XLG Company: Management Accounting Report on Variances and Make or Buy

VerifiedAdded on 2023/01/09

|12

|3302

|69

Report

AI Summary

This report analyzes the financial performance of XLG, a cleaning product company, focusing on variance analysis and a make-or-buy decision. Part A delves into the calculation of sales price and volume contribution variances, material price planning and operational variances, providing detailed formulas and numerical examples. It also critically examines the merits and demerits of using these variances in assessing manager performance, highlighting aspects like cost control, performance evaluation, and accountability. Part B assesses the strategic decision of whether XLG should manufacture famaQ in-house in the UK or continue importing it from Brazil. The report provides a comprehensive overview of management accounting principles, offering insights into variance analysis, its implications, and strategic decision-making within a competitive business environment.

LCBB5002

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

1. Calculation of price and sales volume contribution variance..................................................1

2. The calculation of material price planning variance and material price operational variance 3

3. Changes in operational, critical analysis of merits and demerits of using variances in

assessing managers performance.................................................................................................4

PART B...........................................................................................................................................7

Report assessing the decision to make famaQ in house in the UK to keep importing it from

Brazil............................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

PART A...........................................................................................................................................1

1. Calculation of price and sales volume contribution variance..................................................1

2. The calculation of material price planning variance and material price operational variance 3

3. Changes in operational, critical analysis of merits and demerits of using variances in

assessing managers performance.................................................................................................4

PART B...........................................................................................................................................7

Report assessing the decision to make famaQ in house in the UK to keep importing it from

Brazil............................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Management accounting is an approach which is used by most of the entities for the

purpose of tracking business performance and formulating future decisions. With the help of it,

the managers will be able to decide that whether they have to make changes in organisational

policies or not. There are various internal stakeholders such as employees, manager, board

members, shareholders etc. who use management reports so that they can determine that the

entity is performing properly or not (Adler, 2018). This report is based upon XLG company

which is a cleaning product entity and it is located in eastern part of Britain. There are two

different cleaning agents that are produced by the organisation These are two different chemical

which are X and Y. The competition in the industry for the enterprise is very high. Due to

lockdown because of corona virus the entity planned to move all its sales online. For this

purpose, different aspects will be analysed. These are calculation of variances such as sales price

and volume, material price planning and operational variance and analysis of merits and demerits

of using them in assessing the managers performance. Apart from this, a brief report that

assesses the decision to make famaQ in house in the UK or keep importing it from Brazil is also

prepared in this report.

PART A

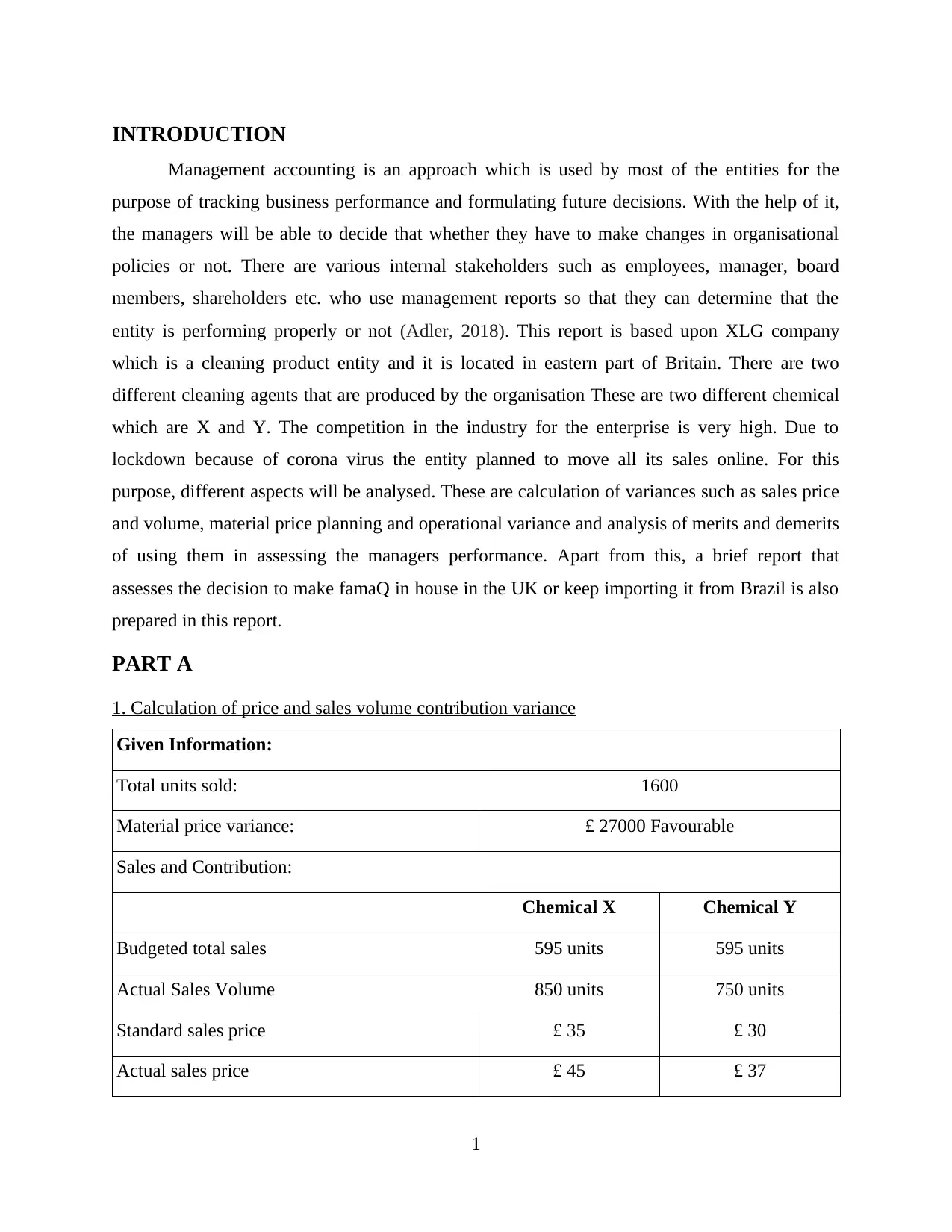

1. Calculation of price and sales volume contribution variance

Given Information:

Total units sold: 1600

Material price variance: £ 27000 Favourable

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

Standard sales price £ 35 £ 30

Actual sales price £ 45 £ 37

1

Management accounting is an approach which is used by most of the entities for the

purpose of tracking business performance and formulating future decisions. With the help of it,

the managers will be able to decide that whether they have to make changes in organisational

policies or not. There are various internal stakeholders such as employees, manager, board

members, shareholders etc. who use management reports so that they can determine that the

entity is performing properly or not (Adler, 2018). This report is based upon XLG company

which is a cleaning product entity and it is located in eastern part of Britain. There are two

different cleaning agents that are produced by the organisation These are two different chemical

which are X and Y. The competition in the industry for the enterprise is very high. Due to

lockdown because of corona virus the entity planned to move all its sales online. For this

purpose, different aspects will be analysed. These are calculation of variances such as sales price

and volume, material price planning and operational variance and analysis of merits and demerits

of using them in assessing the managers performance. Apart from this, a brief report that

assesses the decision to make famaQ in house in the UK or keep importing it from Brazil is also

prepared in this report.

PART A

1. Calculation of price and sales volume contribution variance

Given Information:

Total units sold: 1600

Material price variance: £ 27000 Favourable

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

Standard sales price £ 35 £ 30

Actual sales price £ 45 £ 37

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Standard margin £ 25 £ 20

Sales price variance:

Sales price variance is equivalent to the change between real sales at market price and

estimated sales at target price (Bromwich and Scapens, 2016). Average sales are the sum of the

units currently sold as well as the average price per unit. Similarly, actual sales at the budgeted

level match the total of the units sold and the price per unit budgeted.

Chemicals X Details Amount

Sales Price Variance ( X ) ( Actual Price – Standard Price ) * Actual Unit

= ( 45 – 35 ) * 850 8500

Favourable

Chemicals Y

Sales Price Variance ( Y ) ( Actual Price – Standard Price ) * Actual Unit

= ( 37 – 30 ) * 750 5250

Favourable

What is the total variance?

Sales volume contribution variance:

Sales Volume Variance is the calculation of benefit or expense adjustment as a result of

the discrepancy between real and budgeted volumes of revenue (Eldenburg, Krishnan and

Krishnan, 2017).

Formula:

Sales volume contribution variance = (Actual number of units sold × Budgeted price per unit)

– (budgeted number of units sold × Budgeted price per unit)

Chemicals X Details Amount

2

Sales price variance:

Sales price variance is equivalent to the change between real sales at market price and

estimated sales at target price (Bromwich and Scapens, 2016). Average sales are the sum of the

units currently sold as well as the average price per unit. Similarly, actual sales at the budgeted

level match the total of the units sold and the price per unit budgeted.

Chemicals X Details Amount

Sales Price Variance ( X ) ( Actual Price – Standard Price ) * Actual Unit

= ( 45 – 35 ) * 850 8500

Favourable

Chemicals Y

Sales Price Variance ( Y ) ( Actual Price – Standard Price ) * Actual Unit

= ( 37 – 30 ) * 750 5250

Favourable

What is the total variance?

Sales volume contribution variance:

Sales Volume Variance is the calculation of benefit or expense adjustment as a result of

the discrepancy between real and budgeted volumes of revenue (Eldenburg, Krishnan and

Krishnan, 2017).

Formula:

Sales volume contribution variance = (Actual number of units sold × Budgeted price per unit)

– (budgeted number of units sold × Budgeted price per unit)

Chemicals X Details Amount

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

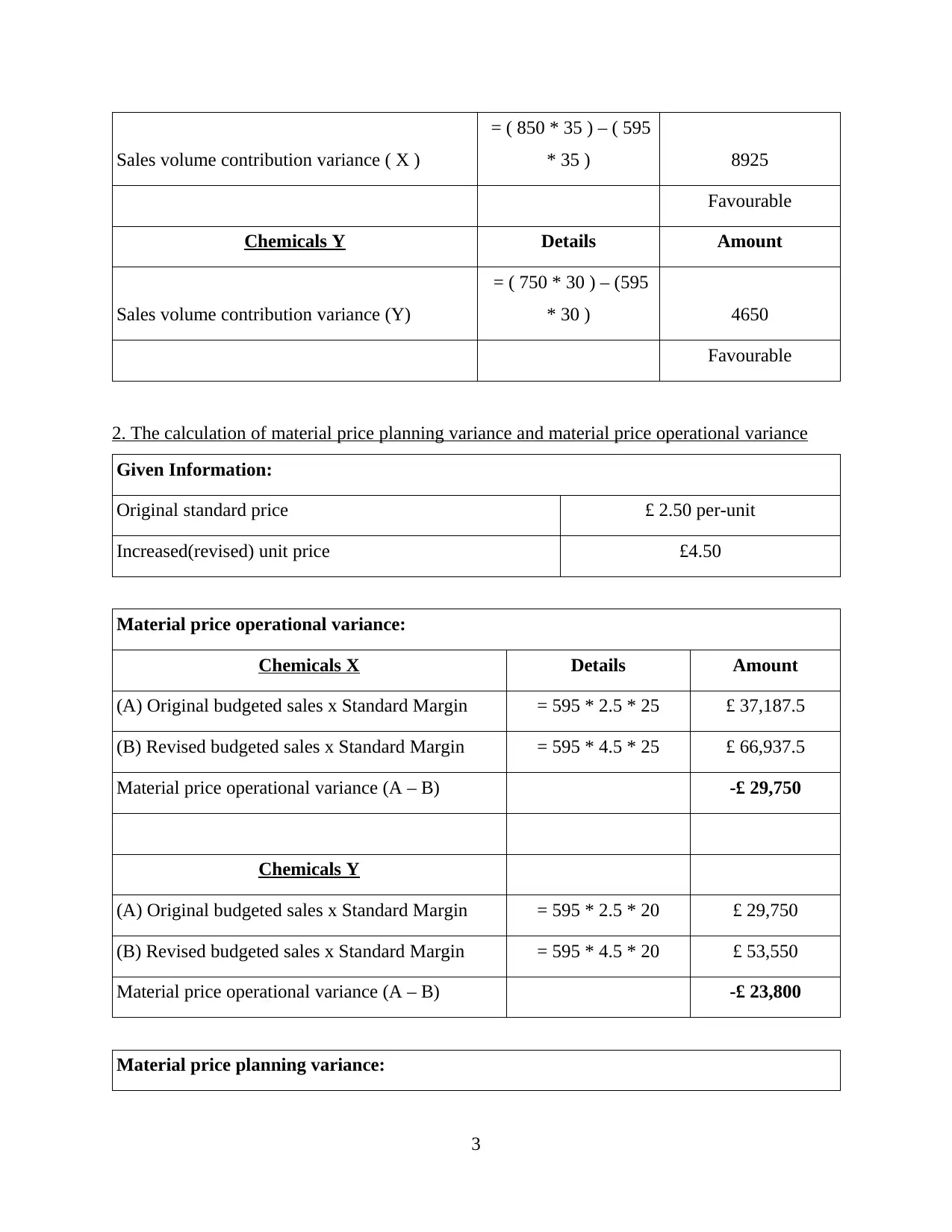

Sales volume contribution variance ( X )

= ( 850 * 35 ) – ( 595

* 35 ) 8925

Favourable

Chemicals Y Details Amount

Sales volume contribution variance (Y)

= ( 750 * 30 ) – (595

* 30 ) 4650

Favourable

2. The calculation of material price planning variance and material price operational variance

Given Information:

Original standard price £ 2.50 per-unit

Increased(revised) unit price £4.50

Material price operational variance:

Chemicals X Details Amount

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 25 £ 37,187.5

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 25 £ 66,937.5

Material price operational variance (A – B) -£ 29,750

Chemicals Y

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 20 £ 29,750

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 20 £ 53,550

Material price operational variance (A – B) -£ 23,800

Material price planning variance:

3

= ( 850 * 35 ) – ( 595

* 35 ) 8925

Favourable

Chemicals Y Details Amount

Sales volume contribution variance (Y)

= ( 750 * 30 ) – (595

* 30 ) 4650

Favourable

2. The calculation of material price planning variance and material price operational variance

Given Information:

Original standard price £ 2.50 per-unit

Increased(revised) unit price £4.50

Material price operational variance:

Chemicals X Details Amount

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 25 £ 37,187.5

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 25 £ 66,937.5

Material price operational variance (A – B) -£ 29,750

Chemicals Y

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 20 £ 29,750

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 20 £ 53,550

Material price operational variance (A – B) -£ 23,800

Material price planning variance:

3

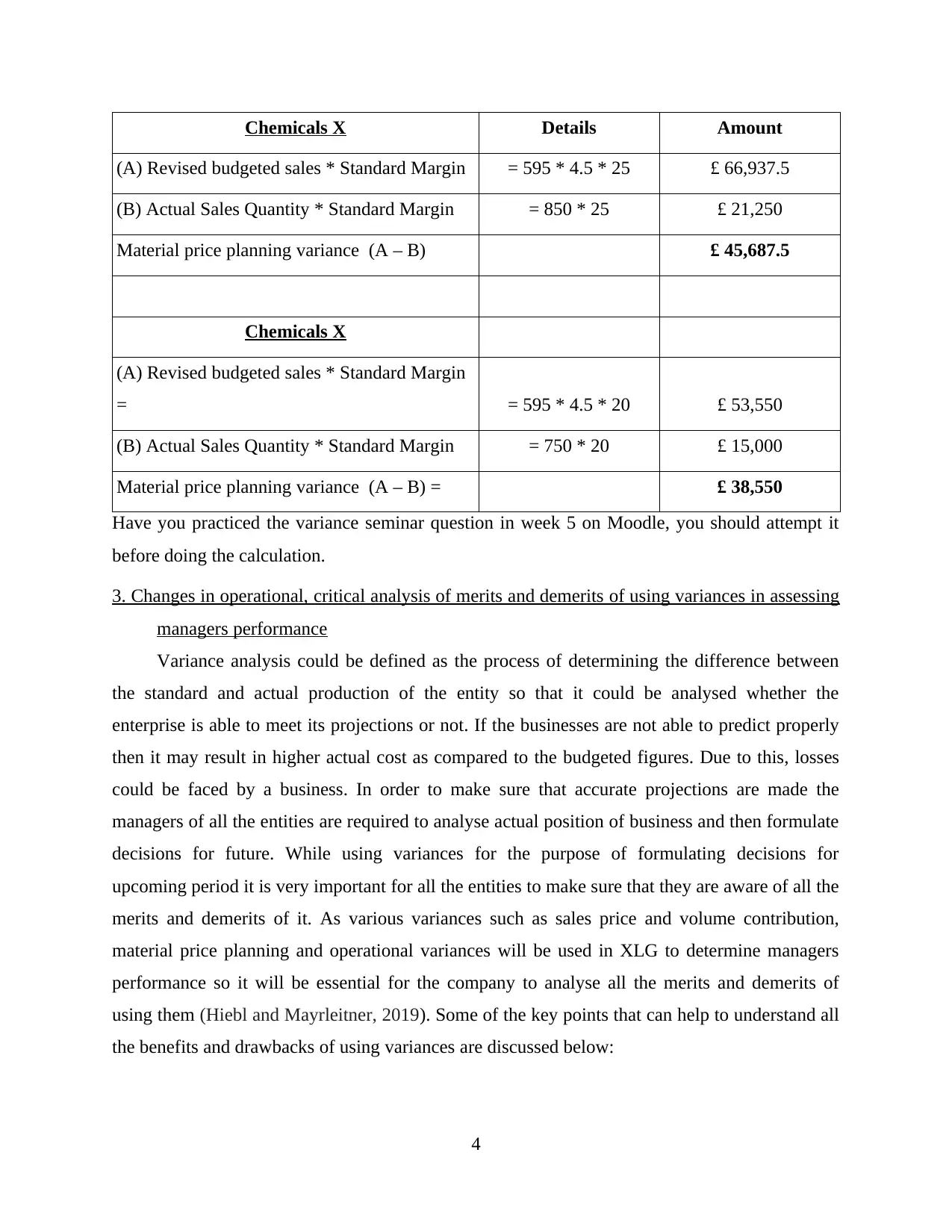

Chemicals X Details Amount

(A) Revised budgeted sales * Standard Margin = 595 * 4.5 * 25 £ 66,937.5

(B) Actual Sales Quantity * Standard Margin = 850 * 25 £ 21,250

Material price planning variance (A – B) £ 45,687.5

Chemicals X

(A) Revised budgeted sales * Standard Margin

= = 595 * 4.5 * 20 £ 53,550

(B) Actual Sales Quantity * Standard Margin = 750 * 20 £ 15,000

Material price planning variance (A – B) = £ 38,550

Have you practiced the variance seminar question in week 5 on Moodle, you should attempt it

before doing the calculation.

3. Changes in operational, critical analysis of merits and demerits of using variances in assessing

managers performance

Variance analysis could be defined as the process of determining the difference between

the standard and actual production of the entity so that it could be analysed whether the

enterprise is able to meet its projections or not. If the businesses are not able to predict properly

then it may result in higher actual cost as compared to the budgeted figures. Due to this, losses

could be faced by a business. In order to make sure that accurate projections are made the

managers of all the entities are required to analyse actual position of business and then formulate

decisions for future. While using variances for the purpose of formulating decisions for

upcoming period it is very important for all the entities to make sure that they are aware of all the

merits and demerits of it. As various variances such as sales price and volume contribution,

material price planning and operational variances will be used in XLG to determine managers

performance so it will be essential for the company to analyse all the merits and demerits of

using them (Hiebl and Mayrleitner, 2019). Some of the key points that can help to understand all

the benefits and drawbacks of using variances are discussed below:

4

(A) Revised budgeted sales * Standard Margin = 595 * 4.5 * 25 £ 66,937.5

(B) Actual Sales Quantity * Standard Margin = 850 * 25 £ 21,250

Material price planning variance (A – B) £ 45,687.5

Chemicals X

(A) Revised budgeted sales * Standard Margin

= = 595 * 4.5 * 20 £ 53,550

(B) Actual Sales Quantity * Standard Margin = 750 * 20 £ 15,000

Material price planning variance (A – B) = £ 38,550

Have you practiced the variance seminar question in week 5 on Moodle, you should attempt it

before doing the calculation.

3. Changes in operational, critical analysis of merits and demerits of using variances in assessing

managers performance

Variance analysis could be defined as the process of determining the difference between

the standard and actual production of the entity so that it could be analysed whether the

enterprise is able to meet its projections or not. If the businesses are not able to predict properly

then it may result in higher actual cost as compared to the budgeted figures. Due to this, losses

could be faced by a business. In order to make sure that accurate projections are made the

managers of all the entities are required to analyse actual position of business and then formulate

decisions for future. While using variances for the purpose of formulating decisions for

upcoming period it is very important for all the entities to make sure that they are aware of all the

merits and demerits of it. As various variances such as sales price and volume contribution,

material price planning and operational variances will be used in XLG to determine managers

performance so it will be essential for the company to analyse all the merits and demerits of

using them (Hiebl and Mayrleitner, 2019). Some of the key points that can help to understand all

the benefits and drawbacks of using variances are discussed below:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Merits of using variances: When variances will be used by entities for evaluating

managers performance and other purposes then it may result in various merits. All of them are as

follows:

Controlling expenses: Variance analysis plays a vital role in controlling the expenses

because when the results of variances will be adverse then the managers can take

appropriate decisions for controlling the negative situation. In order to work properly the

managers, try to find the explanation for the adverse results then they take controlling

related actions so that they can improve the performance of business. In case of XLG

company the actual sale is very high because of the higher demand which has resulted in

the adverse variance. In order to deal with this situation, the managers could have

purchased more material than the standard one as it would have resulted in favourable

variance (Ismail et.al., 2018).

Evaluating performance: Variance analysis is used for the purpose of evaluating

performance of business by analysing that the actual results are compatible with the

budgeted figures or not. It also helps to analyse the performance of controlling managers

because when the variances results are favourable, it reflect good performance. When the

results are adverse then it will reflect that the managers have not made efforts in making

decisions or estimations correctly. How can you relate this to XLG’s variance

calculations?

Analysis of accountability: With the help of variance analysis or the calculations a

system of accountability within the organisation could be established. If a manager takes

action in the future, then it will be the main responsibility to be accountable for the same

so that their performance could be analysed. It will also be very important for them to

take responsibility if the results are adverse. If the level of accountability will be low in

XLG then it will demonstrate the weak performance of the managers.

Adjusting budgeted estimations: Variance analysis facilitate the adjustment of budget

estimations. When the reason for the adverse variance will be wrong estimation in

standard figures then the estimations will be corrected and adjusted. If the managers will

be highly involved in this procedure, then it will help to evaluate their performance easily

and enhance performance of business. It is one of the main merits of using variances for

5

managers performance and other purposes then it may result in various merits. All of them are as

follows:

Controlling expenses: Variance analysis plays a vital role in controlling the expenses

because when the results of variances will be adverse then the managers can take

appropriate decisions for controlling the negative situation. In order to work properly the

managers, try to find the explanation for the adverse results then they take controlling

related actions so that they can improve the performance of business. In case of XLG

company the actual sale is very high because of the higher demand which has resulted in

the adverse variance. In order to deal with this situation, the managers could have

purchased more material than the standard one as it would have resulted in favourable

variance (Ismail et.al., 2018).

Evaluating performance: Variance analysis is used for the purpose of evaluating

performance of business by analysing that the actual results are compatible with the

budgeted figures or not. It also helps to analyse the performance of controlling managers

because when the variances results are favourable, it reflect good performance. When the

results are adverse then it will reflect that the managers have not made efforts in making

decisions or estimations correctly. How can you relate this to XLG’s variance

calculations?

Analysis of accountability: With the help of variance analysis or the calculations a

system of accountability within the organisation could be established. If a manager takes

action in the future, then it will be the main responsibility to be accountable for the same

so that their performance could be analysed. It will also be very important for them to

take responsibility if the results are adverse. If the level of accountability will be low in

XLG then it will demonstrate the weak performance of the managers.

Adjusting budgeted estimations: Variance analysis facilitate the adjustment of budget

estimations. When the reason for the adverse variance will be wrong estimation in

standard figures then the estimations will be corrected and adjusted. If the managers will

be highly involved in this procedure, then it will help to evaluate their performance easily

and enhance performance of business. It is one of the main merits of using variances for

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the purpose of evaluating performance of the managers in XLG (Maas, Schaltegger and

Crutzen, 2016). Can you relate this to the increased demand of chemical X and Y?

Setting system for roles and responsibilities within the enterprise: Variance analysis

is used to set a system so that all the roles and responsibilities could be assigned to staff

members properly. With the help of it, the senior managers can determine ability of all

the manages and then set the system which will help to meet the future goals and

objectives in long run. With the help of it, controls and efficiency within the entity could

be improved and enhanced. Can you relate this to XLG?

Demerits of using variances: There are various types of disadvantages of variances for

XLG company. All of them could be analysed with the help of following discussion:

Time consuming process: Variance analysis is a time-consuming process which takes

too much time to analyse the organisational as well as managerial performance. Due to

this, the senior authority of the organisations are not able to analyse the performance of

managers on time and formulate specific policies for betterment of business. Apart form

this, the calculation of variances diverts the focus from improved performance of

business to assessment of actual business activities which may result in issues in future.

From assessing actual performance, you would know if there is improved performance or

not, you need to be a bit clear on this. Also can you apply it to XLG?

Delayed corrective actions: When the top-level authorities of the organisation will not

be able to determine that whether the managers or company are performing well or not in

time then it will also affect the action taking procedures. It will result in delayed

corrective actions because the top-level executives will not be able to take right decisions

on right time. Due to this, the possibility of decreased performance of business could be

increased which will leave negative implications upon the attainment of all the long-term

goals and objectives (Matsuoka, 2020). Can you relate this to XLG?

Non standardisation production: If an entity is operating under service sector then it

will be very difficult for it to apply variance analysis. As XLG is planning to go online so

it will also be a part of service industry and there will be increased overhead costs so it

may also create difficulties for the business. While taking the sales online it will be very

important for the managers of the enterprise to make sure that they are able to analyse

6

Crutzen, 2016). Can you relate this to the increased demand of chemical X and Y?

Setting system for roles and responsibilities within the enterprise: Variance analysis

is used to set a system so that all the roles and responsibilities could be assigned to staff

members properly. With the help of it, the senior managers can determine ability of all

the manages and then set the system which will help to meet the future goals and

objectives in long run. With the help of it, controls and efficiency within the entity could

be improved and enhanced. Can you relate this to XLG?

Demerits of using variances: There are various types of disadvantages of variances for

XLG company. All of them could be analysed with the help of following discussion:

Time consuming process: Variance analysis is a time-consuming process which takes

too much time to analyse the organisational as well as managerial performance. Due to

this, the senior authority of the organisations are not able to analyse the performance of

managers on time and formulate specific policies for betterment of business. Apart form

this, the calculation of variances diverts the focus from improved performance of

business to assessment of actual business activities which may result in issues in future.

From assessing actual performance, you would know if there is improved performance or

not, you need to be a bit clear on this. Also can you apply it to XLG?

Delayed corrective actions: When the top-level authorities of the organisation will not

be able to determine that whether the managers or company are performing well or not in

time then it will also affect the action taking procedures. It will result in delayed

corrective actions because the top-level executives will not be able to take right decisions

on right time. Due to this, the possibility of decreased performance of business could be

increased which will leave negative implications upon the attainment of all the long-term

goals and objectives (Matsuoka, 2020). Can you relate this to XLG?

Non standardisation production: If an entity is operating under service sector then it

will be very difficult for it to apply variance analysis. As XLG is planning to go online so

it will also be a part of service industry and there will be increased overhead costs so it

may also create difficulties for the business. While taking the sales online it will be very

important for the managers of the enterprise to make sure that they are able to analyse

6

variances properly as it will show their ability to perform their jobs properly. Going

online doesn’t automatically make XLG a service business, remember it actually has

tangible goods (chemical X and Y) which service businesses don’t have.

Behavioural issues: variance analysis may result in short-termism because of the

inherent tendency of it against the quantified and short-term objectives as well as results.

Apart from this, if there will be negative perception about it then it will encourage the sub

optimal behaviour among the employees. One of the examples of it is attempting to

incorporate budget slacks. It is one of the main demerits of using variance analysis for the

purpose of determining that managers are performing well or not (Tekathen, 2019). Can

you relate this to XLG?

PART B

Report assessing the decision to make famaQ in house in the UK to keep importing it from

Brazil

XLG is a chemical company which is operating its business in United Kingdom and some

other locations in Europe. The market in which it is carrying out operations is very competitive

and one of the main chemicals that provides it competitive advantage is famaQ which is

imported from Brazil. In the second quarter of March month of 2020 the nationwide lockdown

took place and it was enforced by the legal authorities of United Kingdom. Due to this, pandemic

the entity planned to move its sales online so that it can deal with all the challenges that are

taking place because of lockdown. As one of the main chemicals which is used by the

organisation to make the final product is imported from Brazil so it may result in problems for

carrying out business in systematic manner. It will be very important for the company to make

sure that it deals with all the negative implications which could be resulted due to this. For XLG

it will be more expensive to import famaQ from Brazil because of Lockdown. Apart from this, if

it will be imported then it may result in various risks. These are increased possibility of

spreading the corona virus, higher delivery time, increased cost etc. Apart from this, if it will not

be imported then it may result is decreased competitive advantage because the main chemical

that helps XLG maintain competitive advantage is famaQ (Van der Stede, 2016). Additionally, it

has been estimated that the demand for chemical X and Y will be increased by 45% and it will

likely continue according to market research. One of the main solutions which could be focused

7

online doesn’t automatically make XLG a service business, remember it actually has

tangible goods (chemical X and Y) which service businesses don’t have.

Behavioural issues: variance analysis may result in short-termism because of the

inherent tendency of it against the quantified and short-term objectives as well as results.

Apart from this, if there will be negative perception about it then it will encourage the sub

optimal behaviour among the employees. One of the examples of it is attempting to

incorporate budget slacks. It is one of the main demerits of using variance analysis for the

purpose of determining that managers are performing well or not (Tekathen, 2019). Can

you relate this to XLG?

PART B

Report assessing the decision to make famaQ in house in the UK to keep importing it from

Brazil

XLG is a chemical company which is operating its business in United Kingdom and some

other locations in Europe. The market in which it is carrying out operations is very competitive

and one of the main chemicals that provides it competitive advantage is famaQ which is

imported from Brazil. In the second quarter of March month of 2020 the nationwide lockdown

took place and it was enforced by the legal authorities of United Kingdom. Due to this, pandemic

the entity planned to move its sales online so that it can deal with all the challenges that are

taking place because of lockdown. As one of the main chemicals which is used by the

organisation to make the final product is imported from Brazil so it may result in problems for

carrying out business in systematic manner. It will be very important for the company to make

sure that it deals with all the negative implications which could be resulted due to this. For XLG

it will be more expensive to import famaQ from Brazil because of Lockdown. Apart from this, if

it will be imported then it may result in various risks. These are increased possibility of

spreading the corona virus, higher delivery time, increased cost etc. Apart from this, if it will not

be imported then it may result is decreased competitive advantage because the main chemical

that helps XLG maintain competitive advantage is famaQ (Van der Stede, 2016). Additionally, it

has been estimated that the demand for chemical X and Y will be increased by 45% and it will

likely continue according to market research. One of the main solutions which could be focused

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by the organisation is making the famaQ in UK so that it can meet the market demand. If it will

be manufactured within United Kingdom then the delivery time will be reduced by 15 working

days which means the entity can start its production early. Apart from this, the per unit cost of

manufacturing famaQ in UK will be 3 pounds which is low as compared to the imported cost

which is 3.7 pounds per unit. It shows that the organisation should make famaQ in UK rather

than importing it from Brazil as it will result in various benefits for business. Some of the key

benefits of it are as follows:

When famaQ will be imported then it will facilitate the business as the cost of

manufacturing is very low as compared to the imported cost.

The delivery time will be reduced by 15 days which can help to start the production

earlier and meet the market demand.

The possibility of spreading corona virus will be nil if the famaQ chemical will be

manufactured rather than importing it from Brazil.

In Lockdown it will be very difficult to import goods so making famaQ in United

Kingdom is right choice for carrying out all the operations in systematic manner in

future.

By analysing all the above aspects, risks from importing and benefits of making famaQ in

UK it has been analysed that XLG should manufacture the chemical in UK rather than importing

it from Brazil as it will be beneficial for growth and development of business (Van der Stede,

2017).

You need to also consider the various costs of manufacturing in the UK, such as setting

up a manufacturing plant etc,

You need to consider both advantages and disadvantages of setting up manufacturing in

the UK or importing it and then make an informed decision.

You made no mention of relevant costing, you need to briefly describe it.

Use headings to separate your point, don’t just keep everything together.

CONCLUSION

The above project report concludes that management accounting is an approach which is

used by internal stakeholders for the purpose of assessing actual position of business. While

planning to make strategic decisions for future it will be very important for all the organisations

to make sure that they are using effective techniques. One of them is variance analysis. With the

8

be manufactured within United Kingdom then the delivery time will be reduced by 15 working

days which means the entity can start its production early. Apart from this, the per unit cost of

manufacturing famaQ in UK will be 3 pounds which is low as compared to the imported cost

which is 3.7 pounds per unit. It shows that the organisation should make famaQ in UK rather

than importing it from Brazil as it will result in various benefits for business. Some of the key

benefits of it are as follows:

When famaQ will be imported then it will facilitate the business as the cost of

manufacturing is very low as compared to the imported cost.

The delivery time will be reduced by 15 days which can help to start the production

earlier and meet the market demand.

The possibility of spreading corona virus will be nil if the famaQ chemical will be

manufactured rather than importing it from Brazil.

In Lockdown it will be very difficult to import goods so making famaQ in United

Kingdom is right choice for carrying out all the operations in systematic manner in

future.

By analysing all the above aspects, risks from importing and benefits of making famaQ in

UK it has been analysed that XLG should manufacture the chemical in UK rather than importing

it from Brazil as it will be beneficial for growth and development of business (Van der Stede,

2017).

You need to also consider the various costs of manufacturing in the UK, such as setting

up a manufacturing plant etc,

You need to consider both advantages and disadvantages of setting up manufacturing in

the UK or importing it and then make an informed decision.

You made no mention of relevant costing, you need to briefly describe it.

Use headings to separate your point, don’t just keep everything together.

CONCLUSION

The above project report concludes that management accounting is an approach which is

used by internal stakeholders for the purpose of assessing actual position of business. While

planning to make strategic decisions for future it will be very important for all the organisations

to make sure that they are using effective techniques. One of them is variance analysis. With the

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

help of it, actual performance of business as well as the managers could be determined. While

using it, it will be very important to be aware of all its merits and demerits so that effective

decisions by using it could be formulated for future.

9

using it, it will be very important to be aware of all its merits and demerits so that effective

decisions by using it could be formulated for future.

9

REFERENCES

Books and Journals:

Adler, R. W., 2018. Strategic performance management: Accounting for organizational control.

Taylor & Francis.

Bromwich, M. and Scapens, R. W., 2016. Management accounting research: 25 years

on. Management Accounting Research. 31. pp.1-9.

Eldenburg, L. G., Krishnan, H. A. and Krishnan, R., 2017. Management accounting and control

in the hospital industry: A review. Journal of Governmental & Nonprofit Accounting.

6(1). pp.52-91.

Hiebl, M. R. and Mayrleitner, B., 2019. Professionalization of management accounting in family

firms: the impact of family members. Review of Managerial Science. 13(5). pp.1037-

1068.

Ismail, K., Isa, C. R. and Mia, L., 2018. Market competition, lean manufacturing practices and

the role of management accounting systems (MAS) information. Jurnal Pengurusan

(UKM Journal of Management). 52.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

Matsuoka, K., 2020. Exploring the interface between management accounting and marketing: a

literature review of customer accounting. Journal of Management Control. pp.1-52.

Tekathen, M., 2019. Unpacking the Fluidity of Management Accounting Concepts: An

Ethnographic Social Site Analysis of Enterprise Risk Management. European

Accounting Review. 28(5). pp.977-1010.

Van der Stede, W. A., 2016. Management accounting in context: Industry, regulation and

informatics. Management Accounting Research. 31. pp.100-102.

Van der Stede, W. A., 2017. “Global” management accounting research: some

reflections. Journal of International Accounting Research. 16(2). pp.1-8.

10

Books and Journals:

Adler, R. W., 2018. Strategic performance management: Accounting for organizational control.

Taylor & Francis.

Bromwich, M. and Scapens, R. W., 2016. Management accounting research: 25 years

on. Management Accounting Research. 31. pp.1-9.

Eldenburg, L. G., Krishnan, H. A. and Krishnan, R., 2017. Management accounting and control

in the hospital industry: A review. Journal of Governmental & Nonprofit Accounting.

6(1). pp.52-91.

Hiebl, M. R. and Mayrleitner, B., 2019. Professionalization of management accounting in family

firms: the impact of family members. Review of Managerial Science. 13(5). pp.1037-

1068.

Ismail, K., Isa, C. R. and Mia, L., 2018. Market competition, lean manufacturing practices and

the role of management accounting systems (MAS) information. Jurnal Pengurusan

(UKM Journal of Management). 52.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136.

pp.237-248.

Matsuoka, K., 2020. Exploring the interface between management accounting and marketing: a

literature review of customer accounting. Journal of Management Control. pp.1-52.

Tekathen, M., 2019. Unpacking the Fluidity of Management Accounting Concepts: An

Ethnographic Social Site Analysis of Enterprise Risk Management. European

Accounting Review. 28(5). pp.977-1010.

Van der Stede, W. A., 2016. Management accounting in context: Industry, regulation and

informatics. Management Accounting Research. 31. pp.100-102.

Van der Stede, W. A., 2017. “Global” management accounting research: some

reflections. Journal of International Accounting Research. 16(2). pp.1-8.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.