

(Mulcahygormanmulcahy.com, 2018)

Surcharge of 3% on non-employment income exceeding Euro 100,000

Moreover, if the return is not submitted within the date specified then he would be liable

for additional surcharge amounting to 5% of tax not exceeding Euro 12,695 if submitted

within 2 months of specified date and 10% of tax maximum of Euro 63,485 in either

cases.

Besides these other levies would be:

Universal Social Charge if gross income would exceed Euro 13,000 p.a (KPMG, 2018).

Local tax on property for residential property owned in Ireland. The tax would be levied

based on the market value of residential property.

Domicile levy if worldwide income is exceeding Euro 1m or property located in Ireland

is worth Euro 5m and more or Irish income tax liability is less than Euro 200,000

(Mulcahygormanmulcahy.com, 2018)

Surcharge of 3% on non-employment income exceeding Euro 100,000

Moreover, if the return is not submitted within the date specified then he would be liable

for additional surcharge amounting to 5% of tax not exceeding Euro 12,695 if submitted

within 2 months of specified date and 10% of tax maximum of Euro 63,485 in either

cases.

Ireland Taxation System

The tax compliance implications of having an Irish rental source of income

Regardless of Individual’s domicile or residence status rental income received by individual

from property is subject to tax. Taxable income is calculated by reducing the allowable expenses

from the gross rent received. The expenses deductible must:

a. Be of revenue nature.

b. Incurred by taxpayer

c. Meet criteria of expenses incurred in regular trade.

When the landlord becomes a non-resident i.e. leaves Ireland further consequences apply. To

receive the rent amount, he should nominate someone as his agent who will collect the rent on

his behalf and file an annual tax return with the tax authorities. If landlord fails to nominate an

agent then the tenant is obliged to deduct a standard rate (20%) of income tax from the gross

amount of rent payable. At the year-end tenant should provide the landlord with the form R185

filed with the revenue so that landlord can take the credit of tax in his annual tax return.

Where the landlord leaves Ireland, he may not be able to deduct mortgage interest from the gross

rent received. For qualifying interest for tax relief, landlord must demonstrate that the property is

still his main residence. Also, to claim the relief other conditions must be fulfilled and landlord’s

annual tax return must be filed.

Therefore, Austin’s rental income would be chargeable to income tax and will be able to

claim the interest relief only if he nominates an agent or fulfills the other conditions mentioned

above.

The tax compliance implications of having an Irish rental source of income

Regardless of Individual’s domicile or residence status rental income received by individual

from property is subject to tax. Taxable income is calculated by reducing the allowable expenses

from the gross rent received. The expenses deductible must:

a. Be of revenue nature.

b. Incurred by taxpayer

c. Meet criteria of expenses incurred in regular trade.

When the landlord becomes a non-resident i.e. leaves Ireland further consequences apply. To

receive the rent amount, he should nominate someone as his agent who will collect the rent on

his behalf and file an annual tax return with the tax authorities. If landlord fails to nominate an

agent then the tenant is obliged to deduct a standard rate (20%) of income tax from the gross

amount of rent payable. At the year-end tenant should provide the landlord with the form R185

filed with the revenue so that landlord can take the credit of tax in his annual tax return.

Where the landlord leaves Ireland, he may not be able to deduct mortgage interest from the gross

rent received. For qualifying interest for tax relief, landlord must demonstrate that the property is

still his main residence. Also, to claim the relief other conditions must be fulfilled and landlord’s

annual tax return must be filed.

Therefore, Austin’s rental income would be chargeable to income tax and will be able to

claim the interest relief only if he nominates an agent or fulfills the other conditions mentioned

above.

Ireland Taxation System

Allowable expenses that can be deducted from gross rents

As per Irish Tax laws following expenses may be deducted from the gross rent:

1. Rates paid for property to the local authority.

2. Rent paid for property.

3. Public liability and fire insurance premiums.

4. Amounts for maintenance of property.

5. Property fees paid before renting out of property like management, legal, accounting

fees.

6. Cost of goods or services provided to tenant which are not repaid by tenant like

electricity, telephone, water charges.

7. Registration cost with Residential Tenancies Board (RTB).

8. Cost of repairs like repairing of doors, windows etc.

9. Fees paid to letting agents.

10. Expenses incurred before renting of property.

11. Capital Expenditure.

12. Premium paid for mortgage protection.

13. Capital allowance can be claimed on cost of furniture and fixture in the property at

12.5% annually on the costs incurred for 8 years maximum.

Relief for mortgage interest can also be claimed against rental income. Interest from a

mortgage must be used in purchasing, improving or repairing rental property.

Relief for mortgage interest cab be claimed in the following circumstances:

1. Time during which property is rented.

2. Between renting of property provided owner does not live in that property during that

period.

3. If registered with Residential Tenancies Board (RTB).

Allowable expenses that can be deducted from gross rents

As per Irish Tax laws following expenses may be deducted from the gross rent:

1. Rates paid for property to the local authority.

2. Rent paid for property.

3. Public liability and fire insurance premiums.

4. Amounts for maintenance of property.

5. Property fees paid before renting out of property like management, legal, accounting

fees.

6. Cost of goods or services provided to tenant which are not repaid by tenant like

electricity, telephone, water charges.

7. Registration cost with Residential Tenancies Board (RTB).

8. Cost of repairs like repairing of doors, windows etc.

9. Fees paid to letting agents.

10. Expenses incurred before renting of property.

11. Capital Expenditure.

12. Premium paid for mortgage protection.

13. Capital allowance can be claimed on cost of furniture and fixture in the property at

12.5% annually on the costs incurred for 8 years maximum.

Relief for mortgage interest can also be claimed against rental income. Interest from a

mortgage must be used in purchasing, improving or repairing rental property.

Relief for mortgage interest cab be claimed in the following circumstances:

1. Time during which property is rented.

2. Between renting of property provided owner does not live in that property during that

period.

3. If registered with Residential Tenancies Board (RTB).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Ireland Taxation System

Mortgage interest cannot be claimed between the time property is bought till the time

property is first let out.

From January 2018, January 2017 and earlier years 85%, 80% and 75% respectively

deduction can be claimed of mortgage interest paid on rental property. (Revenue.ie, 2018)

Property located in Ireland from which rent is earned is tax chargeable under Case V

Schedule

D. Deduction is available for interest paid and repairs and improvement for property.

Austin can claim the expenses mentioned above against the rental income which will reduce

the amount of tax that he needs to pay. For mortgage interest Austin can claim deduction of 85%

of the amount of mortgage interest paid against rental income from the date he rented his

property to his friend.

Mortgage interest cannot be claimed between the time property is bought till the time

property is first let out.

From January 2018, January 2017 and earlier years 85%, 80% and 75% respectively

deduction can be claimed of mortgage interest paid on rental property. (Revenue.ie, 2018)

Property located in Ireland from which rent is earned is tax chargeable under Case V

Schedule

D. Deduction is available for interest paid and repairs and improvement for property.

Austin can claim the expenses mentioned above against the rental income which will reduce

the amount of tax that he needs to pay. For mortgage interest Austin can claim deduction of 85%

of the amount of mortgage interest paid against rental income from the date he rented his

property to his friend.

Ireland Taxation System

Commencement Rules for first three years

First Year: In case of commencement of profession or trade, assessment for first year is

founded on profit or gains which arise from commencement date to following December 31st.

Second Year: 1. where in second year of tax accounting period of 12 month is ending

being the only ending accounting period for the year, then profits assessable would be 12 months

profits.

2. if in second year of tax there is only one accounting period and that is lesser than 12 months,

profits assessable would be 12 months period that ends in accounting date provided that the date

is minimum 12 months after commencing.

3. if there are more than two or two accounting periods then profits assessable would be 12

months profits ending on latest of those dates

4. in other cases profits for year ending December 31.

Third year: 1. Profits for 12 months accounting period ending in the tax year

Commencement Rules for first three years

First Year: In case of commencement of profession or trade, assessment for first year is

founded on profit or gains which arise from commencement date to following December 31st.

Second Year: 1. where in second year of tax accounting period of 12 month is ending

being the only ending accounting period for the year, then profits assessable would be 12 months

profits.

2. if in second year of tax there is only one accounting period and that is lesser than 12 months,

profits assessable would be 12 months period that ends in accounting date provided that the date

is minimum 12 months after commencing.

3. if there are more than two or two accounting periods then profits assessable would be 12

months profits ending on latest of those dates

4. in other cases profits for year ending December 31.

Third year: 1. Profits for 12 months accounting period ending in the tax year

Ireland Taxation System

Calculation of Sean’s Schedule D Case I Tax Adjusted Profits and Capital Allowances for

2016 and 2017

Business Income is chargeable to tax under heading of Schedule D and Case I charges tax

on profit of a trade. Deduction is allowed for legitimate business expenditures being:

Trademark

Knowhow

Expenses of Pre-Trading

Pre-Commencement cost of training staff

Establishing cost of approved employee share options scheme

Double deduction for wages that are paid to previously unemployed person

Deduction is not allowed for following:

Private and Capital Expenses

Entertainment Expenses

Calculation of Sean’s Schedule D Case I Tax Adjusted Profits and Capital Allowances for

2016 and 2017

Business Income is chargeable to tax under heading of Schedule D and Case I charges tax

on profit of a trade. Deduction is allowed for legitimate business expenditures being:

Trademark

Knowhow

Expenses of Pre-Trading

Pre-Commencement cost of training staff

Establishing cost of approved employee share options scheme

Double deduction for wages that are paid to previously unemployed person

Deduction is not allowed for following:

Private and Capital Expenses

Entertainment Expenses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ireland Taxation System

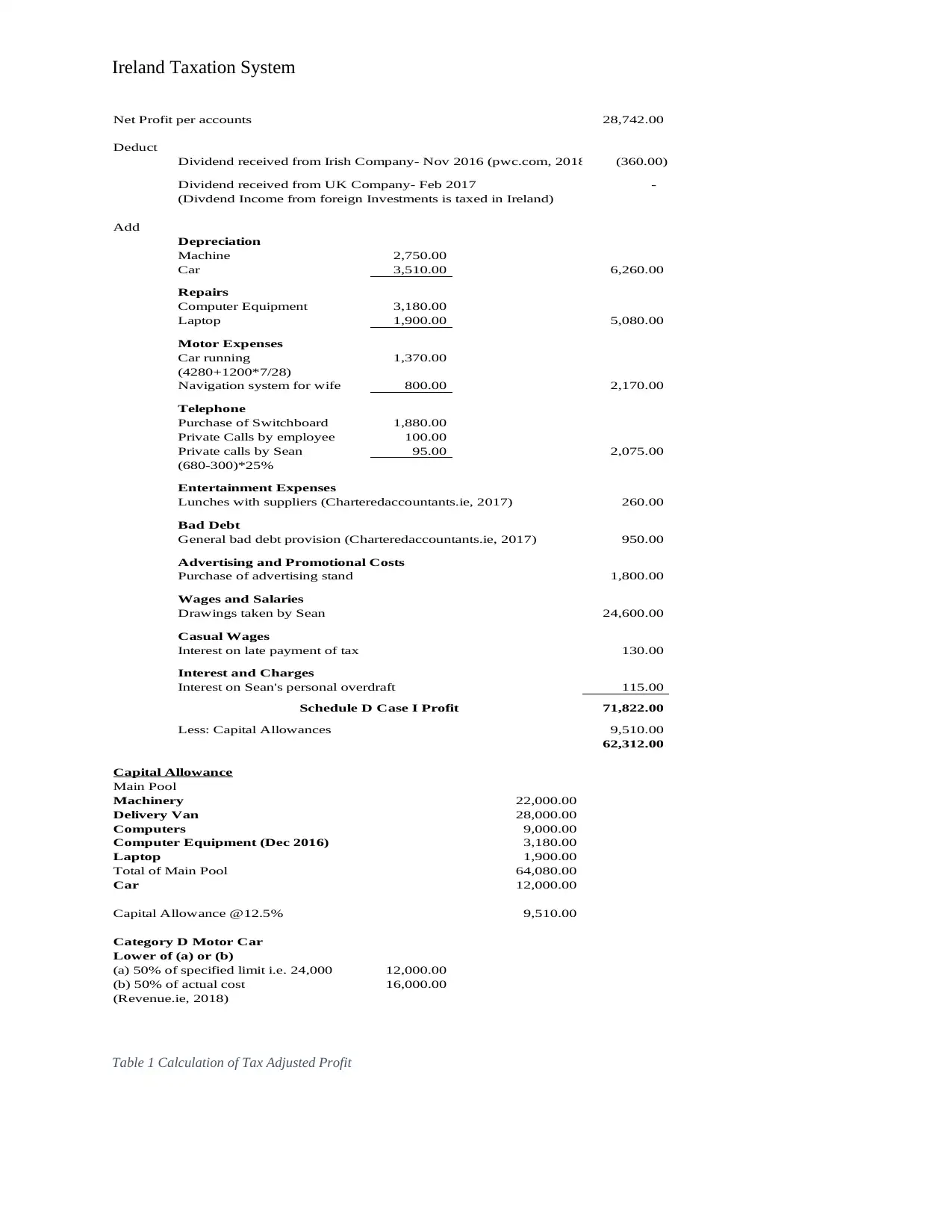

Net Profit per accounts 28,742.00

Deduct

Dividend received from Irish Company- Nov 2016 (pwc.com, 2018 (360.00)

Dividend received from UK Company- Feb 2017 -

(Divdend Income from foreign Investments is taxed in Ireland)

Add

Depreciation

Machine 2,750.00

Car 3,510.00 6,260.00

Repairs

Computer Equipment 3,180.00

Laptop 1,900.00 5,080.00

Motor Expenses

Car running 1,370.00

(4280+1200*7/28)

Navigation system for wife 800.00 2,170.00

Telephone

Purchase of Switchboard 1,880.00

Private Calls by employee 100.00

Private calls by Sean 95.00 2,075.00

(680-300)*25%

Entertainment Expenses

Lunches with suppliers (Charteredaccountants.ie, 2017) 260.00

Bad Debt

General bad debt provision (Charteredaccountants.ie, 2017) 950.00

Advertising and Promotional Costs

Purchase of advertising stand 1,800.00

Wages and Salaries

Drawings taken by Sean 24,600.00

Casual Wages

Interest on late payment of tax 130.00

Interest and Charges

Interest on Sean's personal overdraft 115.00

Schedule D Case I Profit 71,822.00

Less: Capital Allowances 9,510.00

62,312.00

Capital Allowance

Main Pool

Machinery 22,000.00

Delivery Van 28,000.00

Computers 9,000.00

Computer Equipment (Dec 2016) 3,180.00

Laptop 1,900.00

Total of Main Pool 64,080.00

Car 12,000.00

Capital Allowance @12.5% 9,510.00

Category D Motor Car

Lower of (a) or (b)

(a) 50% of specified limit i.e. 24,000 12,000.00

(b) 50% of actual cost 16,000.00

(Revenue.ie, 2018)

Table 1 Calculation of Tax Adjusted Profit

Net Profit per accounts 28,742.00

Deduct

Dividend received from Irish Company- Nov 2016 (pwc.com, 2018 (360.00)

Dividend received from UK Company- Feb 2017 -

(Divdend Income from foreign Investments is taxed in Ireland)

Add

Depreciation

Machine 2,750.00

Car 3,510.00 6,260.00

Repairs

Computer Equipment 3,180.00

Laptop 1,900.00 5,080.00

Motor Expenses

Car running 1,370.00

(4280+1200*7/28)

Navigation system for wife 800.00 2,170.00

Telephone

Purchase of Switchboard 1,880.00

Private Calls by employee 100.00

Private calls by Sean 95.00 2,075.00

(680-300)*25%

Entertainment Expenses

Lunches with suppliers (Charteredaccountants.ie, 2017) 260.00

Bad Debt

General bad debt provision (Charteredaccountants.ie, 2017) 950.00

Advertising and Promotional Costs

Purchase of advertising stand 1,800.00

Wages and Salaries

Drawings taken by Sean 24,600.00

Casual Wages

Interest on late payment of tax 130.00

Interest and Charges

Interest on Sean's personal overdraft 115.00

Schedule D Case I Profit 71,822.00

Less: Capital Allowances 9,510.00

62,312.00

Capital Allowance

Main Pool

Machinery 22,000.00

Delivery Van 28,000.00

Computers 9,000.00

Computer Equipment (Dec 2016) 3,180.00

Laptop 1,900.00

Total of Main Pool 64,080.00

Car 12,000.00

Capital Allowance @12.5% 9,510.00

Category D Motor Car

Lower of (a) or (b)

(a) 50% of specified limit i.e. 24,000 12,000.00

(b) 50% of actual cost 16,000.00

(Revenue.ie, 2018)

Table 1 Calculation of Tax Adjusted Profit

Ireland Taxation System

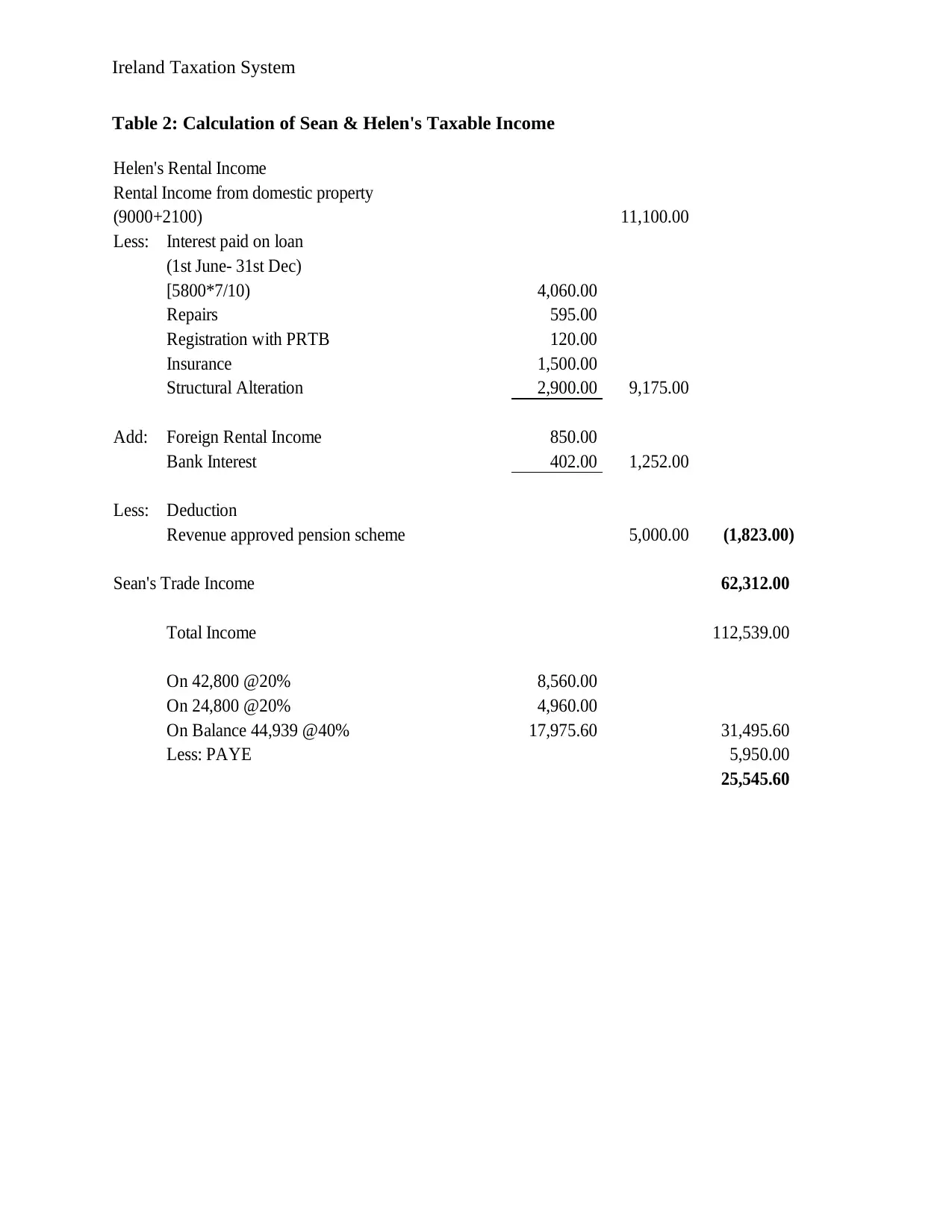

Table 2: Calculation of Sean & Helen's Taxable Income

Helen's Rental Income

Rental Income from domestic property

(9000+2100) 11,100.00

Less: Interest paid on loan

(1st June- 31st Dec)

[5800*7/10) 4,060.00

Repairs 595.00

Registration with PRTB 120.00

Insurance 1,500.00

Structural Alteration 2,900.00 9,175.00

Add: Foreign Rental Income 850.00

Bank Interest 402.00 1,252.00

Less: Deduction

Revenue approved pension scheme 5,000.00 (1,823.00)

Sean's Trade Income 62,312.00

Total Income 112,539.00

On 42,800 @20% 8,560.00

On 24,800 @20% 4,960.00

On Balance 44,939 @40% 17,975.60 31,495.60

Less: PAYE 5,950.00

25,545.60

Table 2: Calculation of Sean & Helen's Taxable Income

Helen's Rental Income

Rental Income from domestic property

(9000+2100) 11,100.00

Less: Interest paid on loan

(1st June- 31st Dec)

[5800*7/10) 4,060.00

Repairs 595.00

Registration with PRTB 120.00

Insurance 1,500.00

Structural Alteration 2,900.00 9,175.00

Add: Foreign Rental Income 850.00

Bank Interest 402.00 1,252.00

Less: Deduction

Revenue approved pension scheme 5,000.00 (1,823.00)

Sean's Trade Income 62,312.00

Total Income 112,539.00

On 42,800 @20% 8,560.00

On 24,800 @20% 4,960.00

On Balance 44,939 @40% 17,975.60 31,495.60

Less: PAYE 5,950.00

25,545.60

Ireland Taxation System

VAT Treatment

An indirect tax named, Value Added Tax(VAT) is levied on the sale/supply of all

services and goods with some exceptions in Ireland by any accountable person.

VAT standard rate is 23% which is applied to Business to Customer(B2C) transactions.

However, there are certain services and good on which reduced rates of 13.5%, 9% and 4.8% is

applied. For fuel (heating oil, gas, coal), building and related services, electricity etc. rate of

13.5% is applied. Rate of 9% is applied to tourism related services and goods (like hotel

accommodation, catering services etc.), hairdressing, sporting facilities and some printed

matters, while the rate of 4.8% is applied to supplies of horses, greyhound and livestock used for

agriculture production.

VAT rates mentioned above only apply if goods are sold within the country. Specific

rules apply if products or services are bought from other countries. These rules also apply if

products are sold to other nations (Tobin and Walsh, 2013). If goods are sold to a business within

the EU, then VAT is not charged if the customer provides a valid VAT number. However, if the

customer does not have a valid VAT number, then VAT should be deducted at the standard rate

that is applicable in Ireland.

On the other hand, if goods are sold to consumers of another country, then the business is

required to register for VAT in that country. After registration for VAT, the business shall charge

VAT at the rate applicable to that country. The company is not required to register for VAT if

sales are below the limit set by that country. The two EU countries selected are Italy and

Germany. The limit set for Italy is €35,000, and for Germany, the limit is €100,000.

VAT Treatment

An indirect tax named, Value Added Tax(VAT) is levied on the sale/supply of all

services and goods with some exceptions in Ireland by any accountable person.

VAT standard rate is 23% which is applied to Business to Customer(B2C) transactions.

However, there are certain services and good on which reduced rates of 13.5%, 9% and 4.8% is

applied. For fuel (heating oil, gas, coal), building and related services, electricity etc. rate of

13.5% is applied. Rate of 9% is applied to tourism related services and goods (like hotel

accommodation, catering services etc.), hairdressing, sporting facilities and some printed

matters, while the rate of 4.8% is applied to supplies of horses, greyhound and livestock used for

agriculture production.

VAT rates mentioned above only apply if goods are sold within the country. Specific

rules apply if products or services are bought from other countries. These rules also apply if

products are sold to other nations (Tobin and Walsh, 2013). If goods are sold to a business within

the EU, then VAT is not charged if the customer provides a valid VAT number. However, if the

customer does not have a valid VAT number, then VAT should be deducted at the standard rate

that is applicable in Ireland.

On the other hand, if goods are sold to consumers of another country, then the business is

required to register for VAT in that country. After registration for VAT, the business shall charge

VAT at the rate applicable to that country. The company is not required to register for VAT if

sales are below the limit set by that country. The two EU countries selected are Italy and

Germany. The limit set for Italy is €35,000, and for Germany, the limit is €100,000.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Ireland Taxation System

VAT does not apply to exempted as well as zero rated supply of services and goods. The

major exempted items include medical as well as its related services, insurance including

reinsurance and financial service provisions. Zero rated services and goods include supply of

children’s clothing, medical appliances and equipment, food items, goods for exportation and

oral medicines.

All taxable businesses can claim the deduction of VAT paid on the purchases of goods or

services from the VAT collected on sales and the net amount of tax payable or refundable is

settled with the tax authorities of Ireland bimonthly (Www2.deloitte.com, 2018).

The invoice of VAT must show the following:

Date of issue

Unique sequence number

Supplier and customer’s full name and their address

Quantity

Vat exclusive price

Discounts

VAT number in cases of interstate supply and reverse charge

VAT does not apply to exempted as well as zero rated supply of services and goods. The

major exempted items include medical as well as its related services, insurance including

reinsurance and financial service provisions. Zero rated services and goods include supply of

children’s clothing, medical appliances and equipment, food items, goods for exportation and

oral medicines.

All taxable businesses can claim the deduction of VAT paid on the purchases of goods or

services from the VAT collected on sales and the net amount of tax payable or refundable is

settled with the tax authorities of Ireland bimonthly (Www2.deloitte.com, 2018).

The invoice of VAT must show the following:

Date of issue

Unique sequence number

Supplier and customer’s full name and their address

Quantity

Vat exclusive price

Discounts

VAT number in cases of interstate supply and reverse charge

Ireland Taxation System

Two-Thirds Rule, Composite and Multiple Supply

Two-Thirds Rule

If a service is supplied and the movable goods value exceeds total contract price’s two-

third, transaction would be treated supply of goods and not supply of services. The rule would be

calculated on VAT- exclusive basis. For example: Some property developer enters into contract

with plumber for supplying and laying pipes for number of houses to be built by him. The price

quoted by plumber is Euro 225,000 excluding VAT. Cost to the plumber for the pipes and fitting

is Euro 148,000 excluding VAT. Labor is priced at Euro 77,000. Since cost of material is not

exceeding Euro 150,000 i.e. 2/3 of Euro 225,000, the rate applying to service @ 13.5% would be

applicable for the whole supply by the plumber (Cpaireland.ie, 2018).

Composite Supply

Composite Supply involves more than two supplies of services or goods that having

conjunction among them and one of them being principal supply. It is charged to VAT at that

rate which is applicable to principal element (Moore, 2018). For example: Supply of instruction

booklet (0% VAT) with mobile phone (standard VAT rate). The booklet is for phone’s better

enjoyment and thus ancillary to the same. Thus, the rate applicable to the principal supply being

mobile phone would be applicable to the instruction booklet regardless of supply consideration

being allocated by supplier.

Two-Thirds Rule, Composite and Multiple Supply

Two-Thirds Rule

If a service is supplied and the movable goods value exceeds total contract price’s two-

third, transaction would be treated supply of goods and not supply of services. The rule would be

calculated on VAT- exclusive basis. For example: Some property developer enters into contract

with plumber for supplying and laying pipes for number of houses to be built by him. The price

quoted by plumber is Euro 225,000 excluding VAT. Cost to the plumber for the pipes and fitting

is Euro 148,000 excluding VAT. Labor is priced at Euro 77,000. Since cost of material is not

exceeding Euro 150,000 i.e. 2/3 of Euro 225,000, the rate applying to service @ 13.5% would be

applicable for the whole supply by the plumber (Cpaireland.ie, 2018).

Composite Supply

Composite Supply involves more than two supplies of services or goods that having

conjunction among them and one of them being principal supply. It is charged to VAT at that

rate which is applicable to principal element (Moore, 2018). For example: Supply of instruction

booklet (0% VAT) with mobile phone (standard VAT rate). The booklet is for phone’s better

enjoyment and thus ancillary to the same. Thus, the rate applicable to the principal supply being

mobile phone would be applicable to the instruction booklet regardless of supply consideration

being allocated by supplier.

Ireland Taxation System

Multiple Supply

Defined as two or more than two supplies in conjunction to customer for total

consideration that covers all supply economically and physically dissociable from one another.

Each of the supplies are viewed as individual supplies and treated exempt/taxable (Moore, 2018).

For example: Repairing service of car is provided with fitting tyres at single consideration. Both

supplies are economically and physically dissociable and consideration needs to be allocated to

tax service at reduced rate and tyres at standard rate (revenue.ie, 2018).

Multiple Supply

Defined as two or more than two supplies in conjunction to customer for total

consideration that covers all supply economically and physically dissociable from one another.

Each of the supplies are viewed as individual supplies and treated exempt/taxable (Moore, 2018).

For example: Repairing service of car is provided with fitting tyres at single consideration. Both

supplies are economically and physically dissociable and consideration needs to be allocated to

tax service at reduced rate and tyres at standard rate (revenue.ie, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ireland Taxation System

References

Citizensinformation.ie (2018). Tax residence and domicile in Ireland. [online]

Citizensinformation.ie. Available at:

http://www.citizensinformation.ie/en/money_and_tax/tax/moving_country_and_taxation/

tax_residence_and_domicile_in_ireland.html [Accessed 19 Jul. 2018].

Charteredaccountants.ie (2017). No 39 of 1997, Schedule 17A, Revenue Note for Guidance.

[online] Charteredaccountants.ie. Available at:

https://www.charteredaccountants.ie/taxsource/1997/en/act/pub/0039/nfg/sched17A-nfg.html

[Accessed 21 Jul. 2018].

Charteredaccountants.ie (2017). No 39 of 1997, Section 840, Revenue Note for Guidance.

[online] Charteredaccountants.ie. Available at:

https://www.charteredaccountants.ie/taxsource/1997/en/act/pub/0039/nfg/sec0840-nfg.html

[Accessed 21 Jul. 2018].

Cpaireland.ie (2018). Taxation. [online] Cpaireland.ie. Available at:

http://www.cpaireland.ie/docs/default-source/Students/april-2015-suggested-solutions/f2---tax-

april-2015.pdf?sfvrsn=2 [Accessed 20 Jul. 2018].

References

Citizensinformation.ie (2018). Tax residence and domicile in Ireland. [online]

Citizensinformation.ie. Available at:

http://www.citizensinformation.ie/en/money_and_tax/tax/moving_country_and_taxation/

tax_residence_and_domicile_in_ireland.html [Accessed 19 Jul. 2018].

Charteredaccountants.ie (2017). No 39 of 1997, Schedule 17A, Revenue Note for Guidance.

[online] Charteredaccountants.ie. Available at:

https://www.charteredaccountants.ie/taxsource/1997/en/act/pub/0039/nfg/sched17A-nfg.html

[Accessed 21 Jul. 2018].

Charteredaccountants.ie (2017). No 39 of 1997, Section 840, Revenue Note for Guidance.

[online] Charteredaccountants.ie. Available at:

https://www.charteredaccountants.ie/taxsource/1997/en/act/pub/0039/nfg/sec0840-nfg.html

[Accessed 21 Jul. 2018].

Cpaireland.ie (2018). Taxation. [online] Cpaireland.ie. Available at:

http://www.cpaireland.ie/docs/default-source/Students/april-2015-suggested-solutions/f2---tax-

april-2015.pdf?sfvrsn=2 [Accessed 20 Jul. 2018].

Ireland Taxation System

deloitte.com (2018). Moving abroad Irish Tax guide. [ebook] Deloitte. Available at:

https://www2.deloitte.com/content/dam/Deloitte/ie/Documents/Tax/ie-tax-ges-moving-abroad-

guide.pdf [Accessed 20 Jul. 2018].

KPMG (2018). Ireland - Income Tax. [online] kpmg.com. Available at:

https://home.kpmg.com/xx/en/home/insights/2011/12/ireland-income-tax.html [Accessed 20 Jul.

2018].

McAteer, C. and Hegarty, C. (2018). Residency and tax exposure - An individual and corporate

tax update. [online] Cpaireland.ie. Available at:

http://www.cpaireland.ie/docs/default-source/Students/exam-related-articles-2014/cpa-p2-

advanced-taxation-examiner-article---double-taxation.pdf?sfvrsn=2 [Accessed 20 Jul. 2018].

Mulcahygormanmulcahy.com (2018). Income Tax 2017. [online] Mulcahygormanmulcahy.com.

Available at: http://www.mulcahygormanmulcahy.com/wp-content/uploads/2017/08/Income-tax-

2017.pdf [Accessed 20 Jul. 2018].

Maneelymccann.ie (2018). Capital allowances Ireland : Maneely Mc Cann. [online]

Maneelymccann.ie. Available at: https://www.maneelymccann.ie/factsheets/corporate-and-

business-tax/capital-allowances [Accessed 21 Jul. 2018].

deloitte.com (2018). Moving abroad Irish Tax guide. [ebook] Deloitte. Available at:

https://www2.deloitte.com/content/dam/Deloitte/ie/Documents/Tax/ie-tax-ges-moving-abroad-

guide.pdf [Accessed 20 Jul. 2018].

KPMG (2018). Ireland - Income Tax. [online] kpmg.com. Available at:

https://home.kpmg.com/xx/en/home/insights/2011/12/ireland-income-tax.html [Accessed 20 Jul.

2018].

McAteer, C. and Hegarty, C. (2018). Residency and tax exposure - An individual and corporate

tax update. [online] Cpaireland.ie. Available at:

http://www.cpaireland.ie/docs/default-source/Students/exam-related-articles-2014/cpa-p2-

advanced-taxation-examiner-article---double-taxation.pdf?sfvrsn=2 [Accessed 20 Jul. 2018].

Mulcahygormanmulcahy.com (2018). Income Tax 2017. [online] Mulcahygormanmulcahy.com.

Available at: http://www.mulcahygormanmulcahy.com/wp-content/uploads/2017/08/Income-tax-

2017.pdf [Accessed 20 Jul. 2018].

Maneelymccann.ie (2018). Capital allowances Ireland : Maneely Mc Cann. [online]

Maneelymccann.ie. Available at: https://www.maneelymccann.ie/factsheets/corporate-and-

business-tax/capital-allowances [Accessed 21 Jul. 2018].

Ireland Taxation System

Moore, A. (2018). WHAT IS A COMPOSITE SUPPLY AND MULTIPLE SUPPLIES?. [Blog]

alanmoore.ie. Available at: https://www.alanmoore.ie/tax-faqs/vat/composite-supply-multiple-

supplies/ [Accessed 20 Jul. 2018].

pwc.com (2018). Ireland - Individual income determination. [online] Taxsummaries.pwc.com.

Available at: http://taxsummaries.pwc.com/ID/Ireland-Individual-Income-determination

[Accessed 21 Jul. 2018].

Revenue.ie (2018). How to know if you are ordinarily resident for tax purposes. [online]

Revenue.ie. Available at: https://www.revenue.ie/en/jobs-and-pensions/tax-residence/how-to-

know-if-you-are-ordinarily-resident-for-tax-purposes.aspx [Accessed 19 Jul. 2018].

revenue.ie (2018). Mixed Supplies of Goods and Services. Office of the Revenue

Commissioners, p.https://www.revenue.ie/en/tax-professionals/tdm/value-added-tax/part06-

rates-and-exemptions/mixed-supplies-of-goods-and-services/rates-mixed-supplies-of-goods-and-

services.pdf.

Revenue.ie (2018). What expenses are allowed?. [online] Revenue.ie. Available at:

https://www.revenue.ie/en/property/rental-income/irish-rental-income/what-expenses-are-

allowed.aspx [Accessed 20 Jul. 2018].

Moore, A. (2018). WHAT IS A COMPOSITE SUPPLY AND MULTIPLE SUPPLIES?. [Blog]

alanmoore.ie. Available at: https://www.alanmoore.ie/tax-faqs/vat/composite-supply-multiple-

supplies/ [Accessed 20 Jul. 2018].

pwc.com (2018). Ireland - Individual income determination. [online] Taxsummaries.pwc.com.

Available at: http://taxsummaries.pwc.com/ID/Ireland-Individual-Income-determination

[Accessed 21 Jul. 2018].

Revenue.ie (2018). How to know if you are ordinarily resident for tax purposes. [online]

Revenue.ie. Available at: https://www.revenue.ie/en/jobs-and-pensions/tax-residence/how-to-

know-if-you-are-ordinarily-resident-for-tax-purposes.aspx [Accessed 19 Jul. 2018].

revenue.ie (2018). Mixed Supplies of Goods and Services. Office of the Revenue

Commissioners, p.https://www.revenue.ie/en/tax-professionals/tdm/value-added-tax/part06-

rates-and-exemptions/mixed-supplies-of-goods-and-services/rates-mixed-supplies-of-goods-and-

services.pdf.

Revenue.ie (2018). What expenses are allowed?. [online] Revenue.ie. Available at:

https://www.revenue.ie/en/property/rental-income/irish-rental-income/what-expenses-are-

allowed.aspx [Accessed 20 Jul. 2018].

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Ireland Taxation System

Revenue.ie (2018). [online] Revenue.ie. Available at: https://www.revenue.ie/en/tax-

professionals/tdm/income-tax-capital-gains-tax-corporation-tax/part-11/11-00-01.pdf [Accessed

21 Jul. 2018].

Tobin, G. and Walsh, K., 2013. What makes a country a tax haven? An Assessment of

international standards shows why Ireland is not a tax haven. The Economic and Social Review,

44(3, Autumn), pp.401- 424.

taxworld.ie (2018). Capital allowances - Taxworld Ireland. [online] Taxworld Ireland. Available

at: https://www.taxworld.ie/income-tax/summary/reliefs/capital-allowances/ [Accessed 21 Jul.

2018].

www.osk.ie (2014). GUIDE FOR INDIVIDUALS OR EMPLOYEES COMING TO WORK IN

IRELAND. [ebook] Dublin: OSK. Available at:

https://www.osk.ie/site/assets/files/1444/guide_for_individuals_or_employees_coming_to_irelan

djune14.pdf [Accessed 19 Jul. 2018].

Www2.deloitte.com (2018). [online] Www2.deloitte.com. Available at:

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-irelandguide-

2017.pdf [Accessed 21 Jul. 2018].

Revenue.ie (2018). [online] Revenue.ie. Available at: https://www.revenue.ie/en/tax-

professionals/tdm/income-tax-capital-gains-tax-corporation-tax/part-11/11-00-01.pdf [Accessed

21 Jul. 2018].

Tobin, G. and Walsh, K., 2013. What makes a country a tax haven? An Assessment of

international standards shows why Ireland is not a tax haven. The Economic and Social Review,

44(3, Autumn), pp.401- 424.

taxworld.ie (2018). Capital allowances - Taxworld Ireland. [online] Taxworld Ireland. Available

at: https://www.taxworld.ie/income-tax/summary/reliefs/capital-allowances/ [Accessed 21 Jul.

2018].

www.osk.ie (2014). GUIDE FOR INDIVIDUALS OR EMPLOYEES COMING TO WORK IN

IRELAND. [ebook] Dublin: OSK. Available at:

https://www.osk.ie/site/assets/files/1444/guide_for_individuals_or_employees_coming_to_irelan

djune14.pdf [Accessed 19 Jul. 2018].

Www2.deloitte.com (2018). [online] Www2.deloitte.com. Available at:

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-irelandguide-

2017.pdf [Accessed 21 Jul. 2018].

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.