Management Accounting: Sales Price and Volume Variances, Material Price Variances, and Analysis of Variances

VerifiedAdded on 2023/01/07

|14

|3328

|40

AI Summary

This article discusses the computation of sales price variances, sales volume contribution variances, material price planning variance, and material price operational variance. It also analyzes the merits and demerits of using variances in determining managers' performance. The case study focuses on the make-or-buy decision for XLG organization.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................4

PART A...........................................................................................................................................4

(i) Computation of the Sales price variances and sales volume contribution variances:............4

(ii). Computation of material price planning variance and material price operational variance: 6

(iii). Comprehend analysis of all substantial merits and demerits linked with variances use in

determining managers’ performance:..........................................................................................8

PART B.........................................................................................................................................11

CONCLUSION.............................................................................................................................14

REFERENCES..............................................................................................................................15

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................4

PART A...........................................................................................................................................4

(i) Computation of the Sales price variances and sales volume contribution variances:............4

(ii). Computation of material price planning variance and material price operational variance: 6

(iii). Comprehend analysis of all substantial merits and demerits linked with variances use in

determining managers’ performance:..........................................................................................8

PART B.........................................................................................................................................11

CONCLUSION.............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

In today 's changing industrialized setting, management accounting framework is

becoming a valuable component of business, managerial accounting guides and supports

management at every level (Zhuo, W., Shao and Yang, 2018). Management accounting as a

whole not only enhances the financial efficacy but also strengthens the efficiency of personnel.

Accounting management boosts the corporation 's competitive capabilities. The goals of the

multiple divisions and departments are outlined in depth, and the attainment of such targets is

employed as a benchmark for assessing their performance. This study deals extensively with

pivotal merits and also demerits of usage of the variances in evaluating business managers'

efficiency and performance. There are also quantitative tasks related to the measurement of

various variances, such as variances in sales price, variances in contribution sales volume,

variances in operational material price and variance in materials price planning. In addition, the

report consisting of debate on role of making or buying decisions focused on XLG business's

case-study.

PART A

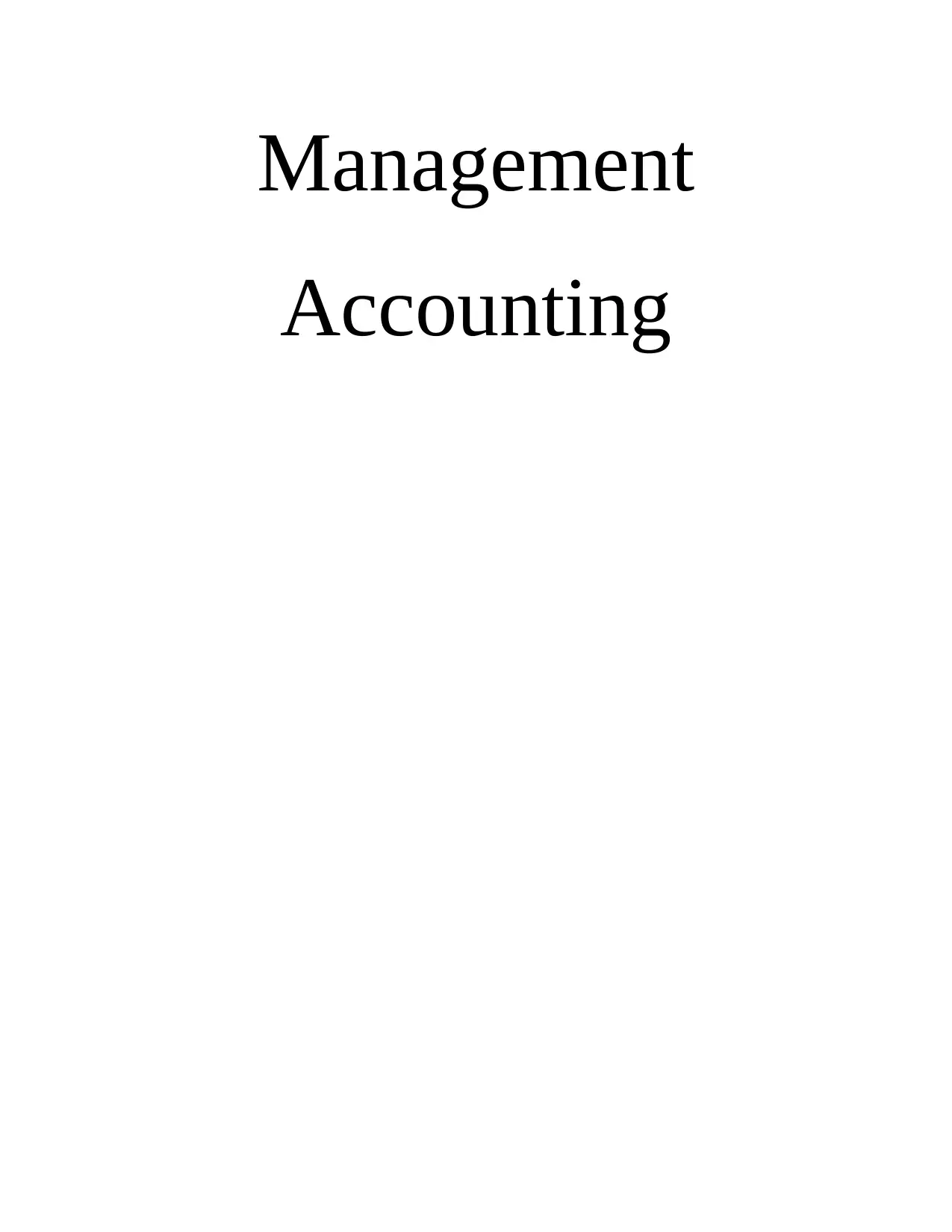

(i) Computation of the Sales price variances and sales volume contribution variances:

Sales price variance: The sale price variance implies difference among actual and the projected

revenue arising from a shift in price of product. The equation is as follows:

Sales price variance = (Actual Price – Standard Price) * Actual Unit

The adverse variance means that actual price is smaller than estimated budgeted price,

whereas favourable variance is result of reverse conditions. budgeted/estimated price for

every product or unit shall be calculated by sales and marketing executives and shall be focused

on their estimate of the potential demand for such goods and services, that, in effect, will be

influenced by common economic circumstances and the acts of the rivals.

In today 's changing industrialized setting, management accounting framework is

becoming a valuable component of business, managerial accounting guides and supports

management at every level (Zhuo, W., Shao and Yang, 2018). Management accounting as a

whole not only enhances the financial efficacy but also strengthens the efficiency of personnel.

Accounting management boosts the corporation 's competitive capabilities. The goals of the

multiple divisions and departments are outlined in depth, and the attainment of such targets is

employed as a benchmark for assessing their performance. This study deals extensively with

pivotal merits and also demerits of usage of the variances in evaluating business managers'

efficiency and performance. There are also quantitative tasks related to the measurement of

various variances, such as variances in sales price, variances in contribution sales volume,

variances in operational material price and variance in materials price planning. In addition, the

report consisting of debate on role of making or buying decisions focused on XLG business's

case-study.

PART A

(i) Computation of the Sales price variances and sales volume contribution variances:

Sales price variance: The sale price variance implies difference among actual and the projected

revenue arising from a shift in price of product. The equation is as follows:

Sales price variance = (Actual Price – Standard Price) * Actual Unit

The adverse variance means that actual price is smaller than estimated budgeted price,

whereas favourable variance is result of reverse conditions. budgeted/estimated price for

every product or unit shall be calculated by sales and marketing executives and shall be focused

on their estimate of the potential demand for such goods and services, that, in effect, will be

influenced by common economic circumstances and the acts of the rivals.

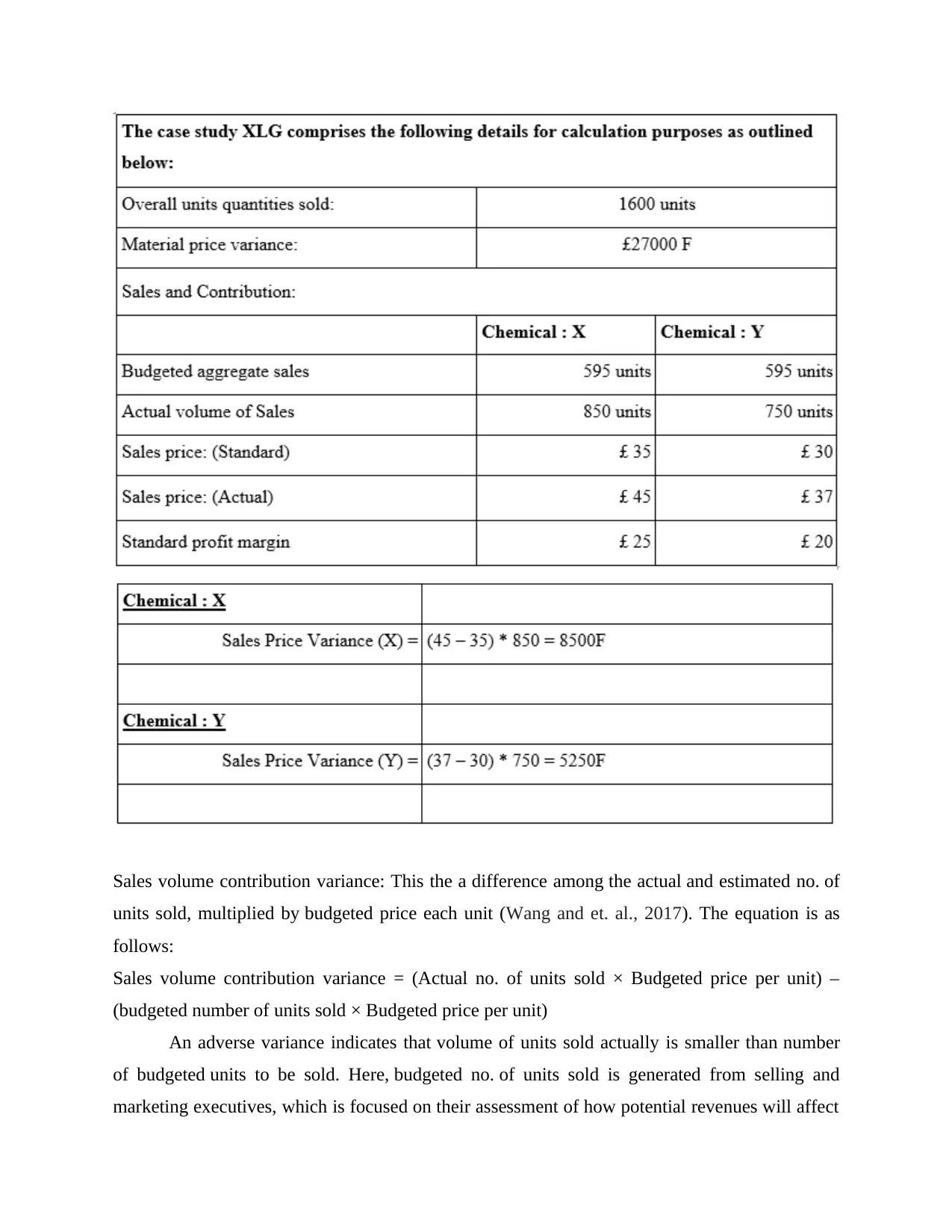

Sales volume contribution variance: This the a difference among the actual and estimated no. of

units sold, multiplied by budgeted price each unit (Wang and et. al., 2017). The equation is as

follows:

Sales volume contribution variance = (Actual no. of units sold × Budgeted price per unit) –

(budgeted number of units sold × Budgeted price per unit)

An adverse variance indicates that volume of units sold actually is smaller than number

of budgeted units to be sold. Here, budgeted no. of units sold is generated from selling and

marketing executives, which is focused on their assessment of how potential revenues will affect

units sold, multiplied by budgeted price each unit (Wang and et. al., 2017). The equation is as

follows:

Sales volume contribution variance = (Actual no. of units sold × Budgeted price per unit) –

(budgeted number of units sold × Budgeted price per unit)

An adverse variance indicates that volume of units sold actually is smaller than number

of budgeted units to be sold. Here, budgeted no. of units sold is generated from selling and

marketing executives, which is focused on their assessment of how potential revenues will affect

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

the corporation 's product market sharing, features, price ranges, planned marketing efforts,

distribution networks which revenues in new areas. If selling price of the commodity is smaller

than the sum budgeted, this will stimulate sales to quite an extent that variance in sell volume is

favourable, even if variance in sell price is adverse.

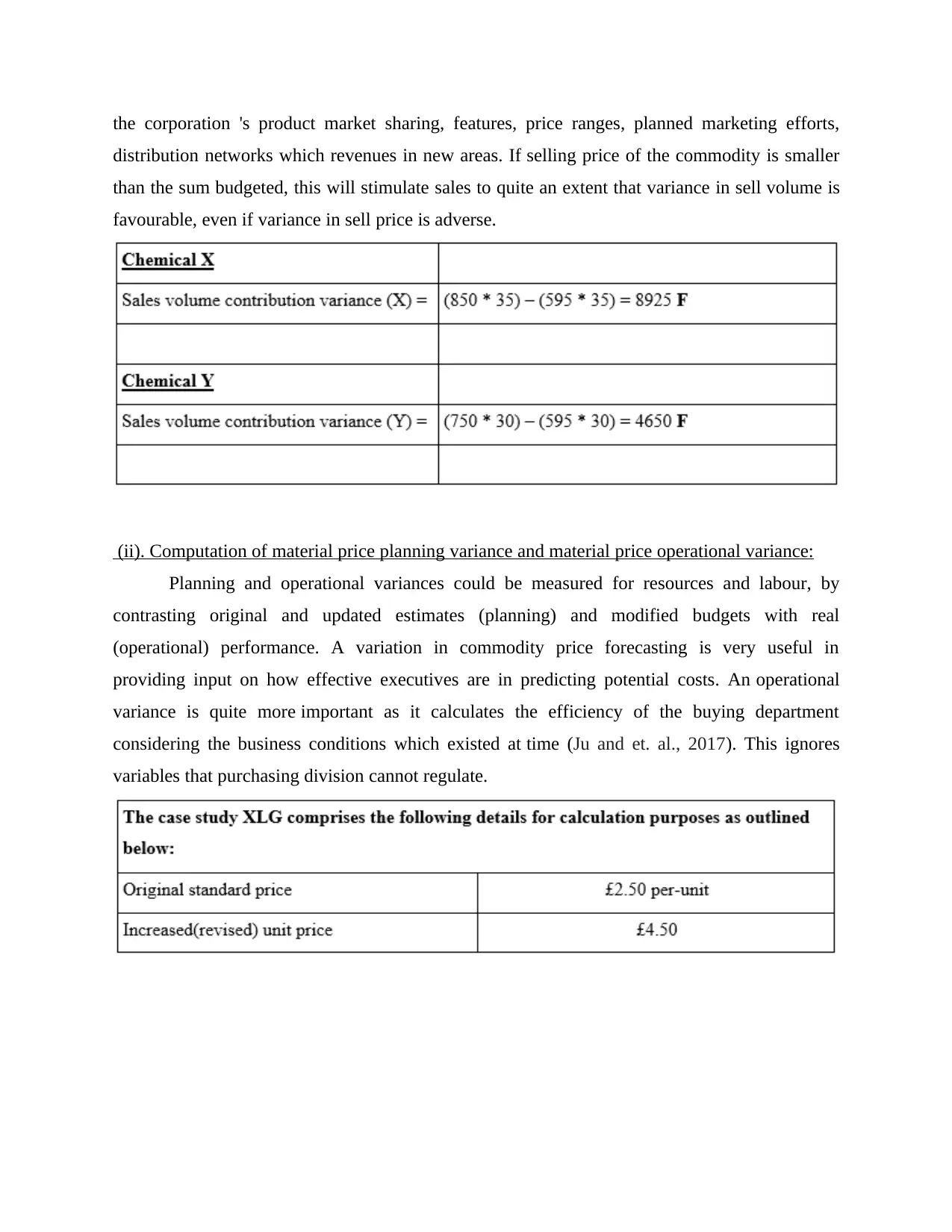

(ii). Computation of material price planning variance and material price operational variance:

Planning and operational variances could be measured for resources and labour, by

contrasting original and updated estimates (planning) and modified budgets with real

(operational) performance. A variation in commodity price forecasting is very useful in

providing input on how effective executives are in predicting potential costs. An operational

variance is quite more important as it calculates the efficiency of the buying department

considering the business conditions which existed at time (Ju and et. al., 2017). This ignores

variables that purchasing division cannot regulate.

distribution networks which revenues in new areas. If selling price of the commodity is smaller

than the sum budgeted, this will stimulate sales to quite an extent that variance in sell volume is

favourable, even if variance in sell price is adverse.

(ii). Computation of material price planning variance and material price operational variance:

Planning and operational variances could be measured for resources and labour, by

contrasting original and updated estimates (planning) and modified budgets with real

(operational) performance. A variation in commodity price forecasting is very useful in

providing input on how effective executives are in predicting potential costs. An operational

variance is quite more important as it calculates the efficiency of the buying department

considering the business conditions which existed at time (Ju and et. al., 2017). This ignores

variables that purchasing division cannot regulate.

(iii). Comprehend analysis of all substantial merits and demerits linked with variances use in

determining managers’ performance:

Analysis of variances is the review of differences in conventional costing method items.

This is analysis and evaluation of all variables which induced the discrepancies among the

standards/targets established and actual outcomes, with the target of minimizing deficiencies.

The review of variances suggests capabilities and major indices but doesn't really specify what

action, if any, ought to be undertaken. Until they could execute control steps the administrators

should be provided to appropriately characterize the true sense of different-different variances.

Cost reduction and Cost control are the major objective which is performed in the activity of

variance analysis. It plays an important role in costing on which efficiency is to be checked in

variance analysis which results as favourable variance and inefficiency leads to unfavourable

variance. By comparing actual with the budgeted, level of deviations is to be found and reason

for such difference are also to be calculated (Fuller and et. al. 2016). If actual cost is less than the

standard cost, then it leads to favourable variance and when the standard cost is less it results as

unfavourable cost. By analysing it helps to find area of improvement for the company. Variance

is to be analyse after considering the factors such as material, labour and overheads. By applying

formula, it is easy to understand and calculate the variances and it became helpful in the activity

of performing budgets also.

Some of the merits of variances are explained below in detail:

1. Measurement of performance: In Variance analysis detailed information after covering

all the relevant facts are considered for measurement (Huang and et. al., 2019).

Performance is not to be measured on the basis of assumption as deep evaluation is

performed to find deviation. With the help of variance analysis, organisations are able to

assess performances made by managers through proper care to not make costly

assumptions as well as mistakes.

2. Accounting Responsibility: Variance analysis helps managers to accountable for the

work they performed. In Companies there are various departments such as sales,

Purchase, Production, Accounts etc. as variance analysis helps to answer for the work

they done. Optimum utilisation of resources is to be done because it is known by

managers and workers that all the performance is to be accountable.

determining managers’ performance:

Analysis of variances is the review of differences in conventional costing method items.

This is analysis and evaluation of all variables which induced the discrepancies among the

standards/targets established and actual outcomes, with the target of minimizing deficiencies.

The review of variances suggests capabilities and major indices but doesn't really specify what

action, if any, ought to be undertaken. Until they could execute control steps the administrators

should be provided to appropriately characterize the true sense of different-different variances.

Cost reduction and Cost control are the major objective which is performed in the activity of

variance analysis. It plays an important role in costing on which efficiency is to be checked in

variance analysis which results as favourable variance and inefficiency leads to unfavourable

variance. By comparing actual with the budgeted, level of deviations is to be found and reason

for such difference are also to be calculated (Fuller and et. al. 2016). If actual cost is less than the

standard cost, then it leads to favourable variance and when the standard cost is less it results as

unfavourable cost. By analysing it helps to find area of improvement for the company. Variance

is to be analyse after considering the factors such as material, labour and overheads. By applying

formula, it is easy to understand and calculate the variances and it became helpful in the activity

of performing budgets also.

Some of the merits of variances are explained below in detail:

1. Measurement of performance: In Variance analysis detailed information after covering

all the relevant facts are considered for measurement (Huang and et. al., 2019).

Performance is not to be measured on the basis of assumption as deep evaluation is

performed to find deviation. With the help of variance analysis, organisations are able to

assess performances made by managers through proper care to not make costly

assumptions as well as mistakes.

2. Accounting Responsibility: Variance analysis helps managers to accountable for the

work they performed. In Companies there are various departments such as sales,

Purchase, Production, Accounts etc. as variance analysis helps to answer for the work

they done. Optimum utilisation of resources is to be done because it is known by

managers and workers that all the performance is to be accountable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Management by exemption: Variance analysis is to be calculated with proper care and

attention, so it became helpful for the managers to understand the work properly by

consuming less time.

4. It helps to find weakness: Deviations are to be found by comparing the actual with the

standard and reasons of such weakness are also be find out.

5. Helpful in budget making: Variance Analysis makes great impact on budgets by

considering all the cost as it helps at the time of preparing budget.

6. Improve the motivation level of employees: In variance analysis labour efficiency is

calculated and if labour works efficiently they will be rewarded by managers which helps

to improve their motivation level.

7. Easy to control: It became easy to control because different departments have different

work and managers of that particular department perform their department function only

it makes easy to find out deviation in variance analysis and makes control over it.

8. Improve skills of Managers: As all the work of calculating variance analysis is performed

by managers with proper care and attention so due to repetition of similar type of work it

improves skill of managers also (Duan and et. al., 2018).

9. Easy to understand: Variance Analysis calculation is easy and simple to understand by

any person whether they have vast knowledge about that or not.

10. Reduces cost: cost reduction is the major objective performed by management. At the

time of analysis of variances unreasonable cost must be excluded from it.

11. Improves quality of leadership: As the variance analysis is calculated by managers which

fixes management responsibility and also improves leadership quality.

12. Level of coordination increase: Variance analysis also improves coordination among

different department as work are interrelated and performed by different managers.

13. Easy to compare: comparison became possible in variance analysis so it is easy to take

remedial action on time.

Demerits are also explained in detail in mentioned below points:

Uncontrollable Variance are related to external factors: At the time of calculating

various analysis some factors are unavoidable and uncontrollable such as non-availability

of raw material due to natural calamity, reduction in the labour etc.

attention, so it became helpful for the managers to understand the work properly by

consuming less time.

4. It helps to find weakness: Deviations are to be found by comparing the actual with the

standard and reasons of such weakness are also be find out.

5. Helpful in budget making: Variance Analysis makes great impact on budgets by

considering all the cost as it helps at the time of preparing budget.

6. Improve the motivation level of employees: In variance analysis labour efficiency is

calculated and if labour works efficiently they will be rewarded by managers which helps

to improve their motivation level.

7. Easy to control: It became easy to control because different departments have different

work and managers of that particular department perform their department function only

it makes easy to find out deviation in variance analysis and makes control over it.

8. Improve skills of Managers: As all the work of calculating variance analysis is performed

by managers with proper care and attention so due to repetition of similar type of work it

improves skill of managers also (Duan and et. al., 2018).

9. Easy to understand: Variance Analysis calculation is easy and simple to understand by

any person whether they have vast knowledge about that or not.

10. Reduces cost: cost reduction is the major objective performed by management. At the

time of analysis of variances unreasonable cost must be excluded from it.

11. Improves quality of leadership: As the variance analysis is calculated by managers which

fixes management responsibility and also improves leadership quality.

12. Level of coordination increase: Variance analysis also improves coordination among

different department as work are interrelated and performed by different managers.

13. Easy to compare: comparison became possible in variance analysis so it is easy to take

remedial action on time.

Demerits are also explained in detail in mentioned below points:

Uncontrollable Variance are related to external factors: At the time of calculating

various analysis some factors are unavoidable and uncontrollable such as non-availability

of raw material due to natural calamity, reduction in the labour etc.

Difficult to predict: In variance analysis calculation, external factors are also being

considered so it is difficult to predict the problem. Forecasting is not to be possible so it

involves huge expenses to meet the requirement of organisation (Gautier and et. al. ,

2017).

Long-time gap which effects remedial action: The activity of variance analysis depends

on financial results so different time period is to be taken which involve large gap due to

which remedy effects.

Manipulation of Variance: To get favourable result incorrect measures are considered at

the time of variance analysis by management to hide their inefficiency.

Time consuming activity: It is not possible to take decision on the basis of little bit

information. Large amount of time is needed to perform the functions of investigation.

Variance analysis also involve various calculations by applying different formulas which

consumes a lot of time.

Reporting Delay: The figures are estimated at the yearend so the period of accounting to

prepare budget is also increase. As calculations of variance analysis are critical in nature

that causes delays in reporting.

Technological industry: It is not convenient to calculate variance analysis for dynamic

industry. Variance analysis is done only in manufacturing industry.

Co related activity: Analysis is correlation activity which is also an another drawback of

variance analysis.

Variance analysis is costly function: Variance analysis become expensive if it is

performed in small business because it requires professionals to find deviations who

charge high charges for the work they performed.

Not to give proper reasons: Reasons of something cannot be explained in variance

analysis only requires allocation in some areas (Das, Ghosh and Jeffery, 2020). Minor

mistake can lead to negative impact as calculation is to be performed by applying

different formulas so it need prompt attention at the time of solving different variances,

inaccurate result shows deficiency in calculation part.

Material requirement is high: Inferior goods is used my managers so more material

requirement is needed time to time which leads to increase in cost.

considered so it is difficult to predict the problem. Forecasting is not to be possible so it

involves huge expenses to meet the requirement of organisation (Gautier and et. al. ,

2017).

Long-time gap which effects remedial action: The activity of variance analysis depends

on financial results so different time period is to be taken which involve large gap due to

which remedy effects.

Manipulation of Variance: To get favourable result incorrect measures are considered at

the time of variance analysis by management to hide their inefficiency.

Time consuming activity: It is not possible to take decision on the basis of little bit

information. Large amount of time is needed to perform the functions of investigation.

Variance analysis also involve various calculations by applying different formulas which

consumes a lot of time.

Reporting Delay: The figures are estimated at the yearend so the period of accounting to

prepare budget is also increase. As calculations of variance analysis are critical in nature

that causes delays in reporting.

Technological industry: It is not convenient to calculate variance analysis for dynamic

industry. Variance analysis is done only in manufacturing industry.

Co related activity: Analysis is correlation activity which is also an another drawback of

variance analysis.

Variance analysis is costly function: Variance analysis become expensive if it is

performed in small business because it requires professionals to find deviations who

charge high charges for the work they performed.

Not to give proper reasons: Reasons of something cannot be explained in variance

analysis only requires allocation in some areas (Das, Ghosh and Jeffery, 2020). Minor

mistake can lead to negative impact as calculation is to be performed by applying

different formulas so it need prompt attention at the time of solving different variances,

inaccurate result shows deficiency in calculation part.

Material requirement is high: Inferior goods is used my managers so more material

requirement is needed time to time which leads to increase in cost.

PART B

Make-or-buy decisions is a process of opting among in-house production or buying a

product by an outside vendor (Roskosz, Chrapoński and Madej, 2020). Make-or-buy decisions,

also refers to an outsourcing decision, contrasts costs and advantages involved with

manufacturing a desired product internally with costs and benefits implicit with selecting an

external supplier for products with query. In order to adequately determine costs, an organization

must recognize all factors relating to the purchase and handling of the products

versus production of the products in-house.

With respect to the in-house production, a company must involve costs related

to procurement of any manufacturing process and cost of manufacturing. Making costs may

include extra labour needed to manufacture the goods, specifications for storage within plant,

total storage costs, including proper handling of any remains or by-products from manufacturing

process (Carvalho and et. al., 2020). The buying costs associated with the purchase of the goods

from an external source must involve price of good itself, certain delivery or import expenses

and relevant local taxes. In addition, expenditures related to handling of incoming item and

labour costs connected with receiving goods in stock must be taken into consideration by the

organization. The findings of quantitative analysis can suffice to render a more efficient

and cost-effective decision dependent on approach. At times, qualitative review explores any

particular issues that a firm cannot objectively quantify.

The case-study presented concerning XLG organization is also focused on decision to

making-or-buy. management needs to draw make-or-buy decision with regard to the famaQ in

the corresponding case-study scenarios. For organization fama Q that is a cleaning agent of

supreme quality is vital item in production that provides it with comparative edge. Patent secures

this product and business XLG aims to producing it in-house. Business imports fama Q from

Brazil and because of country-wide lock-down declared by UK authorities and restrictions, it

was costly to import such item for the corporation. fnow this has to be transported by air

transport but instead through sea transport since lock-down, which has raised the price of unit of

fama Q to 4.5 every unit as-well-as actual price charged is 3.7 each unit.

Make-or-buy decisions is a process of opting among in-house production or buying a

product by an outside vendor (Roskosz, Chrapoński and Madej, 2020). Make-or-buy decisions,

also refers to an outsourcing decision, contrasts costs and advantages involved with

manufacturing a desired product internally with costs and benefits implicit with selecting an

external supplier for products with query. In order to adequately determine costs, an organization

must recognize all factors relating to the purchase and handling of the products

versus production of the products in-house.

With respect to the in-house production, a company must involve costs related

to procurement of any manufacturing process and cost of manufacturing. Making costs may

include extra labour needed to manufacture the goods, specifications for storage within plant,

total storage costs, including proper handling of any remains or by-products from manufacturing

process (Carvalho and et. al., 2020). The buying costs associated with the purchase of the goods

from an external source must involve price of good itself, certain delivery or import expenses

and relevant local taxes. In addition, expenditures related to handling of incoming item and

labour costs connected with receiving goods in stock must be taken into consideration by the

organization. The findings of quantitative analysis can suffice to render a more efficient

and cost-effective decision dependent on approach. At times, qualitative review explores any

particular issues that a firm cannot objectively quantify.

The case-study presented concerning XLG organization is also focused on decision to

making-or-buy. management needs to draw make-or-buy decision with regard to the famaQ in

the corresponding case-study scenarios. For organization fama Q that is a cleaning agent of

supreme quality is vital item in production that provides it with comparative edge. Patent secures

this product and business XLG aims to producing it in-house. Business imports fama Q from

Brazil and because of country-wide lock-down declared by UK authorities and restrictions, it

was costly to import such item for the corporation. fnow this has to be transported by air

transport but instead through sea transport since lock-down, which has raised the price of unit of

fama Q to 4.5 every unit as-well-as actual price charged is 3.7 each unit.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

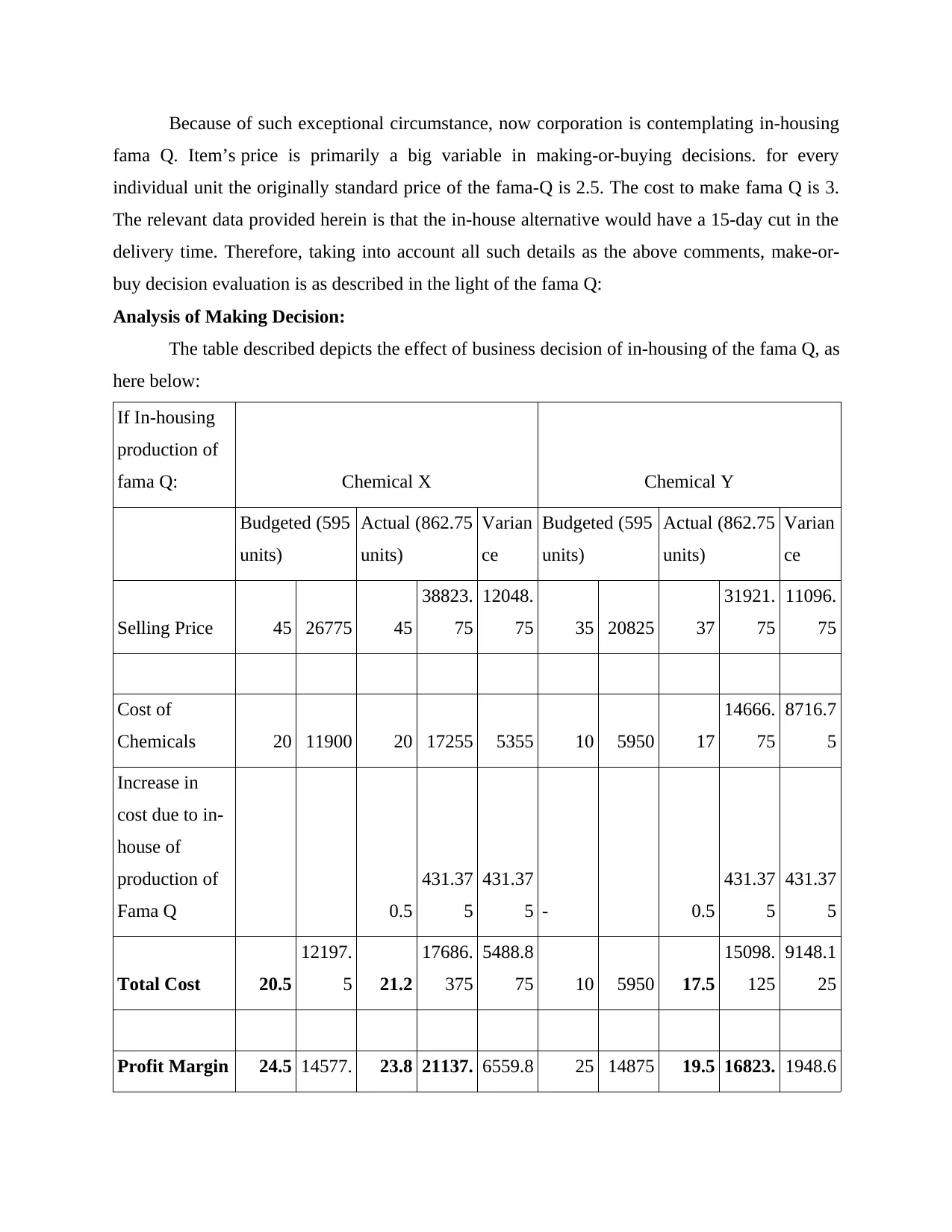

Because of such exceptional circumstance, now corporation is contemplating in-housing

fama Q. Item’s price is primarily a big variable in making-or-buying decisions. for every

individual unit the originally standard price of the fama-Q is 2.5. The cost to make fama Q is 3.

The relevant data provided herein is that the in-house alternative would have a 15-day cut in the

delivery time. Therefore, taking into account all such details as the above comments, make-or-

buy decision evaluation is as described in the light of the fama Q:

Analysis of Making Decision:

The table described depicts the effect of business decision of in-housing of the fama Q, as

here below:

If In-housing

production of

fama Q: Chemical X Chemical Y

Budgeted (595

units)

Actual (862.75

units)

Varian

ce

Budgeted (595

units)

Actual (862.75

units)

Varian

ce

Selling Price 45 26775 45

38823.

75

12048.

75 35 20825 37

31921.

75

11096.

75

Cost of

Chemicals 20 11900 20 17255 5355 10 5950 17

14666.

75

8716.7

5

Increase in

cost due to in-

house of

production of

Fama Q 0.5

431.37

5

431.37

5 - 0.5

431.37

5

431.37

5

Total Cost 20.5

12197.

5 21.2

17686.

375

5488.8

75 10 5950 17.5

15098.

125

9148.1

25

Profit Margin 24.5 14577. 23.8 21137. 6559.8 25 14875 19.5 16823. 1948.6

fama Q. Item’s price is primarily a big variable in making-or-buying decisions. for every

individual unit the originally standard price of the fama-Q is 2.5. The cost to make fama Q is 3.

The relevant data provided herein is that the in-house alternative would have a 15-day cut in the

delivery time. Therefore, taking into account all such details as the above comments, make-or-

buy decision evaluation is as described in the light of the fama Q:

Analysis of Making Decision:

The table described depicts the effect of business decision of in-housing of the fama Q, as

here below:

If In-housing

production of

fama Q: Chemical X Chemical Y

Budgeted (595

units)

Actual (862.75

units)

Varian

ce

Budgeted (595

units)

Actual (862.75

units)

Varian

ce

Selling Price 45 26775 45

38823.

75

12048.

75 35 20825 37

31921.

75

11096.

75

Cost of

Chemicals 20 11900 20 17255 5355 10 5950 17

14666.

75

8716.7

5

Increase in

cost due to in-

house of

production of

Fama Q 0.5

431.37

5

431.37

5 - 0.5

431.37

5

431.37

5

Total Cost 20.5

12197.

5 21.2

17686.

375

5488.8

75 10 5950 17.5

15098.

125

9148.1

25

Profit Margin 24.5 14577. 23.8 21137. 6559.8 25 14875 19.5 16823. 1948.6

5 375 75 625 25

Working Note:

Computation of Demand(units) based on the new scenario: (Demand expected to be risen

by 45 percent)

Chemical X 595 units + 595 units *45% = 862.75

Chemical Y 595 units + 595 units * 45% = 862.75

By reviewing the decision to purchase fama Q, it has been determined that in context of

both chemical X and Y production, profit level would increase by around 6559.87 and 1948.62

respectively. For both cases, the actual profits would therefore surpass the

actual budgeted amount of profits.

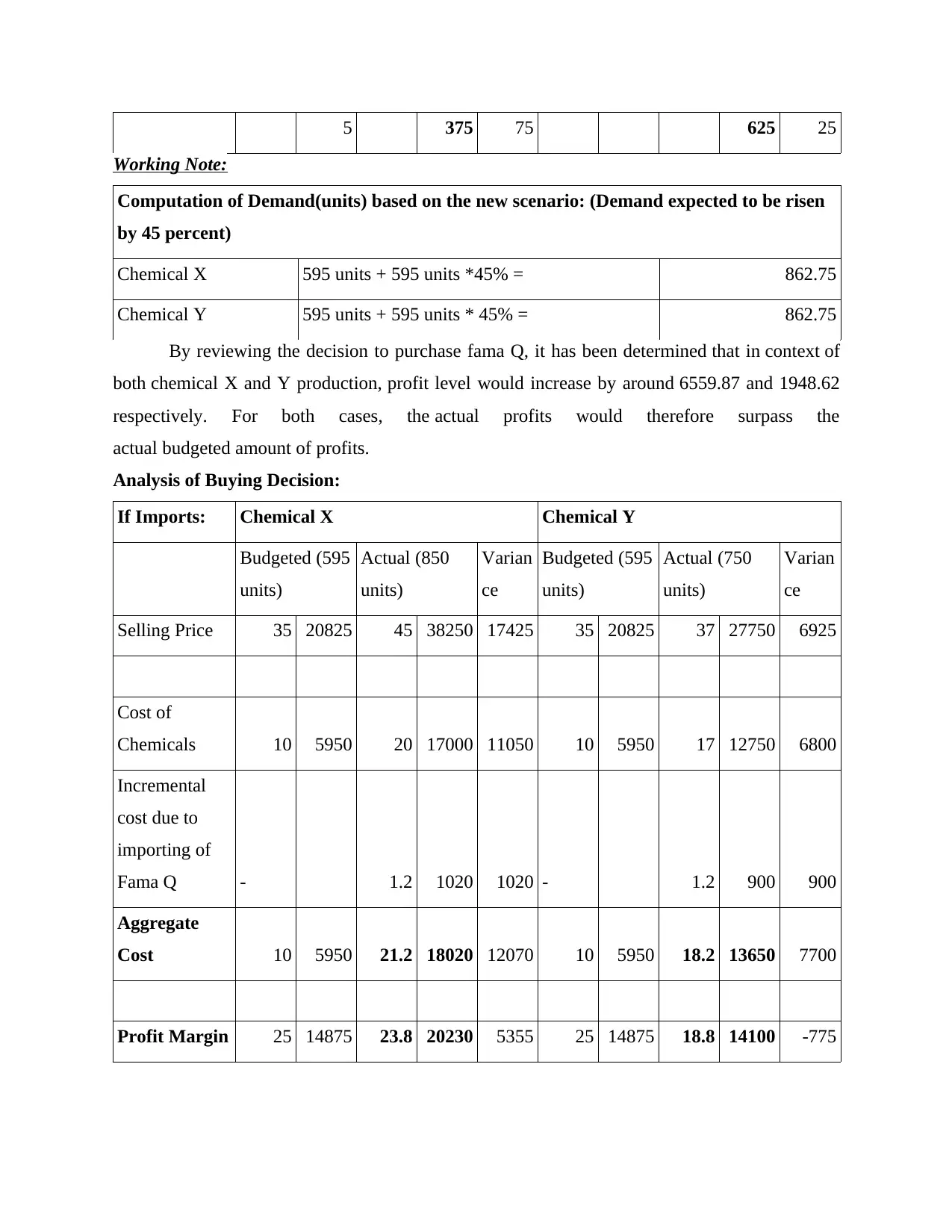

Analysis of Buying Decision:

If Imports: Chemical X Chemical Y

Budgeted (595

units)

Actual (850

units)

Varian

ce

Budgeted (595

units)

Actual (750

units)

Varian

ce

Selling Price 35 20825 45 38250 17425 35 20825 37 27750 6925

Cost of

Chemicals 10 5950 20 17000 11050 10 5950 17 12750 6800

Incremental

cost due to

importing of

Fama Q - 1.2 1020 1020 - 1.2 900 900

Aggregate

Cost 10 5950 21.2 18020 12070 10 5950 18.2 13650 7700

Profit Margin 25 14875 23.8 20230 5355 25 14875 18.8 14100 -775

Working Note:

Computation of Demand(units) based on the new scenario: (Demand expected to be risen

by 45 percent)

Chemical X 595 units + 595 units *45% = 862.75

Chemical Y 595 units + 595 units * 45% = 862.75

By reviewing the decision to purchase fama Q, it has been determined that in context of

both chemical X and Y production, profit level would increase by around 6559.87 and 1948.62

respectively. For both cases, the actual profits would therefore surpass the

actual budgeted amount of profits.

Analysis of Buying Decision:

If Imports: Chemical X Chemical Y

Budgeted (595

units)

Actual (850

units)

Varian

ce

Budgeted (595

units)

Actual (750

units)

Varian

ce

Selling Price 35 20825 45 38250 17425 35 20825 37 27750 6925

Cost of

Chemicals 10 5950 20 17000 11050 10 5950 17 12750 6800

Incremental

cost due to

importing of

Fama Q - 1.2 1020 1020 - 1.2 900 900

Aggregate

Cost 10 5950 21.2 18020 12070 10 5950 18.2 13650 7700

Profit Margin 25 14875 23.8 20230 5355 25 14875 18.8 14100 -775

Review of the table attached-above reveals that in relation to chemical X such decision

will result in profit rise of 5355 whereas in relation to chemical Y there will be loss of GBP775.

In the case of Y, the total budgeted profits will also be decrease from GBP14875 to GBP14100.

Therefore, after analysing both the decisions, it has been ascertained that it will be more

practical and efficient to make decisions in the context of fama Q. Profits would improve

by in house of product fama Q. Rather of purchasing it, company must consider in-housing fama

Q. As profits figure for in-house alternative is higher than for both the chemical X and Y relative

to fama Q purchase / import. Therefore, XLG organization is firmly advised to produce fama Q

in-house, but business must weigh certain considerations relevant to fama Q such as competitive

advantages, fama Q's patent, etc. before making ultimate decisions.

CONCLUSION

It has been examined from the above-mentioned report that business decision-making is

solely based on the management accounting. It helps management to undertake strategic

decisions that are most efficient, important and successful. When making a decision such as

making or purchasing, all potential options and factors that can affect the final decision must be

checked. Examination of variation attributes all the big strengths and limitations as to help

management decisions.

will result in profit rise of 5355 whereas in relation to chemical Y there will be loss of GBP775.

In the case of Y, the total budgeted profits will also be decrease from GBP14875 to GBP14100.

Therefore, after analysing both the decisions, it has been ascertained that it will be more

practical and efficient to make decisions in the context of fama Q. Profits would improve

by in house of product fama Q. Rather of purchasing it, company must consider in-housing fama

Q. As profits figure for in-house alternative is higher than for both the chemical X and Y relative

to fama Q purchase / import. Therefore, XLG organization is firmly advised to produce fama Q

in-house, but business must weigh certain considerations relevant to fama Q such as competitive

advantages, fama Q's patent, etc. before making ultimate decisions.

CONCLUSION

It has been examined from the above-mentioned report that business decision-making is

solely based on the management accounting. It helps management to undertake strategic

decisions that are most efficient, important and successful. When making a decision such as

making or purchasing, all potential options and factors that can affect the final decision must be

checked. Examination of variation attributes all the big strengths and limitations as to help

management decisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Zhuo, W., Shao, L. and Yang, H., 2018. Mean–variance analysis of option contracts in a two-

echelon supply chain. European Journal of Operational Research. 271(2). pp.535-547.

Wang, X. and et. al., 2017. Postharvest quality monitoring and variance analysis of peach and

nectarine cold chain with multi-sensors technology. Applied Sciences. 7(2). p.133.

Ju, S. and et. al., 2017. Effect of energy addition parameters upon scramjet nozzle performances

based on the variance analysis method. Aerospace Science and Technology. 70. pp.511-

519.

Huang, C. M. and et. al., 2019. Uncertainty quantification of a DNA origami mechanism using a

coarse-grained model and kinematic variance analysis. Nanoscale, 11(4), pp.1647-1660.

Duan, Y. and et. al., 2018. Coherence based on spectral variance analysis. Geophysics. 83(3).

pp.O55-O66.

Gautier, G. and et. al. , 2017. Variance analysis for model updating with a finite element based

subspace fitting approach. Mechanical Systems and Signal Processing. 91. pp.142-156.

Das, M., Ghosh, T. S. and Jeffery, I. B., 2020. IPCO: Inference of Pathways from Co-variance

analysis. BMC bioinformatics. 21(1). pp.1-15.

Roskosz, S., Chrapoński, J. and Madej, Ł., 2020. Application of systematic scanning and

variance analysis method to evaluation of pores arrangement in sintered

steel. Measurement, p.108325.

Carvalho, V. S. B. and et. al., 2020. Variance analysis applied to ground-level ozone

concentrations in the state of São Paulo, Brazil. Brazilian Journal of Chemical

Engineering, pp.1-9.

Books and Journals:

Zhuo, W., Shao, L. and Yang, H., 2018. Mean–variance analysis of option contracts in a two-

echelon supply chain. European Journal of Operational Research. 271(2). pp.535-547.

Wang, X. and et. al., 2017. Postharvest quality monitoring and variance analysis of peach and

nectarine cold chain with multi-sensors technology. Applied Sciences. 7(2). p.133.

Ju, S. and et. al., 2017. Effect of energy addition parameters upon scramjet nozzle performances

based on the variance analysis method. Aerospace Science and Technology. 70. pp.511-

519.

Huang, C. M. and et. al., 2019. Uncertainty quantification of a DNA origami mechanism using a

coarse-grained model and kinematic variance analysis. Nanoscale, 11(4), pp.1647-1660.

Duan, Y. and et. al., 2018. Coherence based on spectral variance analysis. Geophysics. 83(3).

pp.O55-O66.

Gautier, G. and et. al. , 2017. Variance analysis for model updating with a finite element based

subspace fitting approach. Mechanical Systems and Signal Processing. 91. pp.142-156.

Das, M., Ghosh, T. S. and Jeffery, I. B., 2020. IPCO: Inference of Pathways from Co-variance

analysis. BMC bioinformatics. 21(1). pp.1-15.

Roskosz, S., Chrapoński, J. and Madej, Ł., 2020. Application of systematic scanning and

variance analysis method to evaluation of pores arrangement in sintered

steel. Measurement, p.108325.

Carvalho, V. S. B. and et. al., 2020. Variance analysis applied to ground-level ozone

concentrations in the state of São Paulo, Brazil. Brazilian Journal of Chemical

Engineering, pp.1-9.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.