Management Accounting Report: Variance Analysis and XLG Case Study

VerifiedAdded on 2023/01/09

|13

|3250

|81

Report

AI Summary

This report delves into the core concepts of management accounting, commencing with an introduction that underscores its significance in modern corporate decision-making. The initial section, Part A, provides a detailed examination of variance analysis, including the calculation of sales price and volume contribution variances for Chemical X and Y, as well as material price planning and operational variances. It critically assesses the merits and demerits of using variances in evaluating managerial performance, offering insights into their advantages and limitations. Part B shifts the focus to a case study involving XLG, a cleaning agent manufacturer, evaluating strategic alternatives, particularly the in-house production of Fama Q, considering factors such as patent protection, supply chain disruptions, and market demand fluctuations. The report concludes with recommendations based on the analysis, highlighting the financial implications of each decision, like changes in profit margins and cost optimization strategies, providing a comprehensive overview of the financial and operational considerations for XLG.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

PART B............................................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

PART B............................................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management Accounting in modern ear is essential aspect of every corporation as this

covers all the managing, finance and accounting operations. This primarily concerned with

organisational decision-making and policies. It involve supply of most useful and effective

information to top managing personnel with aim to enable them in taking effective decisions and

enhance organisation's overall performance (Wen and Siqin, 2020). This support decision-

making tasks which is make it essential for a business organisation operating in competitive

market environment. Management accounting also covers thorough analysis of financial

performance and critical evaluation of all the major alternatives available in business to support

managerial actions. This assessment report is classified into two parts the first one covers

computations of variances and major merits as well as demerits of variances in context of

determining/assessing managers' performance. Report's later part contains critical decision

making and recommendations based on the XLG's case scenario.

PART A

(i) Sales price and volume contribution variance.

Sales Price Variance- It is type of variance whose value is computed by making difference of

prices at different level including market price and budgeted price (Dai, Jin, Kou and Xu, 2020).

The value of this variance is measured by help of a specific formula that is include below in such

manner:

Sales price variance (SPV)= (Actual Price-Standard price) x Actual number of units

Chemical X:

Given information:

Actual price= £45 per unit

Standard price= £35 per unit

Actual number of sales unit= 850 Units

Sales price variance: (45-35) x 850 = 8500 (F)

Chemical Y:

Given information:

Actual price= £37 per unit

Standard price= £30 per unit

Management Accounting in modern ear is essential aspect of every corporation as this

covers all the managing, finance and accounting operations. This primarily concerned with

organisational decision-making and policies. It involve supply of most useful and effective

information to top managing personnel with aim to enable them in taking effective decisions and

enhance organisation's overall performance (Wen and Siqin, 2020). This support decision-

making tasks which is make it essential for a business organisation operating in competitive

market environment. Management accounting also covers thorough analysis of financial

performance and critical evaluation of all the major alternatives available in business to support

managerial actions. This assessment report is classified into two parts the first one covers

computations of variances and major merits as well as demerits of variances in context of

determining/assessing managers' performance. Report's later part contains critical decision

making and recommendations based on the XLG's case scenario.

PART A

(i) Sales price and volume contribution variance.

Sales Price Variance- It is type of variance whose value is computed by making difference of

prices at different level including market price and budgeted price (Dai, Jin, Kou and Xu, 2020).

The value of this variance is measured by help of a specific formula that is include below in such

manner:

Sales price variance (SPV)= (Actual Price-Standard price) x Actual number of units

Chemical X:

Given information:

Actual price= £45 per unit

Standard price= £35 per unit

Actual number of sales unit= 850 Units

Sales price variance: (45-35) x 850 = 8500 (F)

Chemical Y:

Given information:

Actual price= £37 per unit

Standard price= £30 per unit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Actual number of sales unit= 750 units

Sales price variance: (37-30) x 750 = 5250 (F)

Sales volume contribution variance- In this type of variance, changes in profit is measured. This

variation in profit can be because of difference between quantity of actual and estimated sales. In

order to find out accurate value of this variance, there is a formula which is mentioned below in

such manner:

Formula: (Actual units sold × Budgeted price for each unit) – (budgeted unit sold × Budgeted

price for each unit)

Chemical X:

Given information:

Actual units sold= 850 Units

Budgeted price per unit= £35

Budgeted unit sold= 595 Units

Budgeted price per unit= £35

Sales volume contribution variance: (850x35) – (595x35) = 8925 (F)

Chemical Y:

Given information:

Actual units sold= 750 Units

Budgeted price per unit= £30

Budgeted unit sold= 595 Units

Budgeted price per unit= £30

Sales volume contribution variance: (750x30) – (595x30) = 4650 (F)

(ii) The material price planning variance and material price operational variance.

Material price planning variance- It can be understood as a form of variance which is measured

with an aim to get value of budgeted and actual prices of material (Chorley, 2019). In order to

compute this variance, there is a particular formula that is mentioned below in such manner:

Material price planning variance= [(Revised budgeted sales x Standard Margin)- (Actual Sales

Quantity X Standard Margin)]

Chemical X:

Given information-

Revised budgeted sale= 595 units at the rate of 4.5 pounds per unit

Sales price variance: (37-30) x 750 = 5250 (F)

Sales volume contribution variance- In this type of variance, changes in profit is measured. This

variation in profit can be because of difference between quantity of actual and estimated sales. In

order to find out accurate value of this variance, there is a formula which is mentioned below in

such manner:

Formula: (Actual units sold × Budgeted price for each unit) – (budgeted unit sold × Budgeted

price for each unit)

Chemical X:

Given information:

Actual units sold= 850 Units

Budgeted price per unit= £35

Budgeted unit sold= 595 Units

Budgeted price per unit= £35

Sales volume contribution variance: (850x35) – (595x35) = 8925 (F)

Chemical Y:

Given information:

Actual units sold= 750 Units

Budgeted price per unit= £30

Budgeted unit sold= 595 Units

Budgeted price per unit= £30

Sales volume contribution variance: (750x30) – (595x30) = 4650 (F)

(ii) The material price planning variance and material price operational variance.

Material price planning variance- It can be understood as a form of variance which is measured

with an aim to get value of budgeted and actual prices of material (Chorley, 2019). In order to

compute this variance, there is a particular formula that is mentioned below in such manner:

Material price planning variance= [(Revised budgeted sales x Standard Margin)- (Actual Sales

Quantity X Standard Margin)]

Chemical X:

Given information-

Revised budgeted sale= 595 units at the rate of 4.5 pounds per unit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Standard Margin= £25

Actual Sales Quantity= 850 Units

Standard Margin= £25

Material price planning variance: [(595x4.5x25) -(850x25)] = 45687.5

Chemical Y:

Given information-

Revised budgeted sale= 595 units at the rate of £4.5 per unit

Standard Margin= £20

Actual Sales Quantity= 750 Units

Standard Margin= £20

Material price planning variance: [(595x4.5x20) -(750x20)] = 38550

Material price operation variance: It can be defined as a type of variance which is measured in

order to find out difference between actual price of material and budgeted price of material

(Begiazi and Katsiampa, 2019). In accordance of given data set, this type of variance is

computed by applying below mentioned formula:

Material price operation variance: [(Original budgeted sales x Standard Margin) – (Revised

budgeted sales x Standard Margin)]

Chemical X:

Given information:

Original budgeted sales= 595 Units at the rate of £2.5 per unit

Standard Margin= £25

Revised budgeted sales= 595 Units at the rate of £ 4.5 per unit

Standard Margin= £25

Material price planning variance= [(595x2.5x25) -(595x4.5x25)] = -29750

Chemical Y:

Given information:

Original budgeted sale= 595 Units at the rate of £ 2.5 per unit

Standard Margin= £20

Revised budgeted sale= 595 Units at the rate of £ 4.5 per unit

Standard Margin= £20

Material price planning variance= [(595x2.5x20) -(595x4.5x20)] = -23800

Actual Sales Quantity= 850 Units

Standard Margin= £25

Material price planning variance: [(595x4.5x25) -(850x25)] = 45687.5

Chemical Y:

Given information-

Revised budgeted sale= 595 units at the rate of £4.5 per unit

Standard Margin= £20

Actual Sales Quantity= 750 Units

Standard Margin= £20

Material price planning variance: [(595x4.5x20) -(750x20)] = 38550

Material price operation variance: It can be defined as a type of variance which is measured in

order to find out difference between actual price of material and budgeted price of material

(Begiazi and Katsiampa, 2019). In accordance of given data set, this type of variance is

computed by applying below mentioned formula:

Material price operation variance: [(Original budgeted sales x Standard Margin) – (Revised

budgeted sales x Standard Margin)]

Chemical X:

Given information:

Original budgeted sales= 595 Units at the rate of £2.5 per unit

Standard Margin= £25

Revised budgeted sales= 595 Units at the rate of £ 4.5 per unit

Standard Margin= £25

Material price planning variance= [(595x2.5x25) -(595x4.5x25)] = -29750

Chemical Y:

Given information:

Original budgeted sale= 595 Units at the rate of £ 2.5 per unit

Standard Margin= £20

Revised budgeted sale= 595 Units at the rate of £ 4.5 per unit

Standard Margin= £20

Material price planning variance= [(595x2.5x20) -(595x4.5x20)] = -23800

(iii) Given the change in operations, critically analyze the merits and demerits of using variances

in assessing managers’ performance.

The term variance analysis can be defined as a kinds of tool which is associated with finding

difference between actual and estimated financial activities. This technique plays a key role in

order to improve companies’ financial performance as well as enables better allocation of

financial resources into various tasks and activities. There are a range of variances which are

used for a particular aspect. It depends on companies that which type of variance they are using

in order to find out actual performance.

In current time period, competition is increasing rapidly and due to which it is essential for

companies to compute variance so that corrective actions can be carried out in order to manage

financial performance. Herein, it is important to note that this technique of performance analysis

is suitable only for financial aspects. It cannot be applied in non-financial aspect (Zhang, 2020).

Companies who do not use this tool for performance evaluation, they face various kinds of

issues. Therefore, it is important for companies to implement this approach. Some common

example of variance are material variances, labor variances etc. By help of these different kinds

of variances, manager of companies become able to know which activities’ performance is under

or over the expectation level. Each method has some positive and negative points. In regards

with variance analysis, some benefits and limitations of using this technique are mentioned

below in such manner:

Advantages:

The main benefit of this technique is that it acts as controlling method. It becomes

possible because by help of finding difference between actual and estimated financial

data, the manager of companies become able to know that which activities are not

performing well. For instance, if estimated sales of particular commodity is 500 units

while actual sales are of 250 units then variation will be of 250 units (500 units-250

units). By help of this variation, managers of companies can make effective plans and

policies so that sales can boosted.

The variance analysis is helpful for finding actual cause of lower performance and

responsible department for this (Salles, Rocha and Gonçalves, 2020). In other words, by

help of this tool it becomes easier for managers to know that which are of operations need

to be consider effectively. For example, if labor variance is producing unfavorable

in assessing managers’ performance.

The term variance analysis can be defined as a kinds of tool which is associated with finding

difference between actual and estimated financial activities. This technique plays a key role in

order to improve companies’ financial performance as well as enables better allocation of

financial resources into various tasks and activities. There are a range of variances which are

used for a particular aspect. It depends on companies that which type of variance they are using

in order to find out actual performance.

In current time period, competition is increasing rapidly and due to which it is essential for

companies to compute variance so that corrective actions can be carried out in order to manage

financial performance. Herein, it is important to note that this technique of performance analysis

is suitable only for financial aspects. It cannot be applied in non-financial aspect (Zhang, 2020).

Companies who do not use this tool for performance evaluation, they face various kinds of

issues. Therefore, it is important for companies to implement this approach. Some common

example of variance are material variances, labor variances etc. By help of these different kinds

of variances, manager of companies become able to know which activities’ performance is under

or over the expectation level. Each method has some positive and negative points. In regards

with variance analysis, some benefits and limitations of using this technique are mentioned

below in such manner:

Advantages:

The main benefit of this technique is that it acts as controlling method. It becomes

possible because by help of finding difference between actual and estimated financial

data, the manager of companies become able to know that which activities are not

performing well. For instance, if estimated sales of particular commodity is 500 units

while actual sales are of 250 units then variation will be of 250 units (500 units-250

units). By help of this variation, managers of companies can make effective plans and

policies so that sales can boosted.

The variance analysis is helpful for finding actual cause of lower performance and

responsible department for this (Salles, Rocha and Gonçalves, 2020). In other words, by

help of this tool it becomes easier for managers to know that which are of operations need

to be consider effectively. For example, if labor variance is producing unfavorable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

outcome then the managers of company can know that they are not able to hire cost

effectively labors. On the basis of this, managers can take corrective steps and

responsible department can be assigned role to improve their performance in accordance

of need of business entity.

Another plus point of this method is that by help of it, companies can gain competitive

advantage over rivalry firms. It is so because this contributes to business entities in order

to become more proactive towards process of achieving overall goals and objectives. As

well as it also enables to managers to know about current risks and strategies to mitigate

from those risks. Companies who apply this approach become more competitive and

effective in order to beat their competitors.

Disadvantages:

One of the main issue of variance analysis is time delay. This so because managers need

report of variance analysis at the end of each month. For this purpose, accounting staff

has to prepare this report for each and every activity (Zhou and Liang, 2019). As a

consequence, it consumes too much time in entire process of variance analysis. Due to

which managers also make delay in taking effective decision for next month because they

need report of variance analysis which is provided late by accounting staff. Apart from

this, variance analysis is an expensive method which is not affordable for all types of

companies. Specially, small companies cannot implement this approach in their

performance evaluation method of financial perspectives.

Majority of cause for variance are not accessible in accounting records. Due to which

accounting staff has to go through from different information sources such as labor

ratings, bills of material and many more. All these activities make variance analysis less

effective in the context of complex situations.

In addition to these drawbacks, this method is not suitable for non-financial factors. It

considers only financial factors in order to do analysis. As well as the variance analysis

does not provide detailed analysis of any specific aspect. It gives only financial data

related to positive and negative variance. For detailed analysis, managers have to find out

various kinds of information.

effectively labors. On the basis of this, managers can take corrective steps and

responsible department can be assigned role to improve their performance in accordance

of need of business entity.

Another plus point of this method is that by help of it, companies can gain competitive

advantage over rivalry firms. It is so because this contributes to business entities in order

to become more proactive towards process of achieving overall goals and objectives. As

well as it also enables to managers to know about current risks and strategies to mitigate

from those risks. Companies who apply this approach become more competitive and

effective in order to beat their competitors.

Disadvantages:

One of the main issue of variance analysis is time delay. This so because managers need

report of variance analysis at the end of each month. For this purpose, accounting staff

has to prepare this report for each and every activity (Zhou and Liang, 2019). As a

consequence, it consumes too much time in entire process of variance analysis. Due to

which managers also make delay in taking effective decision for next month because they

need report of variance analysis which is provided late by accounting staff. Apart from

this, variance analysis is an expensive method which is not affordable for all types of

companies. Specially, small companies cannot implement this approach in their

performance evaluation method of financial perspectives.

Majority of cause for variance are not accessible in accounting records. Due to which

accounting staff has to go through from different information sources such as labor

ratings, bills of material and many more. All these activities make variance analysis less

effective in the context of complex situations.

In addition to these drawbacks, this method is not suitable for non-financial factors. It

considers only financial factors in order to do analysis. As well as the variance analysis

does not provide detailed analysis of any specific aspect. It gives only financial data

related to positive and negative variance. For detailed analysis, managers have to find out

various kinds of information.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART B

This section of study covers the critical evaluation of alternatives available for XLG

based on case study. Company XLG is maker of cleaning agents branded as Chemical X and Y

and operating business in an environment full of competition. Company's success factor is patent

secured by it against patent. No competitors of company can copy Fama Q. This product also

provide competitive advantages to XLG. As given in XLG's case study company imports Fama

Q form Brazil but due to lock down, coronavirus out break and imposed restrictions on travel

operations this has become expensive to transport goods by air means. Company is now want to

make fama Q in UK instead of importing fama Q. It is also described in XLG's case study that

according to industry and market research it is probable that demand for chemical y and X may

increased by around 45-percent. Thus on the basis of above information this is significant to

analyse available options for corporation and their effects on business in coming period.

Effective evaluation options available in current scenario is most crucial as to increase the

effectiveness and creditability of business decisions (Vaske, 2019). Evaluation of alternatives

also offer a list of all the risk risks and key benefits linked with a particular alternative and assist

in selecting most feasible alternative depending on the present scenario. An incorrect decision

can put question on the survival and performance of business organisation. Following is

comprehensive and thorough evaluation of major options:

In-House production of Fama Q:

Under this alternative there is one major risk exists, fama Q is patent product thus there

may be legal complexities for XLG and also chances that other competitors may copy fama Q.

But also there is a benefit that by in housing the making of fama Q company can minimise the

delivery time 15 days. Also, in lock-down period and travelling restrictions company can

optimise cost to 3 per unit as increased import-price is 3.7 (actually paid) per unit. Further

noticeable thing is that original standardised price of fama-Q is just 2.5 per unit. The below table

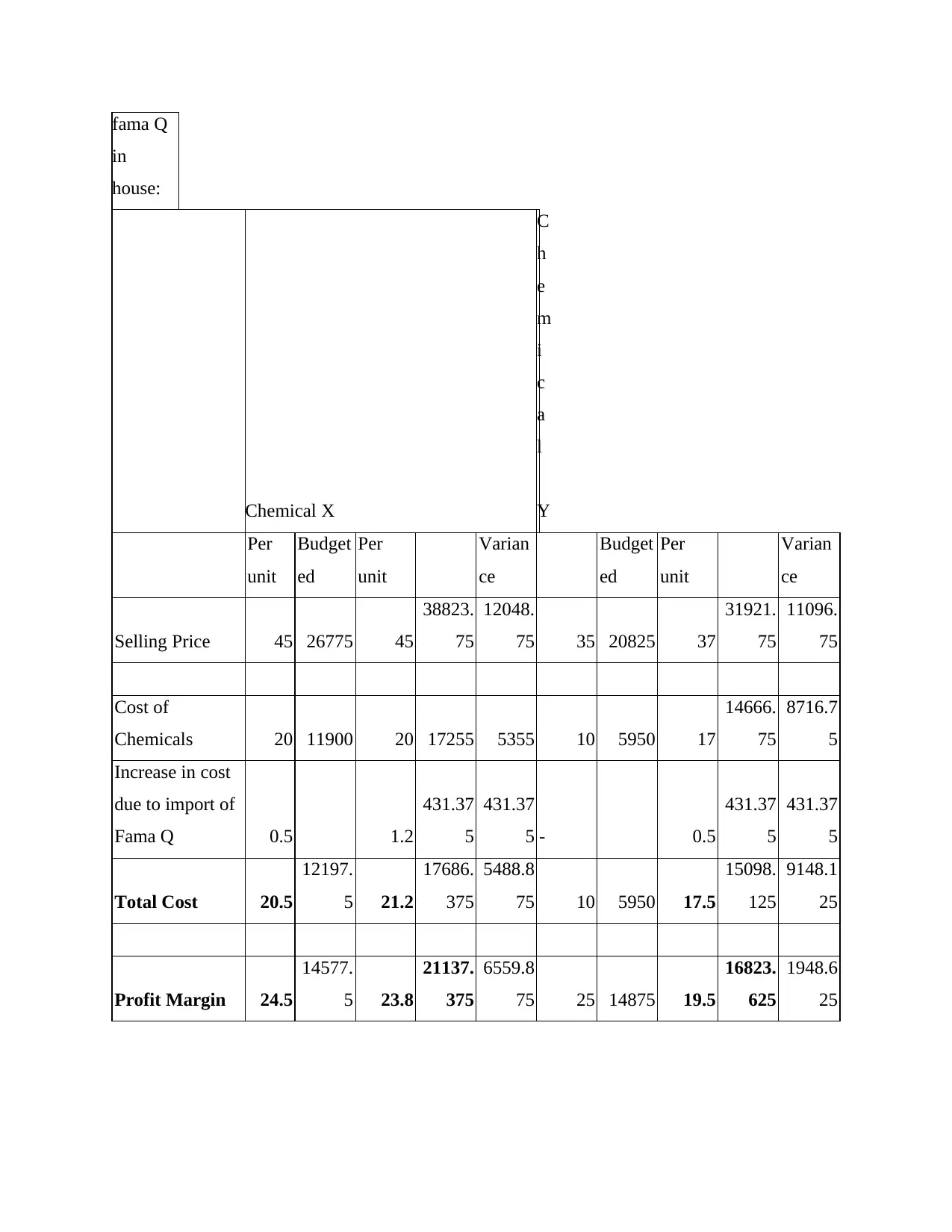

shows the effects on profit margin of XLG if company chooses to make fama Q:

In the

scenario

if XLG

start

making

This section of study covers the critical evaluation of alternatives available for XLG

based on case study. Company XLG is maker of cleaning agents branded as Chemical X and Y

and operating business in an environment full of competition. Company's success factor is patent

secured by it against patent. No competitors of company can copy Fama Q. This product also

provide competitive advantages to XLG. As given in XLG's case study company imports Fama

Q form Brazil but due to lock down, coronavirus out break and imposed restrictions on travel

operations this has become expensive to transport goods by air means. Company is now want to

make fama Q in UK instead of importing fama Q. It is also described in XLG's case study that

according to industry and market research it is probable that demand for chemical y and X may

increased by around 45-percent. Thus on the basis of above information this is significant to

analyse available options for corporation and their effects on business in coming period.

Effective evaluation options available in current scenario is most crucial as to increase the

effectiveness and creditability of business decisions (Vaske, 2019). Evaluation of alternatives

also offer a list of all the risk risks and key benefits linked with a particular alternative and assist

in selecting most feasible alternative depending on the present scenario. An incorrect decision

can put question on the survival and performance of business organisation. Following is

comprehensive and thorough evaluation of major options:

In-House production of Fama Q:

Under this alternative there is one major risk exists, fama Q is patent product thus there

may be legal complexities for XLG and also chances that other competitors may copy fama Q.

But also there is a benefit that by in housing the making of fama Q company can minimise the

delivery time 15 days. Also, in lock-down period and travelling restrictions company can

optimise cost to 3 per unit as increased import-price is 3.7 (actually paid) per unit. Further

noticeable thing is that original standardised price of fama-Q is just 2.5 per unit. The below table

shows the effects on profit margin of XLG if company chooses to make fama Q:

In the

scenario

if XLG

start

making

fama Q

in

house:

Chemical X

C

h

e

m

i

c

a

l

Y

Per

unit

Budget

ed

Per

unit

Varian

ce

Budget

ed

Per

unit

Varian

ce

Selling Price 45 26775 45

38823.

75

12048.

75 35 20825 37

31921.

75

11096.

75

Cost of

Chemicals 20 11900 20 17255 5355 10 5950 17

14666.

75

8716.7

5

Increase in cost

due to import of

Fama Q 0.5 1.2

431.37

5

431.37

5 - 0.5

431.37

5

431.37

5

Total Cost 20.5

12197.

5 21.2

17686.

375

5488.8

75 10 5950 17.5

15098.

125

9148.1

25

Profit Margin 24.5

14577.

5 23.8

21137.

375

6559.8

75 25 14875 19.5

16823.

625

1948.6

25

in

house:

Chemical X

C

h

e

m

i

c

a

l

Y

Per

unit

Budget

ed

Per

unit

Varian

ce

Budget

ed

Per

unit

Varian

ce

Selling Price 45 26775 45

38823.

75

12048.

75 35 20825 37

31921.

75

11096.

75

Cost of

Chemicals 20 11900 20 17255 5355 10 5950 17

14666.

75

8716.7

5

Increase in cost

due to import of

Fama Q 0.5 1.2

431.37

5

431.37

5 - 0.5

431.37

5

431.37

5

Total Cost 20.5

12197.

5 21.2

17686.

375

5488.8

75 10 5950 17.5

15098.

125

9148.1

25

Profit Margin 24.5

14577.

5 23.8

21137.

375

6559.8

75 25 14875 19.5

16823.

625

1948.6

25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

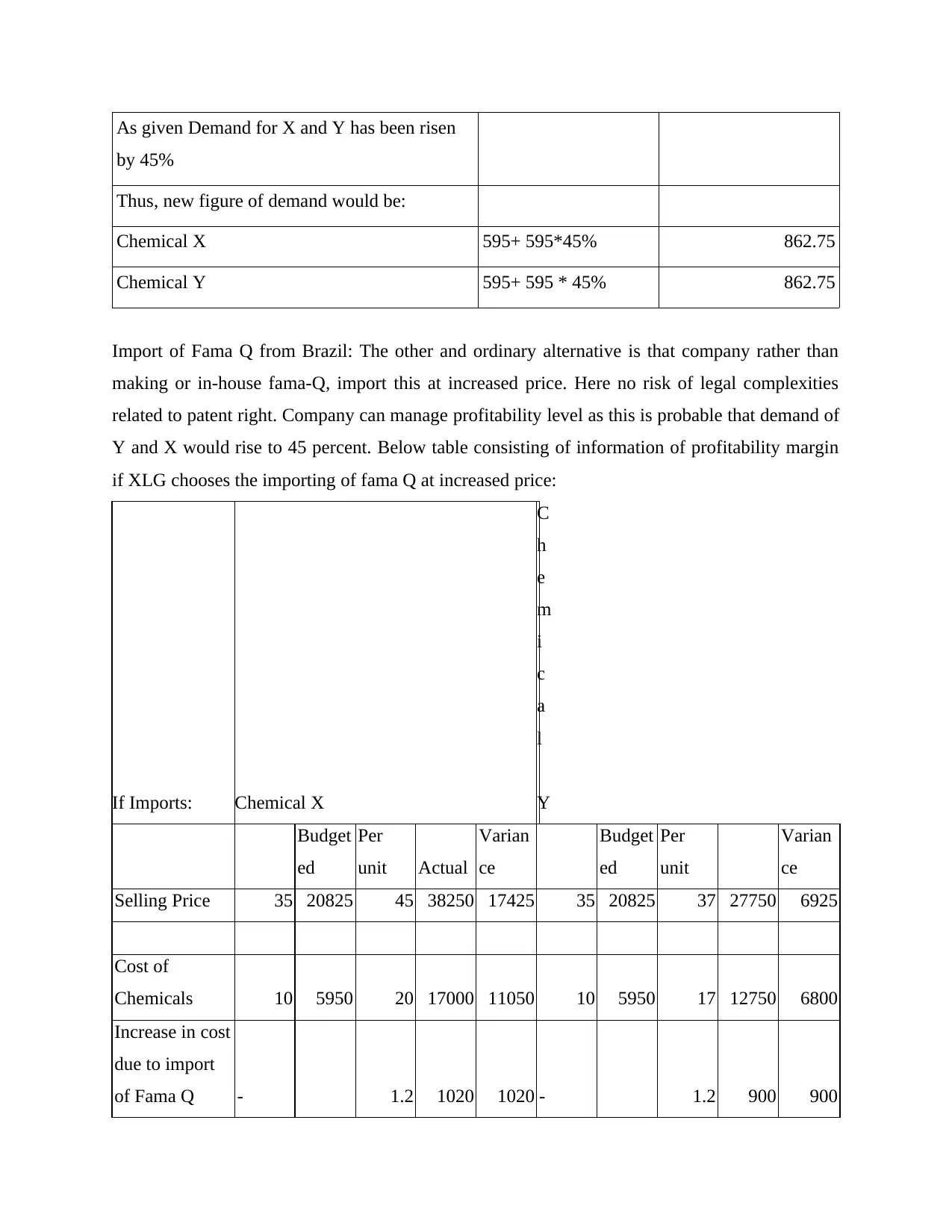

As given Demand for X and Y has been risen

by 45%

Thus, new figure of demand would be:

Chemical X 595+ 595*45% 862.75

Chemical Y 595+ 595 * 45% 862.75

Import of Fama Q from Brazil: The other and ordinary alternative is that company rather than

making or in-house fama-Q, import this at increased price. Here no risk of legal complexities

related to patent right. Company can manage profitability level as this is probable that demand of

Y and X would rise to 45 percent. Below table consisting of information of profitability margin

if XLG chooses the importing of fama Q at increased price:

If Imports: Chemical X

C

h

e

m

i

c

a

l

Y

Budget

ed

Per

unit Actual

Varian

ce

Budget

ed

Per

unit

Varian

ce

Selling Price 35 20825 45 38250 17425 35 20825 37 27750 6925

Cost of

Chemicals 10 5950 20 17000 11050 10 5950 17 12750 6800

Increase in cost

due to import

of Fama Q - 1.2 1020 1020 - 1.2 900 900

by 45%

Thus, new figure of demand would be:

Chemical X 595+ 595*45% 862.75

Chemical Y 595+ 595 * 45% 862.75

Import of Fama Q from Brazil: The other and ordinary alternative is that company rather than

making or in-house fama-Q, import this at increased price. Here no risk of legal complexities

related to patent right. Company can manage profitability level as this is probable that demand of

Y and X would rise to 45 percent. Below table consisting of information of profitability margin

if XLG chooses the importing of fama Q at increased price:

If Imports: Chemical X

C

h

e

m

i

c

a

l

Y

Budget

ed

Per

unit Actual

Varian

ce

Budget

ed

Per

unit

Varian

ce

Selling Price 35 20825 45 38250 17425 35 20825 37 27750 6925

Cost of

Chemicals 10 5950 20 17000 11050 10 5950 17 12750 6800

Increase in cost

due to import

of Fama Q - 1.2 1020 1020 - 1.2 900 900

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

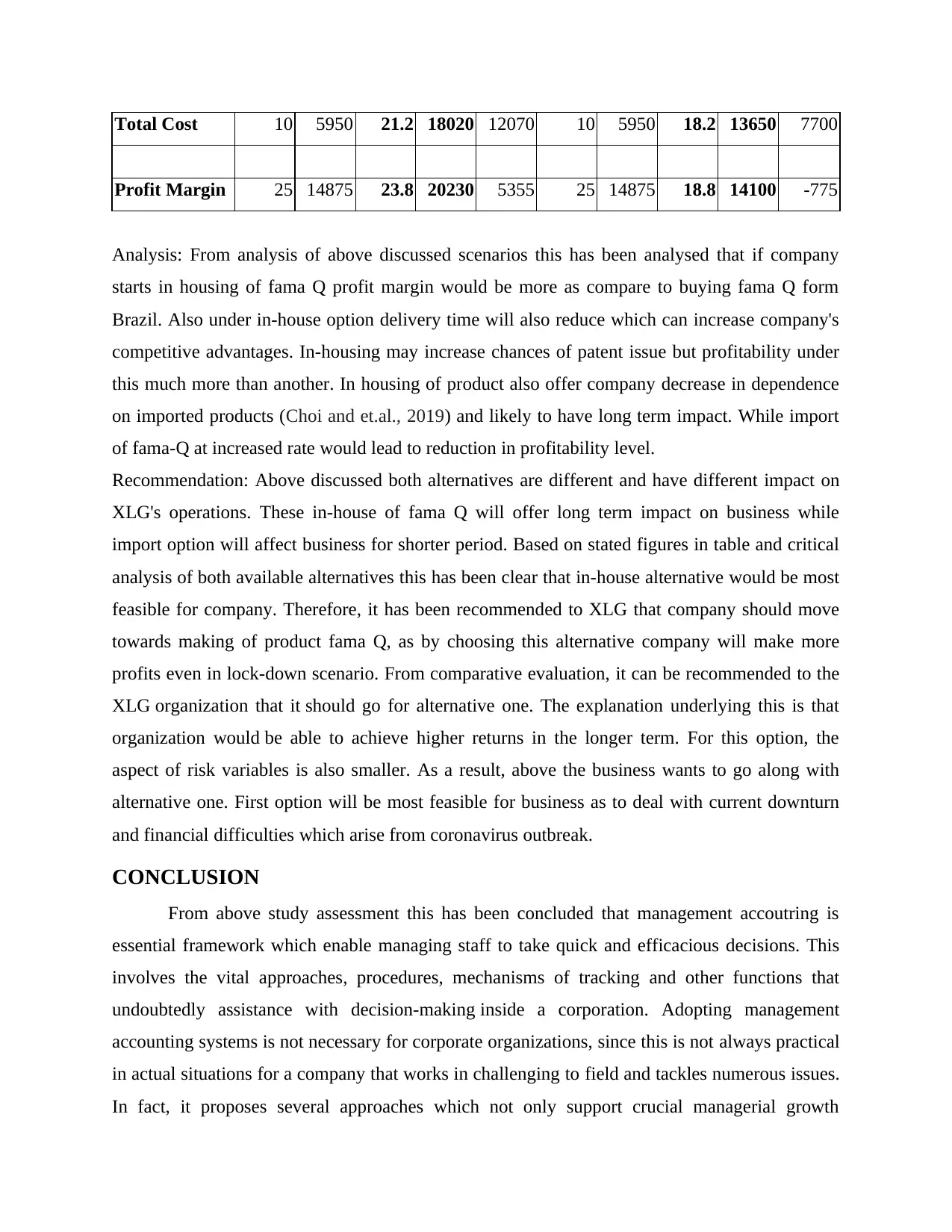

Total Cost 10 5950 21.2 18020 12070 10 5950 18.2 13650 7700

Profit Margin 25 14875 23.8 20230 5355 25 14875 18.8 14100 -775

Analysis: From analysis of above discussed scenarios this has been analysed that if company

starts in housing of fama Q profit margin would be more as compare to buying fama Q form

Brazil. Also under in-house option delivery time will also reduce which can increase company's

competitive advantages. In-housing may increase chances of patent issue but profitability under

this much more than another. In housing of product also offer company decrease in dependence

on imported products (Choi and et.al., 2019) and likely to have long term impact. While import

of fama-Q at increased rate would lead to reduction in profitability level.

Recommendation: Above discussed both alternatives are different and have different impact on

XLG's operations. These in-house of fama Q will offer long term impact on business while

import option will affect business for shorter period. Based on stated figures in table and critical

analysis of both available alternatives this has been clear that in-house alternative would be most

feasible for company. Therefore, it has been recommended to XLG that company should move

towards making of product fama Q, as by choosing this alternative company will make more

profits even in lock-down scenario. From comparative evaluation, it can be recommended to the

XLG organization that it should go for alternative one. The explanation underlying this is that

organization would be able to achieve higher returns in the longer term. For this option, the

aspect of risk variables is also smaller. As a result, above the business wants to go along with

alternative one. First option will be most feasible for business as to deal with current downturn

and financial difficulties which arise from coronavirus outbreak.

CONCLUSION

From above study assessment this has been concluded that management accoutring is

essential framework which enable managing staff to take quick and efficacious decisions. This

involves the vital approaches, procedures, mechanisms of tracking and other functions that

undoubtedly assistance with decision-making inside a corporation. Adopting management

accounting systems is not necessary for corporate organizations, since this is not always practical

in actual situations for a company that works in challenging to field and tackles numerous issues.

In fact, it proposes several approaches which not only support crucial managerial growth

Profit Margin 25 14875 23.8 20230 5355 25 14875 18.8 14100 -775

Analysis: From analysis of above discussed scenarios this has been analysed that if company

starts in housing of fama Q profit margin would be more as compare to buying fama Q form

Brazil. Also under in-house option delivery time will also reduce which can increase company's

competitive advantages. In-housing may increase chances of patent issue but profitability under

this much more than another. In housing of product also offer company decrease in dependence

on imported products (Choi and et.al., 2019) and likely to have long term impact. While import

of fama-Q at increased rate would lead to reduction in profitability level.

Recommendation: Above discussed both alternatives are different and have different impact on

XLG's operations. These in-house of fama Q will offer long term impact on business while

import option will affect business for shorter period. Based on stated figures in table and critical

analysis of both available alternatives this has been clear that in-house alternative would be most

feasible for company. Therefore, it has been recommended to XLG that company should move

towards making of product fama Q, as by choosing this alternative company will make more

profits even in lock-down scenario. From comparative evaluation, it can be recommended to the

XLG organization that it should go for alternative one. The explanation underlying this is that

organization would be able to achieve higher returns in the longer term. For this option, the

aspect of risk variables is also smaller. As a result, above the business wants to go along with

alternative one. First option will be most feasible for business as to deal with current downturn

and financial difficulties which arise from coronavirus outbreak.

CONCLUSION

From above study assessment this has been concluded that management accoutring is

essential framework which enable managing staff to take quick and efficacious decisions. This

involves the vital approaches, procedures, mechanisms of tracking and other functions that

undoubtedly assistance with decision-making inside a corporation. Adopting management

accounting systems is not necessary for corporate organizations, since this is not always practical

in actual situations for a company that works in challenging to field and tackles numerous issues.

In fact, it proposes several approaches which not only support crucial managerial growth

decisions but also include an implantable policy-making mechanism. Management has to focus

towards thorough analysis of key options available and take effective decision as to sustain

business performance in longer term.

towards thorough analysis of key options available and take effective decision as to sustain

business performance in longer term.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.