Strategic Analysis Report: Assignment

VerifiedAdded on 2021/06/05

|20

|4756

|466

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Lewis Road Creamery in 2021

Strategic Analysis Report

Strategic Analysis Report

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive Summary

This means that it is a part of both the food and beverage as well as the dairy industry.

The dairy industry is one of the most important and lucrative in New Zealand. Lewis Road

Creamery leads the flavoured milk sector with 33%. The major strength noted in this report is

the strength of the Lewis Road Creamery branding and its partnerships. Lewis Road

Creamery has become a household name in New Zealand and has also maintained a strong

online presence. It is because of this that customers consistently choose Lewis Road

Creamery, because of its reputation for high quality products. This is a competitive advantage

that other firms will find difficult to imitate. This report found that an important for Lewis

Road Creamery is the pursuit of partnerships in order to promote more excitement for the

company and generate more sales. The strengths listed earlier will also help with a larger,

long term goal of Lewis Road Creamery, international expansion. The main hurdle in

achieving this goal is being able to replicate their popularity overseas in the international

market.

The main weaknesses of the company stem from its reliance on larger corporations.

The dairy industry is completely reliant on the availability of milk and therefore is always at

the mercy of farmers. Lewis Road Creamery is owned by the Southern Pastures farming fund,

making them a small entity in a much larger firm. This means that the majority of operations

are logistical, mainly concerned with organising how products go from farm to fridge.

Another important weakness is the price of their products. Because Lewis Road Creamery

operates in the supermarket sector, the high price of their products will make consumers

choose one of their competitors.

2

This means that it is a part of both the food and beverage as well as the dairy industry.

The dairy industry is one of the most important and lucrative in New Zealand. Lewis Road

Creamery leads the flavoured milk sector with 33%. The major strength noted in this report is

the strength of the Lewis Road Creamery branding and its partnerships. Lewis Road

Creamery has become a household name in New Zealand and has also maintained a strong

online presence. It is because of this that customers consistently choose Lewis Road

Creamery, because of its reputation for high quality products. This is a competitive advantage

that other firms will find difficult to imitate. This report found that an important for Lewis

Road Creamery is the pursuit of partnerships in order to promote more excitement for the

company and generate more sales. The strengths listed earlier will also help with a larger,

long term goal of Lewis Road Creamery, international expansion. The main hurdle in

achieving this goal is being able to replicate their popularity overseas in the international

market.

The main weaknesses of the company stem from its reliance on larger corporations.

The dairy industry is completely reliant on the availability of milk and therefore is always at

the mercy of farmers. Lewis Road Creamery is owned by the Southern Pastures farming fund,

making them a small entity in a much larger firm. This means that the majority of operations

are logistical, mainly concerned with organising how products go from farm to fridge.

Another important weakness is the price of their products. Because Lewis Road Creamery

operates in the supermarket sector, the high price of their products will make consumers

choose one of their competitors.

2

1. Introduction

The purpose of this report is to analyse the strategic issues facing Lewis Road

Creamery in 2021. Lewis Road Creamery is a manufacturer of beverages and dairy products

in New Zealand. Lewis Road Creamery is a growing brand in New Zealand, and because of

this it is important to analyse the company’s plans moving forward. This report will highlight

important details and objectives Lewis Road Creamery should pay attention to. This report

will take into account the industry in which the company resides in, competitors, internal and

external factors as well as a comprehensive SWOT analysis. This report will also use PEST+,

Porters 5 forces, Value Chain and VRIO analysis to clearly show the issues facing Lewis

Road Creamery. This report is aiming to provide Lewis Road Creamery with a clear

direction to follow leading success in the future.

2. External Analysis

2.1. Industry Profile

Lewis Road Creamery is part of the food and beverage sector, more specifically the dairy

industry. The dairy industry is one of the most lucrative in New Zealand, accounting for

almost 3% of the GDP as well as being New Zealand’s largest export earner. Dairy exports in

New Zealand have grown by 7.2% in the last 30 years. The main competitor for Lewis Road

Creamery is Fonterra. Other competitors include smaller firms which compete domestically.

With Fonterra accounting for almost 80% of employment in the dairy industry and

controlling most of its resources, it is New Zealand’s main source of exported dairy products,

making smaller companies compete domestically. Fonterra will also supply smaller

companies with milk when demand is abnormally high or low. The majority of the industry is

held up by Fonterra at times making its competitors also its customers. It is important to

recognise that Fonterra is both a partner and a competitor of Lewis Road Creamery. This is

3

The purpose of this report is to analyse the strategic issues facing Lewis Road

Creamery in 2021. Lewis Road Creamery is a manufacturer of beverages and dairy products

in New Zealand. Lewis Road Creamery is a growing brand in New Zealand, and because of

this it is important to analyse the company’s plans moving forward. This report will highlight

important details and objectives Lewis Road Creamery should pay attention to. This report

will take into account the industry in which the company resides in, competitors, internal and

external factors as well as a comprehensive SWOT analysis. This report will also use PEST+,

Porters 5 forces, Value Chain and VRIO analysis to clearly show the issues facing Lewis

Road Creamery. This report is aiming to provide Lewis Road Creamery with a clear

direction to follow leading success in the future.

2. External Analysis

2.1. Industry Profile

Lewis Road Creamery is part of the food and beverage sector, more specifically the dairy

industry. The dairy industry is one of the most lucrative in New Zealand, accounting for

almost 3% of the GDP as well as being New Zealand’s largest export earner. Dairy exports in

New Zealand have grown by 7.2% in the last 30 years. The main competitor for Lewis Road

Creamery is Fonterra. Other competitors include smaller firms which compete domestically.

With Fonterra accounting for almost 80% of employment in the dairy industry and

controlling most of its resources, it is New Zealand’s main source of exported dairy products,

making smaller companies compete domestically. Fonterra will also supply smaller

companies with milk when demand is abnormally high or low. The majority of the industry is

held up by Fonterra at times making its competitors also its customers. It is important to

recognise that Fonterra is both a partner and a competitor of Lewis Road Creamery. This is

3

because they are a key supplier for Lewis Road Creamery as well manufacturing their own

products. New Zealand is one of the largest exporters of dairy to Asia making the Asian

market a key customer. Another key customer domestically is the restaurant industry,

especially for smaller firms which take pride in their quality. Due to large companies

controlling the majority of the market, other competitors focus on more niche and specialised

products

2.2. Competitor Profiles

A key aspect of the dairy industry especially in the New Zealand market is the massive

amount of influence that Fonterra has over the industry. The majority of smaller firms rely on

them for supplies in order to manufacture their own dairy products and they also produce a

massive amount of products consumed in New Zealand. Along with this Fonterra is the

biggest exporter of dairy products for New Zealand. This forces smaller firms to market

themselves towards more niche customer bases. Fonterra owns the majority of the market but

in New Zealand there is always space for companies looking to provide higher quality niche

products. For Lewis Road Creamery, the boutique nature of the business attracts people

towards their brand. Domestically, Fonterra still holds over 80% of the market, with no other

firms holding more than 10%. It is important to note that Fonterra’s influence is an important

mobility barrier in the dairy industry. The answer for companies looking to be successful in

the dairy industry must look for a way to navigate around Fonterra with more specialised

products rather than directly compete with them. This is the case for both the domestic and

international dairy market. Other small firms are less competitive because they are also

attempting to carve out their own niche in the market

4

products. New Zealand is one of the largest exporters of dairy to Asia making the Asian

market a key customer. Another key customer domestically is the restaurant industry,

especially for smaller firms which take pride in their quality. Due to large companies

controlling the majority of the market, other competitors focus on more niche and specialised

products

2.2. Competitor Profiles

A key aspect of the dairy industry especially in the New Zealand market is the massive

amount of influence that Fonterra has over the industry. The majority of smaller firms rely on

them for supplies in order to manufacture their own dairy products and they also produce a

massive amount of products consumed in New Zealand. Along with this Fonterra is the

biggest exporter of dairy products for New Zealand. This forces smaller firms to market

themselves towards more niche customer bases. Fonterra owns the majority of the market but

in New Zealand there is always space for companies looking to provide higher quality niche

products. For Lewis Road Creamery, the boutique nature of the business attracts people

towards their brand. Domestically, Fonterra still holds over 80% of the market, with no other

firms holding more than 10%. It is important to note that Fonterra’s influence is an important

mobility barrier in the dairy industry. The answer for companies looking to be successful in

the dairy industry must look for a way to navigate around Fonterra with more specialised

products rather than directly compete with them. This is the case for both the domestic and

international dairy market. Other small firms are less competitive because they are also

attempting to carve out their own niche in the market

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2.3. Competitive Analysis (P5F)

Threat of New Entrants

The dairy industry is a well-established industry that will have a strong stream of customers.

The market is highly concentrated, especially in New Zealand with the top players running

over 80% of it. There are already high barriers of entry for this industry and new entrants are

limited to specialising in niche products. One important threat to recognise is the cultural

move away from dairy products allowing for the emergence for a number of firms

specialising in dairy substitutes. Whilst this may make a slight dent in the market the effect is

negligible.

Bargaining Power of Suppliers

The dairy industry completely depends on the supply and demand of milk. Without this raw

material all of the firms cannot continue trade. At first glance, it would seem like dairy

farmers would have a large amount of bargaining power. With Fonterra owning the majority

of resources for processing milk and having influence on the majority of dairy farms in New

Zealand, many specialist firms will attempt to source their raw milk for production, directly

from farms. With this decision comes the added disadvantage of being forced to raise

production costs

Bargaining Power of Customers

Dairy products are almost exclusively bought in supermarkets. Supermarkets are very highly

concentrated with that concentration only increasing. Supermarkets are very often owned by

large multinational corporations, making the price setting dependent on production costs and

suppliers. Many of these corporations may also own their own dairy firms, encouraging to

promote their own brands much harder. The price sensitivity of milk is an important aspect to

5

Threat of New Entrants

The dairy industry is a well-established industry that will have a strong stream of customers.

The market is highly concentrated, especially in New Zealand with the top players running

over 80% of it. There are already high barriers of entry for this industry and new entrants are

limited to specialising in niche products. One important threat to recognise is the cultural

move away from dairy products allowing for the emergence for a number of firms

specialising in dairy substitutes. Whilst this may make a slight dent in the market the effect is

negligible.

Bargaining Power of Suppliers

The dairy industry completely depends on the supply and demand of milk. Without this raw

material all of the firms cannot continue trade. At first glance, it would seem like dairy

farmers would have a large amount of bargaining power. With Fonterra owning the majority

of resources for processing milk and having influence on the majority of dairy farms in New

Zealand, many specialist firms will attempt to source their raw milk for production, directly

from farms. With this decision comes the added disadvantage of being forced to raise

production costs

Bargaining Power of Customers

Dairy products are almost exclusively bought in supermarkets. Supermarkets are very highly

concentrated with that concentration only increasing. Supermarkets are very often owned by

large multinational corporations, making the price setting dependent on production costs and

suppliers. Many of these corporations may also own their own dairy firms, encouraging to

promote their own brands much harder. The price sensitivity of milk is an important aspect to

5

consider because customers from almost all economic classes are dairy consumers. And

increases in price for certain brands will drive lower income customers elsewhere

Threat of Substitutes

As mentioned previously, there has been a recent culturally shift away from dairy products.

As society becomes more health conscious there has been a recent movement of more people

choosing to be vegan and dairy free. Despite this, milk and dairy products are existent in

almost every persons diet and the miniscule percentage that have taken dairy out of their diet

has not had a notable effect on the market

Intensity of Industry Rivalry

For the dairy industry the majority of competition comes from large corporations competing

within their own supermarkets to sell a basic range of products to the average consumer. The

rest of the industry is made up of specialist firms looking to sell to a smaller demographic.

This shows that the size of the firms in the dairy industry is directly correlated to the intensity

of the rivalry

2.4. Driving Forces (From PEST+/PESTLE)

The first influential trend that is important to discuss is the sociocultural. As mentioned

previously there has been a recent surge in people moving away from a non-dairy lifestyle.

Dairy products are a staple in the majority of households, as the number of families that move

away from dairy products increases the competition will only increase. Whilst currently this

number may not have a large effect on the market, overtime this trend will continue driving

more and more customers away. What this will do is increase the popularity in diary

6

increases in price for certain brands will drive lower income customers elsewhere

Threat of Substitutes

As mentioned previously, there has been a recent culturally shift away from dairy products.

As society becomes more health conscious there has been a recent movement of more people

choosing to be vegan and dairy free. Despite this, milk and dairy products are existent in

almost every persons diet and the miniscule percentage that have taken dairy out of their diet

has not had a notable effect on the market

Intensity of Industry Rivalry

For the dairy industry the majority of competition comes from large corporations competing

within their own supermarkets to sell a basic range of products to the average consumer. The

rest of the industry is made up of specialist firms looking to sell to a smaller demographic.

This shows that the size of the firms in the dairy industry is directly correlated to the intensity

of the rivalry

2.4. Driving Forces (From PEST+/PESTLE)

The first influential trend that is important to discuss is the sociocultural. As mentioned

previously there has been a recent surge in people moving away from a non-dairy lifestyle.

Dairy products are a staple in the majority of households, as the number of families that move

away from dairy products increases the competition will only increase. Whilst currently this

number may not have a large effect on the market, overtime this trend will continue driving

more and more customers away. What this will do is increase the popularity in diary

6

alternative products, effectively changing the logistics of the market itself. This change in

competition will have an effect on how companies will have to market their products.

The second important trend is the ecological implications of the dairy industry. New research

has found that dairy farming and livestock is a major reason behind climate change. Because

the dairy industry is so produces so much milk, companies must look for a way to promote a

more sustainable method of farming. This trend is also directly related to the sociocultural

factor. Many people are moving away from dairy products in order to be more eco-friendly.

Systems and processes in dairy farming have been so well established for so long, employing

new methods will be a very difficult undertaking and may cost companies a lot of money in

its initial stages, also possibly raising the prices of milk

3. Internal Analysis

3.1. Strategic Profile

Lewis Road Creamery began as a boutique dairy company out of ex-advertising guru’s Peter

Cullinane's kitchen in 2011. The company was founded as a niche, boutique dairy company for

customers wanting higher quality dairy products. The company remained popular in local

circles but saw it’s prominent rise to popularity following its partnership with Whittakers

chocolate. This caused a huge increase in social media presence making Lewis Road

Creamery a household name in New Zealand. Lewis Road Creamery currently leads the

flavoured milk category in New Zealand with 33%. The founding of Lewis Road Creamery

shows that the company values high quality products that consumers are excited about. They

are focused on providing customers with exciting new products. Lewis Road Creamery

separate themselves from the competition with their boutique and almost up market

7

competition will have an effect on how companies will have to market their products.

The second important trend is the ecological implications of the dairy industry. New research

has found that dairy farming and livestock is a major reason behind climate change. Because

the dairy industry is so produces so much milk, companies must look for a way to promote a

more sustainable method of farming. This trend is also directly related to the sociocultural

factor. Many people are moving away from dairy products in order to be more eco-friendly.

Systems and processes in dairy farming have been so well established for so long, employing

new methods will be a very difficult undertaking and may cost companies a lot of money in

its initial stages, also possibly raising the prices of milk

3. Internal Analysis

3.1. Strategic Profile

Lewis Road Creamery began as a boutique dairy company out of ex-advertising guru’s Peter

Cullinane's kitchen in 2011. The company was founded as a niche, boutique dairy company for

customers wanting higher quality dairy products. The company remained popular in local

circles but saw it’s prominent rise to popularity following its partnership with Whittakers

chocolate. This caused a huge increase in social media presence making Lewis Road

Creamery a household name in New Zealand. Lewis Road Creamery currently leads the

flavoured milk category in New Zealand with 33%. The founding of Lewis Road Creamery

shows that the company values high quality products that consumers are excited about. They

are focused on providing customers with exciting new products. Lewis Road Creamery

separate themselves from the competition with their boutique and almost up market

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

branding. Lewis Road Creamery is available in the majority of major supermarkets, making

high quality products available ot the average consumer. As illustrated through their initial

rise alongside Whittakers chocolate, Lewis Road Creamery is focused on growth through

partnerships in order to offer new products that other dairy manufacturers cannot. Lewis

Road Creamery already has a strong foothold in the New Zealand market making

international expansion an important long term goal.

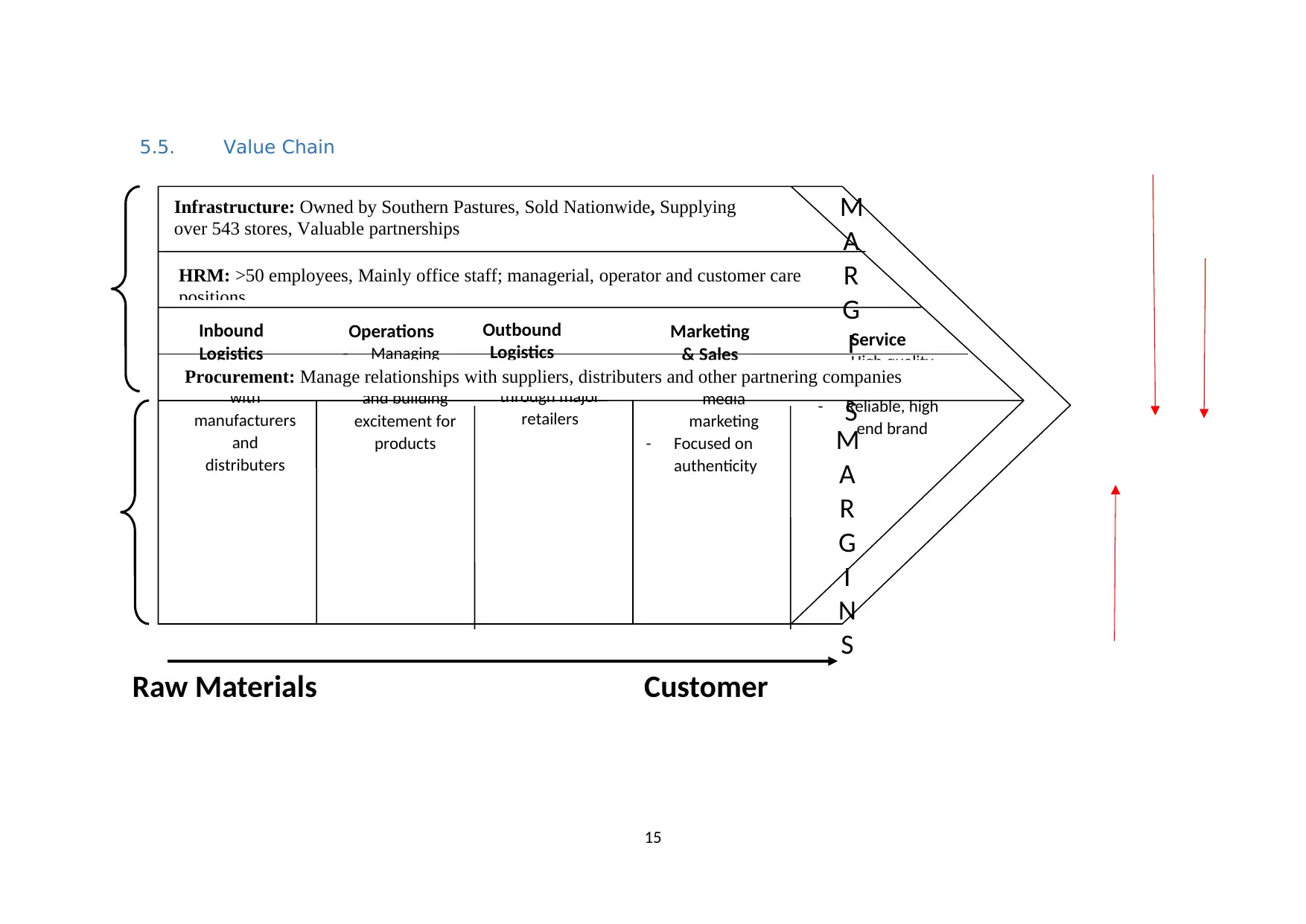

3.2. Value Chain

Following the process learned in Week 4, write up a summary of your Value Chain Analysis

(and put the Value Chain chart in the Appendix). Focus specifically on the linkages between

different activities, and reporting any areas of inconsistency across the value chain. You

should also link the value chain of your company to its business-level strategy (Week 7).

The majority of Lewis Road Creamery’s operation consist of logistics management. Lewis

Road Creamery does not have a factory and rely on manufacturers to create their products.

Lewis Road Creamery is owned by farmland investment fund Southern Pastures. Lewis Road

Creamery products are created with Southern Pastures resources. Along with production,

another important logistical process is managing the distribution of Lewis Road Creamery

products. The majority of strict Lewis Road Creamery employees are responsible for

managing the logistics of the products being manufactured to being placed on supermarket

shelves. The linkages of this process are seen throughout the value chain such as the

procurement, technology, logistics, operations and service. Another valuable component of

the value chain is the marketing of Lewis Road Creamery. Lewis Road Creamery relies on

the strength of its brand in order to generate sales. This means that the company values

managing its online presence as well as trying to secure partnerships with other popular

brands. When discussing their marketing strategy there are links that can be made between

8

high quality products available ot the average consumer. As illustrated through their initial

rise alongside Whittakers chocolate, Lewis Road Creamery is focused on growth through

partnerships in order to offer new products that other dairy manufacturers cannot. Lewis

Road Creamery already has a strong foothold in the New Zealand market making

international expansion an important long term goal.

3.2. Value Chain

Following the process learned in Week 4, write up a summary of your Value Chain Analysis

(and put the Value Chain chart in the Appendix). Focus specifically on the linkages between

different activities, and reporting any areas of inconsistency across the value chain. You

should also link the value chain of your company to its business-level strategy (Week 7).

The majority of Lewis Road Creamery’s operation consist of logistics management. Lewis

Road Creamery does not have a factory and rely on manufacturers to create their products.

Lewis Road Creamery is owned by farmland investment fund Southern Pastures. Lewis Road

Creamery products are created with Southern Pastures resources. Along with production,

another important logistical process is managing the distribution of Lewis Road Creamery

products. The majority of strict Lewis Road Creamery employees are responsible for

managing the logistics of the products being manufactured to being placed on supermarket

shelves. The linkages of this process are seen throughout the value chain such as the

procurement, technology, logistics, operations and service. Another valuable component of

the value chain is the marketing of Lewis Road Creamery. Lewis Road Creamery relies on

the strength of its brand in order to generate sales. This means that the company values

managing its online presence as well as trying to secure partnerships with other popular

brands. When discussing their marketing strategy there are links that can be made between

8

marketing, human resource management and technology. It is also important to recognise that

securing partnerships for the company ties in with other logistical processes of the company.

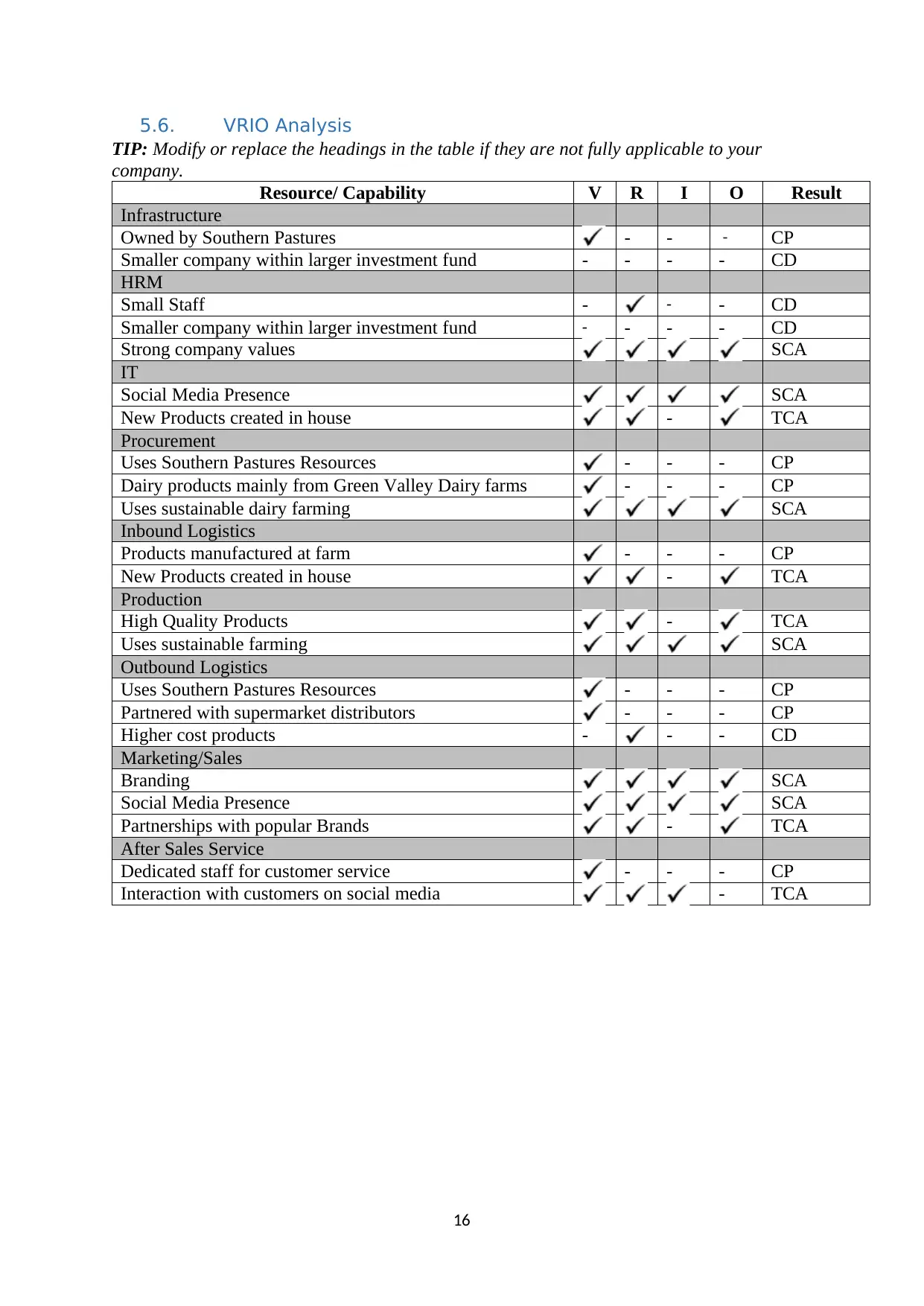

3.3. Competitive Advantage (VRIO) Analysis

Following the process learned in Week 5, write up a summary of your VRIO analysis here.

Concentrate on reporting TCAs, SCAs and CDs. Make a comment on core competence (if

appropriate), referring to the core competence ‘test’ (Week 5).

In the VRIO analysis it is clear that the majority of the company’s advantages come from the

strength of their branding and popularity. Lewis Road Creamery’s marketing and branding is

an advantage that is incredibly valuable and incredibly difficult to replicate. It is also

important to recognise that the company is setup to take advantage of this by interacting with

customers and maintaining brand recognition. Lewis Road Creamery has a lot of competitive

parity in the manufacturing and distribution process as a result of them being owned by a

larger entity. One of the most important competitive disadvantages to recognise is the higher

price point of their products. Because Lewis Road Creamery operates in the supermarket

sector, price point is an important part of informing a consumers decision. Because of the

higher price, Lewis Road Creamery will often lose to its competitors, making it a clear

competitive disadvantage. A temporary advantage of Lewis Road Creamery is its ability to

make new products as well as make partnerships with popular brands. This aspect of Lewis

Road Creamery is not difficult to imitate, the means that companies will try to pursue

lucrative partnerships in the future in order to grow their brand.

9

securing partnerships for the company ties in with other logistical processes of the company.

3.3. Competitive Advantage (VRIO) Analysis

Following the process learned in Week 5, write up a summary of your VRIO analysis here.

Concentrate on reporting TCAs, SCAs and CDs. Make a comment on core competence (if

appropriate), referring to the core competence ‘test’ (Week 5).

In the VRIO analysis it is clear that the majority of the company’s advantages come from the

strength of their branding and popularity. Lewis Road Creamery’s marketing and branding is

an advantage that is incredibly valuable and incredibly difficult to replicate. It is also

important to recognise that the company is setup to take advantage of this by interacting with

customers and maintaining brand recognition. Lewis Road Creamery has a lot of competitive

parity in the manufacturing and distribution process as a result of them being owned by a

larger entity. One of the most important competitive disadvantages to recognise is the higher

price point of their products. Because Lewis Road Creamery operates in the supermarket

sector, price point is an important part of informing a consumers decision. Because of the

higher price, Lewis Road Creamery will often lose to its competitors, making it a clear

competitive disadvantage. A temporary advantage of Lewis Road Creamery is its ability to

make new products as well as make partnerships with popular brands. This aspect of Lewis

Road Creamery is not difficult to imitate, the means that companies will try to pursue

lucrative partnerships in the future in order to grow their brand.

9

4. Strategic Issues: SW+OT

Following the process learned in Week 6, report (approx. 1 page) on the key strengths and

weaknesses of the company (S+W) from across the internal analysis. Combine these with the

opportunities and threats (O+T) from your Assessment 1, and report on what the key issues

are facing the company. These may be problems or opportunities to pursue in the future.

Include a full SWOT figure in the Appendix.

The most obvious key strength for Lewis Road Creamery is the strength of their

branding and their loyal customer base. Lewis Road Creamery has created a household name

that is very difficult replicate. Strong branding along with their partnerships with other brands

allow Lewis Road Creamery to consistently produce high sales numbers. Another important

strength are the strong key values which uphold sustainable farming and high quality

products. This further reinforces their reputation and supports environmentally friendly

production.

The largest weakness of Lewis Road Creamery is their reliance on other companies,

with their ownership and their reliance on famers to produce raw dairy material. This means

that Lewis Road Creamery cannot be sustained independently and will always be at the

mercy of their superiors. Another important weakness is the price point. Because of the high

quality boutique nature of Lewis Road Creamery, many customers will choose their

competitors because of the higher price for their products

The dairy industry is highly concentrated with the majority of the industry functioning

around Fonterra, with access to most of the resources and materials as well as owning a

majority of the manufacturing firms in the industry This has forced other companies to seek

more specialised avenues, creating more niche products for different types of customers. This

is an obvious threat as so much of the industry is dependent on the availability of milk and

whether current practices are sustainable

10

Following the process learned in Week 6, report (approx. 1 page) on the key strengths and

weaknesses of the company (S+W) from across the internal analysis. Combine these with the

opportunities and threats (O+T) from your Assessment 1, and report on what the key issues

are facing the company. These may be problems or opportunities to pursue in the future.

Include a full SWOT figure in the Appendix.

The most obvious key strength for Lewis Road Creamery is the strength of their

branding and their loyal customer base. Lewis Road Creamery has created a household name

that is very difficult replicate. Strong branding along with their partnerships with other brands

allow Lewis Road Creamery to consistently produce high sales numbers. Another important

strength are the strong key values which uphold sustainable farming and high quality

products. This further reinforces their reputation and supports environmentally friendly

production.

The largest weakness of Lewis Road Creamery is their reliance on other companies,

with their ownership and their reliance on famers to produce raw dairy material. This means

that Lewis Road Creamery cannot be sustained independently and will always be at the

mercy of their superiors. Another important weakness is the price point. Because of the high

quality boutique nature of Lewis Road Creamery, many customers will choose their

competitors because of the higher price for their products

The dairy industry is highly concentrated with the majority of the industry functioning

around Fonterra, with access to most of the resources and materials as well as owning a

majority of the manufacturing firms in the industry This has forced other companies to seek

more specialised avenues, creating more niche products for different types of customers. This

is an obvious threat as so much of the industry is dependent on the availability of milk and

whether current practices are sustainable

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

When analysing competitors it is important to recognise how other companies choose

to market their products. Because the majority of dairy products are distributed through

supermarkets, it is not an effective strategy for smaller companies to try and directly compete

with larger corporations. As seen with companies like Open Country Dairy and Tatua, they

are marketing their products to meet certain nutritional needs and as higher quality. This

strategy will work effectively for Lewis Road Creamery as the boutique high quality,

decadent market behind the product will attract a specific kind of consumer. This is an

opportunity available for Lewis Road Creamery to capitalise on.

11

to market their products. Because the majority of dairy products are distributed through

supermarkets, it is not an effective strategy for smaller companies to try and directly compete

with larger corporations. As seen with companies like Open Country Dairy and Tatua, they

are marketing their products to meet certain nutritional needs and as higher quality. This

strategy will work effectively for Lewis Road Creamery as the boutique high quality,

decadent market behind the product will attract a specific kind of consumer. This is an

opportunity available for Lewis Road Creamery to capitalise on.

11

5. Appendices

5.1. Competitor Profiles

Competitor Geographic Scope Range of

Products

Current

Market

Position

Key Strategy

Fonterra International/Domestic Supplies milk

to dairy firms

and

manufactures

its own

products

Dominates

New Zealand

domestic

marker and

supplies other

firms with

resources.

Produces

majority of

exported dairy

for New

Zealand

Supplies the

majority of

the milk to

NZ firms and

creates its

own Milk

products.

Making other

companies

both

customers and

competitors

Open Country

Dairy

International/Domestic Produces

products from

fresh milk

collected from

farms.

Smaller firm

specialising in

specific

products.

Products

available

globally but

more focused

domestically

Provide

customers

with higher

quality dairy

products such

as milk

proteins,

powders, fats,

and cheeses

Tatua Domestic Milk powders

and nutritional

products

Smaller firm

specialising in

specific

products

Specialises in

dairy

ingredients

and dairy

foods for local

consumers

Yashili International Milk formula

products

International

company with

influence in

different

markets

Chinese

owned

company with

a New

Zealand sector

specialising in

nutritional

dairy

products.

Selling to

health

conscious

customers

Meadow

Fresh

International/Domestic Milk, cheese

and yoghurt

Section of a

larger

corporation

Company

owned by

Goodman

12

5.1. Competitor Profiles

Competitor Geographic Scope Range of

Products

Current

Market

Position

Key Strategy

Fonterra International/Domestic Supplies milk

to dairy firms

and

manufactures

its own

products

Dominates

New Zealand

domestic

marker and

supplies other

firms with

resources.

Produces

majority of

exported dairy

for New

Zealand

Supplies the

majority of

the milk to

NZ firms and

creates its

own Milk

products.

Making other

companies

both

customers and

competitors

Open Country

Dairy

International/Domestic Produces

products from

fresh milk

collected from

farms.

Smaller firm

specialising in

specific

products.

Products

available

globally but

more focused

domestically

Provide

customers

with higher

quality dairy

products such

as milk

proteins,

powders, fats,

and cheeses

Tatua Domestic Milk powders

and nutritional

products

Smaller firm

specialising in

specific

products

Specialises in

dairy

ingredients

and dairy

foods for local

consumers

Yashili International Milk formula

products

International

company with

influence in

different

markets

Chinese

owned

company with

a New

Zealand sector

specialising in

nutritional

dairy

products.

Selling to

health

conscious

customers

Meadow

Fresh

International/Domestic Milk, cheese

and yoghurt

Section of a

larger

corporation

Company

owned by

Goodman

12

specialising in

dairy products

Fielder selling

a full range of

dairy products

for the

average

consumer

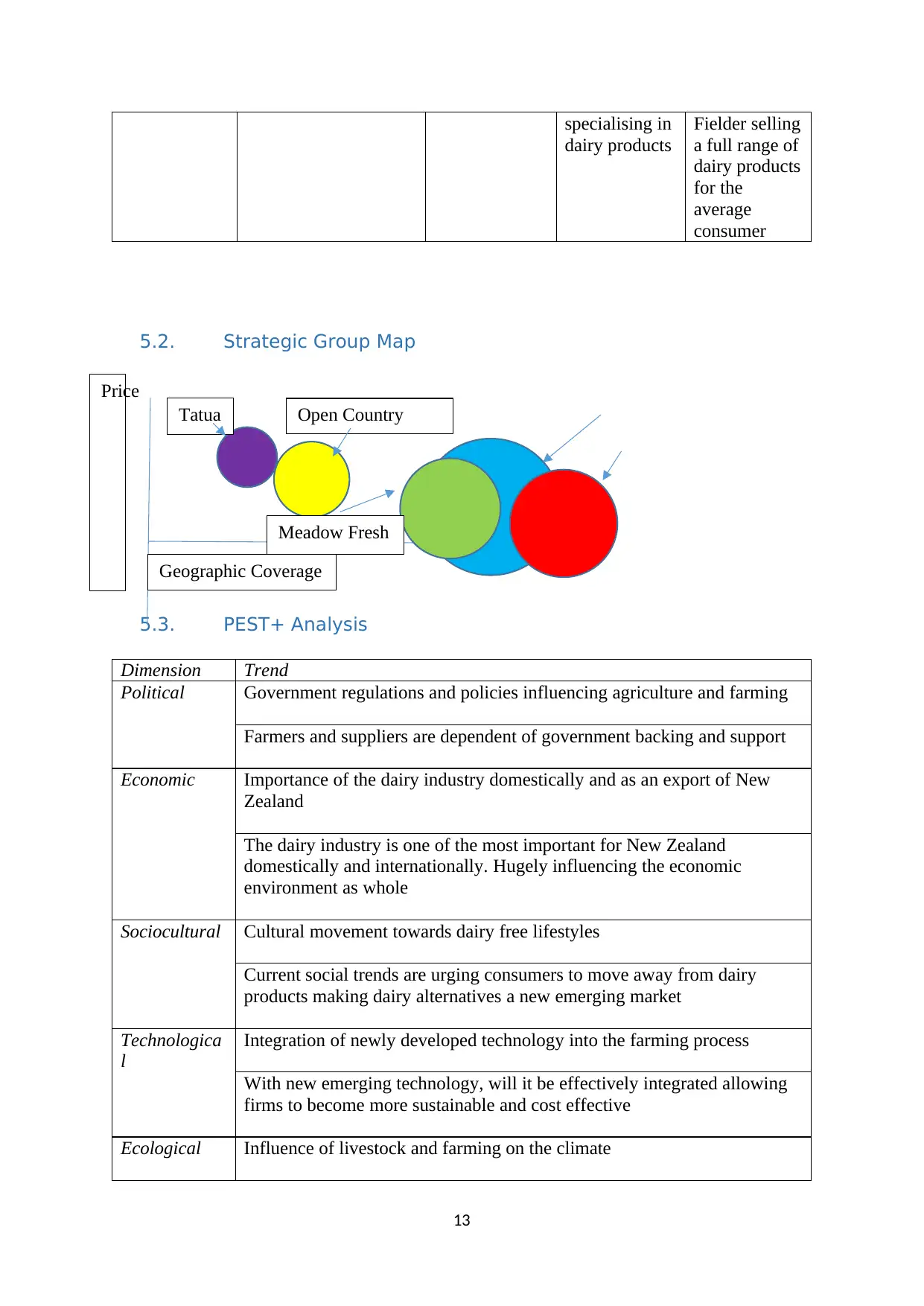

5.2. Strategic Group Map

5.3. PEST+ Analysis

Dimension Trend

Political Government regulations and policies influencing agriculture and farming

Farmers and suppliers are dependent of government backing and support

Economic Importance of the dairy industry domestically and as an export of New

Zealand

The dairy industry is one of the most important for New Zealand

domestically and internationally. Hugely influencing the economic

environment as whole

Sociocultural Cultural movement towards dairy free lifestyles

Current social trends are urging consumers to move away from dairy

products making dairy alternatives a new emerging market

Technologica

l

Integration of newly developed technology into the farming process

With new emerging technology, will it be effectively integrated allowing

firms to become more sustainable and cost effective

Ecological Influence of livestock and farming on the climate

13

Price

Geographic Coverage

Tatua Open Country

Dairy

Meadow Fresh

dairy products

Fielder selling

a full range of

dairy products

for the

average

consumer

5.2. Strategic Group Map

5.3. PEST+ Analysis

Dimension Trend

Political Government regulations and policies influencing agriculture and farming

Farmers and suppliers are dependent of government backing and support

Economic Importance of the dairy industry domestically and as an export of New

Zealand

The dairy industry is one of the most important for New Zealand

domestically and internationally. Hugely influencing the economic

environment as whole

Sociocultural Cultural movement towards dairy free lifestyles

Current social trends are urging consumers to move away from dairy

products making dairy alternatives a new emerging market

Technologica

l

Integration of newly developed technology into the farming process

With new emerging technology, will it be effectively integrated allowing

firms to become more sustainable and cost effective

Ecological Influence of livestock and farming on the climate

13

Price

Geographic Coverage

Tatua Open Country

Dairy

Meadow Fresh

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

New research has shown that dairy farming is a major player in climate

change forcing the dairy industry to consider large changes

Global Prevalence of dairy products in the average consumers diet

5.4. Porters 5 Forces Analysis

14

Threat of New Entrants

- Well established

industry in NZL

- Difficult to enter

Bargaining Power of

Suppliers

- Reliant on suppliers

- All firms dependent

on availability of milk

Intensity of Industry Rivalry

- Larger corporations vs

smaller niche firms

Threat of Substitutes

- Dairy Substitute

products

- Specialist products

Bargaining Power of

Customers

- Majority of dairy

products bought in

supermarkets

change forcing the dairy industry to consider large changes

Global Prevalence of dairy products in the average consumers diet

5.4. Porters 5 Forces Analysis

14

Threat of New Entrants

- Well established

industry in NZL

- Difficult to enter

Bargaining Power of

Suppliers

- Reliant on suppliers

- All firms dependent

on availability of milk

Intensity of Industry Rivalry

- Larger corporations vs

smaller niche firms

Threat of Substitutes

- Dairy Substitute

products

- Specialist products

Bargaining Power of

Customers

- Majority of dairy

products bought in

supermarkets

5.5. Value Chain

15

IT: Large social media presence, management of distribution to major supermarkets

nationwide, New products created in house

M

A

R

G

I

N

S

M

A

R

G

I

N

S

Inbound

Logistics

- Organising

with

manufacturers

and

distributers

Operations

- Managing

partnerships

and building

excitement for

products

Outbound

Logistics

- Distributed

through major

retailers

Service

- High quality

products

- Reliable, high

end brand

Marketing

& Sales

- High social

media

marketing

- Focused on

authenticity

CustomerRaw Materials

Infrastructure: Owned by Southern Pastures, Sold Nationwide, Supplying

over 543 stores, Valuable partnerships

HRM: >50 employees, Mainly office staff; managerial, operator and customer care

positions

Procurement: Manage relationships with suppliers, distributers and other partnering companies

15

IT: Large social media presence, management of distribution to major supermarkets

nationwide, New products created in house

M

A

R

G

I

N

S

M

A

R

G

I

N

S

Inbound

Logistics

- Organising

with

manufacturers

and

distributers

Operations

- Managing

partnerships

and building

excitement for

products

Outbound

Logistics

- Distributed

through major

retailers

Service

- High quality

products

- Reliable, high

end brand

Marketing

& Sales

- High social

media

marketing

- Focused on

authenticity

CustomerRaw Materials

Infrastructure: Owned by Southern Pastures, Sold Nationwide, Supplying

over 543 stores, Valuable partnerships

HRM: >50 employees, Mainly office staff; managerial, operator and customer care

positions

Procurement: Manage relationships with suppliers, distributers and other partnering companies

5.6. VRIO Analysis

TIP: Modify or replace the headings in the table if they are not fully applicable to your

company.

Resource/ Capability V R I O Result

Infrastructure

Owned by Southern Pastures - - - CP

Smaller company within larger investment fund - - - - CD

HRM

Small Staff - - - CD

Smaller company within larger investment fund - - - - CD

Strong company values SCA

IT

Social Media Presence SCA

New Products created in house - TCA

Procurement

Uses Southern Pastures Resources - - - CP

Dairy products mainly from Green Valley Dairy farms - - - CP

Uses sustainable dairy farming SCA

Inbound Logistics

Products manufactured at farm - - - CP

New Products created in house - TCA

Production

High Quality Products - TCA

Uses sustainable farming SCA

Outbound Logistics

Uses Southern Pastures Resources - - - CP

Partnered with supermarket distributors - - - CP

Higher cost products - - - CD

Marketing/Sales

Branding SCA

Social Media Presence SCA

Partnerships with popular Brands - TCA

After Sales Service

Dedicated staff for customer service - - - CP

Interaction with customers on social media - TCA

16

TIP: Modify or replace the headings in the table if they are not fully applicable to your

company.

Resource/ Capability V R I O Result

Infrastructure

Owned by Southern Pastures - - - CP

Smaller company within larger investment fund - - - - CD

HRM

Small Staff - - - CD

Smaller company within larger investment fund - - - - CD

Strong company values SCA

IT

Social Media Presence SCA

New Products created in house - TCA

Procurement

Uses Southern Pastures Resources - - - CP

Dairy products mainly from Green Valley Dairy farms - - - CP

Uses sustainable dairy farming SCA

Inbound Logistics

Products manufactured at farm - - - CP

New Products created in house - TCA

Production

High Quality Products - TCA

Uses sustainable farming SCA

Outbound Logistics

Uses Southern Pastures Resources - - - CP

Partnered with supermarket distributors - - - CP

Higher cost products - - - CD

Marketing/Sales

Branding SCA

Social Media Presence SCA

Partnerships with popular Brands - TCA

After Sales Service

Dedicated staff for customer service - - - CP

Interaction with customers on social media - TCA

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

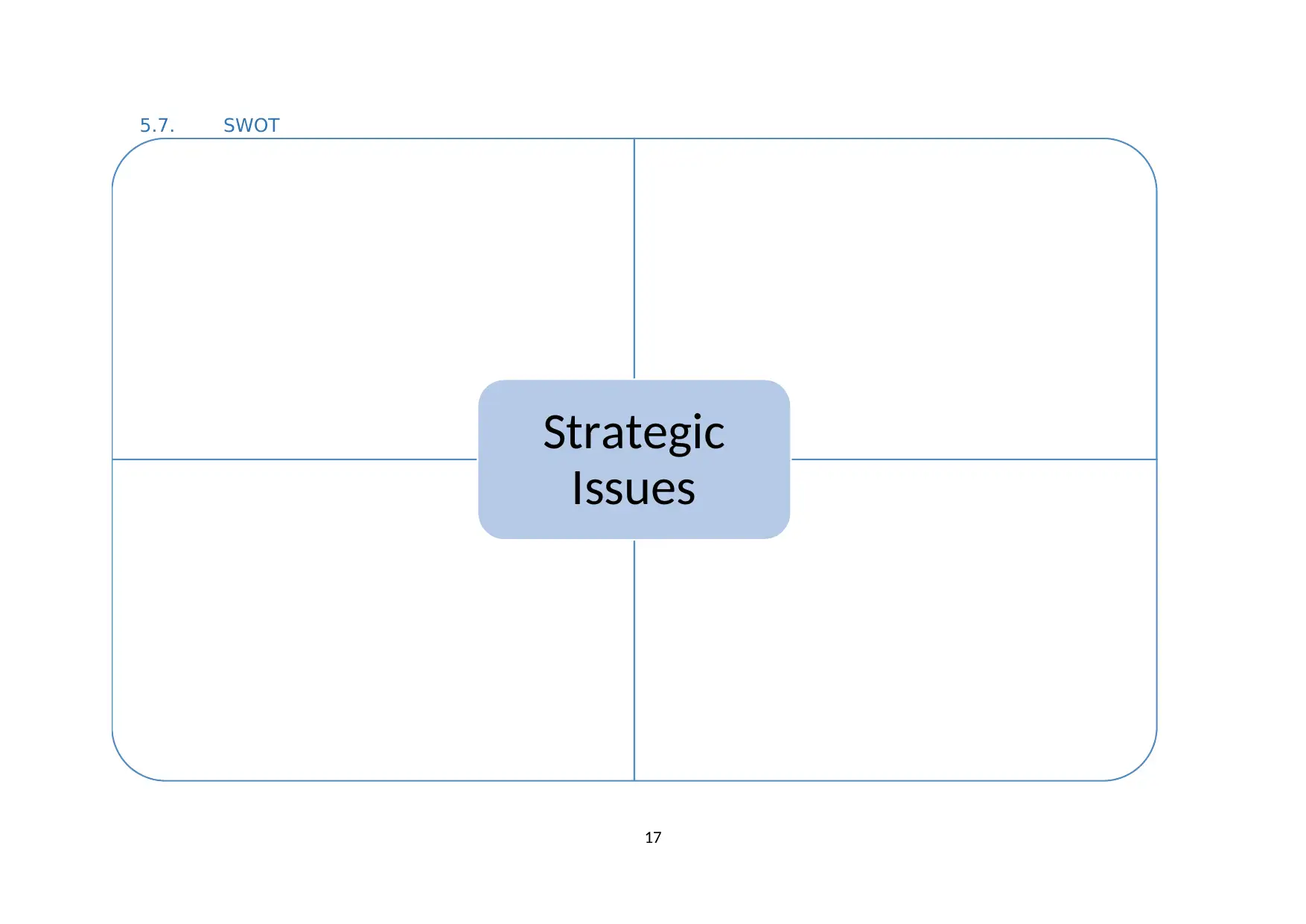

5.7. SWOT

17

Strengths

- Strong branding

- Social Media Presence

- Key company values

Opportunities

- Niche products

- Smaller company

Weaknesses

- Reliance on larger firm

- Reliance on Farms

- Higher price point

Threats

- Fonterra Dominance

- Availability of raw materials

Strategic

Issues

17

Strengths

- Strong branding

- Social Media Presence

- Key company values

Opportunities

- Niche products

- Smaller company

Weaknesses

- Reliance on larger firm

- Reliance on Farms

- Higher price point

Threats

- Fonterra Dominance

- Availability of raw materials

Strategic

Issues

6. Reference List

Armstrong, G., Farley, H., Gray, J., & Durkin, M. (2005). Marketing health‐enhancing foods:

implications from the dairy sector. Marketing Intelligence & Planning.

Aschakulporn, P., & Zhang, J. E. (2020). New Zealand whole milk powder

options. Accounting & Finance.

Barboza, M., Myers, M., & Gardner, L. (2011). Information technology multisourcing at

fonterra: a case study of the world’s largest exporter of dairy ingredients.

Bridges, M. (2018). Moo-ove over, cow’s milk: The rise of plant-based dairy

alternatives. Practical Gastroenterology, 21.

Clark, D. A., Caradus, J. R., Monaghan, R. M., Sharp, P., & Thorrold, B. S. (2007). Issues

and options for future dairy farming in New Zealand. New Zealand journal of

agricultural research, 50(2), 203-221.

Dobson, W. D. (1990). The competitive strategy of the New Zealand dairy

board. Agribusiness, 6(6), 541-558.

Dooley, A. E., Smeaton, D. C., Sheath, G. W., & Ledgard, S. F. (2009). Application of

multiple criteria decision analysis in the New Zealand agricultural industry. Journal

of Multi‐Criteria Decision Analysis, 16(1‐2), 39-53.

DuPuis, E. M. (2000). Not in my body: BGH and the rise of organic milk. Agriculture and

human values, 17(3), 285-295.

18

Armstrong, G., Farley, H., Gray, J., & Durkin, M. (2005). Marketing health‐enhancing foods:

implications from the dairy sector. Marketing Intelligence & Planning.

Aschakulporn, P., & Zhang, J. E. (2020). New Zealand whole milk powder

options. Accounting & Finance.

Barboza, M., Myers, M., & Gardner, L. (2011). Information technology multisourcing at

fonterra: a case study of the world’s largest exporter of dairy ingredients.

Bridges, M. (2018). Moo-ove over, cow’s milk: The rise of plant-based dairy

alternatives. Practical Gastroenterology, 21.

Clark, D. A., Caradus, J. R., Monaghan, R. M., Sharp, P., & Thorrold, B. S. (2007). Issues

and options for future dairy farming in New Zealand. New Zealand journal of

agricultural research, 50(2), 203-221.

Dobson, W. D. (1990). The competitive strategy of the New Zealand dairy

board. Agribusiness, 6(6), 541-558.

Dooley, A. E., Smeaton, D. C., Sheath, G. W., & Ledgard, S. F. (2009). Application of

multiple criteria decision analysis in the New Zealand agricultural industry. Journal

of Multi‐Criteria Decision Analysis, 16(1‐2), 39-53.

DuPuis, E. M. (2000). Not in my body: BGH and the rise of organic milk. Agriculture and

human values, 17(3), 285-295.

18

Flett, R., Alpass, F., Humphries, S., Massey, C., Morriss, S., & Long, N. (2004). The

technology acceptance model and use of technology in New Zealand dairy

farming. Agricultural Systems, 80(2), 199-211.

Gray, S., & Le Heron, R. (2010). Globalising New Zealand: Fonterra Co‐operative Group,

and shaping the future. New Zealand Geographer, 66(1), 1-13.

Lees, I., & Lees, N. J. (2016). Competitive advantage through responsible innovation in the

New Zealand's sheep dairy industry (No. 2107-2018-3786).

Ministry of Business, Innovation & Employment. (2017). THE INVESTOR’S GUIDE TO

THE NEW ZEALAND DAIRY INDUSTRY 2017 (No. 104).

https://www.mbie.govt.nz/assets/ebd383c353/investors-guide-to-the-new-zealand-

dairy-industry-2017.pdf

Oesterle, E. C. (1970). Supermarket Dairy Department Analysis.

Rouquette Jr, M., & Aiken, G. E. (2020). Introduction: Management strategies for sustainable

cattle production in Southern Pastures. In Management Strategies for Sustainable

Cattle Production in Southern Pastures (pp. 1-10). Academic Press.

Schiano, A. N., Harwood, W. S., Gerard, P. D., & Drake, M. A. (2020). Consumer perception

of the sustainability of dairy products and plant-based dairy alternatives. Journal of

Dairy Science, 103(12), 11228-11243.

Stringer, C., Tamásy, C., Le Heron, R., & Gray, S. (2008). Growing a global resource-based

company from New Zealand: The case of dairy giant Fonterra (pp. 189-199).

Aldershot, UK: Ashgate.

19

technology acceptance model and use of technology in New Zealand dairy

farming. Agricultural Systems, 80(2), 199-211.

Gray, S., & Le Heron, R. (2010). Globalising New Zealand: Fonterra Co‐operative Group,

and shaping the future. New Zealand Geographer, 66(1), 1-13.

Lees, I., & Lees, N. J. (2016). Competitive advantage through responsible innovation in the

New Zealand's sheep dairy industry (No. 2107-2018-3786).

Ministry of Business, Innovation & Employment. (2017). THE INVESTOR’S GUIDE TO

THE NEW ZEALAND DAIRY INDUSTRY 2017 (No. 104).

https://www.mbie.govt.nz/assets/ebd383c353/investors-guide-to-the-new-zealand-

dairy-industry-2017.pdf

Oesterle, E. C. (1970). Supermarket Dairy Department Analysis.

Rouquette Jr, M., & Aiken, G. E. (2020). Introduction: Management strategies for sustainable

cattle production in Southern Pastures. In Management Strategies for Sustainable

Cattle Production in Southern Pastures (pp. 1-10). Academic Press.

Schiano, A. N., Harwood, W. S., Gerard, P. D., & Drake, M. A. (2020). Consumer perception

of the sustainability of dairy products and plant-based dairy alternatives. Journal of

Dairy Science, 103(12), 11228-11243.

Stringer, C., Tamásy, C., Le Heron, R., & Gray, S. (2008). Growing a global resource-based

company from New Zealand: The case of dairy giant Fonterra (pp. 189-199).

Aldershot, UK: Ashgate.

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TDB Advisory. (2018, April). New Zealand Dairy Companies Review.

https://www.tdb.co.nz/wp-content/uploads/2018/05/TDB-Dairy-Companies-Review-

2018-1.pdf

Tulloch, L., & Judge, P. (2018). Bringing the calf back from the dead: video activism, the

politics of sight and the New Zealand dairy industry. Video Journal of Education and

Pedagogy, 3(1), 1-20.

Utter, J., Scragg, R., & Schaaf, D. (2006). Associations between television viewing and

consumption of commonly advertised foods among New Zealand children and young

adolescents. Public health nutrition, 9(5), 606-612.

Vandevijvere, S., Aitken, C., & Swinburn, B. (2018). Volume, nature and potential imp

Vergé, X. P. C., Dyer, J. A., Desjardins, R. L., & Worth, D. (2007). Greenhouse gas

emissions from the Canadian dairy industry in 2001. Agricultural Systems, 94(3), 683-

693.

Von Keyserlingk, M. A. G., Martin, N. P., Kebreab, E., Knowlton, K. F., Grant, R. J.,

Stephenson, M., ... & Smith, S. I. (2013). Invited review: Sustainability of the US

dairy industry. Journal of dairy science, 96(9), 5405-5425.

Yin, S., Chen, M., Chen, Y., Xu, Y., Zou, Z., & Wang, Y. (2016). Consumer trust in organic

milk of different brands: The role of Chinese organic label. British Food Journal.

20

https://www.tdb.co.nz/wp-content/uploads/2018/05/TDB-Dairy-Companies-Review-

2018-1.pdf

Tulloch, L., & Judge, P. (2018). Bringing the calf back from the dead: video activism, the

politics of sight and the New Zealand dairy industry. Video Journal of Education and

Pedagogy, 3(1), 1-20.

Utter, J., Scragg, R., & Schaaf, D. (2006). Associations between television viewing and

consumption of commonly advertised foods among New Zealand children and young

adolescents. Public health nutrition, 9(5), 606-612.

Vandevijvere, S., Aitken, C., & Swinburn, B. (2018). Volume, nature and potential imp

Vergé, X. P. C., Dyer, J. A., Desjardins, R. L., & Worth, D. (2007). Greenhouse gas

emissions from the Canadian dairy industry in 2001. Agricultural Systems, 94(3), 683-

693.

Von Keyserlingk, M. A. G., Martin, N. P., Kebreab, E., Knowlton, K. F., Grant, R. J.,

Stephenson, M., ... & Smith, S. I. (2013). Invited review: Sustainability of the US

dairy industry. Journal of dairy science, 96(9), 5405-5425.

Yin, S., Chen, M., Chen, Y., Xu, Y., Zou, Z., & Wang, Y. (2016). Consumer trust in organic

milk of different brands: The role of Chinese organic label. British Food Journal.

20

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.