IBA Finance Assignment: Financial Analysis of Fu-Wang Foods Limited

VerifiedAdded on 2021/09/18

|12

|2689

|129

Report

AI Summary

This assignment is a financial analysis report on Fu-Wang Foods Limited, a public limited company in Bangladesh. The report, prepared for an Introduction to Finance course at Jahangirnagar University's IBA, examines the company's financial performance for the 2019-2020 fiscal year. It includes an overview of the company, a detailed financial analysis using various ratios such as current, quick, inventory turnover, and profitability ratios, and a comparative analysis against industry averages. The analysis also incorporates the DuPont analysis to assess return on assets and equity. The report highlights Fu-Wang's financial challenges, including low liquidity, poor asset management, and negative profitability, likely impacted by the COVID-19 pandemic. Finally, the report concludes with recommendations based on the analysis. The report aims to provide insights into the company's financial health and identify areas for improvement.

Jahangirnagar University

Department/Institute: Institute of Business Administration

(IBA)

Second Year First Semester/Honors/Masters Final Examination-2020

Assignment for Final Examination

Course No.# FIN 201

Course Title# Introduction to Finance

Name of the Student: MD. Obaidur Raman Dip

Class Roll No. #

Examination Roll No. #

Registration No. #

Academic Session #

Total number of written pages in the assignment #10 (Excluding

Top Sheet)

Date of Submission: July 18, 2021

Instructions:

1. Don’t copy from other’s assignment. Copying from others will be

punished severely.

1 | P a g e

192470

2018-2019

20193550199

1939

Department/Institute: Institute of Business Administration

(IBA)

Second Year First Semester/Honors/Masters Final Examination-2020

Assignment for Final Examination

Course No.# FIN 201

Course Title# Introduction to Finance

Name of the Student: MD. Obaidur Raman Dip

Class Roll No. #

Examination Roll No. #

Registration No. #

Academic Session #

Total number of written pages in the assignment #10 (Excluding

Top Sheet)

Date of Submission: July 18, 2021

Instructions:

1. Don’t copy from other’s assignment. Copying from others will be

punished severely.

1 | P a g e

192470

2018-2019

20193550199

1939

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. The student must submit the assignment online (Google

classroom/email/google form etc.) as the course-teacher

prescribes.

3. You must use your name# your EXAM ID only for naming your

submitted file.

Financial Analysis on Fu-Wang

Foods Limited

2 | P a g e

classroom/email/google form etc.) as the course-teacher

prescribes.

3. You must use your name# your EXAM ID only for naming your

submitted file.

Financial Analysis on Fu-Wang

Foods Limited

2 | P a g e

Table of Contents

Introduction......................................................................................................................................4

Company Overview.........................................................................................................................4

Financial Analysis...........................................................................................................................5

Analysis of Financial Performance..............................................................................................5

Comparative Ratios (Benchmarking)..........................................................................................8

Summary of Ratio Analysis (The DuPont Analysis)...................................................................9

Recommendations..........................................................................................................................10

Conclusion.....................................................................................................................................10

Index..............................................................................................................................................11

References......................................................................................................................................12

3 | P a g e

Introduction......................................................................................................................................4

Company Overview.........................................................................................................................4

Financial Analysis...........................................................................................................................5

Analysis of Financial Performance..............................................................................................5

Comparative Ratios (Benchmarking)..........................................................................................8

Summary of Ratio Analysis (The DuPont Analysis)...................................................................9

Recommendations..........................................................................................................................10

Conclusion.....................................................................................................................................10

Index..............................................................................................................................................11

References......................................................................................................................................12

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Financial statements provide information about the position of a firm or company at a point in

time and its operations over some past periods. Moreover, the essence of financial statements lies

in the fact that they can help predict a company’s financial position in the future. It also measures

the number of expected dividends and earnings (Besley and Brigham, 2016). Financial

statements are enriched with numbers, and it becomes difficult for the managers to determine

which number gets higher priority from another one. In order to understand whether a particular

number is of much importance, the general approach in financial statement analysis is to

calculate the ratios that demonstrate key underlying constructs. For example, liquidity,

efficiency, profitability, Etc. (Ak et al., 2013).

This formal assessment is aimed to collect financial statements for a specific year from a public

limited manufacturing company listed under DSE or CSE. The report also suggests calculating

the financial ratios for a given specific year. Finally, a comparison will be made between the

calculated ratios and the industry average.

Company Overview

In this formal assessment, Fu-Wang Foods Ltd. has been selected as the desired company to do

the analysis. Fu-Wang Foods Ltd. is a public limited company incorporated with joint-stock

companies. The company is also publicly listed in Dhaka Stock Exchange Ltd and Chittagong

Stock Exchange Ltd. (Fuwangfoodsltd.com, 2021). People of Bangladesh are well aware of Fu-

Wang. Most people from their early childhood were introduced to the “Instant Noodles” from

Fu-Wang. Other products include bread, biscuits, toast biscuits, wafer bar, chocolate, energy

drink, Etc. Fu-Wang has been incorporated in business since 1997 and has an authorized capital

of 1,500 Million (In Taka). There are approximately 1600 employees in the company

(Fuwangfoodsltd.com, 2021).

Limitations of the Study

While preparing the assignment, strict regulations have been maintained to make it flawless. Yet,

there were few limitations including:

4 | P a g e

Financial statements provide information about the position of a firm or company at a point in

time and its operations over some past periods. Moreover, the essence of financial statements lies

in the fact that they can help predict a company’s financial position in the future. It also measures

the number of expected dividends and earnings (Besley and Brigham, 2016). Financial

statements are enriched with numbers, and it becomes difficult for the managers to determine

which number gets higher priority from another one. In order to understand whether a particular

number is of much importance, the general approach in financial statement analysis is to

calculate the ratios that demonstrate key underlying constructs. For example, liquidity,

efficiency, profitability, Etc. (Ak et al., 2013).

This formal assessment is aimed to collect financial statements for a specific year from a public

limited manufacturing company listed under DSE or CSE. The report also suggests calculating

the financial ratios for a given specific year. Finally, a comparison will be made between the

calculated ratios and the industry average.

Company Overview

In this formal assessment, Fu-Wang Foods Ltd. has been selected as the desired company to do

the analysis. Fu-Wang Foods Ltd. is a public limited company incorporated with joint-stock

companies. The company is also publicly listed in Dhaka Stock Exchange Ltd and Chittagong

Stock Exchange Ltd. (Fuwangfoodsltd.com, 2021). People of Bangladesh are well aware of Fu-

Wang. Most people from their early childhood were introduced to the “Instant Noodles” from

Fu-Wang. Other products include bread, biscuits, toast biscuits, wafer bar, chocolate, energy

drink, Etc. Fu-Wang has been incorporated in business since 1997 and has an authorized capital

of 1,500 Million (In Taka). There are approximately 1600 employees in the company

(Fuwangfoodsltd.com, 2021).

Limitations of the Study

While preparing the assignment, strict regulations have been maintained to make it flawless. Yet,

there were few limitations including:

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Lack of few data categories and for that the assignment has avoided few ratios.

2. There was no past data for commenting on the present situation of the company.

3. Lack of past experience.

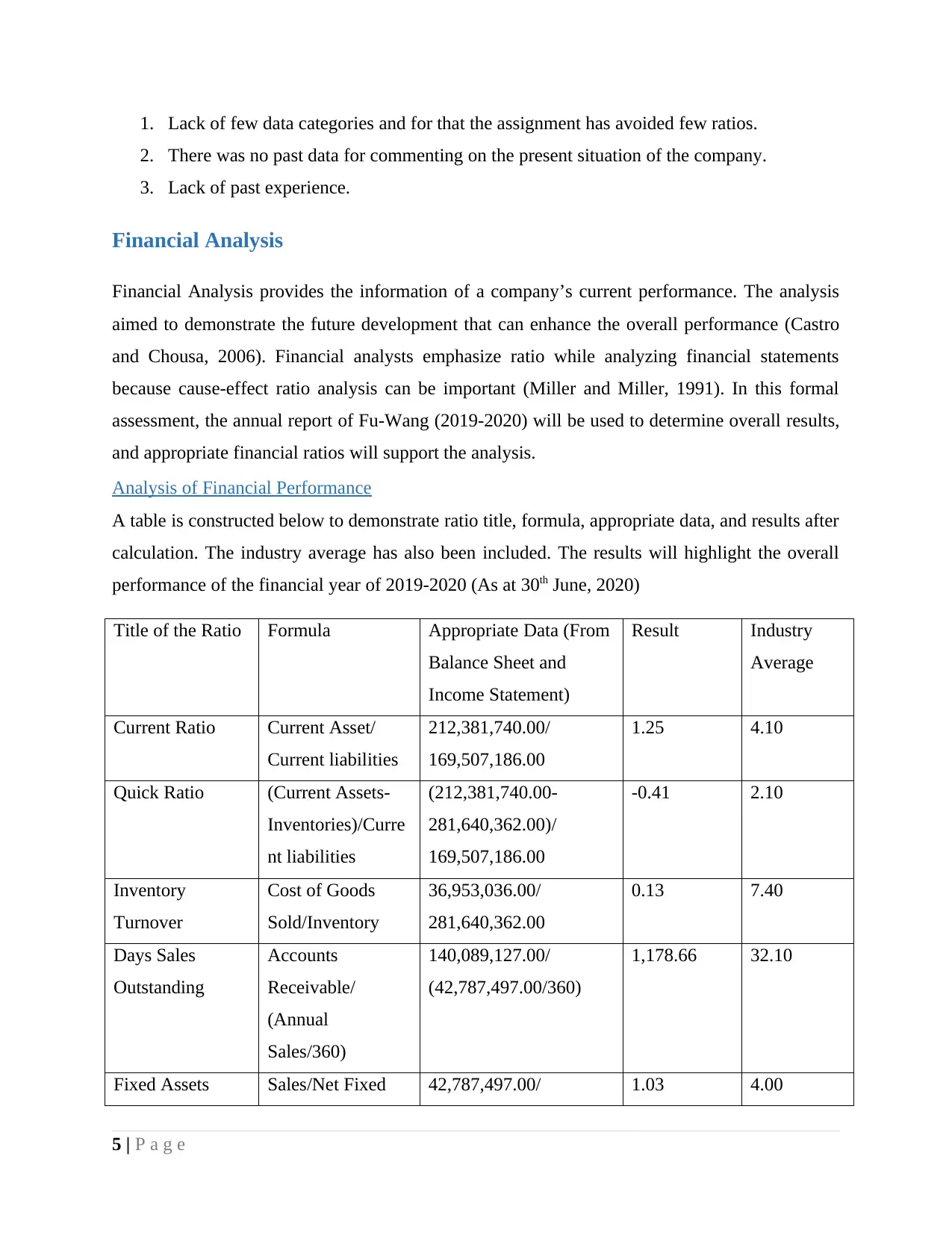

Financial Analysis

Financial Analysis provides the information of a company’s current performance. The analysis

aimed to demonstrate the future development that can enhance the overall performance (Castro

and Chousa, 2006). Financial analysts emphasize ratio while analyzing financial statements

because cause-effect ratio analysis can be important (Miller and Miller, 1991). In this formal

assessment, the annual report of Fu-Wang (2019-2020) will be used to determine overall results,

and appropriate financial ratios will support the analysis.

Analysis of Financial Performance

A table is constructed below to demonstrate ratio title, formula, appropriate data, and results after

calculation. The industry average has also been included. The results will highlight the overall

performance of the financial year of 2019-2020 (As at 30th June, 2020)

Title of the Ratio Formula Appropriate Data (From

Balance Sheet and

Income Statement)

Result Industry

Average

Current Ratio Current Asset/

Current liabilities

212,381,740.00/

169,507,186.00

1.25 4.10

Quick Ratio (Current Assets-

Inventories)/Curre

nt liabilities

(212,381,740.00-

281,640,362.00)/

169,507,186.00

-0.41 2.10

Inventory

Turnover

Cost of Goods

Sold/Inventory

36,953,036.00/

281,640,362.00

0.13 7.40

Days Sales

Outstanding

Accounts

Receivable/

(Annual

Sales/360)

140,089,127.00/

(42,787,497.00/360)

1,178.66 32.10

Fixed Assets Sales/Net Fixed 42,787,497.00/ 1.03 4.00

5 | P a g e

2. There was no past data for commenting on the present situation of the company.

3. Lack of past experience.

Financial Analysis

Financial Analysis provides the information of a company’s current performance. The analysis

aimed to demonstrate the future development that can enhance the overall performance (Castro

and Chousa, 2006). Financial analysts emphasize ratio while analyzing financial statements

because cause-effect ratio analysis can be important (Miller and Miller, 1991). In this formal

assessment, the annual report of Fu-Wang (2019-2020) will be used to determine overall results,

and appropriate financial ratios will support the analysis.

Analysis of Financial Performance

A table is constructed below to demonstrate ratio title, formula, appropriate data, and results after

calculation. The industry average has also been included. The results will highlight the overall

performance of the financial year of 2019-2020 (As at 30th June, 2020)

Title of the Ratio Formula Appropriate Data (From

Balance Sheet and

Income Statement)

Result Industry

Average

Current Ratio Current Asset/

Current liabilities

212,381,740.00/

169,507,186.00

1.25 4.10

Quick Ratio (Current Assets-

Inventories)/Curre

nt liabilities

(212,381,740.00-

281,640,362.00)/

169,507,186.00

-0.41 2.10

Inventory

Turnover

Cost of Goods

Sold/Inventory

36,953,036.00/

281,640,362.00

0.13 7.40

Days Sales

Outstanding

Accounts

Receivable/

(Annual

Sales/360)

140,089,127.00/

(42,787,497.00/360)

1,178.66 32.10

Fixed Assets Sales/Net Fixed 42,787,497.00/ 1.03 4.00

5 | P a g e

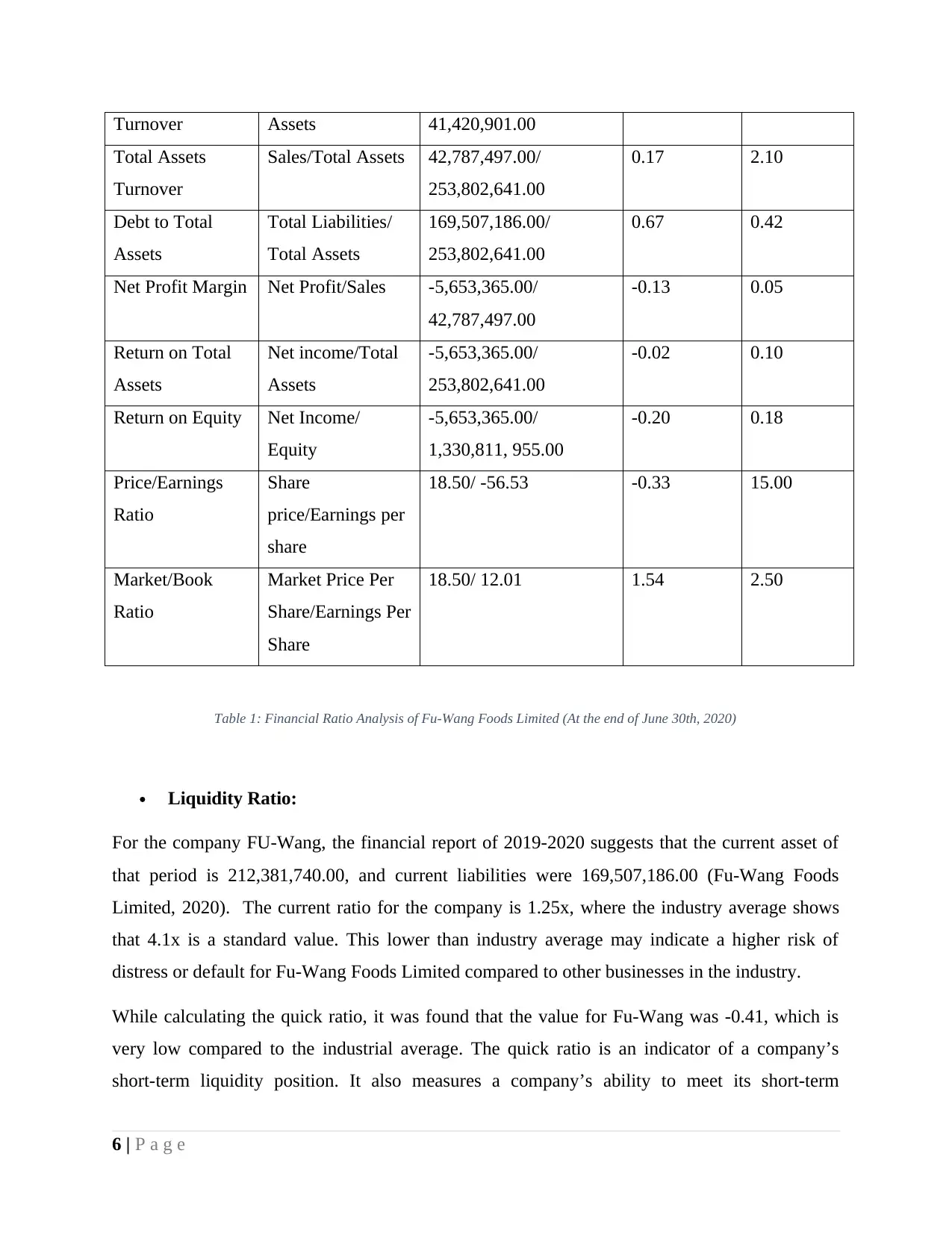

Turnover Assets 41,420,901.00

Total Assets

Turnover

Sales/Total Assets 42,787,497.00/

253,802,641.00

0.17 2.10

Debt to Total

Assets

Total Liabilities/

Total Assets

169,507,186.00/

253,802,641.00

0.67 0.42

Net Profit Margin Net Profit/Sales -5,653,365.00/

42,787,497.00

-0.13 0.05

Return on Total

Assets

Net income/Total

Assets

-5,653,365.00/

253,802,641.00

-0.02 0.10

Return on Equity Net Income/

Equity

-5,653,365.00/

1,330,811, 955.00

-0.20 0.18

Price/Earnings

Ratio

Share

price/Earnings per

share

18.50/ -56.53 -0.33 15.00

Market/Book

Ratio

Market Price Per

Share/Earnings Per

Share

18.50/ 12.01 1.54 2.50

Table 1: Financial Ratio Analysis of Fu-Wang Foods Limited (At the end of June 30th, 2020)

Liquidity Ratio:

For the company FU-Wang, the financial report of 2019-2020 suggests that the current asset of

that period is 212,381,740.00, and current liabilities were 169,507,186.00 (Fu-Wang Foods

Limited, 2020). The current ratio for the company is 1.25x, where the industry average shows

that 4.1x is a standard value. This lower than industry average may indicate a higher risk of

distress or default for Fu-Wang Foods Limited compared to other businesses in the industry.

While calculating the quick ratio, it was found that the value for Fu-Wang was -0.41, which is

very low compared to the industrial average. The quick ratio is an indicator of a company’s

short-term liquidity position. It also measures a company’s ability to meet its short-term

6 | P a g e

Total Assets

Turnover

Sales/Total Assets 42,787,497.00/

253,802,641.00

0.17 2.10

Debt to Total

Assets

Total Liabilities/

Total Assets

169,507,186.00/

253,802,641.00

0.67 0.42

Net Profit Margin Net Profit/Sales -5,653,365.00/

42,787,497.00

-0.13 0.05

Return on Total

Assets

Net income/Total

Assets

-5,653,365.00/

253,802,641.00

-0.02 0.10

Return on Equity Net Income/

Equity

-5,653,365.00/

1,330,811, 955.00

-0.20 0.18

Price/Earnings

Ratio

Share

price/Earnings per

share

18.50/ -56.53 -0.33 15.00

Market/Book

Ratio

Market Price Per

Share/Earnings Per

Share

18.50/ 12.01 1.54 2.50

Table 1: Financial Ratio Analysis of Fu-Wang Foods Limited (At the end of June 30th, 2020)

Liquidity Ratio:

For the company FU-Wang, the financial report of 2019-2020 suggests that the current asset of

that period is 212,381,740.00, and current liabilities were 169,507,186.00 (Fu-Wang Foods

Limited, 2020). The current ratio for the company is 1.25x, where the industry average shows

that 4.1x is a standard value. This lower than industry average may indicate a higher risk of

distress or default for Fu-Wang Foods Limited compared to other businesses in the industry.

While calculating the quick ratio, it was found that the value for Fu-Wang was -0.41, which is

very low compared to the industrial average. The quick ratio is an indicator of a company’s

short-term liquidity position. It also measures a company’s ability to meet its short-term

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

obligations with most liquid assets. As the quick ratio turns out to be negative and less than 1,

Fu-Wang is highly in danger not to pay off its current liabilities in the short term.

Asset Management Ratio:

The Inventory Turnover ratio of Fu-Wang shows that it is very low from the industrial average

given in the core textbook (Essentials of Managerial Finance, Besley and Brigham, 2016). The

inventory turnover ratio of only 0.13 suggests that either the sales were too low or the inventory

were too high. Fu-Wang, regardless of anything, could sell its average inventory in (360/0.13) or

2,700 days approximately. In contrast, other companies with an equal ratio to industrial average

can complete within (360/7.4) or around 49 days only.

The Days Sales Outstanding ratio of Fu-Wang shows a higher DSO than the industrial average of

32.1 days. The result came out around 1170 days. It indicates that Fu-Wang is taking more time

to collect its receivables than other competitors. The receivables might affect the cash-in-hand

for FU-Wang, which is very important for running the business in the industry.

In the financial year 2019-2020, Fu-Wang demonstrated a Fixed Asset Turnover ratio of 1.03x

that is lower than the average industrial ratio of 4.0x. Hence, the company is inefficient to

generate sales with the number of fixed assets they have. On the other hand, the Total Asset

Turnover ratio was 0.17x, whereas the industry average is 2.10x. As previously discussed, the

company is again failed to generate profit from the total assets. As both the Asset Turnover ratio

of Fu-Wang came out low, it indicates the possibility of low sales of Fu-Wang in the financial

year 2019-2020 was affected by the COVID-19 pandemic. The effect is still prevailing during

prolific lockdowns where markets are forced to be closed, and customers are not interested in

buying items other than a regular commodity. The COVID-19 pandemic has been a significant

reason for declining turnover (Fu-Wang Foods Limited, 2020).

Debt Management Ratio:

The total debt to asset ratio of Fu-Wang was calculated, and it was found that the ratio was 0.67,

which is comparatively higher than the industrial average of 0.42. This higher ratio indicates that

the company is at greater risk associated with the firm’s operation. The high debt to asset ratio

also indicates that Fu-Wang has low borrowing capacity and lower financial flexibility.

7 | P a g e

Fu-Wang is highly in danger not to pay off its current liabilities in the short term.

Asset Management Ratio:

The Inventory Turnover ratio of Fu-Wang shows that it is very low from the industrial average

given in the core textbook (Essentials of Managerial Finance, Besley and Brigham, 2016). The

inventory turnover ratio of only 0.13 suggests that either the sales were too low or the inventory

were too high. Fu-Wang, regardless of anything, could sell its average inventory in (360/0.13) or

2,700 days approximately. In contrast, other companies with an equal ratio to industrial average

can complete within (360/7.4) or around 49 days only.

The Days Sales Outstanding ratio of Fu-Wang shows a higher DSO than the industrial average of

32.1 days. The result came out around 1170 days. It indicates that Fu-Wang is taking more time

to collect its receivables than other competitors. The receivables might affect the cash-in-hand

for FU-Wang, which is very important for running the business in the industry.

In the financial year 2019-2020, Fu-Wang demonstrated a Fixed Asset Turnover ratio of 1.03x

that is lower than the average industrial ratio of 4.0x. Hence, the company is inefficient to

generate sales with the number of fixed assets they have. On the other hand, the Total Asset

Turnover ratio was 0.17x, whereas the industry average is 2.10x. As previously discussed, the

company is again failed to generate profit from the total assets. As both the Asset Turnover ratio

of Fu-Wang came out low, it indicates the possibility of low sales of Fu-Wang in the financial

year 2019-2020 was affected by the COVID-19 pandemic. The effect is still prevailing during

prolific lockdowns where markets are forced to be closed, and customers are not interested in

buying items other than a regular commodity. The COVID-19 pandemic has been a significant

reason for declining turnover (Fu-Wang Foods Limited, 2020).

Debt Management Ratio:

The total debt to asset ratio of Fu-Wang was calculated, and it was found that the ratio was 0.67,

which is comparatively higher than the industrial average of 0.42. This higher ratio indicates that

the company is at greater risk associated with the firm’s operation. The high debt to asset ratio

also indicates that Fu-Wang has low borrowing capacity and lower financial flexibility.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profitability Ratio:

The net profit margin after tax is calculated to be -0.13, where the industry average is 0.05. The

result suggests that the amount of selling products is not sufficient to meet up the cost of making

or selling the products of Fu-Wang Foods Limited.

After calculation, it was found that the Return on Total Assets was -0.02, which is still lower

than the usual industrial average of 0.10. This event indicates that the company is not effective in

generating income. On the other hand, the total shareholder’s equity of Fu-Wang amounted to

1,330,811, 955.00 BDT is the major portion of the other side of the balance sheet. The ROE

(Return on Equity) for Fu-Wang was found to be -0.20, which is very low compared to the

industrial average of 0.18. The event suggests that the company incurs a loss, and there is no net

income. Hence, it can be concluded that negative ROE is necessarily bad for a company.

Market Value Ratio:

As the company is currently at a loss, the Price Earnings ratio also turned out to be less than the

industrial average. The ratio was found to be -0.33x, and the industrial average is 15x. Fu-Wang

is currently losing money, and there is a huge risk of bankruptcy if the company does not meet

up with current losses. It also indicates that the stock price is low compared to earnings (Estevez,

2020).

The book value per share of Fu-Wang is calculated to be 1.54x, and the industrial average shows

a ratio of 2.50. It is still less and indicates that investors are less likely to pay more for Fu-

Wang’s share for its book value than the industry.

Comparative Ratios (Benchmarking)

Comparative ratios for many industries are available from several sources, including Dun and

Bradstreet, Robert Morris Associates, and the U.S department of commerce. Hence, the

comparative ratio analysis is described as the ratio calculated for a particular company compared

to those of other companies in the same industries (Besley and Brigham, 2016).

Below table is constructed in the context of Fu-Wang’s financial ratio analysis of the year 2019-

2020.

Ratio Ratio Value Industry Average Comment

8 | P a g e

The net profit margin after tax is calculated to be -0.13, where the industry average is 0.05. The

result suggests that the amount of selling products is not sufficient to meet up the cost of making

or selling the products of Fu-Wang Foods Limited.

After calculation, it was found that the Return on Total Assets was -0.02, which is still lower

than the usual industrial average of 0.10. This event indicates that the company is not effective in

generating income. On the other hand, the total shareholder’s equity of Fu-Wang amounted to

1,330,811, 955.00 BDT is the major portion of the other side of the balance sheet. The ROE

(Return on Equity) for Fu-Wang was found to be -0.20, which is very low compared to the

industrial average of 0.18. The event suggests that the company incurs a loss, and there is no net

income. Hence, it can be concluded that negative ROE is necessarily bad for a company.

Market Value Ratio:

As the company is currently at a loss, the Price Earnings ratio also turned out to be less than the

industrial average. The ratio was found to be -0.33x, and the industrial average is 15x. Fu-Wang

is currently losing money, and there is a huge risk of bankruptcy if the company does not meet

up with current losses. It also indicates that the stock price is low compared to earnings (Estevez,

2020).

The book value per share of Fu-Wang is calculated to be 1.54x, and the industrial average shows

a ratio of 2.50. It is still less and indicates that investors are less likely to pay more for Fu-

Wang’s share for its book value than the industry.

Comparative Ratios (Benchmarking)

Comparative ratios for many industries are available from several sources, including Dun and

Bradstreet, Robert Morris Associates, and the U.S department of commerce. Hence, the

comparative ratio analysis is described as the ratio calculated for a particular company compared

to those of other companies in the same industries (Besley and Brigham, 2016).

Below table is constructed in the context of Fu-Wang’s financial ratio analysis of the year 2019-

2020.

Ratio Ratio Value Industry Average Comment

8 | P a g e

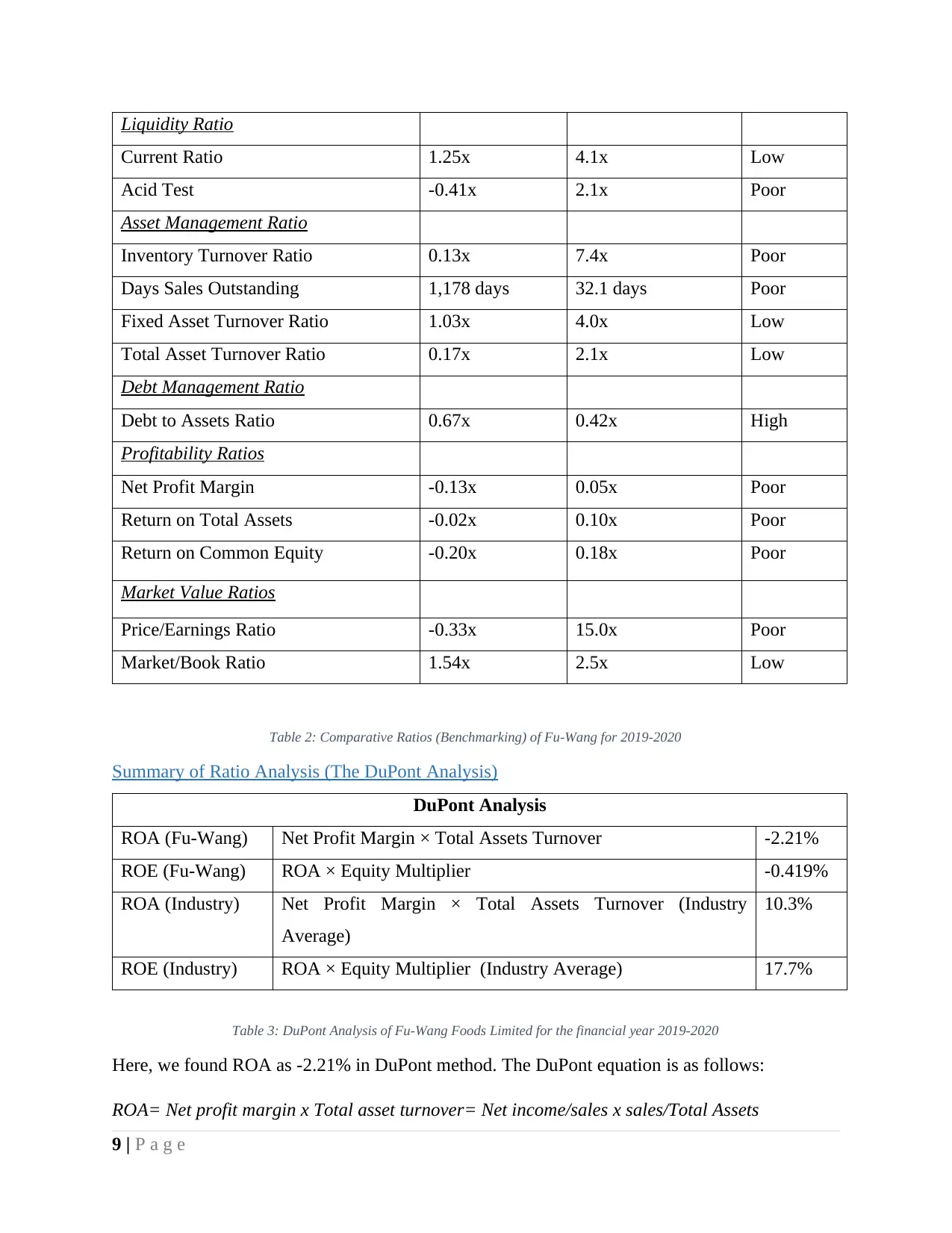

Liquidity Ratio

Current Ratio 1.25x 4.1x Low

Acid Test -0.41x 2.1x Poor

Asset Management Ratio

Inventory Turnover Ratio 0.13x 7.4x Poor

Days Sales Outstanding 1,178 days 32.1 days Poor

Fixed Asset Turnover Ratio 1.03x 4.0x Low

Total Asset Turnover Ratio 0.17x 2.1x Low

Debt Management Ratio

Debt to Assets Ratio 0.67x 0.42x High

Profitability Ratios

Net Profit Margin -0.13x 0.05x Poor

Return on Total Assets -0.02x 0.10x Poor

Return on Common Equity -0.20x 0.18x Poor

Market Value Ratios

Price/Earnings Ratio -0.33x 15.0x Poor

Market/Book Ratio 1.54x 2.5x Low

Table 2: Comparative Ratios (Benchmarking) of Fu-Wang for 2019-2020

Summary of Ratio Analysis (The DuPont Analysis)

DuPont Analysis

ROA (Fu-Wang) Net Profit Margin × Total Assets Turnover -2.21%

ROE (Fu-Wang) ROA × Equity Multiplier -0.419%

ROA (Industry) Net Profit Margin × Total Assets Turnover (Industry

Average)

10.3%

ROE (Industry) ROA × Equity Multiplier (Industry Average) 17.7%

Table 3: DuPont Analysis of Fu-Wang Foods Limited for the financial year 2019-2020

Here, we found ROA as -2.21% in DuPont method. The DuPont equation is as follows:

ROA= Net profit margin x Total asset turnover= Net income/sales x sales/Total Assets

9 | P a g e

Current Ratio 1.25x 4.1x Low

Acid Test -0.41x 2.1x Poor

Asset Management Ratio

Inventory Turnover Ratio 0.13x 7.4x Poor

Days Sales Outstanding 1,178 days 32.1 days Poor

Fixed Asset Turnover Ratio 1.03x 4.0x Low

Total Asset Turnover Ratio 0.17x 2.1x Low

Debt Management Ratio

Debt to Assets Ratio 0.67x 0.42x High

Profitability Ratios

Net Profit Margin -0.13x 0.05x Poor

Return on Total Assets -0.02x 0.10x Poor

Return on Common Equity -0.20x 0.18x Poor

Market Value Ratios

Price/Earnings Ratio -0.33x 15.0x Poor

Market/Book Ratio 1.54x 2.5x Low

Table 2: Comparative Ratios (Benchmarking) of Fu-Wang for 2019-2020

Summary of Ratio Analysis (The DuPont Analysis)

DuPont Analysis

ROA (Fu-Wang) Net Profit Margin × Total Assets Turnover -2.21%

ROE (Fu-Wang) ROA × Equity Multiplier -0.419%

ROA (Industry) Net Profit Margin × Total Assets Turnover (Industry

Average)

10.3%

ROE (Industry) ROA × Equity Multiplier (Industry Average) 17.7%

Table 3: DuPont Analysis of Fu-Wang Foods Limited for the financial year 2019-2020

Here, we found ROA as -2.21% in DuPont method. The DuPont equation is as follows:

ROA= Net profit margin x Total asset turnover= Net income/sales x sales/Total Assets

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fu-Wang Foods Limited has its equity multiplier calculated as 0.190x, which is less than 1. This

ratio indicates that Fu-Wang Foods Limited has fewer debt-financed assets. This incident is also

seen as a positive sign as the debt servicing cost is lower. On the other hand, Fu-Wang may also

be unable to entice lenders to loan it money on favourable terms. The inability to entice loans can

be problematic sometimes.

By using Equity multiplier, ROE is found to be -0.419%. The extended DuPont equation for

ROE is given below:

ROE = Net Profit Margin X Total Assets Turnover X Equity Multiplier

Here, ROE is very low than the industry average for Fu-Wang Foods Limited. The net profit

margin is also lower in this case. The negative ROE is necessarily bad for the company. Here the

costs are the result of improving the business. It can be described as improving business through

reconstruction.

Recommendations

After all the financial analysis, it has been found that despite all the losses that Fu-Wang Foods

limited incurred during the period is fixable. For this, some of the recommendations will be:

1. To overcome the prominent credit risk, Fu-Wang should hold more cash among total

current assets.

2. The company should focus on increasing its utilization of production capacity.

3. Varieties of products should be introduced.

Conclusion

The formal assessment aimed to make the students capable of analyzing the ratios of a certain

company. Hence, a business student can easily make financial analyses that will be beneficial for

future endeavors. In this assignment, a financial ratio analysis of Fu-Wang foods ltd. of

Bangladesh has been conducted. The industry average was taken from the core textbook to

compare the calculated ratios. Finally, a recommendation part has been included for Fu-Wang

Foods ltd. of Bangladesh.

Index

10 | P a g e

ratio indicates that Fu-Wang Foods Limited has fewer debt-financed assets. This incident is also

seen as a positive sign as the debt servicing cost is lower. On the other hand, Fu-Wang may also

be unable to entice lenders to loan it money on favourable terms. The inability to entice loans can

be problematic sometimes.

By using Equity multiplier, ROE is found to be -0.419%. The extended DuPont equation for

ROE is given below:

ROE = Net Profit Margin X Total Assets Turnover X Equity Multiplier

Here, ROE is very low than the industry average for Fu-Wang Foods Limited. The net profit

margin is also lower in this case. The negative ROE is necessarily bad for the company. Here the

costs are the result of improving the business. It can be described as improving business through

reconstruction.

Recommendations

After all the financial analysis, it has been found that despite all the losses that Fu-Wang Foods

limited incurred during the period is fixable. For this, some of the recommendations will be:

1. To overcome the prominent credit risk, Fu-Wang should hold more cash among total

current assets.

2. The company should focus on increasing its utilization of production capacity.

3. Varieties of products should be introduced.

Conclusion

The formal assessment aimed to make the students capable of analyzing the ratios of a certain

company. Hence, a business student can easily make financial analyses that will be beneficial for

future endeavors. In this assignment, a financial ratio analysis of Fu-Wang foods ltd. of

Bangladesh has been conducted. The industry average was taken from the core textbook to

compare the calculated ratios. Finally, a recommendation part has been included for Fu-Wang

Foods ltd. of Bangladesh.

Index

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table 1: Financial Ratio Analysis of Fu-Wang Foods Limited (At the end of June 30th, 2020)....6

Table 2: Comparative Ratios (Benchmarking) of Fu-Wang for 2019-2020....................................9

Table 3: DuPont Analysis of Fu-Wang Foods Limited for the financial year 2019-2020..............9

11 | P a g e

Table 2: Comparative Ratios (Benchmarking) of Fu-Wang for 2019-2020....................................9

Table 3: DuPont Analysis of Fu-Wang Foods Limited for the financial year 2019-2020..............9

11 | P a g e

References

Ak, B., Dechow, P., Sun, Y. and Wang, A., 2013. The use of financial ratio models to help

investors predict and interpret significant corporate events. Australian Journal of Management,

38(3), pp.553-598.

Besley, S. and Brigham, E., 2016. Essentials of Managerial Finance. 14th ed. Mason, OH:

Thomson/South-western, pp.51-52.

Castro, N. and Chousa, J., 2006. An integrated framework for the financial analysis of

sustainability. Business Strategy and the Environment, 15(5), pp.322-333.

Fuwangfoodsltd.com. 2021. About. [online] Available at:

https://www.fuwangfoodsltd.com/about [Accessed 10 July 2021].

Fu-Wang Foods Limited, 2020. Annual Report. Dhaka: Fu-Wang Foods Ltd.

Estevez, E., 2020. Can Stocks have a negative price-to-earnings ratio? [online] Investopedia.

Available at: https://www.investopedia.com/ask/answers/05/negativeeps.asp [Accessed 12 July

2021].

Miller, B. and Miller, D., 1991. How to Interpret Financial Statements for Better Business

Decisions. New York, NY: AMACOM.

12 | P a g e

Ak, B., Dechow, P., Sun, Y. and Wang, A., 2013. The use of financial ratio models to help

investors predict and interpret significant corporate events. Australian Journal of Management,

38(3), pp.553-598.

Besley, S. and Brigham, E., 2016. Essentials of Managerial Finance. 14th ed. Mason, OH:

Thomson/South-western, pp.51-52.

Castro, N. and Chousa, J., 2006. An integrated framework for the financial analysis of

sustainability. Business Strategy and the Environment, 15(5), pp.322-333.

Fuwangfoodsltd.com. 2021. About. [online] Available at:

https://www.fuwangfoodsltd.com/about [Accessed 10 July 2021].

Fu-Wang Foods Limited, 2020. Annual Report. Dhaka: Fu-Wang Foods Ltd.

Estevez, E., 2020. Can Stocks have a negative price-to-earnings ratio? [online] Investopedia.

Available at: https://www.investopedia.com/ask/answers/05/negativeeps.asp [Accessed 12 July

2021].

Miller, B. and Miller, D., 1991. How to Interpret Financial Statements for Better Business

Decisions. New York, NY: AMACOM.

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.