Labour Economics: Analysis of Firm Demand, Discrimination, and Policy

VerifiedAdded on 2023/01/18

|17

|3793

|34

Report

AI Summary

This report delves into key aspects of labour economics, commencing with an in-depth examination of how a firm's demand curve is derived in the long run, utilizing isoquant-isocost analysis, the substitution effect, output effect, and the Hicks-Marshall rules of derived demand. The report then transitions to an empirical analysis of the labour market, focusing on the measurement of labour market discrimination, specifically addressing the extent of wage discrimination faced by females in the UK, supported by statistical data and graphical representations. Finally, the report concludes by outlining the types of policies that should be introduced to reduce high levels of unemployment, providing a comprehensive overview of contemporary labour market challenges and potential solutions. The report uses diagrams for further explanation and is based on a coursework assignment.

Labour Economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Section A.........................................................................................................................................1

Description on how a firm's demand curve is derived in the long run...................................1

Section B..........................................................................................................................................4

Way to measure the labour market and extent to which females in UK face wage

discrimination.........................................................................................................................4

Section C..........................................................................................................................................8

Types of policies need to be introduced for reducing high levels of unemployment.............8

REFERENCES..............................................................................................................................12

.......................................................................................................................................................12

Section A.........................................................................................................................................1

Description on how a firm's demand curve is derived in the long run...................................1

Section B..........................................................................................................................................4

Way to measure the labour market and extent to which females in UK face wage

discrimination.........................................................................................................................4

Section C..........................................................................................................................................8

Types of policies need to be introduced for reducing high levels of unemployment.............8

REFERENCES..............................................................................................................................12

.......................................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section A

Description on how a firm's demand curve is derived in the long run

The demand curve of a firm depicts either its short-run costs or long-run costs, which

mainly depends on fixed costs and variables costs. Long run costs are mainly accumulated when

production levels of firms changes over time, with regards to expected profits or losses

economically (Koval, Polyezhayev and Bezkhlibna, 2019). In this regard, within long run of a

firm there is no fixed factors of production, where resources like land, capital goods, labour and

more, all are varied in response to reach long run cost of a firm for producing a particular good

or service. So, long run needs a proper planning as well as implementation stage for firms, to

determine firms’ current market state with projected state, that helps in making decisions for

production (Auer, 2018). Decisions in this regard includes changes within production quantity,

business expansion, entrance or exit from a marketplace, is taken that directly impact on a firm’s

costs. In terms of economics, long run costs in efficient manner can be sustained when outputs of

a firm i.e. result produces in desired quantity of commodity is combines at minimum possible

cost.

Isoquant-isocost analysis

A firm’s main objective is to maximise its profitability at any costs, depends on short-term

and long-term (Murtin and Robin, 2018). In the short run, the total output that firms produce

remains always fixed because of constraint capacity. While if it is a price-taker, i.e. long-term

then price can be changed in order to remain in a competitive market, so, total revenue in such

condition will remain fixed. Thus, the only manner in which profit can be maximised is minimise

the cost as much as possible. Furthermore, supply and demand curve depends on cost of

production, where decision taken by a firm to supply an extra unit is depended on marginal cost

of producing for that unit (Callaghan, 2018). In long run, firm’s decisions depend on two factors

mainly that are – technical relations which shows how output of product vary as per input vary;

and second one is prices of factors like labour costs, interest rates, capital price and more.

therefore, using these two factors, capital and labour can be represented via equal-product curve,

which is also known as isoquant curve (Brown, 2018). This curve traces out the combination of

two yields that yield with same level of output.

1

Description on how a firm's demand curve is derived in the long run

The demand curve of a firm depicts either its short-run costs or long-run costs, which

mainly depends on fixed costs and variables costs. Long run costs are mainly accumulated when

production levels of firms changes over time, with regards to expected profits or losses

economically (Koval, Polyezhayev and Bezkhlibna, 2019). In this regard, within long run of a

firm there is no fixed factors of production, where resources like land, capital goods, labour and

more, all are varied in response to reach long run cost of a firm for producing a particular good

or service. So, long run needs a proper planning as well as implementation stage for firms, to

determine firms’ current market state with projected state, that helps in making decisions for

production (Auer, 2018). Decisions in this regard includes changes within production quantity,

business expansion, entrance or exit from a marketplace, is taken that directly impact on a firm’s

costs. In terms of economics, long run costs in efficient manner can be sustained when outputs of

a firm i.e. result produces in desired quantity of commodity is combines at minimum possible

cost.

Isoquant-isocost analysis

A firm’s main objective is to maximise its profitability at any costs, depends on short-term

and long-term (Murtin and Robin, 2018). In the short run, the total output that firms produce

remains always fixed because of constraint capacity. While if it is a price-taker, i.e. long-term

then price can be changed in order to remain in a competitive market, so, total revenue in such

condition will remain fixed. Thus, the only manner in which profit can be maximised is minimise

the cost as much as possible. Furthermore, supply and demand curve depends on cost of

production, where decision taken by a firm to supply an extra unit is depended on marginal cost

of producing for that unit (Callaghan, 2018). In long run, firm’s decisions depend on two factors

mainly that are – technical relations which shows how output of product vary as per input vary;

and second one is prices of factors like labour costs, interest rates, capital price and more.

therefore, using these two factors, capital and labour can be represented via equal-product curve,

which is also known as isoquant curve (Brown, 2018). This curve traces out the combination of

two yields that yield with same level of output.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

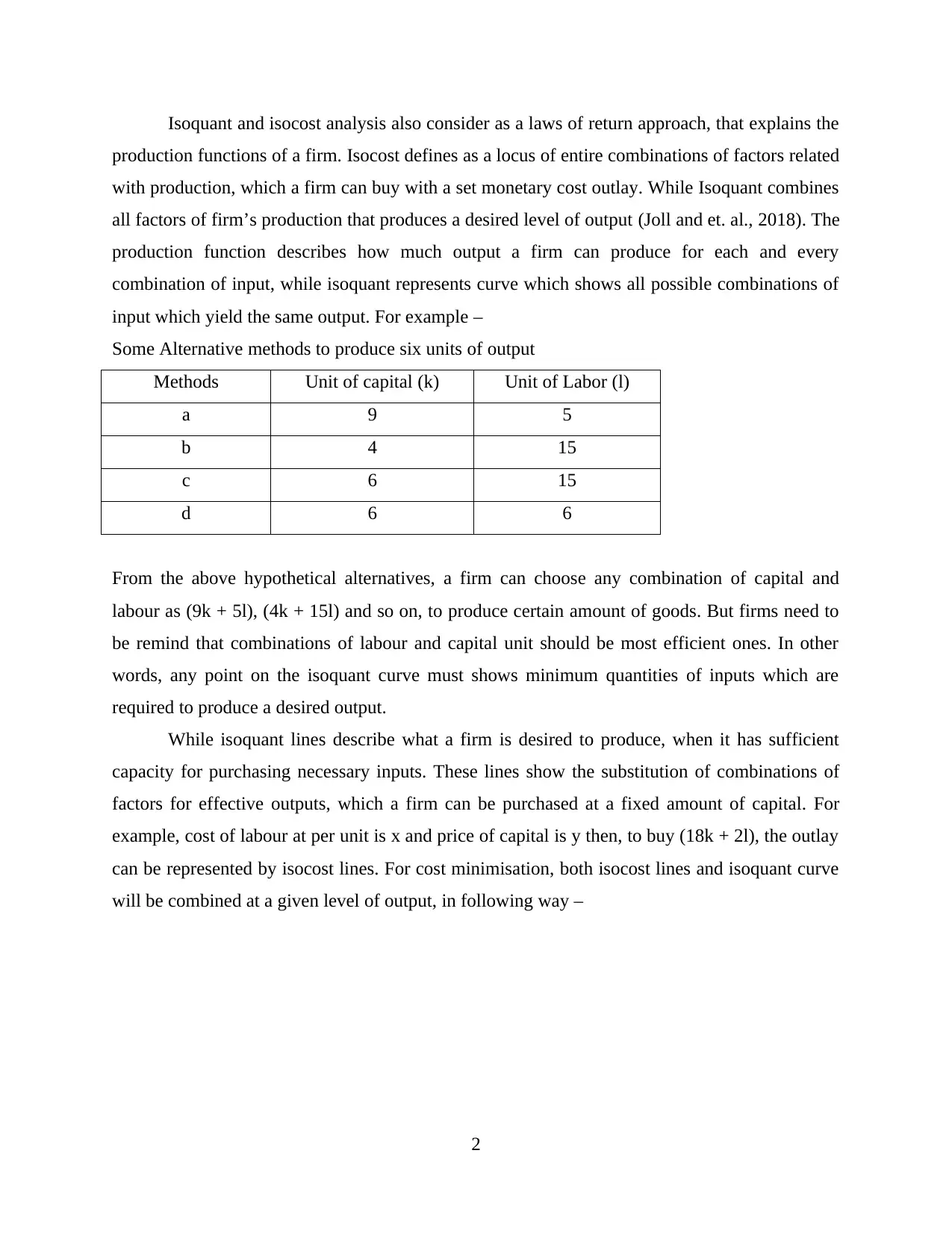

Isoquant and isocost analysis also consider as a laws of return approach, that explains the

production functions of a firm. Isocost defines as a locus of entire combinations of factors related

with production, which a firm can buy with a set monetary cost outlay. While Isoquant combines

all factors of firm’s production that produces a desired level of output (Joll and et. al., 2018). The

production function describes how much output a firm can produce for each and every

combination of input, while isoquant represents curve which shows all possible combinations of

input which yield the same output. For example –

Some Alternative methods to produce six units of output

Methods Unit of capital (k) Unit of Labor (l)

a 9 5

b 4 15

c 6 15

d 6 6

From the above hypothetical alternatives, a firm can choose any combination of capital and

labour as (9k + 5l), (4k + 15l) and so on, to produce certain amount of goods. But firms need to

be remind that combinations of labour and capital unit should be most efficient ones. In other

words, any point on the isoquant curve must shows minimum quantities of inputs which are

required to produce a desired output.

While isoquant lines describe what a firm is desired to produce, when it has sufficient

capacity for purchasing necessary inputs. These lines show the substitution of combinations of

factors for effective outputs, which a firm can be purchased at a fixed amount of capital. For

example, cost of labour at per unit is x and price of capital is y then, to buy (18k + 2l), the outlay

can be represented by isocost lines. For cost minimisation, both isocost lines and isoquant curve

will be combined at a given level of output, in following way –

2

production functions of a firm. Isocost defines as a locus of entire combinations of factors related

with production, which a firm can buy with a set monetary cost outlay. While Isoquant combines

all factors of firm’s production that produces a desired level of output (Joll and et. al., 2018). The

production function describes how much output a firm can produce for each and every

combination of input, while isoquant represents curve which shows all possible combinations of

input which yield the same output. For example –

Some Alternative methods to produce six units of output

Methods Unit of capital (k) Unit of Labor (l)

a 9 5

b 4 15

c 6 15

d 6 6

From the above hypothetical alternatives, a firm can choose any combination of capital and

labour as (9k + 5l), (4k + 15l) and so on, to produce certain amount of goods. But firms need to

be remind that combinations of labour and capital unit should be most efficient ones. In other

words, any point on the isoquant curve must shows minimum quantities of inputs which are

required to produce a desired output.

While isoquant lines describe what a firm is desired to produce, when it has sufficient

capacity for purchasing necessary inputs. These lines show the substitution of combinations of

factors for effective outputs, which a firm can be purchased at a fixed amount of capital. For

example, cost of labour at per unit is x and price of capital is y then, to buy (18k + 2l), the outlay

can be represented by isocost lines. For cost minimisation, both isocost lines and isoquant curve

will be combined at a given level of output, in following way –

2

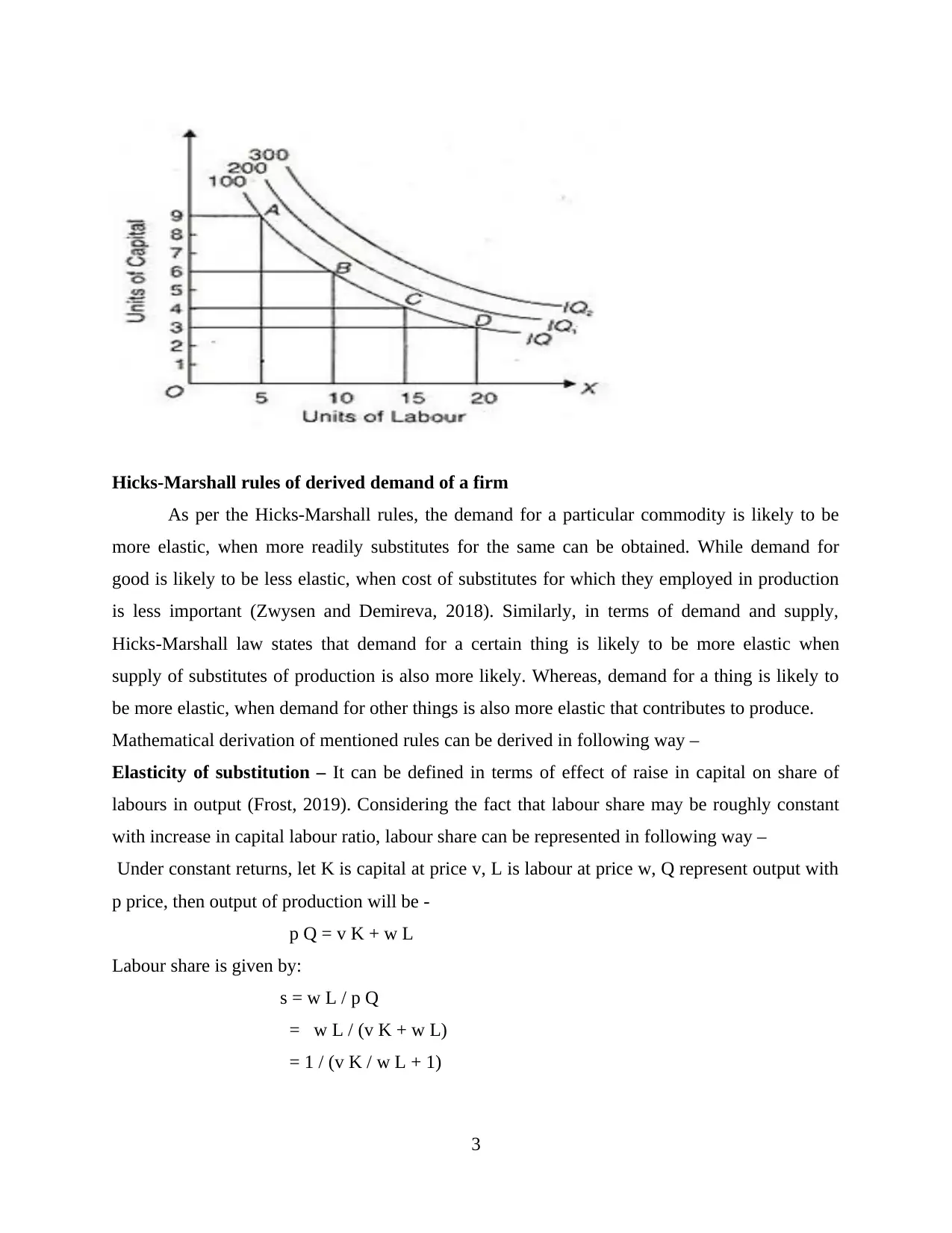

Hicks-Marshall rules of derived demand of a firm

As per the Hicks-Marshall rules, the demand for a particular commodity is likely to be

more elastic, when more readily substitutes for the same can be obtained. While demand for

good is likely to be less elastic, when cost of substitutes for which they employed in production

is less important (Zwysen and Demireva, 2018). Similarly, in terms of demand and supply,

Hicks-Marshall law states that demand for a certain thing is likely to be more elastic when

supply of substitutes of production is also more likely. Whereas, demand for a thing is likely to

be more elastic, when demand for other things is also more elastic that contributes to produce.

Mathematical derivation of mentioned rules can be derived in following way –

Elasticity of substitution – It can be defined in terms of effect of raise in capital on share of

labours in output (Frost, 2019). Considering the fact that labour share may be roughly constant

with increase in capital labour ratio, labour share can be represented in following way –

Under constant returns, let K is capital at price v, L is labour at price w, Q represent output with

p price, then output of production will be -

p Q = v K + w L

Labour share is given by:

s = w L / p Q

= w L / (v K + w L)

= 1 / (v K / w L + 1)

3

As per the Hicks-Marshall rules, the demand for a particular commodity is likely to be

more elastic, when more readily substitutes for the same can be obtained. While demand for

good is likely to be less elastic, when cost of substitutes for which they employed in production

is less important (Zwysen and Demireva, 2018). Similarly, in terms of demand and supply,

Hicks-Marshall law states that demand for a certain thing is likely to be more elastic when

supply of substitutes of production is also more likely. Whereas, demand for a thing is likely to

be more elastic, when demand for other things is also more elastic that contributes to produce.

Mathematical derivation of mentioned rules can be derived in following way –

Elasticity of substitution – It can be defined in terms of effect of raise in capital on share of

labours in output (Frost, 2019). Considering the fact that labour share may be roughly constant

with increase in capital labour ratio, labour share can be represented in following way –

Under constant returns, let K is capital at price v, L is labour at price w, Q represent output with

p price, then output of production will be -

p Q = v K + w L

Labour share is given by:

s = w L / p Q

= w L / (v K + w L)

= 1 / (v K / w L + 1)

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Therefore, change in labour share s depends on elasticity of capital/labour (K/L) with respect to

proportion of price of capital with price of labour (v/w).

Section B

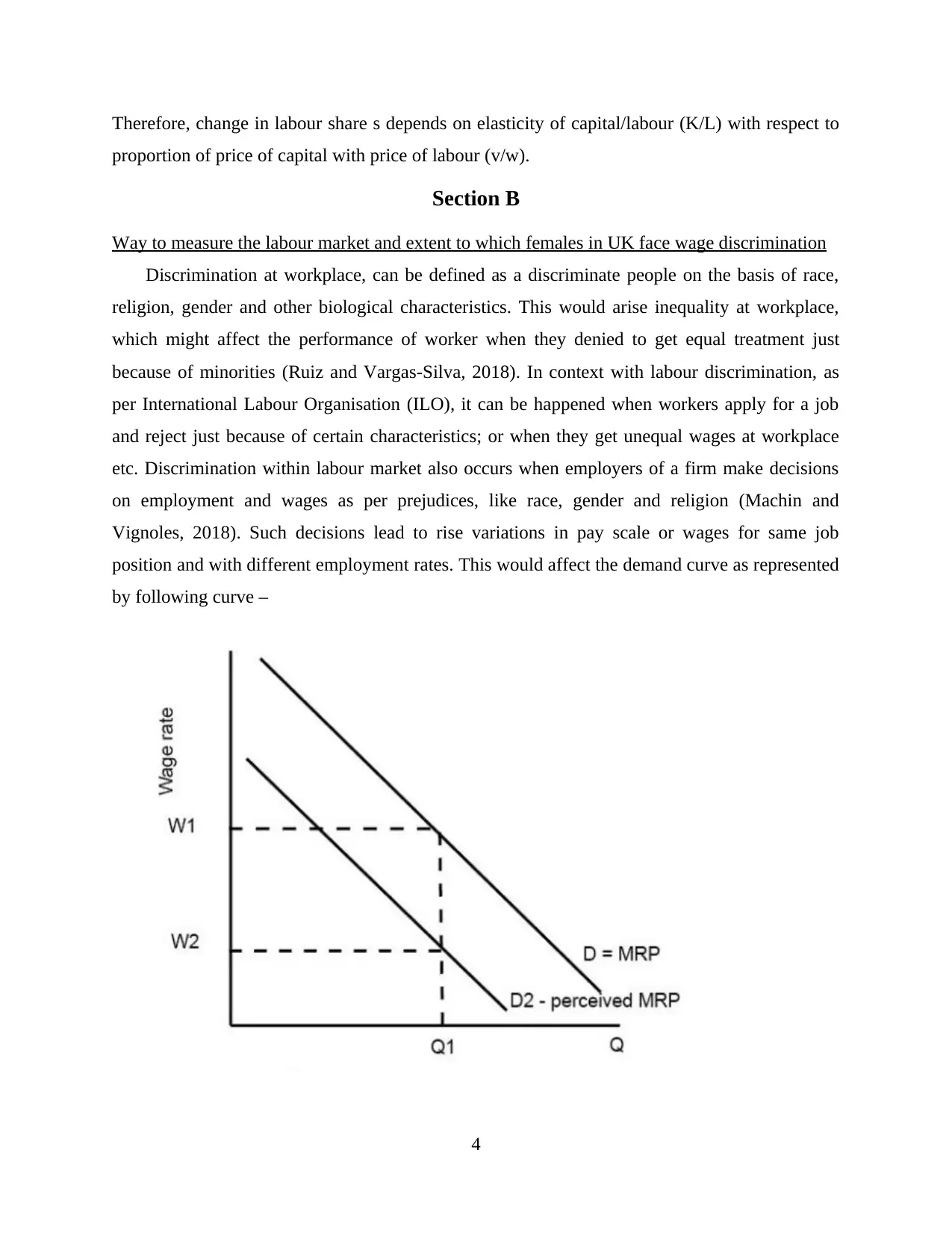

Way to measure the labour market and extent to which females in UK face wage discrimination

Discrimination at workplace, can be defined as a discriminate people on the basis of race,

religion, gender and other biological characteristics. This would arise inequality at workplace,

which might affect the performance of worker when they denied to get equal treatment just

because of minorities (Ruiz and Vargas-Silva, 2018). In context with labour discrimination, as

per International Labour Organisation (ILO), it can be happened when workers apply for a job

and reject just because of certain characteristics; or when they get unequal wages at workplace

etc. Discrimination within labour market also occurs when employers of a firm make decisions

on employment and wages as per prejudices, like race, gender and religion (Machin and

Vignoles, 2018). Such decisions lead to rise variations in pay scale or wages for same job

position and with different employment rates. This would affect the demand curve as represented

by following curve –

4

proportion of price of capital with price of labour (v/w).

Section B

Way to measure the labour market and extent to which females in UK face wage discrimination

Discrimination at workplace, can be defined as a discriminate people on the basis of race,

religion, gender and other biological characteristics. This would arise inequality at workplace,

which might affect the performance of worker when they denied to get equal treatment just

because of minorities (Ruiz and Vargas-Silva, 2018). In context with labour discrimination, as

per International Labour Organisation (ILO), it can be happened when workers apply for a job

and reject just because of certain characteristics; or when they get unequal wages at workplace

etc. Discrimination within labour market also occurs when employers of a firm make decisions

on employment and wages as per prejudices, like race, gender and religion (Machin and

Vignoles, 2018). Such decisions lead to rise variations in pay scale or wages for same job

position and with different employment rates. This would affect the demand curve as represented

by following curve –

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Here, MRP shows the marginal revenue product of labours, where due to discrimination

because of employers preferences for denying jobs to certain groups of workers, then MPR of

that community is lower than others (Economics of Discrimination, 2019). This group will not be

employed at W1 and will have to accept lower wages.

Labour market discrimination explain wage dispersion that occurs among workers,

employers, customers etc., where factors like race and sex are taken into account, when make

economic exchanges (Li and Heath, 2018). In this regard, such kind of discrimination can be

measured in terms of gender and racial differences as – Less female workers at workplace due to

male dominated area, where women get less pay as compared to man on same position;

differences in educational background between majorities and minorities people that affects

employment as well; prejudiced way of employers during employment procedures, where they

hire male people mainly. Similarly, if a company wants to hire only white workers and

discriminates the ethnic minorities then it also increases labour discrimination (Lin, Lutter and

Ruhm, 2018). In context with labour market of UK, it reflects a mixed picture of wage growth

and unemployment, where due to tightening of labour market vacancies are highly fallen. So,

this rises the unemployment ratio in adverse manner (Joll and et. al., 2018). However, as per

report of 2019, in UK employment has been increased up to 115k that reach a record of 32.8

million. But employment rate in such period, still remains same.

Evidence that suggests extent towards which female workers experience wage

discrimination in UK

The gender pay gap for the full-time workers is highly in favours of men belonging to all

occupations. However the occupational crowding has impact since such occupations with small

gender pay gap has equal shares of employment shares that is between women and men (Koval,

Polyezhayev and Bezkhlibna, 2019). The gender pay gap had always been an interesting topic

but for attempting an increase in awareness and improving the quality of pay, the government of

UK has introduced mandatory reporting if gender pay gap for enterprises with around 250 or

more workers by the April, 2018 (Workplace gender discrimination remains rife, survey finds.

2019. ). For UK as a whole, this gap has been reduced in last 10 years but it is still favouring

men.

5

because of employers preferences for denying jobs to certain groups of workers, then MPR of

that community is lower than others (Economics of Discrimination, 2019). This group will not be

employed at W1 and will have to accept lower wages.

Labour market discrimination explain wage dispersion that occurs among workers,

employers, customers etc., where factors like race and sex are taken into account, when make

economic exchanges (Li and Heath, 2018). In this regard, such kind of discrimination can be

measured in terms of gender and racial differences as – Less female workers at workplace due to

male dominated area, where women get less pay as compared to man on same position;

differences in educational background between majorities and minorities people that affects

employment as well; prejudiced way of employers during employment procedures, where they

hire male people mainly. Similarly, if a company wants to hire only white workers and

discriminates the ethnic minorities then it also increases labour discrimination (Lin, Lutter and

Ruhm, 2018). In context with labour market of UK, it reflects a mixed picture of wage growth

and unemployment, where due to tightening of labour market vacancies are highly fallen. So,

this rises the unemployment ratio in adverse manner (Joll and et. al., 2018). However, as per

report of 2019, in UK employment has been increased up to 115k that reach a record of 32.8

million. But employment rate in such period, still remains same.

Evidence that suggests extent towards which female workers experience wage

discrimination in UK

The gender pay gap for the full-time workers is highly in favours of men belonging to all

occupations. However the occupational crowding has impact since such occupations with small

gender pay gap has equal shares of employment shares that is between women and men (Koval,

Polyezhayev and Bezkhlibna, 2019). The gender pay gap had always been an interesting topic

but for attempting an increase in awareness and improving the quality of pay, the government of

UK has introduced mandatory reporting if gender pay gap for enterprises with around 250 or

more workers by the April, 2018 (Workplace gender discrimination remains rife, survey finds.

2019. ). For UK as a whole, this gap has been reduced in last 10 years but it is still favouring

men.

5

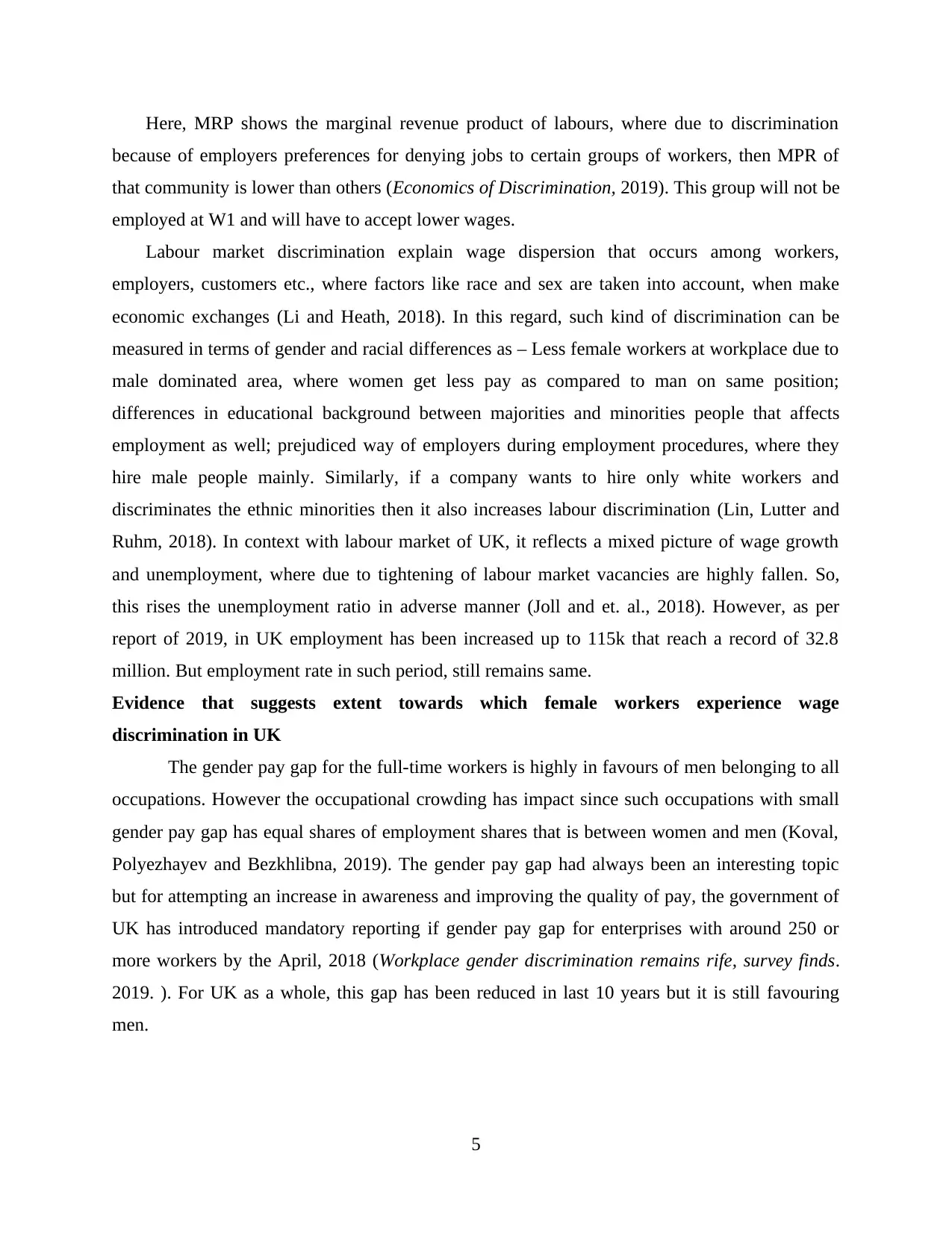

The figure below shows the headline that can be used to measure the gender pay gap in

UK.

Source: Annual Survey of Hours and Earnings (ASHE) – Office for National Statistics.

2019

Illustration: The above graphical figure represents that the hourly gross earnings of women and

men who are full time employees. Between the year 2011 to 2017, the pays of men has been

grown by 10.4% from £13.12 towards £14.48 which is per hour whilst of the payment of the

women and it has grown from £11.75 to £13.16 every per hour (Auer, 2018). In the year 2017,

the average pay of men was £1.32 that it more than women and it is proportion of the men's pay

and there is a gap of around 9.1%. The pay gap has been fallen from 10.5% in the year 2011 up

to 9.1% in the year 2017 but it has remained positive in value which means that men are paid

more than women on an average.

6

Illustration 1: Annual Survey of Hours and Earnings (ASHE) – Office for National Statistics.

2019

UK.

Source: Annual Survey of Hours and Earnings (ASHE) – Office for National Statistics.

2019

Illustration: The above graphical figure represents that the hourly gross earnings of women and

men who are full time employees. Between the year 2011 to 2017, the pays of men has been

grown by 10.4% from £13.12 towards £14.48 which is per hour whilst of the payment of the

women and it has grown from £11.75 to £13.16 every per hour (Auer, 2018). In the year 2017,

the average pay of men was £1.32 that it more than women and it is proportion of the men's pay

and there is a gap of around 9.1%. The pay gap has been fallen from 10.5% in the year 2011 up

to 9.1% in the year 2017 but it has remained positive in value which means that men are paid

more than women on an average.

6

Illustration 1: Annual Survey of Hours and Earnings (ASHE) – Office for National Statistics.

2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There is almost a quarter of 23% in which females of the age group between 16 to 30

have been harassed sexually at workplace but out of them only 8% have reported it, as per the

poll for Young Women's Trust (Murtin and Robin, 2018). Out of the reason for women who are

not reporting at workplace for sexual harassment were fear to loose their job or by not knowing

the way to make complaint (Workplace gender discrimination remains rife, survey finds, 2019).

Around 31% of young women had reported about sex discrimination while working for work and

around 19% said that have been paid less than male colleagues for same work and employment.

In addition to this, around 43% of mothers who are young said that they have also faced

maternity discrimination (Callaghan, 2018). The influence of gender discrimination is

highlighted by 52% of young women who say that their work procedure is having negative

impact upon their mental health. This survey shows that women are having negative impact upon

their financial and mental stability due to this discrimination in UK (Brown, 2018) .

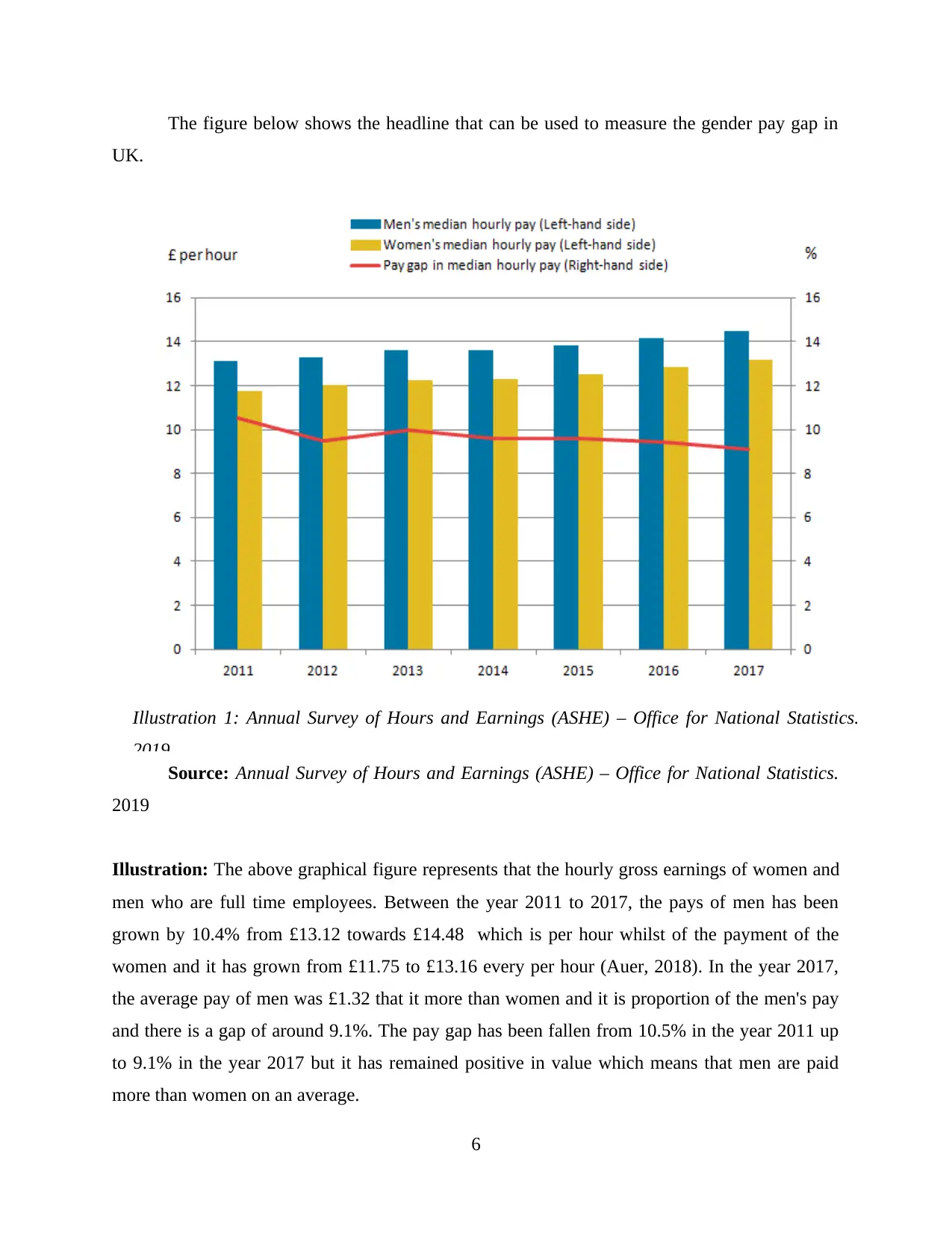

Another main evidence which shows that the unemployment to vacancies ratio in UK and

other countries, can be depicted from given figure -

Percentage of 16 to 64 year old, people who were employed, by ethnicity, disability and gender

Asian 66 48 69 77 59 80 54 39 58

Indian 76 58 79 83 62 86 69 55 71

Pakistani,

Bangladeshi

57 42 61 75 60 78 39 26 42

Asian Other 64 48 66 71 53 74 58 44 60

Black 67 44 71 72 42 76 63 45 66

Mixed 67 44 72 71 48 76 63 41 69

White 77 52 83 81 52 87 73 52 79

White

British

76 52 83 80 52 86 73 52 79

White Other 82 62 84 88 67 90 76 59 78

Other 61 40 65 70 41 76 51 40 54

7

have been harassed sexually at workplace but out of them only 8% have reported it, as per the

poll for Young Women's Trust (Murtin and Robin, 2018). Out of the reason for women who are

not reporting at workplace for sexual harassment were fear to loose their job or by not knowing

the way to make complaint (Workplace gender discrimination remains rife, survey finds, 2019).

Around 31% of young women had reported about sex discrimination while working for work and

around 19% said that have been paid less than male colleagues for same work and employment.

In addition to this, around 43% of mothers who are young said that they have also faced

maternity discrimination (Callaghan, 2018). The influence of gender discrimination is

highlighted by 52% of young women who say that their work procedure is having negative

impact upon their mental health. This survey shows that women are having negative impact upon

their financial and mental stability due to this discrimination in UK (Brown, 2018) .

Another main evidence which shows that the unemployment to vacancies ratio in UK and

other countries, can be depicted from given figure -

Percentage of 16 to 64 year old, people who were employed, by ethnicity, disability and gender

Asian 66 48 69 77 59 80 54 39 58

Indian 76 58 79 83 62 86 69 55 71

Pakistani,

Bangladeshi

57 42 61 75 60 78 39 26 42

Asian Other 64 48 66 71 53 74 58 44 60

Black 67 44 71 72 42 76 63 45 66

Mixed 67 44 72 71 48 76 63 41 69

White 77 52 83 81 52 87 73 52 79

White

British

76 52 83 80 52 86 73 52 79

White Other 82 62 84 88 67 90 76 59 78

Other 61 40 65 70 41 76 51 40 54

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

So, it has been interpreted from this statistical figure, that in the year 2018, the biggest

gap that raise the issue regarding with labour discrimination, is disability. Here, in ethnic group

of Bangladeshi and Pakistan face major issues where near about 60% of disable people have got

employment, where only in female population of disability group, only 26% were employed.

This would shows that female whether properly able to work or suffering from any disability, has

faced higher labour discrimination in entire world.

Section C

Types of policies need to be introduced for reducing high levels of unemployment

Since it has been observed that, labour discrimination raises continuously in entire

including UK due to unequal wages among people on the basis of gender issues (Auer, 2018).

Along with this employers also contributes major role in increasing labour discrimination where

8

gap that raise the issue regarding with labour discrimination, is disability. Here, in ethnic group

of Bangladeshi and Pakistan face major issues where near about 60% of disable people have got

employment, where only in female population of disability group, only 26% were employed.

This would shows that female whether properly able to work or suffering from any disability, has

faced higher labour discrimination in entire world.

Section C

Types of policies need to be introduced for reducing high levels of unemployment

Since it has been observed that, labour discrimination raises continuously in entire

including UK due to unequal wages among people on the basis of gender issues (Auer, 2018).

Along with this employers also contributes major role in increasing labour discrimination where

8

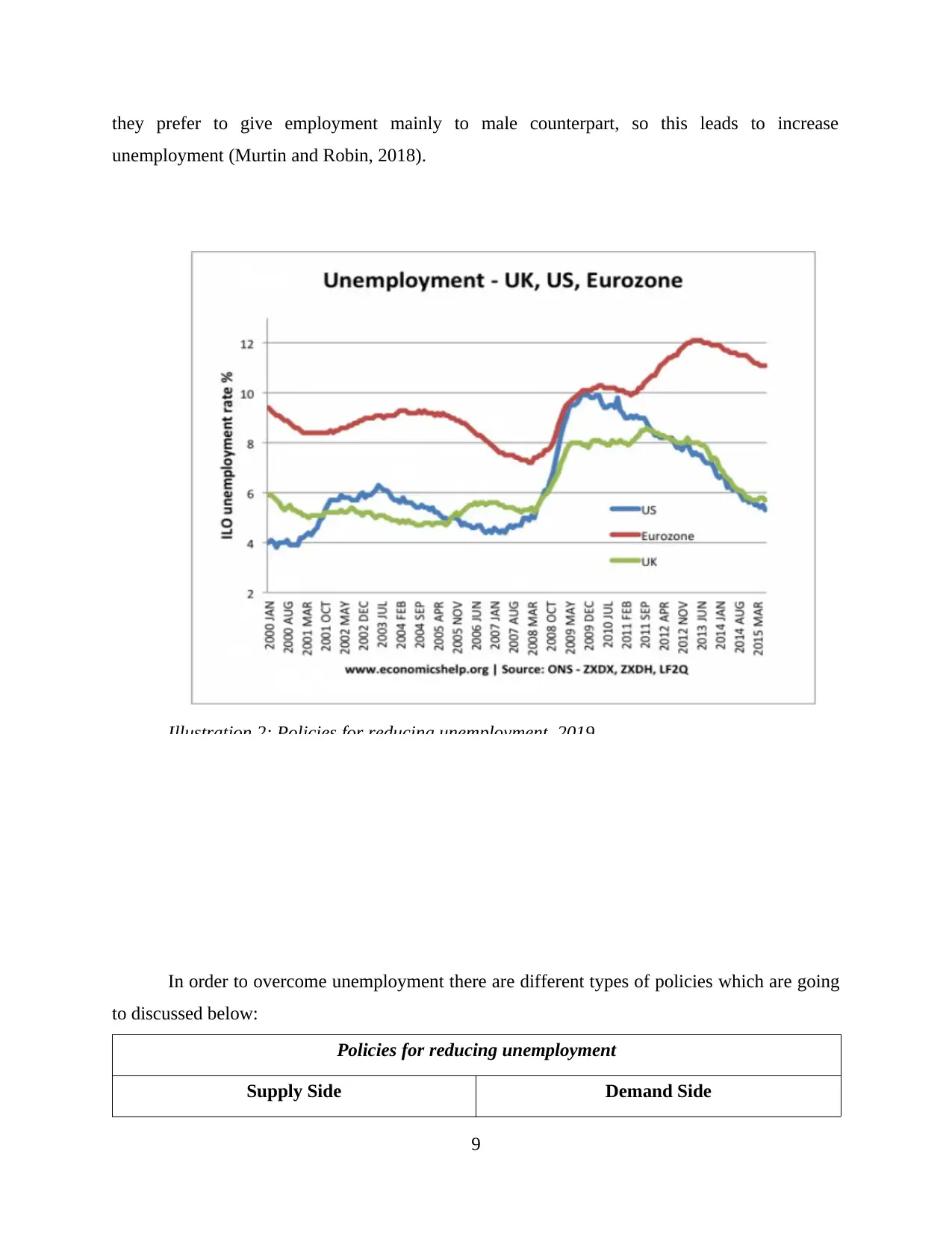

they prefer to give employment mainly to male counterpart, so this leads to increase

unemployment (Murtin and Robin, 2018).

In order to overcome unemployment there are different types of policies which are going

to discussed below:

Policies for reducing unemployment

Supply Side Demand Side

9

Illustration 2: Policies for reducing unemployment. 2019

unemployment (Murtin and Robin, 2018).

In order to overcome unemployment there are different types of policies which are going

to discussed below:

Policies for reducing unemployment

Supply Side Demand Side

9

Illustration 2: Policies for reducing unemployment. 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.