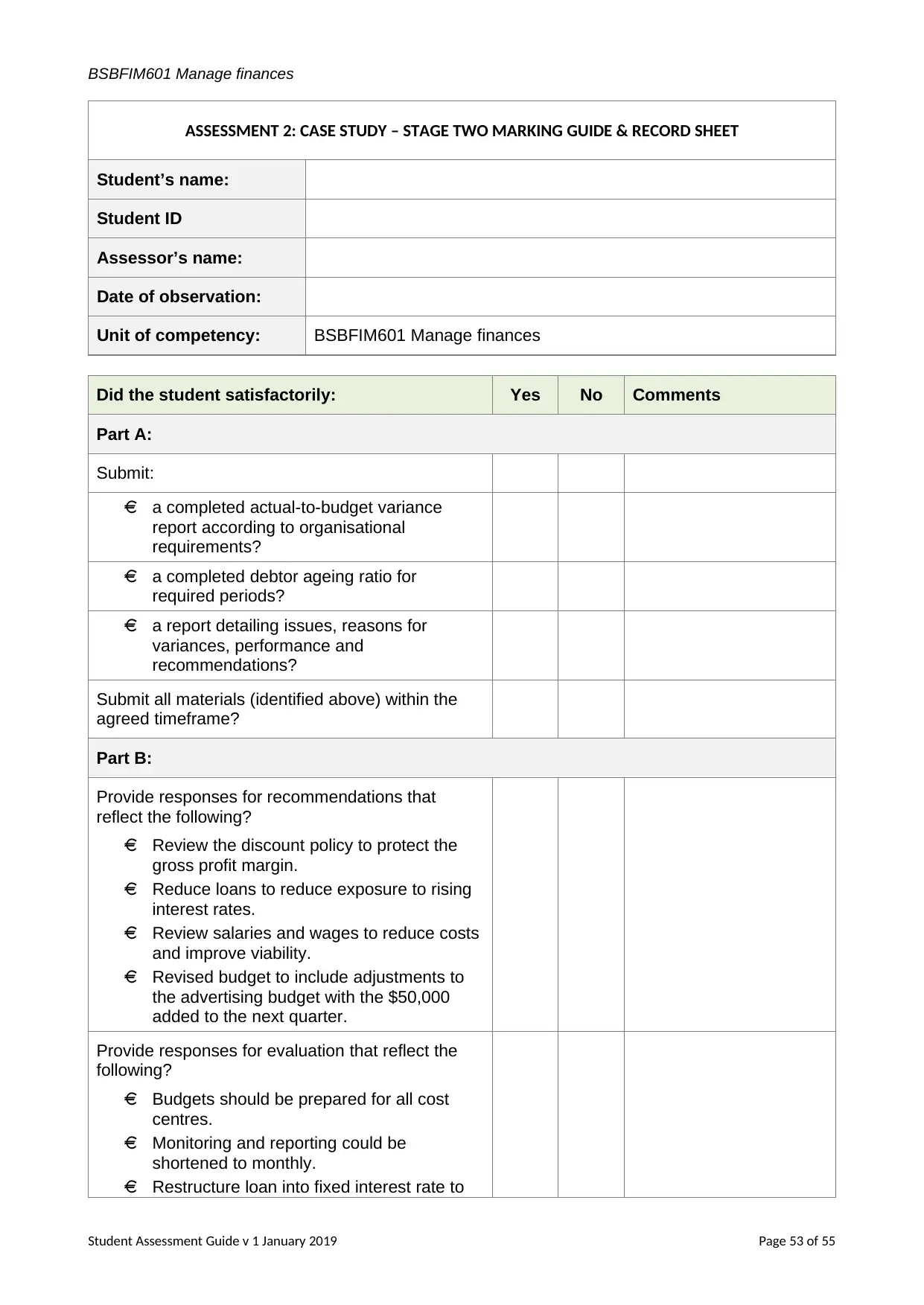

Manage Finances: Assessment Guide for BSBFIM601

VerifiedAdded on 2023/06/18

|55

|16091

|459

AI Summary

The assessment guide for BSBFIM601 Manage Finances includes two assessments: Research Questions and Case Study. The guide provides information about the assessment schedule, instructions, assessment outcomes, and reasonable adjustments. The research questions cover topics such as obligations under the Corporations Act 2001, Australian Accounting Standards, and Privacy Acts and Principles. The case study requires students to undertake budgeting, financial forecasting, and reporting for a simulated business. The guide also outlines the statutory requirements related to tax law compliance for Goods and Services Tax, Fringe Benefits Tax, and Payroll Tax.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ASSESSMENT GUIDE

Student

BSBFIM601 Manage finances

Student

BSBFIM601 Manage finances

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

BSBFIM601 Manage finances

ASSESSMENT

BSBFIM601 Manage finances

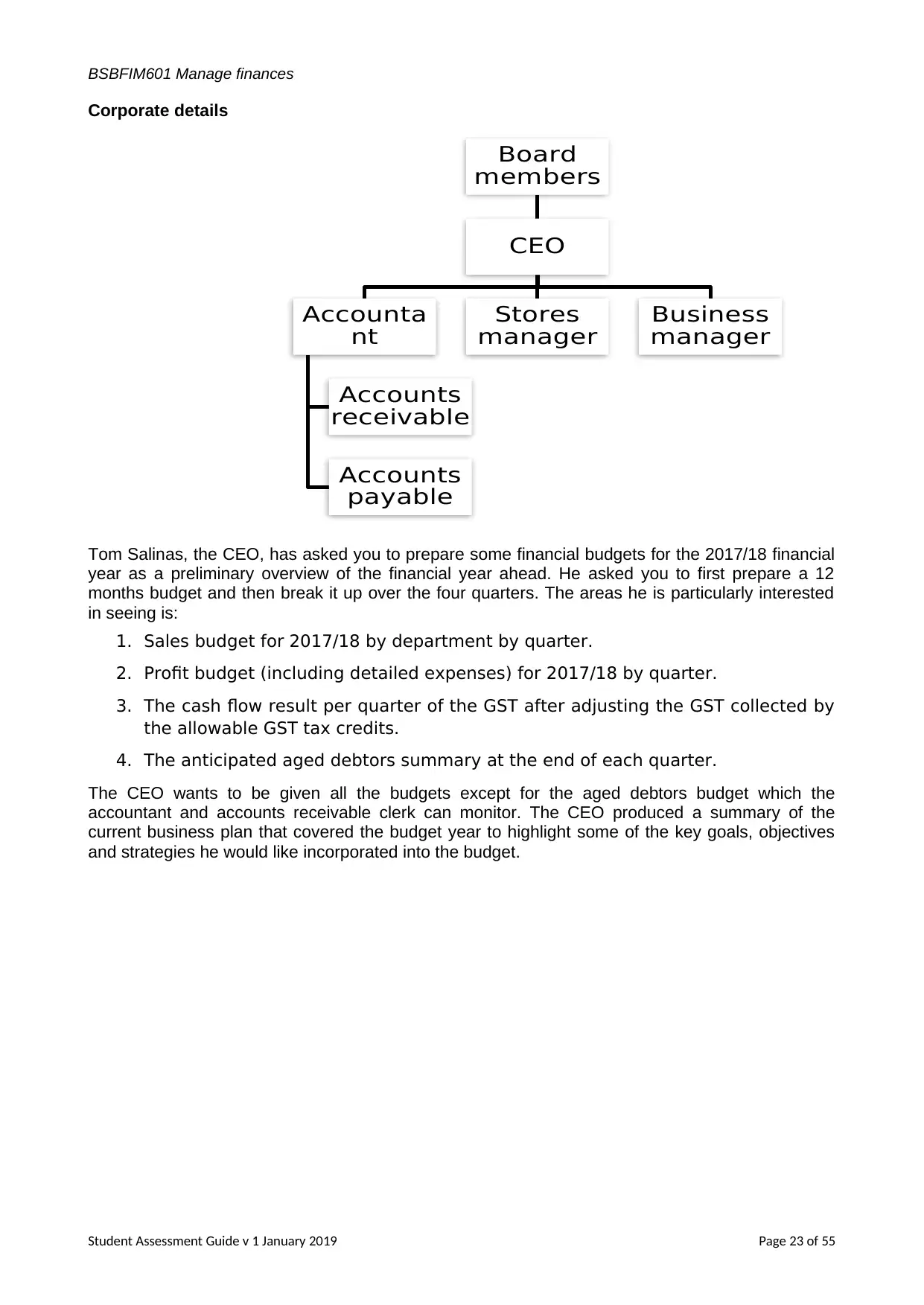

There are two assessments for this unit:

1. Research Questions

Students are to read the questions and respond in writing with the most suitable answer. There are

six questions, all of which must be completed. Most questions require short answers although

some questions require a more detailed response. Students may use various sources of

information including workbooks, internet and other documents, but must list and reference their

sources. Suggested sources and websites are provided.

You need to advise students when this is due. Model answers and a record sheet are provided.

2. Case Study

For this assessment students are to undertake budgeting, financial forecasting and reporting and

to allocate and manage resources to achieve the required outputs for a simulated business.

The case study is in two stages each with 2 parts. Students must complete them all.

Stage One: – based on the given financial information about the simulated business, students

are to prepare a number of budgets and then using appropriate formulae, to analyse financial

data to assess and manage risk and identify discrepancies.

Stage One – requires students to analyse discrepancies and produce a report in which they

account for variations. They are then required to participate in a role play, with you, acting in

the role of company CEO in which they discuss the variances and make financial

recommendations in relation to the company’s financial situation.

Instructions and roles for the role play are provided.

You need to advise students when this is due. A marking guide and record sheet are provided. A

model budget and Sample report and ratios are provided in the Appendices.

Students will need access and are expected to use suitable financial management software

Assessment Schedule

Assessment Due Date

1. Research Questions

2. Case Study:

Stage One

Stage Two

Student Assessment Guide v 1 January 2019 Page 2 of 55

ASSESSMENT

BSBFIM601 Manage finances

There are two assessments for this unit:

1. Research Questions

Students are to read the questions and respond in writing with the most suitable answer. There are

six questions, all of which must be completed. Most questions require short answers although

some questions require a more detailed response. Students may use various sources of

information including workbooks, internet and other documents, but must list and reference their

sources. Suggested sources and websites are provided.

You need to advise students when this is due. Model answers and a record sheet are provided.

2. Case Study

For this assessment students are to undertake budgeting, financial forecasting and reporting and

to allocate and manage resources to achieve the required outputs for a simulated business.

The case study is in two stages each with 2 parts. Students must complete them all.

Stage One: – based on the given financial information about the simulated business, students

are to prepare a number of budgets and then using appropriate formulae, to analyse financial

data to assess and manage risk and identify discrepancies.

Stage One – requires students to analyse discrepancies and produce a report in which they

account for variations. They are then required to participate in a role play, with you, acting in

the role of company CEO in which they discuss the variances and make financial

recommendations in relation to the company’s financial situation.

Instructions and roles for the role play are provided.

You need to advise students when this is due. A marking guide and record sheet are provided. A

model budget and Sample report and ratios are provided in the Appendices.

Students will need access and are expected to use suitable financial management software

Assessment Schedule

Assessment Due Date

1. Research Questions

2. Case Study:

Stage One

Stage Two

Student Assessment Guide v 1 January 2019 Page 2 of 55

BSBFIM601 Manage finances

INFORMATION FOR STUDENTS

General Assessment Information

This information is designed to provide you with a full overview of the tasks you need to

successfully complete to be deemed competent in this unit.

You must achieve a satisfactory performance in each of the assessment tasks in order to be

deemed competent in the relevant unit. Where necessary, the assessment tasks are divided into

parts or steps. These are designed to take you through a step by step approach to completing the

activities.

Instructions

First and foremost, please contact your assessor to discuss any necessary adjustments that may

need to be made prior to completing these tasks. The instructions for each of the assessment

tasks are logically sequenced. If you have any questions, contact your assessor immediately. If

there is a practical component to your assessment, you will need to discuss the arrangements for

its completion with your assessor in advance.

Assessment Cover Sheet

Once you have completed all of the tasks, complete the Assessment Cover Sheet, sign the

declaration and forward along with your documentation to your assessor. It should be uploaded

along with the assessment on to the RTO manager.

Submitting Assessment Tasks

All written assessment tasks must be typed and submitted with the provided cover sheet.

Your trainer/assessor will tell you when assessments are due. It is your responsibility to ensure

that assessment tasks are submitted on or before their due date.

Extensions for individual assessment tasks may be negotiated with your trainer in specific

circumstances. You must request this prior to the due date, and extensions due to illness will

require a medical certificate. Extensions will be confirmed by your trainer/assessor.

Where assessment tasks are submitted following the conclusion of the unit of competency without

a medical certificate or extension, a late submission fee for each assessment task will be charged.

Assessment Outcomes

There are two outcomes of assessment tasks: S = Satisfactory and NS = Not Satisfactory (requires

more training and experience).

You will be awarded C = Competent on completion of the unit when you have achieved S for all

completed assessment tasks and by meeting all the performance criteria. If you fail to meet this

requirement, you will receive the result NYC = Not Yet Competent and will be eligible to be re-

assessed according to George Brown College policy.

If you are deemed Not Competent by your assessor and require re-assessment, you will be

informed of the process. A fee may be charged according to George Brown College policy.

If all assessment tasks are not completed for a qualification, a certificate will not be awarded. A

Statement of Attainment for completed units of competency will be provided.

Your Results

Your assessor is committed to providing you with detailed feedback on the outcomes of the

assessment and will provide guidance on areas for improvement. In most instances, you should

only need to complete the sections of the assessment that were deemed not satisfactory.

Student Assessment Guide v 1 January 2019 Page 3 of 55

INFORMATION FOR STUDENTS

General Assessment Information

This information is designed to provide you with a full overview of the tasks you need to

successfully complete to be deemed competent in this unit.

You must achieve a satisfactory performance in each of the assessment tasks in order to be

deemed competent in the relevant unit. Where necessary, the assessment tasks are divided into

parts or steps. These are designed to take you through a step by step approach to completing the

activities.

Instructions

First and foremost, please contact your assessor to discuss any necessary adjustments that may

need to be made prior to completing these tasks. The instructions for each of the assessment

tasks are logically sequenced. If you have any questions, contact your assessor immediately. If

there is a practical component to your assessment, you will need to discuss the arrangements for

its completion with your assessor in advance.

Assessment Cover Sheet

Once you have completed all of the tasks, complete the Assessment Cover Sheet, sign the

declaration and forward along with your documentation to your assessor. It should be uploaded

along with the assessment on to the RTO manager.

Submitting Assessment Tasks

All written assessment tasks must be typed and submitted with the provided cover sheet.

Your trainer/assessor will tell you when assessments are due. It is your responsibility to ensure

that assessment tasks are submitted on or before their due date.

Extensions for individual assessment tasks may be negotiated with your trainer in specific

circumstances. You must request this prior to the due date, and extensions due to illness will

require a medical certificate. Extensions will be confirmed by your trainer/assessor.

Where assessment tasks are submitted following the conclusion of the unit of competency without

a medical certificate or extension, a late submission fee for each assessment task will be charged.

Assessment Outcomes

There are two outcomes of assessment tasks: S = Satisfactory and NS = Not Satisfactory (requires

more training and experience).

You will be awarded C = Competent on completion of the unit when you have achieved S for all

completed assessment tasks and by meeting all the performance criteria. If you fail to meet this

requirement, you will receive the result NYC = Not Yet Competent and will be eligible to be re-

assessed according to George Brown College policy.

If you are deemed Not Competent by your assessor and require re-assessment, you will be

informed of the process. A fee may be charged according to George Brown College policy.

If all assessment tasks are not completed for a qualification, a certificate will not be awarded. A

Statement of Attainment for completed units of competency will be provided.

Your Results

Your assessor is committed to providing you with detailed feedback on the outcomes of the

assessment and will provide guidance on areas for improvement. In most instances, you should

only need to complete the sections of the assessment that were deemed not satisfactory.

Student Assessment Guide v 1 January 2019 Page 3 of 55

BSBFIM601 Manage finances

However, it is important to remember that depending on the task, it may be necessary to repeat the

whole task (for example presentations or the delivery of a training session).

You are entitled to view your results at any time by viewing them once they are uploaded on

RTOManager.

Reasonable Adjustment

George Brown College supports individual differences in the learning environment and provides

‘reasonable adjustment’ in training and assessment activities to support every learner. If you have

any special needs that make it difficult for you to complete your learning or assessments, you

should discuss this with your assessor beforehand and will be provided with reasonable

alternatives to assist you to complete the required tasks such as completing tests verbally or using

an interpreter.

What happens if you do not agree with the assessment result?

If you do not think the assessment process is valid, or disagree with the decision once it is made,

or believe that you have been treated unfairly, you can appeal. The first step is to discuss the

matter with your trainer.

If you still do not agree with the results, refer to the GBC Complaints and Appeals Policy and speak

to the Student Services Team.

Support

While we may not be in a position to assist you with language training or specific LLN training, our

assessors will work with you to ensure that you are supported throughout your qualification. If you

require individual tutoring this may attract an additional fee (see Student Handbook). Support may

be offered by your assessor, or for more specialist support you may need to contact GBC

administration.

A Note on Plagiarism and Referencing

Plagiarism is a form of theft where the work, ideas, inventions etc. of other people are presented as

your own. Information, ideas etc. quoted or paraphrased from another source such as the Internet,

must be acknowledged with “quotation marks” around the relevant words/sentences or ideas and

the source listed in brackets. You must also list the sources at the end of your assessment.

Sources of information, ideas etc. must be provided in alphabetical order by author’s surname

(including author’s full name, name of document/ book / internet etc. and year and place of

publishing) or may be included in brackets in the text.

As a general rule it is advisable to never copy another person’s work. Should it appear that a

student’s work has been copied or does not appear to be authentic, you will be asked to speak to

your Course Coordinator and required to re-submit it. A fee may be charged according to George

Brown College policy.

Contacting the RTO

If you should need further support or assistance please do not hesitate to contact The Student

Services Team.

Student Assessment Guide v 1 January 2019 Page 4 of 55

However, it is important to remember that depending on the task, it may be necessary to repeat the

whole task (for example presentations or the delivery of a training session).

You are entitled to view your results at any time by viewing them once they are uploaded on

RTOManager.

Reasonable Adjustment

George Brown College supports individual differences in the learning environment and provides

‘reasonable adjustment’ in training and assessment activities to support every learner. If you have

any special needs that make it difficult for you to complete your learning or assessments, you

should discuss this with your assessor beforehand and will be provided with reasonable

alternatives to assist you to complete the required tasks such as completing tests verbally or using

an interpreter.

What happens if you do not agree with the assessment result?

If you do not think the assessment process is valid, or disagree with the decision once it is made,

or believe that you have been treated unfairly, you can appeal. The first step is to discuss the

matter with your trainer.

If you still do not agree with the results, refer to the GBC Complaints and Appeals Policy and speak

to the Student Services Team.

Support

While we may not be in a position to assist you with language training or specific LLN training, our

assessors will work with you to ensure that you are supported throughout your qualification. If you

require individual tutoring this may attract an additional fee (see Student Handbook). Support may

be offered by your assessor, or for more specialist support you may need to contact GBC

administration.

A Note on Plagiarism and Referencing

Plagiarism is a form of theft where the work, ideas, inventions etc. of other people are presented as

your own. Information, ideas etc. quoted or paraphrased from another source such as the Internet,

must be acknowledged with “quotation marks” around the relevant words/sentences or ideas and

the source listed in brackets. You must also list the sources at the end of your assessment.

Sources of information, ideas etc. must be provided in alphabetical order by author’s surname

(including author’s full name, name of document/ book / internet etc. and year and place of

publishing) or may be included in brackets in the text.

As a general rule it is advisable to never copy another person’s work. Should it appear that a

student’s work has been copied or does not appear to be authentic, you will be asked to speak to

your Course Coordinator and required to re-submit it. A fee may be charged according to George

Brown College policy.

Contacting the RTO

If you should need further support or assistance please do not hesitate to contact The Student

Services Team.

Student Assessment Guide v 1 January 2019 Page 4 of 55

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

BSBFIM601 Manage finances

ASSESSMENT

BSBFIM601 Manage finances

There are two assessments for this unit:

1. Research Questions

For this assessment, you are to read the questions and respond in writing with the most suitable

answer. There are six questions, all of which must be completed. Most questions require short

answers although some questions require a more detailed response. You may use various sources

of information including workbooks, internet and other documents, but must list and reference their

sources. Suggested resources and websites are provided.

Your assessor will advise you when this is due.

2. Case Study

For this assessment you are to undertake budgeting, financial forecasting and reporting and to

allocate and manage resources to achieve the required outputs for a simulated business.

The case study is in two stages each with 2 parts. You must complete them all.

Stage One: – based on the given financial information about the simulated business, you are

to prepare a number of budgets and then using appropriate formulae, to analyse financial data

to assess and manage risk and identify discrepancies.

Stage One – requires you to analyse discrepancies and produce a report in which you account

for variations. You are then required to participate in a role play, with the assessor, acting in the

role of company CEO, in which you discuss the variances and make financial

recommendations in relation to the company’s financial situation.

Your assessor will advise when each part is due.

You will need access and are expected to use suitable financial management software

Assessment Schedule

Assessment Due Date

1. Research Questions

2. Case Study:

Stage One

Stage Two

Student Assessment Guide v 1 January 2019 Page 5 of 55

ASSESSMENT

BSBFIM601 Manage finances

There are two assessments for this unit:

1. Research Questions

For this assessment, you are to read the questions and respond in writing with the most suitable

answer. There are six questions, all of which must be completed. Most questions require short

answers although some questions require a more detailed response. You may use various sources

of information including workbooks, internet and other documents, but must list and reference their

sources. Suggested resources and websites are provided.

Your assessor will advise you when this is due.

2. Case Study

For this assessment you are to undertake budgeting, financial forecasting and reporting and to

allocate and manage resources to achieve the required outputs for a simulated business.

The case study is in two stages each with 2 parts. You must complete them all.

Stage One: – based on the given financial information about the simulated business, you are

to prepare a number of budgets and then using appropriate formulae, to analyse financial data

to assess and manage risk and identify discrepancies.

Stage One – requires you to analyse discrepancies and produce a report in which you account

for variations. You are then required to participate in a role play, with the assessor, acting in the

role of company CEO, in which you discuss the variances and make financial

recommendations in relation to the company’s financial situation.

Your assessor will advise when each part is due.

You will need access and are expected to use suitable financial management software

Assessment Schedule

Assessment Due Date

1. Research Questions

2. Case Study:

Stage One

Stage Two

Student Assessment Guide v 1 January 2019 Page 5 of 55

BSBFIM601 Manage finances

ASSESSMENT COVER SHEET

Student Name:

Student ID:

Contact Number:

Email:

Trainer / Assessor Name:

Qualification: BSB60915 Advanced Diploma of Management (Human

Resources

Unit of Competency: BSBFIM601 Manage finances

Assessment:

☐ Research Questions

☐ Case Study:

Stage One

Stage Two

Due Date: Date Submitted:

If your assessment is being submitted after the due date, please attach a copy of the written

confirmation of extension received from your assessor.

Declaration: I have read and understood the following information at the

beginning of this assessment guide (please tick):

☐ Assessment information

☐ Submitting assessments

☐ Plagiarism and referencing

I declare this assessment is my own work and where the work is

of others, I have fully referenced that material.

Name (please print) Signature Date

Student Assessment Guide v 1 January 2019 Page 6 of 55

ASSESSMENT COVER SHEET

Student Name:

Student ID:

Contact Number:

Email:

Trainer / Assessor Name:

Qualification: BSB60915 Advanced Diploma of Management (Human

Resources

Unit of Competency: BSBFIM601 Manage finances

Assessment:

☐ Research Questions

☐ Case Study:

Stage One

Stage Two

Due Date: Date Submitted:

If your assessment is being submitted after the due date, please attach a copy of the written

confirmation of extension received from your assessor.

Declaration: I have read and understood the following information at the

beginning of this assessment guide (please tick):

☐ Assessment information

☐ Submitting assessments

☐ Plagiarism and referencing

I declare this assessment is my own work and where the work is

of others, I have fully referenced that material.

Name (please print) Signature Date

Student Assessment Guide v 1 January 2019 Page 6 of 55

BSBFIM601 Manage finances

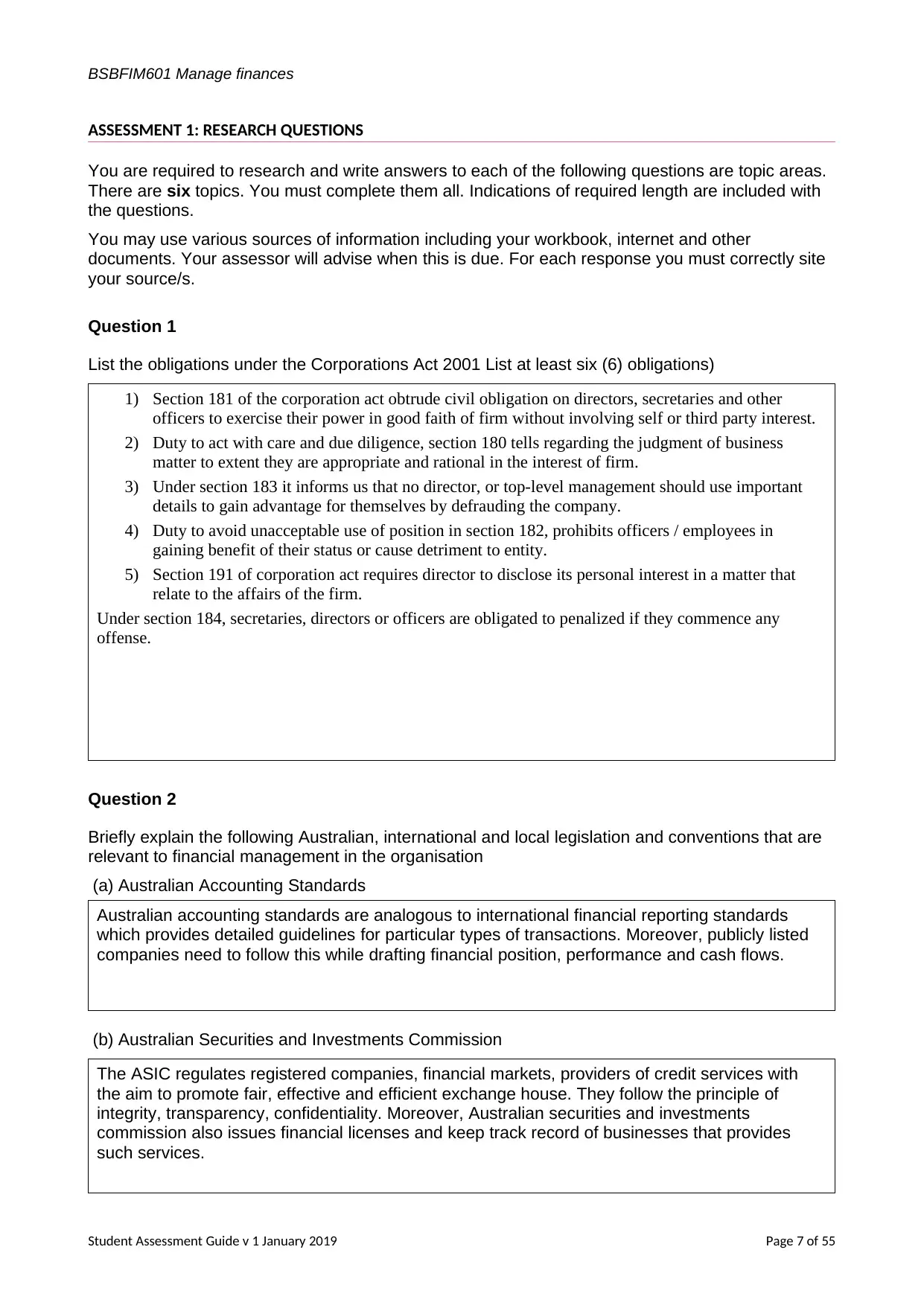

ASSESSMENT 1: RESEARCH QUESTIONS

You are required to research and write answers to each of the following questions are topic areas.

There are six topics. You must complete them all. Indications of required length are included with

the questions.

You may use various sources of information including your workbook, internet and other

documents. Your assessor will advise when this is due. For each response you must correctly site

your source/s.

Question 1

List the obligations under the Corporations Act 2001 List at least six (6) obligations)

1) Section 181 of the corporation act obtrude civil obligation on directors, secretaries and other

officers to exercise their power in good faith of firm without involving self or third party interest.

2) Duty to act with care and due diligence, section 180 tells regarding the judgment of business

matter to extent they are appropriate and rational in the interest of firm.

3) Under section 183 it informs us that no director, or top-level management should use important

details to gain advantage for themselves by defrauding the company.

4) Duty to avoid unacceptable use of position in section 182, prohibits officers / employees in

gaining benefit of their status or cause detriment to entity.

5) Section 191 of corporation act requires director to disclose its personal interest in a matter that

relate to the affairs of the firm.

Under section 184, secretaries, directors or officers are obligated to penalized if they commence any

offense.

Question 2

Briefly explain the following Australian, international and local legislation and conventions that are

relevant to financial management in the organisation

(a) Australian Accounting Standards

Australian accounting standards are analogous to international financial reporting standards

which provides detailed guidelines for particular types of transactions. Moreover, publicly listed

companies need to follow this while drafting financial position, performance and cash flows.

(b) Australian Securities and Investments Commission

The ASIC regulates registered companies, financial markets, providers of credit services with

the aim to promote fair, effective and efficient exchange house. They follow the principle of

integrity, transparency, confidentiality. Moreover, Australian securities and investments

commission also issues financial licenses and keep track record of businesses that provides

such services.

Student Assessment Guide v 1 January 2019 Page 7 of 55

ASSESSMENT 1: RESEARCH QUESTIONS

You are required to research and write answers to each of the following questions are topic areas.

There are six topics. You must complete them all. Indications of required length are included with

the questions.

You may use various sources of information including your workbook, internet and other

documents. Your assessor will advise when this is due. For each response you must correctly site

your source/s.

Question 1

List the obligations under the Corporations Act 2001 List at least six (6) obligations)

1) Section 181 of the corporation act obtrude civil obligation on directors, secretaries and other

officers to exercise their power in good faith of firm without involving self or third party interest.

2) Duty to act with care and due diligence, section 180 tells regarding the judgment of business

matter to extent they are appropriate and rational in the interest of firm.

3) Under section 183 it informs us that no director, or top-level management should use important

details to gain advantage for themselves by defrauding the company.

4) Duty to avoid unacceptable use of position in section 182, prohibits officers / employees in

gaining benefit of their status or cause detriment to entity.

5) Section 191 of corporation act requires director to disclose its personal interest in a matter that

relate to the affairs of the firm.

Under section 184, secretaries, directors or officers are obligated to penalized if they commence any

offense.

Question 2

Briefly explain the following Australian, international and local legislation and conventions that are

relevant to financial management in the organisation

(a) Australian Accounting Standards

Australian accounting standards are analogous to international financial reporting standards

which provides detailed guidelines for particular types of transactions. Moreover, publicly listed

companies need to follow this while drafting financial position, performance and cash flows.

(b) Australian Securities and Investments Commission

The ASIC regulates registered companies, financial markets, providers of credit services with

the aim to promote fair, effective and efficient exchange house. They follow the principle of

integrity, transparency, confidentiality. Moreover, Australian securities and investments

commission also issues financial licenses and keep track record of businesses that provides

such services.

Student Assessment Guide v 1 January 2019 Page 7 of 55

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BSBFIM601 Manage finances

(c) Privacy Acts and Principles

Privacy act 1988, is a principal of Australian legislation. This includes the collection, protection, use,

store and disclosing personal information in federal public sector and private sector whenever required.

Principles of privacy act are:

1) Accountability: The resource person must be accountable to the person for any misuse of his

personal information which is shared with or transferred to other organization.

2) Identify the purpose: Member of commission should identify the reason of procuring

information from the person, what is its purpose, how it will be used, etc.

3) Obtain consent: Before acquiring any personal data from the individual the purpose must be

disclosed to them, and should take consent, Therefore, consent should not obtain by ambiguous

way or providing misleading details.

4) Be accurate: Information collected must be accurate and complete so that decisions can be made

by another organization easily.

(d) International regulations (a brief overview)

This regulation occurs at international level, exercised by foreign organisations. Moreover, aims at

preventing, reducing and controlling pollution of the marine environment from ships to a global level.

Hence, it is the body of legal rules, norms and standards that apply between sovereign states with other

legal entities.

Question 3

Research tax law compliance and outline statutory requirements related to each of the following:

Tax Requirements

(a) Goods and Services Tax It is the tax which is payable by the company or the

individual on the import of goods and services and must

be registered for GST if it exceeds the threshold limit.

(b) Payroll tax Payroll tax is a self-assessed, general purpose state and

territory tax assessed on wages paid or payable by an

employer to its employees,

(c) Income tax It is the tax which is being paid on the income earned by

the individual or the business. For individual, tax is

payable when income exceeds $18200

(d) Fringe benefit tax It is the tax employers pays on the benefits paid to an

employee in addition to their salary and wages.

(e) PAYG withholding payable When payment is made to employees, contractors or the

other businesses, there is a need to withhold an amount

from the payment and send it to the ATO which is called

PAYG withholding and it prevents workers from having a

large amount of tax to pay at year end.

Student Assessment Guide v 1 January 2019 Page 8 of 55

(c) Privacy Acts and Principles

Privacy act 1988, is a principal of Australian legislation. This includes the collection, protection, use,

store and disclosing personal information in federal public sector and private sector whenever required.

Principles of privacy act are:

1) Accountability: The resource person must be accountable to the person for any misuse of his

personal information which is shared with or transferred to other organization.

2) Identify the purpose: Member of commission should identify the reason of procuring

information from the person, what is its purpose, how it will be used, etc.

3) Obtain consent: Before acquiring any personal data from the individual the purpose must be

disclosed to them, and should take consent, Therefore, consent should not obtain by ambiguous

way or providing misleading details.

4) Be accurate: Information collected must be accurate and complete so that decisions can be made

by another organization easily.

(d) International regulations (a brief overview)

This regulation occurs at international level, exercised by foreign organisations. Moreover, aims at

preventing, reducing and controlling pollution of the marine environment from ships to a global level.

Hence, it is the body of legal rules, norms and standards that apply between sovereign states with other

legal entities.

Question 3

Research tax law compliance and outline statutory requirements related to each of the following:

Tax Requirements

(a) Goods and Services Tax It is the tax which is payable by the company or the

individual on the import of goods and services and must

be registered for GST if it exceeds the threshold limit.

(b) Payroll tax Payroll tax is a self-assessed, general purpose state and

territory tax assessed on wages paid or payable by an

employer to its employees,

(c) Income tax It is the tax which is being paid on the income earned by

the individual or the business. For individual, tax is

payable when income exceeds $18200

(d) Fringe benefit tax It is the tax employers pays on the benefits paid to an

employee in addition to their salary and wages.

(e) PAYG withholding payable When payment is made to employees, contractors or the

other businesses, there is a need to withhold an amount

from the payment and send it to the ATO which is called

PAYG withholding and it prevents workers from having a

large amount of tax to pay at year end.

Student Assessment Guide v 1 January 2019 Page 8 of 55

BSBFIM601 Manage finances

(f) Company tax It is the tax amount which the companies are required to

pay on the income earned by the business. The current

company tax rate is 30%.

Question 4

Describe the “principles of accounting” and financial systems.

1) Revenue recognition principle: The company follows accrual basis of accounting. Therefore,

revenue is recognised in the period when goods or services are provided and not when cash is

received.

2) Cost principle: It states that entities assets are recorded in the books of accounts at the price it is

acquired and not on the resell cost.

3) Matching principle: In this the expenses and revenues of companies need to be matched within

same accounting year to derived accurate profit of that period.

4) Objectivity principle: The accounting is done on the basis of assumptions and concepts so in this

case company always states verifiable data in its financial books. Further, they ignore subjective

details even if it seems to be important.

Question 5

Describe the requirements and implications of “financial probity”.

Requirements and implications of financial probity:

The company must comes with the tender that is true and fair by following the proper code of

conduct which will not harm the environment.

Tender participants must be treated equally by the procurement agencies. They ought to have

same information as all contenders are having.

Agencies must have to keep the competitors safely without the purpose embezzling them.

Procurement institutions must be accountable to all partakers involve in the business and should

provide some access towards their rights.

Tender participant and agency must move on parallel basis, they both need to disclose every

material details that is necessary for selection process and take decision.

Question 6

Recommend commercially available software that is suitable for financial management.

Student Assessment Guide v 1 January 2019 Page 9 of 55

(f) Company tax It is the tax amount which the companies are required to

pay on the income earned by the business. The current

company tax rate is 30%.

Question 4

Describe the “principles of accounting” and financial systems.

1) Revenue recognition principle: The company follows accrual basis of accounting. Therefore,

revenue is recognised in the period when goods or services are provided and not when cash is

received.

2) Cost principle: It states that entities assets are recorded in the books of accounts at the price it is

acquired and not on the resell cost.

3) Matching principle: In this the expenses and revenues of companies need to be matched within

same accounting year to derived accurate profit of that period.

4) Objectivity principle: The accounting is done on the basis of assumptions and concepts so in this

case company always states verifiable data in its financial books. Further, they ignore subjective

details even if it seems to be important.

Question 5

Describe the requirements and implications of “financial probity”.

Requirements and implications of financial probity:

The company must comes with the tender that is true and fair by following the proper code of

conduct which will not harm the environment.

Tender participants must be treated equally by the procurement agencies. They ought to have

same information as all contenders are having.

Agencies must have to keep the competitors safely without the purpose embezzling them.

Procurement institutions must be accountable to all partakers involve in the business and should

provide some access towards their rights.

Tender participant and agency must move on parallel basis, they both need to disclose every

material details that is necessary for selection process and take decision.

Question 6

Recommend commercially available software that is suitable for financial management.

Student Assessment Guide v 1 January 2019 Page 9 of 55

BSBFIM601 Manage finances

The best available software for financial management are mentioned below:

Quick books: This software aids the small and medium enterprises accountants with the bank

reconciliation, invoices, payroll, tracking record and advanced reporting. Moreover, it's a

powerful feature for the entities who deal in high volume of manufacturing or retail sector.

Zoho finance plus: Zoho software helps the employees working in back office operations like

accounts department, finance department, inventory handling department, etc. Therefore, this

application acts as a backbone for systematic arrangement of all crucial business related data.

Oracle financials cloud: It is an enterprise resource planning system accessed on the cloud.

Moreover, this is good for the organisation who looks towards controllability with scalability, they

are the comprehensive and integrated ecosystem of finance tools.

Student Assessment Guide v 1 January 2019 Page 10 of 55

The best available software for financial management are mentioned below:

Quick books: This software aids the small and medium enterprises accountants with the bank

reconciliation, invoices, payroll, tracking record and advanced reporting. Moreover, it's a

powerful feature for the entities who deal in high volume of manufacturing or retail sector.

Zoho finance plus: Zoho software helps the employees working in back office operations like

accounts department, finance department, inventory handling department, etc. Therefore, this

application acts as a backbone for systematic arrangement of all crucial business related data.

Oracle financials cloud: It is an enterprise resource planning system accessed on the cloud.

Moreover, this is good for the organisation who looks towards controllability with scalability, they

are the comprehensive and integrated ecosystem of finance tools.

Student Assessment Guide v 1 January 2019 Page 10 of 55

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

BSBFIM601 Manage finances

Suggested Resources:

Manage finance – BSBFIM601, 2015, 1st Edition, Version 1, Innovation and Business Industry Skills

Council Ltd Australia, East Melbourne, VIC, Australia

Australian Taxation Office viewed November 2017

https://www.ato.gov.au/

Policy and legislation, Australian Government, Department of finance, viewed

November2017

https://finance.gov.au/policy-legislation.html

Federal register of legislation, Corporations Act 2001- C2017C00328, In force-

latest version,

Australian Government, viewed November 2017

https://www.legislation.gov.au/Details/C2017C00328

Budget 2017-18 Viewed November 2017

http://www.budget.gov.au/

Budget, budgeting and variance analysis, Building the business case analysis,

viewed November 2017

https://www.business-case-analysis.com/budget.html

Student Assessment Guide v 1 January 2019 Page 11 of 55

Suggested Resources:

Manage finance – BSBFIM601, 2015, 1st Edition, Version 1, Innovation and Business Industry Skills

Council Ltd Australia, East Melbourne, VIC, Australia

Australian Taxation Office viewed November 2017

https://www.ato.gov.au/

Policy and legislation, Australian Government, Department of finance, viewed

November2017

https://finance.gov.au/policy-legislation.html

Federal register of legislation, Corporations Act 2001- C2017C00328, In force-

latest version,

Australian Government, viewed November 2017

https://www.legislation.gov.au/Details/C2017C00328

Budget 2017-18 Viewed November 2017

http://www.budget.gov.au/

Budget, budgeting and variance analysis, Building the business case analysis,

viewed November 2017

https://www.business-case-analysis.com/budget.html

Student Assessment Guide v 1 January 2019 Page 11 of 55

BSBFIM601 Manage finances

ASSESSMENT 2: CASE STUDY – STAGE ONE

Overview

For this assessment you are to demonstrate that you have the skills and knowledge to:

Plan for financial management

establish budgets and allocate funds

This assessment is the first of two stages in this case study, each of which has several parts. You

must complete them all.

For this stage you are to read the business scenario and complete the tasks or answer the

questions.

There are two parts to this assessment. You must complete them both.

Tasks:

Part A

Read and analyse the case study information that follows and complete the tasks or answer the

questions.

Make sure you analyse the business plan summary, and the previous year’s financial data.

Now complete the following.

1. Develop a:

(a) Sales Budget,

(b) Profit Budget,

(c) Cash Flow Budget

(d) Debtor Ageing Summary

Instructions:

You must use electronic spreadsheets, for example MS Excel, and each budget must be in

a separate worksheet

Each budget must be divided into quarterly periods

Make sure that you use the previous year’s financial data to determine allocations for

resources.

Ensure each budget you prepare complies with the organisational and policies and

procedures as provided.

Student Assessment Guide v 1 January 2019 Page 12 of 55

ASSESSMENT 2: CASE STUDY – STAGE ONE

Overview

For this assessment you are to demonstrate that you have the skills and knowledge to:

Plan for financial management

establish budgets and allocate funds

This assessment is the first of two stages in this case study, each of which has several parts. You

must complete them all.

For this stage you are to read the business scenario and complete the tasks or answer the

questions.

There are two parts to this assessment. You must complete them both.

Tasks:

Part A

Read and analyse the case study information that follows and complete the tasks or answer the

questions.

Make sure you analyse the business plan summary, and the previous year’s financial data.

Now complete the following.

1. Develop a:

(a) Sales Budget,

(b) Profit Budget,

(c) Cash Flow Budget

(d) Debtor Ageing Summary

Instructions:

You must use electronic spreadsheets, for example MS Excel, and each budget must be in

a separate worksheet

Each budget must be divided into quarterly periods

Make sure that you use the previous year’s financial data to determine allocations for

resources.

Ensure each budget you prepare complies with the organisational and policies and

procedures as provided.

Student Assessment Guide v 1 January 2019 Page 12 of 55

BSBFIM601 Manage finances

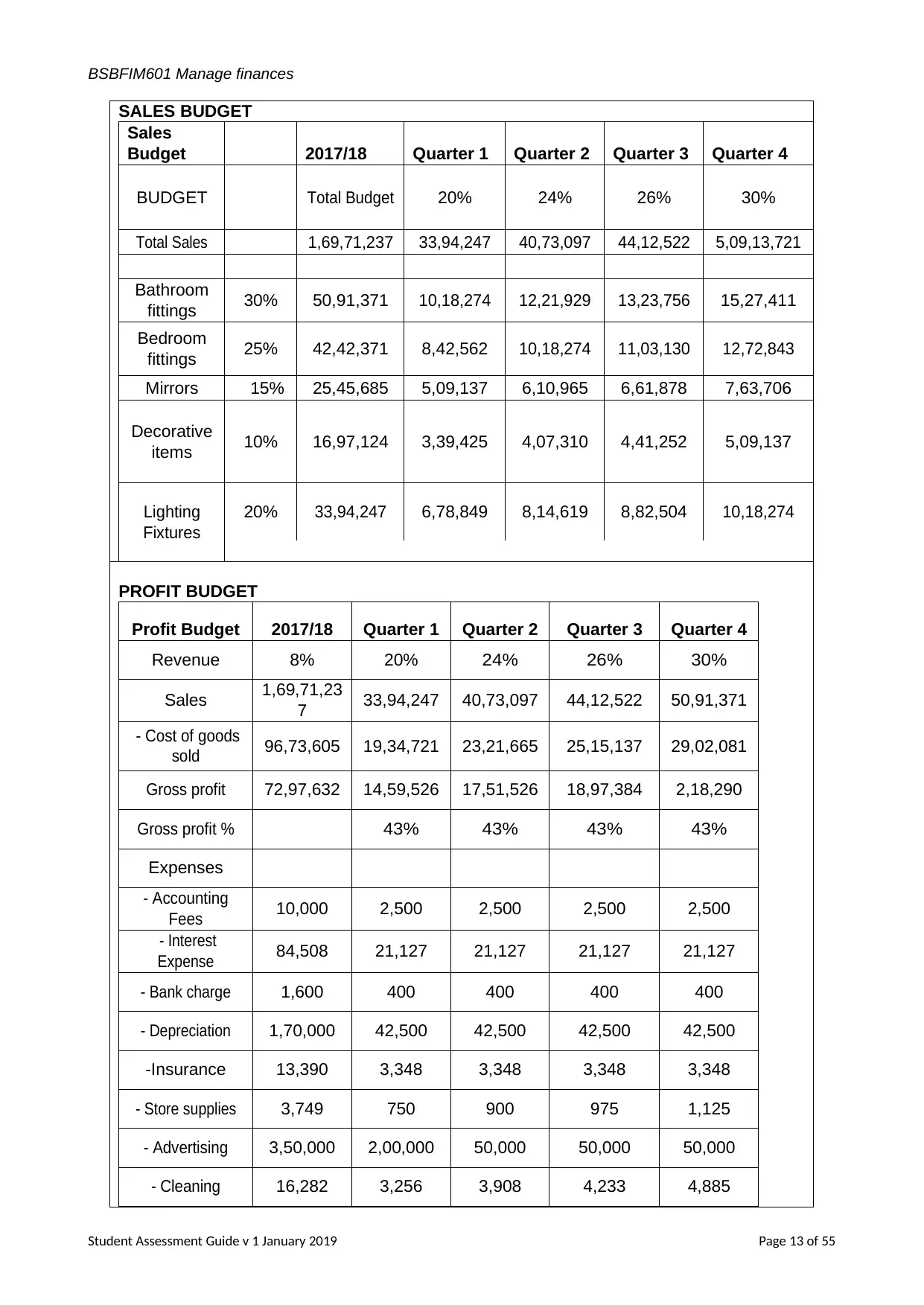

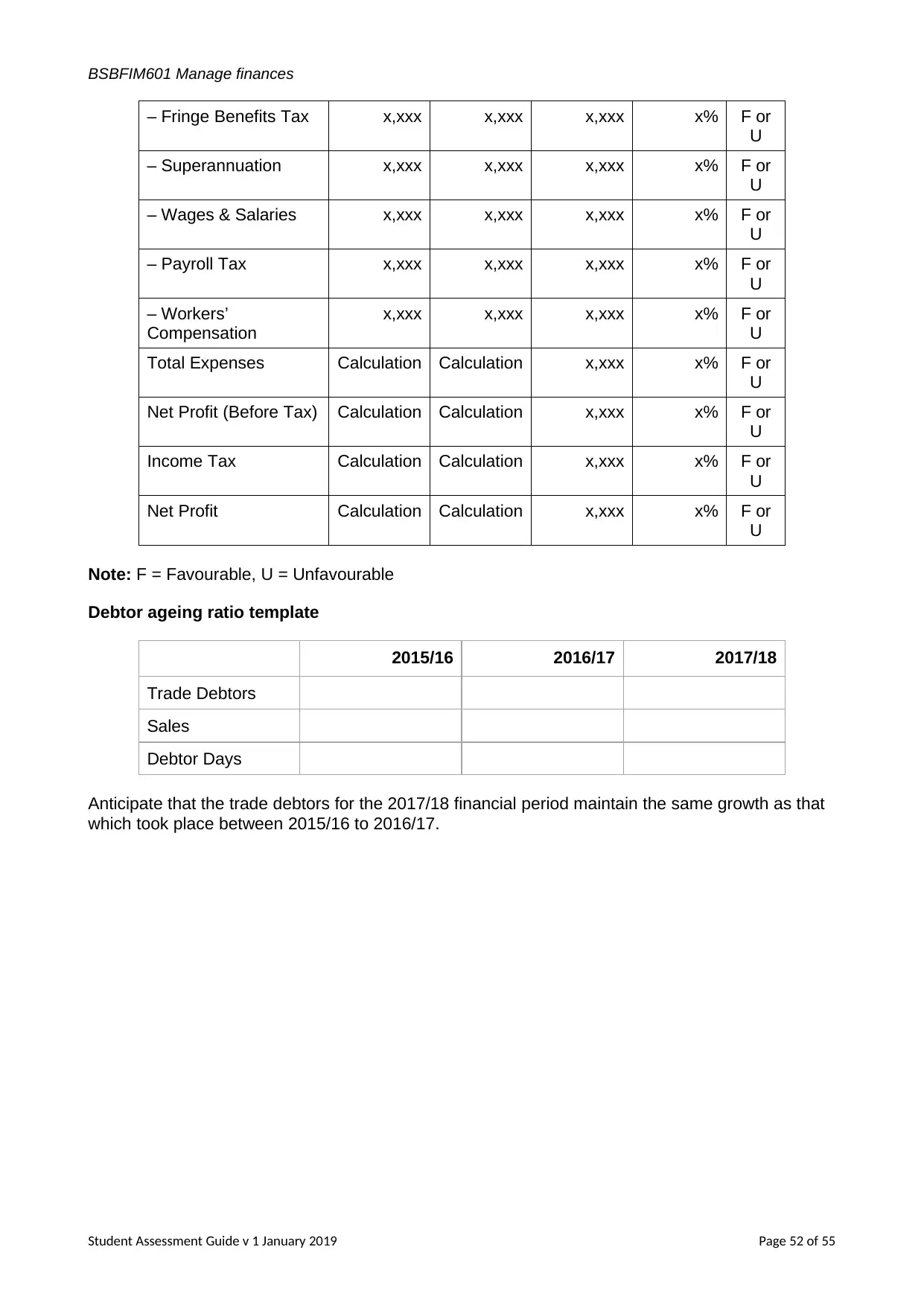

SALES BUDGET

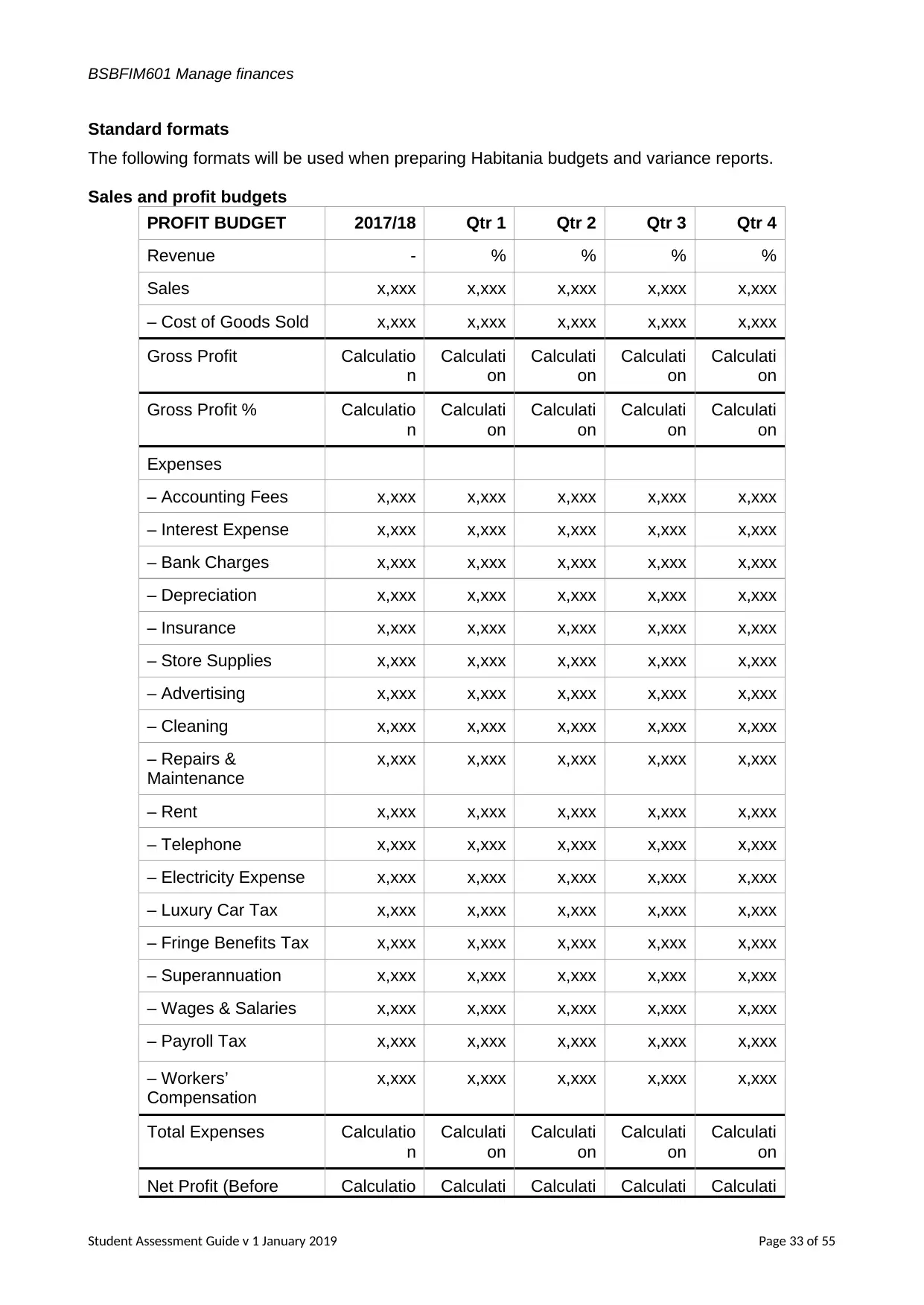

Sales

Budget 2017/18 Quarter 1 Quarter 2 Quarter 3 Quarter 4

BUDGET Total Budget 20% 24% 26% 30%

Total Sales 1,69,71,237 33,94,247 40,73,097 44,12,522 5,09,13,721

Bathroom

fittings 30% 50,91,371 10,18,274 12,21,929 13,23,756 15,27,411

Bedroom

fittings 25% 42,42,371 8,42,562 10,18,274 11,03,130 12,72,843

Mirrors 15% 25,45,685 5,09,137 6,10,965 6,61,878 7,63,706

Decorative

items 10% 16,97,124 3,39,425 4,07,310 4,41,252 5,09,137

Lighting

Fixtures

20% 33,94,247 6,78,849 8,14,619 8,82,504 10,18,274

PROFIT BUDGET

Profit Budget 2017/18 Quarter 1 Quarter 2 Quarter 3 Quarter 4

Revenue 8% 20% 24% 26% 30%

Sales 1,69,71,23

7 33,94,247 40,73,097 44,12,522 50,91,371

- Cost of goods

sold 96,73,605 19,34,721 23,21,665 25,15,137 29,02,081

Gross profit 72,97,632 14,59,526 17,51,526 18,97,384 2,18,290

Gross profit % 43% 43% 43% 43%

Expenses

- Accounting

Fees 10,000 2,500 2,500 2,500 2,500

- Interest

Expense 84,508 21,127 21,127 21,127 21,127

- Bank charge 1,600 400 400 400 400

- Depreciation 1,70,000 42,500 42,500 42,500 42,500

-Insurance 13,390 3,348 3,348 3,348 3,348

- Store supplies 3,749 750 900 975 1,125

- Advertising 3,50,000 2,00,000 50,000 50,000 50,000

- Cleaning 16,282 3,256 3,908 4,233 4,885

Student Assessment Guide v 1 January 2019 Page 13 of 55

SALES BUDGET

Sales

Budget 2017/18 Quarter 1 Quarter 2 Quarter 3 Quarter 4

BUDGET Total Budget 20% 24% 26% 30%

Total Sales 1,69,71,237 33,94,247 40,73,097 44,12,522 5,09,13,721

Bathroom

fittings 30% 50,91,371 10,18,274 12,21,929 13,23,756 15,27,411

Bedroom

fittings 25% 42,42,371 8,42,562 10,18,274 11,03,130 12,72,843

Mirrors 15% 25,45,685 5,09,137 6,10,965 6,61,878 7,63,706

Decorative

items 10% 16,97,124 3,39,425 4,07,310 4,41,252 5,09,137

Lighting

Fixtures

20% 33,94,247 6,78,849 8,14,619 8,82,504 10,18,274

PROFIT BUDGET

Profit Budget 2017/18 Quarter 1 Quarter 2 Quarter 3 Quarter 4

Revenue 8% 20% 24% 26% 30%

Sales 1,69,71,23

7 33,94,247 40,73,097 44,12,522 50,91,371

- Cost of goods

sold 96,73,605 19,34,721 23,21,665 25,15,137 29,02,081

Gross profit 72,97,632 14,59,526 17,51,526 18,97,384 2,18,290

Gross profit % 43% 43% 43% 43%

Expenses

- Accounting

Fees 10,000 2,500 2,500 2,500 2,500

- Interest

Expense 84,508 21,127 21,127 21,127 21,127

- Bank charge 1,600 400 400 400 400

- Depreciation 1,70,000 42,500 42,500 42,500 42,500

-Insurance 13,390 3,348 3,348 3,348 3,348

- Store supplies 3,749 750 900 975 1,125

- Advertising 3,50,000 2,00,000 50,000 50,000 50,000

- Cleaning 16,282 3,256 3,908 4,233 4,885

Student Assessment Guide v 1 January 2019 Page 13 of 55

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BSBFIM601 Manage finances

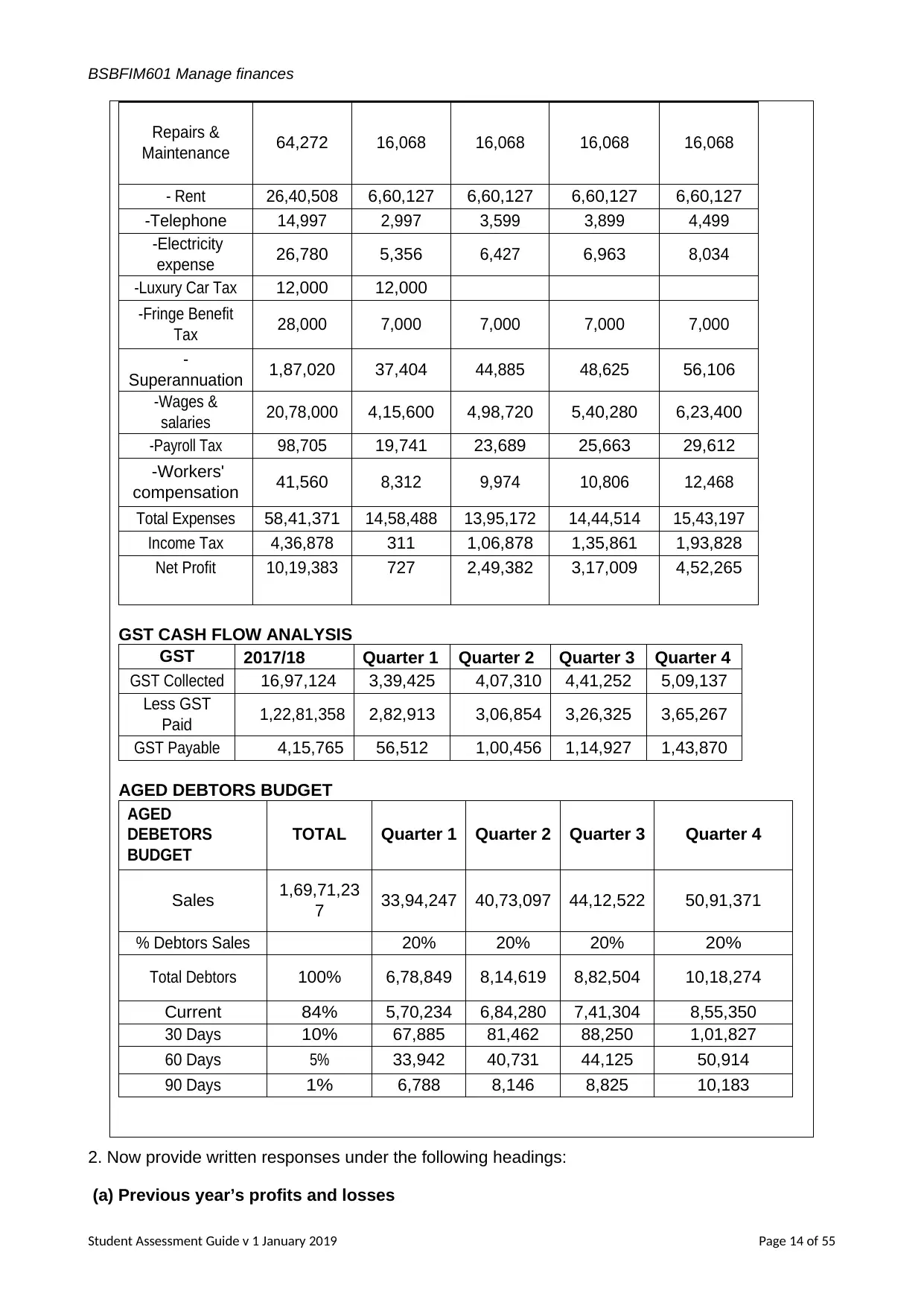

Repairs &

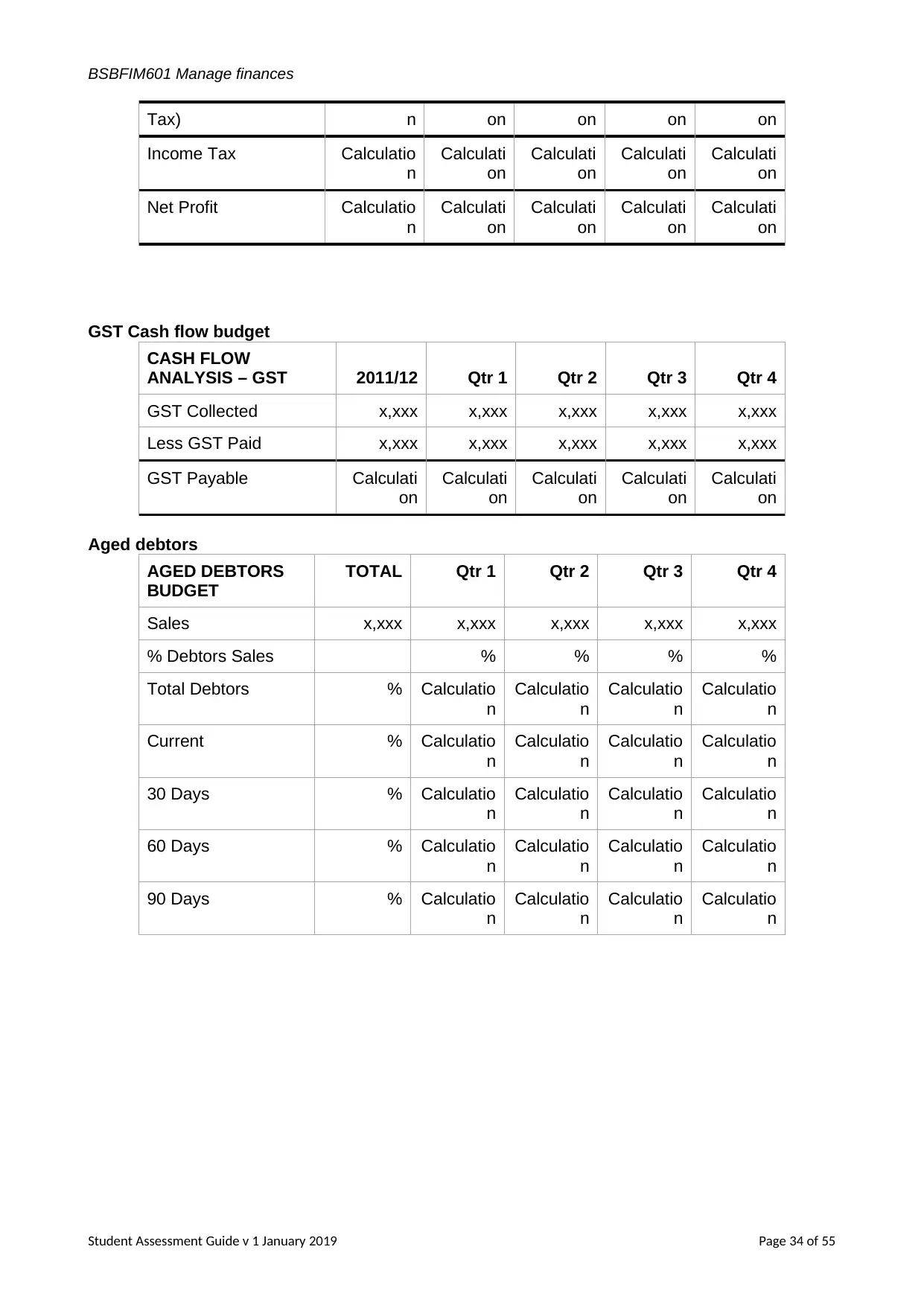

Maintenance 64,272 16,068 16,068 16,068 16,068

- Rent 26,40,508 6,60,127 6,60,127 6,60,127 6,60,127

-Telephone 14,997 2,997 3,599 3,899 4,499

-Electricity

expense 26,780 5,356 6,427 6,963 8,034

-Luxury Car Tax 12,000 12,000

-Fringe Benefit

Tax 28,000 7,000 7,000 7,000 7,000

-

Superannuation 1,87,020 37,404 44,885 48,625 56,106

-Wages &

salaries 20,78,000 4,15,600 4,98,720 5,40,280 6,23,400

-Payroll Tax 98,705 19,741 23,689 25,663 29,612

-Workers'

compensation 41,560 8,312 9,974 10,806 12,468

Total Expenses 58,41,371 14,58,488 13,95,172 14,44,514 15,43,197

Income Tax 4,36,878 311 1,06,878 1,35,861 1,93,828

Net Profit 10,19,383 727 2,49,382 3,17,009 4,52,265

GST CASH FLOW ANALYSIS

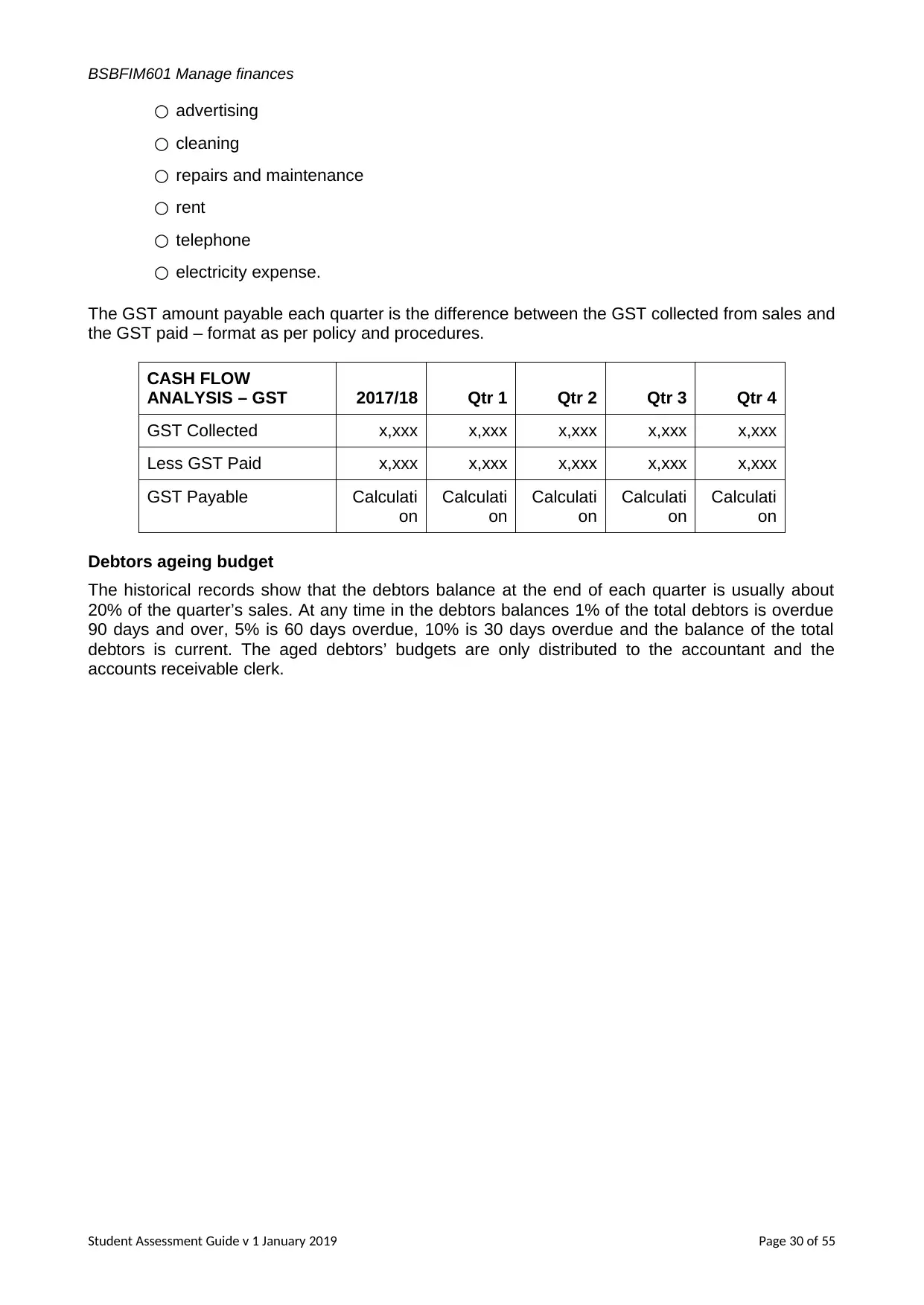

GST 2017/18 Quarter 1 Quarter 2 Quarter 3 Quarter 4

GST Collected 16,97,124 3,39,425 4,07,310 4,41,252 5,09,137

Less GST

Paid 1,22,81,358 2,82,913 3,06,854 3,26,325 3,65,267

GST Payable 4,15,765 56,512 1,00,456 1,14,927 1,43,870

AGED DEBTORS BUDGET

AGED

DEBETORS

BUDGET

TOTAL Quarter 1 Quarter 2 Quarter 3 Quarter 4

Sales 1,69,71,23

7 33,94,247 40,73,097 44,12,522 50,91,371

% Debtors Sales 20% 20% 20% 20%

Total Debtors 100% 6,78,849 8,14,619 8,82,504 10,18,274

Current 84% 5,70,234 6,84,280 7,41,304 8,55,350

30 Days 10% 67,885 81,462 88,250 1,01,827

60 Days 5% 33,942 40,731 44,125 50,914

90 Days 1% 6,788 8,146 8,825 10,183

2. Now provide written responses under the following headings:

(a) Previous year’s profits and losses

Student Assessment Guide v 1 January 2019 Page 14 of 55

Repairs &

Maintenance 64,272 16,068 16,068 16,068 16,068

- Rent 26,40,508 6,60,127 6,60,127 6,60,127 6,60,127

-Telephone 14,997 2,997 3,599 3,899 4,499

-Electricity

expense 26,780 5,356 6,427 6,963 8,034

-Luxury Car Tax 12,000 12,000

-Fringe Benefit

Tax 28,000 7,000 7,000 7,000 7,000

-

Superannuation 1,87,020 37,404 44,885 48,625 56,106

-Wages &

salaries 20,78,000 4,15,600 4,98,720 5,40,280 6,23,400

-Payroll Tax 98,705 19,741 23,689 25,663 29,612

-Workers'

compensation 41,560 8,312 9,974 10,806 12,468

Total Expenses 58,41,371 14,58,488 13,95,172 14,44,514 15,43,197

Income Tax 4,36,878 311 1,06,878 1,35,861 1,93,828

Net Profit 10,19,383 727 2,49,382 3,17,009 4,52,265

GST CASH FLOW ANALYSIS

GST 2017/18 Quarter 1 Quarter 2 Quarter 3 Quarter 4

GST Collected 16,97,124 3,39,425 4,07,310 4,41,252 5,09,137

Less GST

Paid 1,22,81,358 2,82,913 3,06,854 3,26,325 3,65,267

GST Payable 4,15,765 56,512 1,00,456 1,14,927 1,43,870

AGED DEBTORS BUDGET

AGED

DEBETORS

BUDGET

TOTAL Quarter 1 Quarter 2 Quarter 3 Quarter 4

Sales 1,69,71,23

7 33,94,247 40,73,097 44,12,522 50,91,371

% Debtors Sales 20% 20% 20% 20%

Total Debtors 100% 6,78,849 8,14,619 8,82,504 10,18,274

Current 84% 5,70,234 6,84,280 7,41,304 8,55,350

30 Days 10% 67,885 81,462 88,250 1,01,827

60 Days 5% 33,942 40,731 44,125 50,914

90 Days 1% 6,788 8,146 8,825 10,183

2. Now provide written responses under the following headings:

(a) Previous year’s profits and losses

Student Assessment Guide v 1 January 2019 Page 14 of 55

BSBFIM601 Manage finances

Identify the reasons for the previous year’s profits and losses.

The previous years incurred profits and the reason behind the rise in profit is because of the rise

in the customer base and also the business is built upon the high quality after sales service. The

store supplies, cleanings, payroll tax, electricity expenses and the other expenses have relatively

resulted into decline in profits while other expenses have remained the same.

(b) Financial management approaches

Comment on the effectiveness of existing financial management approaches

The stated expenses have risen due to the inflation and thus, the profits had been derived from

the prior years are the results of the outcome of the right and accurate control. Thus, there were

no losses and for the future years, it is important to have more strict control over the business

expenses. Along with this, it is crucial to be able to effectively handling the money and

understanding how and where to spend.

(c) Budget assumptions

What assumptions did you make in creating the budgets?

In developing budgets, inflation is taken to be 4% each year and all the costs have seen this

increase and along with that, the extra business-related expenses and taxes such as the

bathroom and bedroom fittings and the mirrors and the decorative items in addition to the

lighting fixtures. The main aspect for meeting higher profits is the high quality after sales service

which assists in establishing a strong customer base which assisted in generating loyalty sales.

It has been assumed that the sales will grow at the same rate 2017-18 as 2016-17 and the rate

of inflation will be 4% annually with the gross profit expected to reduce by 1%. Apart from this,

there is increase in the budget for advertising by $70,000 over the 2016-17 outcome. $200,000

was planned for the 1st quarter with the balance to be apportioned equally in the other quarters.

There is rise in wages and salaries by $172,500 over the 2016-17 amounts and the accounting

fees is the fixed amount of $10,000.

(d) Implementation and monitoring of budget

What relevant thoughts do you have regarding the implementation and monitoring of budget

expenditure?

Student Assessment Guide v 1 January 2019 Page 15 of 55

Identify the reasons for the previous year’s profits and losses.

The previous years incurred profits and the reason behind the rise in profit is because of the rise

in the customer base and also the business is built upon the high quality after sales service. The

store supplies, cleanings, payroll tax, electricity expenses and the other expenses have relatively

resulted into decline in profits while other expenses have remained the same.

(b) Financial management approaches

Comment on the effectiveness of existing financial management approaches

The stated expenses have risen due to the inflation and thus, the profits had been derived from

the prior years are the results of the outcome of the right and accurate control. Thus, there were

no losses and for the future years, it is important to have more strict control over the business

expenses. Along with this, it is crucial to be able to effectively handling the money and

understanding how and where to spend.

(c) Budget assumptions

What assumptions did you make in creating the budgets?

In developing budgets, inflation is taken to be 4% each year and all the costs have seen this

increase and along with that, the extra business-related expenses and taxes such as the

bathroom and bedroom fittings and the mirrors and the decorative items in addition to the

lighting fixtures. The main aspect for meeting higher profits is the high quality after sales service

which assists in establishing a strong customer base which assisted in generating loyalty sales.

It has been assumed that the sales will grow at the same rate 2017-18 as 2016-17 and the rate

of inflation will be 4% annually with the gross profit expected to reduce by 1%. Apart from this,

there is increase in the budget for advertising by $70,000 over the 2016-17 outcome. $200,000

was planned for the 1st quarter with the balance to be apportioned equally in the other quarters.

There is rise in wages and salaries by $172,500 over the 2016-17 amounts and the accounting

fees is the fixed amount of $10,000.

(d) Implementation and monitoring of budget

What relevant thoughts do you have regarding the implementation and monitoring of budget

expenditure?

Student Assessment Guide v 1 January 2019 Page 15 of 55

BSBFIM601 Manage finances

Determining the ways in which the assumptions can be implemented effectively which will help

in ensuring that budgets are prepared as per the business requirements. Along with this,

determining the time period in which monitoring of the budget should be carried out.

Budget Evaluation/Audit-

Major Activities:

Physical assessment to determine value for money,

Prevent or reduce the impact of frauds and losses

Determine compliance or violations of financial rules and procedures.

Part B

Based on the information provided in the case study answer the following questions in the space

provided below: You must read and analyse the information in the case study on page 12

1. Identify the current statutory requirements for tax compliance and list and calculate the

tax liabilities for Habitania Pty Ltd under taxation legislation.

Income Tax: This is the amount which every business organization and individuals are

required to pay on its income of the year.

GST: It is paid by the business which provides goods and services.

Superannuation: This tax is paid by the organization on the behalf of the employee and itis

calculated by the organization's payroll system.

Company tax: It is the tax which is being paid by the company on the assessable income and

the tax rate is 30% of the income.

Following are the calculated tax of the organization:

Income tax: 436,878

Payroll tax: 98,705

Superannuation: 187,020

Fringe Benefits Tax: 28,000

Luxury Car Tax: 12,000

2. Identify the current compliance requirements and liabilities for this organisation under

the Corporations Act 20XX.

Student Assessment Guide v 1 January 2019 Page 16 of 55

Determining the ways in which the assumptions can be implemented effectively which will help

in ensuring that budgets are prepared as per the business requirements. Along with this,

determining the time period in which monitoring of the budget should be carried out.

Budget Evaluation/Audit-

Major Activities:

Physical assessment to determine value for money,

Prevent or reduce the impact of frauds and losses

Determine compliance or violations of financial rules and procedures.

Part B

Based on the information provided in the case study answer the following questions in the space

provided below: You must read and analyse the information in the case study on page 12

1. Identify the current statutory requirements for tax compliance and list and calculate the

tax liabilities for Habitania Pty Ltd under taxation legislation.

Income Tax: This is the amount which every business organization and individuals are

required to pay on its income of the year.

GST: It is paid by the business which provides goods and services.

Superannuation: This tax is paid by the organization on the behalf of the employee and itis

calculated by the organization's payroll system.

Company tax: It is the tax which is being paid by the company on the assessable income and

the tax rate is 30% of the income.

Following are the calculated tax of the organization:

Income tax: 436,878

Payroll tax: 98,705

Superannuation: 187,020

Fringe Benefits Tax: 28,000

Luxury Car Tax: 12,000

2. Identify the current compliance requirements and liabilities for this organisation under

the Corporations Act 20XX.

Student Assessment Guide v 1 January 2019 Page 16 of 55

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

BSBFIM601 Manage finances

Following are the certain essential requirements which are needed to be complied by

this organization under the Corporation Act.

An annual return along with all the information pertaining to the company and its

activities must to submitted to the Australian Securities and Investment Commission.

Keeping the complete information and records in order to explain reports and the

records for at least 7 years.

The organization is required to abide by the rules and guidelines set out by ASIC for

the purpose of internal management of the company.

The directors of the company are required to act within the set limits. In addition to

this, the directors must keep the records of minutes and resolution in writing.

The organization should notify ASIC of the registered office along with the principle

place of business.

It mandatory to make use of the company name and CAN on all the public

documents, business premises, cheques and the ASIC lodged documents.

The organization is required to submit its financial statements and is required to

have their financial statements audited.

3. Review commercially available financial management software to select the most suitable

software for Habitania Pty Ltd.

Ensure you diagnose software options by comparing two commercially available software titles

against the capabilities of the existing technology for the organisation and against the prioritised

requirements, and outline the reasons that lead you to this recommendation.

MYOB:

It is a single user bookkeeping system which is mainly suitable for micro-level businesses.

It has integrated modules and the software remains up to date with ATO and along

with this, it provides fast and easy tax updates.

XERO:

It can be stated as an online accounting software pertaining to the business concerns. It

assists in identifying the real time cash flows of the business. It also offers various

other features such as invoicing and quotes, bank reconciliation and managing the

inventory records.

EXCEL:

It is a entire accounting solution in respect to the small business concerns which helps in

offering benefits like non complex accounting terms, easy management of account

book. It is not essential to have bookkeeping knowledge and skills.

Recommendation for Habitania Pty Ltd

The company should adopt and purchase XERO financial accounting software as

supports real time access to the cash flow and it remain updated all the time. Thus,

the existing accounting software must be replaced and the add-on must be made in

respect to the accounting system of the organization.

4. Explain how you can apply the following principles of accounting in developing the

budgets required for this task:

(a) matching principle

(b) account groups

Student Assessment Guide v 1 January 2019 Page 17 of 55

Following are the certain essential requirements which are needed to be complied by

this organization under the Corporation Act.

An annual return along with all the information pertaining to the company and its

activities must to submitted to the Australian Securities and Investment Commission.

Keeping the complete information and records in order to explain reports and the

records for at least 7 years.

The organization is required to abide by the rules and guidelines set out by ASIC for

the purpose of internal management of the company.

The directors of the company are required to act within the set limits. In addition to

this, the directors must keep the records of minutes and resolution in writing.

The organization should notify ASIC of the registered office along with the principle

place of business.

It mandatory to make use of the company name and CAN on all the public

documents, business premises, cheques and the ASIC lodged documents.

The organization is required to submit its financial statements and is required to

have their financial statements audited.

3. Review commercially available financial management software to select the most suitable

software for Habitania Pty Ltd.

Ensure you diagnose software options by comparing two commercially available software titles

against the capabilities of the existing technology for the organisation and against the prioritised

requirements, and outline the reasons that lead you to this recommendation.

MYOB:

It is a single user bookkeeping system which is mainly suitable for micro-level businesses.

It has integrated modules and the software remains up to date with ATO and along

with this, it provides fast and easy tax updates.

XERO:

It can be stated as an online accounting software pertaining to the business concerns. It

assists in identifying the real time cash flows of the business. It also offers various

other features such as invoicing and quotes, bank reconciliation and managing the

inventory records.

EXCEL:

It is a entire accounting solution in respect to the small business concerns which helps in

offering benefits like non complex accounting terms, easy management of account

book. It is not essential to have bookkeeping knowledge and skills.

Recommendation for Habitania Pty Ltd

The company should adopt and purchase XERO financial accounting software as

supports real time access to the cash flow and it remain updated all the time. Thus,

the existing accounting software must be replaced and the add-on must be made in

respect to the accounting system of the organization.

4. Explain how you can apply the following principles of accounting in developing the

budgets required for this task:

(a) matching principle

(b) account groups

Student Assessment Guide v 1 January 2019 Page 17 of 55

BSBFIM601 Manage finances

(c) time periods.

(a) Matching Principle: It states that the expenses should be recognized in the same period

in which the revenues related to those expenses are recognized within the financial

statements. It is essential to acknowledge that the most of the company’s planning are

made through specialists who acquires a commission. If the association has $60000 of

offers in December, then the amount of commission would be $6000 @10%.

(b) Account groups: It accounts for the summary of the accounts which is based upon the

criteria of how master records are being created and also determines the number of

intervals from which the accounts is being created from the general ledger. In creation of

the financial records, the company makes use of the past information pertaining to the

various accounts. This will result into providing more accurate and appropriate

disclosure about the accounts leading to preparing relevant reports.

(c) Time periods: It will support the organization in differentiating and obtaining the results in

different time frames. This can be further utilized for the purpose of evaluation and

decision making.

5. Explain and discuss the implications of probity when preparing and revising budgets.

Strict adherence to the code of ethics based upon the undeviating honesty mainly in

respect to monetary matters and the beyond legal needs. Implications of probity while

preparing and revising budgets are- providing accountability, maintaining integrity,

complying with the processes, avoiding the chances of misconduct, fraud and

corruption.

6. List the critical dates and initiatives that will require or generate resources for Habitania

Pty Ltd in the next financial cycle.

Completion of debtor analysis to reduce cash tied up in outstanding debts.

Increase in the wages and salaries by $172,500.

Reduction of the principal loan by $100,000 on 31st December.

Gross profit rate reduction by 1%.

Increase in the advertising budget by $70,000.

7. List the additional items you would recommend for inclusion in the budgets for Habitania

Pty Ltd.

Student Assessment Guide v 1 January 2019 Page 18 of 55

(c) time periods.

(a) Matching Principle: It states that the expenses should be recognized in the same period

in which the revenues related to those expenses are recognized within the financial

statements. It is essential to acknowledge that the most of the company’s planning are

made through specialists who acquires a commission. If the association has $60000 of

offers in December, then the amount of commission would be $6000 @10%.

(b) Account groups: It accounts for the summary of the accounts which is based upon the

criteria of how master records are being created and also determines the number of

intervals from which the accounts is being created from the general ledger. In creation of

the financial records, the company makes use of the past information pertaining to the

various accounts. This will result into providing more accurate and appropriate

disclosure about the accounts leading to preparing relevant reports.

(c) Time periods: It will support the organization in differentiating and obtaining the results in

different time frames. This can be further utilized for the purpose of evaluation and

decision making.

5. Explain and discuss the implications of probity when preparing and revising budgets.

Strict adherence to the code of ethics based upon the undeviating honesty mainly in

respect to monetary matters and the beyond legal needs. Implications of probity while

preparing and revising budgets are- providing accountability, maintaining integrity,

complying with the processes, avoiding the chances of misconduct, fraud and

corruption.

6. List the critical dates and initiatives that will require or generate resources for Habitania

Pty Ltd in the next financial cycle.

Completion of debtor analysis to reduce cash tied up in outstanding debts.

Increase in the wages and salaries by $172,500.

Reduction of the principal loan by $100,000 on 31st December.

Gross profit rate reduction by 1%.

Increase in the advertising budget by $70,000.

7. List the additional items you would recommend for inclusion in the budgets for Habitania

Pty Ltd.

Student Assessment Guide v 1 January 2019 Page 18 of 55

BSBFIM601 Manage finances

Warehouse expenses and cleaning and maintaining expenses could be included. The

training fees should be recognized as an administrative expense for the company for

making its employees efficient and suitable for the job.

8. List the new or modified internal controls that could improve risk management for

Habitania Pty Ltd including the maintenance of audit trails.

Risk management would include internal control additions and modifications like:

Safeguard assets - well designed internal controls protects the assets from

accidental loss or loss from fraud.

Ensure the reliability and integrity of financial information – Internal controls ensure

that management has accurate, timely and complete information, including

accounting records, in order to plan, monitor and report business operations.

Accomplishment of goals and objectives - Internal controls system provide a

mechanism for management to monitor the achievement of operational goals and

objectives.

Audit trail includes:

Paperwork with all the required details must be filled and provided with which is used

as a evidence of any receipt or payment.

Secondary control of the receipt of cash like the cash register or a second person.

9. Case study situation:

The CEO of Habitania Pty Ltd, Tom Salinas explained that he prefers to discuss the budgets with

all senior managers prior to their distribution in order to ensure a corporate view of the strategic

plans. He then meets with each group separately to answer questions and concerns about their

particular area. Eventually the budgets will be printed in hard copy and bound as well distributed as

an electronic spreadsheet.

Student Assessment Guide v 1 January 2019 Page 19 of 55

Warehouse expenses and cleaning and maintaining expenses could be included. The

training fees should be recognized as an administrative expense for the company for

making its employees efficient and suitable for the job.

8. List the new or modified internal controls that could improve risk management for

Habitania Pty Ltd including the maintenance of audit trails.

Risk management would include internal control additions and modifications like:

Safeguard assets - well designed internal controls protects the assets from

accidental loss or loss from fraud.

Ensure the reliability and integrity of financial information – Internal controls ensure

that management has accurate, timely and complete information, including

accounting records, in order to plan, monitor and report business operations.

Accomplishment of goals and objectives - Internal controls system provide a

mechanism for management to monitor the achievement of operational goals and

objectives.

Audit trail includes:

Paperwork with all the required details must be filled and provided with which is used

as a evidence of any receipt or payment.

Secondary control of the receipt of cash like the cash register or a second person.

9. Case study situation:

The CEO of Habitania Pty Ltd, Tom Salinas explained that he prefers to discuss the budgets with

all senior managers prior to their distribution in order to ensure a corporate view of the strategic

plans. He then meets with each group separately to answer questions and concerns about their

particular area. Eventually the budgets will be printed in hard copy and bound as well distributed as

an electronic spreadsheet.

Student Assessment Guide v 1 January 2019 Page 19 of 55

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BSBFIM601 Manage finances

Upon completion of the budgets you meet with Tom to provide an overview of the information

contained within the budgets, the budget notes and recommendations regarding the internal

controls to prepare him for the meetings with the senior managers. To clarify his understanding of

the information, Tom asks you a series of questions, which you are to answer orally to Tom (played

by your assessor).

Submission Requirements

You must submit:

a completed annual budget in a single spread sheet with a separate sheet for each budget

component (Refer to instructions under Task 1)

budget notes and question answers in a written format. (Refer to instructions under Task 1)

Assessment Criteria

Your assessor will be looking for:

evidence you have reviewed the case study information provided by submitting an

appropriate budget with budget notes

evidence that you understand, and can explain, the required legislative requirements of

financial management (and outline statutory requirements of ATO, GST, company tax,

PAYG) (Refer to online resources)

evidence that you can outline compliance requirements for the Corporations Act 2001

(Refer to online resources)

evidence that you can identify and recommend use of suitable software for financial

management

evidence that you have clearly communicated information regarding the budget and

correctly responded to a series of questions (e.g. describe the principles of accounting and

financial systems)

evidence that you can describe implications of financial probity

evidence that you can outline the critical dates/initiatives that will require or generate

resources

evidence that you have provided for additional items (as necessary and appropriate) in the

budget

evidence that you have recommended new or modified internal controls that could improve

risk management and maintenance of audit trails

Student Assessment Guide v 1 January 2019 Page 20 of 55

Upon completion of the budgets you meet with Tom to provide an overview of the information

contained within the budgets, the budget notes and recommendations regarding the internal

controls to prepare him for the meetings with the senior managers. To clarify his understanding of

the information, Tom asks you a series of questions, which you are to answer orally to Tom (played

by your assessor).

Submission Requirements

You must submit:

a completed annual budget in a single spread sheet with a separate sheet for each budget

component (Refer to instructions under Task 1)

budget notes and question answers in a written format. (Refer to instructions under Task 1)

Assessment Criteria

Your assessor will be looking for:

evidence you have reviewed the case study information provided by submitting an

appropriate budget with budget notes

evidence that you understand, and can explain, the required legislative requirements of

financial management (and outline statutory requirements of ATO, GST, company tax,

PAYG) (Refer to online resources)

evidence that you can outline compliance requirements for the Corporations Act 2001

(Refer to online resources)