Variance Analysis in Management Accounting

Added on 2023-01-09

12 Pages3302 Words69 Views

LCBB5002

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

1. Calculation of price and sales volume contribution variance..................................................1

2. The calculation of material price planning variance and material price operational variance 3

3. Changes in operational, critical analysis of merits and demerits of using variances in

assessing managers performance.................................................................................................4

PART B...........................................................................................................................................7

Report assessing the decision to make famaQ in house in the UK to keep importing it from

Brazil............................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

PART A...........................................................................................................................................1

1. Calculation of price and sales volume contribution variance..................................................1

2. The calculation of material price planning variance and material price operational variance 3

3. Changes in operational, critical analysis of merits and demerits of using variances in

assessing managers performance.................................................................................................4

PART B...........................................................................................................................................7

Report assessing the decision to make famaQ in house in the UK to keep importing it from

Brazil............................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

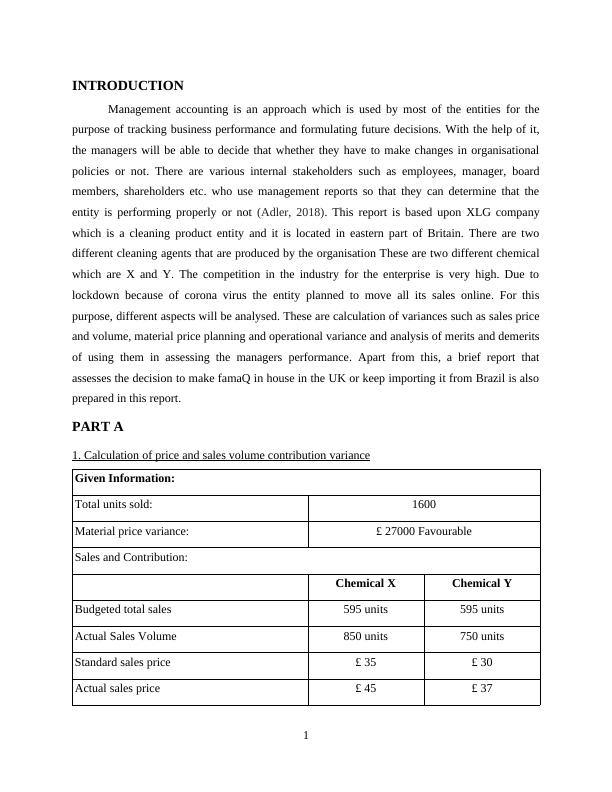

INTRODUCTION

Management accounting is an approach which is used by most of the entities for the

purpose of tracking business performance and formulating future decisions. With the help of it,

the managers will be able to decide that whether they have to make changes in organisational

policies or not. There are various internal stakeholders such as employees, manager, board

members, shareholders etc. who use management reports so that they can determine that the

entity is performing properly or not (Adler, 2018). This report is based upon XLG company

which is a cleaning product entity and it is located in eastern part of Britain. There are two

different cleaning agents that are produced by the organisation These are two different chemical

which are X and Y. The competition in the industry for the enterprise is very high. Due to

lockdown because of corona virus the entity planned to move all its sales online. For this

purpose, different aspects will be analysed. These are calculation of variances such as sales price

and volume, material price planning and operational variance and analysis of merits and demerits

of using them in assessing the managers performance. Apart from this, a brief report that

assesses the decision to make famaQ in house in the UK or keep importing it from Brazil is also

prepared in this report.

PART A

1. Calculation of price and sales volume contribution variance

Given Information:

Total units sold: 1600

Material price variance: £ 27000 Favourable

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

Standard sales price £ 35 £ 30

Actual sales price £ 45 £ 37

1

Management accounting is an approach which is used by most of the entities for the

purpose of tracking business performance and formulating future decisions. With the help of it,

the managers will be able to decide that whether they have to make changes in organisational

policies or not. There are various internal stakeholders such as employees, manager, board

members, shareholders etc. who use management reports so that they can determine that the

entity is performing properly or not (Adler, 2018). This report is based upon XLG company

which is a cleaning product entity and it is located in eastern part of Britain. There are two

different cleaning agents that are produced by the organisation These are two different chemical

which are X and Y. The competition in the industry for the enterprise is very high. Due to

lockdown because of corona virus the entity planned to move all its sales online. For this

purpose, different aspects will be analysed. These are calculation of variances such as sales price

and volume, material price planning and operational variance and analysis of merits and demerits

of using them in assessing the managers performance. Apart from this, a brief report that

assesses the decision to make famaQ in house in the UK or keep importing it from Brazil is also

prepared in this report.

PART A

1. Calculation of price and sales volume contribution variance

Given Information:

Total units sold: 1600

Material price variance: £ 27000 Favourable

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

Standard sales price £ 35 £ 30

Actual sales price £ 45 £ 37

1

Standard margin £ 25 £ 20

Sales price variance:

Sales price variance is equivalent to the change between real sales at market price and

estimated sales at target price (Bromwich and Scapens, 2016). Average sales are the sum of the

units currently sold as well as the average price per unit. Similarly, actual sales at the budgeted

level match the total of the units sold and the price per unit budgeted.

Chemicals X Details Amount

Sales Price Variance ( X ) ( Actual Price – Standard Price ) * Actual Unit

= ( 45 – 35 ) * 850 8500

Favourable

Chemicals Y

Sales Price Variance ( Y ) ( Actual Price – Standard Price ) * Actual Unit

= ( 37 – 30 ) * 750 5250

Favourable

What is the total variance?

Sales volume contribution variance:

Sales Volume Variance is the calculation of benefit or expense adjustment as a result of

the discrepancy between real and budgeted volumes of revenue (Eldenburg, Krishnan and

Krishnan, 2017).

Formula:

Sales volume contribution variance = (Actual number of units sold × Budgeted price per unit)

– (budgeted number of units sold × Budgeted price per unit)

Chemicals X Details Amount

2

Sales price variance:

Sales price variance is equivalent to the change between real sales at market price and

estimated sales at target price (Bromwich and Scapens, 2016). Average sales are the sum of the

units currently sold as well as the average price per unit. Similarly, actual sales at the budgeted

level match the total of the units sold and the price per unit budgeted.

Chemicals X Details Amount

Sales Price Variance ( X ) ( Actual Price – Standard Price ) * Actual Unit

= ( 45 – 35 ) * 850 8500

Favourable

Chemicals Y

Sales Price Variance ( Y ) ( Actual Price – Standard Price ) * Actual Unit

= ( 37 – 30 ) * 750 5250

Favourable

What is the total variance?

Sales volume contribution variance:

Sales Volume Variance is the calculation of benefit or expense adjustment as a result of

the discrepancy between real and budgeted volumes of revenue (Eldenburg, Krishnan and

Krishnan, 2017).

Formula:

Sales volume contribution variance = (Actual number of units sold × Budgeted price per unit)

– (budgeted number of units sold × Budgeted price per unit)

Chemicals X Details Amount

2

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting: Calculation of Variances and Evaluation of Manager's Performancelg...

|11

|3101

|70

Management Accounting and Variance Analysis in XLG Companylg...

|12

|3086

|40

MANAGEMENT ACCOUNTING - REPORTlg...

|12

|3134

|71

Management Accounting: Sales Price Variance, Material Price Variance, and Performance Evaluationlg...

|15

|3285

|47

Variance in Assessing Performance and Decision Makinglg...

|15

|3344

|66

Management Accounting: Computation of Variances and Make-or-Buy Decisionlg...

|13

|3368

|73