Management Accounting: Calculation of Costs and Budgetary Control

Added on 2023-01-12

13 Pages3204 Words100 Views

Management Accounting

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 2............................................................................................................................................1

P3) Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs......................................................................1

TASK 3............................................................................................................................................5

P4) Advantages and disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................5

TASK 4............................................................................................................................................8

P5) Effectiveness of management accounting systems to respond on financial problems....8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 2............................................................................................................................................1

P3) Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs......................................................................1

TASK 3............................................................................................................................................5

P4) Advantages and disadvantages of different types of planning tools used for budgetary

control.....................................................................................................................................5

TASK 4............................................................................................................................................8

P5) Effectiveness of management accounting systems to respond on financial problems....8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting is the analysis of budgets and expenses that administrators

inside the company need to be available. The main aim of this study to collect all the relevant

information in regard of business. This is the method of the identification, classification and

analysis of the records and details (Arroyo, 2012). This report based on the Prime furniture

which is situated in UK and provides their services to design effective furniture. It provides

facility to people to design their furniture according to their interest. In this report consist of

various techniques to calculate numerical problems and analysis the importance of management

accounting in regard of decision making procedure. Additionally, use different budgets as

planning tools to forecast future results that help in gain good return on capital. There are

identifying various problems that can sort out through accounting systems and tools use to

identify these problems.

TASK 2

P3) Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs

Different types of techniques

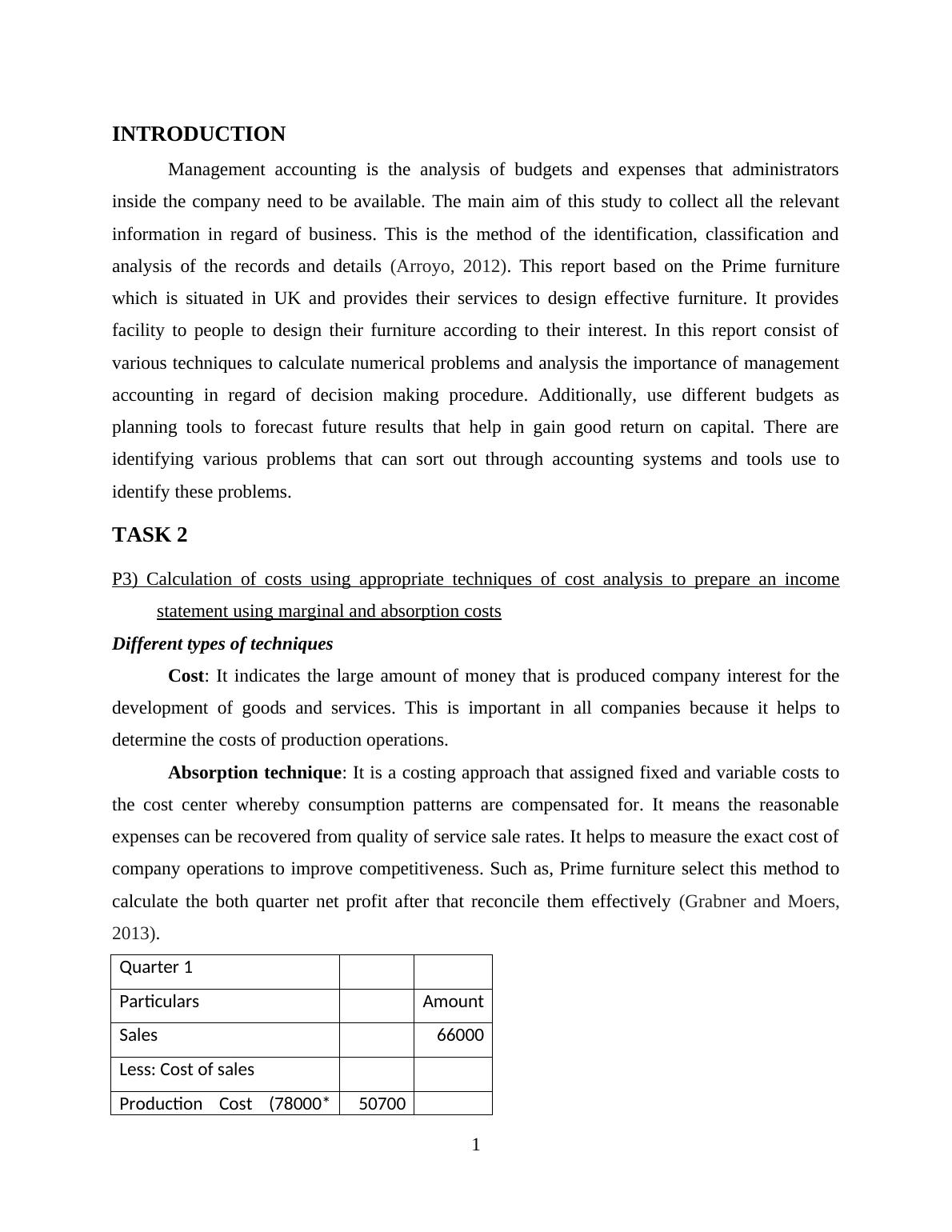

Cost: It indicates the large amount of money that is produced company interest for the

development of goods and services. This is important in all companies because it helps to

determine the costs of production operations.

Absorption technique: It is a costing approach that assigned fixed and variable costs to

the cost center whereby consumption patterns are compensated for. It means the reasonable

expenses can be recovered from quality of service sale rates. It helps to measure the exact cost of

company operations to improve competitiveness. Such as, Prime furniture select this method to

calculate the both quarter net profit after that reconcile them effectively (Grabner and Moers,

2013).

Quarter 1

Particulars Amount

Sales 66000

Less: Cost of sales

Production Cost (78000* 50700

1

Management accounting is the analysis of budgets and expenses that administrators

inside the company need to be available. The main aim of this study to collect all the relevant

information in regard of business. This is the method of the identification, classification and

analysis of the records and details (Arroyo, 2012). This report based on the Prime furniture

which is situated in UK and provides their services to design effective furniture. It provides

facility to people to design their furniture according to their interest. In this report consist of

various techniques to calculate numerical problems and analysis the importance of management

accounting in regard of decision making procedure. Additionally, use different budgets as

planning tools to forecast future results that help in gain good return on capital. There are

identifying various problems that can sort out through accounting systems and tools use to

identify these problems.

TASK 2

P3) Calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs

Different types of techniques

Cost: It indicates the large amount of money that is produced company interest for the

development of goods and services. This is important in all companies because it helps to

determine the costs of production operations.

Absorption technique: It is a costing approach that assigned fixed and variable costs to

the cost center whereby consumption patterns are compensated for. It means the reasonable

expenses can be recovered from quality of service sale rates. It helps to measure the exact cost of

company operations to improve competitiveness. Such as, Prime furniture select this method to

calculate the both quarter net profit after that reconcile them effectively (Grabner and Moers,

2013).

Quarter 1

Particulars Amount

Sales 66000

Less: Cost of sales

Production Cost (78000* 50700

1

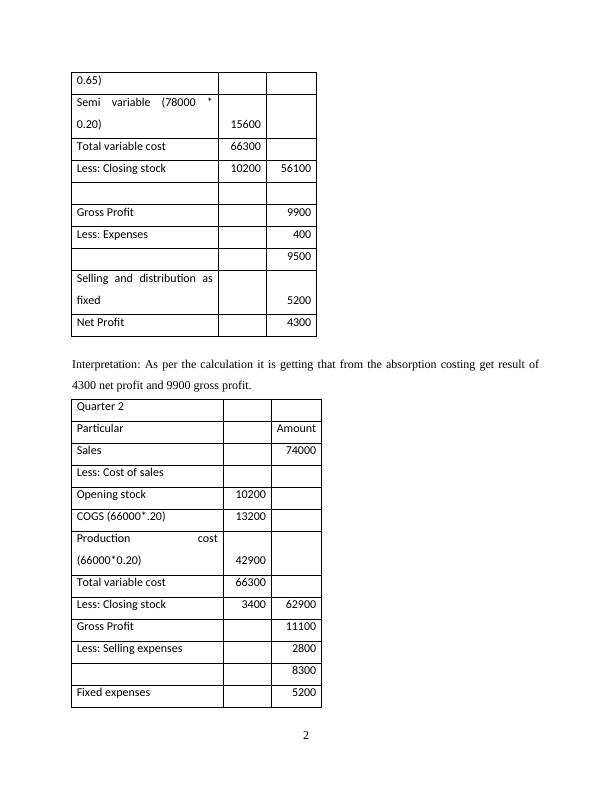

0.65)

Semi variable (78000 *

0.20) 15600

Total variable cost 66300

Less: Closing stock 10200 56100

Gross Profit 9900

Less: Expenses 400

9500

Selling and distribution as

fixed 5200

Net Profit 4300

Interpretation: As per the calculation it is getting that from the absorption costing get result of

4300 net profit and 9900 gross profit.

Quarter 2

Particular Amount

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*.20) 13200

Production cost

(66000*0.20) 42900

Total variable cost 66300

Less: Closing stock 3400 62900

Gross Profit 11100

Less: Selling expenses 2800

8300

Fixed expenses 5200

2

Semi variable (78000 *

0.20) 15600

Total variable cost 66300

Less: Closing stock 10200 56100

Gross Profit 9900

Less: Expenses 400

9500

Selling and distribution as

fixed 5200

Net Profit 4300

Interpretation: As per the calculation it is getting that from the absorption costing get result of

4300 net profit and 9900 gross profit.

Quarter 2

Particular Amount

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*.20) 13200

Production cost

(66000*0.20) 42900

Total variable cost 66300

Less: Closing stock 3400 62900

Gross Profit 11100

Less: Selling expenses 2800

8300

Fixed expenses 5200

2

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Cost Assessment and Review of Financial Statementslg...

|12

|3177

|57

Cost Estimation and Analysis of Financial Statements through Marginal and Absorption Processlg...

|12

|3219

|60

Management Accounting: Cost Analysis, Planning Tools, and Techniqueslg...

|27

|3194

|314

Management Accounting: Tools and Techniques for Planning and Decision Makinglg...

|16

|3775

|50

Management Accountinglg...

|11

|417

|50

Management Accounting: Costing Techniques, Budgetary Control, and Financial Analysislg...

|13

|3204

|33