Macroeconomics: Interest Rates and the Australian Housing Market

VerifiedAdded on 2023/06/09

|13

|2037

|97

Essay

AI Summary

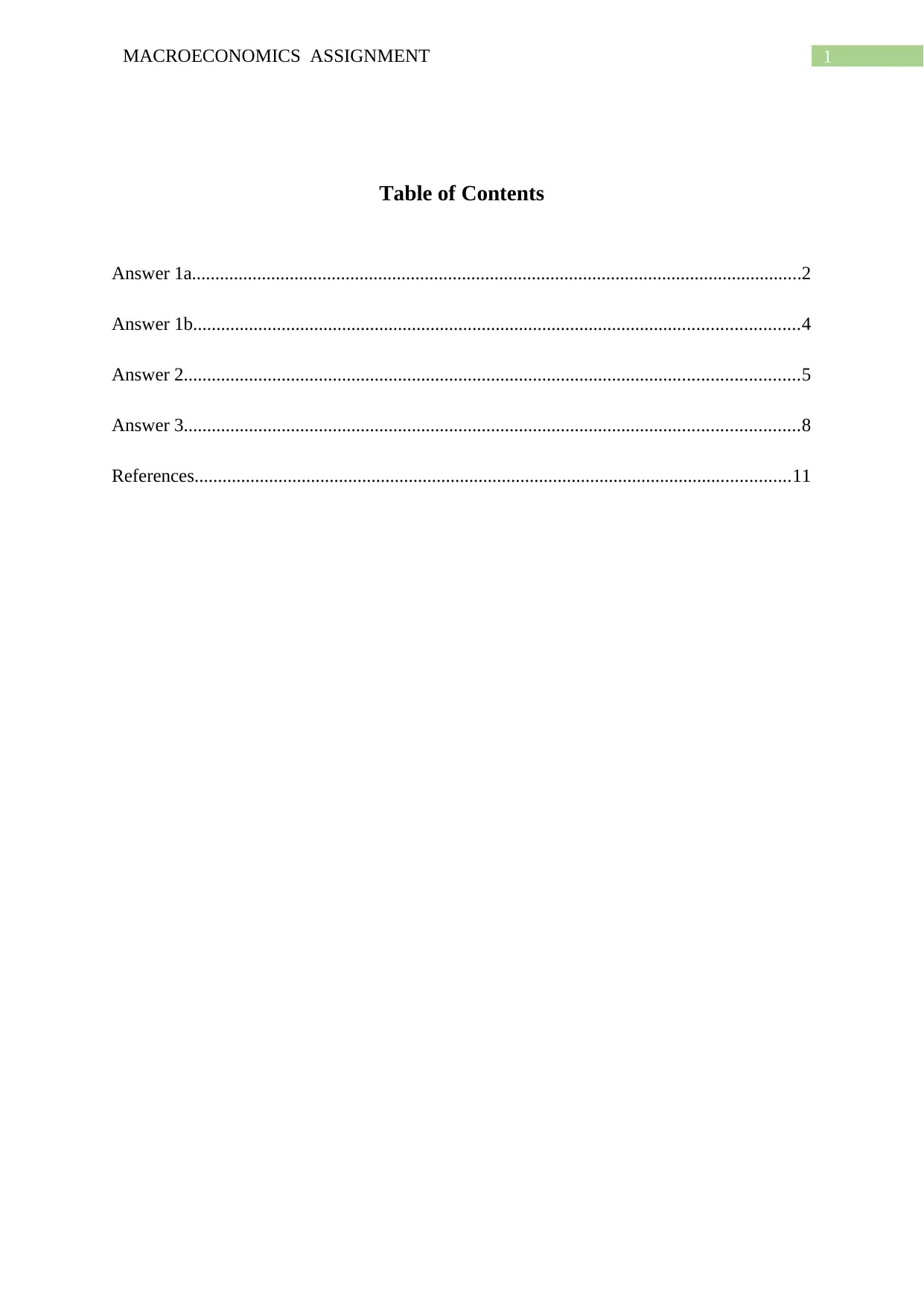

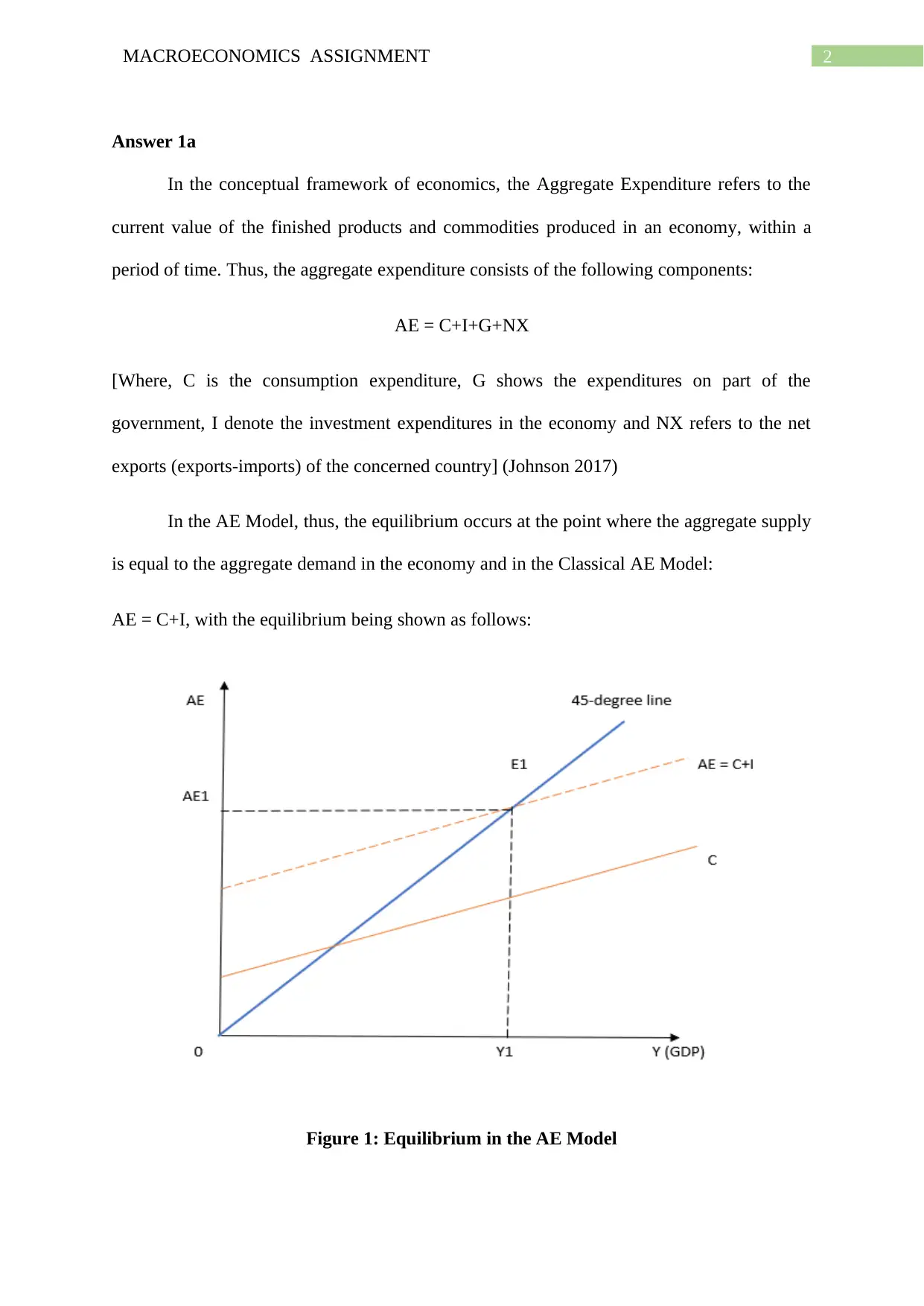

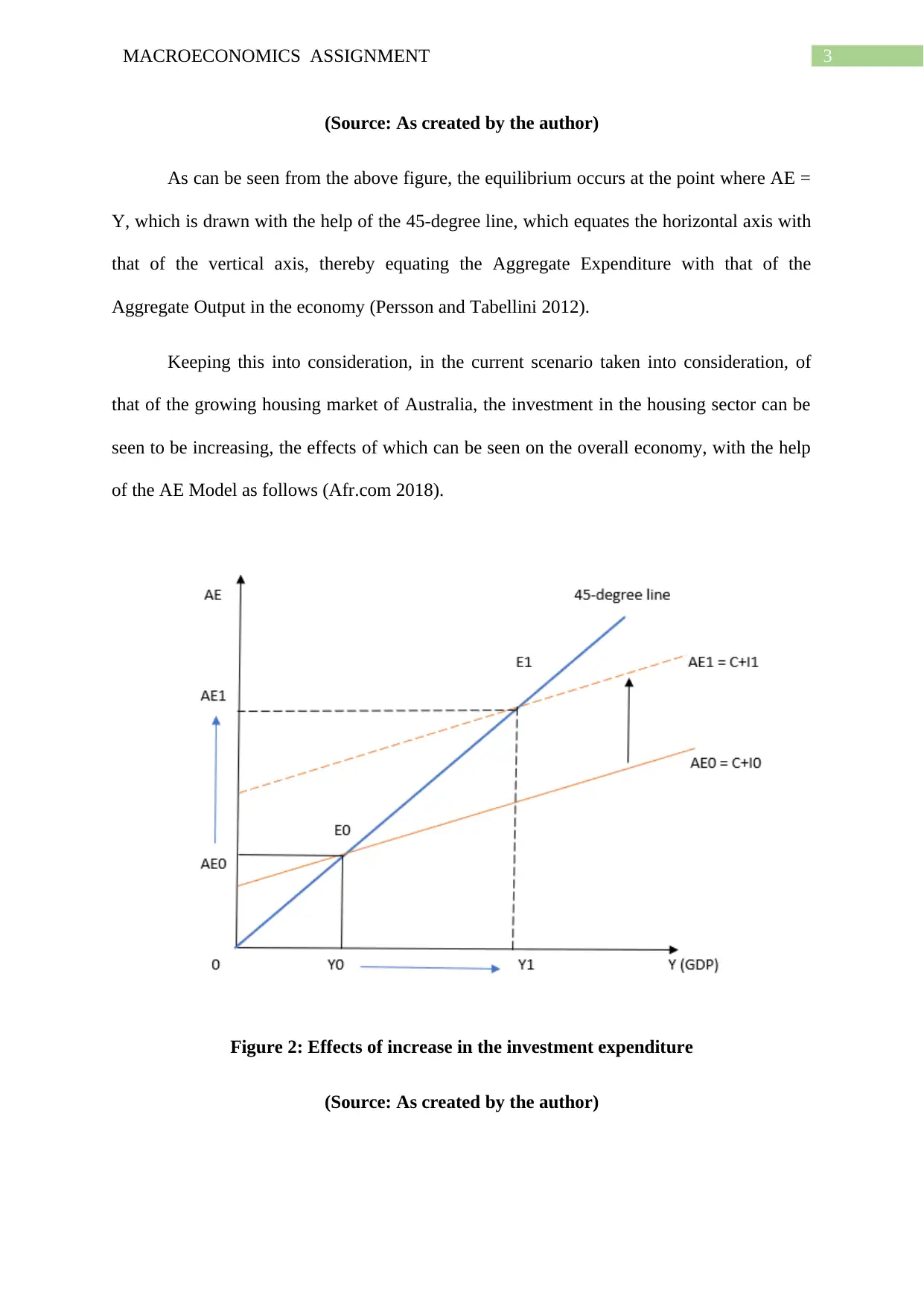

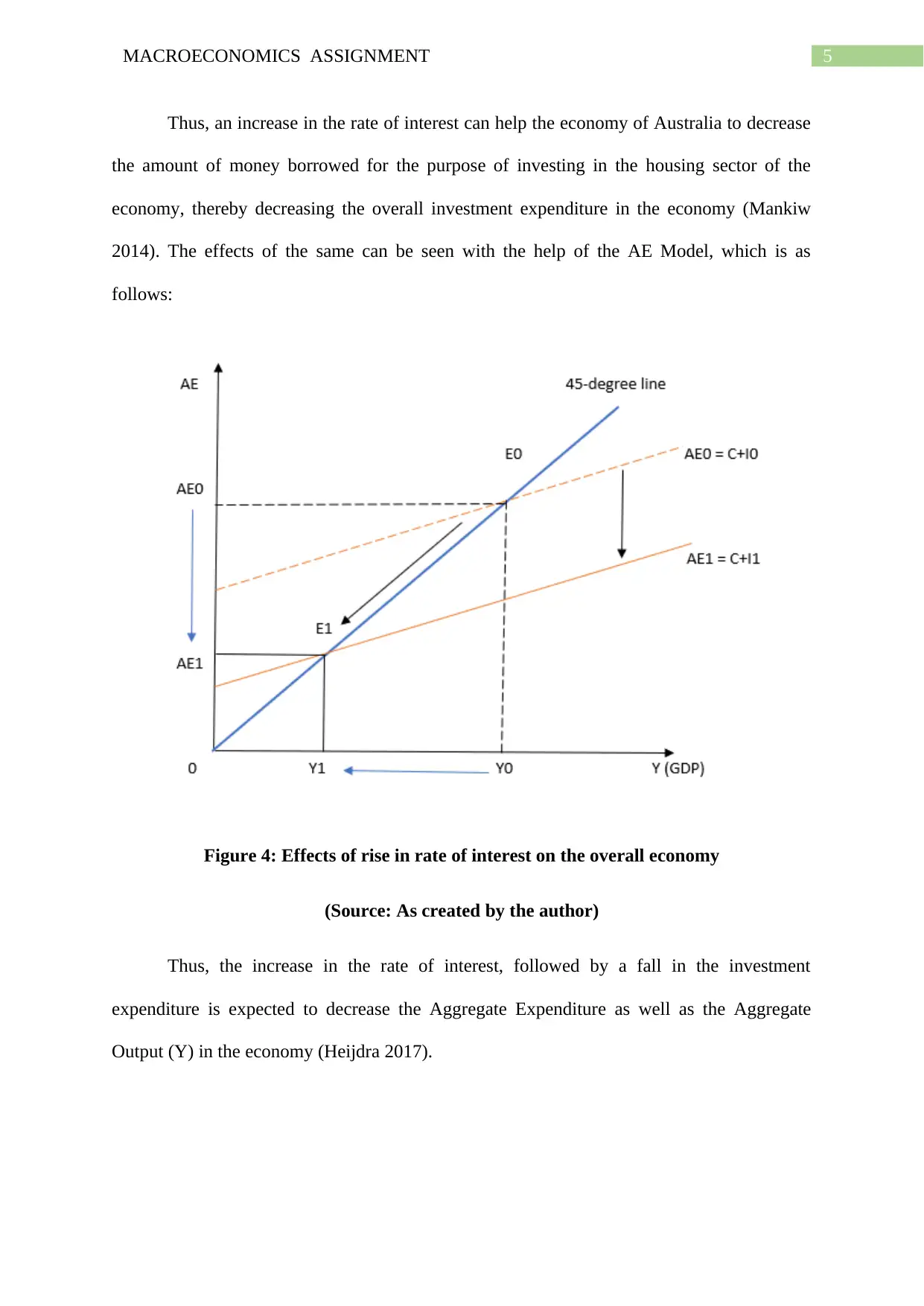

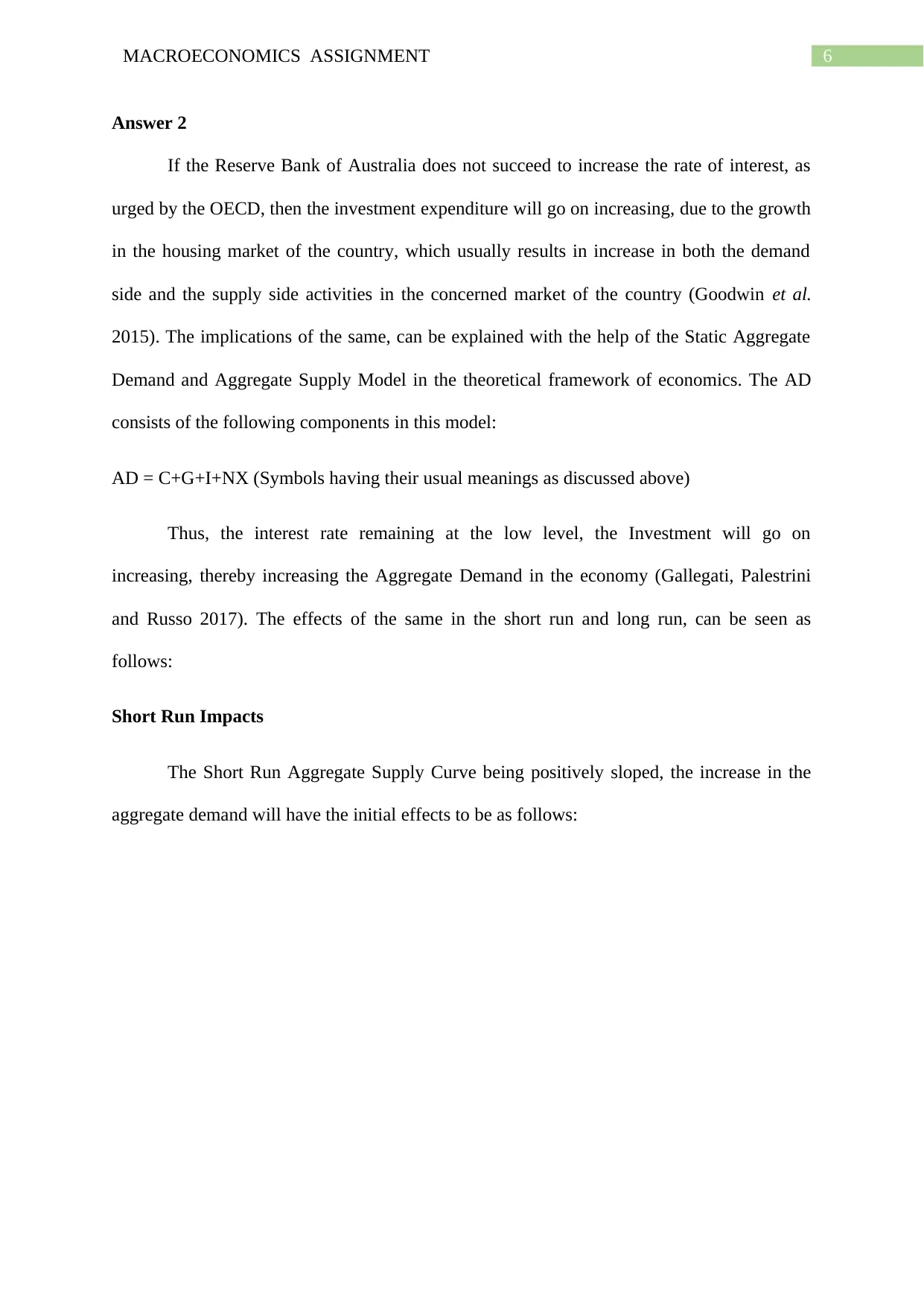

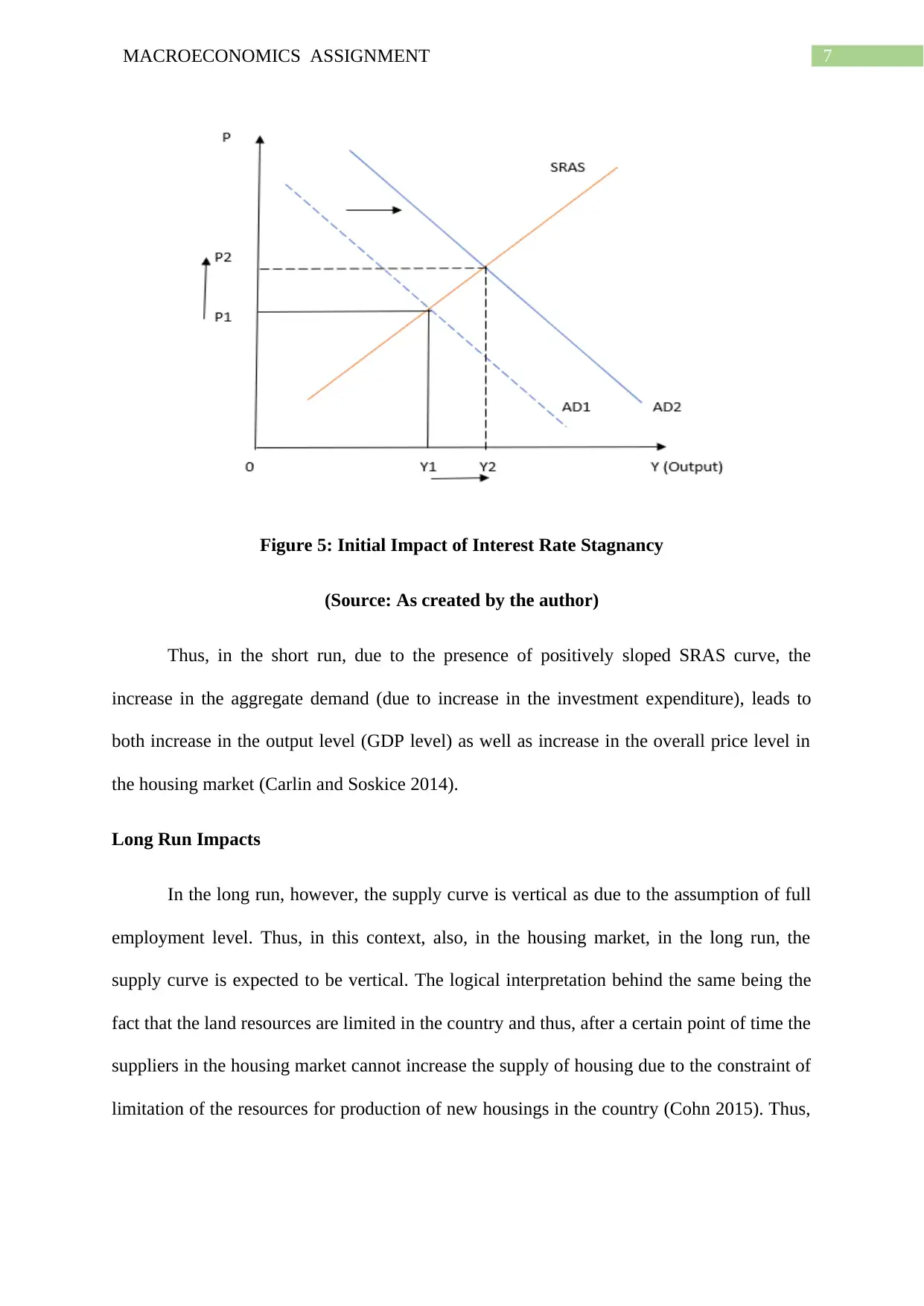

This essay provides a detailed macroeconomic analysis of the Australian housing market, focusing on the impact of interest rates and the recommendations of the OECD. It employs the Aggregate Expenditure (AE) model, the Static Aggregate Demand and Aggregate Supply (AD-AS) model, and the Dynamic AD-AS model to evaluate the effects of interest rate policies on investment, output, and price levels. The analysis considers both short-run and long-run implications, including potential recessionary scenarios and the limitations of land resources. The essay concludes by examining the dynamic interactions between aggregate demand and aggregate supply, highlighting the potential for decreased output and employment if interest rate increases lead to a long-term decline in investment and economic activity. Desklib offers a range of study tools and resources for students.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.