Management Accounting: Tools and Techniques for Planning and Decision Making

Added on 2022-12-27

16 Pages3775 Words50 Views

Management Accounting

INTRODUCTION

Management accounting is highly significant which lays focus on preparing and

providing specific information to the managers for decision making. In the context of business

organization, management accounting helps in exerting effectual control on undesirable activities

and thereby leads performance improvement. By applying the tools of MA organization can get

appropriate information within suitable time frame and thereby become able to implement

competent framework for business success. The present report is based on the case scenario of

Prime Furniture ltd which offers unique products or services to the customers at suitable prices.

In this, report will provide deeper insight about the tools & techniques that can be used by the

firm for planning purpose. Besides this, it will also shed light on the significance of marginal and

absorption costing method for the assessment of both cost as well as profitability. Further, report

will also depict managerial accounting techniques which help in dealing with monetary problems

effectually.

TASK 2

P3. Assessing cost and profit with the help of absorption and marginal costing method

There are mainly two techniques which business units undertake for doing analysis of

both cost and profitability. Marginal costing technique is undertaken by the company for

determining total cost associated with production aspect. However, in this technique, only

variable expenses are included while assessing production cost. This in turn leads the problem of

under-recovery of overheads and closing stock (Shields, 2015). On the other side, absorption

costing method emphasizes on capturing all the costs associated with production related

activities. In addition to this, in this, overheads are allocated referring the related cost-Centre

(Cooper, Ezzamel and Qu, 2017). This method is effectual as it complies with GAAP and

provides assistance in preparing reports in relation to accounting & stock.

Calculation of cost per unit in different costing method is as follows:

Particulars Absorption costing (in £) Marginal costing (in £)

Variable cost 52000 / 80000 52000 / 80000

Management accounting is highly significant which lays focus on preparing and

providing specific information to the managers for decision making. In the context of business

organization, management accounting helps in exerting effectual control on undesirable activities

and thereby leads performance improvement. By applying the tools of MA organization can get

appropriate information within suitable time frame and thereby become able to implement

competent framework for business success. The present report is based on the case scenario of

Prime Furniture ltd which offers unique products or services to the customers at suitable prices.

In this, report will provide deeper insight about the tools & techniques that can be used by the

firm for planning purpose. Besides this, it will also shed light on the significance of marginal and

absorption costing method for the assessment of both cost as well as profitability. Further, report

will also depict managerial accounting techniques which help in dealing with monetary problems

effectually.

TASK 2

P3. Assessing cost and profit with the help of absorption and marginal costing method

There are mainly two techniques which business units undertake for doing analysis of

both cost and profitability. Marginal costing technique is undertaken by the company for

determining total cost associated with production aspect. However, in this technique, only

variable expenses are included while assessing production cost. This in turn leads the problem of

under-recovery of overheads and closing stock (Shields, 2015). On the other side, absorption

costing method emphasizes on capturing all the costs associated with production related

activities. In addition to this, in this, overheads are allocated referring the related cost-Centre

(Cooper, Ezzamel and Qu, 2017). This method is effectual as it complies with GAAP and

provides assistance in preparing reports in relation to accounting & stock.

Calculation of cost per unit in different costing method is as follows:

Particulars Absorption costing (in £) Marginal costing (in £)

Variable cost 52000 / 80000 52000 / 80000

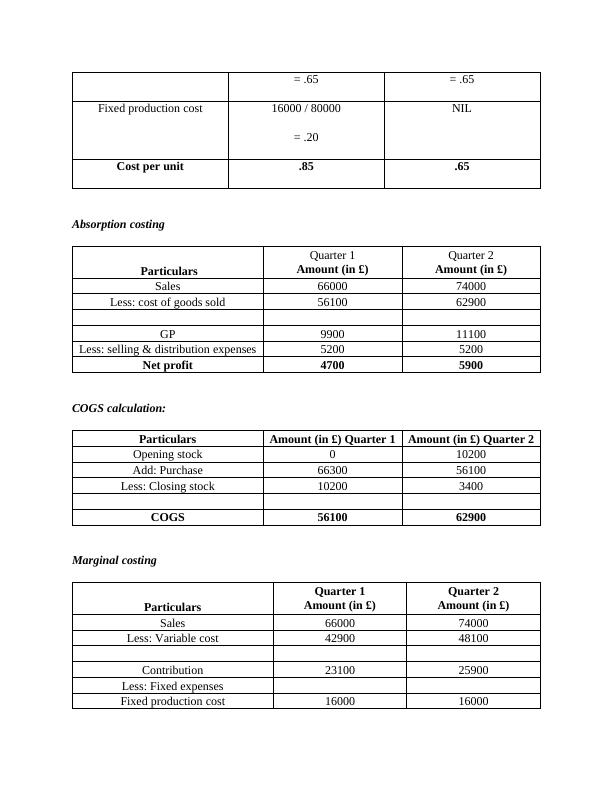

= .65 = .65

Fixed production cost 16000 / 80000

= .20

NIL

Cost per unit .85 .65

Absorption costing

Particulars

Quarter 1

Amount (in £)

Quarter 2

Amount (in £)

Sales 66000 74000

Less: cost of goods sold 56100 62900

GP 9900 11100

Less: selling & distribution expenses 5200 5200

Net profit 4700 5900

COGS calculation:

Particulars Amount (in £) Quarter 1 Amount (in £) Quarter 2

Opening stock 0 10200

Add: Purchase 66300 56100

Less: Closing stock 10200 3400

COGS 56100 62900

Marginal costing

Particulars

Quarter 1

Amount (in £)

Quarter 2

Amount (in £)

Sales 66000 74000

Less: Variable cost 42900 48100

Contribution 23100 25900

Less: Fixed expenses

Fixed production cost 16000 16000

Fixed production cost 16000 / 80000

= .20

NIL

Cost per unit .85 .65

Absorption costing

Particulars

Quarter 1

Amount (in £)

Quarter 2

Amount (in £)

Sales 66000 74000

Less: cost of goods sold 56100 62900

GP 9900 11100

Less: selling & distribution expenses 5200 5200

Net profit 4700 5900

COGS calculation:

Particulars Amount (in £) Quarter 1 Amount (in £) Quarter 2

Opening stock 0 10200

Add: Purchase 66300 56100

Less: Closing stock 10200 3400

COGS 56100 62900

Marginal costing

Particulars

Quarter 1

Amount (in £)

Quarter 2

Amount (in £)

Sales 66000 74000

Less: Variable cost 42900 48100

Contribution 23100 25900

Less: Fixed expenses

Fixed production cost 16000 16000

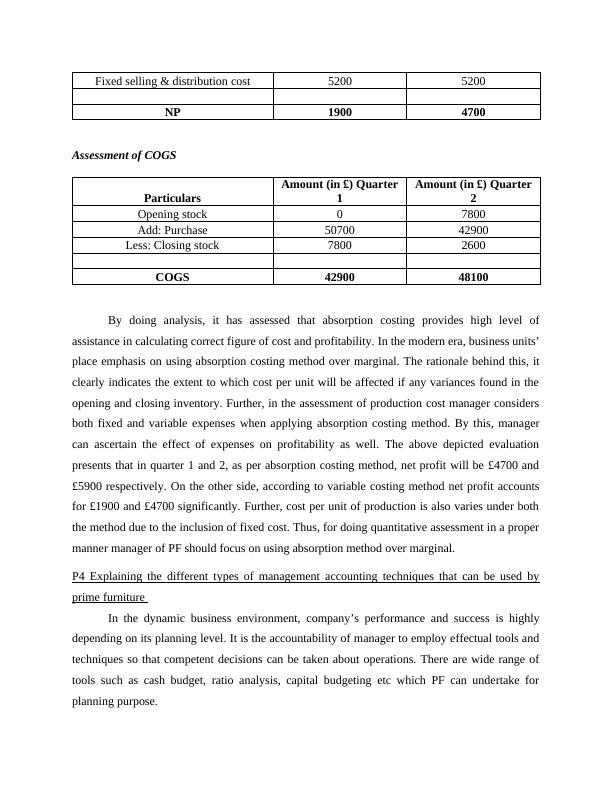

Fixed selling & distribution cost 5200 5200

NP 1900 4700

Assessment of COGS

Particulars

Amount (in £) Quarter

1

Amount (in £) Quarter

2

Opening stock 0 7800

Add: Purchase 50700 42900

Less: Closing stock 7800 2600

COGS 42900 48100

By doing analysis, it has assessed that absorption costing provides high level of

assistance in calculating correct figure of cost and profitability. In the modern era, business units’

place emphasis on using absorption costing method over marginal. The rationale behind this, it

clearly indicates the extent to which cost per unit will be affected if any variances found in the

opening and closing inventory. Further, in the assessment of production cost manager considers

both fixed and variable expenses when applying absorption costing method. By this, manager

can ascertain the effect of expenses on profitability as well. The above depicted evaluation

presents that in quarter 1 and 2, as per absorption costing method, net profit will be £4700 and

£5900 respectively. On the other side, according to variable costing method net profit accounts

for £1900 and £4700 significantly. Further, cost per unit of production is also varies under both

the method due to the inclusion of fixed cost. Thus, for doing quantitative assessment in a proper

manner manager of PF should focus on using absorption method over marginal.

P4 Explaining the different types of management accounting techniques that can be used by

prime furniture

In the dynamic business environment, company’s performance and success is highly

depending on its planning level. It is the accountability of manager to employ effectual tools and

techniques so that competent decisions can be taken about operations. There are wide range of

tools such as cash budget, ratio analysis, capital budgeting etc which PF can undertake for

planning purpose.

NP 1900 4700

Assessment of COGS

Particulars

Amount (in £) Quarter

1

Amount (in £) Quarter

2

Opening stock 0 7800

Add: Purchase 50700 42900

Less: Closing stock 7800 2600

COGS 42900 48100

By doing analysis, it has assessed that absorption costing provides high level of

assistance in calculating correct figure of cost and profitability. In the modern era, business units’

place emphasis on using absorption costing method over marginal. The rationale behind this, it

clearly indicates the extent to which cost per unit will be affected if any variances found in the

opening and closing inventory. Further, in the assessment of production cost manager considers

both fixed and variable expenses when applying absorption costing method. By this, manager

can ascertain the effect of expenses on profitability as well. The above depicted evaluation

presents that in quarter 1 and 2, as per absorption costing method, net profit will be £4700 and

£5900 respectively. On the other side, according to variable costing method net profit accounts

for £1900 and £4700 significantly. Further, cost per unit of production is also varies under both

the method due to the inclusion of fixed cost. Thus, for doing quantitative assessment in a proper

manner manager of PF should focus on using absorption method over marginal.

P4 Explaining the different types of management accounting techniques that can be used by

prime furniture

In the dynamic business environment, company’s performance and success is highly

depending on its planning level. It is the accountability of manager to employ effectual tools and

techniques so that competent decisions can be taken about operations. There are wide range of

tools such as cash budget, ratio analysis, capital budgeting etc which PF can undertake for

planning purpose.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accountinglg...

|11

|417

|50

Management Accounting: Cost Analysis, Planning Tools, and Techniqueslg...

|27

|3194

|314

Management Accounting: Tools and Techniques for Planninglg...

|17

|3871

|97

Management Accounting Techniques and Planning Toolslg...

|16

|3634

|455

Management Accounting: Costing Techniques, Budgetary Control, and Financial Analysislg...

|13

|3204

|33

Management Accounting: Calculation of Costs and Budgetary Controllg...

|13

|3204

|100